Coconut Sugar Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

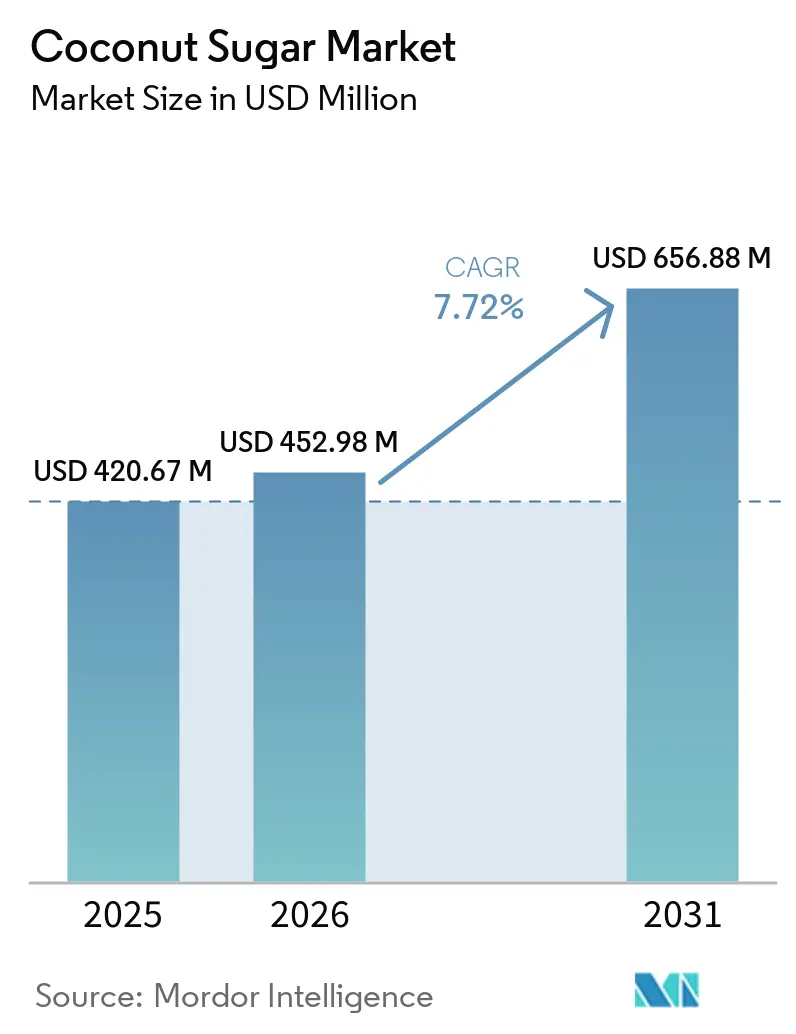

| Market Size (2026) | USD 452.98 Million |

| Market Size (2031) | USD 656.88 Million |

| Growth Rate (2026 - 2031) | 7.72% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coconut Sugar Market Analysis by Mordor Intelligence

The coconut sugar market size was valued at USD 420.67 million in 2025 and estimated to grow from USD 452.98 million in 2026 to reach USD 656.88 million by 2031, at a CAGR of 7.72% during the forecast period (2026-2031). Rising demand for natural, low-glycemic sweeteners, functional beverage launches showcasing mineral-rich coconut nectar, and advances in low-moisture powder formats collectively propel the coconut sugar market. Indonesia continues to supply about 90% of global output, yet this geographic concentration magnifies climate-related risk. Certification has become a strategic necessity as European and North American retailers insist on USDA Organic, Fair for Life, and Non-GMO verification. Meanwhile, processors that invest in spray-drying or vacuum-evaporation equipment are winning contracts with meal-replacement, confectionery, and instant beverage brands that value fast solubility.

Key Report Takeaways

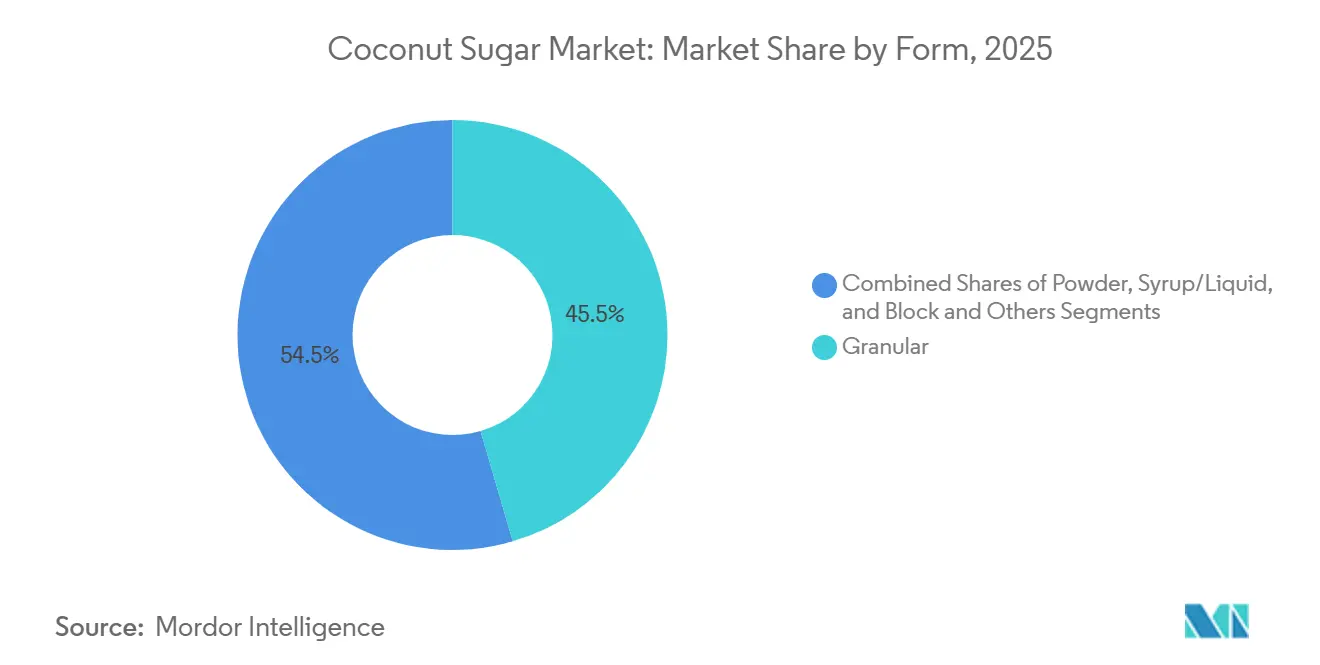

- By form segment, granular forms led with 45.47% of the coconut sugar market share in 2025, while powder formats will expand at a CAGR of 8.25% through 2031.

- By category segment, conventional products captured 53.36% of the coconut sugar market in 2025; organic variants will grow at a CAGR of 9.14% through 2031.

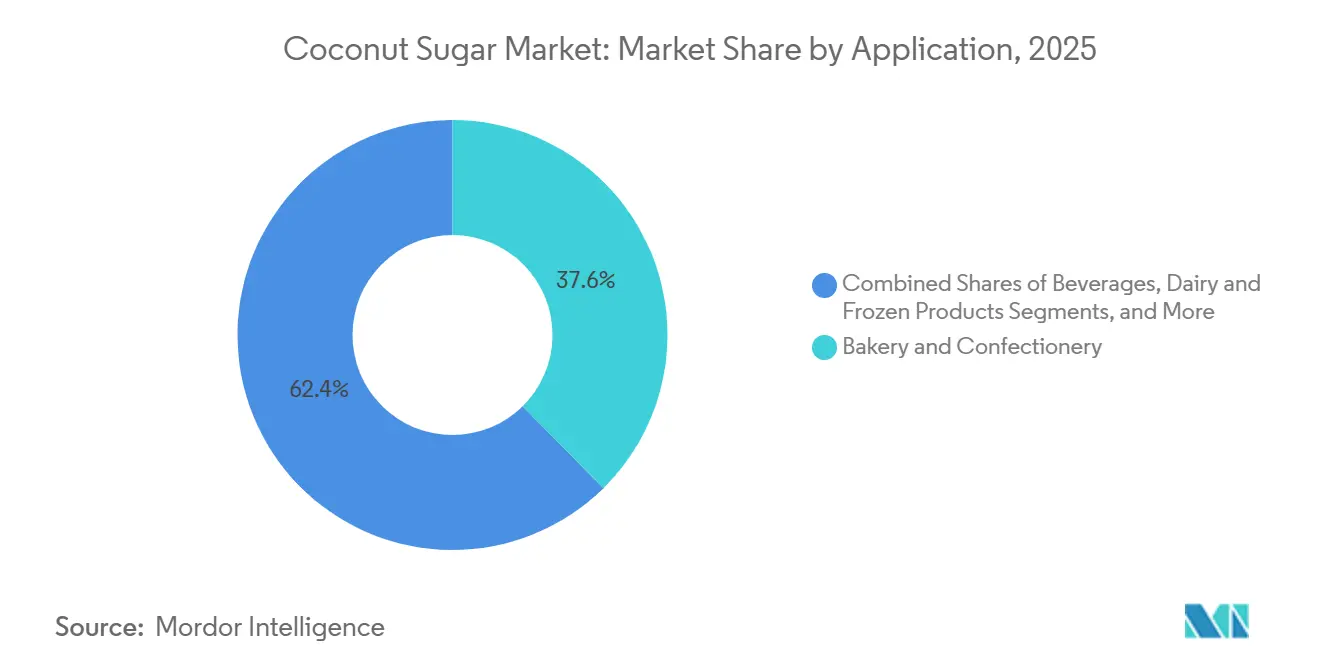

- By application segment, bakery and confectionery accounted for 37.62% of demand in 2025, yet beverages will advance at a CAGR of 8.46% through 2031.

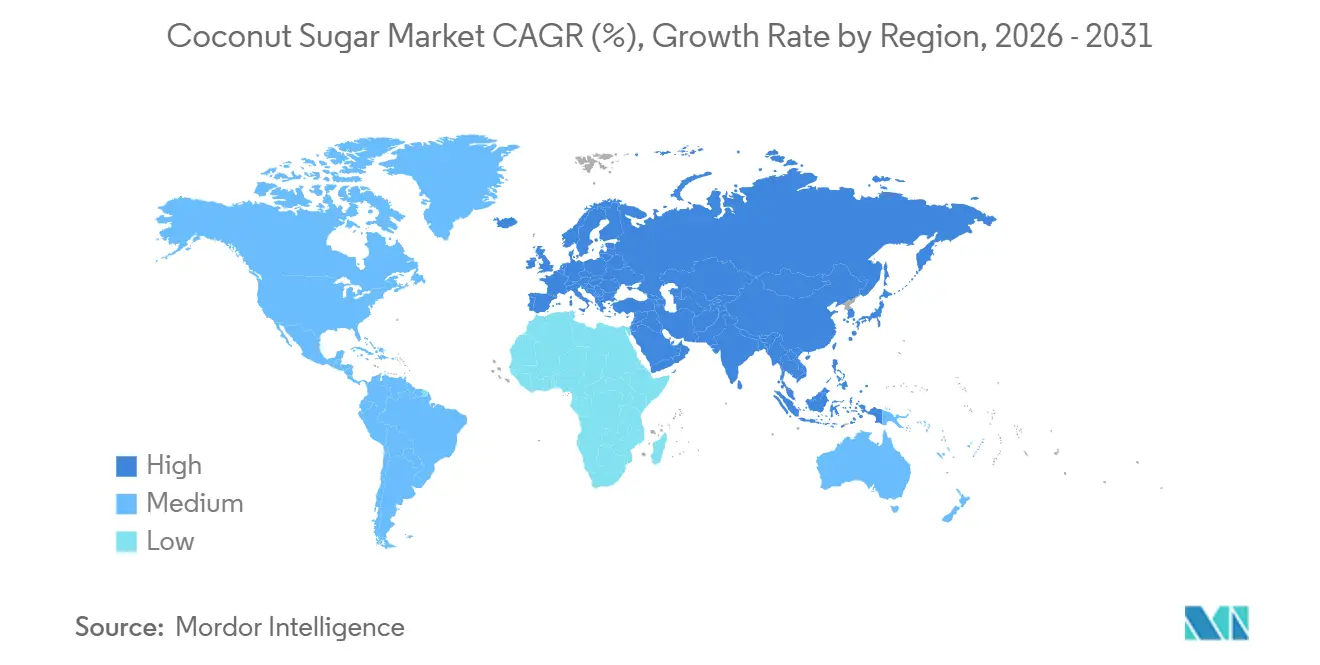

- By geography segment, Asia-Pacific commanded 52.74% of the 2025 value, whereas Europe will log the fastest regional growth at a CAGR of 8.37% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coconut Sugar Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Natural Low-GI Sweeteners | +1.8% | North America, Europe | Medium term (2-4 years) |

| Expansion of Functional Beverages Using Traditional Sweeteners | +1.5% | North America, Asia-Pacific | Short term (≤ 2 years) |

| Product Innovation in Low-Moisture Powder Formats | +1.2% | North America, Europe | Medium term (2-4 years) |

| Growing Demand for Mild-Flavored Alternative Sweeteners | +1.0% | North America, Western Europe | Long term (≥ 4 years) |

| Application in Natural Personal Care and Cosmetics | +0.8% | Europe, North America | Long term (≥ 4 years) |

| Demand for Non-GMO Verified Sweeteners | +0.9% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for natural low-GI sweeteners

Coconut sugar's glycemic index of 35-54 positions it below cane sugar's 60-65 range, a differential that resonates with diabetic and pre-diabetic consumers seeking postprandial glucose moderation without artificial sweeteners. The FDA's food composition database includes coconut sugar as a natural sweetener requiring no GRAS determination, streamlining formulation for U.S. food manufacturers, while the Philippines' PNS/BAFPS 22:2013 standard codifies quality parameters, including moisture content below 3% and sucrose purity thresholds[1]Source: U.S. Food and Drug Administration, “Food Data Central—Coconut Sugar,” FDA.GOV. Peer-reviewed studies confirm coconut sugar retains trace minerals, potassium, magnesium, zinc, and iron, at levels 10-100 times higher than refined cane sugar, though absolute quantities remain nutritionally modest at typical serving sizes. The Non-GMO Project verified 1,200+ coconut sugar products in 2024, a 22% increase from 2023, reflecting retailer mandates for clean-label positioning as consumers conflate GMO-free claims with broader health attributes despite coconut palms' non-GMO status by botanical definition. This driver's 1.8 percentage-point contribution to CAGR is most pronounced in North America and Europe, where premium pricing for low-GI sweeteners sustains margins 40-60% above those of conventional cane sugar, yet adoption in Asia-Pacific remains constrained by price sensitivity and entrenched cane sugar use in traditional confectionery.

Expansion of functional beverages using traditional sweeteners

Functional beverage formulators increasingly substitute coconut flower nectar and coconut sugar for cane syrups to achieve mineral fortification and lower fructose levels without synthetic additives, a trend exemplified by CocoGen's August 2025 Singapore launch of functional coconut water variants that deliver 25% more electrolytes and magnesium via coconut sugar infusion. CÓCOES SLOW's carbonated beverages using coconut flower nectar as the primary sweetener entered European markets in 2025, targeting consumers seeking "swicy" (sweet-spicy) flavor profiles, a segment that NCSolutions' May 2024 survey of 1,114 U.S. adults found 74% eager to trial. Big Tree Farms' vacuum-evaporated coconut nectar (VECN) technology, commercialized in 2022, reduces moisture content by 30% and minimizes caramelization, enabling instant beverage and meal-replacement brands to achieve 1:1 cane sugar substitution without reformulation. This driver contributes 1.5 percentage points to CAGR, with short-term impact concentrated in North America and Asia-Pacific urban centers where functional beverage penetration exceeds 15% of total beverage sales, yet scalability hinges on securing a stable organic coconut sugar supply as European buyers increasingly mandate Fair for Life certification.

Product innovation in low-moisture, free-flowing powder formats

Spray-drying technology incorporating resistant dextrin (NUTRIOSE®) as a glass-forming agent achieves a glass transition temperature of 137.53°C, solving the moisture-caking challenges that previously limited coconut sugar powder's shelf stability in humid climates. Vacuum drying at 70°C for 56 hours produces amorphous powder with faster dissolution rates than granular formats, enabling instant beverage and confectionery applications where solubility benchmarks demand 90% dissolution within 30 seconds. Fluidized bed agglomeration further improves instant properties by creating porous particle structures with increased surface area, a process adopted by Indonesian processors targeting B2B channels in North America and Europe, where meal-replacement and protein powder brands require free-flowing sweeteners compatible with automated filling lines. This innovation cluster contributes 1.2 percentage points to CAGR, with medium-term impact as powder formats command 15-25% price premiums over granular variants yet require capital investments of USD 500,000-1.5 million for spray-drying infrastructure, a barrier for smallholder cooperatives that dominate Indonesian production. The adoption trajectory will depend on whether regional processors can access concessional financing or form joint ventures with multinational ingredient suppliers seeking to diversify beyond cane-derived maltodextrin.

Growing demand for mild-flavored alternative sweeteners

Coconut sugar's caramel and toffee notes, while valued in bakery applications, limit its utility in neutral-flavored formulations such as dairy alternatives and nutraceutical tablets, driving demand for mild-flavored variants produced via controlled crystallization and pH stabilization. Processors in Central Java are experimenting with mineral management and time-temperature-Brix optimization to reduce browning during evaporation, achieving lighter color profiles (L* values above 55 versus 40-45 for traditional coconut sugar) that expand application scope into white chocolate and yogurt formulations. Big Tree Farms' Organic Golden Coconut Sugar, launched in 2025, targets this segment by sourcing sap from younger flower buds with lower polyphenol content, though yields are 15-20% lower than mature-bud tapping. This driver adds 1.0 percentage point to CAGR over the long term, as mild-flavored variants remain niche (estimated 8-12% of total coconut sugar volume in 2025) but command 20-30% price premiums in European organic channels where formulators seek clean-label alternatives to decolorized cane sugar. Scaling mild-flavored production requires agronomic research into bud-stage optimization and post-harvest enzymatic treatments, areas where the Philippines' Bureau of Agricultural Research and Indonesia's Ministry of Agriculture have initiated pilot programs but lack the funding to reach commercial scale.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Yield Efficiency Compared to Cane Sugar Production | -0.6% | Global, most acute in Indonesia and Philippines production zones | Long term (≥ 4 years) |

| High Production Cost and Price Volatility | -0.8% | Global, with pronounced effects in Asia-Pacific origin markets | Short term (≤ 2 years) |

| Long Production Cycle from Sap Collection to Crystallization | -0.4% | Indonesia, Philippines, Thailand, and other origin countries | Medium term (2-4 years) |

| Adulteration/Contamination Supply-Chain Risk | -0.5% | Global, concentrated in unregulated export channels from Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited yield efficiency compared to cane sugar production

Coconut palms yield 1.5-2 times the sugar per acre of cane yet require labor-intensive daily tapping and rapid processing, creating a structural productivity gap that limits supply elasticity. The Philippines Coconut Authority's sequential coconut tapping for nipa palm (SCTNP) program generates approximately PHP 71,000 per hectare annually, compared with PHP 7,500 for nut-only production, but tapper availability constrains expansion as aging demographics and youth disinterest reduce the active workforce. Banyumas district registered only 6,699 of its 22,000 palm tappers with the state insurer BPJS Ketenagakerjaan as of mid-2025, reflecting the prevalence of informal labor and safety concerns[2]Source: ANTARA News Desk, “Sweeting the World: Inside Banyumas' Global Coconut Sugar Ambition,” ANTARANEWS.COM. India's CPCRI study of WCT coconut varieties recorded 960 ml sap per palm per day, translating to 96-144 kg sugar per hectare annually at 11-15% sugar content, compared to 6,000-8,000 kg per hectare for cane sugar in optimal conditions. This -0.6 percentage-point drag on CAGR persists over the long term unless dwarf coconut varieties, which enable tappers to service 100 trees daily versus 25 for tall palms, achieve commercial scale, a transition requiring 5-7 years for new plantings to reach productive maturity and capital investments exceeding USD 3,000 per hectare for seedlings and infrastructure.

High production cost and price volatility

Coconut sugar production costs in Indonesia's Banyumas region range from USD 1.80-2.50 per kg, driven by labor-intensive sap collection (40-50% of total cost), firewood for evaporation (15-20%), and packaging (10-15%), yet European retail prices of EUR 15-27 per kg (USD 16-29) reflect 6-10x markups that squeeze mid-chain processors and limit mass-market penetration. Wholesale prices in the U.S. fluctuate between USD 300-650 per MT for blended products, though pure organic coconut sugar commands USD 4,000-6,000 per MT FOB Indonesia, a volatility driven by seasonal sap flow variations (yields drop 30-40% during dry months), currency fluctuations (IDR depreciation of 8-12% annually against USD since 2020), and competing demand for coconuts in copra and desiccated coconut markets. This -0.8 percentage-point impact on CAGR is most acute in the short term as 2025-2026 organic coconut sugar supply tightness, cited by multiple European importers, pushes spot prices 15-25% above contract levels, eroding margins for confectionery and beverage brands that lack long-term supply agreements. Tradin Organic's research into alternative cooking stoves aims to reduce fuel costs by 30-40% and cut respiratory health impacts, yet adoption requires upfront investments of USD 150-300 per tapper household, a barrier without subsidized financing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Formats Gain Traction via Solubility Breakthroughs

Granular coconut sugar commanded 45.47% of market value in 2025, favored for its direct substitutability for cane sugar in bakery and confectionery applications where caramel notes enhance flavor profiles, yet powder formats are expanding at 8.25% CAGR through 2031 as spray-drying technology incorporating resistant dextrin achieves glass-transition temperatures above 137°C, solving moisture-caking challenges that previously limited shelf stability in humid climates. Vacuum drying at 70°C for 56 hours produces an amorphous powder that dissolves 90% within 30 seconds, meeting instant beverage and meal-replacement benchmarks, whereas granular formats require 2-3 minutes of stirring. Syrup and liquid formats are concentrated in foodservice channels, where bulk handling and pumping systems favor liquid sweeteners; however, viscosity variations (3,000-8,000 cP at 25°C, depending on Brix) complicate standardization across suppliers. Block and other formats (compressed tablets, single-serve sachets) predominantly in Southeast Asian retail, where traditional cooking methods favor solid sweeteners that can be grated or dissolved incrementally.

The powder segment's acceleration reflects Big Tree Farms' 2022 commercialization of vacuum-evaporated coconut nectar (VECN) with 30% lower moisture content and reduced caramelization, enabling chocolate and confectionery brands to achieve 1:1 cane sugar substitution without reformulation. Fluidized bed agglomeration, adopted by Indonesian processors targeting North American B2B channels, creates porous particle structures with increased surface area that improve flowability in automated filling lines, a critical requirement for protein powder and nutraceutical manufacturers where segregation and clumping trigger batch rejections. Syrup formats face headwinds from cold-chain requirements and shorter shelf life (6-9 months versus 18-24 months for powder and granular), limiting export viability to markets within 3-4 weeks shipping time from Indonesia or the Philippines. Granular formats retain dominance in bakery applications due to their moisture-retention properties and Maillard reaction contributions during baking, yet the segment's 4-5% CAGR lags overall market growth as formulators increasingly prioritize instant solubility and neutral flavor profiles achievable only with advanced powder processing.

By Category: Organic Variants Surge on Certification Mandates

Conventional coconut sugar held 53.36% of market value in 2025, reflecting price sensitivity in Asia-Pacific domestic markets and foodservice channels where organic premiums of 40-60% exceed willingness-to-pay thresholds, yet organic variants are accelerating at 9.14% CAGR through 2031 as European and North American retailers mandate USDA Organic and Fair for Life certifications for shelf placement. Big Tree Farms' January 2026 commitment to expand its certified farmer network from 17,000 to 25,000 smallholders and increase sustainably managed land from 1,400 hectares to 6,000 hectares signals that certification is transitioning from a differentiation tool to a baseline requirement for export channels[3]Source: Press Office, “Mirova Invests USD 10 Million in Big Tree Farms,” MIROVA.COM. European organic coconut sugar sales grew in 2024-2025, outpacing the broader organic food market's annual growth, as consumers conflate organic certification with broader sustainability attributes, including carbon footprint and farmer welfare. Conventional formats remain dominant in Indonesia's domestic market, where coconut sugar retails at IDR 15,000-25,000 per kg (USD 1.00-1.65) versus IDR 35,000-50,000 (USD 2.30-3.30) for organic variants, a premium that limits penetration beyond urban middle-class households.

The organic segment's momentum is reinforced by Tradin Organic's three-year grant project targeting 2,275 smallholder farmers in Central Java with interventions including alternative cooking stoves, carbon insetting to valorize emission reductions, and dwarf coconut feasibility studies. Certification costs of USD 2,000-5,000 annually for Non-GMO Project verification plus 0.5-1.5% of sales for organic certification favor larger exporters over smallholder cooperatives, potentially accelerating consolidation as evidenced by CBL Group's USD 25 million acquisition of PT TJT Indonesia to secure certified supply for European markets. The Philippines Coconut Authority's partnership with the Sustainable Coconut Roundtable in 2024 aims to streamline group certification for smallholders, though uptake remains below 15% of eligible producers due to documentation burdens and three-year transition periods required for organic certification. Conventional coconut sugar reflects steady demand growth in Asia-Pacific foodservice and industrial channels, yet the segment faces margin pressure as European buyers increasingly reject non-certified supply, forcing conventional producers to either invest in certification or accept lower-value spot-market sales.

By Application: Beverages Outpace Bakery via Functional Innovation

Bakery and confectionery applications commanded 37.62% of coconut sugar demand in 2025, leveraging the sweetener's moisture-retention properties and Maillard reaction contributions that enhance browning and flavor development in cookies, cakes, and chocolate, yet beverages are expanding at 8.46% CAGR through 2031 as functional drink formulators substitute coconut flower nectar for cane syrups to achieve lower fructose profiles and mineral fortification without synthetic additives. CocoGen's August 2025 Singapore launch of functional coconut water variants delivering 25% more electrolytes and magnesium via coconut sugar infusion exemplifies this shift, as does CÓCOES SLOW's carbonated beverages using coconut flower nectar to target "swicy" flavor preferences, a segment that NCSolutions' May 2024 survey found 74% of U.S. adults eager to trial. Dairy and frozen desserts concentrated in coconut milk ice cream and yogurt alternatives, where coconut sugar's caramel notes complement coconut fat's creamy mouthfeel, though formulation challenges around ice crystal formation and syneresis limit penetration in premium frozen novelties.

Nutraceuticals and supplements are primarily used as tablet binders and syrup bases, where coconut sugar's trace mineral content supports "whole food" positioning, yet the segment lags beverages due to competition from monk fruit and stevia in zero-calorie formulations. Personal care and cosmetics represented a nascent application driven by coconut shell extract patents (EP3429695A1, US10980736B2) describing anti-glycation and skin-lightening properties, though commercialization remains limited to fewer than 50 SKUs globally as of 2025. Big Tree Farms' October 2025 launch of Naughty Bali BBQ sauces at Sprouts and Publix, formulated with organic coconut sugar, coconut aminos, and coconut vinegar, signals diversification into savory condiments, a category where coconut sugar's caramel notes and lower glycemic index differentiate against cane-sweetened competitors. Bakery application reflects steady demand growth in artisan and gluten-free segments, yet the category faces headwinds from erythritol and allulose adoption in low-carb baking mixes where coconut sugar's 4 grams carbohydrate per teaspoon exceeds keto diet thresholds.

Geography Analysis

Asia-Pacific commanded 52.74% of the global coconut sugar market value in 2025 and is forecast to grow at 7.2% CAGR through 2031, underpinned by Indonesia's dominance as the source of approximately 90% of the global supply and the Philippines' 100 million coconut planting target by 2028, aimed at expanding value-added processing capacity. Indonesia's Banyumas region produces roughly 80% of the country's coconut sugar output, with major coconut-producing provinces including Riau, North Sulawesi, and East Java. However, smallholder production creates traceability and quality-control challenges that favor vertically integrated exporters. December 2025 export data from Indonesia recorded shipments of 1.054 million kg of coconut sap sugar, with China, Malaysia, Thailand, and the Netherlands as the primary destinations. The Philippines' Northern Mindanao region, with over 304,000 hectares and 32 million bearing trees, is positioning itself as a secondary supply hub, though PCA-registered processors currently produce only approximately 4,000 MT annually, a fraction of Indonesia's estimated 140,000-160,000 MT output.

Europe is expanding at 8.37% CAGR through 2031, the fastest regional growth rate, driven by organic certification mandates and Non-GMO Project verification requirements that command 40-60% price premiums over conventional cane sugar in premium retail channels. European organic coconut sugar sales grew in 2024-2025, outpacing the broader organic food market, as Netherlands, Germany, and France emerge as primary import hubs leveraging Rotterdam and Hamburg port infrastructure for re-export to smaller EU markets. The region's market size in 2025 reflects nascent penetration, yet the trajectory is supported by EU Novel Foods framework clarity and Eurostat HS 17029 trade data showing coconut sugar import volumes rising. CBL Group's January 2026 acquisition of PT TJT Indonesia for over USD 25 million, backed by the International Finance Corporation, explicitly targets European market expansion by leveraging Indonesia's trade agreements and the acquired facility's existing certifications.

North America characterized by vertically integrated importers such as Big Tree Farms (sourcing from 17,000 Indonesian smallholders) and Nutiva (USDA Organic and Non-GMO Project Verified supply) that control supply chains from farm-gate to retail shelf. The region's growth is constrained by competition from monk fruit, allulose, and erythritol in zero-calorie formulations, yet functional beverage innovation and clean-label mandates sustain demand for coconut sugar in premium natural products channels including Whole Foods, Sprouts, and Publix. Big Tree Farms' October 2025 national launch of Naughty Bali BBQ sauces at Sprouts and Publix signals retail channel expansion beyond sweetener aisles into condiments, leveraging consumer research showing majority of U.S. adults prioritize clean-label attributes. South America and Middle East and Africa reflects a limited supply-chain infrastructure and price sensitivity that favors conventional cane sugar, though niche organic retailers in São Paulo, Dubai, and Johannesburg are beginning to stock coconut sugar as part of broader natural sweetener assortments.

Competitive Landscape

The coconut sugar market exhibits moderate fragmentation, reflecting a competitive structure where regional processors in Java and Mindanao compete alongside vertically integrated exporters such as Big Tree Farms, Coco Sugar Indonesia, The Coconut Company Ltd., Nutiva, and Madhava Natural Sweeteners, yet consolidation pressure is mounting as evidenced by CBL Group's USD 25 million acquisition of PT TJT Indonesia in January 2026 and Century Pacific's USD 45 million purchase of a South Cotabato coconut processing plant in December 2025. Strategy patterns bifurcate between cost leadership, pursued by Indonesian processors leveraging smallholder networks and open-fire evaporation to achieve FOB prices of USD 1.80-2.50 per kg, and differentiation via organic certification, Fair for Life verification, and Regeneratively Organic Certified (ROC) labeling that command 40-60% premiums in North American and European retail channels.

White-space opportunities include mild-flavored variants for neutral applications (dairy alternatives, nutraceutical tablets), personal care formulations leveraging coconut shell polyphenol extracts, and powder formats optimized for instant solubility in meal-replacement and protein powder applications, segments where incumbents have limited presence and barriers to entry remain surmountable for processors willing to invest in spray-drying or vacuum-evaporation infrastructure. Emerging disruptors include Sri Lankan engineering firm ISF, which partnered with Indonesia's NICO COCO in October 2024 to design AI-driven coconut processing plants incorporating real-time management information systems, productivity improvement algorithms, and energy-efficient evaporators that could reduce processing costs 20-30% versus traditional open-fire methods.

Technology adoption for competitive advantage is exemplified by Big Tree Farms' vacuum-evaporated coconut nectar (VECN) technology, commercialized in 2022, which delivers 30% lower moisture content and reduced caramelization, enabling 1:1 cane sugar substitution in chocolate and instant beverage applications where traditional granular formats previously failed solubility benchmarks. Blockchain traceability systems, piloted by Big Tree Farms and Tradin Organic, address adulteration risks by enabling batch-level isotope testing and farmer-to-consumer transparency, a capability increasingly demanded by European organic certifiers and North American retailers following isotope analysis revelations that 17-38% of commercial samples contain C4 cane sugar additions. The competitive landscape is further shaped by the International Finance Corporation's support for cross-border M&A, as seen in CBL Group's acquisition, signaling that access to concessional financing and trade-agreement leverage will determine which players can scale certified supply chains to meet European and North American demand growth.

Coconut Sugar Industry Leaders

Big Tree Farms

Coco Sugar Indonesia

The Coconut Company Ltd.

Nutiva Inc.

Madhava Natural Sweeteners

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mirova, an affiliate of Natixis Investment Managers, invested USD 10 million in Big Tree Farms to expand the company's smallholder farmer network from 17,000 to 25,000, double production capacity, and increase sustainably managed land from 1,400 hectares to 6,000 hectares by the end of the investment period.

- January 2026: CBL Group, a Sri Lankan diversified food manufacturer, acquired PT Tri Jaya Tangguh Indonesia (TJT), a large Indonesian coconut processing facility employing over 800 people, for over USD 25 million, with support from the International Finance Corporation, aiming to expand capacity.

- December 2025: Century Pacific Food Inc., via wholly-owned subsidiary Coco Harvest Inc., acquired a 2.2-hectare coconut processing plant in South Cotabato, Mindanao, from Roxas Sigma Agriventures for USD 45 million.

Global Coconut Sugar Market Report Scope

Coconut sugar is a natural sweetener derived from the sap of coconut palm flowers, valued for its caramel-like flavor and minimal processing. The coconut sugar market is segmented by form, category, application, and geography. By form, the market includes powder, granular, syrup/liquid, block, and other forms. By category, the market is divided into organic and conventional products. Based on application, the market covers bakery and confectionery, beverages (including craft), dairy and frozen desserts, nutraceuticals and supplements, personal care and cosmetics, and other uses. By geography, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market size and forecasts provided for each region. For each segment, market sizing and forecasts have been conducted on a value basis (USD million).

| Powder |

| Granular |

| Syrup/Liquid |

| Block and Others |

| Organic |

| Conventional |

| Bakery and Confectionery |

| Beverages (incl. craft) |

| Dairy and Frozen Desserts |

| Nutraceuticals and Supplements |

| Personal Care and Cosmetics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Form | Powder | |

| Granular | ||

| Syrup/Liquid | ||

| Block and Others | ||

| By Category | Organic | |

| Conventional | ||

| By Application | Bakery and Confectionery | |

| Beverages (incl. craft) | ||

| Dairy and Frozen Desserts | ||

| Nutraceuticals and Supplements | ||

| Personal Care and Cosmetics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the coconut sugar market by 2031?

The coconut sugar market size is forecast to reach USD 656.58 million by 2031, expanding at a 7.72% CAGR.

Which form will grow fastest through 2031?

Powder formats should post the quickest rise at an 8.25% CAGR as spray-drying eliminates caking and speeds dissolution.

Why are organic variants gaining ground?

Retailers in Europe and North America demand USDA Organic and Fair for Life seals, pushing organic volume at a 9.14% CAGR while premiums protect margins.

Which region shows the highest growth rate?

Europe is set to lead regional growth with an 8.37% CAGR, driven by certification requirements and clean-label preferences.

Page last updated on: