Cognitive Computing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

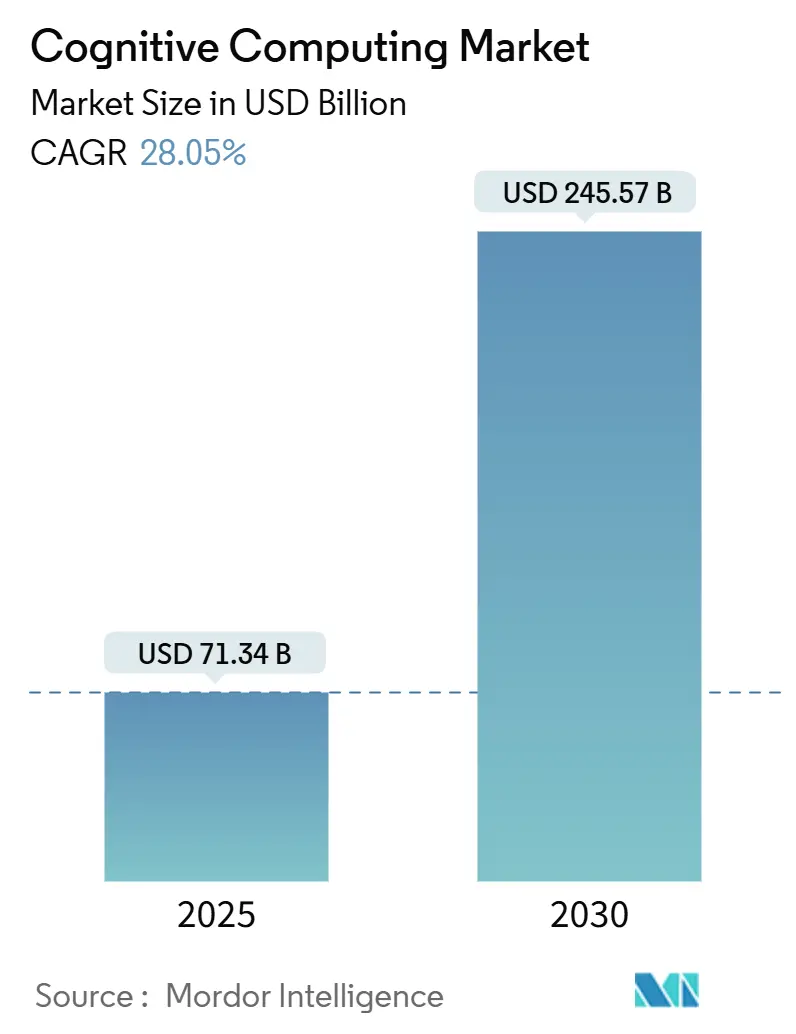

| Market Size (2025) | USD 71.34 Billion |

| Market Size (2030) | USD 245.57 Billion |

| Growth Rate (2025 - 2030) | 28.05% CAGR |

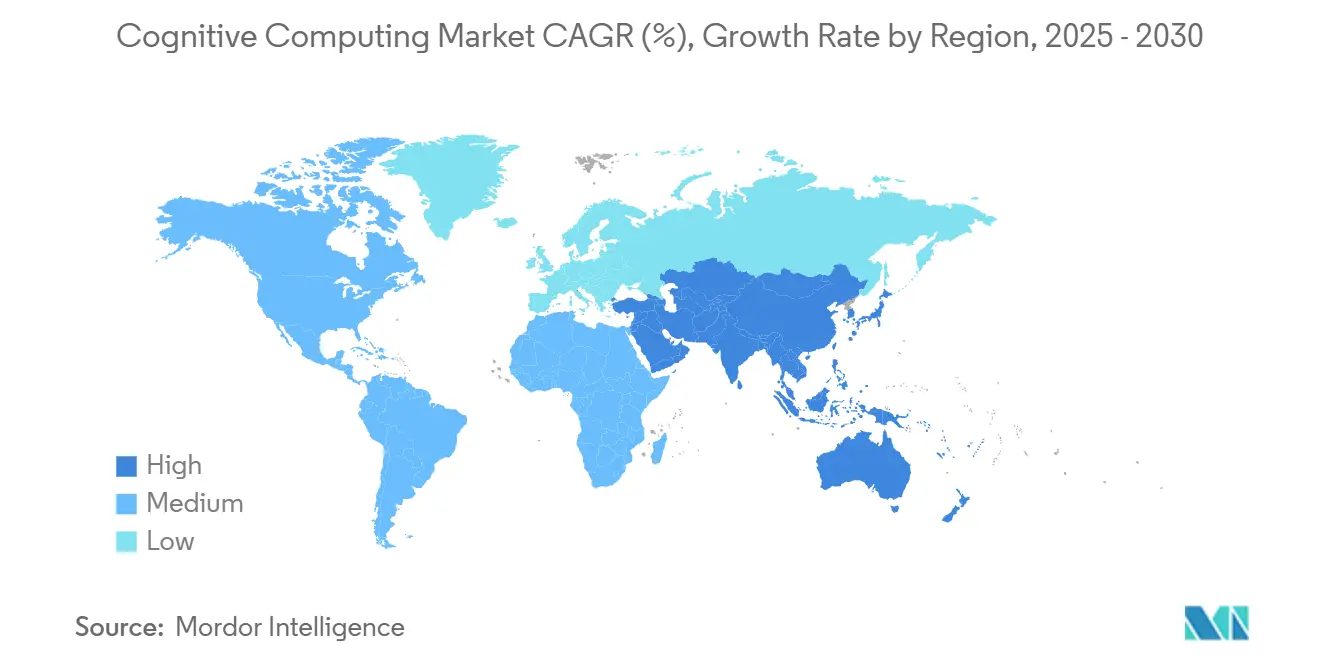

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cognitive Computing Market Analysis by Mordor Intelligence

The cognitive computing market size is USD 71.34 billion in 2025 and is forecast to climb to USD 245.57 billion by 2030, reflecting a 28.05% CAGR over the period. Growth rests on three pillars: cloud-hosted cognitive platforms that strip away capital barriers, real-time decision support needs in regulated sectors, and the arrival of domain-trained foundation models that shorten pilot-to-production cycles. Enterprises are moving unstructured data workloads to cognitive engines, leveraging natural language, vision, and multimodal analytics to replace rule-based systems and address skill shortages. Cloud hyperscalers widen the addressable base through subscription pricing and continuous model upgrades, while hardware advances such as integrated NPUs raise performance per watt. At the same time, “Green-AI” mandates and data-sovereignty rules are shaping deployment choices and sparking demand for cost-efficient, compliant architectures.

Key Report Takeaways

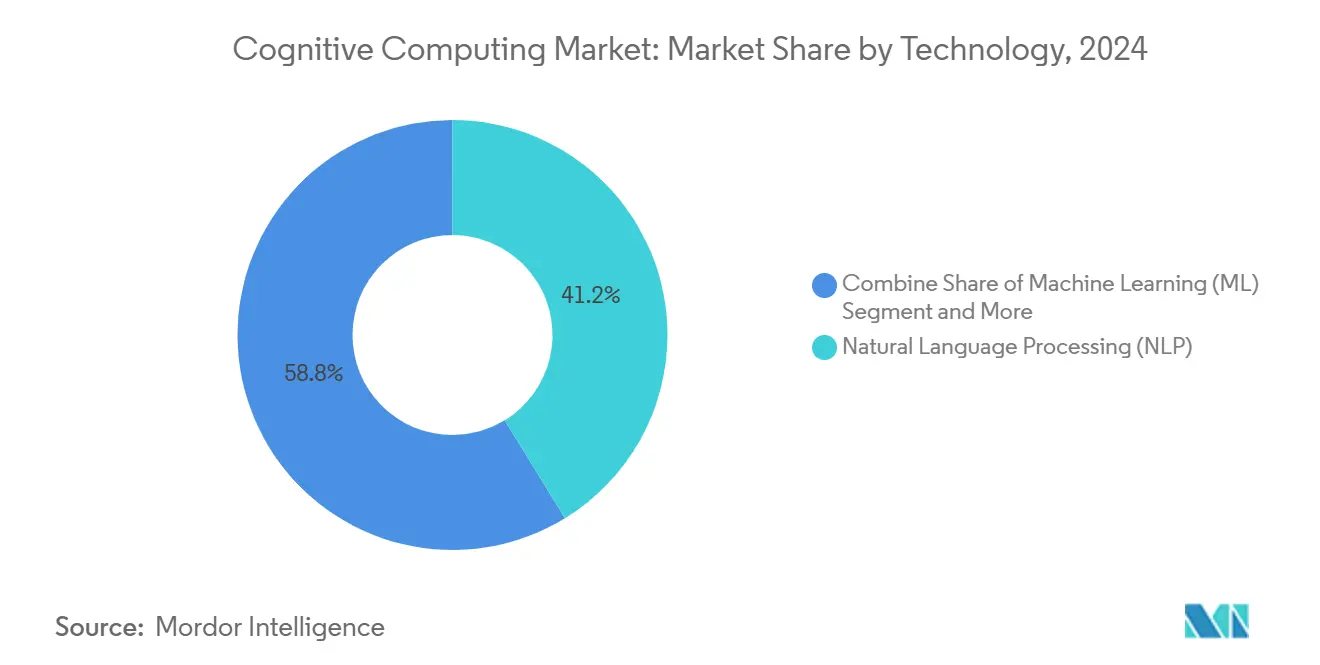

- By technology, Natural Language Processing led with 41.23% of the cognitive computing market share in 2024, whereas Machine Learning is projected to expand at a 31.46% CAGR through 2030.

- By deployment type, on-premise accounted for 51.54% of the cognitive computing market size in 2024, and cloud deployments are advancing at a 30.68% CAGR to 2030.

- By organization size, large enterprises held 64.65% share of the cognitive computing market size in 2024, while Small and Medium Enterprises are growing at a 29.76% CAGR.

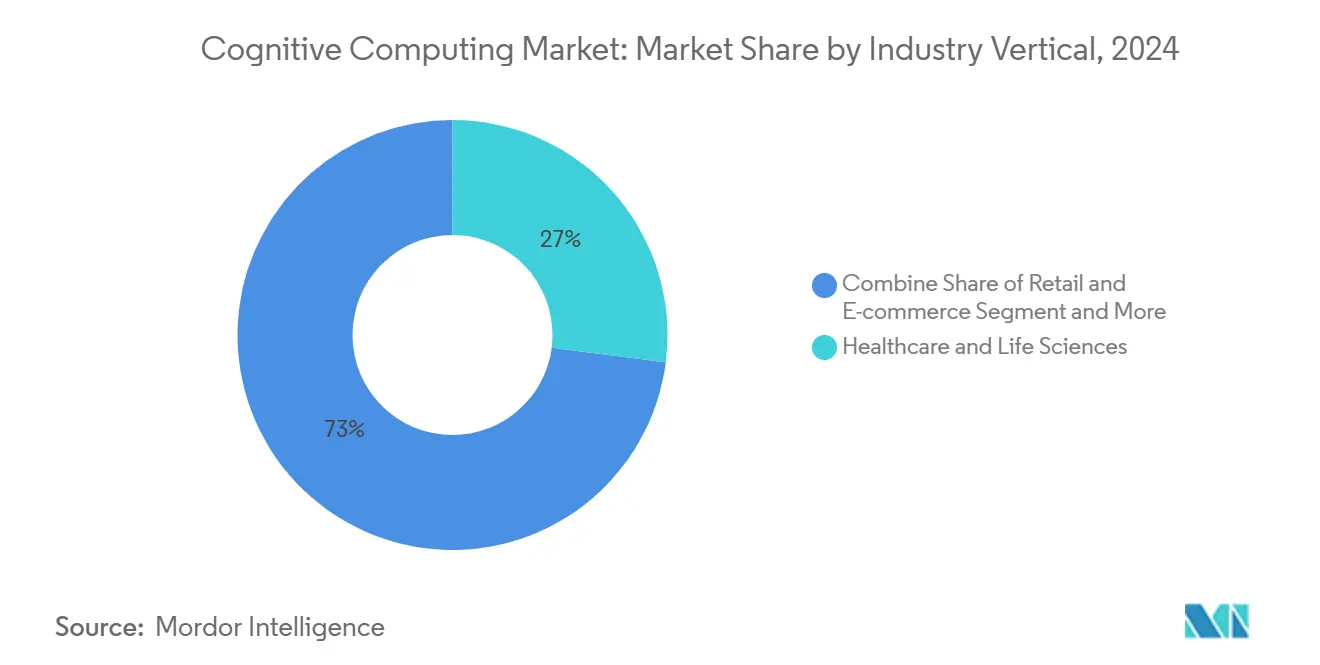

- By industry vertical, healthcare and life sciences captured 27.03% of the cognitive computing market share in 2024, and retail and e-commerce are set to surge at a 33.85% CAGR.

- By application, customer service and virtual assistants claimed 28.32% of the cognitive computing market size in 2024, and risk and fraud management is forecast to progress at a 32.76% CAGR.

- North America commanded 38.43% of the cognitive computing market share in 2024; Asia-Pacific is on track for a 32.12% CAGR through 2030.

Global Cognitive Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of enterprise unstructured data volumes | +6.2% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising demand for AI-powered customer engagement tools | +5.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Cloud-based cognitive platforms lowering entry barriers | +4.9% | Global, faster in Asia-Pacific and MEA | Medium term (2-4 years) |

| Accelerated healthcare decision-support adoption | +4.1% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Industry-specific foundation models gain traction | +3.7% | North America and Europe, selective Asia-Pacific | Medium term (2-4 years) |

| “Green-AI” mandates spur cognitive optimization | +2.9% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Enterprise Unstructured Data Volumes

Enterprises now ingest petabytes of unstructured text, images, and sensor streams every month, far outpacing traditional analytics capacity. Cognitive engines process these mixed data types in real time, enabling contextual insights that feed product quality initiatives and regulatory reporting. IBM’s 2024 deployment with Novate Solutions cut manufacturing waste by 15% and improved quality by 30%. The self-reinforcing cycle of data generation and insight creation has turned cognitive tools from optional add-ons into operational necessities, particularly in compliance-sensitive industries.

Rising Demand for AI-Powered Customer Engagement Tools

Customer expectations for instant, personalized responses drive firms to embed conversational AI that grasps sentiment and intent across channels. More than 3,000 companies adopted Salesforce’s autonomous Agentforce suite by late 2024, trimming service costs by 25% while lifting satisfaction metrics. [1]Salesforce, “Agentforce Is Here,” Investor Relations Salesforce, investor.salesforce.com Amazon’s Q assistant, integrated with 40 enterprise systems, highlights how cognitive platforms convert support desks from cost centers to revenue engines. These deployments generate behavior data that loops back into training pipelines, continuously enhancing model accuracy.

Cloud-Based Cognitive Platforms Lowering Entry Barriers

Subscription pricing and managed infrastructure let firms pilot cognitive workloads without large capital outlays. AWS’s Generative AI Partner Innovation Alliance moved half of its proofs of concept into production within one year. [2]Amazon.com, Inc., “Amazon Q,” About Amazon, aboutamazon.com BT Group’s GenAI Gateway centralizes model governance, reducing duplication risk and tightening cost control. The pay-as-you-go model also extends advanced capabilities to emerging markets, where scarce AI talent once delayed adoption.

Accelerated Healthcare Decision-Support Adoption

Hospitals deploy cognitive engines to read medical images, extract patterns from electronic health records, and cross-check clinical literature simultaneously. Cognitive surveillance reduced Nasdaq’s market investigation cycle by 33%, a framework now mirrored in complex clinical review pathways. As physician burnout rises, AI assists with rote analysis, freeing clinicians for patient-facing tasks and raising diagnostic accuracy benchmarks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation and training costs | -3.8% | Global, higher in emerging markets | Short term (≤ 2 years) |

| Data-privacy and compliance burden | -2.9% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Scarcity of standards for synthetic training data | -2.1% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Auditor scepticism on explainability in finance | -1.6% | North America and Europe, selective Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Training Costs

Total outlays often exceed software licences by 200–300% once data engineering, model tuning, and workforce skilling are factored in. Intel’s 2024 restructuring, aimed at trimming USD 10 billion in costs and 15% of staff, signals the pressure even technology leaders face when scaling cognitive stacks. [3]Intel Corporation, “Intel Reports Second-Quarter 2024 Financial Results,” Intel, intc.comSMEs struggle most, yet they also stand to gain the greatest efficiency upside once entry obstacles fall.

Data-Privacy and Compliance Burden

Firms must reconcile large-scale data ingestion with strict privacy norms such as Japan’s pending AI law that mandates transparency in automated decisions. Financial institutions additionally require auditable model outputs, inflating governance budgets by up to 40%. The resulting friction slows agility and forces trade-offs between model complexity and explainability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: NLP Strength Meets ML Momentum

Natural Language Processing held 41.23% of the cognitive computing market in 2024, anchored in document analytics and customer support chatbots. The cognitive computing market size for Machine Learning-centric solutions is projected to record the fastest 31.46% CAGR, reflecting the adoption of self-training models that span text, vision, and tabular data. Deep Learning keeps a foothold in image-heavy use cases, while Computer Vision gains share in smart-factory rollouts. Enterprises often begin with rule-based NLP, then graduate to ML once data pipelines mature. Fujitsu’s Kozuchi agent mixes NLP, ML, and reasoning to automate meeting follow-ups, illustrating convergent architectures. As the cognitive computing market deepens, Automated Reasoning’s explainable outputs are drawing interest from financial auditors who reject opaque models.

By Deployment Type: Cloud Ascendancy Challenges On-Premise

On-premise deployments accounted for 51.54% of the cognitive computing market share in 2024, reflecting data-sovereignty mandates in banking and healthcare. The cognitive computing market size for cloud deployments is forecast to grow at 30.68% CAGR as subscription economics prevail. Hybrid models reconcile latency and compliance demands by splitting sensitive data from intensive inference jobs. AWS government clouds and Microsoft compliance blueprints ease security doubts, while Intel’s Xeon 6 processors lift both on-prem and cloud throughput by 70% per watt. Decision makers now allocate workloads by sensitivity, driving multicloud orchestration tools that fine-tune cost and governance.

By Organization Size: SME Upsurge Pressures Enterprise Lead

Large enterprises controlled 64.65% of revenue in 2024 thanks to in-house talent and integration budgets. Yet SMEs are expected to log a 29.76% CAGR, propelled by low-code studios and pay-as-you-go billing that compress time-to-value. IBM notes that 20% of new small businesses treat generative AI as a virtual co-founder, automating paperwork and ideation. As the cognitive computing market democratizes, SMEs focus on out-of-the-box use cases, whereas enterprises wrestle with legacy system sprawl.

By Industry Vertical: Healthcare Lead Faces Retail Acceleration

Healthcare and life sciences contributed 27.03% to 2024 revenue as hospitals integrated image analysis and clinical NLP into diagnostic routines. Retail and e-commerce will add the highest incremental value, expanding at 33.85% CAGR on the back of personalisation engines and dynamic pricing. NEC’s Japanese-tuned language models support healthcare’s documentation load, while Amazon-backed Midea cut call-center costs by 30% through generative agents. Financial services maintain steady fraud and compliance spend, and manufacturers push predictive maintenance at the edge.

By Application: Customer Service Lead Meets Fraud Detection Surge

Customer service and virtual assistants represented 28.32% of 2024 spending as firms sought consistent multichannel support. Risk and fraud management solutions are on a trajectory for a 32.76% CAGR, driven by real-time anomaly detection. JPMorgan’s AI engine flags fraudulent activity 300 times faster, saving USD 200 million a year. Predictive maintenance and intelligent process automation gain favour in capital-intensive sectors, while sales-and-marketing optimisers mine behavioural data for conversion gains.

Geography Analysis

North America retained 38.43% of revenue in 2024, buoyed by venture funding, skilled talent, and established cloud estates. United States federal AI programmes and Intel’s 500 model optimisations keep the region on the leading edge. Canada advances ethical-AI sandboxes, whereas Mexico pilots cognitive quality control in export manufacturing.

Asia-Pacific is slated to post a 32.12% CAGR to 2030 as governments bankroll sovereign AI stacks. Japan’s JPY 150 billion (USD 960 million) commitment through SoftBank to home-grown large language models typifies the strategic push. India’s developer pool crafts cost-effective engines, while South Korea integrates cognitive layers into consumer electronics. China scales smart-city pilots, and ASEAN firms adopt cloud cognitive suites to leapfrog legacy IT.

Europe balances innovation with oversight, favouring explainable systems that pass GDPR scrutiny. Germany’s Industry 4.0 factories embed vision-based defect detection, the United Kingdom drives reg-tech in financial hubs, and France deploys AI across aerospace supply chains. Nordic utilities pilot “green-AI” optimisers that cut inference energy by 25%. Middle East oil economies fund smart-city cognitive grids, and several African nations deploy mobile-first chatbots for financial inclusion.

Competitive Landscape

The cognitive computing market shows moderate concentration: platform leaders IBM, Microsoft, Google, and Amazon combine broad tool stacks with proprietary data troves. Specialist vendors thrive by drilling into vertical niches such as Nuance’s clinical speech or Darktrace’s cyber-defence algorithms. Hardware titans Intel and NVIDIA compete underneath, embedding accelerators that lift throughput while shaving joules per inference.

Strategic patterns fall into three camps. First, platform expansion: Microsoft layers Copilot across Office and Azure. Second, vertical depth: Fujitsu’s Kozuchi targets factory and legal workflows with domain-trained models. Third, infrastructure focus: Intel’s Xeon 6 boosts radio-access network AI, trimming telecom energy budgets by 70% per watt. Patent filings cluster around generative learning, edge inference, and privacy-preserving training as firms seek defensible moats.

White-space opportunities remain in hybrid orchestration, industry foundation models, and low-resource language coverage. Vendors that marry compliance, energy efficiency, and seamless integration are positioned to outpace generalists in heavily regulated or sustainability-focused markets. Overall, sustained R&D investment and ecosystem partnerships will dictate share movement through 2030.

Cognitive Computing Industry Leaders

International Business Machines Corporation

Microsoft Corporation

Alphabet Inc.

Amazon.com, Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Intel unveiled Xeon 6 SoCs with 2.4× RAN capacity and 70% efficiency gains, adding AI acceleration for virtual and open RAN rollouts.

- January 2025: Intel introduced Core Ultra 200V processors with integrated NPUs and vPro security, targeting next-generation business laptops.

- December 2024: Fujitsu developed a multimodal video analytics agent to automate frontline reporting and improvement planning.

- December 2024: AWS disclosed that appliance maker Midea deployed Amazon Connect across 14 countries, achieving a 95% connection rate in under 60 seconds and 30% cost savings.

Global Cognitive Computing Market Report Scope

| Natural Language Processing (NLP) |

| Machine Learning (ML) |

| Deep Learning |

| Automated Reasoning |

| Computer Vision |

| On-Premise |

| Cloud |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Healthcare and Life Sciences |

| Banking, Financial Services and Insurance |

| Retail and E-commerce |

| IT and Telecom |

| Manufacturing |

| Government and Defense |

| Energy and Utilities |

| Other Industry Vertical |

| Customer Service and Virtual Assistants |

| Risk and Fraud Management |

| Predictive Maintenance |

| Intelligent Process Automation |

| Sales and Marketing Optimization |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology | Natural Language Processing (NLP) | ||

| Machine Learning (ML) | |||

| Deep Learning | |||

| Automated Reasoning | |||

| Computer Vision | |||

| By Deployment Type | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Industry Vertical | Healthcare and Life Sciences | ||

| Banking, Financial Services and Insurance | |||

| Retail and E-commerce | |||

| IT and Telecom | |||

| Manufacturing | |||

| Government and Defense | |||

| Energy and Utilities | |||

| Other Industry Vertical | |||

| By Application | Customer Service and Virtual Assistants | ||

| Risk and Fraud Management | |||

| Predictive Maintenance | |||

| Intelligent Process Automation | |||

| Sales and Marketing Optimization | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the market value of cognitive computing in 2025?

The cognitive computing market is valued at USD 71.34 billion in 2025.

How fast will global demand grow through 2030?

Revenue is forecast to rise at a 28.05% CAGR, taking the market to USD 245.57 billion by 2030.

Which technology holds the largest share today?

Natural Language Processing leads with 41.23% share of 2024 revenue.

Why are SMEs adopting cognitive tools so quickly?

Low-code platforms and subscription pricing cut capital costs, letting SMEs scale projects and achieve ROI rapidly.

Which region is expanding the fastest?

Asia-Pacific is set for a 32.12% CAGR through 2030 as government programmes and digitalisation accelerate adoption.

What are the biggest hurdles to implementation?

High setup costs and stringent data-privacy regulations add complexity and can delay full-scale deployment.

Page last updated on: