Cloud Data Warehouse Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

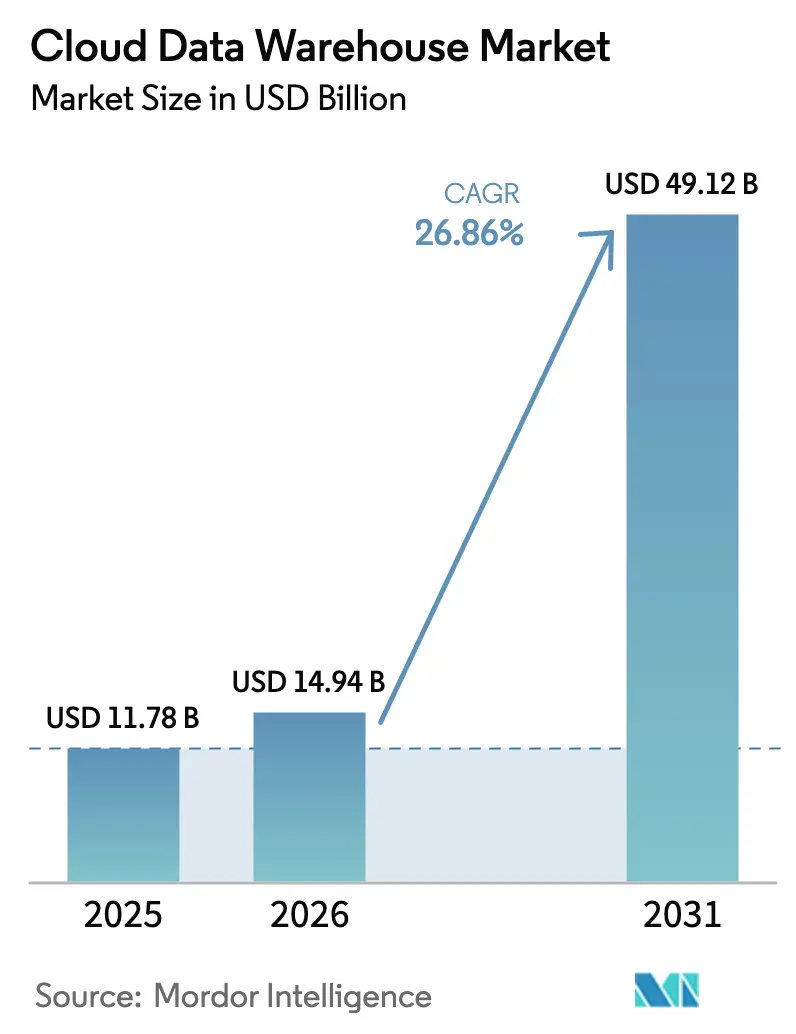

| Market Size (2026) | USD 14.94 Billion |

| Market Size (2031) | USD 49.12 Billion |

| Growth Rate (2026 - 2031) | 26.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Data Warehouse Market Analysis by Mordor Intelligence

The cloud data warehouse market size is expected to grow from USD 11.78 billion in 2025 to USD 14.94 billion in 2026 and is forecast to reach USD 49.12 billion by 2031 at 26.86% CAGR over 2026-2031. Fierce demand for real-time analytics, AI-ready data pipelines, and elastic compute power is steering enterprises away from fixed on-premises appliances toward serverless, consumption-priced architectures. Regulatory pressure, especially Sarbanes-Oxley and data-sovereignty mandates, is amplifying adoption as organizations seek unified governance across ever-larger data estates. Vendors are embedding AI services directly inside the warehouse layer, turning the platform into the operational core for predictive modelling and generative workloads rather than a passive repository. Hyperscale clouds are out-investing rivals in specialized AI infrastructure, underlining capital commitments that exceed USD 100 billion for 2025 alone. North America retains early-mover advantage, yet government-backed cloud programs across Asia-Pacific signal faster growth trajectories as localization rules spur hybrid and sovereign-cloud patterns.

Key Report Takeaways

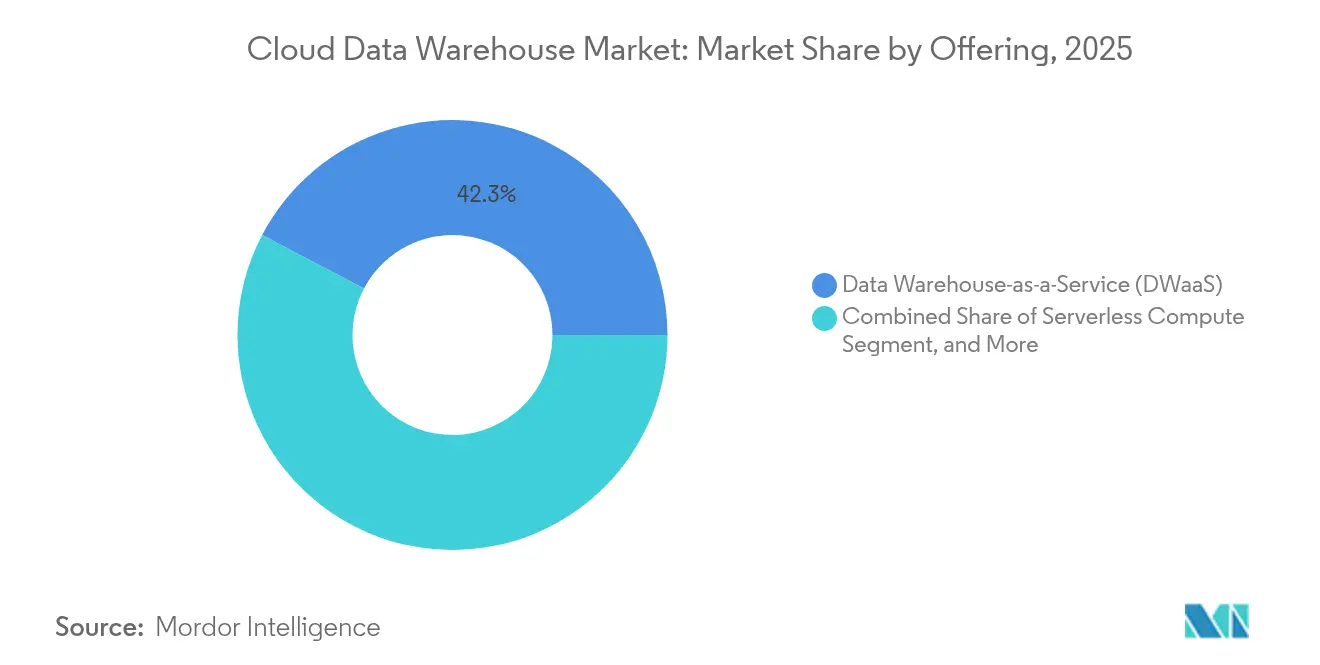

- By offering, Data Warehouse-as-a-Service led with 42.30% revenue share in 2025; serverless compute is forecast to expand at a 29.94% CAGR to 2031.

- By deployment model, public cloud held 63.92% of the cloud data warehouse market share in 2025, while the segment itself is projected to grow at 30.75% through 2031.

- By end-user industry, banking, financial services, and insurance captured 27.45% of the cloud data warehouse market size in 2025; healthcare and life sciences is advancing at a 26.95% CAGR during 2026-2031.

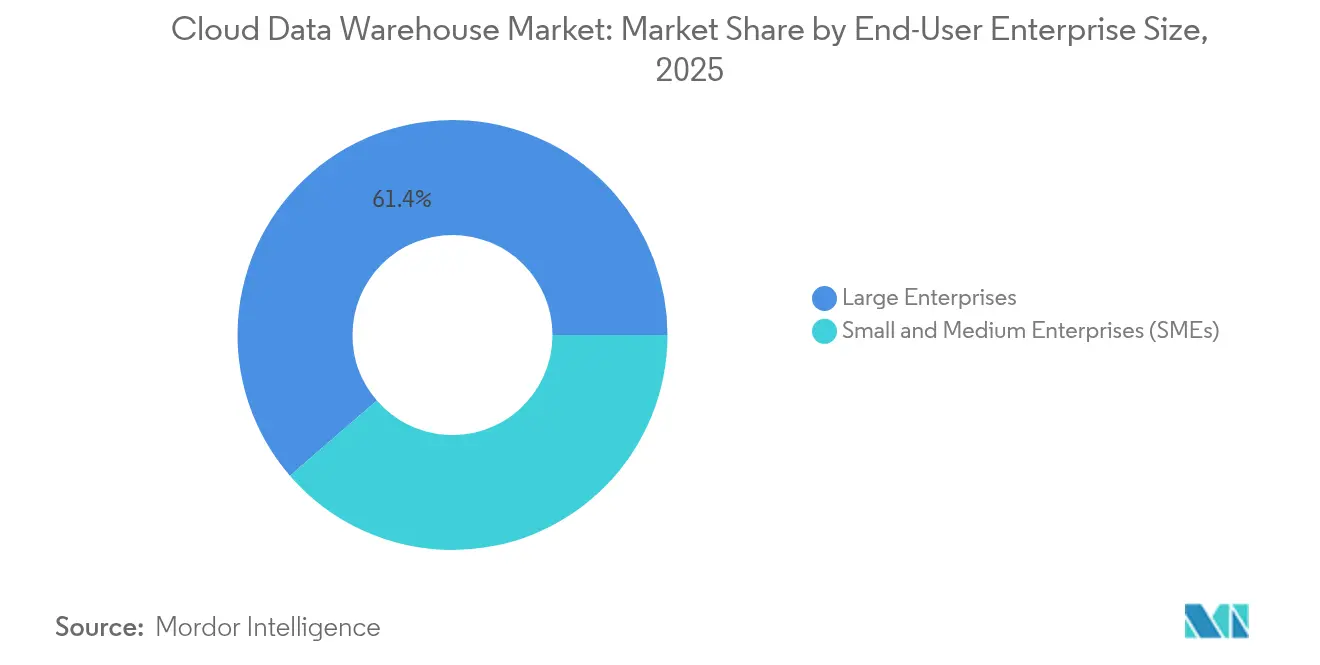

- By enterprise size, large enterprises accounted for 61.35% share of the cloud data warehouse market in 2025, whereas small and mid-sized enterprises exhibit a 31.2% CAGR outlook.

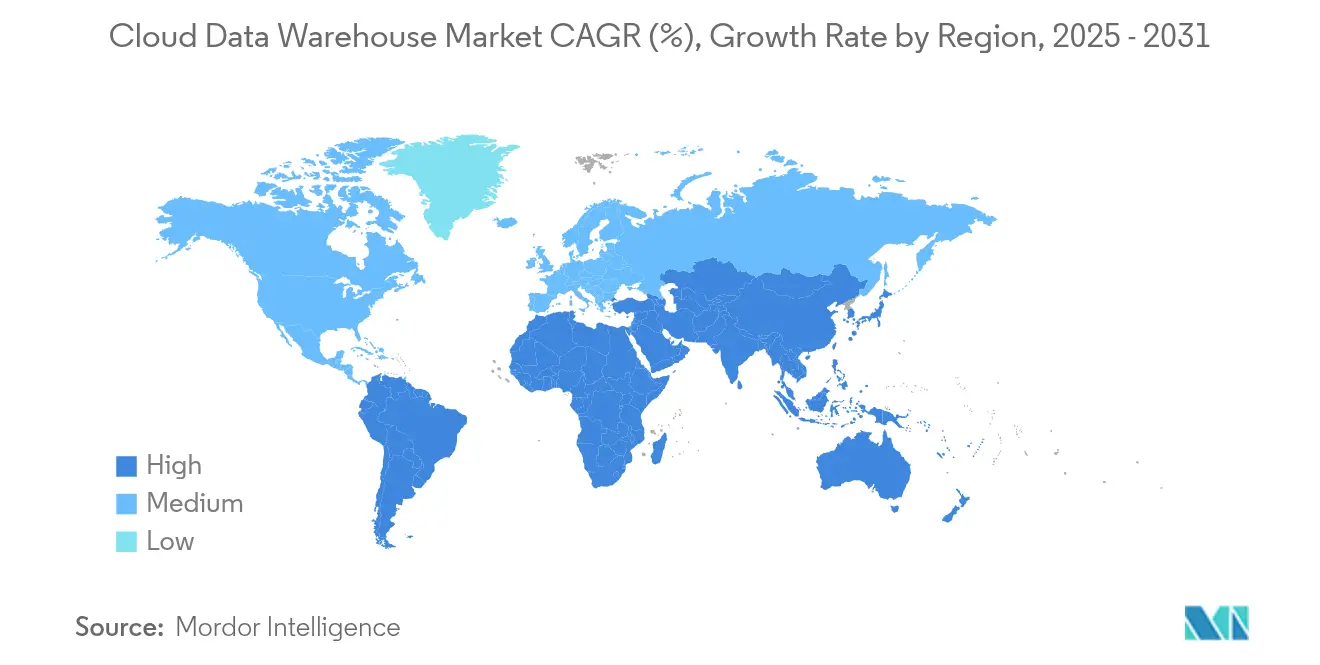

- By geography, North America commanded 46.20% of 2025 revenues; Asia-Pacific is poised for the fastest 33.6% CAGR through 2031.

- Amazon Web Services, Microsoft, Google Cloud, and Snowflake collectively represented 68% of 2024 vendor revenue.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Data Warehouse Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for advanced analytics and BI | +6.2% | North America and Europe | Medium term (2-4 years) |

| Exploding enterprise data volumes | +7.8% | Asia-Pacific-led global | Long term (≥ 4 years) |

| Cost-efficiency versus on-prem DWs | +4.5% | North America and EU | Short term (≤ 2 years) |

| Elastic scalability of hyperscale clouds | +5.1% | Global, stronger in Asia-Pacific | Medium term (2-4 years) |

| Shift to serverless pay-per-query models | +3.9% | North America expanding globally | Medium term (2-4 years) |

| ESG-grade audit trails | +2.8% | EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Demand for Advanced Analytics and Business Intelligence

Enterprises are shifting from scheduled reporting toward instantaneous insight generation, integrating machine-learning models inside the warehouse to cut data-movement latency. Azure AI services jumped 157% year-over-year in Q3 FY25 as companies embedded large language models where their data already lives, removing the need for parallel analytics stacks.[1]Microsoft Learn, “Sarbanes-Oxley Compliance in the Cloud,” learn.microsoft.com Financial institutions now trigger millisecond fraud-detection routines across petabyte stores, illustrating how compute-intensive BI workloads rely on columnar warehouses for sub-second joins. Snowflake’s joint stack with NVIDIA positions GPU-accelerated inference next to governed data, signalling that warehousing has become the foundational layer of enterprise AI strategies.[2]Snowflake, “Snowflake Announces NVIDIA Partnership,” snowflake.com Procurement teams therefore rank unified analytics-plus-AI capability above raw storage density when selecting a platform.

Exploding Enterprise Data Volumes

IoT rollouts, clickstream telemetry, and high-resolution media assets are swelling corporate datasets to exabyte scale, far exceeding economical limits of appliance-based storage. AWS disclosed a multibillion-dollar AI business that rides on surging training and inference traffic, underscoring how fast-growing data pipelines reshape infrastructure budgets. Real-time ingestion now eclipses batch ETL; Google Cloud’s AI Infrastructure revenue helped lift Q3 2024 cloud sales 35% to USD 11.4 billion, powered by customers analysing streaming data on shared storage blocks. Healthcare and manufacturing firms, compelled to keep data decades for compliance yet analyse it instantly for patient monitoring or quality control, typify this twin retention-and-speed requirement.

Cost-Efficiency Versus On-Premises Data Warehouses

Variable pricing lets enterprises match spend with query intensity, eliminating idle hardware expenses. Microsoft’s Intelligent Cloud segment booked USD 26.8 billion Q3 FY25 revenue as customers converted capital budgets to operating lines by retiring on-prem appliances. Net revenue retention of 126% at Snowflake shows organisations scaling workloads once they confirm savings from elastic allocation. Managed services further relieve enterprises of patching, capacity planning, and disaster-recovery burdens, freeing IT teams for value-added data engineering.

Elastic Scalability of Hyperscale Clouds

Separation of compute and storage underpins the ability to burst from gigabytes to petabytes without redesign. AWS earmarked USD 105 billion capex for 2025 data-centre builds optimised for AI, ensuring that capacity can be provisioned on demand for risk simulations or holiday retail peaks.[3]CNBC, “AWS to Spend $105 Billion on Data Centers for AI,” cnbc.comGoogle Cloud lets customers orchestrate analytical, transactional, and generative workloads on the same fabric, aligning resource bookings with real-time application load. Financial and retail firms that endure hourly swings in query volume value the confidence that surge traffic will not deteriorate performance or spike costs unpredictably.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security and compliance worries | -3.4% | Regulated global markets | Short term (≤ 2 years) |

| Cloud vendor lock-in risk | -2.8% | North America and Europe | Medium term (2-4 years) |

| Rising energy-use caps on hyperscale data centres | -1.9% | EU and California | Long term (≥ 4 years) |

| Sovereign-cloud fragmentation mandates | -2.1% | Asia-Pacific and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Security and Compliance Worries

Highly regulated industries hesitate to relocate sensitive datasets without airtight assurances on residency, encryption, and auditability. Sarbanes-Oxley drives strict governance, while GDPR fines intensify scrutiny of cross-border transfers. Multinationals confront a patchwork of laws such as Russia’s on-shore processing rules, compelling hybrid patterns where critical tables remain on-prem and less sensitive workloads move to the cloud. Providers counter with dedicated instances and bring-your-own-key encryption, yet perceptions of diminished control still delay large migrations.

Cloud Vendor Lock-in Risk

Proprietary storage formats and procedural SQL dialects can trap data and workloads. Snowflake’s support for Apache Iceberg and Polaris Catalog, plus Databricks’ USD 1 billion purchase of Tabular, show suppliers racing to adopt open table standards to reassure customers about exit options. Enterprises increasingly score bids on the ease of exporting data without rewrite, pushing vendors to expose industry-standard APIs and promote multi-cloud deployments that hedge dependency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Fully Managed Services Dominate while Serverless Compute Gains Pace

Data Warehouse-as-a-Service held 42.30% revenue in 2025, testament to executive demand for turnkey operations that shift maintenance to the vendor. Serverless compute expands at a 29.94% CAGR as pay-per-query charges tie spend to business value, and the cloud data warehouse market size for this segment is projected to widen sharply between 2026 and 2031. AWS commits multiyear capex to auto-scaling serverless primitives, while Snowflake integrates Cortex AISQL for natural language interactions that require no dedicated clusters. Managed governance, security, and observability add-ons round out offerings for firms short on specialised engineers.

Spending patterns illustrate a pivot from licence-plus-hardware models toward operational expenditure that flexes with data-growth curves. The cloud data warehouse market share lead held by DWaaS is under pressure as serverless models trim idle-capacity overhead and open new entry points for mid-market adopters. Providers bundle AI accelerators into the consumptive layer, monetising both storage and high-margin inference cycles.

By Deployment Model: Public Cloud’s Lead Strengthens

Public cloud deployments controlled 63.92% of 2025 revenue and will widen their advantage on a 30.75% CAGR, reflecting hyperscalers’ investment velocity and security certifications that meet or beat private alternatives. The cloud data warehouse market size tied to public instances is accelerating as Azure and Google roll out proprietary generative AI engines available only on shared infrastructure. Private and hybrid remain critical for governments or banks bound by data-residency clauses, yet growth lags because on-prem hardware refresh cycles cannot match the pace of cloud feature releases.

Strategic decisions now revolve around jurisdictional compliance rather than technology gaps. Where legislation demands local storage, sovereign regions lean on dedicated zones or local partner clouds, but even these typically expose interfaces identical to the public service. Consequently, enterprises treat private cloud as a tactical satellite to a core public strategy.

By End-user Enterprise Size: Large Organisations Still Dominate but SME Uptake Surges

Large enterprises owned 61.35% of 2025 spend, buoyed by multi-petabyte migrations and data-mesh initiatives that knit dozens of source systems into governed fabrics. Yet SMEs post a blistering 31.2% CAGR, using consumption pricing to bypass capital barriers. Asia-Pacific policy frameworks, notably India’s National Cloud effort, subsidise SME onboarding costs and amplify regional traction.

For midmarket firms, the cloud data warehouse industry removes expertise hurdles by packaging automation for provisioning, tuning, and security. Large enterprises gravitate to multi-cloud tactics that arbitrage performance or redundancy across providers, further enlarging average contract value once foundational data sets land in cloud stores.

By End-user Industry: Financial Services Commands Spend; Healthcare Races Ahead

Financial institutions contributed 27.45% of 2025 revenue by harnessing event-stream analytics for trading surveillance and real-time risk scoring. Healthcare leads future expansion at a 26.95% CAGR as electronic medical records, imaging, and genomic data converge on unified stores that power precision-medicine models. Using the cloud data warehouse market size benchmarks, insurers and banks continue to budget heavily for regulatory reporting engines, while life-science firms fund petabyte archives for AI-assisted drug discovery.

Manufacturers deploy predictive-maintenance routines that correlate IoT sensor feeds with historical faults, and retailers stream click-and-cart data to personalise promotions. Each vertical seeks domain-specific compliance features, driving vendors to assemble blueprints and partner ecosystems targeted at sector regulations and vocabularies.

Geography Analysis

North America anchors 46.20% of 2025 revenue, reflecting early adoption curves and headquarters proximity to major vendors. US federal cloud-first directives and Department of Defense residency rules sustain momentum for both commercial and public-sector migrations. Canadian policy requires Protected B and C data to stay onshore, fostering regional data-centre build-outs.

Asia-Pacific posts a 33.6% CAGR to 2031, catalysed by China’s USD 1 billion state cloud investment and India’s central-bank plan for domestic financial-sector cloud services. Southeast Asian nations roll out ‘Cloud First’ procurement stances, while Australia allocates budget to sovereign clouds that satisfy public-sector residency constraints. These policies funnel spend toward local availability zones, accelerating regional vendor hiring and partner ecosystems.

Europe sustains steady growth under GDPR, with enterprises valuing demonstrable audit trails and in-region encryption key hosting. France enforces retention statutes that block data export, compelling cloud providers to certify local facilities. The EU’s broader push for sovereign capabilities sees consortiums forming to create Gaia-X compliant offerings.

Middle East and Africa emerge as nascent opportunity pools; Saudi Arabia’s regulations prohibit unapproved offshoring of public-sector data, prompting investments in Riyadh-based hyperscale zones. Telecom operators in the Gulf align with US and Chinese cloud titans to co-build sovereign nodes, ensuring that latency and compliance needs are met simultaneously.

Competitive Landscape

Market concentration is moderate, with AWS, Microsoft, Google Cloud, and Snowflake aggregating 68% of 2024 revenue. AWS leverages an expansive global footprint and vertical solution kits; however, data-center hardware constraints slowed its Q1 2025 growth. Microsoft amplifies its enterprise ties and integrates AI to achieve 33% Azure growth, while Google differentiates itself through generative AI accelerators.

Strategy skews toward ecosystem expansion. Salesforce agreed to buy Informatica for USD 8 billion to integrate mesh, governance, and warehousing into its platform. Databricks spent USD 1 billion acquiring Tabular to solidify its Iceberg leadership, bridging the lakehouse and warehouse paradigms. Niche players such as Firebolt and ClickHouse carve out space in ultra-low-latency analytics, serving gaming and ad-tech cases that require millisecond response times.

Partnership models intensify as Snowflake allies with NVIDIA for GPU-accelerated AI, and SAP connects its data warehouse cloud to its enterprise resource planning stack. Multi-cloud capabilities and open table formats remain decisive differentiators as buyers stipulate exit flexibility.

Cloud Data Warehouse Industry Leaders

Amazon Web Services, Inc.

Google LLC

Microsoft Corporation

Snowflake Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Snowflake acquired Crunchy Data for USD 250 million, introducing native PostgreSQL support and broadening its AI-ready transactional footprint.

- May 2025: Salesforce signed a definitive agreement to acquire Informatica for USD 8 billion to enrich its Customer 360 data foundation.

- May 2025: Fivetran agreed to buy Census, creating an end-to-end data-movement suite with more than 900 connectors.

- September 2024: Firebolt launched its next-generation cloud data warehouse, delivering sub-second analytics with efficiency gains over previous releases.

Global Cloud Data Warehouse Market Report Scope

A cloud data warehouse is a cloud-based repository for the storage, retrieval, and manipulation of large datasets that can be used to support analytics projects. It allows organizations to store and process their data in a secure environment without additional hardware or software investments.

The cloud data warehouse market is segmented by offerings (dwaas, data storage), by deployment (public cloud, private cloud, hybrid cloud), by end-user (BFSI, IT and telecom, government, healthcare, retail, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Data Warehouse-as-a-Service (DWaaS) |

| Cloud-native Storage |

| Data Integration and ELT Services |

| Serverless Compute / Query Accelerators |

| Managed Services (Governance, Security, Ops) |

| Public Cloud |

| Private Cloud |

| Large Enterprises |

| Small and Mid-sized Enterprises |

| BFSI |

| IT and Telecom |

| Government and Public Sector |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Manufacturing |

| Media and Entertainment |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Offering | Data Warehouse-as-a-Service (DWaaS) | ||

| Cloud-native Storage | |||

| Data Integration and ELT Services | |||

| Serverless Compute / Query Accelerators | |||

| Managed Services (Governance, Security, Ops) | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| By End-user Enterprise Size | Large Enterprises | ||

| Small and Mid-sized Enterprises | |||

| By End-user Industry | BFSI | ||

| IT and Telecom | |||

| Government and Public Sector | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Southeast Asia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the cloud data warehouse market?

The market stands at USD 14.94 billion in 2026.

How fast is the cloud data warehouse market expected to grow?

It is projected to expand at a 26.86% CAGR, reaching USD 49.12 billion by 2031.

Which region leads the cloud data warehouse market?

North America leads with 46.20% share, although Asia-Pacific shows the fastest growth.

Which is the fastest growing region in Cloud Data Warehouse Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Why are enterprises adopting serverless compute in data warehousing?

Serverless models align costs with query demand and eliminate idle capacity, supporting a 29.94% CAGR in this segment

What is driving healthcare adoption of cloud data warehouses?

Electronic medical records, imaging, and genomic analytics require scalable, governed storage, resulting in a 26.95% CAGR for healthcare.

Page last updated on: