Cloud Information Technology Service Management (ITSM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

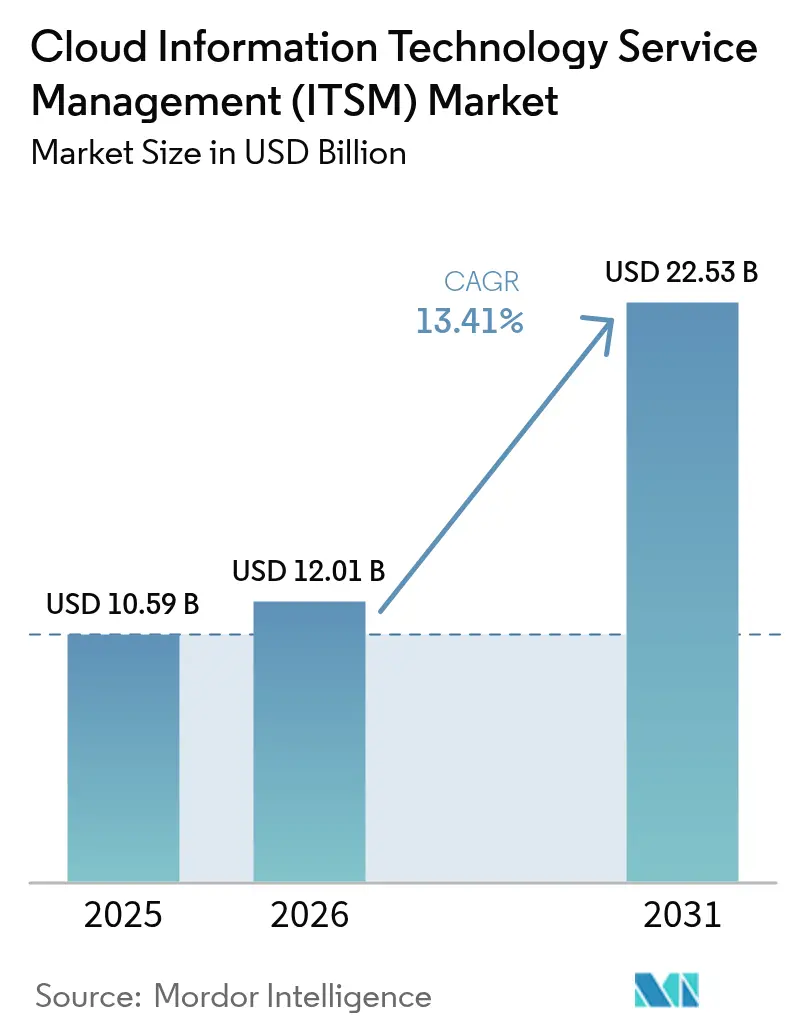

| Market Size (2026) | USD 12.01 Billion |

| Market Size (2031) | USD 22.53 Billion |

| Growth Rate (2026 - 2031) | 13.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Information Technology Service Management (ITSM) Market Analysis by Mordor Intelligence

The cloud information technology service management (ITSM) market size in 2026 is estimated at USD 12.01 billion, growing from 2025 value of USD 10.59 billion with 2031 projections showing USD 22.53 billion, growing at 13.41% CAGR over 2026-2031. Steady growth reflects the enterprise's preference for subscription models that convert capital expenses into predictable operating costs, the rising adoption of AI-driven automation that cuts mean time to resolution, and a continued shift toward multi-cloud governance. Vendors are differentiating themselves through the accuracy of predictive analytics, which already delivers 99.46% precision in incident categorization, while customers insist on tighter integration with DevOps pipelines. Cost control through FinOps, data-sovereignty rules that favor regional deployments, and mounting pressure to streamline tool sprawl remain key strategic considerations for both buyers and suppliers.

Key Report Takeaways

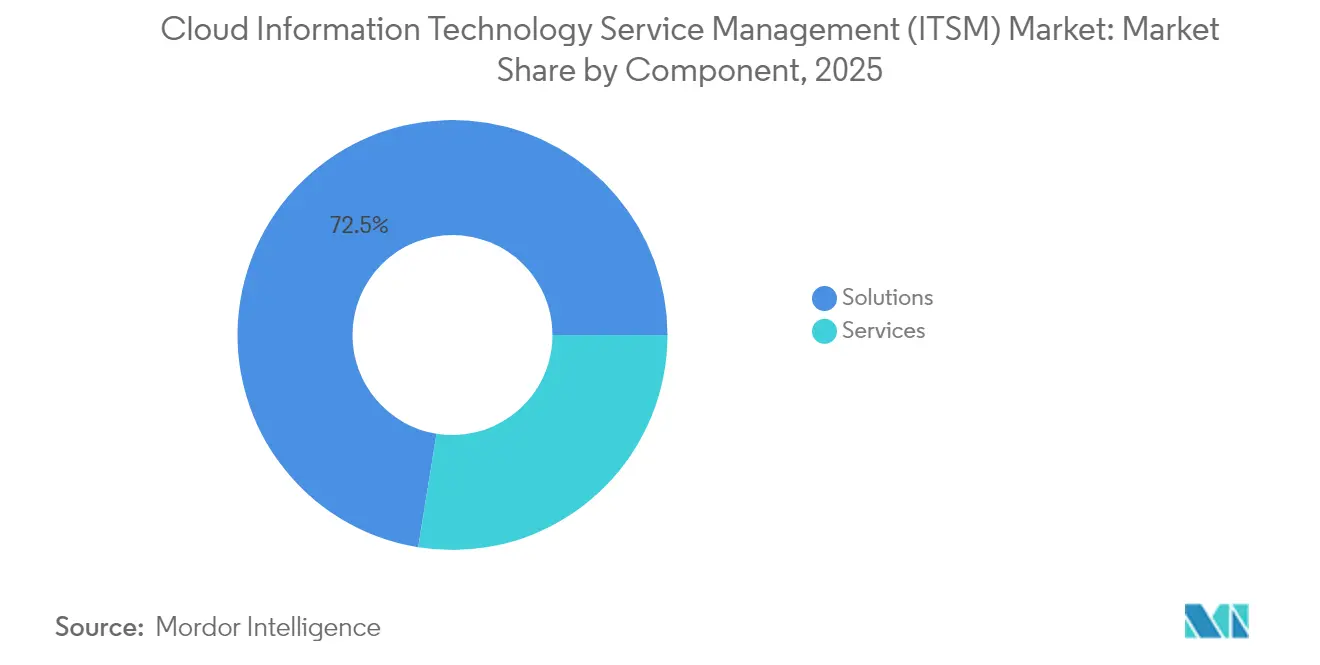

- By component, solutions held 72.45% of the cloud information technology service management (ITSM) market share in 2025, while Services are projected to expand at a 18.65% CAGR through 2031.

- By deployment model, public Cloud retained 57.30% of the cloud information technology service management market size in 2025, whereas Hybrid Cloud is expected to exhibit the fastest growth at a 16.08% CAGR to 2031.

- By organization size, large enterprises accounted for 59.20% of the cloud information technology service management market in 2025; SMEs, on the other hand, recorded the highest CAGR of 18.22% through 2031.

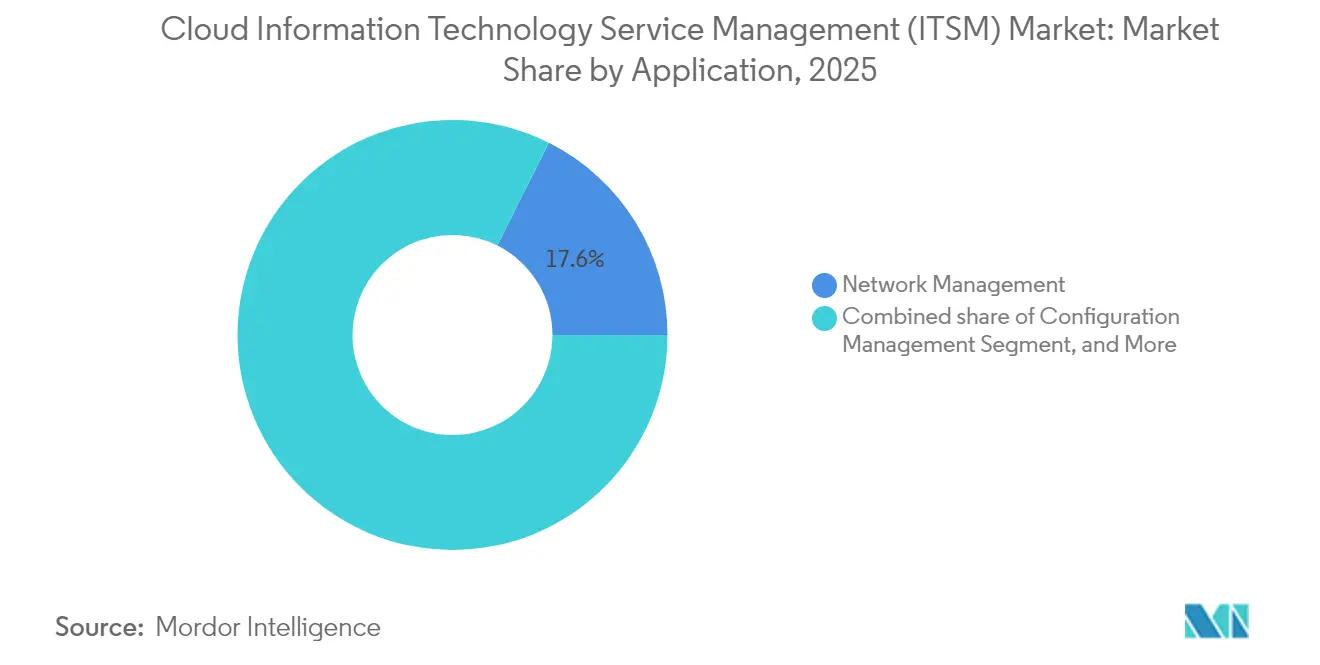

- By application, network management led the cloud information technology service management market with an 17.60% share in 2025; Service Desk and Incident Management is forecast to accelerate at a 13.92% CAGR.

- By end-user vertical, IT and telecommunications accounted for a 23.70% share of the cloud information technology service management market size in 2025, while Healthcare and Life Sciences is advancing at an 17.95% CAGR.

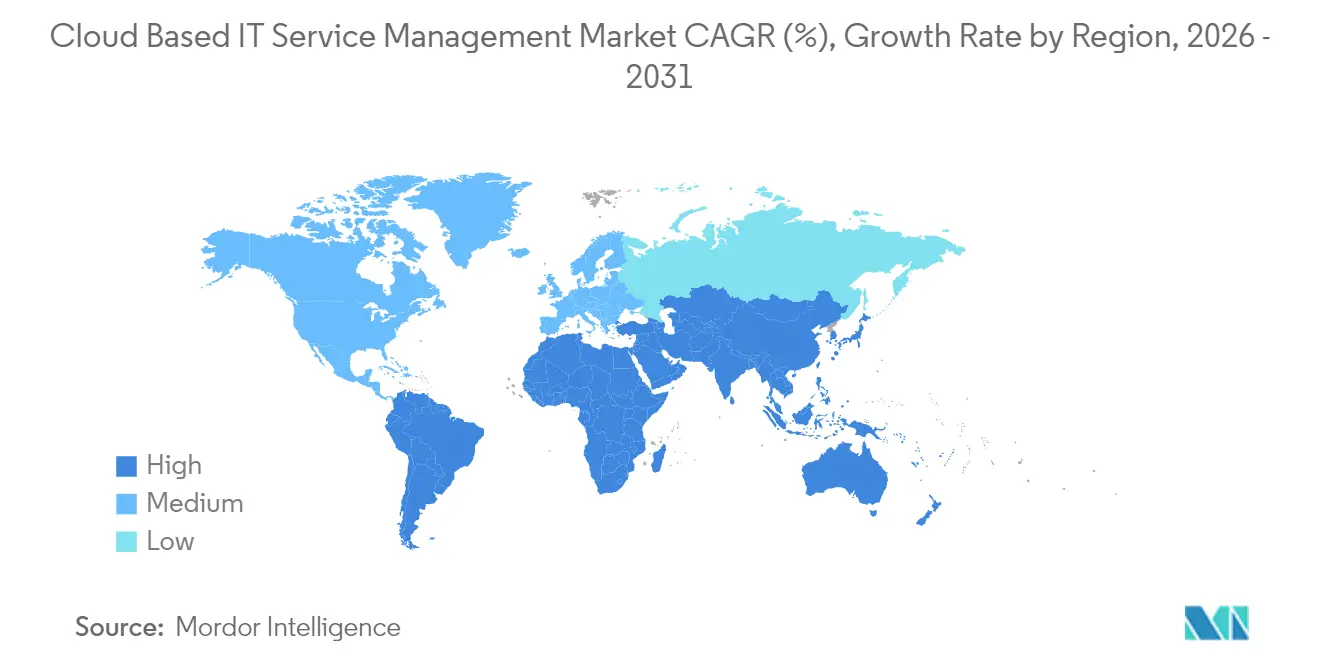

- By geography, North America represented 39.60% of the overall cloud information technology service management market in 2025; Asia-Pacific is the fastest-growing region at 17.08% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Information Technology Service Management (ITSM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Multi-Cloud Service Governance Across Distributed DevOps Teams | +2.5% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Accelerated Shift to Remote and Hybrid Work Requiring ITSM Automation | +1.8% | Global, particularly APAC and North America | Short term (≤ 2 years) |

| Proliferation of ITIL 4 Adoption Among Enterprises Driving SaaS ITSM Upgrades | +2.1% | Europe and North America core, expanding to APAC | Medium term (2-4 years) |

| Integration of AI/ML for Predictive Incident Management Reducing MTTR | +1.4% | Global, led by developed markets | Long term (≥ 4 years) |

| Subscription-Based Opex Models Preferred Over Capex Especially Among SMEs | +0.9% | Global, with strong SME adoption in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising demand for multi-cloud governance across distributed DevOps teams

Enterprises running workloads across AWS, Microsoft Azure, and Google Cloud face escalating complexity as microservices span multiple regions and providers. Unified cloud information technology service management market platforms now offer automated discovery and dependency mapping that correlate incidents across hybrid estates, allowing DevOps teams to maintain service levels without juggling point tools.[1]ServiceNow, “Q2 2024 Earnings Release,” servicenow.com Consolidating visibility enables predictive analytics on containerized applications, reduces duplicated monitoring overhead, and provides compliance reporting that satisfies auditors evaluating cross-border data flows.

Accelerated shift to remote and hybrid work requiring ITSM automation

Permanent hybrid workforces demand always-on self-service portals and AI chatbots integrated with collaboration hubs such as Teams and Slack. Modern cloud information technology service management market platforms embed natural-language virtual agents that resolve routine tickets in seconds and escalate complex issues with full context attached, trimming support queues and enhancing employee experience.[2]ManageEngine, “Hybrid Work and IT Service Automation,” manageengine.com Predictive insights flag device failures before users are disrupted, a capability viewed as essential infrastructure for dispersed operations.

Proliferation of ITIL 4 adoption driving SaaS ITSM upgrades

The ITIL 4 framework emphasizes value streams, Agile alignment, and end-to-end service orchestration. Organizations therefore migrate from legacy on-prem tools to cloud architectures that natively support the four-dimensions model and built-in continual improvement practices. Vendors respond with configurable workflows, low-code automation, and pre-built integrations that enable rapid compliance without heavy custom code.

Integration of AI/ML for predictive incident management

Machine-learning models analyze historical tickets, performance telemetry, and environmental variables to detect anomalies hours before users notice degradation. Early warning allows automated remediation scripts to execute, halving mean time to resolution and boosting customer satisfaction scores.[3]Virtana, “Predictive AIOps for Hybrid Clouds,” virtana.com Advanced NLP extracts resolution steps from unstructured notes, guiding first-level agents and increasing knowledge-base utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Residency Regulations Limiting Cross-Border Incident Data Flow | -1.2% | EU, APAC (particularly China, South Korea), emerging in other regions | Medium term (2-4 years) |

| Legacy Tool Sprawl Hindering Unified CMDB Migration to Cloud | -0.8% | Global, with higher impact in mature markets with established IT infrastructure | Long term (≥ 4 years) |

| Visibility Gaps in Highly Containerised Micro-services Environments | -1.1% | Global, concentrated in technology-forward organizations and cloud-native companies | Medium term (2-4 years) |

| Rising Cloud Opex Costs Triggering FinOps Scrutiny and Renewal Delays | -0.7% | Global, particularly impacting cost-sensitive SMEs and budget-constrained enterprises | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data residency regulations limiting cross-border incident data flow

Frameworks such as the EU’s Digital Operational Resilience Act and South Korea’s data sovereignty mandates require local storage of incident logs that may contain personal information, constraining central analytics and forcing cloud information technology service management market vendors to build regional data centers.[4]Cryptomathic, “Digital Operational Resilience Act Becomes Effective,” cryptomathic.com Multinationals deploy separate instances to comply, which increases operational costs and fragments global dashboards.

Legacy tool sprawl hindering unified CMDB migration to cloud

Large enterprises often maintain dozens of monitoring utilities accumulated over many years. Harmonizing asset records, deleting duplicates, and mapping dependencies slows transitions to a single cloud information technology service management market platform. Extended dual-run periods and custom connector development inflate migration budgets and postpone ROI.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions dominate despite services acceleration

Solutions captured 72.45% of the cloud information technology service management market share in 2025, reflecting customers priority to secure a robust platform foundation. Subscription revenues at vendors such as ServiceNow surpassed USD 2.5 billion in Q2 2024, illustrating demand for AI automation modules, workflow engines, and low-code app builders.

Services revenue is climbing at 18.65% CAGR as enterprises realize the transformation effort required to configure intelligent routing, federate CMDBs, and embed DevOps pipelines. Managed providers now offer outcome-based agreements tied to MTTR and Net Promoter Scores, transferring operational risk and assuring value delivery.

By Deployment Model: Hybrid cloud gains momentum

The public cloud is expected to represent 57.30% of the cloud information technology service management market size in 2025, driven by rapid provisioning and lower infrastructure overhead. Yet, Hybrid cloud is rising at a 16.08% CAGR because regulated sectors keep sensitive data on private nodes while exploiting public-cloud AI engines for analytics.

A hybrid stance also mitigates vendor lock-in: organizations can redirect workloads if pricing or performance shifts. Vendors, therefore, invest in portable architectures that synchronize policies across environments and respect locality constraints without duplicating administrative effort.

By Organization Size: SME adoption accelerates

Large Enterprises command 59.20% of current spending, thanks to intricate estates requiring advanced governance. However, SME uptake is expanding at an 18.22% CAGR, as low-cost subscriptions and turnkey integrations remove barriers to entry. Research shows that SMEs can cut operating costs by 20% and increase customer satisfaction by 15% after deploying cloud-based information technology service management industry solutions that automate ticket triage.

New entrants prefer all-inclusive bundles that bundle endpoint management, observability, and self-service know-how out of the box, allowing lean IT teams to focus on strategic initiatives instead of basic upkeep.

By Application: Service desk transformation drives growth

Network Management retained an 17.60% slice of the cloud information technology service management market in 2025, ensuring holistic visibility across multi-cloud networking layers. However, Service Desk and Incident Management is forecast to grow the fastest at 13.92% CAGR as conversational AI, dynamic knowledge surfacing, and intelligent routing redefine end-user support experiences.

Automated problem clustering links symptoms across microservices, expediting root cause isolation and surfacing impact analysis for stakeholders in minutes rather than hours.

By End-user Vertical: Healthcare leads digital transformation

IT and Telecommunications held 23.70% of 2025 revenue, mirroring tech firms’ appetite for continual innovation and superior customer SLAs. Conversely, Healthcare and Life Sciences exhibits an 17.95% CAGR, driven by HIPAA-aligned workflows, medical device inventories, and protected health information encryption requirements.

Specialty templates now embed compliance checkpoints, audit trails, and patient data segregation as standard features, lowering validation effort and accelerating go-live schedules for hospital systems modernizing clinical service desks.

Geography Analysis

North America contributed 39.60% of total spending in 2025, enabled by deep cloud adoption, readily available AI skills, and active partnership ecosystems between hyperscalers and platform providers. Enterprises monitor cloud bills more closely and pursue FinOps governance to validate the business value of expansions. Investment continues where automation yields measurable productivity gains, particularly in highly competitive service industries.

The Asia-Pacific region is the fastest-growing region, with a 17.08% CAGR through 2031. National digital agendas in South Korea and Singapore incentivize local data centers, while businesses adopt cloud information technology service management market platforms to comply with data residency mandates. Atlassian’s decision to offer Seoul-hosted Jira Service Management illustrates the vendor's response to country-specific rules. Rapid SME formation in India and Indonesia also contributes to the growth in volume.

Europe expands at a steady pace, shaped by GDPR and, from 2025, DORA for finance. Organizations prefer suppliers offering strong encryption, granular audit logs, and documented breach-notification workflows. Middle East and Africa join the adoption curve as government entities pursue smart-city ambitions and require resilient IT backbones. Latin America follows with moderate, cost-sensitive uptake, favoring lighter bundles that address essential incident tracking and knowledge management.

Competitive Landscape

The cloud information technology service management market shows moderate concentration. ServiceNow leads with a broad Now Platform, achieving a 23% quarterly subscription growth, and strategic alliances that embed its workflows into Microsoft Copilot and Nvidia AI models. Microsoft, IBM, and Oracle cross-sell ITSM modules into existing infrastructure footprints, strengthening stickiness.

Atlassian targets mid-market and agile teams, posting USD 4.4 billion FY 2024 revenue on the strength of Jira Service Management and integrated DevOps toolchains. Freshworks, BMC, and Ivanti differentiate on rapid deployment, vertical templates, or outcome-priced managed services. Emerging vendors compete on niche regulatory expertise and domain-specific data models that incumbents lack.

Competitive advantages are increasingly based on embedded AI accuracy, open integration frameworks, and proof points that link platform usage to quantifiable operational outcomes. Providers invest in low-code customization and marketplace ecosystems to reduce the total cost of ownership and shorten the time to value for customers shifting from legacy landscapes.

Cloud Information Technology Service Management (ITSM) Industry Leaders

IBM Corporation

BMC Software Inc.

Micro Focus International PLC

ASG Technologies Group, Inc.

Atlassian Corporation Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ServiceNow released the Xanadu update, adding generative AI copilots and automated incident remediation that reduce manual triage, positioning the firm to reinforce AI leadership in large-enterprise accounts.

- February 2025: Alpha Data PJSC secured capital to expand across the Gulf region, strengthening its end-to-end digital-transformation services that bundle ITSM with cybersecurity and cloud migration consulting.

- January 2025: The EU’s DORA framework came into force, compelling financial institutions to adopt rigorous ICT risk controls and galvanizing demand for compliant ITSM tooling with auditable incident lifecycle tracking.

- August 2024: Atlassian opened a Seoul cloud region to satisfy South Korea’s data sovereignty laws, allowing regulated customers to adopt cloud based IT service management market capabilities while keeping data in-country.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the cloud IT service management (ITSM) market as every subscription-based software platform and managed service that helps enterprises design, deliver, support, and continuously improve IT services across public, private, and hybrid cloud estates. Value is captured at end-user spend, covering core modules, incident, change, asset, request, knowledge, configuration, and self-service, plus allied automation and analytics features that ship inside the ITIL 4 framework.

(Scope exclusion: on-premises-only ITSM suites, bespoke consulting projects, and stand-alone DevOps toolchains sit outside this sizing.)

Segmentation Overview

- By Component

- Solutions

- Services

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Application

- Configuration Management

- Performance Management

- Network Management

- Database Management

- Service Desk and Incident Management

- Problem Management

- Other Applications

- By End-user Vertical

- IT and Telecom

- BFSI

- Retail and Consumer Goods

- Healthcare and Life Sciences

- Manufacturing

- Government and Public Sector

- Education

- Other End-user Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East

- Saudi Arabia

- United Arab Emirates

- Qatar

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

To validate desk findings, we interview cloud architects, enterprise service-desk leads, and MSP product heads across North America, Europe, and Asia-Pacific. These conversations test deployment patterns, average selling prices, and renewal cycles, and they flag regional nuances, such as data-sovereignty rules in Europe, that shape adoption curves.

Desk Research

Mordor analysts first comb publicly available, high-trust sources such as U.S. Bureau of Labor Statistics, Eurostat cloud-computing adoption files, OECD ICT indicators, and ITU telecom datasets, then parse sector statements from leading vendors' 10-Ks, S-1s, and earnings calls. Trade associations, including itSMF and the Cloud Industry Forum, shed light on process maturity levels, while patent analytics from Questel hint at emerging AITSM capabilities. Paid libraries like D&B Hoovers and Dow Jones Factiva round out revenue splits and M&A activity. This list is illustrative, not exhaustive; dozens of further publications underpin each model assumption.

Market-Sizing & Forecasting

We apply a top-down construct: worldwide cloud software spend is mapped, then filtered for IT operations share and finally for ITSM penetration, using inputs like licensed user counts, average seats-per-agent ratios, SaaS price bands, multi-cloud workload growth, and ITIL certification trends. Select bottom-up checks, supplier roll-ups of disclosed subscription revenues and sampled ASP-times-volume math, anchor the totals. Forecasts utilize multivariate regression where cloud workload intensity, remote-work prevalence, and AI-driven automation indices act as leading variables; scenario analysis stress-tests currency swings and macro shocks. Data gaps from privately held vendors are bridged through median ASP inference and regional channel cross-checks.

Data Validation & Update Cycle

Outputs pass three layers: automated anomaly flags, peer analyst review, and a senior sign-off. Variances above pre-set thresholds trigger re-contact with primary respondents. The model refreshes annually, with ad-hoc updates for material events such as landmark vendor acquisitions.

Why Mordor's Cloud Based IT Service Management Baseline Commands Reliability

Published figures often diverge because firms pick different scopes, base years, currency conversions, and refresh cadences. Component carve-outs, for example, excluding managed services, aggressive seat-price assumptions, or retrospective re-allocations of on-prem revenue can move totals by billions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.59 B (2025) | Mordor Intelligence | - |

| USD 9.50 B (2024) | Global Consultancy A | excludes premium support services and uses list instead of net ASPs |

| USD 9.01 B (2024) | Trade Journal B | reallocates legacy maintenance to cloud without primary validation |

| USD 4.15 B (2019) | Industry Consultancy C | dated base year and straight-line growth assumption to 2025 |

These contrasts show that, by selecting a recent base year, blending top-down penetration math with bottom-up revenue probes, and vetting every assumption through live operator feedback, Mordor delivers a balanced, transparent baseline that decision-makers can reproduce and trust.

Key Questions Answered in the Report

What is the current size of the cloud information technology service management market?

The market is valued at USD 12.01 billion in 2026 and is projected to reach USD 22.53 billion by 2031.

Which deployment model is growing fastest?

Hybrid cloud deployments show the highest growth, expanding at a 16.08% CAGR as firms balance compliance and scalability.

Why are SMEs adopting cloud information technology service management platforms rapidly?

Subscription pricing removes large upfront costs, while turnkey automation cuts operating expense by up to 20% and boosts customer satisfaction.

How do data residency laws impact vendor selection?

Enterprises operating in regions such as the EU and South Korea require vendors with local data centers or sovereign-cloud options to stay compliant.

Which application area offers the greatest growth opportunity?

Service Desk & Incident Management, driven by AI-powered virtual agents and predictive triage, is expected to grow at 13.92% CAGR.

What role does AI play in modern ITSM platforms?

AI enables predictive incident detection, automated categorization with 99% precision, and contextual knowledge recommendations that dramatically reduce mean time to resolution.

Page last updated on: