Cognitive Data Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

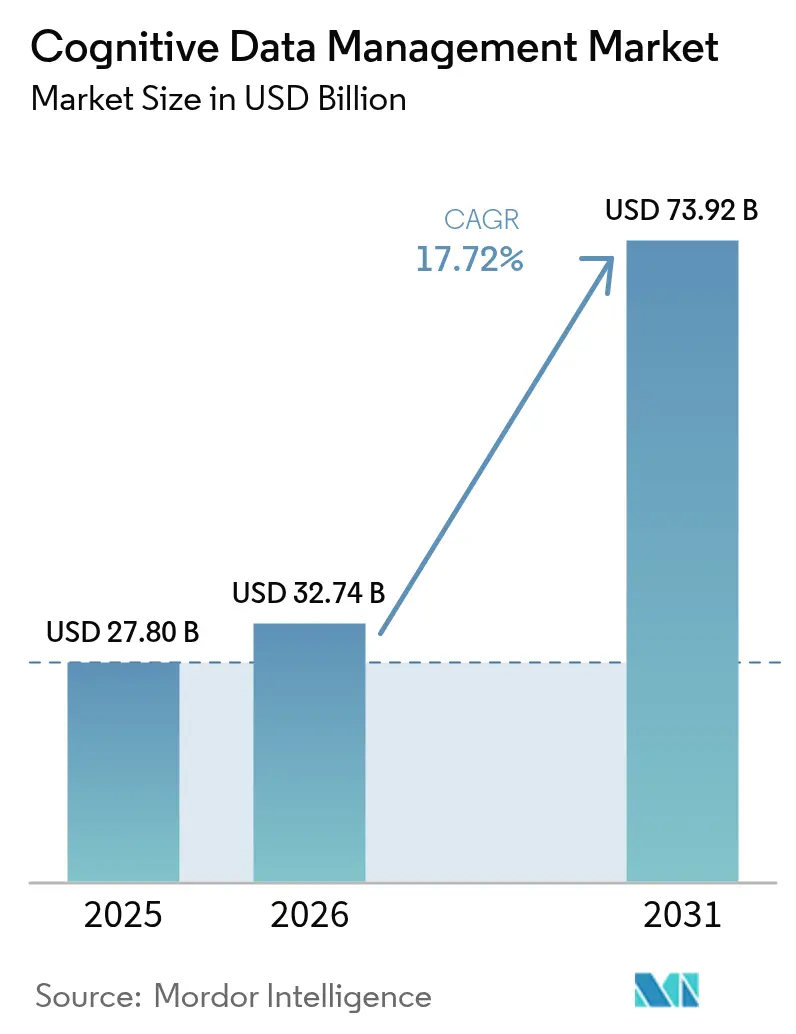

| Market Size (2026) | USD 32.74 Billion |

| Market Size (2031) | USD 73.92 Billion |

| Growth Rate (2026 - 2031) | 17.72% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cognitive Data Management Market Analysis by Mordor Intelligence

The Cognitive Data Management Market size was valued at USD 27.80 billion in 2025 and estimated to grow from USD 32.74 billion in 2026 to reach USD 73.92 billion by 2031, at a CAGR of 17.72% during the forecast period (2026-2031).

The rapid adoption of generative AI in enterprises, escalating regulatory scrutiny, and the surge in IoT-sourced data drive the expansion of the cognitive data management market. Foundational AI models now perform metadata enrichment in minutes rather than months, while privacy-preserving clean-room architectures support cross-enterprise analytics without exposing sensitive information. Cloud platforms equipped with GPU clusters enable real-time data orchestration, and industry-specific solutions shorten compliance cycles for healthcare, financial services, and manufacturing. Moderate vendor fragmentation encourages specialized entrants that focus on sector-tailored governance, automated lineage, and vector-ready cataloging capabilities.

Key Report Takeaways

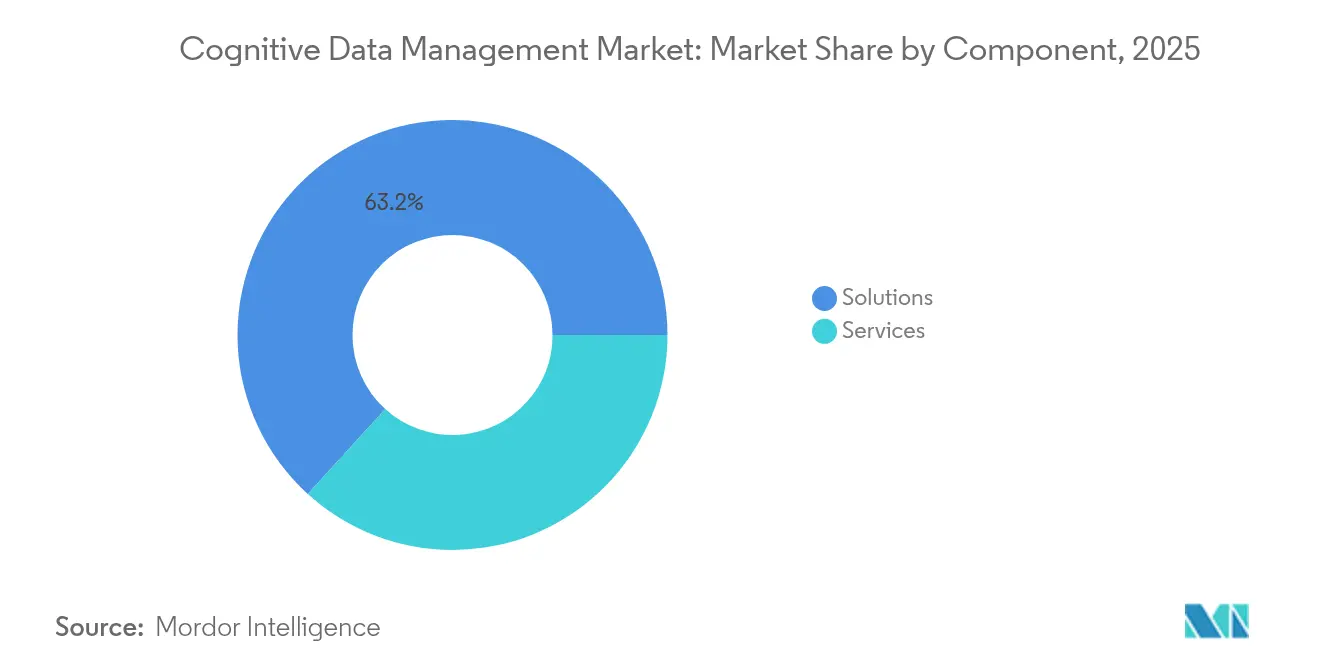

- By component, solutions led with 63.25% revenue share in 2025 in the cognitive data management market; services are projected to advance at a 24.1% CAGR to 2031.

- By deployment type, cloud captured 60.45% of the cognitive data management market share in 2025, while hybrid and multi-cloud deployments are forecast to expand at a 22.9% CAGR through 2031.

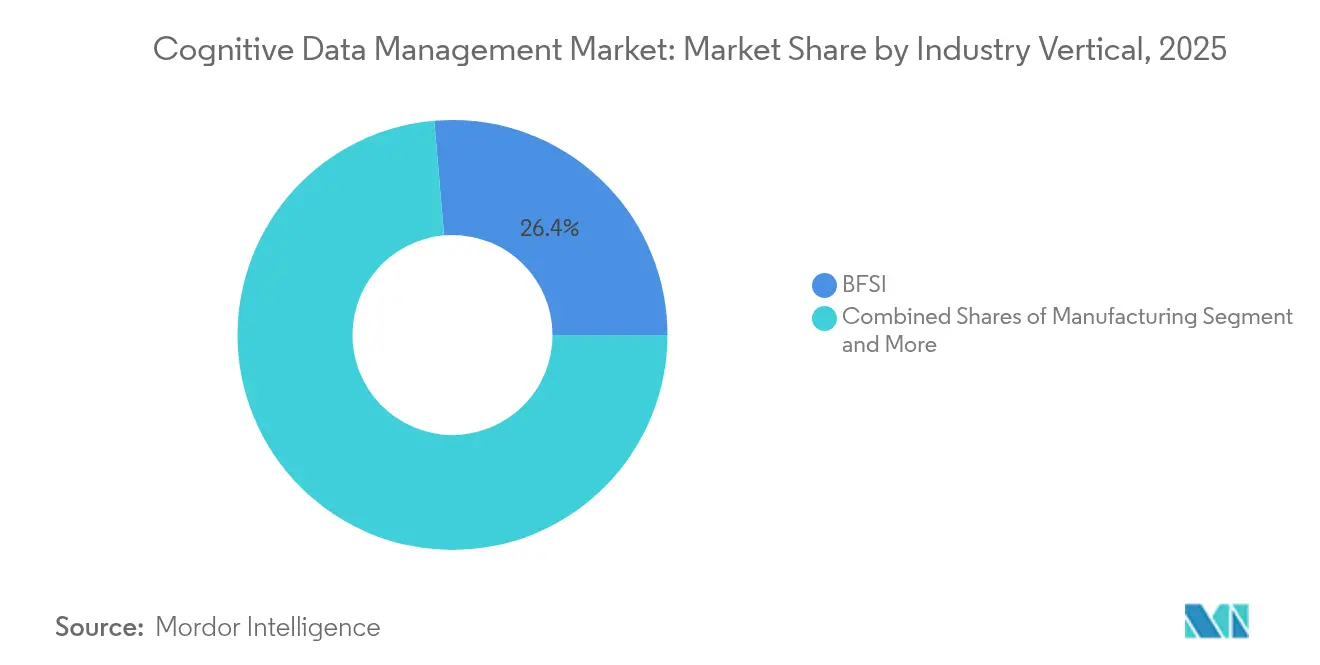

- By industry vertical, the BFSI sector held 26.35% of the cognitive data management market size in 2025; healthcare is the fastest-growing vertical with a 21.1% CAGR between 2026 and 2031.

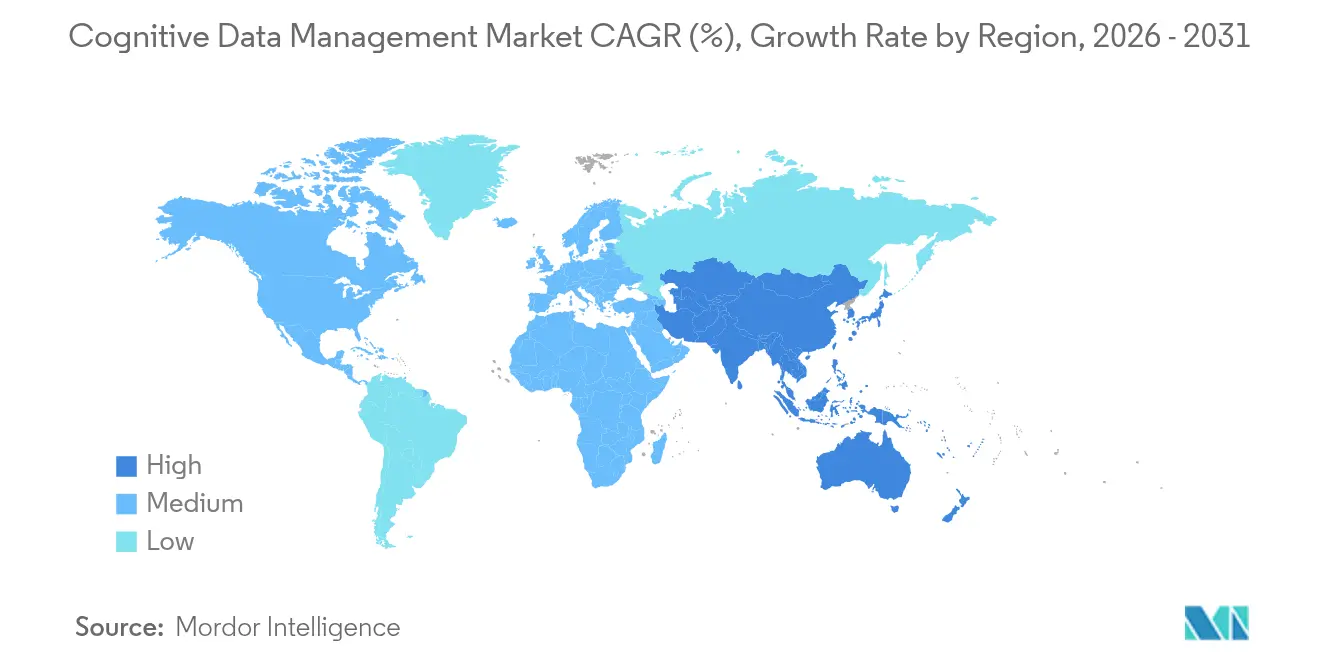

- By geography, North America commanded 41.20% revenue share in 2025 in the cognitive data management market; APAC is projected to record the quickest expansion at a 20.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cognitive Data Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IoT-linked data deluge | +4.2% | Global, with APAC leading edge deployments | Medium term (2-4 years) |

| Hyper-scale analytics & Gen-AI adoption | +5.8% | North America and EU core, expanding to APAC | Short term (≤ 2 years) |

| Mandatory data-governance regulations | +3.1% | EU leading, North America following, APAC emerging | Long term (≥ 4 years) |

| Foundation-model-driven metadata enrichment | +2.9% | Global, concentrated in tech hubs | Medium term (2-4 years) |

| Rise of privacy-preserving data clean rooms | +1.8% | Global, with early adoption in BFSI and healthcare | Short term (≤ 2 years) |

| Cloud-native data-fabric services from hyperscalers | +2.3% | North America and EU leading, rapid APAC adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IoT-Linked Data Deluge

Manufacturing plants, connected vehicles, and healthcare wearables now produce terabytes of telemetry every day. Cognitive data management platforms ingest, classify, and flag anomalies in real time, ensuring data is actionable at the edge while remaining governed centrally. Automotive fleets such as Tesla’s generate more than 1.6 petabytes of driving data each month, compelling the cognitive data management market to offer high-throughput pipelines that feed autonomous-driving models.[1]Tesla Inc., “Autopilot Data and Fleet Learning,” tesla.com Local processing at the edge reduces latency, yet cloud orchestration preserves a unified governance layer for compliance and model training.

Hyper-Scale Analytics and Generative-AI Adoption

Large language model programs shorten the data-to-insight cycle by 40-60% when underpinned by intelligent cataloging and quality-assessment engines.[2]Salesforce, “State of Data & Analytics,” salesforce.com Cognitive platforms automate data discovery inside massive lakes, connect to vector stores for retrieval-augmented generation, and maintain complete lineage for model explainability. Automated pipeline optimization lowers computation spending, a key benefit as enterprises train ever-larger models.

Mandatory Data-Governance Regulations

The EU AI Act obliges detailed tracking of training data sources, logic, and outcomes, prompting enterprises to embed automated lineage and audit capabilities. Financial institutions must co-comply with GDPR and new AI rules, while healthcare organizations balance HIPAA with cross-border data-sharing needs. Cognitive data management systems embed policy engines that classify data, restrict residency, and generate real-time compliance dashboards.

Foundation-Model-Driven Metadata Enrichment

Platforms such as IBM watsonx cut metadata creation time by up to 80% through self-supervised models that learn enterprise taxonomies.[3]IBM Corp., “watsonx Data Catalog,” ibm.com Automatic detection of personally identifiable and proprietary content strengthens governance, and domain-tuned models improve discovery in specialized fields like pharmaceuticals. Continuous user feedback loops refine enrichment accuracy, ensuring that catalog quality improves over time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex analytical workflows | -2.8% | Global, particularly affecting legacy enterprise environments | Medium term (2-4 years) |

| Persistent data-security gaps | -1.9% | Global, with heightened concerns in regulated industries | Short term (≤ 2 years) |

| Scarcity of data engineering talent | -2.1% | North America and EU core, emerging impact in APAC | Long term (≥ 4 years) |

| High carbon footprint of AI-grade infra | -1.4% | Global, concentrated in hyperscale deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Complex Analytical Workflows

Enterprises run multi-cloud estates that span AWS, Azure, and Google Cloud, with 76% operating mixed environments.[4]Microsoft, “2025 Multi-Cloud Trends Report,” microsoft.comCognitive data management platforms must orchestrate data movement, enforce consistent policies, and integrate mainframe feeds—all without performance loss. Custom connectors and real-time requirements add cost and lengthen implementation cycles, which dampens immediate growth.

Persistent Data-Security Gaps

Distributed architectures enlarge attack surfaces. AI models often require decrypted data during computation, exposing a potential breach window that traditional encryption approaches cannot close. Third-party models introduce supply-chain vulnerabilities, and the shortage of 200,000 cybersecurity professionals with AI expertise limits enterprises’ ability to harden deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Accelerate Through Implementation Complexity

Solutions accounted for 63.25% of 2025 revenue, reflecting the entrenched adoption of software suites that automate cataloging, lineage, and policy enforcement. Services expand at 24.1% CAGR to 2031 as organizations seek advisory, integration, and managed operations support for advanced AI governance. The cognitive data management market size for services is projected to move in tandem with large digital-transformation programs that lack in-house talent. Professional services dominate today, while managed services show the fastest pick-up in regulated verticals.

Implementation partners help clients embed foundation models, build anonymization frameworks, and connect legacy sources, reducing time-to-value. The talent gap in AI-ready engineering pushes enterprises toward outsourcing, making services pivotal for risk-controlled deployments. Vendors package ongoing model-curation services and compliance reporting into subscription models that promise predictable costs.

By Deployment Type: Cloud Dominance Reflects AI Infrastructure Requirements

Cloud deployments own 60.45% of 2025 spending and grow at 22.6% CAGR because cognitive workloads need elastic GPU farms and low-latency interconnects. The cognitive data management market size for cloud deployment benefits from capex avoidance and access to managed AI services. On-premises remain relevant in defense, healthcare, and banking, yet face slower upgrades and higher hardware outlays.

Hybrid configurations arrive as a pragmatic compromise. Sensitive assets stay inside private data centers, while burst computing and advanced foundation models run in public clouds. Leading providers invest in regional data centers to satisfy residency mandates. Edge extensions process IoT streams locally, then synchronize metadata and insights with central catalogs, ensuring unified governance.

By Industry Vertical: Healthcare Transformation Drives Fastest Growth

The BFSI sector held 26.35% of the cognitive data management market share in 2025, fueled by risk analytics and real-time fraud prevention. Healthcare records a 21.1% CAGR to 2031 as genomic sequencing, clinical imaging, and drug-discovery workflows demand automated stewardship. The cognitive data management industry applies de-identification, consent tracking, and lineage to comply with HIPAA while enabling AI research.

Manufacturing, telecom, and retail also adopt cognitive platforms for predictive maintenance, network optimization, and hyper-personalized commerce. Pharmaceutical firms leverage domain-tuned models to mine unstructured research papers, accelerating molecule discovery. Government agencies use automated classification to satisfy freedom-of-information laws and national security rules.

Geography Analysis

North America accounts for 41.20% of global revenue in 2025, upheld by mature cloud ecosystems, concentrated tech expertise, and aggressive enterprise AI rollouts in BFSI and healthcare. Ongoing investments, such as Snowflake’s USD 200 million AI hub in Silicon Valley, reinforce the region’s innovation leadership. Regulatory certainty and a large skilled workforce support stable growth, though talent shortages persist in specialty AI engineering roles.

APAC exhibits the swiftest trajectory with a 20.85% CAGR through 2031. Japan’s Society 5.0 framework, Singapore’s Smart Nation program, and China’s sovereign-AI agenda accelerate spending on cognitive data management. Local manufacturing digitization and 5G expansion intensify data-volume challenges, and regional governance models spark demand for automated residency controls. India’s IT services sector expands managed offerings that deliver cognitive capabilities worldwide.

Europe grows steadily as GDPR enforcement and the EU AI Act heighten compliance pressures. Enterprises prioritize privacy-preserving analytics using federated learning and differential privacy, which align well with cognitive platforms. Germany leads manufacturing adoption, the UK propels financial services use cases, and Nordic countries integrate sustainability metrics, tracking the carbon footprint of AI infrastructure alongside data governance.

Middle East and Africa and South America represent emerging opportunities. Governments launch digital-economy initiatives, and telcos modernize networks with AI-ready data fabrics. Infrastructure gaps and skills deficits temper near-term growth, yet localized regulations and cloud-region buildouts lay groundwork for future expansion.

Competitive Landscape

The cognitive data management market features moderate fragmentation; no vendor exceeds 15% share. Established providers, IBM, Microsoft, and Oracle, leverage installed bases and broad product suites to add cognitive features. Cloud-native players such as Snowflake and Databricks design architectures optimized for modern workloads, while AI-first startups focus on vector search, automated lineage, and privacy-by-design tooling.

Strategic consolidation intensifies. Salesforce announced a USD 27 billion Informatica takeover to fuse CRM data with AI-powered governance, while IBM bought DataStax for NoSQL and vector search capabilities. Partnerships also proliferate; Snowflake integrates Azure OpenAI Service, bringing state-of-the-art models into its secure environment. Patent filings rose 45% in 2024, centered on automated metadata generation and federated learning. Vendors differentiate on model accuracy, industry compliance packs, and ease of integration rather than price alone.

Managed services emerge as a growth lever. Clients lacking AI talent opt for turnkey operations that bundle software, infrastructure, and governance. Distributors and SI-partners build vertical-focused offerings, healthcare data fabrics, financial-risk hubs, and smart-factory control planes, built atop vendor platforms. Open-source projects gain mindshare for transparent governance frameworks but depend on integrators for enterprise-grade support.

Cognitive Data Management Industry Leaders

IBM Corporation

SAP SE

Salesforce.com, Inc.

SAS Institute Inc.

Informatica Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Snowflake acquired Crunchy Data for USD 250 million to add enterprise-grade PostgreSQL services that support transactional AI applications.

- June 2025: Snowflake unveiled Cortex AISQL and Snowflake Intelligence, embedding natural-language queries and autonomous agents that streamline analytics workflows.

- May 2025: Salesforce agreed to acquire Informatica for USD 27 billion, merging CRM, integration, and AI-driven governance.

- May 2025: IBM completed its DataStax acquisition, bringing NoSQL and vector search into its hybrid-cloud AI stack.

Global Cognitive Data Management Market Report Scope

Cognitive data management refers to the use of cognitive computing to automate manual activities in data management. This helps in reducing the administrative burden imposed by data management and minimize errors. Earlier, data management practitioners used manual processes to analyze the data. These initiatives helped developers and analysts to gain an understanding of their data and have improved their ability to comply with data regulations.

| Solutions |

| Services |

| On-Premises |

| Cloud |

| BFSI |

| Healthcare and Pharmaceuticals |

| IT and Telecommunication |

| Manufacturing |

| Other Verticals |

| North America |

| South America |

| Europe |

| Asia Pacific |

| Middle East and Africa |

| By Component | Solutions |

| Services | |

| By Deployment Type | On-Premises |

| Cloud | |

| By Industry Vertical | BFSI |

| Healthcare and Pharmaceuticals | |

| IT and Telecommunication | |

| Manufacturing | |

| Other Verticals | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

What is driving the rapid growth of the cognitive data management market?

Enterprises face escalating regulatory demands and massive data growth from IoT and generative-AI projects, pushing them to adopt AI-enabled governance platforms that automate classification, lineage, and compliance.

Which component segment is expanding the fastest?

Services are rising at a 24.1% CAGR between 2026 and 2031 as organizations seek expert guidance and managed operations for complex AI data-governance deployments.

Why is healthcare the fastest-growing vertical?

Healthcare data volumes from genomics, imaging, and patient monitoring require de-identification and strict lineage tracking, capabilities that cognitive platforms deliver while supporting AI-driven research, resulting in a 21.1% CAGR.

How significant is cloud deployment in this market?

Cloud captures 60.45% revenue share thanks to elastic GPU resources and managed AI services, and it is forecast to grow at a 22.6% CAGR through 2031.

What regions present the strongest expansion prospects?

APAC leads with a 20.85% CAGR as Japan, Singapore, and China invest in sovereign-AI strategies and digital-industry programs that rely on advanced data-management capabilities.

How fragmented is vendor competition?

No supplier controls more than 15% share; the market holds a concentration score of 5, meaning established firms coexist with agile AI-first entrants that target niche compliance and automation needs.

Page last updated on: