Cloth Diaper Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

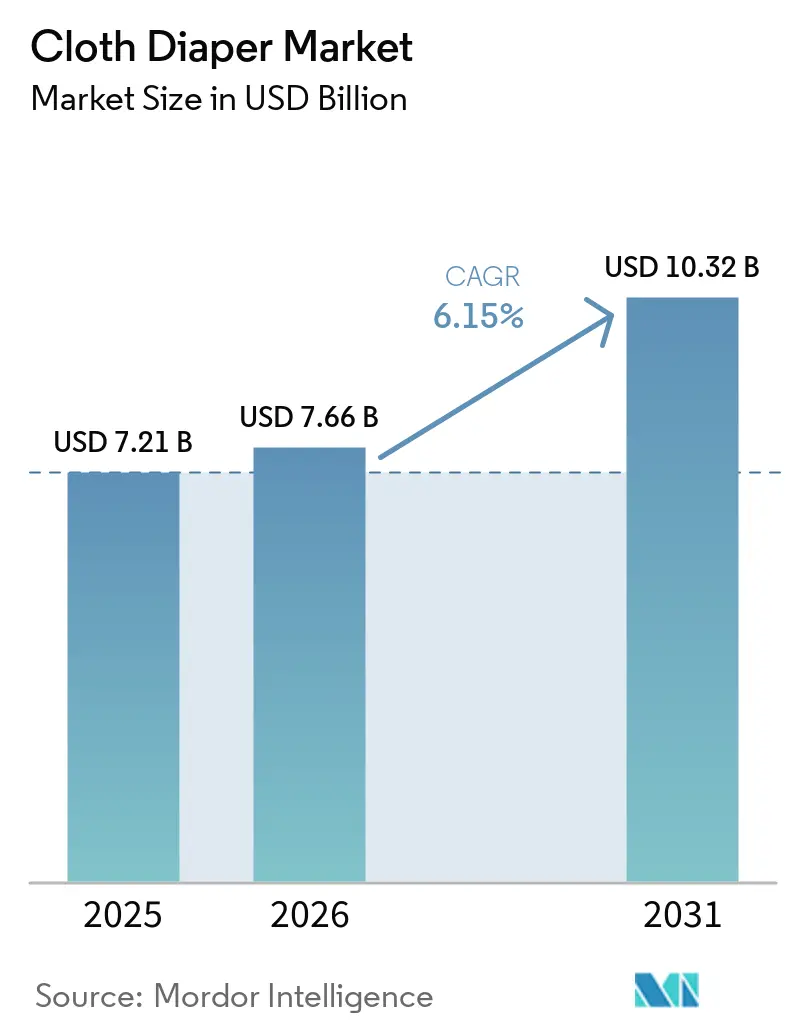

| Market Size (2026) | USD 7.66 Billion |

| Market Size (2031) | USD 10.32 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

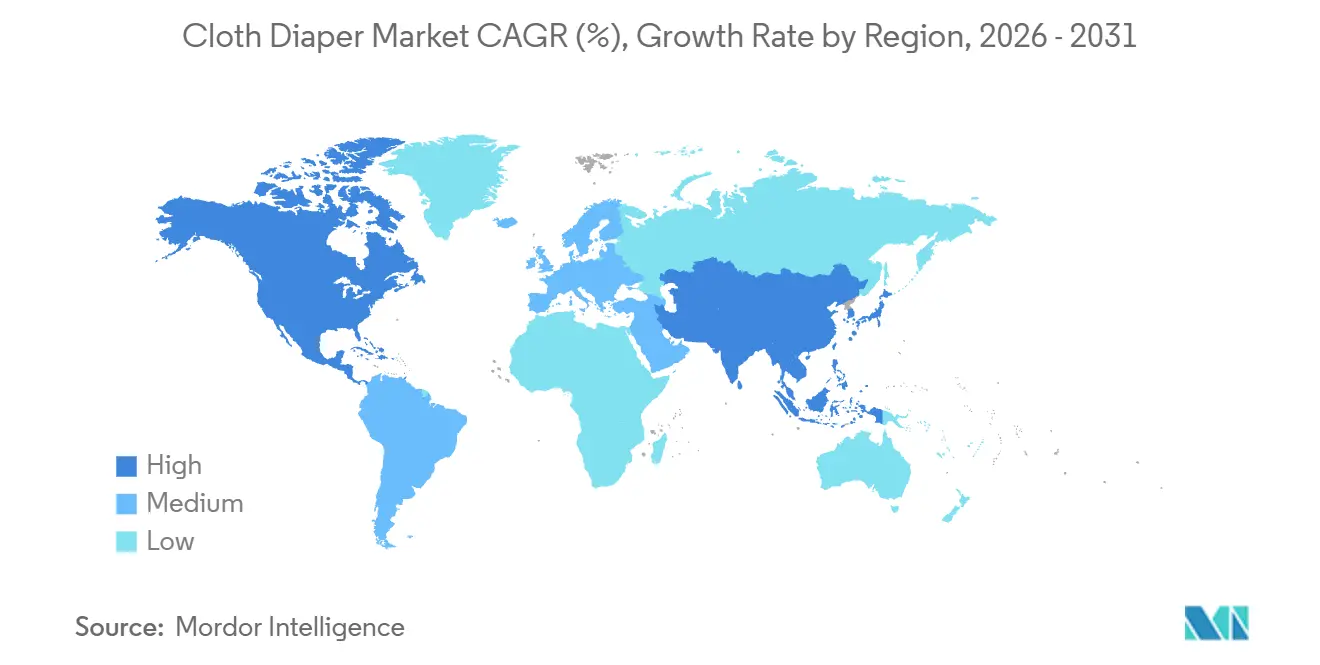

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloth Diaper Market Analysis by Mordor Intelligence

The cloth diaper market is projected to grow from USD 7.21 billion in 2025 to USD 7.66 billion in 2026 and reach USD 10.32 billion by 2031, with a CAGR of 6.15% from 2026 to 2031. Regulatory changes, such as the European Union’s Extended Producer Responsibility rules effective January 2025, are increasing costs for disposable diaper makers, making reusable options more economical. Demographic shifts, including declining fertility rates in 24 countries and aging populations in China, Japan, and Germany, are reducing baby-care demand but boosting adult diaper consumption. In 2025, Asia-Pacific will account for 39.4% of market revenue, driven by manufacturing hubs in China’s Fujian and Hebei provinces, where unit costs range from USD 0.03 to USD 1.80 with minimum orders of 50,000–340,000 pieces. The Middle East and Africa are expected to lead growth with a 7.45% CAGR through 2031, fueled by population growth in Sub-Saharan Africa and landfill limitations.

Key Report Takeaways

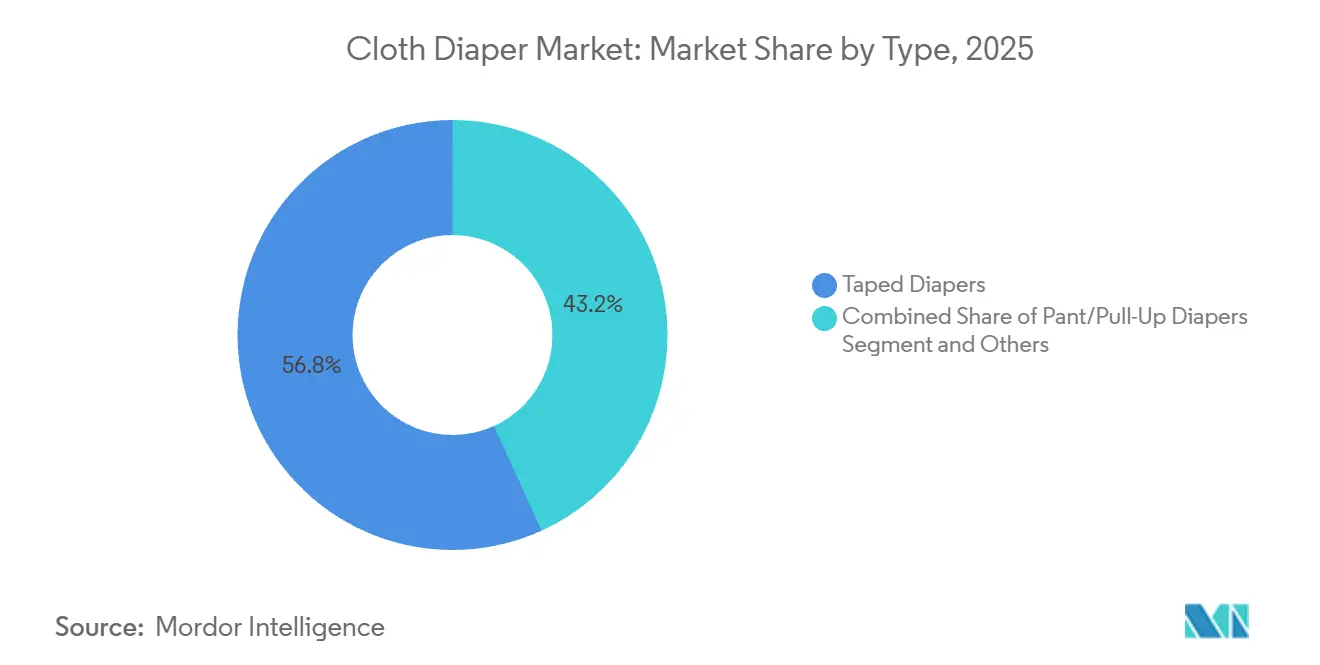

- By product type, taped variants led with 56.8% revenue share in 2025; pant-style pull-ups are projected to advance at a 6.95% CAGR through 2031.

- By end-user, babies accounted for 90.23% of the cloth diaper market share in 2025, while adult usage records the highest expected CAGR at 8.34% to 2031.

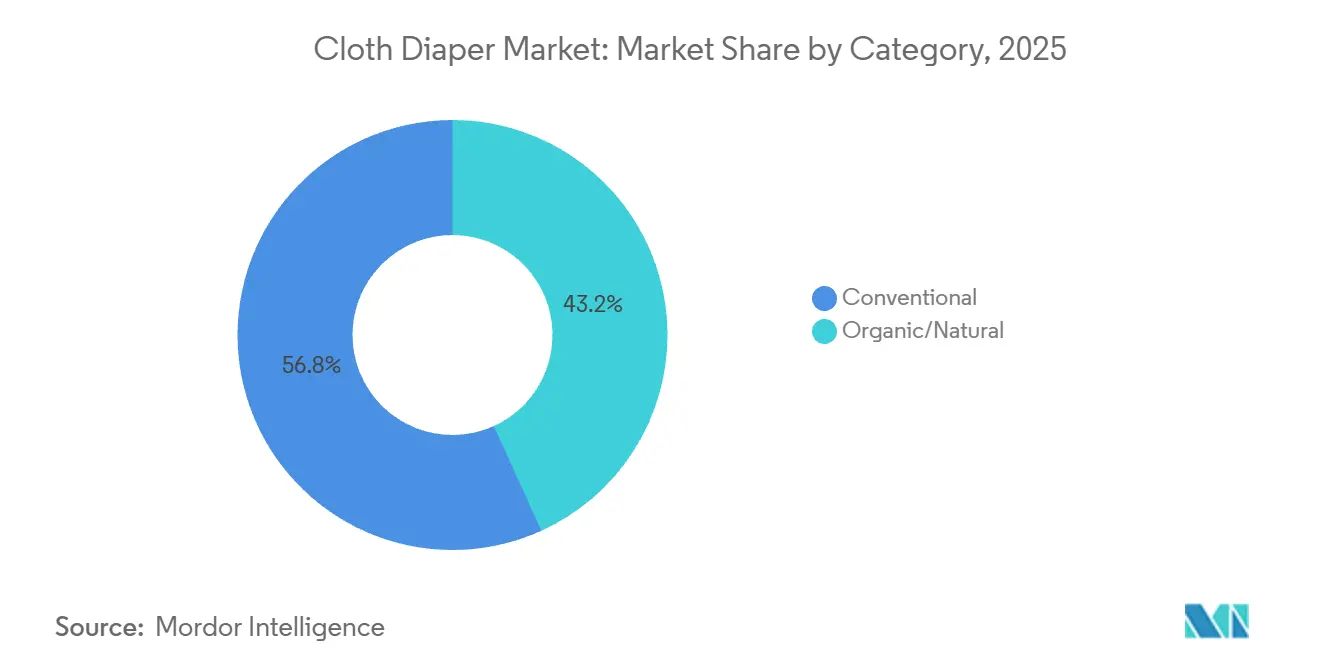

- By category, conventional diapers held 56.78% of 2025 revenue; organic and natural offerings are forecast to grow at 7.99% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets captured 35.43% of 2025 sales, yet health and specialty stores are set to climb at an 8.23% CAGR to 2031.

- By geography, Asia-Pacific dominated with 39.4% 2025 sales, whereas the Middle East and Africa are the fastest-growing regions at 7.45% CAGR until 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cloth Diaper Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened awareness of environmental issues and push for sustainability | +1.2% | Global, with peak adoption in EU, North America, and urban Asia-Pacific | Medium term (2-4 years) |

| Demand for personalized products and visual allure | +0.6% | North America, Europe, Australia | Short term (≤ 2 years) |

| Surge in promotions via social media and influencers | +0.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Rising emphasis on health of infant skin | +1.0% | Global, with regulatory tailwinds in EU and North America | Medium term (2-4 years) |

| Advancements in materials including bamboo, hemp, and antimicrobial fabrics | +1.3% | Global, manufacturing concentrated in Asia-Pacific | Long term (≥ 4 years) |

| Expansion of e-commerce and diverse distribution avenues | +1.4% | Global, accelerated in Asia-Pacific and MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Heightened Awareness of Environmental Issues and Push for Sustainability

Regulatory changes are reshaping the cost dynamics between single-use and reusable diapers in developed markets. Starting January 2025, the European Union's Waste Framework Directive will require disposable diaper manufacturers to pay for the collection, sorting, and recycling of their products under the Extended Producer Responsibility rule[1]Source: European Commission, “Waste Framework Directive—Textiles EPR Amendment,” ec.europa.eu. This additional cost does not apply to washable cloth diaper systems, giving them a financial advantage. In the United States, New York and California will introduce ingredient disclosure laws in 2025, mandating that disposable diaper brands list all chemical ingredients on their packaging. Organic cloth diaper producers already comply with these transparency standards through GOTS v8.0 certification. A 2025 lifecycle assessment in the Netherlands found that centralized cloth diaper laundry services can lower carbon emissions by 40% compared to home washing and by 60% compared to disposable diapers, provided the service covers more than 10,000 households. Furthermore, the OEKO-TEX Standard 100 Annex 6 certification, which restricts formaldehyde to below 16 ppm and bans over 100 harmful substances, has become an essential standard for brands targeting health-conscious parents in Europe and North America.

Advancements in Materials Including Bamboo, Hemp, and Antimicrobial Fabrics

Material innovation is bridging the gap with disposable products while ensuring they remain washable. In November 2022, Products On The Go received U.S. Patent 11,490,770 for biodegradable bamboo wipes. These wipes are infused with natural cleansing ingredients like aloe vera, chamomile, and tea tree oil. The same formulation is used in bamboo-fiber diaper liners, which are hypoallergenic and antibacterial, and do not require pesticides or irrigation during production. Jude's Family developed a 12-layer organic cotton weave that performs exceptionally well. It achieves liquid absorption in less than 10 seconds and keeps rewet values below 0.3 grams, meeting or exceeding the standards of disposable products. Despite this performance, the material maintains a slim, dry thickness of under 3 millimeters. In September 2023, W. Pelz GmbH was granted a European patent EP 4,248,926 for a hybrid diaper system. This system combines a reusable outer garment, which has high moisture vapor transmission rates of over 8,000 grams per square meter per 24 hours, with disposable absorbent pads. This design allows parents to wash the outer garment only after every 3 to 5 diaper changes[2]Source: European Patent Office, “EP 4,248,926,” epo.org . Meanwhile, hemp-blend fabrics are gaining popularity for their strength and antimicrobial properties. Suppliers in China's Hunan province are offering hemp-cotton blends at wholesale prices ranging from USD 0.15 to USD 0.40 per unit for orders exceeding 100,000 pieces.

Expansion of E-Commerce and Diverse Distribution Avenues

Direct-to-consumer channels are simplifying the process from manufacturing to the end-user, making it easier to implement subscription models that ensure steady revenue. Brands like Smart Bottoms and HIRO provide subscription services, delivering fresh cloth diapers every 4 to 6 weeks. These services achieve repeat purchase rates of over 40%, with customer lifetime values ranging from USD 500 to USD 1,200, particularly for organic-focused brands. In 2025, Amazon's U.S. baby-care category saw an increase in cloth diaper listings. During the two years leading up to April 2025, imports from China tripled by weight as manufacturers used lower labor costs and government subsidies to offer more competitive prices than Western brands. Influencer marketing has become a key tool for product discovery. For example, Caden Lane created 920 sponsored posts in the 12 months ending in 2026, with 61% of the content focused on Instagram Reels and 39% on static posts. Activity in December 2025 surged by 48% above the monthly average, targeting holiday gifting demand. Health and specialty stores are enhancing customer experiences by pairing cloth diapers with natural baby-care products. This approach creates a "halo effect," increasing basket sizes by 30% to 50% compared to typical supermarket purchases.

Rising Emphasis on Health of Infant Skin

As parents become more aware of the ingredients in disposable diapers, they are turning to breathable and chemical-free fabrics. In 2025, California and New York introduced ingredient disclosure mandates, revealing that many disposable diaper brands contain small amounts of phthalates, parabens, and synthetic fragrances. These harmful compounds are not found in GOTS-certified organic cotton cloth diapers. For example, Jude's Family's organic cotton inner diaper has a surface pH below 5.5, which helps maintain vaginal pH balance and reduces bacterial growth. In comparison, synthetic nonwovens have pH levels above 7, which can increase the risk of bacterial growth[3]Source: State of California, “Diaper Readability and Ingredient Disclosure Act 2025,” ca.gov. In 2024, the U.S. Food and Drug Administration updated its guidelines, recommending that infant hygiene products minimize formaldehyde exposure. This aligns with the OEKO-TEX Standard 100 Annex 6, which already limits formaldehyde levels to 16 ppm. Bamboo-fiber diapers, known for being naturally hypoallergenic and antibacterial, are emerging as premium options. Supporting this trend, Products On The Go offers patented bamboo wipes that are free from parabens, phthalates, and petroleum-based ingredients, meeting the growing demand for clean-label products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Challenges in cleaning and maintenance | -0.7% | Global, acute in urban Asia-Pacific and MEA with limited washing infrastructure | Medium term (2-4 years) |

| Higher initial investment | -0.9% | Economical-tier markets in South Asia, Sub-Saharan Africa, and Latin America | Short term (≤ 2 years) |

| Limited awareness or misconceptions regarding advantages of cloth diapers | -0.5% | MEA, South America, and rural Asia-Pacific | Long term (≥ 4 years) |

| Facing competition from hybrid diaper options | -0.6% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Challenges in Cleaning and Maintenance

In rapidly growing regions, challenges in washing infrastructure limit adoption, particularly in areas with water shortages or unreliable electricity. Sub-Saharan Africa, where the population is expected to grow from 1.22 billion in 2024 to 2.2 billion by 2054, faces severe water stress in 17 countries. This makes it difficult for many households to wash cloth diapers daily. Similarly, in Asia-Pacific cities, many urban residents lack washing machines in their apartments and rely on shared facilities or hand-washing, which is time-consuming. Disposable diapers help address this issue by saving time and effort. Diaper laundry services, first introduced in the U.S. in 1946, are making a comeback by offering centralized washing and delivery. However, these services are not yet widely available in most emerging markets. In 2023, W. Pelz GmbH introduced a hybrid chassis-and-pad system in Europe. This system allows parents to reuse the outer garment for multiple diaper changes by replacing only the absorbent pad. While this reduces the need for frequent washing, the use of disposable components raises concerns about their environmental impact.

Higher Initial Investment

Despite the promise of long-term savings, upfront costs pose a significant barrier, especially in price-sensitive markets. A complete cloth diaper starter set, which includes 24 diapers, 6 covers, and various accessories, is priced between USD 400 and USD 600. In contrast, disposable diapers cost between USD 0.20 and USD 0.40 each. While families typically spend around EUR 3,000 (equivalent to USD 3,180) on disposable diapers for a single child over a span of 2.5 years, the initial investment in cloth diaper systems can be a financial strain. This is especially true in economies where the median monthly household income is under USD 500. To alleviate this perceived risk, brands like Jude's Family offer a 100-day money-back trial. However, awareness of such initiatives is notably low in emerging markets. Subscription models, like those from Smart Bottoms, offer monthly plans ranging from USD 30 to USD 50, making cloth diapers more affordable by spreading out costs. Yet, these models hinge on a dependable payment infrastructure and consumer comfort with recurring charges, both of which are still maturing in regions like Sub-Saharan Africa and parts of South Asia.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Taped Diapers Dominate Newborn Care; Pull-Ups Accelerate with Potty Training

In 2025, taped diapers accounted for 56.8% of market revenue, highlighting their suitability for newborns and infants who need frequent changes and cannot stand during diapering. These diapers are versatile, fitting babies from birth to toddlerhood, with adjustable closures accommodating weights from 6 to over 35 pounds. For example, bumGenius's Elemental one-size diaper, priced at USD 24.95, adjusts to fit infants from 8 to over 35 pounds, simplifying inventory for retailers and purchase decisions for parents. Taped diapers also allow caregivers to change babies while they lie flat, an essential feature for newborns lacking head and neck control. In the Asia-Pacific region, cultural preferences for traditional cloth diapering, which uses rectangular or prefold designs secured with pins or Snappis, align well with taped diaper designs, further driving their popularity.

Pant-style pull-up diapers are growing at a 6.95% CAGR through 2031, driven by the rise of elimination communication (EC) practices and their convenience for mobile toddlers. According to Judes Family, toddlers using cloth diapers with wetness feedback often achieve potty training about a year earlier than those using disposables, as they can feel moisture and associate it with toileting. A U.S. Patent (20240091079) published in March 2024 introduces a belt-suspended, detachable cloth diaper system that allows front or rear openings, making it easier for caregivers to support EC and potty training without removing outer clothing. Bambino Mio’s Elite Potty Training Pant, launching in March 2026, features a 100% cotton core and OEKO-TEX certified fabrics, targeting toddlers transitioning from diapers to underwear. This stage sees lower brand loyalty, encouraging parents to try new products. Pull-up diapers also cater to adult incontinence users, offering the convenience of standing diaper changes, a feature emphasized in U.S. Patent 20240091079 with its single-hand operation design.

By Price Point: Economical Tier Anchors Mass Adoption; Premium Segment Captures DTC Momentum

In 2025, the economic price tier dominated 62.5% of the market share, driven by affordable mass-market brands sold in supermarkets and hypermarkets. These brands appeal to cost-conscious consumers and benefit from economies of scale. In China's Fujian and Hebei provinces, which produce over 70% of certified cloth diapers, large factories manufacture millions of units annually, offering wholesale prices between USD 0.03 and USD 1.80 per diaper. Similarly, Indian suppliers on TradeIndia list 188 products priced from INR 40 to INR 890 (USD 0.48 to USD 10.68), targeting export markets like Australia, North America, Europe, and the Middle East. The economic tier thrives in emerging markets where median monthly household incomes are below USD 500. However, the upfront cost of USD 400 to USD 600 for a cloth diaper starter set remains a challenge for many families, despite long-term savings over disposable diapers.

The premium segment is growing at a 7.21% CAGR through 2031, led by direct-to-consumer brands offering organic certification, unique designs, and subscription plans. For example, bumGenius's Elemental diaper, priced at USD 24.95 per unit or USD 18.70 in a 24-pack, features 100% organic cotton, adjustable sizing, and free U.S. shipping on orders over USD 100. Premium brands achieve customer lifetime values of USD 500 to USD 1,200 through repeat purchases of accessories and replacements. Subscription models, like Smart Bottoms' plans priced at USD 30 to USD 50, spread costs and ensure recurring revenue, with repeat purchase rates exceeding 40%. In December 2023, Charlie Banana launched 13 new designs in FSC-certified recyclable paper packaging, eliminating plastic. This initiative earned the 2023 Good Housekeeping Sustainable Innovation Award, reinforcing its premium and sustainable positioning.

By Category: Conventional Cloth Retains Cost Advantage; Organic Variants Lead on Health Positioning

In 2025, conventional cloth diapers held a 56.78% market share due to cost-effective materials and established supply chains. Standard cotton and polyester blends, which do not require organic certification, keep production costs low. China's Fujian province supports large-scale manufacturing, with suppliers offering hemp-cotton blends at USD 0.15 to USD 0.40 per unit for bulk orders over 100,000 pieces, making them more affordable than organic options. These diapers also benefit from wide retail availability in supermarkets and hypermarkets, where high-volume products with faster turnover dominate. In emerging markets like Sub-Saharan Africa, South Asia, and Latin America, households with median monthly incomes below USD 500 prioritize affordability over organic certification. Additionally, conventional diapers avoid the lengthy 6-to-12-month GOTS v8.0 certification process, enabling quicker product launches and faster adaptation to fashion trends.

Organic and natural cloth diapers are growing at a 7.99% CAGR through 2031, the fastest among all segments, as parents increasingly prefer chemical-free and sustainably sourced products. GOTS v8.0 certification, requiring 95% organic fibers and banning harmful chemicals, is now essential for brands targeting health-conscious consumers in North America and Europe. Judes Family’s 12-layer organic cotton weave, made in Europe, ensures quick liquid absorption and maintains a skin-friendly pH below 5.5. Products On The Go, with U.S. Patent 11,490,770 granted in November 2022, offers biodegradable bamboo-fiber diaper liners that are hypoallergenic and antibacterial, addressing concerns about chemical exposure. Regulatory changes, such as California and New York’s 2025 ingredient disclosure laws, require disposable diaper brands to list all chemical components. Organic cloth diaper producers already meet these transparency standards, giving them a competitive edge as clean-label preferences grow.

By End-User: Babies Segment Anchors Volume; Adult Incontinence Leads Growth Trajectory

In 2025, the babies segment dominated with a 90.23% market share, driven by the high demand for cloth diapers in infant care. Infants require 6 to 10 diaper changes daily during their first 2.5 years, leading families to spend around EUR 3,000 (USD 3,180) on disposable diapers. Cloth diapers offer a cost-effective alternative, with a one-time investment of USD 400 to USD 600 for a starter set. Retail distribution through baby specialty stores and supermarkets supports this segment, while cultural norms emphasize diapering as essential for infant care. Bambino Mio's March 2026 SS26 collection, featuring 15 new OEKO-TEX certified prints and an updated reusable nappy, targets millennial and Gen Z parents who often share diapering choices on social media. In the Asia-Pacific region, cultural preferences for reusable diapers and cost-consciousness contribute to a 42.3% market share for cloth diapers in 2024.

The adult segment, though smaller at 9.77% of the volume in 2025, is growing at 8.34% CAGR through 2031, driven by aging populations in developed markets. Group A countries, including China, Japan, and Germany, face a 14% population decline by 2054, but the share of people aged 65 and older is rising, increasing demand for adult incontinence solutions. Reusable products like EcoAble's Pull-On Diaper 2.0 (USD 44.99–50.99) and LeakMaster's Adult AIO (USD 42.95) offer cost savings compared to disposable briefs priced at USD 0.80–1.50 per unit. U.S. Patent 20240091079, published in March 2024, introduced a belt-suspended, detachable cloth diaper system for both infant potty training and adult incontinence care, enabling easier use for caregivers. Healthcare partnerships are also growing, with nursing homes and assisted living facilities adopting reusable adult cloth diapers to cut waste disposal costs and meet sustainability goals.

By Distribution Channel: Supermarkets Leverage Foot Traffic; Health Stores Capture Premium Shift

In 2025, supermarkets and hypermarkets held 35.43% of the market share, driven by high foot traffic, convenient one-stop shopping, and competitive pricing for economical cloth diapers. These stores leverage strong ties with mass-market brands and cross-merchandise cloth diapers with baby food, formula, and disposable diapers, encouraging impulse purchases. Immediate product availability gives them an edge, especially for parents needing urgent diaper restocks. Their dominance is notable in emerging markets where e-commerce is underdeveloped, and cash transactions are common. However, supermarkets face challenges like low margins from budget pricing and limited ability to educate consumers, restricting their growth in the premium and organic segments.

Health and specialty stores are growing at an 8.23% CAGR through 2031, the fastest among distribution channels. These stores pair cloth diapers with natural baby-care products, boosting basket sizes by 30% to 50% compared to supermarkets. Parents often buy organic diapers along with chemical-free wipes, plant-based detergents, and wooden toys, increasing revenue per visit. Trained staff provide education on certifications and washing practices, easing concerns for first-time buyers. Premium brands like Jude's Family and Bambino Mio use these stores for launches, offering in-store demos and 100-day trial programs to build trust. Influencer campaigns also drive growth; for example, Caden Lane's 920 Instagram posts in 2026, with 77.2% using Reels, created awareness that translated into in-store purchases.

Geography Analysis

In 2025, Asia-Pacific generated 39.4% of global cloth diaper revenue, driven by manufacturing hubs in China's Fujian (Quanzhou, Jinjiang) and Hebei provinces. Over 70% of certified producers in these areas operate large factories with capacities in the millions. Minimum order quantities range from 50,000 to 340,000 pieces, with unit prices between USD 0.03 and USD 1.80, depending on customization and organic certification. Indian suppliers from cities like Delhi, Mumbai, Chennai, Pune, and Tirupur offer 188 products on TradeIndia, priced between INR 40 and INR 890 (USD 0.48 to USD 10.68), targeting export markets such as Australia, North America, Europe, and the Middle East. Domestically, cultural preferences for reusable diapers and cost sensitivity support market growth in the Asia-Pacific region in 2024. Awareness of GOTS and OEKO-TEX certifications remains limited to urban, high-income groups. The China International Baby & Kids Expo in Guangzhou, with 1,500 exhibitors annually, is a key platform for global buyers seeking private-label manufacturing partnerships.

The Middle East and Africa are the fastest-growing regions, with a 7.45% CAGR projected through 2031. Sub-Saharan Africa’s population is expected to grow from 1.22 billion in 2024 to 2.2 billion by 2054, outpacing waste management infrastructure. Water scarcity in 17 Sub-Saharan countries limits daily washing of cloth diapers, creating demand for hybrid systems or centralized laundry services, which are still emerging. Indian manufacturers target these markets with competitively priced cloth diapers ranging from INR 40 to INR 200 (USD 0.48 to USD 2.40), offering affordable solutions in regions where median monthly household incomes are below USD 500. In North America and Europe, high disposable incomes drive demand for premium products despite slower volume growth. Brands like bumGenius, Jude's Family, and Bambino Mio attract eco-conscious parents with GOTS certification and direct-to-consumer subscription models.

South America, led by Brazil, Argentina, and Colombia, holds a smaller market share but benefits from influencer marketing targeting Portuguese- and Spanish-speaking audiences. For instance, Caden Lane’s 920 sponsored posts in the year leading to 2026 included 3.0% focused on Brazil, signaling early brand investment. While South America’s regulations are less strict than Europe’s EPR directives, reducing the cost advantage of reusable systems, rising environmental awareness among urban middle-class families is driving trials of organic cloth diapers priced between USD 15 and USD 30 per unit. In North America, e-commerce plays a significant role, with Amazon listings for cloth diapers showing positive year-over-year growth in 2025. Chinese imports have tripled by weight over two years, narrowing price gaps with domestic products. In Europe, strict OEKO-TEX and GOTS compliance requirements create barriers for non-certified manufacturers, protecting premium brands like Judes Family (Germany) and TotsBots (Scotland, rebranded as Real TotsBots after 2023).

Competitive Landscape

The cloth diaper market, characterized by its moderate fragmentation, presents avenues for both established entities and new entrants to carve out their niches through distinct positioning and focused strategies. This fragmented landscape allows specialized firms to flourish in niche areas, especially in organic materials and adult incontinence. In contrast, larger corporations harness economies of scale and extensive distribution networks to secure a widespread market foothold. Notable players in the arena include Quanzhou Unicare Hygiene Products Co., Ltd, Cotton Babies, Inc., Kanga Care, Thirsties Inc., and Mama Koala.

Strategic maneuvers predominantly revolve around vertical integration. Successful firms are taking the reins of their supply chains, overseeing everything from raw material procurement to direct sales to consumers. This hands-on approach not only ensures quality control but also optimizes profit margins, bolstering their competitive stance. Embracing technology has become a pivotal differentiator. Companies are channeling investments into advanced manufacturing techniques and honing their digital marketing prowess to effectively engage their desired audiences. A case in point is The Honest Company. Their initiative underscores a commitment to clean ingredients and eco-friendly practices. They've adeptly maintained a broad market reach, thanks to collaborations with retail giants like Target and Amazon.

Yet, the adult incontinence sector beckons with promise. Here, reusable products stand out, offering healthcare institutions notable cost efficiencies. Additionally, emerging markets are witnessing a push for cloth diaper adoption, buoyed by supportive government initiatives. Newer players are harnessing the power of social media and direct sales models, rapidly amplifying brand visibility and fostering customer loyalty. Meanwhile, seasoned companies are not resting on their laurels. They're actively pursuing acquisitions and channeling funds into innovation, ensuring they remain pertinent in this swiftly changing market landscape.

Cloth Diaper Industry Leaders

Quanzhou Unicare Hygiene Products Co., Ltd.

Cotton Babies, Inc.

Thirsties Inc.

Hong Kong Mama Koala Co., Limited (Mama Koala)

Kanga Care

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Kanga Care LLC, the parent company of the award-winning Rumparooz One Size Cloth Diaper brand, announced its acquisition of GroVia, a prominent name in modern cloth diapering. This strategic move united two pioneering brands, both committed to sustainable parenting, industry innovation, and global family support.

- May 2025: Cottonsie launched its new diapering solution for parents who prioritize sustainability and natural ingredients in their baby care products. Cottonsie has replaced plastic with 100% breathable cotton in key diaper layers, including the top sheet, back sheet, acquisition distribution layer (ADL), and core wrap.

- January 2025: Kanga Care LLC, a pioneer and leader in the cloth diaper industry, announced a licensing partnership with Kinder Cloth Diaper Co. This agreement made Kinder Cloth Diaper Co. the third company authorized to incorporate Kanga Care’s patented Double Inner Gusset Technology into their cloth diaper designs. Effective immediately, the collaboration allowed Kinder Cloth Diaper Co. to utilize this innovative leak prevention technology to elevate their product offerings.

Global Cloth Diaper Market Report Scope

| Taped Diapers |

| Pant/Pull-Up Diapers |

| Others |

| Economical |

| Premium |

| Organic/Natural |

| Conventional |

| Babies |

| Adults |

| Supermarkets/Hypermarkets |

| Health and Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Taped Diapers | |

| Pant/Pull-Up Diapers | ||

| Others | ||

| By Price Point | Economical | |

| Premium | ||

| By Category | Organic/Natural | |

| Conventional | ||

| By End-User | Babies | |

| Adults | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global cloth diaper market?

The cloth diaper market size reached USD 7.66 billion in 2026 and is forecast to climb to USD 10.32 billion by 2031, expanding at a 6.15% CAGR over 2026-2031.

Which region leads sales today?

Asia-Pacific generated 39.4% of global revenue in 2025, anchored by large manufacturing hubs in China that support competitive pricing.

Why are premium organic cloth diapers growing faster than conventional options?

Ingredient-disclosure laws and rising skin-health awareness push parents toward GOTS-certified organic cotton and bamboo fabrics that avoid formaldehyde and phthalates, driving the premium tier’s 7.99% CAGR.

How fast is the adult reusable incontinence segment expanding?

Aging populations in China, Japan, and Germany are propelling adult cloth diaper demand at an 8.34% CAGR, the highest among all end-user groups.

Page last updated on: