Cognitive Operations Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

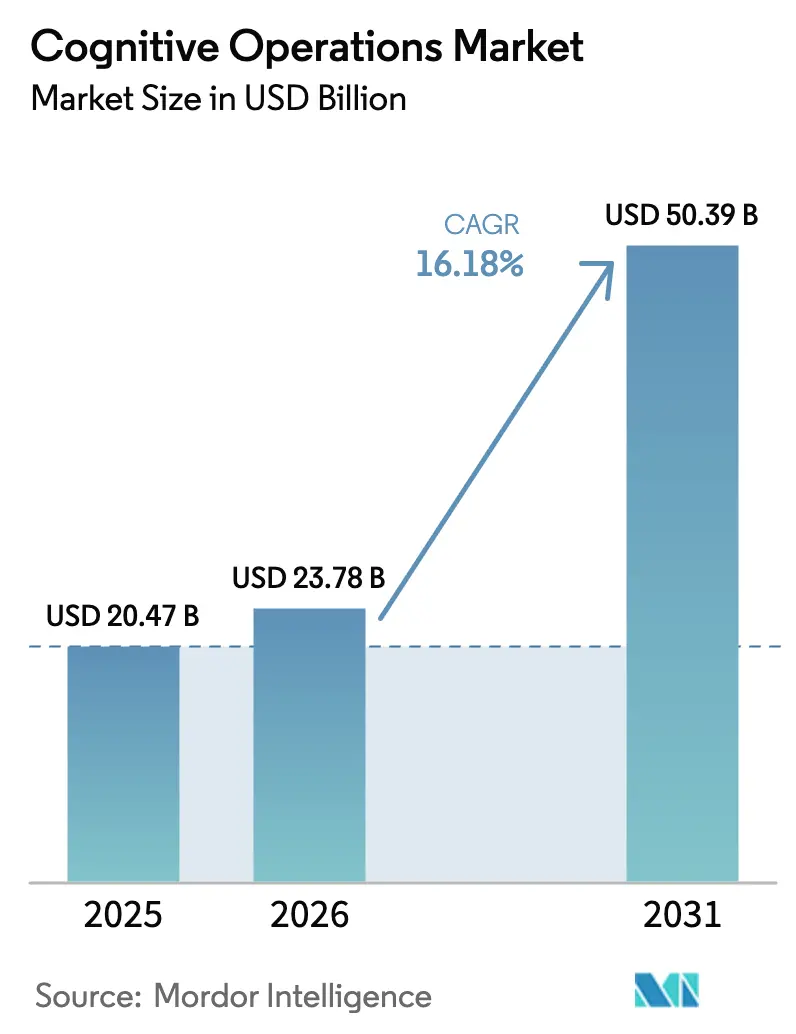

| Market Size (2026) | USD 23.78 Billion |

| Market Size (2031) | USD 50.39 Billion |

| Growth Rate (2026 - 2031) | 16.18% CAGR |

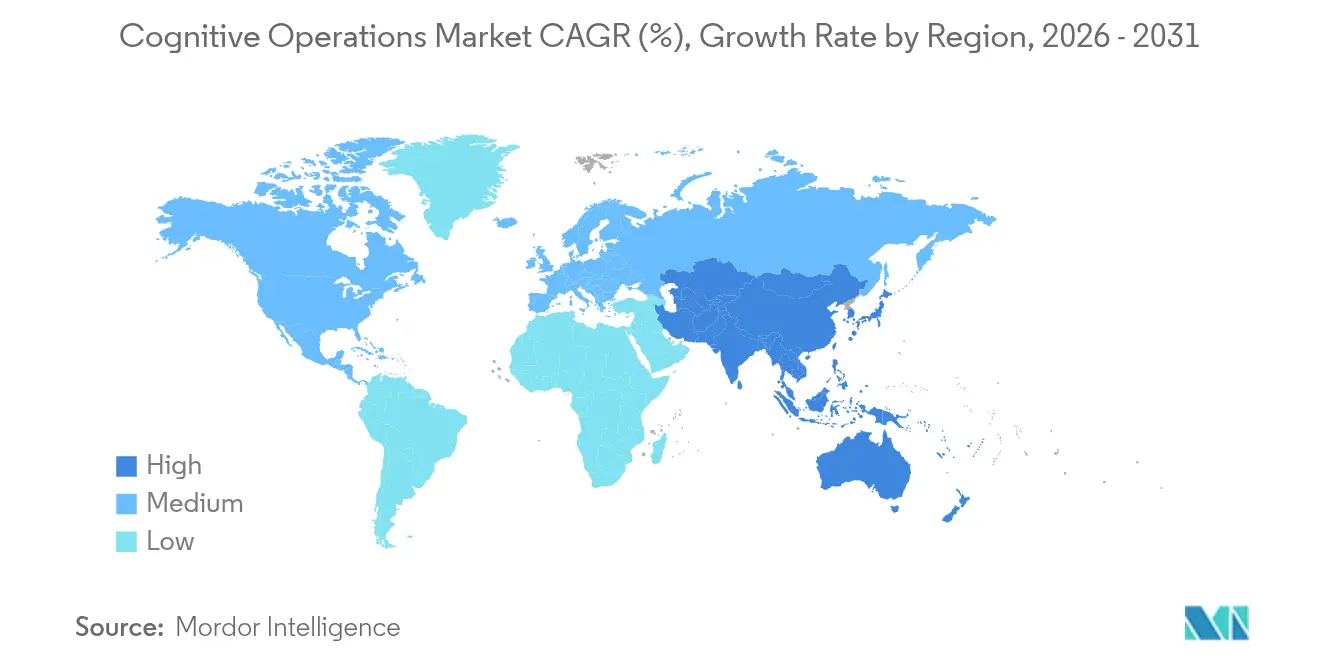

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

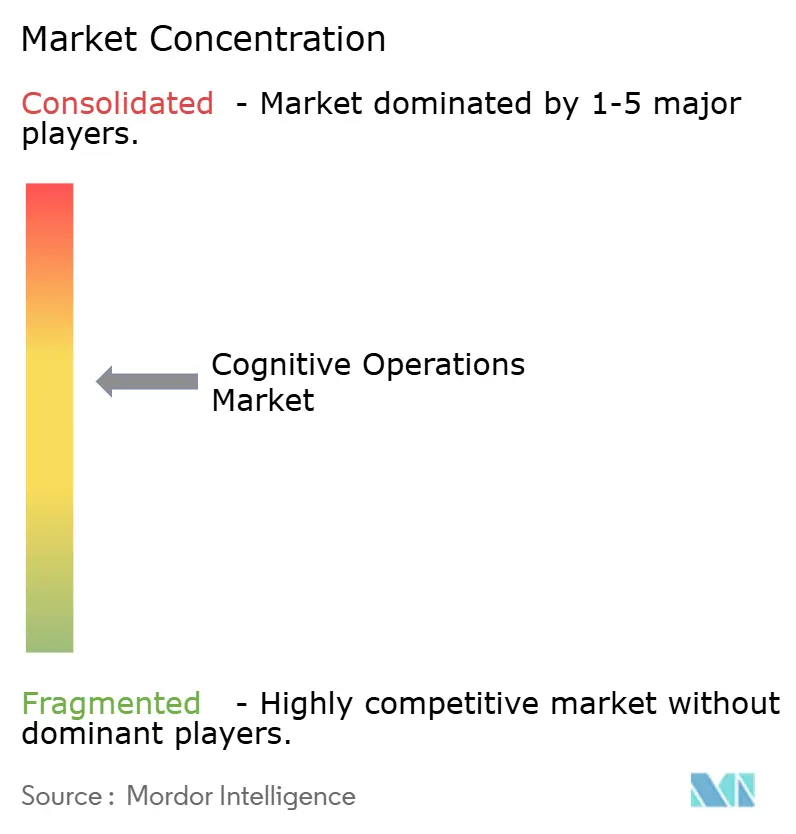

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cognitive Operations Market Analysis by Mordor Intelligence

The Cognitive Operations Market size was valued at USD 20.47 billion in 2025 and estimated to grow from USD 23.78 billion in 2026 to reach USD 50.39 billion by 2031, at a CAGR of 16.18% during the forecast period (2026-2031).

Rapid enterprise digitization, surging telemetry volumes, and a strategic pivot toward autonomous IT operations underpin this expansion. Enterprises deploy AI-driven operational intelligence to predict and avert service disruptions, trimming unplanned downtime and safeguarding customer experience. Cloud-native platforms dominate because they scale elastically, process petabyte-scale data streams in near real-time, and lower total cost of ownership by up to 40% versus legacy on-premises tools. M&A activity, most notably Cisco’s USD 28 billion purchase of Splunk, is accelerating platform consolidation and broadening feature breadth. Simultaneously, a skills gap and legacy-system integration hurdles temper the pace of rollouts, especially in regulated industries.

Key Report Takeaways

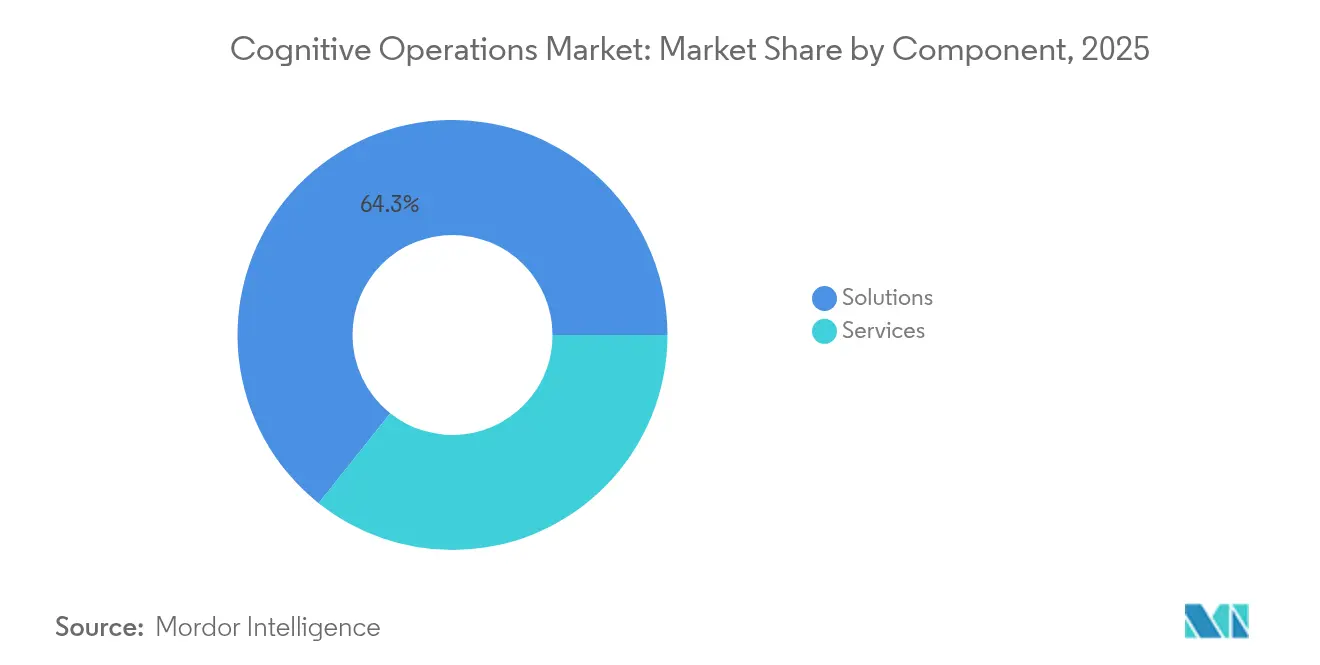

- By component, Solutions captured 64.30% of the cognitive operations market share in 2025, while Services are forecast to expand at a 17.05% CAGR through 2031.

- By deployment mode, cloud deployment held 71.20% share of the cognitive operations market size in 2025 and is set to grow at a 17.55% CAGR to 2031.

- By enterprise size, large enterprises commanded a 58.30% share in 2025; SMEs recorded the fastest growth at 16.68% CAGR.

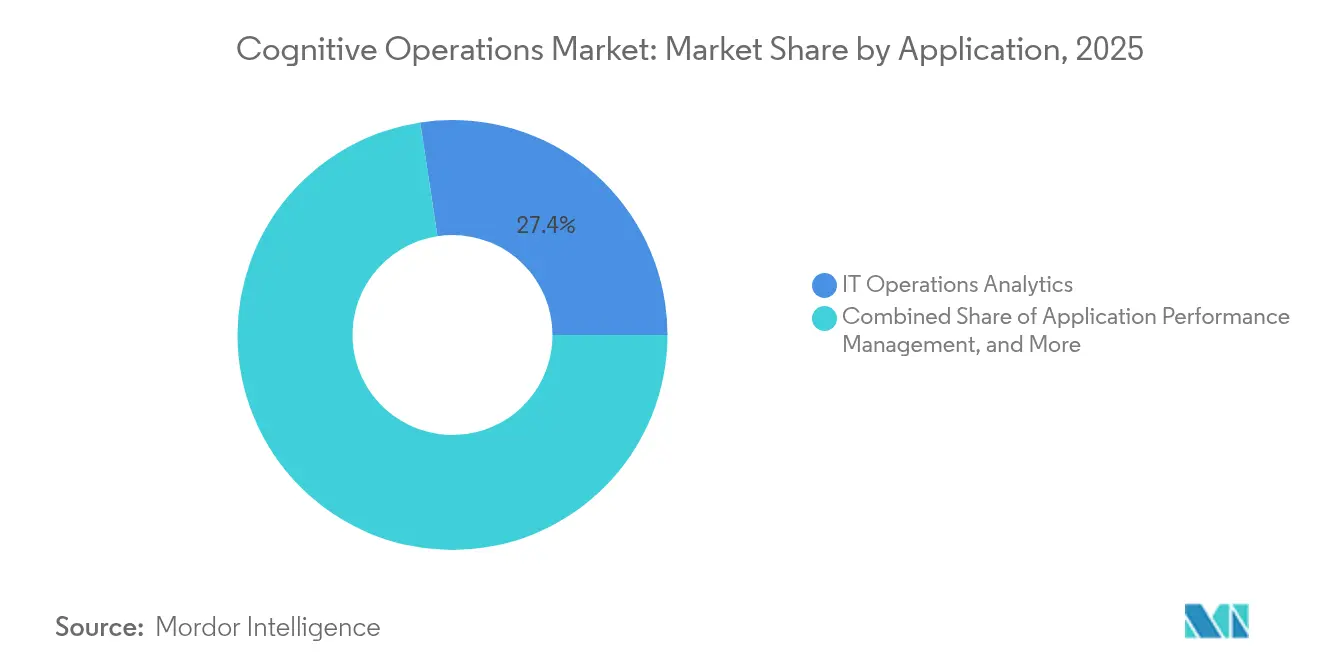

- By application, IT Operations Analytics led with a 27.40% share in 2025, whereas Security Analytics is advancing at an 17.56% CAGR through 2031.

- By industry vertical, BFSI held 23.60% share in 2025; Healthcare and Life Sciences is projected to register the highest 16.94% CAGR.

- By geography, North America accounted for 37.40% of the cognitive operations market share in 2025, while Asia Pacific is poised for an 17.61% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cognitive Operations Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-based cognitive IT operations | +3.20% | Global; North America & Europe lead | Medium term (2-4 years) |

| Monitoring complex IT environments | +2.80% | Global; APAC and North America | Short term (≤ 2 years) |

| IT-Ops data surge from digital transformation | +2.10% | Global; strongest in emerging markets | Long term (≥ 4 years) |

| AI-driven proactive incident management | +1.90% | North America & Europe, rising in APAC | Medium term (2-4 years) |

| Edge-native AIOps for 5G slices | +1.40% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| GreenOps for energy-optimised AI-Ops | +1.20% | Europe & North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Focus on Cloud-Based Cognitive IT Operations

Cloud-native cognitive operations platforms deliver on-demand scalability that traditional on-premises tools cannot match. Enterprises leverage built-in AI services from global cloud providers to ingest, store, and analyse petabytes of telemetry while maintaining sub-second alerting. The model lowers infrastructure overhead and cuts mean time to recovery by up to 40%, freeing engineering teams for higher-value tasks. Cloud adoption also accelerates feature velocity, allowing vendors to push daily enhancements that sharpen anomaly detection accuracy. As a result, organisations re-evaluate build-versus-buy strategies and overwhelmingly favour subscription models anchored in usage-based pricing.

Rising Demand for Monitoring Complex IT Environments

Microservices, containers, serverless functions, and edge nodes now form the backbone of digital business. A single customer transaction may traverse dozens of loosely coupled services spanning multiple clouds, making fault isolation arduous. Cognitive operations platforms apply unsupervised learning to correlate subtle signals across this sprawl, preventing cascading failures that could degrade user experience in milliseconds. Reported reductions of up to 80% in unplanned downtime translate directly into higher Net Promoter Scores and revenue retention for digital-first enterprises.

Surge in IT-Ops Data Volume from Digital Transformation

Telemetric data generation grows exponentially as IoT sensors, e-commerce events, and 5G endpoints stream logs, metrics, and traces around the clock. Processing costs can swallow 30% of an operation's budget, pressuring teams to adopt efficient data-pipeline architectures. GPU shortages in 2024-2025 forced enterprises to optimise existing clusters, catalysing interest in edge analytics and smart sampling to curb storage spend while preserving insight fidelity. Financial services firms running high-frequency trading systems exemplify the urgency, analysing terabytes of data daily to flag anomalies that could trigger regulatory scrutiny.

AI-Driven Proactive Incident Management Adoption

Machine-learning models trained on historical incidents now forecast impending outages with high confidence, allowing pre-emptive fixes during planned maintenance. Banking, healthcare, and telecom operators embed these capabilities into service-level agreements that demand 99.99% uptime. Organisations report 60-70% faster mean time to resolution after deploying AI-enabled runbooks that automate escalation and remediation workflows[1]ServiceNow, “Proactive Operations with AI-Driven Workflows,” servicenow.com . Beyond cost avoidance, proactive operations strengthen brand equity and regulatory compliance by preventing customer-visible disruptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration challenges with legacy systems | -1.80% | Global; acute in large incumbents | Short term (≤ 2 years) |

| Dearth of skills and expertise | -1.50% | Global; pronounced in emerging markets | Medium term (2-4 years) |

| Proprietary algorithms pose governance risk | -0.90% | Europe & North America | Long term (≥ 4 years) |

| Privacy regulations limit telemetry capture | -0.70% | Europe, spreading globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Challenges with Legacy Systems

Mainframe and proprietary applications dating back decades often lack modern observability hooks, forcing bespoke connectors that inflate project cost and risk. Financial institutions contend with COBOL-based core banking engines that must exchange data securely with AI-driven analytics without disrupting transaction throughput. Such integration work can consume up to half of total deployment budgets and elongate payback periods. The scarcity of professionals who understand both legacy architectures and AIOps exacerbates delays.

Dearth of Skills and Expertise

Cognitive operations demand cross-disciplinary know-how in machine learning, site-reliability engineering, and domain-specific IT operations. Universities lag in producing graduates with this blend, prompting enterprises to invest in internal academies or premium consulting engagements that command salary uplifts exceeding 30% over traditional roles. Talent concentration in major tech hubs widens adoption gaps between large urban centres and secondary markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Acceleration Drives Market Evolution

Solutions retained a 64.30% share of the cognitive operations market in 2025, cementing their role as the architectural backbone for telemetry collection, correlation, and automation. Yet Services revenue is projected to climb at 17.05% CAGR to 2031 as enterprises recognise that algorithm tuning, continuous model retraining, and organisational change management dictate ultimate ROI. The cognitive operations market size for professional services is forecast to reach USD 18.8 billion by 2031, reflecting a shift from license sales to outcome-based engagements.

Ongoing optimisation contracts and managed service offerings flourish because platforms require constant calibration to accommodate new microservices, evolving threat landscapes, and compliance mandates. Service providers deliver 24/7 monitoring, reducing incident fatigue for in-house teams and accelerating mean time to detection. As the scarcity of specialised talent persists, advisory and managed offerings become the fastest route to operational maturity for resource-constrained enterprises.

By Deployment Mode: Cloud Dominance Reshapes Operational Architecture

Cloud accounts for 71.20% of the cognitive operations market size and will continue expanding at a 17.55% CAGR, mirroring enterprise migration from monolithic data centres to elastic multi-cloud footprints. Vendors deliver platform updates weekly, embedding new analytics models without customer intervention, which shortens innovation cycles and lifts detection accuracy.

On-premises deployments persist in defence and financial services where data sovereignty is paramount, but even these sectors adopt hybrid models that offload heavy-duty analytics to the cloud while keeping raw data local. Edge-native AIOps emerges as a complementary approach for 5G and industrial IoT use cases requiring sub-millisecond inference. The interplay of cloud, on-premises, and edge options expands vendor differentiation beyond features to encompass data-gravity, latency, and regulatory considerations.

By Enterprise Size: SME Adoption Accelerates Through Cloud Accessibility

Large enterprises dominated early uptake with 58.30% revenue share in 2025, leveraging deep budgets to pilot full-stack solutions across global estates. However, SMEs are forecast to post a 16.68% CAGR as SaaS delivery compresses time-to-value and removes capital-expenditure hurdles. Tailored, click-to-deploy packages now ship with pre-configured templates and guided workflows, allowing smaller teams to monitor critical workloads without hiring dedicated data scientists. Multi-tenant architectures let vendors amortize compute costs, lowering entry-level pricing and aligning spend with usage. As SME digital transactions grow, customer expectations for always-on services push owners to invest in proactive monitoring to stay competitive. The democratization of AIOps thereby broadens the global customer base of the cognitive operations market and smooths revenue cyclicality for vendors.

By Application: Security Analytics Convergence Drives Innovation

IT Operations Analytics a held 27.40% share in 2025, underscoring its status as the cornerstone use case for capacity planning, performance tuning, and root-cause analysis. Yet Security Analytics is primed for the fastest 17.56% CAGR because advanced threats increasingly masquerade as innocuous performance anomalies. Platforms that fuse observability and security telemetry enrich context, enabling earlier breach detection and faster containment.

Cross-domain correlation unlocks zero-trust strategies by identifying irregular east-west traffic, insider risk, and credential misuse. Regulatory regimes such as the EU’s Digital Operational Resilience Act (DORA) mandate integrated operational and cyber resilience reporting, further accelerating convergence. Vendors that natively embed security analytics inside their cognitive operations suites differentiate through unified dashboards, shared metadata models, and consolidated incident resolution workflows.

By Industry Vertical: Healthcare Transformation Accelerates Adoption

BFSI remained the largest adopter with a 23.60% share in 2025 due to stringent uptime mandates and financial risk exposure. However, Healthcare and Life Sciences is expected to outpace peers at a 16.94% CAGR through 2031. Hospitals deploy AI-enabled observability to ensure electronic health record availability, monitor medical device telemetry, and predict capacity bottlenecks that could affect patient throughput.

Failure of a medication-dispensing robot or imaging workstation can jeopardize clinical outcomes and invite regulatory penalties. Cognitive operations continuously assess latency, packet loss, and configuration drift across hospital networks, automatically routing alerts to biomedical engineers for remediation. Pharmaceutical plants employ similar analytics to maintain Good Manufacturing Practice (GMP) compliance by detecting equipment degradation before it triggers batch scrap. With patient safety and regulatory fines on the line, healthcare CIOs fast-track AIOps funding despite budget constraints.

Geography Analysis

North America commands 37.40% of 2025 revenue, buoyed by the tight integration of observability with cloud-service portfolios from AWS, Microsoft Azure, and Google Cloud. Venture-capital inflows into AIOps start-ups surpassed USD 4.6 billion between 2024 and 2025, accelerating product maturity and ecosystem depth. Major acquisitions, exemplified by Cisco’s purchase of Splunk, broaden platform capability from log analytics to full-stack security and network telemetry. US financial institutions and hyperscalers act as anchor tenants, pushing vendors toward FedRAMP and SOC 2 certifications that, once achieved, unlock adjacent public-sector opportunities.

Asia Pacific is the fastest-growing region, expanding at an 17.61% CAGR. Telecommunications operators in Japan and South Korea rely on edge-native analytics to orchestrate 5G network slices, while Chinese cloud providers embed AIOps directly into Infrastructure-as-a-Service layers for manufacturing and ecommerce customers. India’s managed-service giants deploy cognitive operations to meet stringent service-level objectives for global clients, turning the subcontinent into a talent hub for AIOps engineering. Regional governments, meanwhile, invest in national AI strategies that subsidize research and lower barriers to enterprise adoption.

Europe exhibits steady but compliance-conscious growth. The EU’s AI Act and GDPR necessitate privacy-by-design data pipelines, compelling vendors to implement granular telemetry filtering and sovereign-cloud deployment options. German automotive OEMs tie cognitive operations to smart-factory rollouts, optimizing robotics uptime and energy consumption. The United Kingdom emphasizes operational resilience in financial services, requiring annual impact tolerance tests that stimulate spending on automated failover and chaos-engineering tools. Sustainability mandates further spur GreenOps modules that quantify carbon emissions and suggest workload re-balancing across greener data centers.

Regulatory Landscape

Cognitive operations deployments increasingly fall under AI governance regimes that combine model-risk controls with data-protection and operational-resilience requirements. In the European Union, the AI Act framework (Regulation (EU) 2024/1689) raises transparency and governance obligations for AI systems used in customer-facing and operational workflows, and it runs alongside GDPR constraints on telemetry collection and processing. In the United States, adoption is shaped more by standards and sector guidance than a single federal AI law, with NISTs AI Risk Management Framework (AI RMF) and related profiles used as a common reference for documenting risk controls, validation, and accountability in operational AI use cases.

2026 also added more specific compliance anchors for cognitive operations platforms that embed GenAI and automated decisioning into IT workflows. South Korea enacted the AI Basic Act in February 2026, adding risk-management requirements for high-impact AI, while NIST released an April 2026 concept note for an AI RMF Profile focused on Trustworthy AI in Critical Infrastructure, signaling tighter scrutiny for operators of essential services. In Europe, policy attention shifted toward implementation pacing and enforceability, with AI Act transparency and general-purpose AI governance rules becoming enforceable in August 2026, and later omnibus actions deferring certain high-risk compliance dates. Vendors have leaned more on privacy-by-design telemetry controls, audit trails, and explainability workflows to support regulated-industry sales.

Value Chain Analysis

The cognitive operations value chain begins with telemetry generation across applications, infrastructure, networks, and security tools, then moves into data ingestion and normalization (logs, metrics, traces, events), storage and stream processing, and AI/ML analytics for anomaly detection, correlation, and root-cause inference. Upstream inputs include cloud infrastructure and data platforms (compute, GPU/accelerators, object storage), observability and ITSM/ITOM data sources, and connectors for legacy systems. Midstream layers cover model development and tuning, policy and governance controls, and automation orchestration (runbooks, workflow engines, and integrations), while downstream delivery is dominated by SaaS subscriptions, managed services, and professional services for integration, model retraining, and change management.

Ecosystem structure continues to consolidate around platform vendors, hyperscalers, and service partners that package end-to-end outcomes. Alliances such as BMCs partnerships with Google Cloud and Amdocs reinforce the need for scalable ingestion and telecom-specific integrations. Innovation is supported by AI-native specialists and automation-first offerings, including ScienceLogic introducing a generative AI engine for incident triage, alongside funding for automation-focused entrants such as Selector AI and Ciroos to expand network-centric and SRE automation. Key bottlenecks remain at integration and governance layers, where legacy estates often require bespoke connectors, regulated industries require auditability for automated actions, and the skills gap shifts value toward services, managed operations, and packaged accelerators rather than standalone tooling.

Competitive Landscape

The cognitive operations market hosts a moderately fragmented roster in which the top five vendors control roughly 48% of global revenue, leaving ample room for niche specialists. IBM leverages decades of IT-service-management know-how and Red Hat OpenShift integration to retain enterprise workloads that demand hybrid flexibility. Broadcom complements its infrastructure monitoring suite with VMware Cloud Foundation, carving out private-cloud relevance[3]Broadcom, “VMware Cloud Foundation for Hybrid Cloud,” broadcom.com. BMC Helix refocuses on software-as-a-service delivery after a 2025 corporate split designed to spur innovation speed.

Cloud-native disruptors accelerate feature velocity through continuous deployment and intuitive user experiences. Datadog grew quarterly revenue 25% year-over-year in Q1 2025, added 3,770 customers with USD 100k+ ARR, and acquired Eppo and Metaplane to fold feature-flag governance and data observability into its stack. ServiceNow’s USD 2.85 billion acquisition of Moveworks adds conversational AI, enabling contextual incident triage through natural language. Selector AI specialises in network-centric cognitive operations for telcos, raising USD 33 million to expand across Asia and Europe.

Partnership ecosystems now differentiate leading platforms. BMC collaborates with Google Cloud for scalable ingestion pipelines, while Cisco aligns Splunk’s log analytics with AppDynamics’ application performance monitoring capabilities. Vendors also integrate with DevOps, SecOps, and FinOps tooling to deliver unified governance dashboards. Competitive success hinges on proving tangible business outcomes shorter mean time to detection, lower cloud spend, and verified compliance, rather than merely touting algorithmic sophistication.

Cognitive Operations Industry Leaders

IBM Corporation

Micro Focus International Plc

VMware, Inc.

Splunk Inc.

Broadcom Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space is most visible where buyers need closed-loop remediation across hybrid estates but run into governance and data-sovereignty constraints. Platforms that embed policy controls at runtime and support sovereign deployment patterns fit regulated and public-sector buyers that cannot centralize raw telemetry, reinforcing demand for hybrid architectures that keep sensitive data local while still enabling high-scale analytics. Vendor moves in 2026, including IBM positioning an AI-powered operations layer for coordinated response and introducing a sovereign core concept for policy enforcement, highlight how compliance-ready operating models are becoming part of product decisions rather than an after-deployment add-on.

An additional opportunity sits in modernizing operations centers in telecom and large enterprises, shifting from alert-driven workflows toward autonomous, model-assisted operations that correlate observability and security signals. In technology and telecom specifically, published industry programs on sovereign and industrial AI infrastructure, such as Deutsche Telekoms industrial AI cloud initiative in Munich going live in early 2026 as referenced in Tech Mahindra industry insights, point to ongoing investment in AI-ready operational backbones. The market also leaves room for specialist solutions that reduce operational toil in complex environments, such as SRE assistants and GenAI triage, as long as they integrate into existing ITSM/ITOM stacks, which aligns with ScienceLogic launching generative incident triage and funding rounds for automation-focused entrants like Ciroos and Selector AI.

Recent Industry Developments

- July 2026: IBM highlighted IBM Power Autonomous Operations as an AI-enabled approach to managing Power environments by automating observation, analysis, and selected operational tasks. The update extends autonomous operations concepts beyond x86-centric estates into IBM Power footprints that are common in large enterprises, reinforcing demand for unified AIOps practices across heterogeneous infrastructure.

- May 2026: Broadcom announced VMware Cloud Foundation 9.1, positioning it as a secure and cost-effective private cloud platform for production AI with mixed-compute support. This strengthens private cloud relevance for cognitive operations buyers that need consistent observability and automation controls while running sensitive workloads outside public cloud-only architectures.

- November 2024: ScienceLogic unveiled Skylar AI, a generative AI engine aimed at automating real-time incident triage. By accelerating how teams interpret and act on operational signals, the launch supported the shift from manual alert handling toward AI-assisted decisioning inside IT operations workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the cognitive operations market covers software and related services that use AI and analytics to monitor, predict, and automate IT and business operations workflows. This includes operational insights, event correlation, and guided remediation across major enterprise environments.

Scope exclusions: purely manual IT managed services without a cognitive layer, generic infrastructure hardware, and standalone cybersecurity products not positioned for operations analytics are excluded.

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Mode

- Cloud

- On-Premises

- By Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By Application

- IT Operations Analytics

- Application Performance Management

- Network Analytics

- Security Analytics

- Infrastructure Management

- Other Applications

- By Industry Vertical

- BFSI

- Healthcare and Life Sciences

- IT and Telecom

- Retail and E-commerce

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and build the first demand and supply signals that can be verified. We relied on public and official sources such as NIST publications, IEEE and ACM digital library articles, U.S. SEC filings, Bureau of Labor Statistics series on IT and software employment, and OECD indicators that help explain enterprise digital spend capacity.

To translate scope into measurable inputs, we reviewed company annual reports and investor presentations, product documentation and public pricing cues where available, and trusted press coverage on enterprise AI operations rollouts. Patent database scans were also used to understand where engineering focus is rising, and a company financials and intelligence subscription was used selectively to normalize segment-level revenue disclosures. These sources are illustrative, and many other public documents were also referenced to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with enterprise IT operations leaders, platform owners, system integrators, and domain specialists who manage AIOps, observability, and automation programs. Since adoption differs by cloud maturity and regulated industry intensity, we gathered views across major regions and across both large enterprises and scaling mid-size adopters to close gaps left by public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 17% | APAC: 43% |

| Mid tier: 48% | Functional/Unit leaders: 26% | EMEA: 37% |

| Smaller Players: 19% | Managers: 57% | Americas: 20% |

Market-Sizing & Forecasting

Sizing started with a top-down build where enterprise software and IT operations spend pools were reconstructed by region, then filtered by the attach rate of cognitive operations use cases across monitoring, application performance management, network analytics, security analytics, and infrastructure management. After shaping the demand pool, adoption intensity was adjusted using inputs like cloud migration pace, observability tooling penetration, typical deployment mix (cloud versus on-premises), and the share of spend going to services versus tools.

The totals were then corroborated using selective bottom-up approximations, including sampled vendor revenue splits discussed in public materials, channel checks with service providers, and simple ASP times volume checks using seat, node, or workload based pricing proxies. Where disclosures were missing, gaps were handled by using peer averages within the same product motion, followed by adjustments during interview validation.

For forecasting, scenario analysis was used, since spending can swing with IT budget cycles and platform consolidation waves. Growth paths were guided by expert consensus on AI assistant adoption in operations teams, expansion of automation coverage, and faster incident response targets, then translated into annual penetration and price progression assumptions.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as enterprise software growth trends, IT services momentum, and cloud operations complexity indicators, and then reviewed for outliers by region and application. When a variance appeared, we traced the underlying driver back to a specific input, and re-contacted respondents where the assumption could not be supported with a clear rationale.

Before sign-off, the numbers go through multi-step analyst review, including consistency checks across historical progression and implied spend per adopting enterprise. Reports are refreshed annually, with interim updates when material changes affect adoption or pricing expectations. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Cognitive Operations Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for cognitive operations, even when the same label is used. Differences usually come from what is counted as cognitive operations versus adjacent tools, which year is treated as the anchor, and how services revenue is handled when platforms are sold through partners.

Key gaps also show up in how pricing is projected, since some estimates assume flat average selling prices while others model discounting, bundling, or module expansion over time. Currency conversion timing, treatment of multi-year contracts, and how quickly the model is refreshed after major AI releases can also move the total in a meaningful way. By tracking deployment mix, services attach, and application coverage, Mordor Intelligence keeps the cognitive operations total limited to solutions and services tied to operations analytics and automation, and then rechecks assumptions with fresh expert feedback before the final number is locked.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 23.78 B (2026) | |

| Trade Journal A | USD 34.75 B (2029) | Uses a later target year and often blends broader cognitive software categories into the total, which can pull in adjacent AI platform and automation revenues beyond operations workflows. |

| Industry Portal B | USD 16.72 B (2025) | Anchors on an earlier year and applies a higher headline CAGR without clearly separating services versus software, which can shift the starting point and the implied price curve. |

The spread in the table is mostly explained by scope boundaries and timing choices, followed by how services and pricing progression are treated. When variables are defined in plain terms and checked against interview feedback and public demand signals, the result is easier to trace and simpler to update when market conditions change.

Key Questions Answered in the Report

What is the current value of the cognitive operations market and its growth outlook?

The cognitive operations market size stood at USD 23.78 billion in 2026 and is forecast to grow to USD 50.39 billion by 2031 at a 16.18% CAGR.

Which deployment model is growing fastest?

Cloud deployment leads with 71.20% revenue share in 2025 and is projected to register the fastest 17.55% CAGR because of its elastic scalability and lower ownership costs.

Why is Security Analytics the fastest-growing application category?

Convergence of observability and cybersecurity allows early breach detection; hence Security Analytics is expected to post an 17.56% CAGR through 2031.

What regions should vendors prioritise for expansion?

Asia Pacific offers the highest 17.61% CAGR, driven by aggressive 5G rollouts, AI-friendly policies, and rapid cloud adoption across manufacturing and finance.

How are skills shortages affecting market adoption?

A scarcity of cross-disciplinary AIOps professionals extends project timelines and inflates costs, prompting enterprises to rely on managed-service partners and internal training programs.

What level of market fragmentation exists today?

The market earns a concentration score of 6; top five players hold under 50% combined share, so new entrants still have considerable opportunity to capture niche segments.

Page last updated on: