Cloud High Performance Computing (HPC) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 37.07 Billion |

| Market Size (2031) | USD 47.93 Billion |

| Growth Rate (2026 - 2031) | 5.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud High Performance Computing (HPC) Market Analysis by Mordor Intelligence

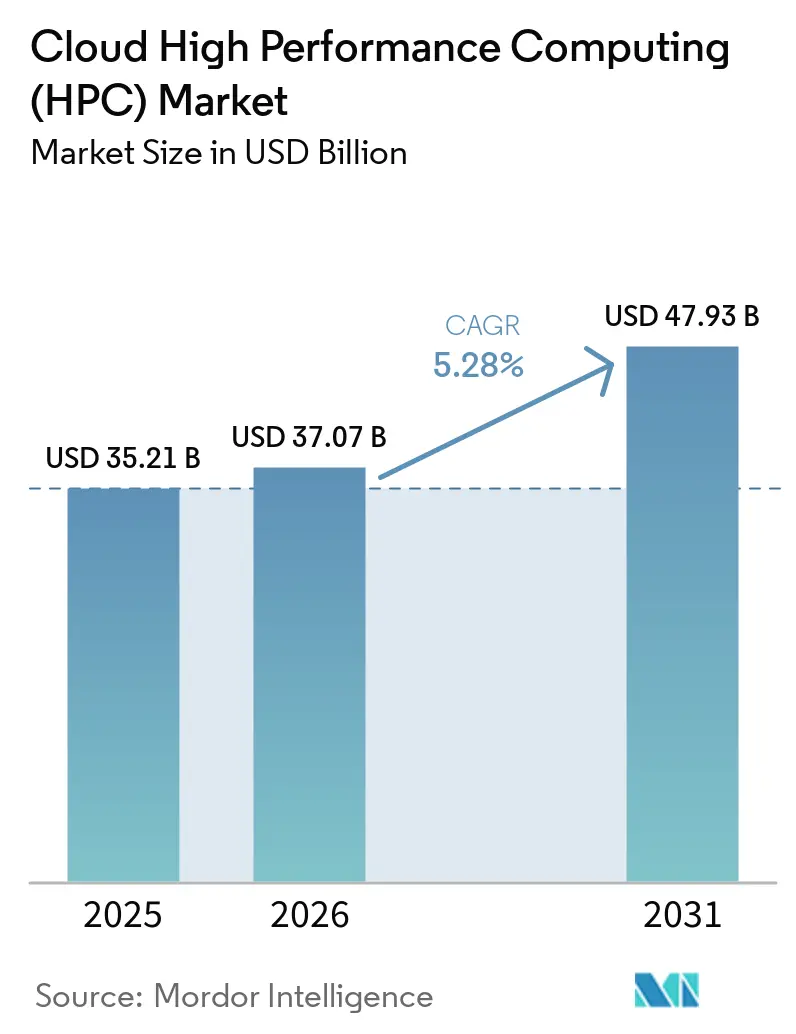

The Cloud High Performance Computing market size was valued at USD 35.21 billion in 2025 and estimated to grow from USD 37.07 billion in 2026 to reach USD 47.93 billion by 2031, at a CAGR of 5.28% during the forecast period (2026-2031). Rising migration from fixed-capacity on-premises supercomputers to elastic cloud-native clusters, coupled with the convergence of simulation and artificial intelligence workloads, underpins this steady expansion. Accelerated processors, high-bandwidth fabrics, and sophisticated orchestration software now give public clouds the raw throughput and low-latency characteristics historically reserved for purpose-built supercomputing sites. Sector stakeholders also benefit from expanding pay-as-you-go options, which lower capital barriers for small and medium-sized enterprises, and from strategic government programs that emphasize sovereign AI capabilities in North America, Europe, and the Asia-Pacific. Market participants continue to differentiate through vertical integration, custom silicon, and workload-specific platform services, driving both performance and price competition across the ecosystem.

Key Report Takeaways

- By component, hardware led with 44.12% revenue share in 2025, while software is projected to register an 8.42% CAGR through 2031.

- By deployment model, the public cloud captured a 67.95% share in 2025; the private cloud is poised for the fastest growth, at a 7.52% CAGR, through 2031.

- By service model, Infrastructure as a Service accounted for 53.85% of the Cloud High Performance Computing market size in 2025, whereas Platform as a Service is set to advance at a 7.05% CAGR.

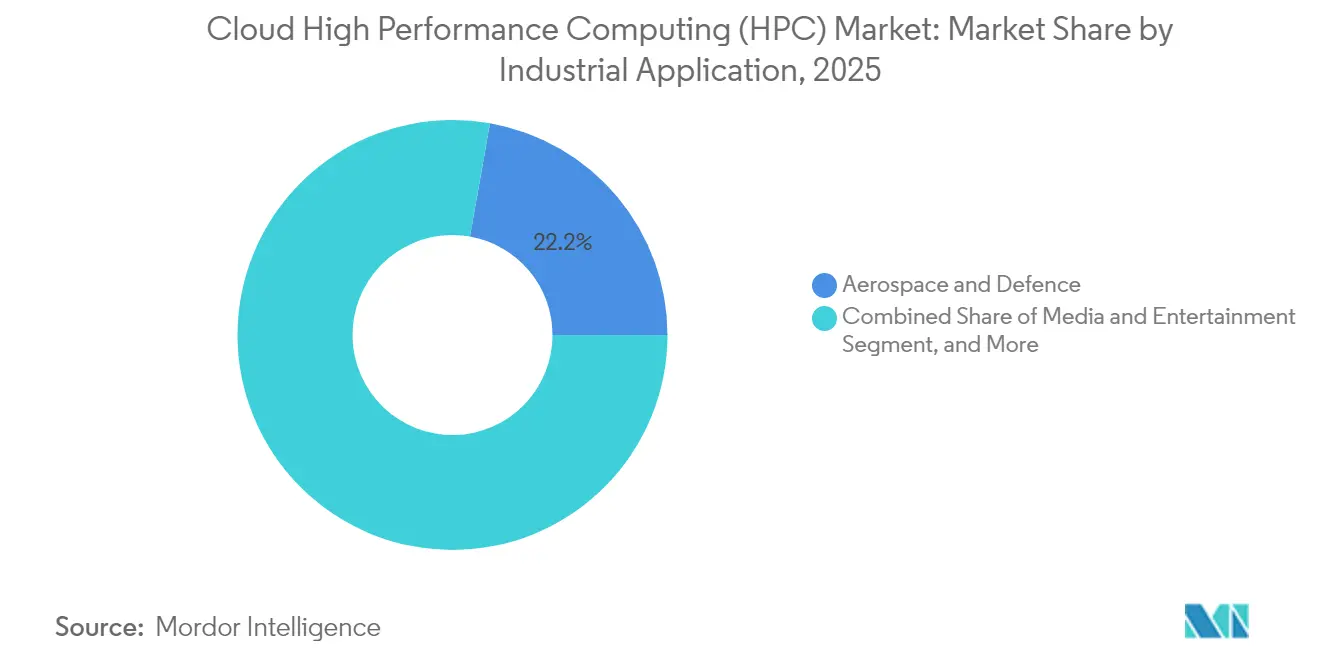

- By industrial application, the aerospace and defense sector dominated the Cloud High Performance Computing market with a 22.21% market share in 2025; the media and entertainment sector is forecast to expand at a 8.62% CAGR.

- By organization size, large enterprises held 64.15% of the 2025 revenue base, yet small and medium enterprises are projected to grow at 6.98% CAGR during 2026-2031.

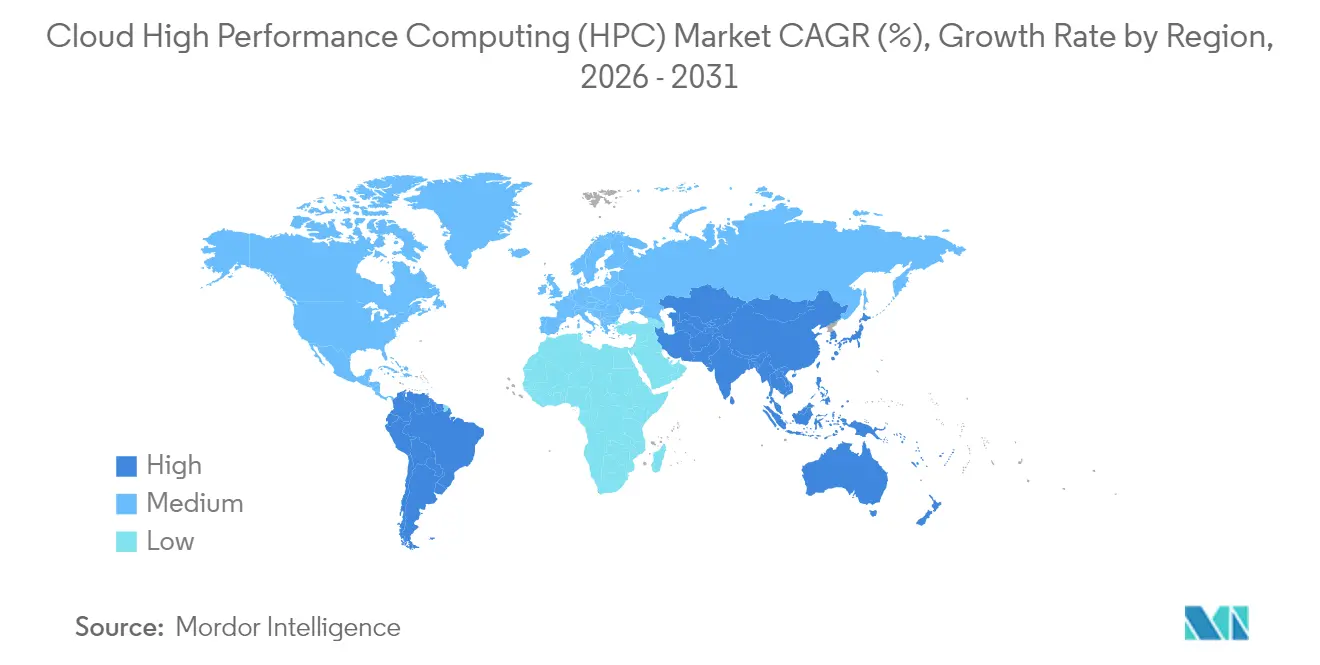

- By geography, North America remained the largest regional cluster at 39.94% in 2025, while Asia-Pacific is expected to post a 8.77% CAGR, making it the fastest-advancing territory.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud High Performance Computing (HPC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging AI and Generative Workloads in Cloud HPC | +1.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Rapid Expansion of High-Bandwidth Interconnects and Accelerators | +1.2% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Growing Adoption of Hybrid and Multicloud HPC Strategies | +0.9% | Global, with emphasis in Europe and North America | Medium term (2-4 years) |

| Increasing Availability of HPC-Optimized Cloud Instances | +0.7% | Global, with leading deployment in North America | Short term (≤ 2 years) |

| Demand for Sustainability-Focused HPC Infrastructure | +0.6% | Global, with regulatory emphasis in Europe | Long term (≥ 4 years) |

| Government-Funded Exascale and Sovereign AI Initiatives | +0.5% | North America, Asia-Pacific, and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging AI and Generative Workloads in Cloud HPC

Artificial intelligence training now consumes 40% of total cloud HPC cycles, up from 15% in 2022, a leap that reflects the compute-hungry nature of transformer-based language and vision models. Large batch sizes, distributed data-parallel algorithms, and fine-tuned hyper-parameter searches require thousands of GPUs for days at a time, conditions that correlate poorly with fixed on-premises capacity. Cloud platforms, therefore, supply elastic clusters that can be spun up for model training and spun down once validation is complete, minimizing idle capital. In 2024, Amazon Web Services released Deadline Cloud for scalable AI-assisted media rendering, signaling the depth of workload-tailored offerings.[1]Amazon Web Services, “AWS Deadline Cloud General Availability,” aws.amazon.com Defense and pharmaceutical organizations follow a similar pattern, utilizing cloud supercomputing for language-driven molecular design and autonomous vehicle perception pipelines, thereby shortening R&D loops and compressing time-to-insight.

Rapid Expansion of High-Bandwidth Interconnects and Accelerators

Next-generation fabrics, such as NVIDIA Quantum-2 InfiniBand and emerging 800-Gigabit Ethernet links, now deliver microsecond-level latency, enabling tightly coupled message-passing applications to run in the cloud without significant performance penalties. GPU advances, led by NVIDIA-based Grace Hopper superchips and Intel's Ponte Vecchio data-center GPUs, increase per-node throughput while improving energy efficiency.[2]Intel Corporation, “Ponte Vecchio GPU Architecture for Cloud HPC,” intel.comHyperscalers are increasingly integrating custom ASICs to balance compute, memory, and network flows, effectively bridging the historical gaps between commercial clouds and national lab supercomputers. These technical leaps are pivotal for weather prediction, crash simulation, and seismic imaging solutions that rely on dense, low-latency node interconnects.

Growing Adoption of Hybrid and Multicloud HPC Strategies

Enterprises are increasingly orchestrating workflows across private clusters and one or more public clouds, a trend driven by regulatory compliance, data residency requirements, and cost optimization. Platforms such as Microsoft Azure CycleCloud automate cloud bursting for peak loads, keep baseline jobs on local gear, and harmonize scheduler policies between environments.[3]Microsoft Corporation, “Azure CycleCloud for Hybrid HPC Deployments,” azure.microsoft.comFinancial institutions rely on hybrid deployment to run sensitive risk analytics in-house while shifting Monte Carlo stress tests outward, thereby scaling capacity without adding data-center footprint. Container-native workloads and open queue managers, such as Slurm, simplify transfers between vendor ecosystems, granting teams the flexibility to bid out cycles by price, geography, or carbon intensity.

Increasing Availability of HPC-Optimized Cloud Instances

Hyperscalers now offer memory-dense, bare-metal, and GPU-packed instance families tuned for genomics, computational fluid dynamics, and finite element analysis. Google Cloud’s C3D machines illustrate this trend, pairing latest-generation CPUs with high-ratio cache per core and bespoke software images to slash iterative solver times.[4]Google Cloud, “C3D Instances for Computational Workloads,” cloud.google.comSpot market auctions further democratize access by delivering transient capacity at 70-90% discounts, a boon to academic consortia and startup researchers. One-click HPC clusters, with pre-installed MPI libraries and domain-specific tools, reduce time-to-science from weeks to minutes, helping expand the Cloud High Performance Computing market across non-traditional user bases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated Cloud Egress and Data-Movement Costs | -1.1% | Global, with particular impact in data-intensive sectors | Short term (≤ 2 years) |

| Talent Shortage in Cloud-Native HPC Operations | -0.8% | Global, with acute shortages in North America and Europe | Medium term (2-4 years) |

| Export Controls on Advanced Accelerators | -0.4% | Global, with primary impact on China and restricted entities | Medium term (2-4 years) |

| Latency-Sensitive Workloads Still Favor On-Premises Clusters | -0.3% | Global, with emphasis in financial services and real-time applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Cloud Egress and Data-Movement Costs

For multi-petabyte simulations, outbound data charges can eclipse compute fees by 200%, eroding the savings realized from on-demand resources. Genomics pipelines, seismic imaging, and high-density Monte Carlo workloads repeatedly shuttle intermediate files between object stores, databases, and downstream analytics platforms, amplifying the egress bill with each iteration. While hyperscalers have introduced reduced-tariff research channels and offline transfer appliances, the foundational economics remain challenging. Organizations therefore weigh architecture choices that minimize data round-trips, adopt in-situ analytics, or colocate post-processing near the simulation nodes, yet each workaround carries new operational complexity.

Talent Shortage in Cloud-Native HPC Operations

Running petascale simulations in the cloud demands expertise at the intersection of cluster science, containerization, and cost-aware scheduling; however, graduate programs and mid-career tracks rarely cover all three domains. Universities and national labs report difficulties hiring faculty competent in teaching cloud-native HPC concepts, curbing the pipeline of qualified engineers. Consulting integrators have stepped into the gap, but their services add cost and can slow internal capability development. The scarcity is pronounced in emergent vectors like quantum and neuromorphic computing, where the toolchain remains nascent and the talent pool extremely limited, stalling wider adoption despite vendor enthusiasm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Stability Underpins Software Acceleration

Hardware contributed 44.12% of 2025 revenue, underscoring the capital-intensive nature of datacenter racks loaded with GPUs, high-bandwidth memory, and NVMe-backed storage arrays. NVIDIA confirmed that cloud providers form its fastest-growing commercial channel, a testament to ongoing spending on accelerators and interconnect switches. Vendors anchor differentiation around node density, energy efficiency, and thermally optimized form factors, as fleet operators chase lower watts per teraflop.

Software, however, posts the highest momentum, with an expected 8.42% CAGR through 2031, driven by schedulers that tune allocations in real-time, AI-assisted performance profilers, and workflow managers that span multicloud and hybrid estates. The expansion of the Cloud High Performance Computing market size on the software side also benefits from subscription licensing models that align costs with active use minutes, shifting budgets from capital to operating expenses.

By Deployment Model: Public Dominance Balanced by Private Resurgence

The public cloud garnered 67.95% share in 2025 and remains the backbone for elastic, project-based simulation bursts that characterize media rendering, computer-aided engineering, and life sciences searches. Providers win workloads by exposing granular billing meters, utilizing spot pools for non-urgent jobs, and maintaining regional zones to comply with data-residency laws.

Private cloud, while smaller, is projected to log a 7.52% CAGR as regulated verticals emphasize deterministic latency and sovereign control. Enterprises craft internal clouds atop converged HPC appliances that mimic the elasticity of hyperscale data centers while maintaining air-gapped security. Hybrid orchestrators integrate these estates, presenting users with a single submission portal that assigns jobs based on cost curves and queue depth.

By Service Model: IaaS Core with PaaS Lift

Infrastructure as a Service (IaaS) accounted for 53.85% of global spend in 2025, as affirmed by customers who require granular control over operating systems, libraries, and tuning flags. Bare-metal nodes, with root access and no hypervisor overhead, enable performance-sensitive codes, such as lattice QCD or direct numerical simulation, to run at near-native speeds.

Platform as a Service, forecast to expand at 7.05% CAGR, packages middleware, compilers, and domain-specific solvers behind curated interfaces, letting researchers concentrate on problem statements rather than kernel parameters. This abstraction resonates with digital media studios, pharmaceutical labs, and automotive design teams that prioritize rapid turnaround over fine-tuning. Software as a Service (SaaS) remains a niche yet important option for turnkey vertical workflows, such as cloud-based electronic design automation suites that charge per solver iteration.

By Industrial Application: Aerospace Command and Media Velocity

Aerospace and defense held 22.21% share in 2025, anchored by flight dynamics, radar cross-section modeling, and secure mission planning workloads that find value in burst scalability and classified enclave options. The U.S. Department of Defense’s multiyear blanket purchase agreements for cloud HPC underscore this reliance.

Media and entertainment, posting a 8.62% CAGR outlook, uses elastic GPU pools for path-traced rendering, volumetric scene generation, and generative character animation. The Cloud High Performance Computing market size for creative studios increases as frame counts, resolution, and generative passes rise with each production cycle. Secondary verticals, including energy reservoir modeling and BFSI risk analytics, sustain steady demand but grow at mid-single-digit rates through incremental simulation complexity.

By Organization Size: Enterprise Capital Meets SME Access

Enterprises with annual revenues exceeding USD 1 billion commanded 64.15% of 2025 consumption, enabled by in-house architecture teams and consolidated software tooling that leveraged volume discounts across regions. Established manufacturers co-locate design optimization loops with cloud solver farms, blending internal and external clusters to shave product cycles.

Small and medium enterprises, expanding at 6.98% CAGR, springboard into the market through pay-per-job portals that remove procurement hurdles. Pre-packaged clusters, tutorial-driven onboarding, and credit-based billing enable early-stage biotech firms, VFX boutiques, and academic consortia to reach teraflop-hour scales that were previously out of reach. This democratization effect drives the emergence of new workload categories and propels the Cloud High Performance Computing market toward a wider range of use cases.

Geography Analysis

North America retained 39.94% share in 2025, supported by dense hyperscale footprints and federally backed exascale initiatives that validate cloud-first architectures. Continuous improvement funds from defense and space agencies feed sustained demand for advanced simulation, while a vibrant commercial ecosystem of semiconductor design, autonomous systems, and digital media consolidates regional leadership. Regulatory clarity regarding data export and encryption further accelerates cloud HPC adoption in heavily controlled industries.

The Asia-Pacific region records the highest forward growth at a 8.77% CAGR as governments earmark billions for sovereign AI and semiconductor design capacity. China increases cloud HPC budgets despite export constraints on advanced accelerators by investing in homegrown GPU alternatives and quantum-classical hybrid centers. Japan aligns HPC roadmaps with Society 5.0, pushing edge-to-cloud integration for smart manufacturing, while India’s Digital Public Infrastructure initiative creates demand for large-scale language modeling in regional dialects. Regional telcos partner with hyperscalers to host in-country availability zones, alleviating data-locality concerns and facilitating broader market entry.

Europe commands a strong though more measured trajectory, aided by the European High-Performance Computing Joint Undertaking that co-finances petascale systems within EU borders. Automotive OEMs in Germany offload aerodynamic simulations to cloud instances when factory clusters max out, and renewable energy operators in the Nordics harness low-carbon datacenters driven by abundant hydro power. GDPR compliance stimulates hybrid adoption patterns, keeping sensitive telemetry on-premises but using cloud scale for large design-of-experiments runs. National digital strategies and carbon-neutral targets jointly influence procurement models, nudging adoption toward green-certified cloud regions.

Competitive Landscape

Competition in the Cloud High-Performance Computing market revolves around three key areas: infrastructure ownership, platform services, and workload-specific tooling. Amazon Web Services, Microsoft Azure, and Google Cloud collectively supply the majority of rentable petaflops, each armed with proprietary interconnect fabrics and custom accelerators to preserve a competitive edge. Their vertical stacks include compilers, schedulers, and cost-aware advisors that reinforce user stickiness.

Chip vendors such as NVIDIA, AMD, and Intel contest socket share by releasing architectural roadmaps tailored for cloud tenancy, emphasizing high memory bandwidth, multi-instancing support, and driver stacks optimized for Kubernetes orchestration. Systems integrators, from HPE to Dell Technologies, round out offerings with GreenLake-style consumption models, bridging private and public estates for regulated customers.

The software-defined layer attracts emerging startups that target performance optimization niches, such as automatic CUDA-to-HIP translation, AI-based queue prediction, or energy-aware job packing. Patent filings tracked by the United States Patent and Trademark Office confirm an accelerated research and development (R&D) spend on cloud-native job schedulers and telemetry-driven performance analytics. Mergers center on capability absorption rather than outright scale, reflecting the market’s moderate fragmentation. Overall, the top five providers account for roughly 60-65% of total spend.

Cloud High Performance Computing (HPC) Industry Leaders

Amazon Web Services Inc.

Microsoft Corporation

Google LLC

International Business Machines Corporation

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft announced the preview of Azure HPC-Quantum Scheduler, a unified queue that allocates classical and quantum resources within the same job graph, targeting drug-discovery labs.

- October 2024: Amazon Web Services released Deadline Cloud, a managed render farm scaled to thousands of GPUs for real-time content creation.

- September 2024: Microsoft launched Azure Quantum Elements, integrating chemistry solvers with quantum simulators.

Global Cloud High Performance Computing (HPC) Market Report Scope

The Cloud High Performance Computing (HPC) Market Report is Segmented by Component (Hardware, Software, and Services), Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Service Model (Infrastructure As A Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS), and Managed HPC Services), Industrial Application (Aerospace and Defense, Energy and Utilities, Banking, Financial Services and Insurance, Media and Entertainment, Manufacturing, Life Science and Healthcare, Academic and Research, Government, and Other Industrial Applications), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Servers |

| Storage | |

| Networking Devices | |

| Accelerators (GPUs/TPUs) | |

| Software | |

| Services |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Infrastructure as a Service (IaaS) |

| Platform as a Service (PaaS) |

| Software as a Service (SaaS) |

| Managed HPC Services |

| Aerospace and Defence |

| Energy and Utilities |

| Banking, Financial Services and Insurance |

| Media and Entertainment |

| Manufacturing |

| Life Science and Healthcare |

| Academic and Research |

| Government |

| Other Industrial Applications |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Hardware | Servers |

| Storage | ||

| Networking Devices | ||

| Accelerators (GPUs/TPUs) | ||

| Software | ||

| Services | ||

| By Deployment Model | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By Service Model | Infrastructure as a Service (IaaS) | |

| Platform as a Service (PaaS) | ||

| Software as a Service (SaaS) | ||

| Managed HPC Services | ||

| By Industrial Application | Aerospace and Defence | |

| Energy and Utilities | ||

| Banking, Financial Services and Insurance | ||

| Media and Entertainment | ||

| Manufacturing | ||

| Life Science and Healthcare | ||

| Academic and Research | ||

| Government | ||

| Other Industrial Applications | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the Cloud High Performance Computing market in 2031?

The market is expected to reach USD 47.93 billion by 2031, expanding at a 5.28% CAGR.

Which deployment model will grow fastest through 2031?

Private cloud is forecast to advance at 7.52% CAGR as enterprises seek tighter data control and predictable latency.

Why are AI workloads critical to cloud HPC growth?

AI training already consumes 40% of cloud HPC capacity; elastic GPU clusters shorten training cycles, driving sustained demand.

How does cloud egress pricing affect HPC economics?

For data-intensive simulations, outbound transfer fees can exceed compute costs by up to 200%, making in-situ analytics and data localization crucial.

Which region offers the highest growth opportunity?

Asia-Pacific is set to deliver a 8.77% CAGR, propelled by sovereign AI funding and the rapid digitization of manufacturing.

What is the role of Platform as a Service in cloud HPC?

PaaS abstracts infrastructure, bundles domain toolchains, and is projected to grow at 7.05% CAGR as users favor managed environments.

Page last updated on: