Coconut Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

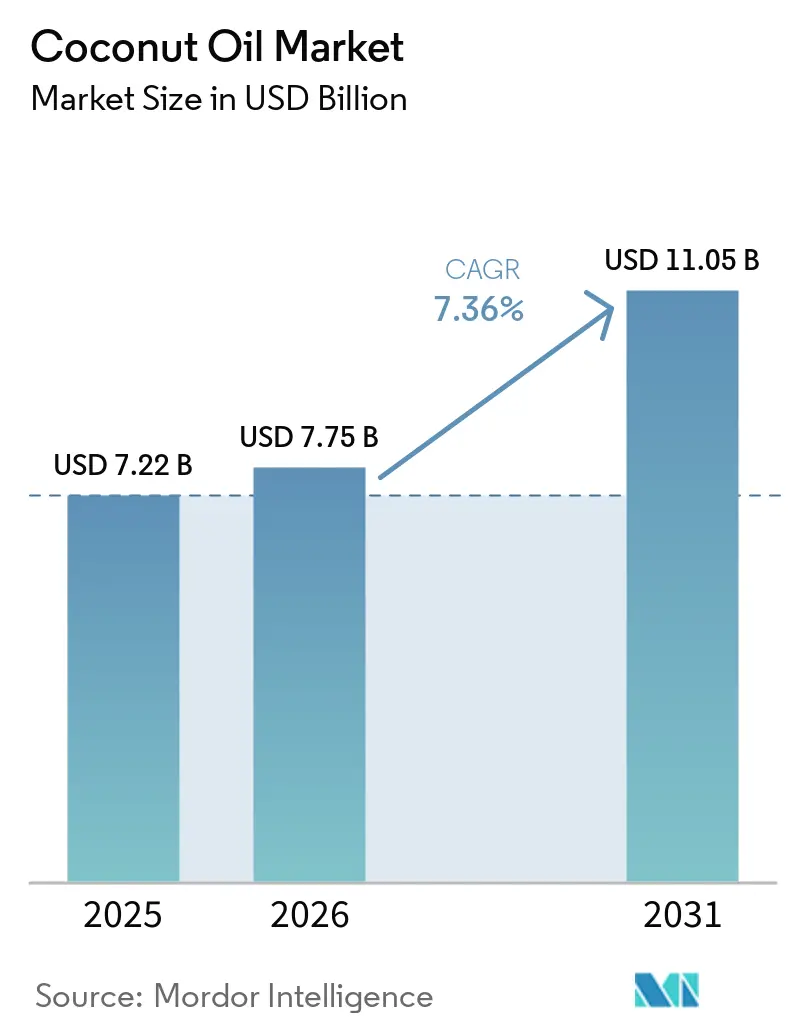

| Market Size (2026) | USD 7.75 Billion |

| Market Size (2031) | USD 11.05 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Coconut Oil Market Analysis by Mordor Intelligence

The coconut oil market size was valued at USD 7.22 billion in 2025 and estimated to grow from USD 7.75 billion in 2026 to reach USD 11.05 billion by 2031, at a CAGR of 7.36% during the forecast period (2026-2031). Heightened demand in the coconut oil market for clean-label fats in packaged foods, accelerating use as a pharmaceutical excipient, and premium personal-care launches that leverage lauric acid’s antimicrobial profile anchor this expansion. Moreover, government initiatives in the coconut oil industry in the Philippines and Indonesia are designed to stabilize raw-material availability, while organic certification mandates from North American and European retailers are reshaping procurement strategies. Competitive intensity in the coconut oil market stays moderate as multinational processors vie with vertically integrated Asian exporters and specialty organic brands for channel influence and pricing power.

Key Report Takeaways

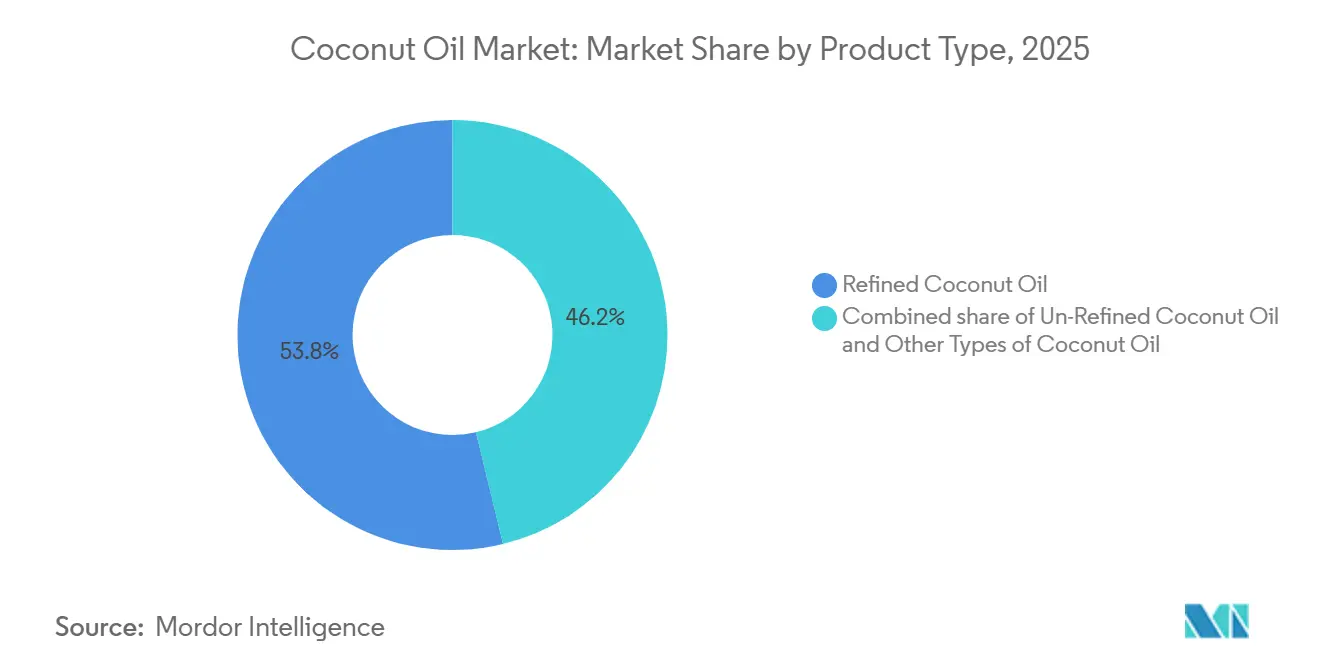

- By product type, refined grades held 53.78% of the coconut oil market share in 2025, while un-refined variants are advancing at an 8.31% CAGR through 2031.

- By nature, conventional production captured 74.16% of the coconut oil market size in 2025, whereas organic grades are expanding at an 8.42% CAGR through 2031.

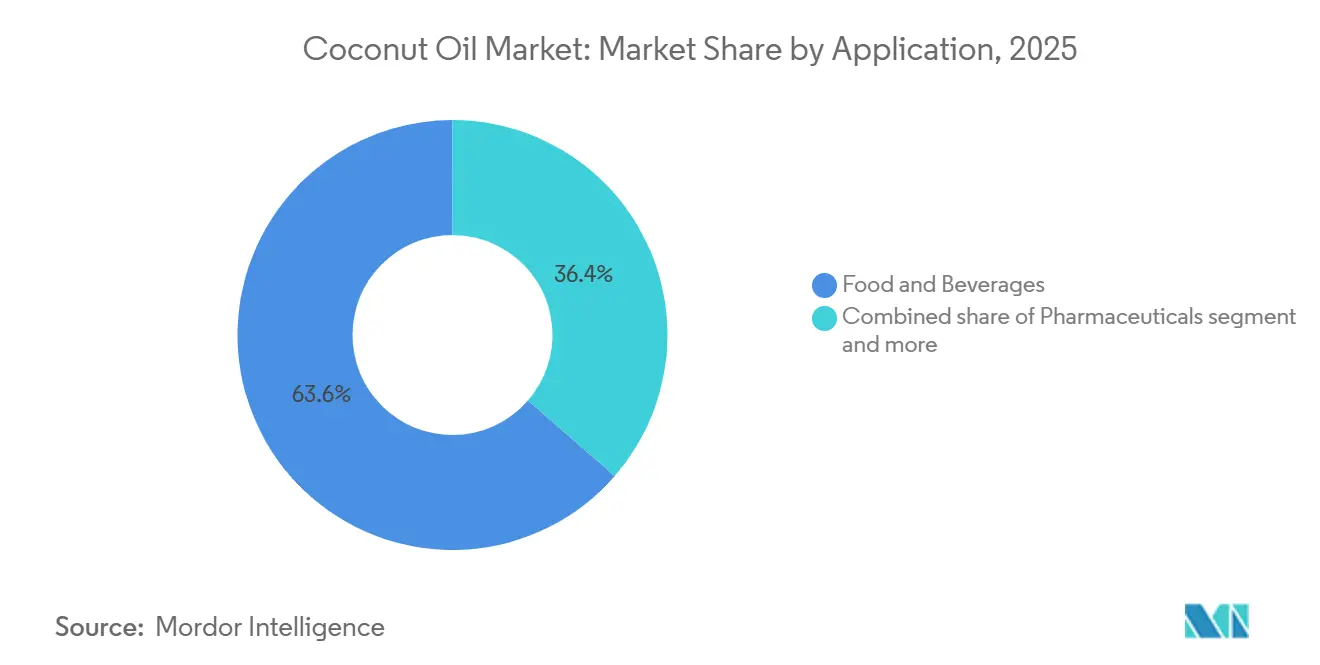

- By application, food and beverages accounted for 63.62% of demand in 2025, and cosmetics and personal care are growing at a 7.75% CAGR to 2031.

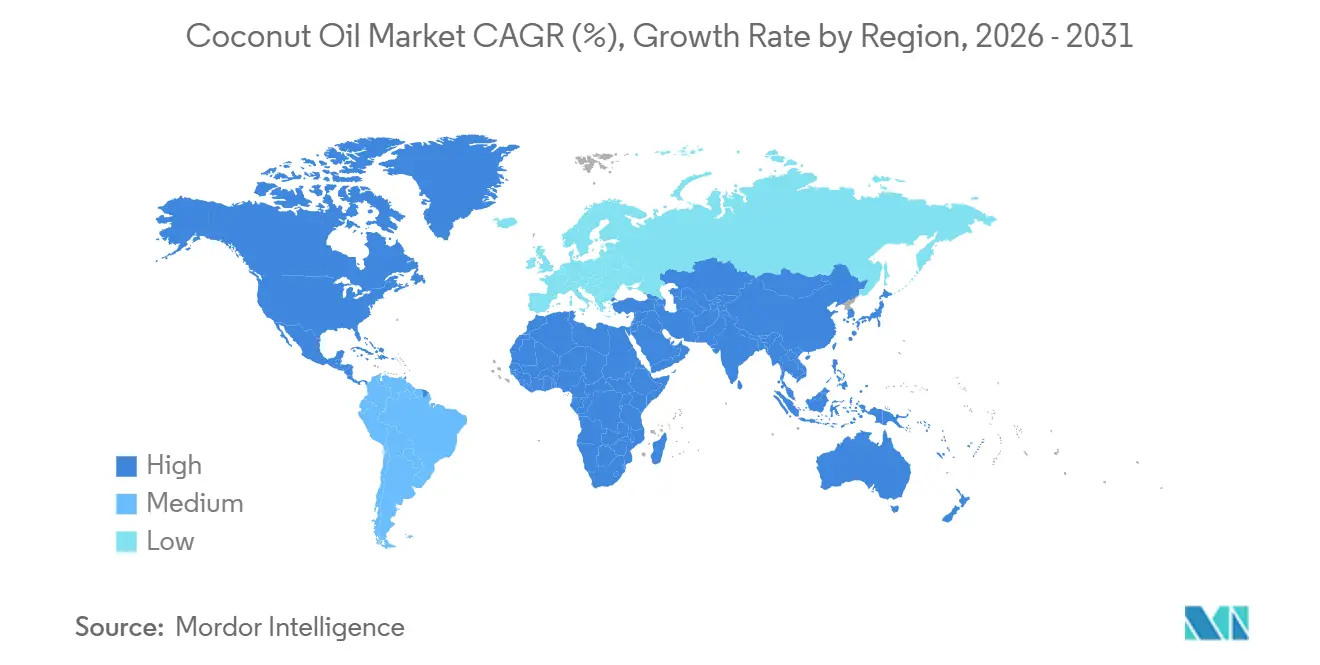

- By geography, Asia-Pacific commanded 74.24% of global volume in 2025, and North America leads growth with an 8.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coconut Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for clean-label and natural cooking oils in household and foodservice applications | +1.8% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific markets | Medium term (2-4 years) |

| Growing awareness of the health benefits associated with coconut oil driving market growth | +1.5% | Global, particularly North America, Europe, and health-conscious segments in Asia-Pacific | Long term (≥ 4 years) |

| Expansion in product offerings, such as virgin, cold-pressed, and infused coconut oils, attracting diverse consumer groups | +1.2% | North America, Europe, and premium retail channels in Asia-Pacific | Medium term (2-4 years) |

| Government initiatives supporting coconut cultivation and exports in major producing countries | +1.0% | Asia-Pacific core (Philippines, Indonesia, India, Sri Lanka), with export spillover to global markets | Long term (≥ 4 years) |

| Increased use in cosmetics and personal care products due to its moisturizing and nourishing properties | +0.9% | Global, with early adoption in North America and Europe, expanding to Asia-Pacific and Middle East | Short term (≤ 2 years) |

| Expanding industrial applications, including biofuels and lubricants | +0.6% | Asia-Pacific and select biofuel-mandate markets in Europe and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for clean-label and natural cooking oils in household and foodservice applications

In the coconut oil market, consumer demand for clean-label and natural cooking oils in household and foodservice applications is being driven by a preference for transparency, sustainability, and health-conscious formulations. A 2025 survey by the National Sanitation Foundation (NSF) revealed that 82% of consumers seek detailed processing information, 80% prioritize clearer allergen disclosure, and 83% actively read food labels before purchasing, emphasizing the critical role of label integrity in purchasing decisions [1]Source: National Sanitation Foundation (NSF), "NSF Research Shows Americans Demand Greater Clarity and Standardization in Food Labeling," nsf.org. This trend within the coconut oil market is prompting manufacturers and foodservice operators to transition from refined or synthetic oils to natural, minimally processed alternatives such as cold-pressed coconut oil. Companies like Cargill and AarhusKarlshamn (AAK) are addressing this demand by offering refined and fractionated coconut oils that align with clean-label standards, meeting both performance requirements and consumer expectations. These industrial players are reformulating oils to reduce chemical processing while maintaining essential stability and functionality for applications such as frying, baking, and product formulation. This shift reflects the broader clean-label movement, where simplicity in ingredients intersects with ethical sourcing and sustainability goals, enhancing brand credibility. In the global market, natural oil processors in the coconut oil industry are focusing on traceable supply chains and minimizing refining processes to meet these evolving standards. The combined impact of consumer demand for ingredient transparency and industry adaptation toward cleaner, natural oils is redefining quality benchmarks and driving innovation in the cooking oil industry, positioning it to meet future expectations for health, sustainability, and ethical practices.

Growing awareness of the health benefits associated with coconut oil driving market growth

The increasing recognition of the health benefits in the coconut oil market, particularly its medium-chain triglycerides (MCTs) that make up approximately 60% of its fatty acid profile, is driving its adoption across various industries. MCTs facilitate hepatic oxidation without requiring carnitine transport, a metabolic pathway distinct from long-chain saturated fats, which enhances their value as a functional food ingredient. In the coconut oil market, this unique profile has enabled its application in diverse areas, including pharmaceuticals, as evidenced by a 2024 peer-reviewed study. The study highlighted that coconut oil-based self-nanoemulsifying drug delivery systems not only improved dissolution but also mitigated the ulcerogenic side effects of nonsteroidal anti-inflammatory drugs, thereby extending their utility beyond nutrition.[2]Source: National Library of Medicine, "Coconut Oil Based Self-Nano Emulsifying Delivery Systems Mitigate Ulcerogenic NSAIDS Side Effect and Enhance Drug Dissolution: Formula Optimization, In-vitro, and In-vivo Assessments," pubmed.ncbi.nlm.nih.gov Industrial suppliers such as Wilmar International are capitalizing on this MCT-rich composition by producing bulk fractionated coconut oil for functional food formulations and nutraceutical blends, ensuring product stability while meeting the rising health-driven demand. The synergy between rapid metabolism and therapeutic potential has reinforced coconut oil’s role in plant-based diets and wellness products, driving innovation in delivery systems that align metabolic benefits with pharmaceutical advancements. Across foodservice and industrial sectors, brands are prioritizing MCT potency for applications such as sustained energy and anti-inflammatory benefits. The distinct oxidation pathway of MCTs complements findings on bioavailability, positioning coconut oil as a versatile ingredient that bridges nutritional and medicinal uses. With industrial players ensuring scalable supply and validated health claims, coconut oil continues to evolve from a basic fat to a premium functional component, fueling growth across multiple industries.

Government initiatives supporting coconut cultivation and exports in major producing countries

In the coconut oil industry, government initiatives in major coconut-producing countries are driving significant advancements in supply capacity, value addition, and export competitiveness. In the Philippines, the Philippine Coconut Authority (PCA) has implemented a five-year program to plant 100 million coconut trees by 2028, with a revised target of 50 million trees by 2026, up from the initial 25 million. Progress is evident, with over 8.5 million trees planted in 2024 and an additional 15 million targeted within the same year, ensuring long-term feedstock security for industrial processors and exporters [3]Source: Department of Agriculture Philippines, "Philippines Accelerates Coconut Planting to Regain Global Lead," da.gov.ph . In India, the Coconut Development Board’s schemes for area expansion, seedling support, and export promotion that promote downstream processing, logistics improvements, and expanded market access are channeling coconuts into higher-value oil and derivative exports, amplifying the impact of cultivation support on processed-product motion, and enhancing farmer productivity while maintaining a steady supply of raw materials for large-scale crushers and specialty oil manufacturers. These policies in the coconut oil market also align with export development efforts, such as participation in international trade events and compliance with global quality standards, benefiting industrial brands engaged in B2B supply chains. Companies like ADM capitalize on these government-backed expansions and infrastructure improvements to secure consistent volumes of crude and refined coconut oil for applications in food, personal care, and oleochemical products, reinforcing their role as industrial suppliers. In Indonesia, strategies promoting downstream processing, logistics improvements, and expanded market access are channeling coconuts into higher-value oil and derivative exports, amplifying the impact of cultivation support on processed product trade. These coordinated public and private investments in replanting, farmer support, refining, and export facilitation stabilize supply and pricing for global buyers, enabling long-term sourcing, innovation in functional formulations, and meeting rising demand across food, cosmetic, and pharmaceutical applications.

Increased use in cosmetics and personal care products due to its moisturizing and nourishing properties

The cosmetics and personal care segment in the coconut oil market increasingly relies on coconut oil due to its emollient properties, with medium-chain fatty acids that penetrate the stratum corneum more effectively than long-chain triglycerides. This enables deeper moisturization and barrier support in leave-on skincare products, hair conditioners, and lip balms, particularly those emphasizing natural origin claims. Its ability to provide occlusive yet lightweight nourishment aligns with clean-beauty trends, driving reformulation of existing products and accelerating new launches, thereby contributing to the growth of the global coconut oil market in this segment. Formulators are replacing mineral oils and synthetic emollients with plant-derived alternatives while maintaining texture, spreadability, and sensory performance. North America and Europe lead in adoption, driven by higher clean-beauty penetration compared to traditional prestige cosmetics channels, creating demand for certified, traceable coconut oil for high-performance applications. Rising disposable incomes and the influence of Western beauty standards in Asia-Pacific and the Middle East have further encouraged local and regional brands to incorporate coconut oil into hybrid formats such as treatment oils, scalp serums, and multi-function balms, expanding its applications. Industrial suppliers in the coconut oil industry, like BASF provide cosmetic-grade fractionated and hydrogenated coconut oil derivatives, including emollient esters and surfactants, to global manufacturers, ensuring stable, scalable ingredients for mass-market and premium formulations. These suppliers collaborate with beauty brands to align coconut-oil-based ingredients with claims around hydration, barrier repair, and "naturally derived" content, enhancing their value in claims-driven marketing. The interplay between consumer demand for natural, clean-label products and the technical benefits of coconut oil in formulation chemistry underscores its strategic importance in the cosmetics industry, driving its integration into core product formulations globally.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from substitute oils such as olive, avocado, and almond oil | -1.2% | Global, with pronounced effects in North America and Europe premium retail segments | Medium term (2-4 years) |

| Health concerns related to the saturated fat content in coconut oil | -0.8% | North America, Europe, and health-conscious urban markets globally | Long term (≥ 4 years) |

| Price fluctuations driven by weather-dependent crop yields and seasonal production | -0.7% | Global, originating in Asia-Pacific production zones with transmission to import markets | Short term (≤ 2 years) |

| Inconsistent quality standards across various production regions | -0.5% | Asia-Pacific production regions, affecting export competitiveness in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from substitute oils such as olive, avocado, and almond oil

In the coconut oil market, substitute oils, including olive, avocado, and almond oil, are increasingly capturing market share in both culinary and cosmetic applications, posing challenges to the growth of the global coconut oil market. Olive oil, with its monounsaturated fatty acid composition and strong association with the Mediterranean diet, has established premium shelf positioning in North American and European grocery channels, where per-capita consumption exceeds 1 liter annually. Health-conscious consumers in these regions exhibit high brand loyalty, favoring heart-healthy alternatives to tropical saturated fats. Avocado oil has rapidly gained traction in mainstream retail due to its high smoke point and neutral flavor profile, displacing coconut oil in sautéing and roasting applications as consumers seek plant oils with clear functional and nutritional advantages over coconut oil’s distinct taste and MCT-heavy composition. Almond oil, despite its higher cost, appeals to clean-label formulators in cosmetics for its nut-derived emollience and to culinary users desiring subtle flavor notes absent in coconut oil, intensifying cross-category competition. Price dynamics in the coconut oil market further exacerbate these challenges, particularly during coconut supply shocks. World Bank data indicates that coconut oil was priced at USD 2,599 per metric tonne in October 2025, approximately 40% higher than palm kernel oil and 20% higher than high-oleic sunflower oil, compressing margins for cost-sensitive food manufacturers and prompting shifts to more affordable substitutes. This pricing vulnerability is estimated to reduce the compound annual growth rate by 1.2% points, with the impact most pronounced in North America and Europe, where premium retail segments and superior distribution networks for substitute oils drive competitive pressure. Industrial suppliers, such as IOI Group, face additional challenges as foodservice operators and personal care formulators increasingly opt for alternatives, forcing suppliers to diversify portfolios to maintain volume stability.

Health concerns related to the saturated fat content in coconut oil

In the coconut oil market, concerns surrounding the high saturated fat content of coconut oil are influencing consumer preferences and industry practices, particularly as health organizations and regulatory bodies emphasize the associated risks. With approximately 90% saturated fat, coconut oil has been linked by entities such as the American Heart Association (AHA) and the World Health Organization (WHO) to elevated LDL ("bad") cholesterol levels and increased cardiovascular risk. Although it provides some HDL ("good") cholesterol benefits, these are insufficient to offset the concerns. Meta-analyses of clinical trials indicate that coconut oil raises LDL cholesterol levels similarly to other saturated fats, countering claims of superior metabolism benefits from its medium-chain triglycerides (MCTs). Consequently, health experts recommend limiting its intake to no more than 13 grams per day on a 2,000-calorie diet. Public health messaging has further positioned coconut oil as less heart-healthy compared to polyunsaturated oils like canola or sunflower oil, creating confusion and hesitancy among consumers, particularly those focused on cholesterol management and cardiovascular disease prevention. Dietary guidelines from organizations such as the AHA advocate replacing saturated fats, including coconut oil, with unsaturated alternatives to mitigate heart disease risk. This guidance has influenced retail stocking, food formulation, and marketing strategies, with industrial suppliers like Peter Cremer observing reduced reliance on coconut oil in favor of blended or alternative vegetable oils. The ongoing debate, despite distinctions related to MCTs, continues to erode coconut oil’s positioning as a functional ingredient. Healthcare professionals’ conservative stances amplify negative perceptions, particularly in developed markets, prompting formulators to limit or substitute their use. These factors, combined with wellness trends favoring low-saturated fat alternatives, present significant challenges to coconut oil’s broader market penetration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Un-Refined Variants Capture Premium Positioning

In the coconut oil market, refined coconut oil remains a dominant choice in foodservice and industrial applications, accounting for 53.78% of 2025 revenue. Its cost-effective profile and neutral flavor, achieved through refining, bleaching, and deodorization processes, make it suitable for applications requiring extended shelf life and bulk handling. These processes remove free fatty acids and volatile compounds, ensuring performance stability in demanding uses such as bakery shortenings and confectionery fats, where sensory attributes are less critical. Industrial suppliers in the coconut oil market, like KLK Oleo, provide refined coconut oil to global manufacturers, enabling scalable production. Additionally, the fractionated variant of refined coconut oil, produced by isolating caprylic and capric acids, serves niche markets in cosmetics and pharmaceuticals. Its liquid state and oxidative stability make it ideal for preservative-free personal-care formulations and pharmaceutical excipients. These specialized attributes allow fractionated oil to command premium pricing, complementing the volume leadership of refined coconut oil by addressing high-value specialty segments.

Unrefined coconut oil, including virgin and cold-pressed varieties, is gaining significant traction due to its alignment with premiumization trends in natural-foods retail in the coconut oil market. Consumers increasingly associate these variants with superior nutritional retention and sensory qualities, such as robust aroma and flavor. This segment is outperforming refined grades by leveraging attributes like organic certification, fair-trade sourcing, and minimal processing, which help preserve antioxidants and bioactive compounds. These factors are driving a compound annual growth rate (CAGR) of 8.31% through 2031. Brands are capitalizing on these characteristics to achieve price points 30% to 50% higher than refined alternatives in health-focused markets. Furthermore, a 2024 peer-reviewed study underscores the functional utility of un-refined coconut oil, demonstrating that virgin coconut oil-based nanostructured lipid carriers achieved 75.6% rosuvastatin encapsulation efficiency while enhancing hypolipidemic efficacy in vivo. This highlights its expanding appeal from nutrition to pharmaceutical applications.

By Nature: Organic Certification Drives Fastest Expansion

Conventional coconut oil maintained its dominance, accounting for 74.16% of the global coconut oil market volume in 2025. Its competitive advantage lies in lower production costs and robust supply chains, making it the preferred choice for price-sensitive applications. Large processors, such as AAK, achieve economies of scale by sourcing from aggregators who blend output from thousands of smallholders. This cost-efficient structure secures conventional coconut oil's position in industrial applications, including foodservice frying and oleochemicals, where organic price premiums are less justifiable. While organic coconut oil benefits from sustainability commitments, such as multinational corporations aiming for 100% certified sustainable coconut oils by 2025, conventional variants continue to lead in volume due to their reliable availability and cost-effectiveness in high-throughput segments.

Organic coconut oil, on the other hand, is experiencing significant growth, with a compound annual growth rate (CAGR) of 8.42% projected through 2031. This growth outpaces the overall market by more than one percentage point, driven by increasing consumer demand for clean and sustainable ingredients. The USDA organic certification process, which includes a three-year land transition period, bans on synthetic pesticides and fertilizers, and mandatory annual third-party audits, ensures stringent quality standards. These requirements create a clear distinction from conventional grades but also present challenges for smallholders in key producing countries like the Philippines and Indonesia, where average farm sizes range from 2 to 3 hectares and extension support is limited. The resulting scarcity of organic coconut oil supports premium pricing and enhances its appeal in corporate procurement, where traceability is highly valued. Furthermore, European Union organic standards under Regulation (EU) 2018/848 impose dual-certification requirements for exporters targeting North American and European markets, further elevating the value of organic coconut oil in regulated premium channels.

By Application: Cosmetics and Personal Care Emerge as Growth Engine

The food and beverage segment in the coconut oil market accounted for 63.62% of coconut oil demand in 2025, driven by its diverse applications in cooking oils, bakery shortenings, confectionery coatings, and dairy alternatives, particularly in tropical and subtropical cuisines. Its solid-at-room-temperature texture and high smoke point make it well-suited for frying, baking, and chocolate tempering, enhancing product quality through stability and effective flavor release without synthetic additives. Industrial suppliers, such as Musim Mas, cater to food manufacturers by providing refined and fractionated coconut oil in bulk, supporting large-scale applications like snack production and plant-based spreads that benefit from its clean-label appeal. This established role in the food and beverages sector ensures sustained volume leadership, as cost efficiency and performance reliability remain key factors over premium health claims in routine consumption.

The cosmetics and personal care segment in the coconut oil market is anticipated to grow at a compound annual growth rate (CAGR) of 7.75% through 2031, driven by increasing demand for clean-beauty products and regulatory requirements emphasizing transparency. Coconut oil is widely used in moisturizing emulsions, hair treatments, and balms, while pharmaceutical applications, though smaller in volume, achieve the highest price per kilogram due to its role in advanced formulations such as nanostructured lipid carriers and liposomal systems that enhance drug bioavailability. A study published in August 2024 demonstrated that virgin coconut oil-based carriers for rosuvastatin achieved 75.6% encapsulation efficiency, significantly reducing triglycerides, total cholesterol, and LDL levels in obese rat models. Suppliers like Croda provide cosmetic-grade coconut oil derivatives, meeting the precision needs of pharmaceutical applications while supporting scalability in cosmetics. By 2028, the cosmetics segment is expected to surpass pharmaceutical applications in volume, driven by consumer preferences for natural active ingredients.

Geography Analysis

Asia-Pacific dominated global consumption in 2025, accounting for 74.24% of the coconut oil market. This is driven by production hubs in the Philippines, Indonesia, India, and Sri Lanka, which collectively supply approximately 85% of global exports. Strong domestic demand, supported by culinary traditions such as curries, stir-fries, and baked goods, further reinforces the region's position. The Philippines Coconut Authority's initiative to plant 100 million trees by 2028 aims to address aging palm stocks, which currently yield below 1 tonne of copra per hectare. This program is expected to stabilize export volumes at USD 2-3 billion annually through 2026 while ensuring a consistent industrial supply. In India, the Coconut Development Board's extension programs focus on integrated pest management and fertigation to combat issues like rhinoceros beetle infestations and bud rot, improving per-palm yields. However, domestic consumption limits India's export potential, sustaining premium international pricing. Sri Lanka's production in 2023-2024 has declined due to fertilizer shortages and political instability, creating supply gaps that have redirected demand to the Philippines and Indonesia, tightening global spot prices.

North America is expected to lead regional growth in the coconut oil market with a compound annual growth rate (CAGR) of 8.58% through 2031. This growth is supported by the premium positioning of natural-food products, clean-label packaged goods reformulation, and pharmaceutical research and development utilizing coconut oil as an excipient in lipid-based delivery systems. Europe channels imports through the Netherlands for distribution to Germany, France, and the United Kingdom, with demand emphasizing organic and fair-trade certifications that command sustainability premiums. Codex Alimentarius standards on free fatty acid and peroxide values guide quality, but inconsistent enforcement has led to multinational audits and traceability platforms verifying origins.

Emerging regions in the coconut oil market, including South America, the Middle East, and Africa are also contributing to growth, driven by urbanization and rising incomes. Brazil and Argentina import coconut oil for cosmetics and specialty foods, while the United Arab Emirates and Saudi Arabia favor refined grades for halal-certified products and hot-climate shelf stability, with Dubai serving as a re-export hub to Africa and Central Asia. In Africa, countries like Nigeria and South Africa are driving growth in urban beauty and bakery applications, though price sensitivity limits overall volumes. Turkey, benefiting from its European Union customs union, supports Balkan re-exports. Industrial players like Naturin contribute to the market by supplying fractionated coconut oil for Middle Eastern emulsions, integrating emerging logistics into global value chains.

Competitive Landscape

Leading players in the coconut oil market, such as Cargill, Archer Daniels Midland (ADM), and Bunge, maintain dominance in the global market through extensive sourcing networks and large-scale refining operations, highlighting moderate market fragmentation. These companies ensure a reliable supply for industrial buyers by bundling coconut oil with other products like palm kernel oil, soybean oil, and specialty fats. This approach streamlines procurement for food manufacturers while offering technical support for clean-label reformulations in bakery, confectionery, and dairy alternatives. Their economies of scale in logistics and processing enable cost efficiencies, allowing them to maintain competitive pricing even during supply disruptions from Asian origins.

In the coconut oil industry, vertically integrated producers in Asia, including Greenville Agro Corporation, Celebes Coconut Corporation, and Thai Coconut Public Company, oversee the entire value chain from plantations to exports. This integration ensures stringent quality control and rapid responses to fluctuations in demand. By addressing risks such as aging coconut palms and weather-related challenges, these producers support initiatives like the Philippines Coconut Authority's tree-planting programs to sustain yields. Their focus on refined and virgin coconut oil grades for export complements the blending strategies of multinational companies, catering to high-value segments in the cosmetics and pharmaceutical industries.

Innovative biotechnology firms in the coconut oil market are emerging as disruptors by employing microbial fermentation to produce lauric acid and medium-chain triglycerides, reducing dependence on agricultural factors like monsoons and land availability. Technological advancements, including blockchain and QR-code traceability, are enhancing transparency and validating organic certifications, particularly in the pharmaceutical and cosmetics sectors. These developments address rising ISO 9001 and ISO 22000 contract requirements. Meanwhile, competition in North America and Europe intensifies due to substitutes like olive, avocado, and almond oils, as well as private-label products. Organic specialists such as Liberty Oils defend their market position through certifications and direct distribution channels, linking compliance with sustained premium pricing.

Coconut Oil Industry Leaders

-

Cargill Incorporated

-

Bunge Limited

-

Greenville Agro Corporation

-

Archer Daniels Midland Company

-

Celebes Coconut Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BASF expanded its portfolio of natural ingredients with the introduction of Dehyton PK45 GA/RA, a sustainable betaine derived from coconut. Dehyton PK45 GA/RA was an amphoteric surfactant that was readily biodegradable and was particularly suitable for applications in shampoos, shower and bath products, and skin cleansers, offering excellent foaming properties.

- July 2024: AAK introduced AkoVeg 163-14, a product combining coconut oil and insoluble fiber flakes. AkoVeg enabled formulators to develop plant-based meat products with reduced total fat content and no cholesterol. The solution offered manufacturers benefits such as heat tolerance and stability, enhanced firmness and sliceability, consistent flavor delivery and mouthfeel, optimized production processes, and improved labeling options.

- January 2024: AAK expanded its AkoPlanet platform for plant-based foods in the United States by introducing a new coconut oil, AkoPlanet CNO 16-001. This addition aimed to support a sustainable coconut oil supply chain. The AkoPlanet line comprises plant-based oil ingredients designed for plant-based food applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the coconut oil market as the aggregated value of virgin, refined, and crude coconut oils that are pressed from the kernel of Cocos nucifera, traded in bulk or packaged form, and ultimately consumed across food, cosmetics, pharmaceutical, and industrial channels. Volumes converted to retail-equivalent value through country-level average selling prices anchor the base year.

Scope exclusion: Fractionated coconut oil destined exclusively for oleochemical intermediates is outside the current scope.

Segmentation Overview

-

By Product Type

- Refined Coconut Oil

- Un-Refined Coconut Oil

- Other Types of Coconut Oil

-

By Nature

- Conventional

- Organic

-

By Application

- Food and Beverages

- Pharmaceuticals

- Cosmetics and Personal Care

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed processors in Southeast Asia, distributors in Europe and North America, and brand formulators in cosmetics and nutrition to validate yield assumptions, purity-grade price spreads, and regional usage trends. Follow-up surveys with importers clarified seasonality and the pass-through of copra price shocks to shelf prices.

Desk Research

We began with public datasets from the Philippine Statistics Authority, UN Comtrade, and the International Coconut Community that map production, export, and import flows. Trade association releases such as the Asian and Pacific Coconut Community, peer-reviewed journals covering medium-chain triglyceride (MCT) science, and filings from listed edible-oil manufacturers enriched supply, demand, and price patterns. Company 10-Ks, investor decks, and reputable business press filled short-term demand shifts. Subscription portals like D&B Hoovers and Dow Jones Factiva supplied audited revenue splits and real-time news. The sources cited illustrate our desk inputs and are not exhaustive; many further repositories supported data checks.

Market-Sizing & Forecasting

A top-down construct translates country production plus net trade into available supply, which is then reconciled with end-use consumption pools. Select bottom-up roll-ups of leading refineries and sampled retail scan data stress-test the totals. Key variables feeding the model include copra output, refinery utilization, virgin-oil penetration in packaged foods, per-capita natural-cosmetic spend, and freight indices that sway landed cost. Forecasts apply multivariate regression blended with ARIMA to project these drivers, while expert consensus guides scenario bounds. Data gaps in minor economies are bridged using regional per-capita proxies before final balancing.

Data Validation & Update Cycle

Outputs pass anomaly checks against historical trade ratios, external price benchmarks, and prior editions. A senior analyst reviews deviations, and we refresh every twelve months, with interim revisions when hurricanes, tariff changes, or plant shutdowns materially alter the outlook. Before release, an analyst performs a fresh audit so clients receive the latest view.

Why Mordor's Coconut Oil Baseline Commands Reliability

Estimates published by different firms often diverge because each chooses distinct product mixes, price reference points, and refresh calendars.

Key gap drivers for this market include whether virgin and RBD grades are combined, the treatment of industrial oleochemical off-take, currency-year alignment, and how aggressively future penetration into plant-based foods is modeled. Mordor applies a consistent grade mix, converts every figure to constant 2025 USD, and revisits model drivers annually, leading to a steadier baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.21 B (2025) | Mordor Intelligence | - |

| USD 5.70 B (2022) | Global Consultancy A | Narrower scope omits crude grade and inflates 3-year CAGR to extrapolate |

| USD 5.45 B (2025) | Trade Journal B | Relies on static copra-to-oil conversion and does not net re-exports |

| USD 5.90 B (2023) | Regional Consultancy C | Uses list prices without weighting for bulk discounts |

In sum, by aligning scope with observable trade flows, balancing top-down and bottom-up checks, and refreshing inputs every year, Mordor delivers a transparent, dependable starting point for strategic decisions.

Key Questions Answered in the Report

What is the projected compound annual growth rate for the global coconut oil market through 2031?

The worldwide coconut oil market is forecast to expand at a 7.36% CAGR between 2026 and 2031.

Why are cosmetics and personal-care uses expanding more quickly than food applications?

Brands are reformulating to meet clean-beauty standards, and coconut-based emollients replace mineral oil and silicone, pushing the segment to a 7.75% CAGR, faster than any other end use.

Which region is expected to record the fastest demand growth over the next five years?

North America leads growth with an 8.58% CAGR for the 2026-2031 period, driven by clean-label adoption and premium personal-care launches.

What is the main downside risk that could slow coconut oil demand in Western markets?

Ongoing consumer concern about its high saturated-fat content keeps some buyers favoring olive, avocado, or almond oils, tempering growth potential.

Page last updated on: