Business Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

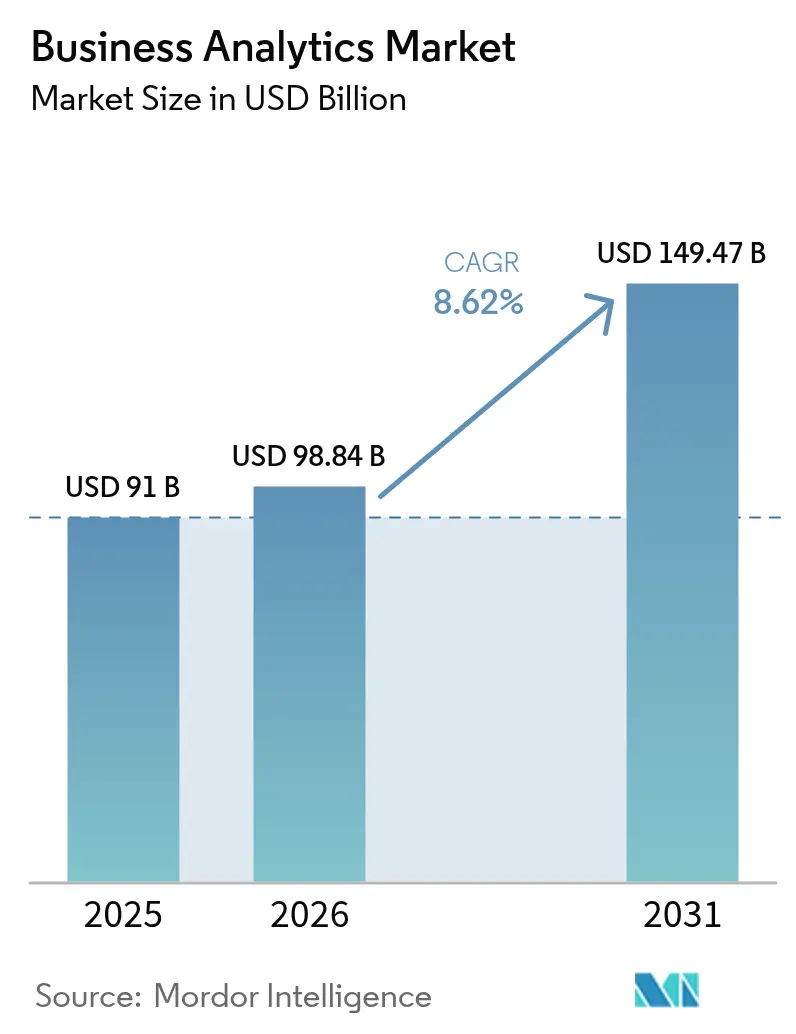

| Market Size (2026) | USD 98.84 Billion |

| Market Size (2031) | USD 149.47 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Business Analytics Market Analysis by Mordor Intelligence

The business analytics market size was valued at USD 91 billion in 2025 and estimated to grow from USD 98.84 billion in 2026 to reach USD 149.47 billion by 2031, at a CAGR of 8.62% during the forecast period (2026-2031). Cloud-native platforms, AI-driven automation, and a widespread push for digital transformation underpin this expansion. Organizations across industries now embed analytics into day-to-day workflows to uncover inefficiencies, sharpen customer engagement, and shorten decision cycles. The convergence of artificial intelligence with established analytics stacks is shifting the discipline from retrospective reporting toward real-time predictive intelligence, while pervasive cloud adoption lowers entry barriers for firms of every size. Competitive intensity remains lively as incumbent enterprise software vendors revamp portfolios to match the pace set by cloud specialists and AI-first start-ups that promise faster deployment and simpler user experiences. Talent shortages, data-sovereignty rules, and high initial costs continue to temper growth yet have not derailed the structural migration toward data-centric operations.

Key Report Takeaways

- By deployment model, the cloud segment captured 64.72% of business analytics market share in 2025 and is expanding at a 10.18% CAGR through 2031.

- By analytics type, descriptive analytics held 32.05% of revenue in 2025, while predictive analytics is forecast to grow at an 8.74% CAGR to 2031.

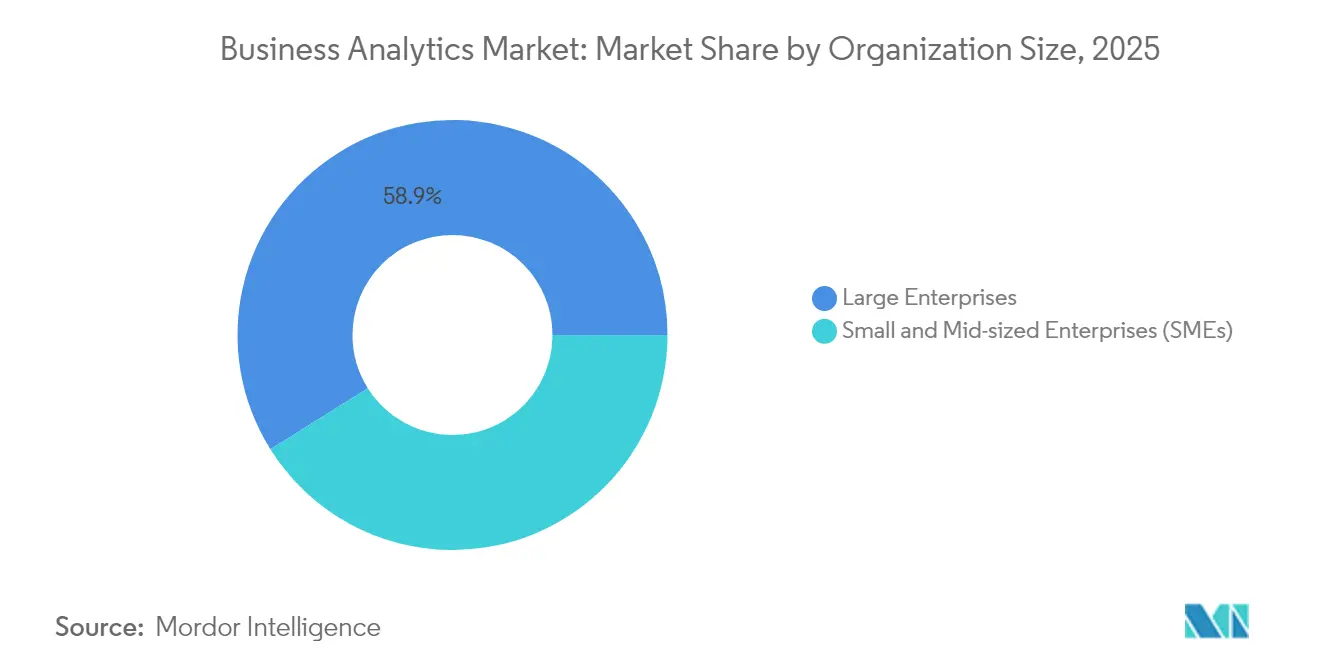

- By organization size, large enterprises commanded 58.92% share of the business analytics market size in 2025; small and mid-sized enterprises post the fastest growth at 8.98% CAGR.

- By end-user industry, BFSI led with 27.95% revenue share in 2025; healthcare and life sciences is projected to advance at a 9.31% CAGR.

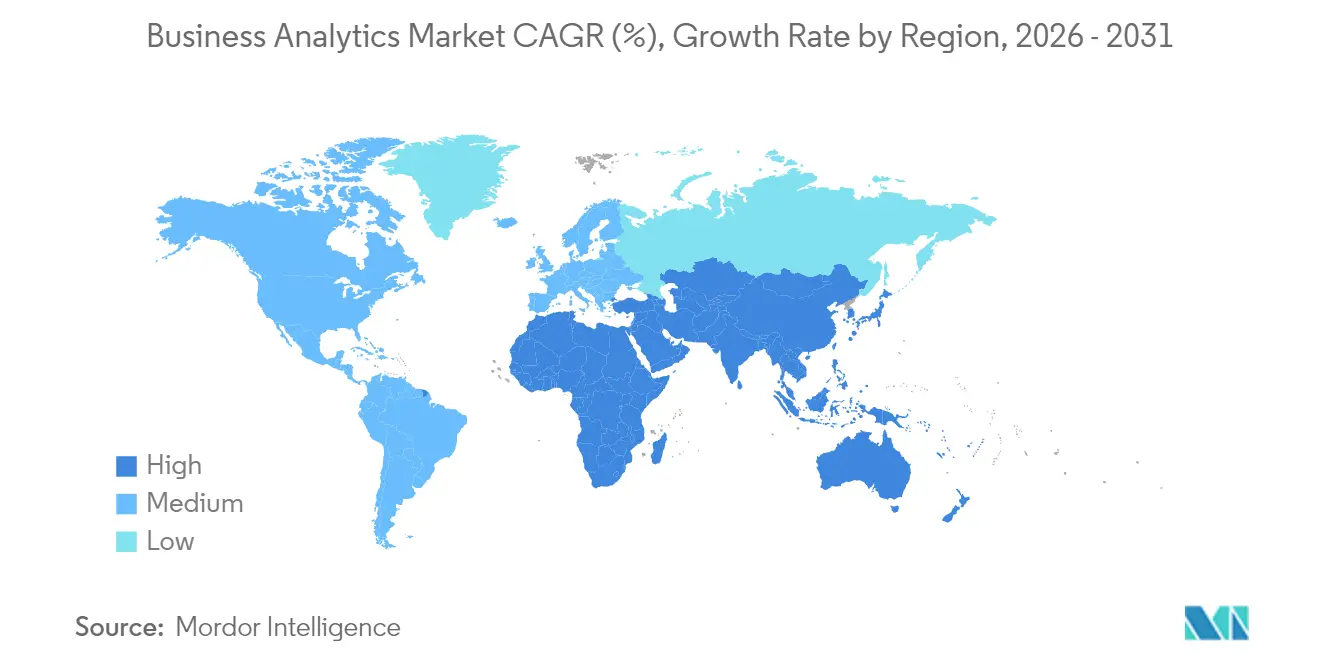

- By geography, North America retained 26.98% of global revenue in 2025, whereas Asia Pacific is on track for a 10.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Business Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of big data and cloud adoption | +2.1% | Global, with North America and Asia-Pacific leading | Medium term (2-4 years) |

| Need for real-time decision-making | +1.8% | Global, particularly manufacturing and finance sectors | Short term (≤ 2 years) |

| AI/ML infusion into analytics platforms | +2.3% | North America, Europe, and Asia-Pacific core markets | Medium term (2-4 years) |

| Regulatory push for data-driven compliance | +1.2% | Europe and North America primarily | Long term (≥ 4 years) |

| Edge analytics for IoT-heavy industries | +1.4% | Asia-Pacific manufacturing hubs, North America industrial | Medium term (2-4 years) |

| Privacy-preserving data clean rooms | +0.9% | Global, with early adoption in advertising and healthcare | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI and ML infusion into analytics platforms

Artificial intelligence has shifted from a bolt-on feature to a core capability within business analytics platforms. New releases such as Snowflake Cortex and Microsoft 365 Copilot’s Analyst agent interpret natural language, auto-generate SQL, and surface predictive insights that once required a data scientist. [1]Microsoft, “Microsoft 365 Copilot: Analyst Agent,” microsoft.com Companies adopting these capabilities report 30–50% productivity lifts in marketing, supply-chain, and finance teams. As model training costs fall, platform vendors embed generative AI to widen access and automate data preparation, ushering in an era of “agentic analytics” where autonomous agents orchestrate complex analysis pipelines without human coding.

Proliferation of big data and cloud adoption

Volume, velocity, and variety of data keep rising. More than 6,000 organizations exchange upward of 275 petabytes each week on BigQuery, highlighting how elastic cloud storage and compute have become the default substrate for analytics. [2]Google Cloud, “BigQuery Data Sharing Statistics,” cloud.google.com Joint innovation programs, such as the five-year agreement between ClickHouse and AWS, accelerate purpose-built solutions for finance and e-commerce workloads. Cloud frameworks also let firms pair localized IoT data processing with centralized dashboards, delivering 10% gains in equipment efficiency and 30% reductions in unplanned downtime in industrial settings.

Need for real-time decision-making

Competitive pressure forces businesses to treat insights as perishables. Insurers use real-time pricing to lift revenue double digits, and transport operators feed live sensor streams into traffic models that predict congestion with near-perfect precision. Edge-enabled plants trim time-to-market by one-quarter and shave hundreds of thousands of dollars off energy bills every month. Retailers similarly lean on streaming pipelines to cut inventory days while raising product availability and customer satisfaction.

Edge analytics for IoT-heavy industries

Manufacturers, utilities, and smart-city operators deploy analytics at the network edge to eliminate latency, preserve bandwidth, and respect data-protection rules. Local models inspect sensor output, flag anomalies, and act automatically. Worldwide edge spending reached USD 232 billion in 2024, and half of enterprises expect to standardize edge workflows by 2025. Secure partnerships among device makers, telcos, and platform providers anchor these projects to ensure encrypted data transfer and automated policy enforcement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost and ROI uncertainty | -1.5% | Global, particularly SMEs in emerging markets | Short term (≤ 2 years) |

| Talent shortage in advanced analytics | -1.8% | North America and Europe primarily | Medium term (2-4 years) |

| Data-sovereignty restrictions | -1.1% | Europe, Asia Pacific with cross-border operations | Long term (≥ 4 years) |

| ESG-data quality gaps | -0.7% | Global, with emphasis on regulated industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-sovereignty restrictions

Conflicting rules among GDPR, the CLOUD Act, and emerging national laws force multinationals to architect region-specific data stacks. Deployments must ensure local processing, encrypted transfers, and auditable consent, adding cost and complexity.[3]ISACA, “Data-Sovereignty Challenges in Public Cloud,” isaca.orgSovereign-cloud offerings from hyperscalers and regional providers address the issue, yet organizations still juggle multiple vendors and controls to satisfy regulators without fracturing analytical coherence.

Talent shortage in advanced analytics

Demand for data scientists, ML engineers, and analytics translators exceeds supply. Surveys show three-quarters of professionals expect the shortage to persist, eroding competitiveness. Organizations invest in reskilling, hackathons, and partnerships with universities, yet complex AI initiatives still stall when critical roles remain vacant. Low-code interfaces and automated feature engineering close part of the gap, but specialist talent remains crucial for governance and model-risk oversight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Infrastructure Drives Market Evolution

The cloud segment accounts for 64.72% of 2025 revenue, and its 10.18% CAGR means it will command an even larger slice of the business analytics market size by 2031. Lower capital expenditure, elastic scaling, and rapid integration with data lakes and AI services cement its appeal. Security certifications and automated compliance features now cover finance, healthcare, and government workloads, eroding the last strongholds of on-premise advocates.

On-premise deployments persist where strict latency, legacy integration, or regulatory mandates prevail, but their share recedes every year. Hybrid blueprints, in which sensitive workloads stay behind the firewall while burst processing moves to the cloud, offer a transitional path. Providers bundle migration toolkits, managed services, and consumption-based pricing to nudge hesitant customers toward the cloud, reinforcing its position as both market leader and growth engine.

By Analytics Type: Predictive Intelligence Reshapes Decision-Making

Descriptive analytics retained 32.05% of 2025 revenue, the largest slice of the business analytics market, yet predictive techniques outpace all categories with an 8.74% CAGR. Organizations evolve from “what happened” dashboards to forward-looking models that flag churn risk, optimize inventory, and route maintenance crews before breakdowns occur. Generative AI enhances predictive workflows by auto-coding complex time-series models and surfacing scenario simulations for non-technical users.

Diagnostic analytics serves as a bridge, explaining root causes and feeding features into forecasting algorithms. Prescriptive tools close the loop by recommending the best action under constraints such as budget or staffing. Early success stories like a consumer-products maker saving up to USD 200,000 weekly through optimized production schedules fuel wider adoption. As toolkits mature, predictive and prescriptive layers will jointly convert historical data into automated, context-aware decisions across functions.

By Organization Size: SME Growth Democratizes Analytics Access

Large enterprises continue to drive volume, holding 58.92% of 2025 revenue. They invest heavily in multi-cloud data fabrics, explainable AI, and governance frameworks that scale across business units. Yet the small and mid-sized segment grows fastest at 8.98% CAGR, propelled by low-code platforms, bundled data models, and tiered subscriptions that align with tight budgets. Customer programs granting service credits and guided onboarding compress deployment cycles to weeks rather than months.

This democratization reshapes vendor go-to-market approaches. Tools now default to natural-language queries, automated insights, and embedded training to accommodate lean IT teams. At the same time, large enterprises demand advanced features such as multi-modal data integration, lineage tracking, and policy-driven access control, sustaining a two-speed market in which ease of use and enterprise-grade governance coexist.

By End-User Industry: Healthcare Transformation Accelerates Growth

BFSI institutions captured 27.95% of 2025 spending as risk analytics, fraud detection, and regulatory reporting remain core mandates. They pursue omnichannel customer views and real-time credit scoring to differentiate services. Healthcare and life sciences, however, post the strongest outlook at 9.31% CAGR. Hospitals use predictive models to balance bed capacity and automate inventory allocation, while pharmaceutical firms deploy AI to streamline clinical-trial recruitment and optimize supply chains.

Manufacturing uses edge analytics to raise overall equipment effectiveness by double digits, and retailers employ demand forecasting to cut stockouts and markdowns. Telecom operators analyze network telemetry to predict outages and upsell value-added services, whereas utilities apply predictive maintenance to grids and pipelines. Public-sector agencies embrace data platforms for tax compliance and citizen services, while energy producers monitor emissions to meet net-zero targets.

Geography Analysis

North America holds 26.98% of 2025 revenue thanks to a mature technology ecosystem, abundant talent, and early cloud adoption. Enterprises refine existing platforms with AI accelerators, streaming pipelines, and automated governance, squeezing incremental efficiency from established data assets. The United States leads spending, and Canada leverages analytics in natural-resources and financial-services verticals. Mexico adopts cloud platforms to support export-oriented manufacturing and cross-border logistics.

Asia Pacific is the fastest-growing region at a 10.12% CAGR, fueled by government AI strategies, widespread mobile adoption, and greenfield cloud deployments. China commands 37.5% of the regional business analytics market, backed by large-scale digital payment ecosystems and industrial upgrade programs. High-growth economies such as Vietnam and the Philippines exceed 19% annual expansion as SMEs embrace SaaS analytics to leapfrog legacy systems. India, Japan, South Korea, and Thailand channel public-sector grants into workforce upskilling and data-ecosystem development, creating fertile ground for platform vendors.

Europe advances steadily underpinned by strong privacy regulations and industry digitization funding. Germany, France, and the United Kingdom deploy analytics for manufacturing efficiency and financial compliance, while southern nations expand tourism and retail analytics use cases. Sovereign-cloud frameworks and privacy-enhancing technologies address GDPR-driven demands. The Middle East and Africa benefit from smart-city agendas, especially in the Gulf states, whereas South America gains traction through cloud uptake in Brazil and Argentina, although infrastructure gaps and currency volatility temper the slope of adoption

Competitive Landscape

The business analytics market features moderate fragmentation. Top five providers account for roughly 55% of revenue, leaving a sizeable long-tail of niche specialists. Cloud hyperscalers such as AWS, Google Cloud, and Microsoft accelerate feature velocity through integrated AI services and managed data fabrics. Independent data-platform leaders Snowflake and Databricks expand ecosystems via venture arms, strategic investments, and industry solution bundles. Legacy enterprise vendors SAP, Oracle, and IBM embed AI and natural-language querying into established suites to defend installed bases.

Competition intensifies around three axes. First, time-to-value: self-service tools and automated ingestion shrink deployment from quarters to weeks. Second, unified governance: buyers insist that lineage, quality, and policy controls travel with data across clouds. Third, vertical depth: vendors pre-package financial-crime models, patient-risk scores, or production-line templates to reduce customization. Start-ups differentiate through specialist AI agents, causal inference engines, or privacy-preserving analytics, often partnering with larger platforms for distribution.

Mergers, investments, and product launches underscore the race to build end-to-end stacks. Cisco moved to acquire Splunk for unified observability and security analytics. Fivetran purchased Census to blend ETL and reverse-ETL workflows into one pipeline. Databricks took a stake in Omni to streamline BI on its Lakehouse platform. Providers also form multi-year alliances ClickHouse with AWS, for instance to co-engineer high-performance solutions for regulated industries. These actions signal ongoing consolidation even as new entrants continue to surface.

Business Analytics Industry Leaders

Oracle Corporation

IBM Corporation

SAP SE

Microsoft Corporation

Tibco Software Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ClickHouse entered a five-year strategic collaboration agreement with AWS to integrate ClickHouse Cloud with AWS services for real-time analytics solutions in finance and e-commerce.

- June 2025: Data Poem launched an AI large causal model aimed at improving mission-critical decision-making for enterprises.

- May 2025: Fivetran agreed to acquire Census, creating an end-to-end data movement platform with more than 900 connectors.

- May 2025: Press Ganey Forsta acquired InMoment to expand AI-driven experience measurement for 43,000 clients.

- April 2025: Crisp bought Atheon Analytics and ClearBox Analytics, adding 120 customers to its retail data platform.

Global Business Analytics Market Report Scope

Business analytics refers to the technologies, practices, and skills for continual step-by-step exploration and investigation of the past performance of the businesses to gain various insights and drive business strategy and planning accordingly. Companies use business analytics software for query reporting and analysis tools, advanced and predictive analytics, location intelligence, content analytics, data warehousing platforms, and enterprise performance management.

The business analytics market is segmented by Deployment (Cloud, On-premise, and Hybrid), End-user Industry (BFSI, Healthcare, Manufacturing, Retail, IT, and Telecom), and Geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| On-Premise |

| Cloud |

| Descriptive |

| Diagnostic |

| Predictive |

| Prescriptive |

| Large Enterprises |

| Small and Mid-sized Enterprises (SMEs) |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Manufacturing |

| Retail and E-commerce |

| Telecom and IT |

| Government and Public Sector |

| Energy and Utilities |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | On-Premise | ||

| Cloud | |||

| By Analytics Type | Descriptive | ||

| Diagnostic | |||

| Predictive | |||

| Prescriptive | |||

| By Organisation Size | Large Enterprises | ||

| Small and Mid-sized Enterprises (SMEs) | |||

| By End-user Industry | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Retail and E-commerce | |||

| Telecom and IT | |||

| Government and Public Sector | |||

| Energy and Utilities | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the business analytics market and its growth outlook?

The business analytics market stands at USD 98.84 billion in 2026 and is expected to reach USD 149.47 billion by 2031, equating to an 8.62% CAGR.

Which deployment model holds the largest business analytics market share?

Cloud deployment leads with 64.72% share in 2025 and is also the fastest-growing segment at a 10.18% CAGR.

Which analytics type is projected to grow fastest through 2031?

Predictive analytics shows the strongest momentum, expanding at an 8.74% CAGR as firms shift from descriptive reporting to forward-looking insights.

Why is Asia Pacific viewed as the growth engine for business analytics?

Government AI initiatives, rapid cloud adoption, and strong digital-economy expansion drive a regional CAGR of 10.12%, the highest worldwide.

What is the primary restraint hindering wider analytics adoption?

A persistent talent shortage in advanced analytics roles subtracts an estimated 1.8 percentage points from potential CAGR, delaying projects and raising costs.

Page last updated on: