Agave Syrup Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

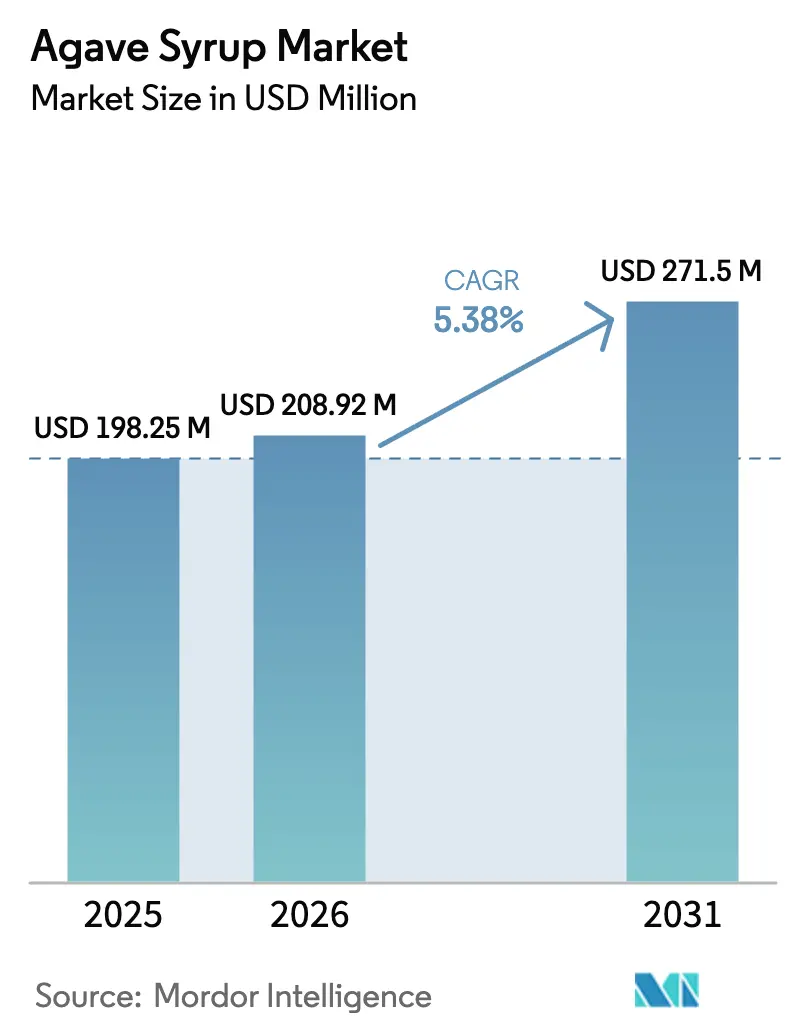

| Market Size (2026) | USD 208.92 Million |

| Market Size (2031) | USD 271.5 Million |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

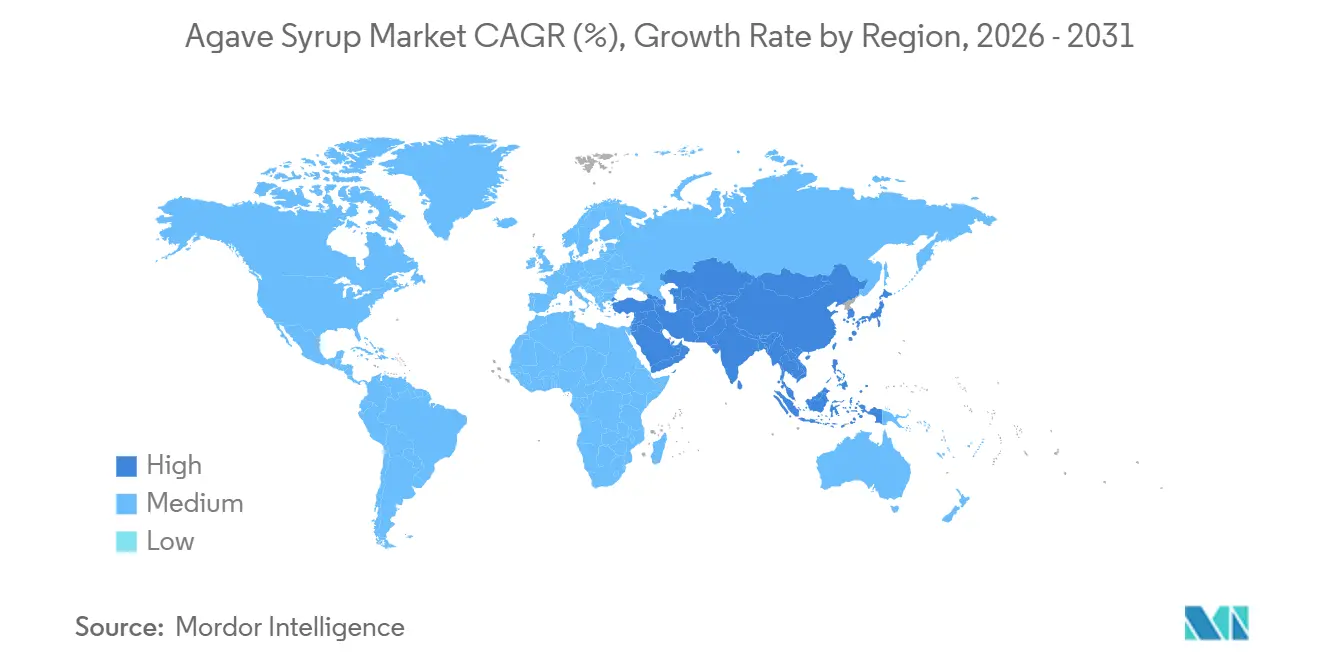

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Agave Syrup Market Analysis by Mordor Intelligence

The Global Agave Syrup Market size is expected to grow from USD 198.25 billion in 2025 to USD 208.92 million in 2026 and is forecast to reach USD 271.5 million by 2031, expanding at a compound annual growth rate of 5.38% during the forecast period. This growth trajectory highlights the sweetener's balancing act: on one hand, there is a rising consumer appetite for plant-based, clean-label alternatives; on the other, there is increasing scrutiny over fructose content. Rather than merely expanding in volume, the market is evolving through premiumization. Organic-certified and flavored agave variants are seizing a larger share of the market's value, even as mainstream sugar alternatives face commoditization. Positioned strategically, agave syrup sits between nutritive sweeteners like honey and non-nutritive ones such as stevia. It attracts consumers who value its natural origins and versatility over mere zero-calorie claims.

In 2025, North America held a 35.12% share of the agave syrup market, bolstered by Mexico's leading blue agave production and U.S. consumers' growing familiarity with the ingredient via specialty foods. North America is expected to be the fastest-growing market through 2031, while Asia-Pacific remains the largest regional market and is projected to expand at a 6.56% CAGR through 2031. This growth is fueled by rising disposable incomes, the expansion of modern retail, and a regulatory green light for imported natural sweeteners in China, India, and Japan.

As the market evolves towards 2031, the challenge for producers will be striking a balance between premiumization and affordability. According to the Organisation for Economic Co-operation and Development-Food and Agriculture Organization (OECD-FAO) Agricultural Outlook published in July 2025, global sugar prices are expected to see a slight dip until 2034, coinciding with a 15 percent rise in global production, reaching 205 million metric tons[1]Source: Organization for Economic Co-operation and Development-Food and Agriculture Organization "OECD-FAO Agricultural Outlook 2025-2034," oecd.org. However, brands might counteract this by justifying premium prices through verifiable sustainability, traceability, or innovations like reduced-sugar formulations.

Key Report Takeaways

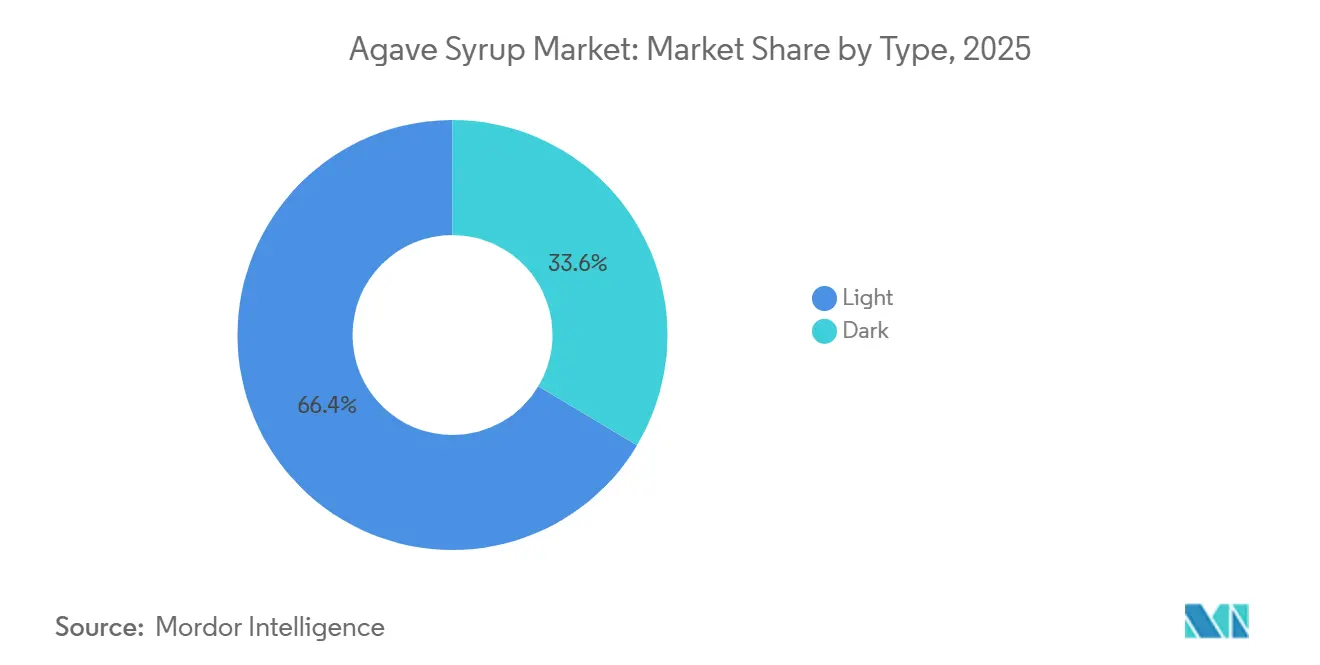

- By type, light variants commanded 66.43% of agave syrup market share in 2025; dark syrup is forecast to expand at a 6.02% CAGR through 2031.

- By category, conventional products held 82.11% revenue share in 2025, while organic syrup is advancing at a 6.34% CAGR to 2031.

- By raw material, blue agave delivered 78.84% of the agave syrup market size in 2025, whereas salmiana-based syrup is rising at a 5.68% CAGR through 2031.

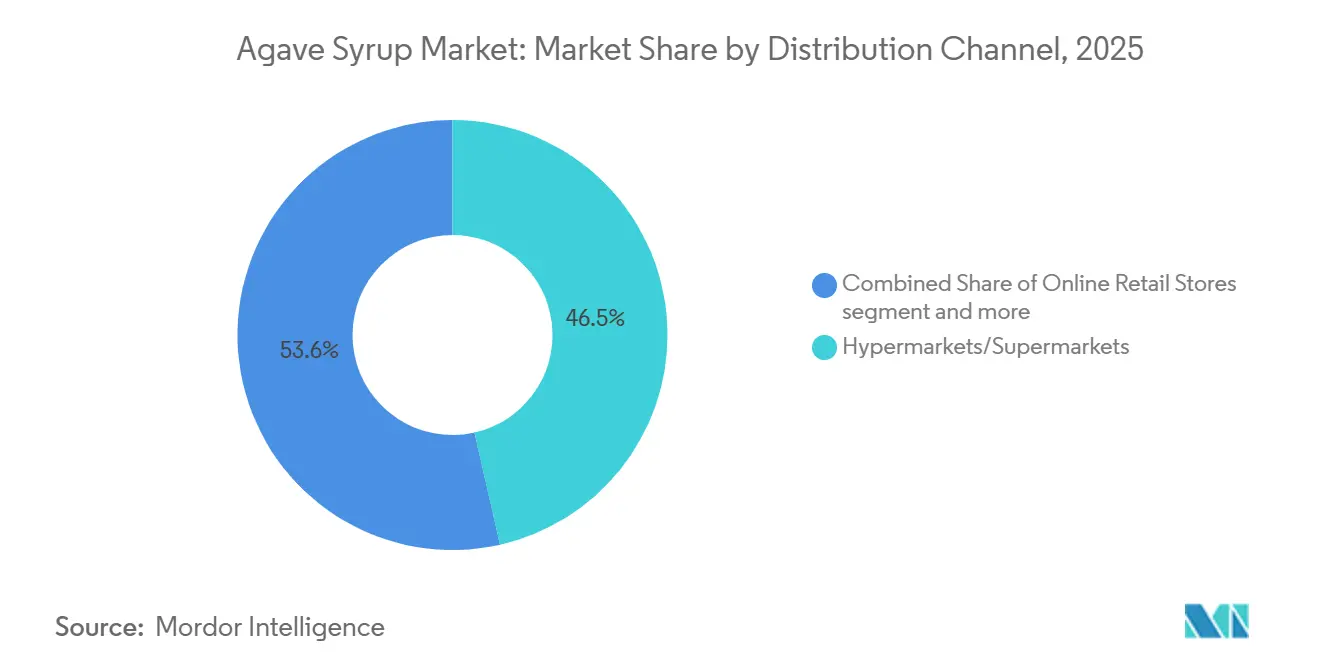

- By distribution channel, hypermarkets and supermarkets accounted for 46.45% sales value in 2025; online retail is the fastest-growing route at a 7.13% CAGR to 2031.

- By geography, North America led with 35.12% revenue share in 2025, while Asia-Pacific is set to record the highest regional CAGR of 6.56% over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agave Syrup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for natural sweeteners over artificial sweeteners | +0.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increasing adoption of vegan and plant-based diets | +0.6% | Global, led by North America, Europe, and Asia-Pacific urban centers | Long term (≥ 4 years) |

| Demand for clean-label and minimally processed products | +0.5% | North America and Europe, spillover to urban Asia-Pacific | Medium term (2-4 years) |

| Rising interest in organic-certified sweeteners | +0.4% | Global, strongest in North America and Europe | Long term (≥ 4 years) |

| Development of flavored agave syrups | +0.3% | North America and Europe, emerging in Asia-Pacific | Short term (≤ 2 years) |

| Rising consumer preference for sustainably sourced sweeteners | +0.4% | Global, with premium positioning in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising preference for natural sweeteners over artificial sweeteners

As regulatory scrutiny intensifies and negative media coverage mounts, consumer trust in synthetic sweeteners is declining, accelerating a shift towards natural alternatives. Agave syrup is well-positioned to benefit from the transition towards natural sugar, as it is plant-derived and requires less processing than chemically altered sweeteners. However, it faces a challenge: its high fructose content, depending on processing, undermines the health narrative that initially attracts consumers. In response, brands are introducing reduced-sugar alternatives. For example, Urban Platter offers Mexican Blue Agave Syrup, a plant-based sweetener that claims to be a natural sweetener with low carbs, low GI, and a mild flavor. This trend highlights that agave syrup's advantage lies not in directly replacing sugar but in enabling partial sugar reduction in recipes that still require bulk and browning functionality. However, as consumers become more informed about ingredients, the distinction between natural fructose and artificial high-fructose corn syrup may become less clear. This shift pushes agave producers to emphasize factors such as terroir, organic certification, and sustainable sourcing as key differentiators, rather than relying solely on the natural label.

Increasing adoption of vegan and plant-based diets

As the world increasingly embraces plant-based diets, agave syrup is emerging as a favored vegan substitute for honey. The Vegan Society highlighted the growing trend, noting that millions of individuals took part in "Veganuary" in January 2025. According to the Good Food Institute, global retail sales of plant-based foods experienced steady growth in 2024[2]Source: Good Food Institute "State of the Industry: Plant-based meat, seafood, eggs, dairy, and ingredients," gfi.org. Agave syrup, often used as a direct substitute for honey, is riding this wave of plant-based popularity. However, its adoption varies by region. In India, where a notable percentage of the population identifies as vegan and vegetarian, agave syrup faces challenges. Despite being a high-potential market, its growth is hampered by limited retail distribution and a price sensitivity when compared to local sweeteners like jaggery and date syrup. On the other hand, European nations, particularly Germany, showcase a different story. With a small but significant portion of its population adhering to a vegan diet, there's a pronounced willingness to pay a premium for certified vegan ingredients. This divergence in market dynamics suggests a tailored approach for agave syrup brands. In established vegan markets, the focus should be on flavor innovation and organic certification. Conversely, in emerging markets, the emphasis should be on affordability and matching the functionality of traditional sweeteners. However, a looming challenge persists: as plant-based diets gain mainstream traction, there's a risk that consumers might gravitate towards the cheapest vegan sweetener. This shift could undermine agave syrup's premium positioning unless producers can firmly establish its value through unique sensory attributes or strong sustainability credentials.

Demand for clean-label and minimally processed products

As consumers increasingly scrutinize not just the ingredients in their food and beverages but also the methods of production, the demand for clean labels is reshaping food choices. In Germany, a growing preference for recognizable ingredients and transparent sourcing has boosted the appeal of agave syrup. This trend gains momentum in the European Union, where Regulation 1169/2011 mandates thorough ingredient disclosure and allergen labeling. The production of agave syrup, which involves the extraction of aguamiel from agave plants, enzymatic hydrolysis, and concentration, utilizes fewer chemical inputs compared to refined cane sugar or corn syrup, branding it as a minimally processed alternative. Yet, the category grapples with a credibility challenge: darker agave syrups, which undergo extended heating and caramelization, boast elevated levels of 5-hydroxymethylfurfural. This compound, a byproduct of thermal processing, stands in stark contrast to the "minimally processed" claim. Addressing this dilemma, brands like The Groovy Food Company, Matcha Agave in the United Kingdom are blending agave syrup with functional ingredients like matcha. This strategy not only differentiates their products but also justifies a premium price tag through health benefits rather than mere processing claims. The key opportunity lies in transparency: brands that openly share third-party audits of their production and ingredient sourcing can command higher prices, especially in markets where skepticism towards clean labels is on the rise. However, there is a looming risk: as consumer awareness deepens, terms like "natural" and "minimally processed" may be seen as mere marketing ploys, not regulated standards. This shift could push agave producers to compete on tangible attributes like organic certification, fair trade status, or carbon footprint, rather than ambiguous claims.

Rising interest in organic-certified sweeteners

Organic certification is evolving from a niche differentiator to a standard expectation in premium sweetener categories. Under the United States Department of Agriculture (USDA) Organic standards (7 CFR Part 205), agave syrup must be produced without synthetic pesticides, genetically modified organisms (GMOs), or prohibited processing aids. Meanwhile, European Union (EU) Regulation 2018/848 not only mandates traceability but also restricts certain extraction methods[3]Source: Electronic Code of Federal Regulations (eCFR) "PART 205—NATIONAL ORGANIC PROGRAM," ecfr.gov. Organic agave syrup is experiencing faster growth compared to its conventional counterpart. This surge is bolstered by retailers like Whole Foods Market and Trader Joe's broadening their organic selections, alongside consumers willing to pay significant premiums for certified products. Mexico's Consejo Regulador del Tequila, overseeing blue agave cultivation across Jalisco and four other states, has rolled out sustainability protocols echoing organic principles. These include limiting herbicide use and emphasizing soil conservation. Such standards pave the way for tequila producers to branch into organic agave syrup, capitalizing on their existing certification systems and agronomic know-how. However, a hurdle remains: organic certification mandates a three-year transition for land once treated with synthetic inputs. This creates supply constraints, curbing short-term volume growth. Brands locking in long-term contracts with certified organic agave growers can secure their supply and benefit from widening organic premiums. In contrast, those dependent on spot markets risk volatility as demand surpasses certified acreage. Strategically, vertical integration or forming cooperatives with smallholder farmers may offer a more stable route to organic supply security than mere transactional procurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising concerns about high fructose content in agave syrup | -0.7% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Increased preference for alternatives like stevia, monk fruit, and coconut sugar | -0.6% | Global, led by health-conscious segments in developed markets | Long term (≥ 4 years) |

| Stricter regulations on labeling and health claims | -0.3% | Europe and North America, with emerging scrutiny in Asia-Pacific | Short term (≤ 2 years) |

| Growing skepticism about healthy sweetener claims | -0.4% | Global, strongest in markets with high nutrition literacy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising concerns about high fructose content in agave syrup

Recent clinical evidence linking high fructose intake to metabolic dysfunction is challenging the health claims traditionally associated with agave syrup. A recent study highlighted that agave syrup's fructose content, depending on processing, surpasses that found in high-fructose corn syrup. This revelation has raised alarms about potential health issues, including dental caries, insulin resistance, and non-alcoholic fatty liver disease. Harvard Health Publishing emphasized that fructose, distinct from glucose, sidesteps insulin-mediated pathways. Instead, it is predominantly metabolized in the liver, where excessive intake can lead to fat production and an accumulation of triglycerides. These insights challenge previous marketing claims that touted agave syrup as a low-glycemic alternative to table sugar. As a result, brands are now shifting their messaging focus from health benefits to culinary uses. However, there's a strategic dilemma: consumers who once embraced agave syrup for its supposed health advantages might completely forsake it upon learning of its fructose content, rather than merely transitioning to reduced-sugar alternatives. The looming concern is that as nutritionists and dietitians increasingly recommend curbing all added sugars, agave syrup risks losing its unique standing against conventional sweeteners, leading to potential commoditization.

Stricter regulations on labeling and health claims

Brands are now compelled to back their marketing claims with clinical evidence due to tightening regulations on sweetener labeling and health assertions. The European Food Safety Authority's Regulation 1924/2006 mandates that nutrition and health claims must be underpinned by peer-reviewed studies showcasing significant benefits. Similarly, the United States Food and Drug Administration, in a draft guidance released in January 2025, emphasized that plant-based sweeteners shouldn't suggest a health edge over traditional sugars without backing from randomized controlled trials. These stringent standards impose compliance costs on agave syrup brands, which had previously leaned on terms like "natural" or "raw" to hint at health benefits. The challenge lies in the significant expense of clinical trials, making it a daunting task for smaller producers. In contrast, larger entities like Wholesome Sweeteners, which was bought by Whole Earth Brands for a substantial amount, can spread these regulatory costs across a wider product range, giving them a competitive edge and potentially speeding up market consolidation. As regulators intensify their scrutiny of unsupported claims, agave syrup brands might find themselves competing primarily on price and availability. This shift could squeeze profit margins and diminish the allure of quality differentiation. However, brands that take the initiative to invest in third-party testing and clear labeling, such as revealing fructose-to-glucose ratios and glycemic index values, stand to gain consumer trust. Such transparency might also open doors to retailer wellness programs, boosting their distribution reach.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dark Variants Capture Premium Demand

Dark agave syrup is expected to grow at a CAGR of 6.02% through 2031, outpacing the overall market even as light agave syrup held a 66.43% market share in 2025. Chefs and mixologists are increasingly choosing dark agave syrup for its caramel and molasses flavor notes. Its culinary appeal lies in its ability to enhance marinades, glazes, and cocktails without the sulfurous undertones of molasses or the overly sweet profile of light agave syrup. This unique flavor profile allows dark agave syrup to command a premium price, where its flavor intensity and visual appeal justify higher costs. On the other hand, light agave syrup remains dominant due to its neutral flavor, which makes it an ideal substitute for honey or sugar as it is used in cooking without altering the original taste. The processing methods differ significantly, as light agave syrup is filtered and minimally heated, while dark agave syrup undergoes extended heating that caramelizes sugars and deepens its color. This creates a trade-off between clean-label positioning and flavor intensity.

Amber agave syrup, positioned between light and dark variants, holds a small but stable niche in the natural foods retail sector. It appeals to consumers who prefer moderate flavor without the intensity of dark syrup. However, a key challenge is educating consumers about the differences between light, amber, and dark agave syrups. Retail buyers may not fully recognize these distinctions, leading to stock-keeping unit (SKU) rationalization that favors the dominant light variant. Brands that invest in point-of-sale materials and recipe content to showcase the unique use cases for each syrup type can protect their shelf space and capitalize on premiumization opportunities. However, as private-label agave syrups become more prevalent in mainstream grocery stores, there is a risk that differentiation will simplify into a basic light-versus-dark comparison. This shift could eliminate the middle-tier amber syrup, forcing brands to either compete on price with the light variant or adopt a premium positioning similar to dark syrup.

By Category: Organic Certification Drives Premiumization

Organic agave syrup is expected to grow at a CAGR of 6.34% through 2031, outpacing conventional products, which held an 82.11% market share in 2025. This growth highlights the development of organic supply chains and the commitment of premium retailers to allocate shelf space to certified products that align with their wellness-focused branding. The United States Department of Agriculture (USDA) Organic certification, under 7 CFR Part 205, requires agave plants to be grown without synthetic pesticides or fertilizers for at least three years before harvest. Additionally, processing must avoid prohibited substances such as sulfites and synthetic enzymes. Similarly, the European Union (EU) Regulation 2018/848 enforces stricter traceability requirements, ensuring that organic agave syrup is traceable from the field to the finished product through batch coding and third-party audits. While these standards protect certified producers from low-cost competition, they also create supply constraints, as organic producers cannot quickly expand acreage due to the three-year transition period required for certification.

Conventional agave syrup continues to dominate, primarily serving price-sensitive markets, where organic certification does not significantly influence purchasing decisions. A strategic opportunity exists in adopting a hybrid approach, where brands offer both organic and conventional options. This strategy allows companies to capture premium-tier retail markets. Brands are differentiating themselves by obtaining additional certifications, such as Fair Trade, Rainforest Alliance, or Regenerative Organic Certified, which can help maintain premium positioning even as baseline organic certification becomes more common.

By Raw Material: Salmiana Agave Expands Beyond Blue Agave

In 2025, blue agave dominated the retail agave syrup market, holding a commanding 78.84% share. This dominance is a testament to consumer familiarity and the ubiquitous presence of blue agave syrups on supermarket shelves. Shoppers often link blue agave with a clean, neutral taste, solidifying its status as the go-to choice for sweetening beverages, baking, and general household use.

Meanwhile, salmiana agave is on the rise, projected to grow at a 5.68% CAGR through 2031. This growth presents retail brands with a golden opportunity to diversify their product offerings. Thriving in the semi-arid highlands of central Mexico (specifically in Hidalgo, Puebla, and Tlaxcala), salmiana boasts a higher yield of aguamiel per plant, which can be transformed into syrup. Marketed as a distinctive, artisanal alternative, salmiana syrups offer a flavor profile that's slightly more vegetal and robust than blue agave. This unique taste appeals to consumers seeking authenticity and a regional identity. While its pronounced flavor might limit its use in neutral-preferred categories, it carves out a niche for premium positioning in retail.

Other agave varieties, like Agave atrovirens and Agave angustifolia, remain on the fringes of the retail market. Their limited processing infrastructure and low consumer recognition hinder their growth. Unlike more regulated categories, agave syrup production grants brands the leeway to experiment with alternative species. While this flexibility fosters innovation, it also poses challenges: non-blue agave syrups often grapple with less established quality standards and traceability protocols, heightening the risk of inconsistent product quality.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Online retail stores are expected to grow at a CAGR of 7.13% through 2031, making it the fastest-growing distribution channel. In comparison, hypermarkets and supermarkets held a 46.45% market share in 2025. This shift highlights the increasing adoption of e-commerce in the food and beverage sector, a trend accelerated by the pandemic-driven shift to online grocery shopping. The convenience of subscription models and the emergence of direct-to-consumer brands have further sustained this growth. Brands such as Madhava Natural Sweeteners and NOW Health Group have strategically invested in Amazon storefronts and direct-to-consumer websites. By bypassing traditional retail intermediaries, these brands not only achieve better profit margins but also build direct relationships with their customers. The key advantage of online channels lies in their ability to capture valuable data, enabling brands to track purchase frequency, basket composition, and customer demographics. These insights are critical for product development and targeted marketing, capabilities that are not available through wholesale distribution.

Convenience and grocery stores continue to hold a stable but slow-growing segment, catering to impulse purchases and quick shopping trips. However, the premium positioning of agave syrup limits its trial in these channels. Other distribution channels, including natural foods stores, club stores, and others, account for the remaining market share and serve distinct customer groups. Natural foods stores attract health-conscious consumers who are willing to pay a premium for organic and specialty products, while club stores like Costco appeal to bulk buyers. As online retail expands, traditional retailers are increasingly demanding exclusivity or private-label partnerships to protect their market share.

Geography Analysis

The North America region dominated with a 35.12% of the market share in 2025, buoyed by Mexico's status as the top agave producer and the U.S.'s well-established specialty foods retail scene. In the United States, retailers like Whole Foods and Sprouts prominently feature organic sweeteners, while Canadian chains such as Loblaws and Metro are broadening their distribution in response to a surge in plant-based diet interest. However, with specialty retail nearing saturation, brands are shifting to mainstream grocery outlets, where they face heightened competition from private-label sweeteners.

Asia-Pacific is projected to grow at a 6.56% CAGR through 2031. This surge is attributed to rising disposable incomes, the expansion of modern retail, and a growing consumer preference for clean-label imports. While China's burgeoning middle class drives demand for premium sweeteners, agave syrup finds itself in competition with local favorites like maltose and date syrups. In India, a vast vegetarian and vegan populace presents a lucrative opportunity, yet challenges like price sensitivity and sparse retail distribution persist. Japan's specialty food market is increasingly embracing organic and flavored syrups, and in Australia, major chains like Woolworths and Coles are bolstering agave syrup's retail footprint through strategic supplier partnerships.

Europe, with Germany, the UK, France, and the Netherlands at the helm, remains a pivotal retail market for agave syrup. The EU Regulation 1169/2011, which champions ingredient transparency, plays to agave syrup's advantage due to its straightforward profile. Germany's penchant for organic products amplifies the demand for certified syrups, and in the UK, specialty food retailers such as Waitrose and Sainsbury's are showcasing premium agave variants. With Europe's ongoing clean-label and organic trends, agave syrup is increasingly viewed as a wholesome alternative to refined sugar, ensuring its steady retail growth.

Competitive Landscape

The global retail agave syrup market boasts a diverse landscape, featuring both multinational natural sweetener giants and regional specialists. In North America, leading brands like Wholesome Sweeteners, Madhava Natural Sweeteners, and Agave In The Raw (Cumberland Packing Corp.) command significant shelf space. These players, bolstered by robust distribution networks, have forged strong ties with both mainstream grocery outlets and specialty retailers. By prioritizing organic certifications, fair-trade sourcing, and a clean-label approach, they've not only garnered consumer trust but also managed to uphold premium pricing amidst fierce competition.

Across Europe, brands such as Clarks UK Ltd. and The Groovy Food Company have successfully carved out their niches. By championing sustainability and transparency, they've aligned closely with EU regulations on ingredient disclosure. These European brands, often emphasizing regional authenticity and organic credentials, predominantly compete in specialty and premium retail channels. On the other hand, Mexican producers like The IIDEA Company and Nekutli Agave Nectar are making waves on the international stage. By leveraging fair-trade and origin-centric branding, they're setting themselves apart in the bustling retail arena.

In the Asia-Pacific region and other emerging markets, nimble and innovative brands like BEVS in India and Gerard Family Foods in Australia are making their mark. Targeting urban consumers, they're finding success through both modern retail chains and online platforms. While global titans maintain their dominance, these local entrants are adeptly customizing their product positioning. Whether it's emphasizing vegan attributes in India or spotlighting functional health claims in China, they're resonating with regional preferences. The competition in the retail agave syrup market is heating up. Established brands are fiercely guarding their premium status, while newcomers are carving out their space with a focus on affordability, flavor innovation, and savvy digital retail strategies.

Agave Syrup Industry Leaders

-

The IIDEA Company

-

Wholesome Sweeteners Inc.

-

Madhava Natural Sweeteners

-

Agave In The Raw

-

Clarks UK Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The Groovy Food Company, a United Kingdom-based natural food brand, unveiled its latest offering: Organic Matcha Agave. Touted as a pioneering innovation in the UK market, Organic Matcha Agave seamlessly blends the trendy premium matcha with The Groovy Food Company's signature natural agave syrup. This new product not only delivers a clean energy boost but also imparts a subtle green tea flavor, making it an ideal addition to iced coffees, hot beverages, porridge drizzles, or smoothie blends.

- July 2025: Beso de Agave, the agave syrup brand from The Romantic Agave Company, forged a partnership with Las Espirituosas, marking its inaugural entry into the Mexican market. Crafted in Jalisco, Mexico, Beso de Agave is designed to elevate the flavor and aroma of cocktails.

- March 2023: Monin Americas announced the release of their brand-new Spicy Agave Sweetener, made from organic agave specially blended with Hatch and Guajillo chiles.

Global Agave Syrup Market Report Scope

Agave syrup (also called agave nectar) is a natural sweetener made from the sap of the agave plant, primarily species such as Agave tequilana (blue agave) and Agave salmiana. It is a liquid sweetener, slightly thinner than honey, with a high fructose content that makes it taste sweeter than table sugar.

The global agave market is segmented by type, category, raw material, distribution channel, and geography. By type, the market is segmented into light and dark. By category, the market is segmented into organic and conventional. By raw material, the market is segmented into Blue Agave (A. tequilana), Salmiana Agave, and other varieties. By distribution channel, the market is segmented into hypermarkets/supermarkets, convenience/grocery stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Light |

| Dark |

| Organic |

| Conventional |

| Blue Agave (A. tequilana) |

| Salmiana Agave |

| Other Varieties (Atrovirens, Angustifolia, etc.) |

| Hypermarkets/Supermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Type | Light | |

| Dark | ||

| By Category | Organic | |

| Conventional | ||

| By Raw Material | Blue Agave (A. tequilana) | |

| Salmiana Agave | ||

| Other Varieties (Atrovirens, Angustifolia, etc.) | ||

| By Distribution Channel | Hypermarkets/Supermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the agave syrup market in 2031?

The category is expected to reach USD 271.5 million by 2031, reflecting a 5.38% CAGR from 2026.

Which region will see the fastest growth for agave syrup by 2031?

Asia-Pacific is forecast to record a 6.56% CAGR due to rising disposable incomes and expanding modern retail.

How is online retail influencing agave syrup distribution?

E-commerce is growing at 7.13% CAGR, enabling direct-to-consumer sales, subscription models, and richer customer data insights.

What strategic risks do agave syrup brands face from regulators?

Stricter labeling rules in the U.S. and EU limit health claims, compelling brands to emphasize culinary functionality and sustainability.

What years does this Agave Syrup Market cover, and what is the market size in 2026?

The report covers the Agave Syrup Market study period from 2021 to 2031, with 2025 as the base year and 2026 as the current year. In 2026, the Agave Syrup Market size stands at USD 208.92 million, and the market is forecast through 2031.

Page last updated on: