Intelligent Apps Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 63.42 Billion |

| Market Size (2031) | USD 266.24 Billion |

| Growth Rate (2026 - 2031) | 33.23% CAGR |

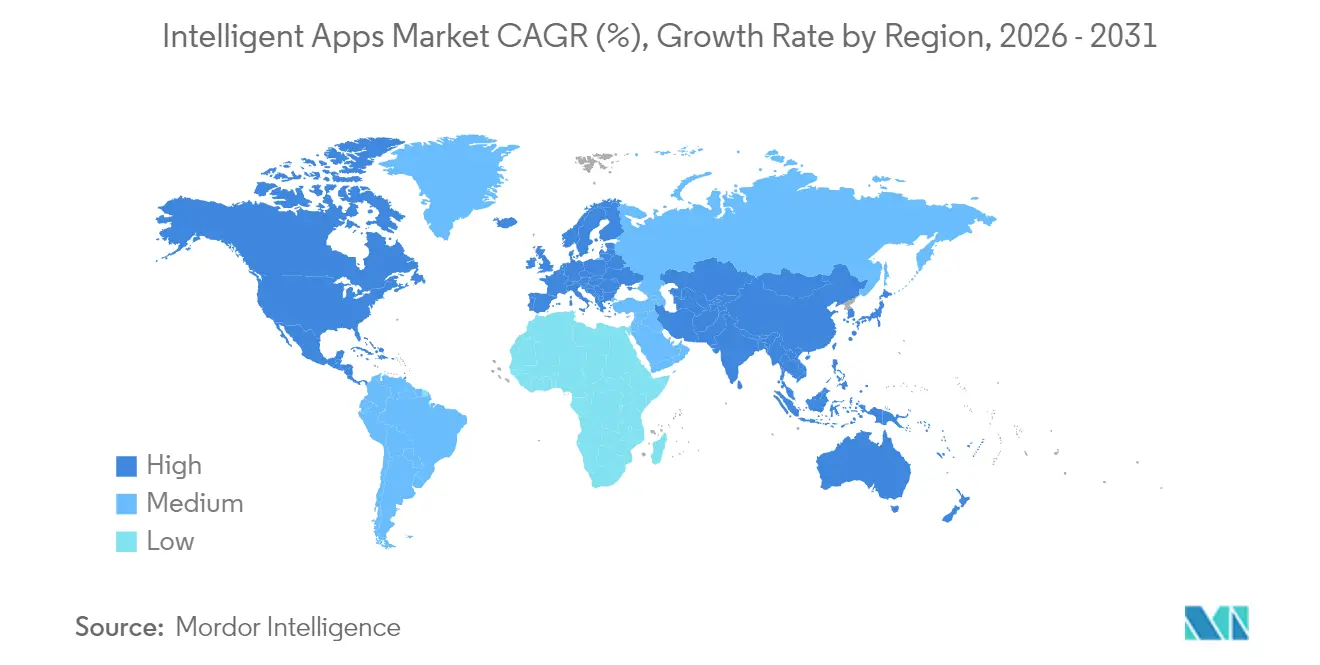

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

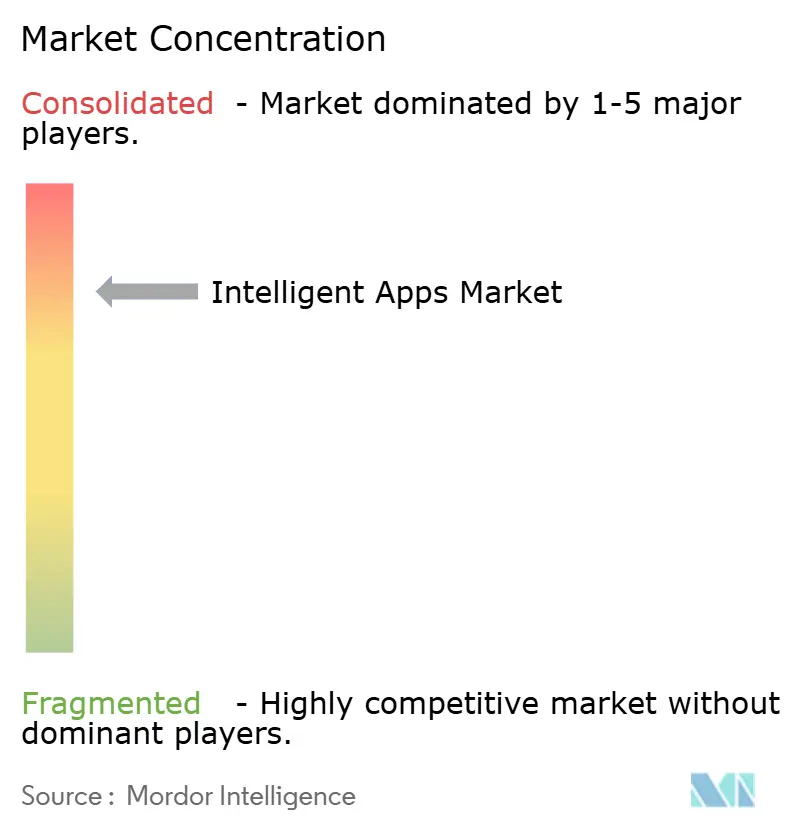

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intelligent Apps Market Analysis by Mordor Intelligence

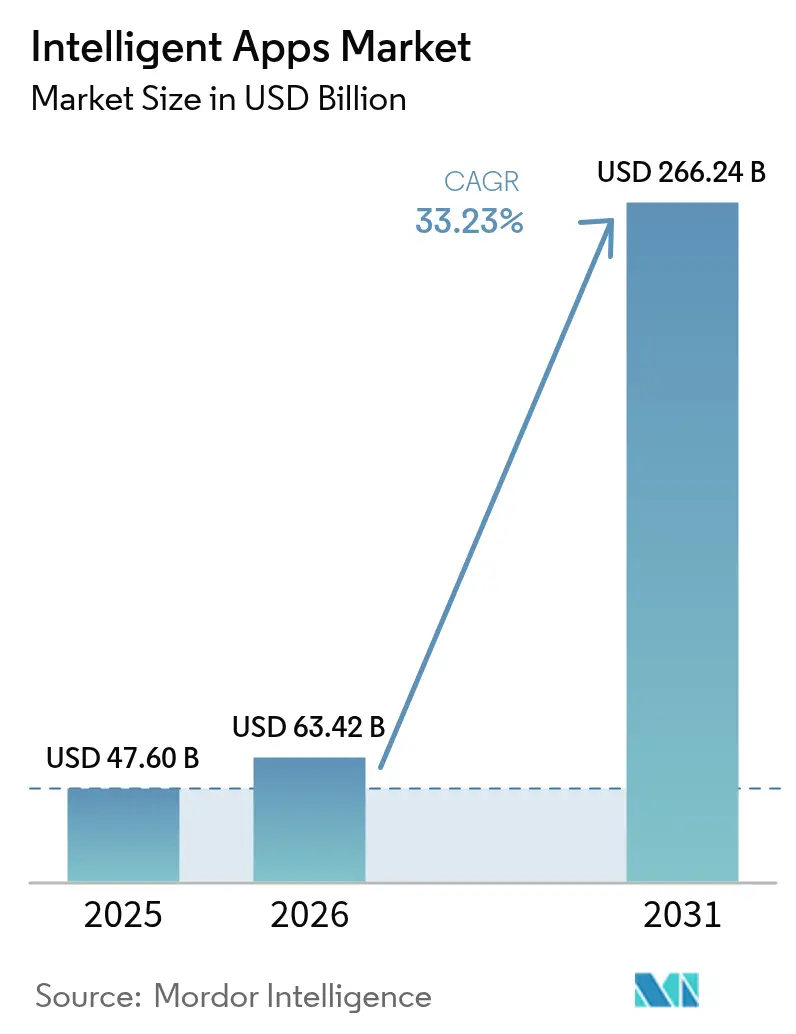

The intelligent apps market size was valued at USD 47.60 billion in 2025 and estimated to grow from USD 63.42 billion in 2026 to reach USD 266.24 billion by 2031, at a CAGR of 33.23% during the forecast period (2026-2031). Rapid enterprise digital-transformation programs are pushing organizations to embed AI directly into everyday software rather than treat it as a bolt-on capability. Cloud-native tooling, pre-trained foundation models and pay-as-you-go compute pricing have removed most capital barriers, allowing even midsized firms to roll out production-grade intelligent applications inside 90 days. On the demand side, business functions now expect real-time personalization and autonomous task automation, shifting AI from experimental pilots to revenue-bearing workloads. The intelligent apps market is also benefiting from a strong mobile hardware refresh cycle that puts dedicated AI accelerators in consumer devices, opening an offline channel for low-latency inference. Finally, tightening accessibility regulations in North America and the EU are turning AI-driven compliance features—such as real-time captioning and adaptive layouts—into mandatory product requirements.

Key Report Takeaways

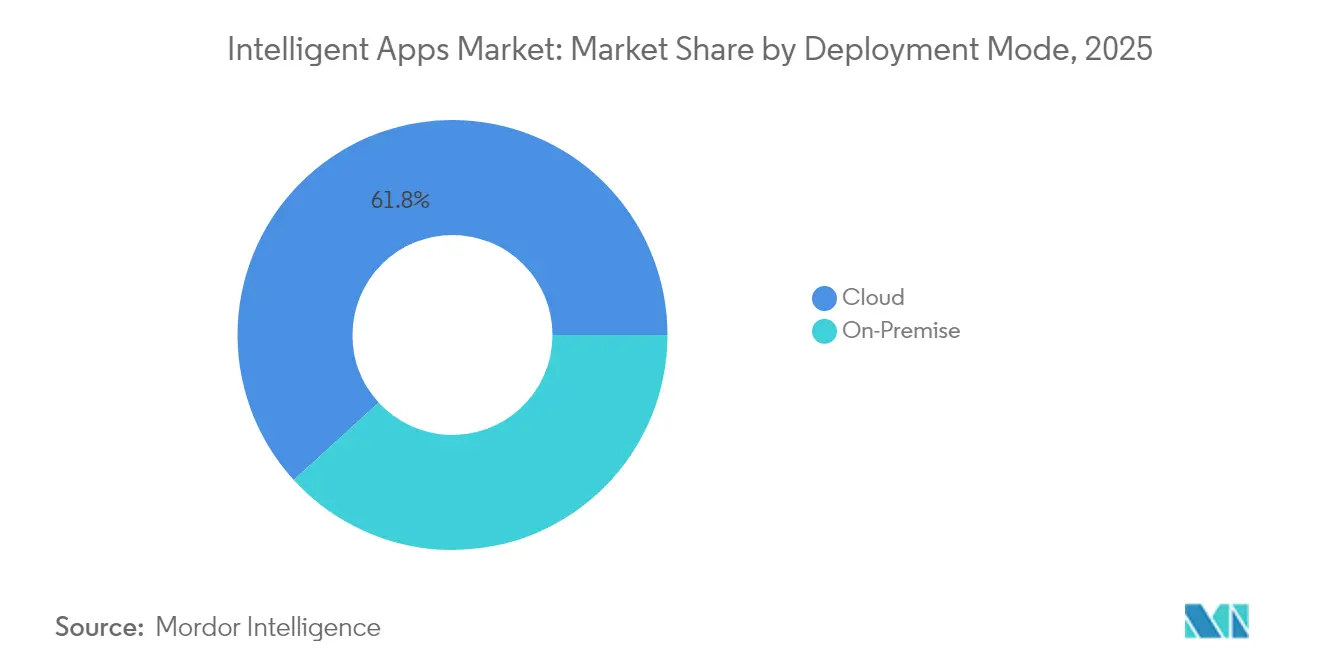

- By deployment mode, cloud services held 61.78% of the intelligent apps market share in 2025 and are growing at a 38.65% CAGR through 2031.

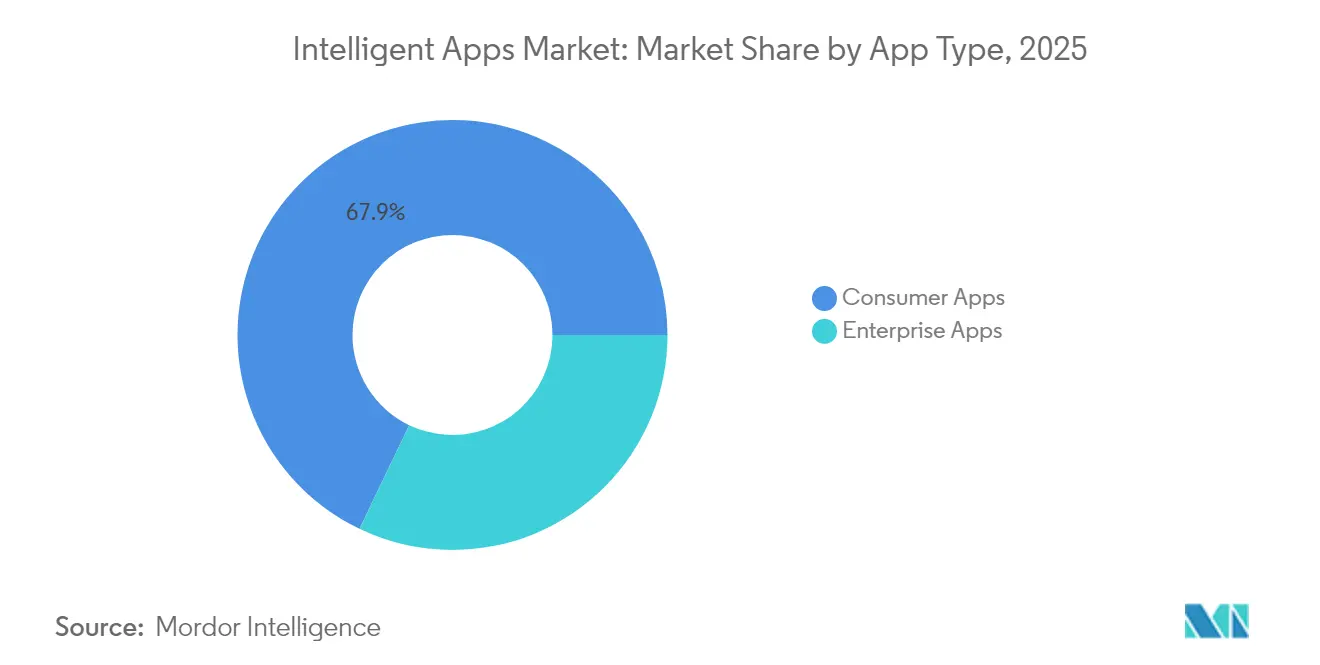

- By application type, consumer apps dominated with 67.88% revenue share in 2025, while enterprise apps post the fastest expansion at 33.75% CAGR.

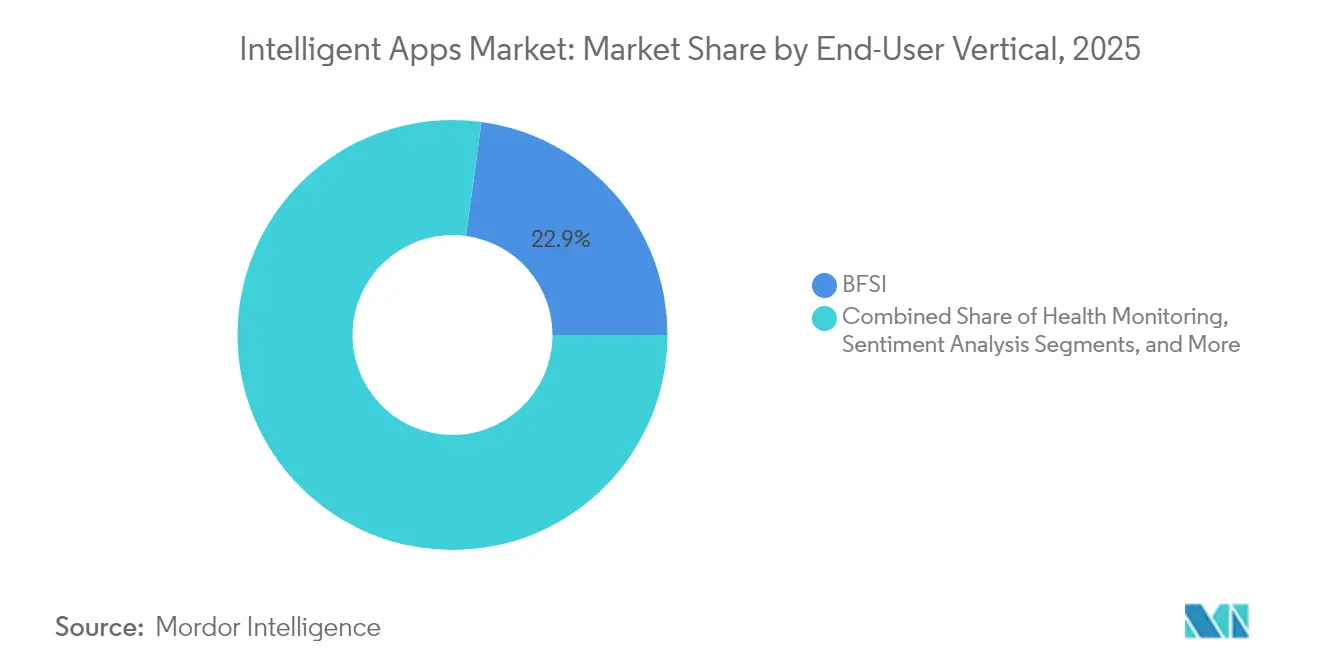

- By end-user vertical, Banking, Financial Services and Insurance contributed 22.85% of the intelligent apps market size in 2025; Healthcare and Life Sciences is advancing at a 33.45% CAGR to 2031.

- By geography, North America accounted for 37.55% revenue share in 2025, whereas Asia-Pacific records the quickest growth at 39.18% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intelligent Apps Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smartphone proliferation and mobile-first journeys | +8.2% | Global, led by Asia-Pacific | Medium term (2-4 years) |

| Enterprise AI budgets for intelligent apps | +9.1% | North America and EU, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Cloud AI platforms lowering dev barriers | +7.8% | Global, cloud-first regions | Short term (≤ 2 years) |

| On-device AI accelerators for offline use | +4.3% | North America, China, South Korea | Long term (≥ 4 years) |

| Accessibility regulations | +2.1% | North America and EU | Medium term (2-4 years) |

| Edge AI for millisecond personalisation | +3.0% | Urban 5G-enabled regions worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Digital-Transformation Budgets for AI-Powered Apps

Enterprise AI spending soared 130% in 2024 to USD 13.8 billion as leadership teams prioritized revenue-generating intelligent applications over cost-cutting chatbots. More than half of large companies now expect AI to deliver top-line growth, redirecting budgets away from traditional licenses and toward AI-native platforms. Microsoft alone reported USD 13 billion in AI revenue in 2024 and allocated USD 80 billion to new infrastructure, ensuring adequate GPU capacity for corporate customers.[1]Microsoft Corporation, “FY24 Q4 Earnings Transcript,” microsoft.com Financial firms illustrate the return potential: US banks already route 73% of employee tasks through generative AI helpers, and Citi estimates USD 170 billion in profit uplift by 2028 from intelligent automation. The pattern is similar in logistics, energy and retail where AI agents now supervise high-volume, transaction-heavy workflows.

Cloud AI Platforms Lowering Development Barriers

Public-cloud AI services processed 1.3 million GPU hours in 2024 across Amazon, Microsoft and Google estates, placing industrial-grade model training within reach of mid-level developers. No-code builders and pre-trained vision, speech and language APIs let business analysts create production apps without data-science expertise. While speed-to-value accelerates, governance overhead is rising: chief risk officers must now certify every model for fairness, robustness and explainability before launch. Leaders respond by adopting centralized MLOps hubs that automate version control, bias scans and audit logs, striking a balance between rapid deployment and responsible AI.

Proliferation of Smartphones and Mobile-First Customer Journeys

Mobile AI apps generated USD 3.3 billion in 2024 revenue, up 51% year over year, spurred by device-level neural processors that run complex models locally.[2]Sensor Tower, “Generative AI Mobile App Revenue 2024,” sensortower.com Apple’s integration of ChatGPT into Siri triggered 160 million downloads by August 2024, proving mainstream appetite for conversational interfaces. By end-2028, more than half of new smartphones will ship with generative AI features, creating a vast installed base for developers. For enterprises, a mobile-first strategy slashes latency, cuts cloud egress fees and unlocks new use cases—such as industrial field inspections—where real-time inference is essential even when connectivity is poor.

Embedded On-Device AI Accelerators Enable Offline Intelligence

NVIDIA booked USD 60 billion in 2024 silicon revenue, driven by edge-class GPUs and system-on-a-chip designs for smartphones, cars and IoT rigs. As hardware reaches 10-trillion-operation benchmarks, tasks once reserved for data-center clusters now execute on handheld devices. This shift is critical for autonomous vehicles, smart-factory robots and extended-reality headsets that cannot tolerate cloud round-trip delays. Developers face fresh challenges in pruning and quantizing models to fit power-constrained environments, yet those who succeed enjoy a differentiated UX that operates even in network dead zones.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented app ecosystems and integration complexity | -4.7% | Global, affects cross-platform builds | Short term (≤ 2 years) |

| Data-privacy compliance (GDPR, CPRA) | -3.2% | EU, California, spreading worldwide | Medium term (2-4 years) |

| Shortage and cost of specialised AI hardware | -2.8% | Global supply chains | Medium term (2-4 years) |

| Brand-risk from algorithmic bias litigation | -1.9% | North America and EU courts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented App Ecosystems and Integration Complexity

Developers must now reconcile half-century-old industrial controllers, three generations of ERP suites and half-dozen mobile OS versions when rolling out unified intelligent apps. The resulting integration bills can consume 20% of total project spend, especially in manufacturing where legacy machinery still lacks modern APIs. Hybrid deployments add layers of orchestration, forcing teams to juggle latency, security and data-sovereignty constraints across cloud and on-prem nodes. Vendors are countering with universal connectors and AI-centric event buses, yet interview data from CIOs suggests full interoperability will remain elusive for at least two more years.

Data-Privacy Compliance (GDPR, CPRA, etc.)

Europe’s GDPR and California’s CPRA mandate consent dashboards, algorithmic transparency and data-minimization routines that frequently strip training sets of valuable context. Financial institutions now devote up to 15% of AI budgets to compliance tooling, including data-lineage trackers and synthetic-data generators that offset access limits. Multinationals often choose to implement the strictest regional standard worldwide to avoid code forks, pushing smaller firms toward managed-service providers that bake compliance into the platform. Over the medium term, privacy-enhancing techniques such as federated learning and homomorphic encryption may lower the overhead, but current deployments still face extended testing and audit cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Accelerates Enterprise Migration

Cloud deployments captured 61.78% of the intelligent apps market size in 2025, and the same segment is expanding at a 38.65% CAGR thanks to elastic GPU clusters and consumption-based pricing. Enterprises value the ability to spin up sandbox environments in minutes, run experiments against terabyte-scale datasets and then retire resources when finished. Meanwhile, procurement leaders report a 2-to-1 reduction in time-to-value compared with on-prem refresh cycles. A counter-trend is visible: 47% of large organizations are building GenAI workloads in-house, eyeing hybrid patterns that keep sensitive data close while exploiting cloud for burst training. Analysts note that on-prem-centric designs may cut recurring inference costs by as much as one-third for high-volume use cases.

On-premises systems, although smaller in share, are benefitting from purpose-built AI servers from HPE and Dell that bundle accelerators, high-bandwidth memory and turnkey MLOps stacks. HPE grew AI hardware revenue 16% to USD 1.5 billion in 2024, affirming latent demand among regulated industries that prize data residency and predictable latency. As a result, hybrid topologies—cloud for model development, edge or data-center for inference—are poised to define the next phase of intelligent apps market evolution.

By App Type: Consumer Volume Meets Enterprise Value Creation

Consumer-facing software delivered 67.88% of 2025 revenue, fuelled by viral companion bots and generative content tools. Network effects and app-store distribution create massive user pools where even freemium conversion rates of 3% translate into tens of millions in annual sales. Nevertheless, enterprise-grade offerings deliver higher per-seat economics, driving a 33.75% CAGR for business deployments through 2031. Corporate buyers value deep integrations with ERP, CRM and unified communications stacks that magnify productivity across thousands of employees. Microsoft’s Copilot suite showcases this dynamic, with firms reporting measurable gains that offset subscription costs in under six months. As workflows hard-wire AI agents into approval chains and knowledge bases, switching costs escalate, reinforcing vendor lock-in and expanding lifetime value.

By End-User Vertical: Financial Services Leads, Healthcare Accelerates

Banking, Financial Services and Insurance captured 22.85% of the intelligent apps market share in 2025, the largest slice within any vertical. Institutions deploy AI agents for fraud detection, customer-service chat, and real-time compliance checks that interpret complex regulations more reliably than human teams. Pioneers such as Bank of America’s Erica and Wells Fargo’s AI fraud monitors show how conversational interfaces and continuous risk scoring shorten response times while reducing manual effort. Insurers mirror this trend by automating claims triage and policy underwriting, freeing specialist staff for higher-value advisory roles. As a result, BFSI remains the anchor customer group for platform vendors that need high-volume, high-value reference wins to validate enterprise performance.

Healthcare and Life Sciences is the fastest-growing vertical, advancing at a 33.45% CAGR through 2031 as hospitals and research centers seek to curb clinician burnout and improve diagnostic accuracy. Outside the two headline sectors, retail, manufacturing, telecoms, education and hospitality are scaling pilot projects that personalize shopping journeys, optimize factory maintenance and automate campus-wide helpdesks. Each niche rewards domain-specific data and compliance expertise, giving rise to specialist vendors that complement broad cloud platforms rather than compete head-on.

Geography Analysis

North America commanded 37.55% of 2025 revenue, making it the largest regional contributor to the intelligent apps market. The region benefits from abundant venture capital, dense clusters of AI talent and mature cloud infrastructure. US companies alone poured USD 290 billion into AI R&D over the past five years, speeding commercialization across banking, healthcare and advanced manufacturing. Regulatory frameworks—such as NIST’s AI Risk Management Framework—offer clear guardrails that balance innovation with consumer protection, further strengthening adoption momentum.

Asia-Pacific is the growth engine, projected to compound at 39.18% annually through 2031. China’s USD 2.1 billion public-sector investment and Singapore’s USD 1 billion National AI Strategy 2.0 supply both capital and policy tailwinds. Mobile-first digital economies, combined with large manufacturing bases, create immediate demand for predictive maintenance, quality control and hyper-personalized commerce. Local hyperscalers, including Alibaba Cloud and Tencent Cloud, add language-specific models that accelerate regional uptake.

Europe occupies a middle ground where the intelligent apps market grows steadily under stricter privacy rules. The forthcoming AI Act requires mandatory risk assessments and transparency labels, nudging vendors toward explainable architectures and privacy-preserving techniques. While compliance adds friction, it also positions European providers as trusted partners for critical sectors such as healthcare and public administration, creating a differentiated export opportunity.

South America, the Middle East and Africa remain nascent but promising. Telecom operators are rolling out low-code AI platforms that allow small retailers and fintech startups to embed chat and voice bots without in-house data-science teams. Government-backed digital-ID programs in Brazil and the UAE further expand addressable use cases by providing standardized data sources for KYC and fraud analytics.

Competitive Landscape

The intelligent apps market displays moderate concentration. Platform giants—Microsoft, Amazon, Google and Apple—anchor end-to-end stacks that span cloud infrastructure, orchestration frameworks and consumer endpoints. Microsoft posted USD 13 billion in AI revenue for 2024 and earmarked USD 80 billion for additional data-center build-outs, cementing scale economics that discourage new entrants. Rather than acquire outright, incumbents increasingly opt for minority stakes or joint ventures to secure frontier models while sidestepping antitrust scrutiny. Meta’s USD 14.3 billion investment for 49% of Scale AI typifies this partnership model, allowing Meta to tap curated data pipelines without dismantling Scale’s multi-client business.[3]IBM, “Global AI Adoption Index 2024,” ibm.com

White-space opportunities persist in vertical niches requiring domain know-how and compliance IP. Startups focusing on clinical-decision support, risk analytics or autonomous factory lines leverage specialized datasets and subject-matter expertise to differentiate. Incumbent ERP providers also wield influence: SAP, Oracle and Salesforce embed AI across order management and HR modules, bundling features at marginal cost to defend against stand-alone disruptors. Looking forward, open-source foundation models and sovereign-cloud initiatives may loosen platform lock-in, but network effects around data and distribution will keep bargaining power tilted toward ecosystem leaders.

Intelligent Apps Industry Leaders

IBM Corporation

Apple Inc,

Microsoft Corporation

Google LLC

Amazon Web Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Meta invested USD 14.3 billion for a 49% stake in Scale AI, recruiting CEO Alexandr Wang to head a new research group targeting artificial general intelligence.

- May 2025: Netflix debuted a generative AI search assistant that lets subscribers use natural-language queries to surface personalized content.

- May 2025: Microsoft created the CoreAI engineering division under Jay Parikh to build an “AI-first app stack” spanning Azure, GitHub and Visual Studio Code.

- March 2025: Adobe and Microsoft launched a private preview connecting Adobe Marketing Agent and Adobe Express Agent to Microsoft 365 Copilot, allowing marketers to generate visuals and campaigns inside familiar Office workflows.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the intelligent apps market as all packaged or cloud-delivered software whose core user experience is dynamically shaped by embedded artificial-intelligence techniques, most commonly machine learning, natural-language processing, computer vision, and emerging agentic AI models. These applications range from consumer-facing mobile super-apps to enterprise productivity, analytics, and vertical-specific suites.

Scope exclusions, one quick line: infrastructure-only AI runtimes, stand-alone developer frameworks, and traditional rule-based applications with no self-learning loop are left outside our sizing.

Segmentation Overview

- By Deployment Mode

- On-Premise

- Cloud

- By App Type

- Consumer Apps

- Enterprise Apps

- By End-User Vertical

- BFSI

- Retail and E-commerce

- Healthcare and Life Sciences

- Media and Entertainment

- Telecom and IT

- Hospitality and Travel

- Manufacturing

- Education

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Spain

- Switzerland

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Malaysia

- Singapore

- Vietnam

- Indonesia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- Nigeria

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed software product leaders, cloud-channel partners, and CIOs across North America, Europe, and fast-growing Asia-Pacific markets. These conversations clarified average selling prices, seat counts, and penetration hurdles, enabling us to refine assumptions that secondary data alone could not fully explain.

Desk Research

We compiled foundational inputs from reputable, non-paywalled sources such as the OECD AI Policy Observatory, the US Bureau of Economic Analysis, Eurostat digital-economy dashboards, Gartner technology trend notes, and IDC enterprise-software trackers. Company 10-Ks, investor decks, and global trade filings enriched adoption indicators. Paid resources from D&B Hoovers and Dow Jones Factiva helped us cross-check revenue splits and newsflow on major vendors. The sources listed are illustrative; many additional datasets were tapped for validation.

Market-Sizing & Forecasting

A top-down demand-pool build starts with enterprise IT spend and consumer app store revenue, reconstructed from national accounts and marketplace disclosures; this is subsequently corroborated with sampled bottom-up checks such as vendor revenue roll-ups and channel ASP x active-user estimates. Key model drivers include the number of cloud-native developers, mobile device install base with on-device AI accelerators, freemium-to-paid conversion rates, regulatory AI spending incentives, and average agentic-feature attach rates. A multivariate regression blends these variables, while scenario analysis captures shifts in pricing or privacy rules. Gaps where supplier data run thin are bridged using regional ASP medians and usage intensity multipliers reviewed with expert respondents.

Data Validation & Update Cycle

Outputs pass anomaly and variance screens, after which a senior analyst audits assumptions. Reports refresh annually; material events, major regulatory changes or breakthrough model launches, trigger interim revisions. A final pre-publication sweep ensures clients receive the latest calibrated view.

Why Mordor's Intelligent Apps Baseline Commands Reliability

Published estimates often diverge because firms slice the market along different functionality lines, bundle adjacent services, or apply contrasting currency year bases.

Key gap drivers include some studies that restrict scope to mobile AI apps, others that track only agentic AI modules, and a few that extrapolate global totals from limited vendor samples, choices that compress or overinflate the baseline relative to Mordor's broader yet clearly demarcated definition. Our annual refresh cadence and explicit exclusion of infrastructure revenue further separate our view from snapshots using older exchange rates or mixed-year data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 47.60 B (2025) | Mordor Intelligence | - |

| USD 27.70 B (2025) | Global Consultancy A | mobile-only scope, filters out enterprise web apps |

| USD 5.13 B (2025) | Trade Journal B | tracks AI apps with paid downloads only; ignores SaaS subscriptions |

| USD 5.25 B (2024) | Industry Research C | focuses on autonomous "AI agents," excludes legacy ML-enabled apps |

Taken together, the comparison shows that when scope, base year, and revenue channels are aligned, Mordor's disciplined mix of macro demand pools, selective bottom-up checks, and continuous expert feedback yields a balanced, transparent baseline clients can trust for strategic planning.

Key Questions Answered in the Report

What is the current intelligent apps market size?

The intelligent apps market size stands at USD 63.42 billion in 2026 and is projected to reach USD 266.24 billion by 2031.

Which deployment model grows fastest?

Cloud deployments exhibit the quickest expansion, registering a 38.65% CAGR while already holding 61.78% share in 2025.

Which is the fastest growing region in Intelligent Apps Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which vertical generates the highest revenue today?

Banking, Financial Services and Insurance leads, accounting for 22.85% of 2025 revenue as institutions deploy intelligent apps for fraud detection and customer service.

Which region offers the strongest growth outlook?

Asia-Pacific is forecast to rise at a 39.18% CAGR through 2031, buoyed by large-scale government AI investments and mobile-first digital economies.

How are regulations shaping intelligent app design?

GDPR, CPRA and upcoming EU AI Act rules require privacy-by-design, algorithmic transparency and risk assessments, prompting vendors to embed compliance mechanisms from the outset.

Page last updated on: