Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 87.14 Billion |

| Market Size (2026) | USD 89.25 Billion |

| Market Size (2031) | USD 100.53 Billion |

| Growth Rate (2026 - 2031) | 2.42% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Cane Sugar Market Analysis by Mordor Intelligence

The Asia-Pacific cane sugar market size in 2026 is estimated at USD 89.25 billion, growing from 2025 value of USD 87.14 billion with 2031 projections showing USD 100.53 billion, growing at 2.42% CAGR over 2026-2031. While the regional landscape sees a moderate expansion, individual countries tell a different story. China, despite accounting for 28.42% of the 2024 volume, is advancing at a pace below the trend due to slower-than-expected industrial demand and limited policy support for production expansion. In contrast, Vietnam is surging ahead with a 7.25% CAGR, buoyed by 90% mechanization, which has significantly improved efficiency, and the rollout of carbon-credit pilots that incentivize sustainable practices. Policy shifts are also making waves in the supply chain: In November 2023, India paused juice-to-ethanol conversions, redirecting 4.27 billion liters of feedstock back to milling, which has temporarily boosted short-term output and stabilized domestic supply. Meanwhile, Thailand, facing an 11.7-million-ton drought setback in 2023-24, adapted with varietal changes and precision irrigation techniques, enabling the country to recover and aim for a projected 90-million-ton harvest in 2024-25. The cane sugar market in the region remains buoyant, driven by increasing demand from food, pharmaceutical, and craft-beverage sectors, alongside a surge in online grocery shopping, which has expanded consumer access and convenience.

Key Report Takeaways

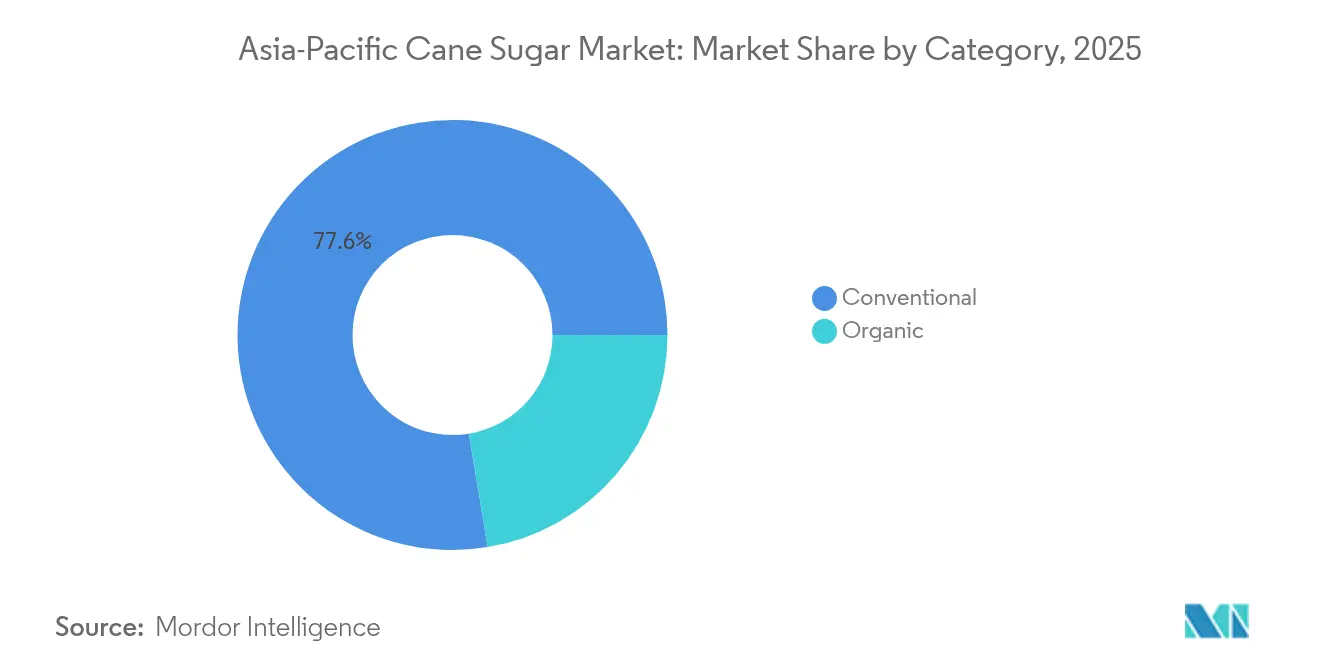

- Conventional cane sugar captured 77.62% of the Asia-Pacific cane sugar market share in 2025, while organic variants are projected to expand at a 4.03% CAGR through 2031.

- Crystallised sugar accounted for 61.44% of the Asia-Pacific cane sugar market size in 2025, yet liquid syrup leads growth at a 5.12% CAGR during 2026-2031.

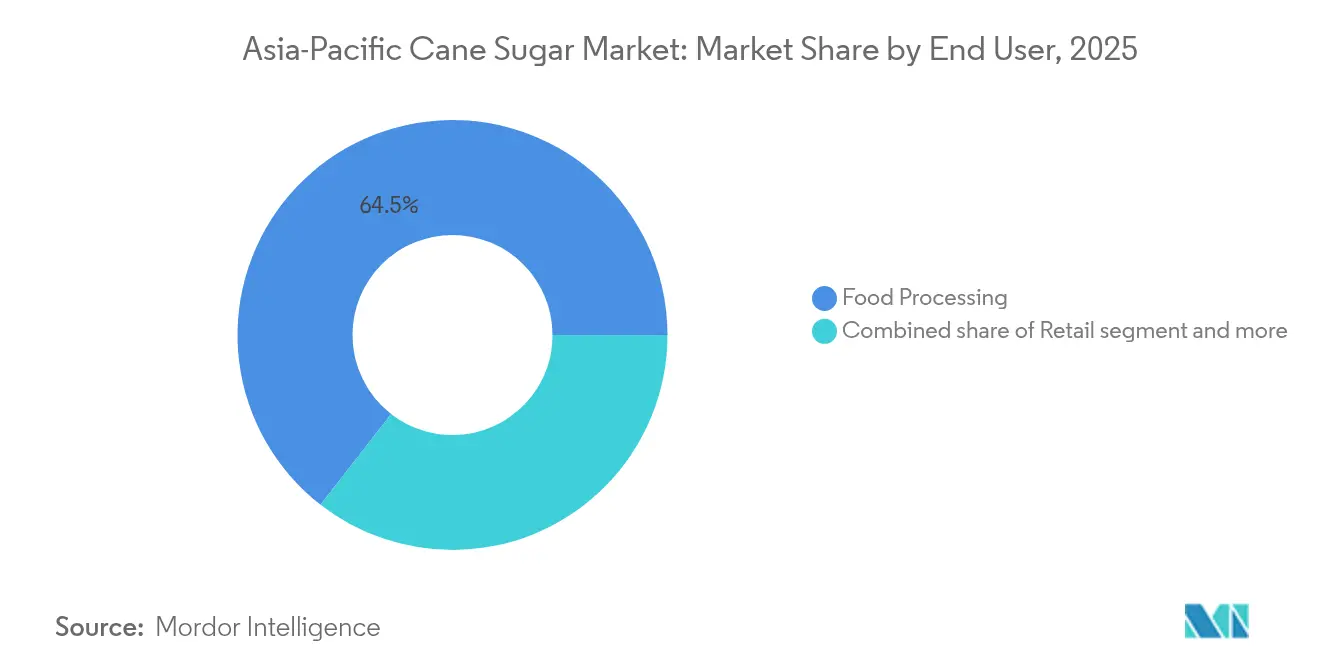

- Food processing commanded 64.48% share of the Asia-Pacific cane sugar market size in 2025, whereas pharmaceutical and nutraceutical applications are advancing at a 4.58% CAGR to 2031.

- China held 28.10% of the Asia-Pacific cane sugar market share in 2025; Vietnam is forecast to register the fastest 6.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Cane Sugar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising per-capita sugar intake in emerging Asia-Pacific economies | 0.5% | India, Indonesia, Vietnam, with spillover to Philippines and Bangladesh | Medium term (2-4 years) |

| Rapid expansion of regional Food and Beverage processing capacity | 0.6% | China, India, Vietnam, Indonesia, Thailand | Short term (≤ 2 years) |

| Yield gains from precision agronomy and mill automation | 0.3% | Vietnam, Thailand, Australia, with adoption spreading to India's Uttar Pradesh and Punjab | Long term (≥ 4 years) |

| Government ethanol-blending mandates boosting cane demand | 0.4% | India (E20 by 2025-26), Indonesia (B40 bioethanol roadmap), Thailand (molasses-based programs) | Medium term (2-4 years) |

| Niche demand for craft-beverage "single-origin" cane sugars | 0.1% | Japan, South Korea, Australia, urban centers in China and India | Long term (≥ 4 years) |

| Direct-to-consumer e-grocery platforms broadening retail reach | 0.2% | China, India, Indonesia, Malaysia, with rapid penetration in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising per-capita sugar intake in emerging Asia-Pacific economies

Asia, with an average sugar consumption of 21.2 kg per capita, lags behind the global mean of 23.1 kg. However, due to its vast population, Asia is projected to account for 64% of the incremental global sugar demand through 2034, highlighting the region's critical role in shaping global sugar markets[1]Source: Organisation for Economic Co-operation and Development, "Agriculture and fisheries", oecd.org. In 2024, Indonesia consumed 7.2 million tons of sugar, but with only 2.2 million tons produced domestically, the nation faces a significant 69% import gap. This gap underscores Indonesia's heavy reliance on imports, which persists even as the government prioritizes achieving self-sufficiency through policy measures and domestic production initiatives. Meanwhile, India ramped up its sugar consumption to 29 million tons in 2024-25, driven by a surge in packaged food popularity in tier-2 cities, where rising disposable incomes and urbanization are fueling demand. In Vietnam, competitive farmgate pricing ensures attractive margins for downstream players, encouraging sustained production and investment in the sector. On the other hand, China's per-capita sugar intake stands at 11 kg, indicating potential growth opportunities for the market, even as state campaigns advocate for reduced sugar consumption to address health concerns and promote healthier dietary habits.

Rapid expansion of regional food and beverage processing capacity

In 2024, food processors captured 65.17% of the regional demand and are ramping up their capacities at a pace outstripping consumption growth, driven by increasing demand for processed and packaged food products. The bakery sector in India poured in a hefty USD 600 million into automated lines, specifically those utilizing liquid syrup for continuous mixing, to enhance production efficiency and meet the growing consumer preference for consistent product quality. In a bid to sustain sweetness while reducing sugar content per serving, beverage manufacturers in China upped their liquid-sugar concentrations by 8% in 2023, ensuring steady industrial demand and aligning with health-conscious consumer trends. Dairy producers in Vietnam are using 15-20% more sugar per liter compared to ambient products, leading to an uptick in refined sugar imports from Thailand and Australia to meet the rising demand for sweetened dairy products. Snack manufacturers in Indonesia are blending cane and palm sugars to meet halal standards, thereby tapping into hybrid channels that traditional classifications have previously overlooked, enabling them to cater to a broader consumer base while adhering to regulatory requirements.

Yield gains from precision agronomy and mill automation

Due to the adoption of the KK3 varietal and 90% mechanization, Vietnam tops ASEAN with a yield of 6.79 tons of sugar per hectare, showcasing the country's advancements in agricultural practices. In Thailand, Mitr Phol enhances recovery rates by 1.2 percentage points and cuts manpower needs in half by leveraging real-time moisture sensors and automated juice extraction technologies, setting a benchmark for efficiency in the region. Australia boasts a fully mechanized harvest, producing 4.2 million tons of sugar annually. However, with labor costs ranging from USD 16-20 per hour, smaller mills find it challenging to compete without hefty capital investments, highlighting the disparity in operational scales. While mechanization in India's Uttar Pradesh has reached 22%, the national average remains below 15%, primarily due to the steep costs of harvesters, which limit widespread adoption. In China, Guangxi experiments with drone fertilization and satellite irrigation scheduling to modernize its agricultural processes, but its yields still trail behind regional frontrunners, indicating room for further improvement.

Government ethanol-blending mandates boosting cane demand

In 2023-24, India's E20 initiative diverted 4.27 billion liters of ethanol, translating to 2.5 million tons of sugar. This diversion underscores the country's commitment to reducing its dependence on fossil fuels and promoting renewable energy sources. However, a temporary freeze on converting juice to ethanol highlights the volatility in policy, which could impact the consistency of ethanol supply and sugar production. Meanwhile, Indonesia's B40 initiative is vying for feedstock, further straining resources and exacerbating the domestic sugar deficit, as the country struggles to balance its biofuel ambitions with sugar availability. Thailand, on the other hand, is strategically utilizing molasses and cassava for ethanol production, ensuring its sugar exports remain robust and unaffected by domestic ethanol demands. On a global scale, the diversion of sugar crops for fuel is set to rise from 18% in 2024 to 24% by 2034, driven by increasing biofuel mandates and energy transition goals. Asia is expected to account for 15% of this increase, reflecting the region's growing role in the global biofuel market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sugar-reduction health policies and taxation | -0.70% | Malaysia, Singapore, Thailand, Vietnam, Indonesia, China | Short term (≤ 2 years) |

| Weather-driven price volatility and supply shocks | -0.60% | Thailand, India, Australia, Vietnam | Short term (≤ 2 years) |

| Farm-labour scarcity accelerating costly mechanisation | -0.40% | India, Thailand, Indonesia, China | Medium term (2-4 years) |

| Substitution by alternative sweeteners and HFCS | -0.50% | China, Japan, South Korea, Australia, urban Asia-Pacifc markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sugar-reduction health policies and taxation

In 2025, Malaysia raised its excise tax to RM 0.90 per liter, prompting 96% of beverage companies to reformulate their products, reducing sugar content by as much as 15%. This move aimed to address rising health concerns related to sugar consumption and encourage healthier product offerings. Singapore's Nutri-Grade labeling, introduced to promote transparency in sugar levels, compelled major cola brands to cut their sugar content by up to 18%, reflecting the growing regulatory pressure on the beverage industry. Between 2022 and 2024, Thailand's tiered excise system led to an 8% reduction in sugar use in drinks, showcasing the effectiveness of fiscal measures in influencing product reformulation. Vietnam is mulling over a similar two-tier levy, which could further dampen demand and align with regional efforts to curb sugar consumption[2]Source: World Health Organization, "It is time for Viet Nam to tax sugary drinks", who.int. Meanwhile, Indonesia has proposed a draft regulation capping sugar in packaged foods at 10 g per serving, signaling a broader regional trend towards stricter sugar regulations to combat health issues like obesity and diabetes.

Weather-driven price volatility and supply shocks

Thailand's drought in 2023-24 significantly reduced cane output by 11.7 million tons, leading to a tighter sugar supply and driving up regional prices. This reduction has created ripple effects across the sugar market, impacting both domestic and international stakeholders. In India, disruptions caused by the monsoon in Maharashtra are projected to lower the 2024-25 sugar output from 32 million tons to approximately 27 million tons, marking a notable decline that could affect both domestic consumption and export commitments. Meanwhile, Australia’s sugar industry faces challenges as cyclone risks threaten its exportable surplus of 3.5 million tons, potentially disrupting global supply chains and trade flows[3]Source: United States Department of Agriculture, "Sugar Semi-annual", apps.fas.usda.gov. In Vietnam, salt-water intrusion in the Mekong Delta poses a serious risk, with the potential to reduce output by 20% during unfavorable years, further straining regional supply. Furthermore, domestic sugar prices in India experienced a sharp 23% fluctuation in 2024, significantly increasing hedging costs for processors and adding financial strain to the industry, which may lead to higher consumer prices and reduced profit margins for producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Organic Certification Premiums Drive Niche Expansion

In 2025, conventional cane sugar dominated the Asia-Pacific market, seizing a 77.62% share. Its stronghold is bolstered by cost advantages, well-established refining networks, and consistent demand from packaged foods, beverages, and retail sectors. With FOB prices hovering between USD 400–450 per ton, conventional sugar lures large-scale buyers eyeing stable input costs. Additionally, small and mid-tier refiners lean towards conventional throughput, not only to optimize asset utilization but also to shield against raw sugar price fluctuations, solidifying the segment's role in regional trade dynamics.

While organic cane sugar remains a niche player, it's the segment with the most momentum, forecasted to grow at a 4.03% CAGR until 2031. This surge is largely attributed to Fairtrade premiums, ranging from 13–20% in India and Thailand, which effectively counterbalance certification and compliance expenses. Innovative approaches, such as Lasuco’s carbon-credit-backed low-chemical farming in Vietnam, are paving the way for smaller farmers to navigate the certification maze. Furthermore, major confectionery corporations in Japan and South Korea are locking in long-term contracts for organic supplies, spurring increased production from Thai exporters. Despite the allure, with annual audit costs between USD 1,500–2,500 per farm, organic adoption faces hurdles. Yet, with e-grocery platforms booming in China's major cities and the potential for premium margins 18–25% above standard commodity grades, mills see organic sugar as a promising diversification, especially against a backdrop of stable conventional prices.

By Form: Liquid Syrup Gains in Automated Processing Lines

Crystallised sugar remained the largest format in the Asia-Pacific cane sugar market, commanding 61.44% of the total market size in 2025. Its dominance reflects broad versatility, long shelf life, and suitability for both household retail and food-service channels. Industrial users favor granulated sugar for its ease of handling, reliable portioning, and recipe consistency across bakery and confectionery operations. Household consumption continues to account for more than one-third of total volume, reinforcing the segment’s stability even as automation advances in industrial applications.

Liquid syrup represents the fastest-growing format, projected to expand at a 5.12% CAGR through 2031, surpassing the overall market pace. Growth is driven by the shift toward precision dosing in continuous-mixing bakeries and high-speed beverage lines, improving efficiency and reducing waste. China’s bottlers, for instance, raised syrup concentrations by 8% in 2023 to maintain taste with less sugar per serving, while India’s automated bakeries achieved 20–25% higher throughput through bulk syrup integration. In Vietnam and South Korea, dairy and refining industries increasingly adopt liquid and invert syrups for improved homogeneity, cold-chain stability, and processing cost savings, setting the stage for gradual share gains in industrial sugar applications.

By End User: Pharmaceutical Applications Outpace Food Processing Growth

Food processing remained the largest end-use segment in the Asia-Pacific cane sugar market, accounting for 64.48% of total demand in 2025. The segment’s dominance is anchored in bakery, confectionery, dairy, and beverage manufacturing, which collectively drive substantial industrial sugar consumption. Population growth and rising disposable incomes in Indonesia and Vietnam continue to sustain baseline volume growth despite the gradual rollout of sugar-reduction policies. Bakeries alone absorbed 40% of industrial usage as Western-style snacking expanded beyond urban centers, while beverage producers retained high absolute volumes even under taxation pressures, reflecting resilient consumer demand.

The pharmaceutical and nutraceutical segment is the fastest-growing channel, projected to expand at a 4.58% CAGR through 2031. India’s prominent vaccine production capacity and China’s expanding supplement market underpin steady demand for excipient-grade sugar that meets USP–NF standards. Such high-purity inputs command 15–20% premiums and provide price stability for compliant mills operating under rigorous audit regimes. Demand from biologics manufacturers for sucrose in cell-culture media and freeze-drying processes further buffers the sector from confectionery and beverage cyclicality. This diversification toward regulated applications enhances revenue resilience and underscores traceability as a strategic differentiator in the region’s evolving cane sugar value chain.

Geography Analysis

In 2025, China dominated the regional landscape, accounting for 28.10% of the volume with a production of 10.5 million tons. This output met 68% of its consumption, which stood at 15.5 million tons. With central subsidies of CNY 15,000 per hectare, the goal is to boost self-sufficiency to 85% by 2030. However, yields in Guangxi, at 6.5 tons per hectare, lag behind Vietnam’s mechanized benchmark, posing a challenge to this ambition. Despite state-led campaigns advocating for reduced sugar intake, imports remain vital under the tariff-rate quota system. COFCO is capitalizing on this, expanding its refining operations to trade in raw sugars.

Vietnam is leading the regional charge with a robust 6.98% CAGR, bolstered by 90% mechanization, the adoption of the KK3 varietal, and a nurturing carbon-credit ecosystem. Trade defense mechanisms protect domestic mills from Thai competition, ensuring attractive farmgate prices and incentivizing planting. With a growing focus on dairy and beverages, Vietnam is not only curbing its export reliance but also solidifying the value within its local supply chain.

India's output dipped to around 27 million tons in 2024-25, influenced by erratic monsoons. However, the nation still boasts the capacity to swing-export. While policy fluctuations regarding ethanol blending introduce complexities in supply planning, the robust internal demand provides a cushion for producers. Thailand, buoyed by investments in precision irrigation, is set to bounce back to a projected 10.3 million tons in 2024-25. Indonesia, heavily reliant on imports at 69%, stands as the region's largest deficit market. Meanwhile, Malaysia leans on refiners like MSM to meet nearly all its domestic requirements. In 2024, Australia, with a crop yield of 4.2 million tons, is exporting a significant 85% to North Asian buyers, aligning its strategies with Wilmar’s expansion plans.

Competitive Landscape

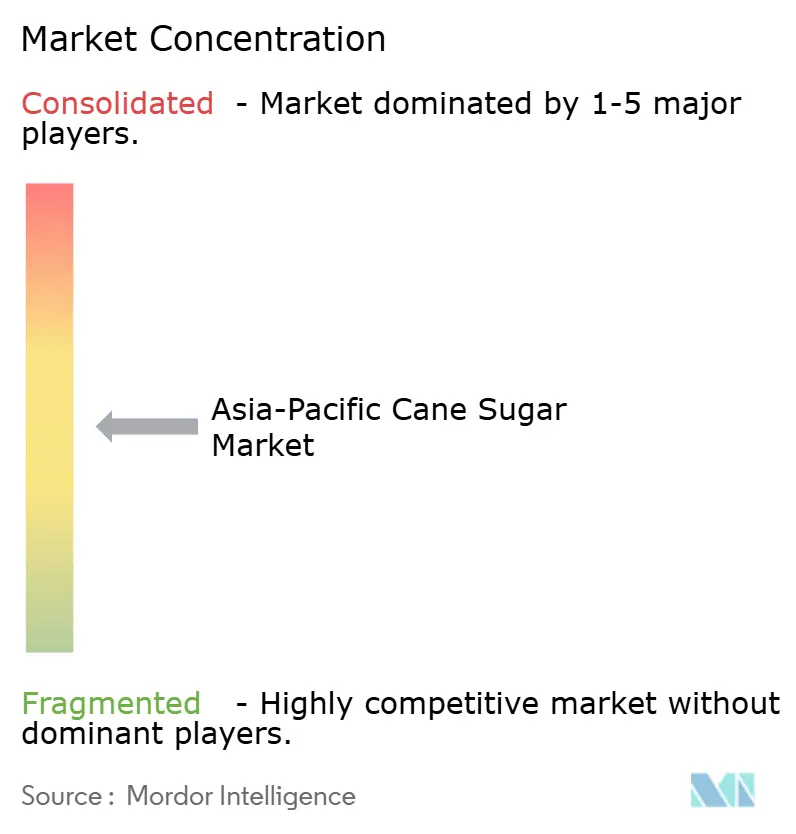

The Asia-Pacific cane sugar market exhibits moderate fragmentation. Here, leading players hold a moderate share, overshadowed by numerous smaller mills. In Q3 2024, Wilmar International reported a robust sugar revenue of USD 1.33 billion. The company capitalized on vertical integration, spanning from Australian cane fields to retail outlets in China, effectively harnessing logistics and refining margins. Mitr Phol operates 20,000-ton-per-day mills equipped with Industry 4.0 systems, achieving a 1.2-point boost in extraction yields and slashing manpower needs by half. This feat, however, poses a challenge for smaller mills in Thailand, which find it hard to replicate without significant capital investments. Meanwhile, Shree Renuka's acquisition of Brazilian acreage diversifies its crushing operations, providing a buffer against earnings dips during weaker harvest years in India.

As technology adoption surges, a pronounced productivity gap emerges. Vietnam leads with 90% mechanization, followed by Thailand at 50%. In stark contrast, India lags with under 15% and Indonesia even lower at sub-5%. This disparity signals potential structural consolidation or exits for operators lacking adequate capital. In both China and India, e-commerce channels are circumventing traditional wholesale tiers. This shift allows brands to pocket an additional 8-12% margin, simultaneously heightening price transparency. Furthermore, specialty single-origin sugars, particularly sought after for craft beverages, command a premium mark-up of 25-35%. This lucrative segment is enticing mid-tier refiners to delve into niche branding.

Key strategic maneuvers in 2024 spotlight Wilmar's ambitious USD 89 million Australian refining expansion, Shree Renuka's USD 45 million plantation acquisition in Brazil, and Mitr Phol's USD 22 million rollout of AI-driven maintenance. Ethanol diversification is gaining traction among regional players, underscored by Triveni's establishment of a 100-KLPD unit and DCM Shriram's capacity expansion, signaling the fuel blend's escalating significance in their portfolios. Highlighting the industry's shift towards premium segments, joint ventures like Thai Roong Ruang and Mitsui are setting their sights on organic exports, aiming for the lucrative margins they offer.

Asia-Pacific Cane Sugar Industry Leaders

-

Global Organics, Ltd.

-

Louis Dreyfus Company B.V.

-

Tate & Lyle PLC

-

American Sugar Refining, Inc.

-

Wilmar Sugar Australia Holdings Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Padma Shri Dr Vitthalrao Vikhe Patil Cooperative Sugar Factory, located in Pravara Nagar, is set to enhance its mill capacity and modernize operations. This initiative aims to bolster Maharashtra’s cooperative sugar sector and support local cane growers. The expanded facilities in Loni, often referred to as the “land of cooperation,” will be inaugurated by Union Home Minister Amit Shah, highlighting the project's political and cooperative significance for the region's sugar industry and its rural economy.

- September 2024: Mala’s Fruit Products unveiled its new Liquid Sugar Syrup, a ready-to-use sweetening solution crafted to perfect the sweetness of desserts and beverages. Packaged in a user-friendly PET bottle, the syrup offers a smooth, pourable sweetness that dissolves effortlessly. This innovation aids home bakers, cafés, and foodservice operators in saving preparation time while guaranteeing a consistent taste and quality across their recipes.

- December 2021: MSM Malaysia Holdings Bhd (MSM Malaysia) and Wilmar Sugar Pty Ltd (Wilmar Sugar) inked a collaboration agreement to build a sustainable sugar supply chain. MSM Malaysia and Wilmar Sugar will embark on joint efforts to assist and support each other to pilot an approach to enable sustainable raw sugar sourcing within both companies' joint supply chains by focusing on traceability reporting of sugar supplies and monitoring sustainability performance based on the NDPE Sugar Policy.

- November 2021: DCM Shriram Ltd announced an investment of over USD 4.22 million to expand the capacity of sugar mills. The company approved three investment proposals for the sugar business to capitalize on the increase in sugarcane availability in its catchment area, enhance the capacity for the production of refined sugar due to consumer preference, and build feedstock flexibility for its distilleries.

Asia-Pacific Cane Sugar Market Report Scope

Cane sugar is the sugar obtained from the processing of sugarcane.

The Asia-Pacific cane sugar market is segmented by category, form, application, and geography. Based on the category, the market is segmented into organic and conventional. Based on the form, the market is segmented into crystallized sugar and liquid syrup. Based on the application, the market is segmented into bakery and confectionery, dairy, beverages, and other applications. Based on geography, the market is segmented into China, Japan, India, Australia, and the Rest of Asia-Pacific.

For each segment, the market sizing and forecasts have been done based on value (in USD Million).

By Category

| Organic |

| Conventional |

By Form

| Crystallised Sugar |

| Liquid Syrup |

By End User

| Food | Retail | |

| Food Processing | Bakery and Confectionery | |

| Dairy | ||

| Beverages | ||

| Savory Snacks | ||

| Others | ||

| Food Services | ||

| Others | ||

Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| South Korea |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Category | Organic | ||

| Conventional | |||

| By Form | Crystallised Sugar | ||

| Liquid Syrup | |||

| By End User | Food | Retail | |

| Food Processing | Bakery and Confectionery | ||

| Dairy | |||

| Beverages | |||

| Savory Snacks | |||

| Others | |||

| Food Services | |||

| Others | |||

| Country | Australia | ||

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Malaysia | |||

| South Korea | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

What is the current value of the Asia Pacific cane sugar market?

The cane sugar market size stands at USD 89.25 billion in 2026 and is projected to rise to USD 100.53 billion by 2031.

Which country leads regional consumption?

China leads, accounting for 28.10% of 2025 demand despite its relatively low per-capita intake.

Which segment is growing fastest by form?

Liquid syrup is expanding at a 5.12% CAGR between 2026 and 2031, outpacing crystallised formats.

Why is Vietnam’s growth rate higher than the regional average?

Mechanization at 90%, high-yield KK3 varietals, and supportive trade defense measures propel a 6.98% CAGR through 2031.

Page last updated on: