Diaper Rash Cream Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

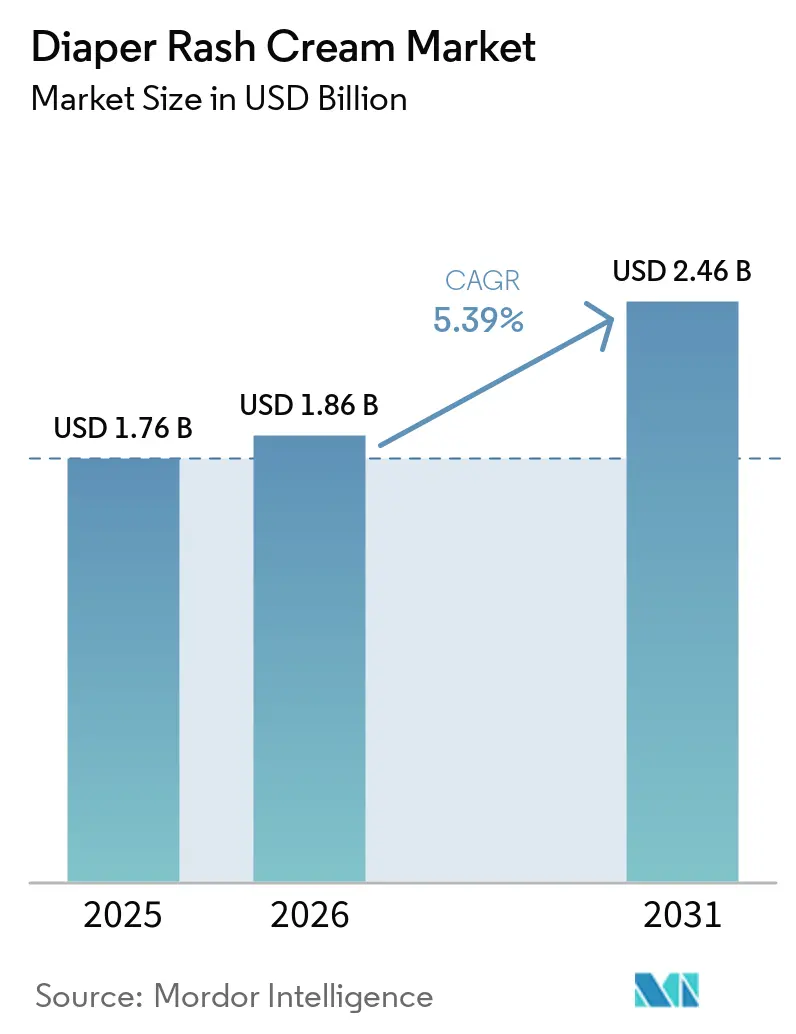

| Market Size (2026) | USD 1.86 Billion |

| Market Size (2031) | USD 2.46 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Diaper Rash Cream Market Analysis by Mordor Intelligence

The diaper rash cream market size is expected to grow from USD 1.76 billion in 2025 to USD 1.86 billion in 2026 and is forecast to reach USD 2.46 billion by 2031 at 5.39% CAGR over 2026-2031. Shifting birth dynamics, an expanding range of adult-incontinence applications, and a move from petrolatum to plant-based emollients are driving product demand. These factors reflect changing consumer preferences and a growing emphasis on sustainability and health-conscious formulations. Innovations in breathable diapers, the rise of subscription-based e-commerce, and the growth of private labels are transforming market strategies, particularly pressuring prices at the budget end. Subscription models, in particular, are enhancing customer retention and providing steady revenue streams for manufacturers. Meanwhile, new U.S. Pharmacopeia PAH testing regulations and limits on zinc-oxide levels are increasing compliance costs, compelling manufacturers to adapt their formulations and processes. In response, manufacturers are turning to premiumization, bolstered by clinical endorsements from dermatologists and sustainability certifications, which help differentiate their products in a competitive market. As a result, the baby diaper rash cream market is evolving into a barbell structure: while high-zinc-oxide ointments and multifunctional balms are reaping rewards due to their targeted benefits and clean-label appeal, mid-priced preventive products are feeling the squeeze on margins, struggling to maintain profitability amidst rising costs and competitive pressures.

Key Report Takeaways

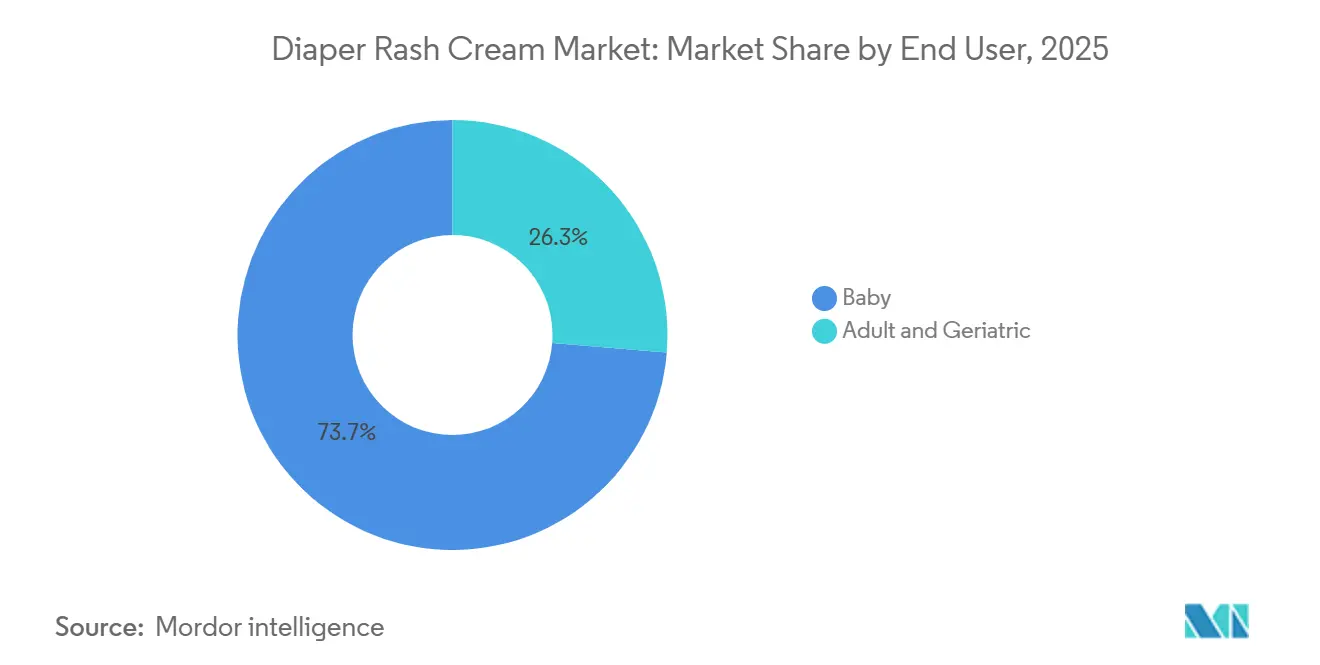

- By end user, babies held 73.17% of the baby diaper rash cream market share in 2025 while the adult and geriatric segment is projected to expand at 6.14% CAGR through 2031.

- By category, mass-market formulations accounted for 65.62% of the baby diaper rash cream market size in 2025; premium and clean-label variants are forecast to grow at 5.42% CAGR between 2026-2031.

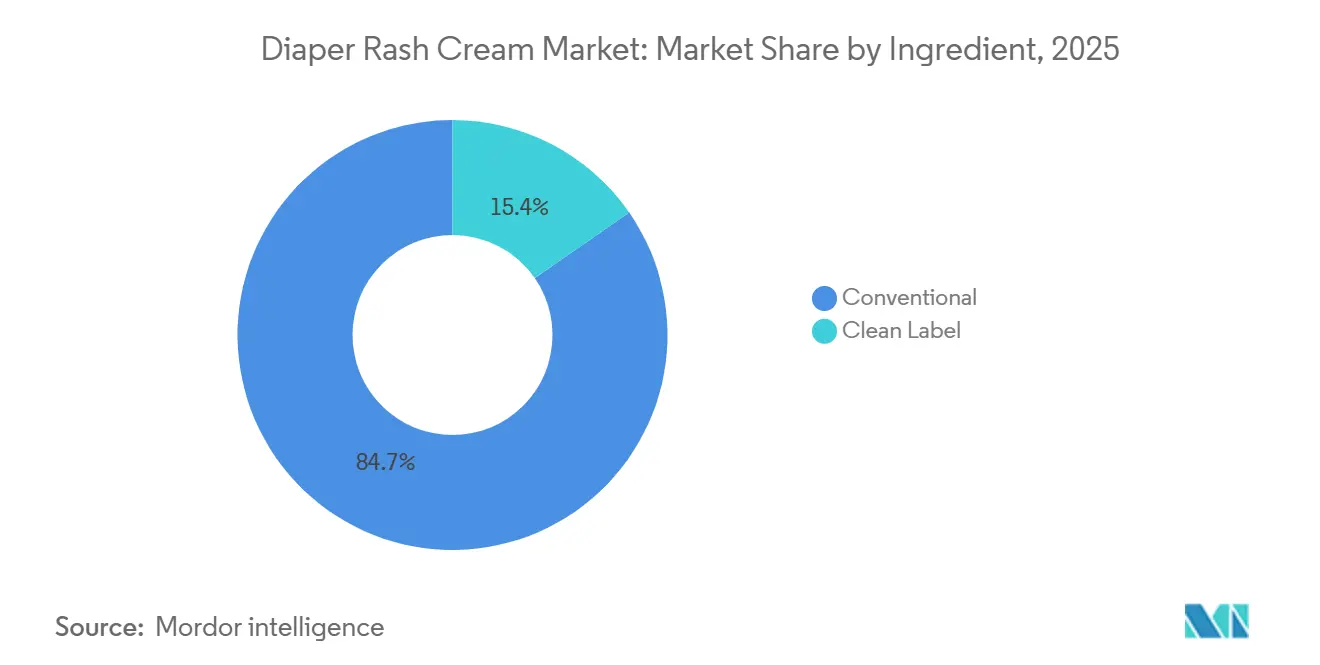

- By ingredient, conventional zinc-oxide products captured 65.62% baby diaper rash cream market share in 2025, whereas plant-based and organic alternatives are expected to advance at 5.42% CAGR over 2026-2031.

- By distribution channel, supermarkets/hypermarkets retained 39.23% of the 2025 revenue, but online retail is set to rise at 5.76% CAGR through 2031.

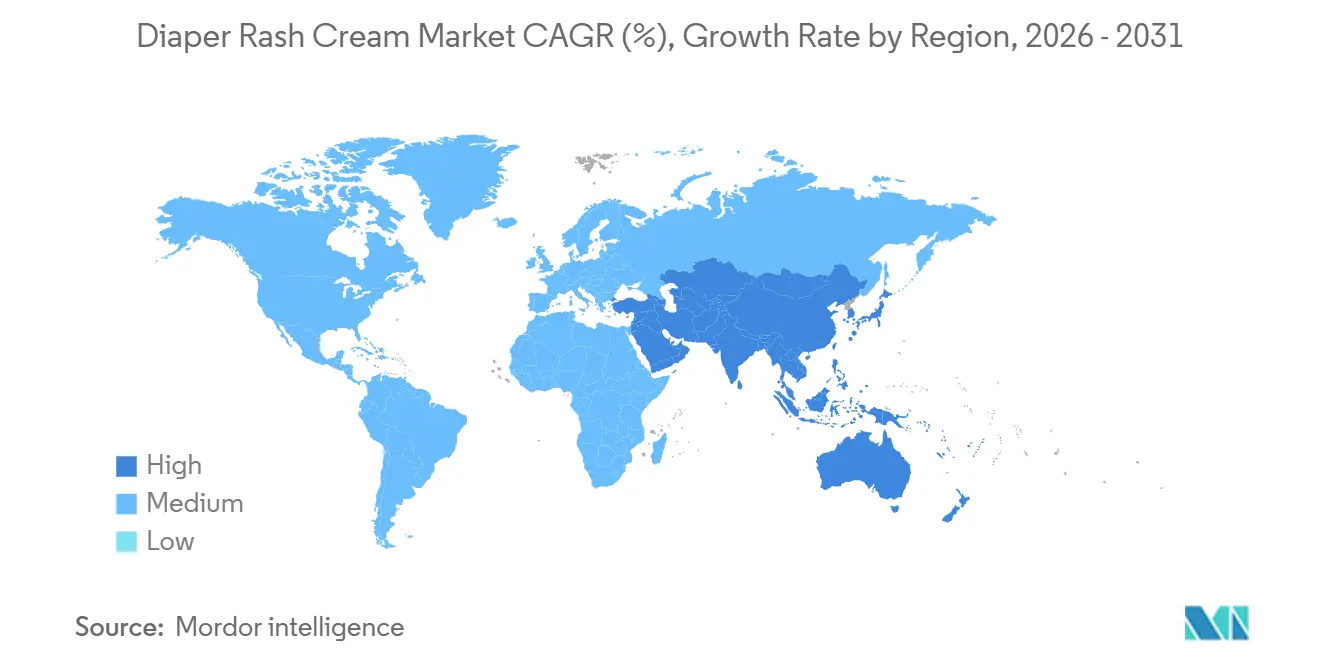

- By geography, North America led with 33.38% of 2025 sales, yet Asia-Pacific is projected to record the fastest 5.65% CAGR through 2031 .

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Diaper Rash Cream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing preference for high-potency zinc-oxide formulations | +0.9% | North America, Europe | Medium term (2-4 years) |

| Rapid growth of online baby-care retail channels | +1.2% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Expansion of the adult incontinence consumer segment | +0.7% | North America, Europe, Japan | Long term (≥ 4 years) |

| Rising traction for natural and zinc-oxide-free alternatives | +0.8% | North America, Europe, Australia | Medium term (2-4 years) |

| Introduction of multifunctional 3-in-1 cleanse-hydrate-protect bars | +0.5% | Europe, North America | Medium term (2-4 years) |

| Advances in breathable diaper technology driving complementary cream usage | +0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing preference for high-potency zinc-oxide formulations

Desitin Maximum Strength, in a company-sponsored pediatric study, demonstrated a 20% reduction in erythema within three hours, establishing high-concentration ointments with up to 40% zinc oxide as the clinical standard for treating severe dermatitis. While the U.S. FDA allows ointments to contain up to 40% zinc oxide, the EU imposes a 25% cap and prohibits spray formats to reduce inhalation risks[1]Source: U.S Food and Drug Administration," Skin Protectant Drug Products for Over-the-Counter Human Use", fda.gov . Brand owners, aiming for dermatologist endorsements and commanding price premiums of 20-40%, are infusing ceramides and provitamin B5 into their products. This strategy is underscored by the March 2026 debut of Aquaphor Baby Sensitive Lotion. Following warnings from scientific committees about the photoclastogenic effects of particles smaller than 30 nm, parents are increasingly gravitating towards “non-nano” labels. This shift has led to prominent “non-nano” claims on packaging in both U.S. mass and European pharmacy outlets. These trends highlight the growing consumer demand for safer and dermatologist-recommended formulations in the baby care market.

Rapid growth of online baby-care retail channels

In 2025, e-commerce accounted for over a third of the global baby-care market, with subscription programs for diaper rash creams boasting retention rates exceeding 70% over six months, as highlighted in filings from Amazon and Walmart. Digital retail not only offers detailed ingredient transparency and real-time parent reviews but also features exclusive marketplace items, like The Honest Company's Disney-branded line, which made its debut in September 2025. The Asia-Pacific region is outpacing traditional brick-and-mortar stores: mobile-centric applications are granting caregivers in tier-2 cities of India and Indonesia swift access to clean-label imports, effectively narrowing the historical distribution divide. This shift is driven by increasing smartphone penetration and improved internet connectivity in these regions. Consequently, online sales of diaper rash creams are growing at a 5.76% CAGR, challenging the supremacy of supermarkets, all while benefiting from repeat-purchase behavior that bolsters unit economics.

Expansion of the adult incontinence consumer segment

In response, institutional care protocols are increasingly adopting pediatric-like regimens, emphasizing barrier ointment application at every change. In Spain, pharmacies consistently report a steady demand for Bayer's Bepanthen, a 5% dexpanthenol tube priced between EUR 7-12 (USD 7.5-12.9). This trend highlights caregivers' readiness to pay a moderate premium for incontinence-related dermatitis treatments. Given that adult skin is thinner, frequently medicated, and subjected to prolonged wear, manufacturers are pivoting. They're reformulating products with higher-viscosity petrolatum bases or vegetable-wax systems to prevent migration. These reformulations aim to enhance product efficacy and ensure better skin protection for elderly users. While nursing homes rely on institutional bulk packs, family caregivers show a preference for smaller, fragrance-free tubes, ensuring overnight protection.

Rising traction for natural and zinc-oxide-free alternatives

In 2023, Consumer Reports flagged potential PAH contamination in petrolatum and mineral oil, drawing heightened scrutiny despite FDA's safety nod. Brands like Curasalve and Alphanova Bébé are now pivoting: they're infusing calendula-based balms with olive oil, jojoba oil, and beeswax, often pairing these with non-nano zinc oxide or skipping zinc altogether. Responding to these industry shifts, the German Federal Institute for Risk Assessment has called for a reduction in MOAH impurities. They've advocated for the use of UV-refined petrolatum or vegetable substitutes. While challenges like oxidation persist, they're being tackled with natural antioxidants such as tocopherols. This shift has propelled clean-label SKUs to achieve a 5.42% CAGR, making inroads into pharmacies that once leaned heavily on traditional petrolatum ointments. The growing consumer preference for safer and more sustainable products is driving this transition in the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reduced incidence of skin rashes driven by advanced breathable diaper designs | -0.7% | Europe, Asia-Pacific | Medium term (2-4 years) |

| Regulatory constraints on over-the-counter zinc-oxide concentration levels | -0.4% | Europe, North America | Short term (≤ 2 years) |

| Rising sustainability concerns over petrolatum- and mineral-oil-based formulations | -0.5% | Europe, North America, Australia | Medium term (2-4 years) |

| Intensifying price competition from private-label diaper rash creams | -0.8% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Reduced incidence of skin rashes driven by advanced breathable diaper designs

Microporous films, boasting breathability levels surpassing 5,000 g/m²·24 h, are curbing the volume of preventive creams as instances of diaper rash decline. Ontex’s Climaflex channels and WEHOO Hygiene’s AIR-Hoo backsheet not only mitigate humidity but also promote extended all-night usage. This extension increases exposure time. Newclears, a Chinese contract manufacturer, highlights a fivefold surge in breathable diaper volumes from 2019 to 2023, juxtaposed with a 20% decline in conventional lines, signaling a shift in category dynamics. This trend underscores the growing consumer preference for products that combine comfort with enhanced functionality. In response, manufacturers are intensifying their marketing of maximum-strength ointments for urgent needs and pairing creams with overnight diaper SKUs to maintain their market relevance. Additionally, companies are leveraging these innovations to differentiate their offerings in an increasingly competitive market.

Regulatory constraints on over-the-counter zinc-oxide concentration levels

While the FDA permits ointments to contain up to 40% zinc oxide, EU regulations impose a stricter limit of 25% and outright ban sprays. This discrepancy necessitates dual formulations for manufacturers, complicating inventory management. In the wake of Brexit, the UK introduced new substance limits in January 2025, with a sell-off deadline stretching to October 2026. Meanwhile, harmonized petrolatum monographs from the United States Pharmacopeia, set to take effect in August 2026, will require UV absorbance testing for PAHs. This mandates refineries to either upgrade their processes or transition to vegetable waxes. Such global inconsistencies not only challenge the "maximum strength" branding outside North America but also inflate compliance costs, particularly for smaller brands. Additionally, these regulatory variations create barriers to market entry for new players, further consolidating the industry. Companies must now allocate significant resources to regulatory compliance, diverting focus from innovation and product development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Adult Upswing Alters Demand Mix

In 2025, baby diaper rash creams command a dominant 73.17% market share, bolstered by consistently high diaper usage and strong global brand penetration. However, with the rise of breathable diapers leading to fewer rashes, growth in this segment shows signs of moderation. In a strategic pivot, leading brands are enhancing their premium status, incorporating advanced ingredients like ceramides and hyaluronic acid. These upgrades not only aim to draw in consumers but also offset the slowdown in growth. Additionally, the increasing awareness of baby skincare among parents is driving demand for high-quality products. Companies are also leveraging digital marketing channels to educate consumers and promote their premium offerings.

The adult and geriatric segment is the fastest-growing, boasting a CAGR of 6.14% from 2026 to 2031. This growth is driven by global longevity and an increasing prevalence of incontinence among the elderly. Demand varies by channel: care facilities prefer institutional bulk packaging, while retail consumers gravitate towards smaller, fragrance-free options. Innovations focus on long-wear adhesion and effective odor control. Furthermore, the growing acceptance of adult incontinence products is reducing stigma and encouraging adoption. Manufacturers are also investing in research and development to create more discreet and comfortable solutions for end-users.

By Category: Premium Tier Harvests Clean-Label Loyalty

In 2025, the mass-market segment is set to dominate, capturing 65.62% of total revenue. This stronghold is attributed to its affordability, broad accessibility, and robust distribution channels in both developed and emerging markets. Even amidst rising competition, mass brands are staying relevant by integrating functional ingredients like ceramide blends. They're also rolling out value multipacks to cater to price-sensitive shoppers and secure their shelf presence. Concurrently, retailers are bolstering their private label offerings, intensifying the competitive landscape in this segment.

Meanwhile, the premium and clean-label segment is on a rapid ascent, projected to grow at a CAGR of 5.42% from 2026 to 2031. This surge is largely driven by millennial parents, who are increasingly willing to shell out a 20–40% premium for hypoallergenic and safer product formulations. North America and Germany stand out as key markets for this segment, where endorsements from dermatologists and sustainability certifications play a pivotal role in shaping purchasing choices. Brands are capitalizing on these endorsements to carve out a niche and validate their premium pricing. With a growing consumer consciousness about ingredient safety and environmental ramifications, the appetite for premium products is only set to expand.

By Ingredient: Conventional Dominance Meets Organic Surge

In 2025, conventional zinc-oxide ointments dominate the market, making up 65.62%. Their leading position stems from established clinical validation and a strong consumer trust in petrolatum-based formulations. Widely endorsed for their efficacy in treating and preventing diaper rash, these products benefit from robust availability and affordability, solidifying their stance in global markets. Consequently, they remain the preferred choice for many caregivers. Additionally, their long shelf life and compatibility with sensitive skin further enhance their appeal. The consistent performance of these ointments across diverse demographics underscores their reliability and widespread acceptance.

Petroleum-free and clean-label creams are emerging as the fastest-growing segment, projected to expand at a CAGR of 5.42% from 2026 to 2031. This growth is fueled by a rising consumer appetite for transparency, vegan formulations, and ingredient safety. In response, manufacturers are pivoting, reformulating products with alternatives like shea butter, coconut oil, and beeswax to align with shifting regulatory and consumer demands. While zinc-oxide-free variants hold a niche position, they're gaining momentum, especially within cloth-diaper communities and zero-waste marketplaces. Furthermore, industry innovation is being spurred by regulatory backing, including the European Union's initiative to reduce microplastics and the FDA's leniency towards alternative actives, contingent upon their successful safety and irritation tests[2]Source: U.S Food and Drug Administration, "Maximal Usage Trials for Topically Applied Active Ingredients Being Considered for Inclusion in an Over-The-Counter Monograph: Study Elements and Considerations",fda.gov. The increasing availability of these products in mainstream retail channels is also contributing to their growth. Furthermore, marketing efforts emphasizing eco-friendly and cruelty-free attributes are resonating strongly with environmentally conscious consumers.

By Distribution Channel: Subscriptions Erode Shelf Reliance

In 2025, supermarkets are projected to command a dominant 39.23% share of total sales. Their leading position stems from strong in-store visibility, diverse product assortments, and the convenience they offer for everyday purchases. Shoppers are drawn to supermarkets for their immediate product availability and the opportunity to compare various brands side by side. Moreover, promotional pricing and bundled deals play a pivotal role in driving high sales volumes. This broad accessibility cements supermarkets' status as the go-to shopping destination. Supermarkets also benefit from their ability to cater to a wide demographic, offering products across various price points. Additionally, their integration of private-label brands has further strengthened their market position by providing cost-effective alternatives to consumers.

Online channels are emerging as the fastest-growing segment, boasting a CAGR of 5.76% from 2026 to 2031. This surge is largely attributed to subscription-based models that not only automate replenishment but also provide cost-saving incentives, especially appealing to parents. The e-commerce boom is notably vibrant in emerging markets like India and Indonesia, where digital adoption is on a steep rise. The integration of mobile wallets streamlines transactions, promoting repeat purchases through effortless reordering. Consequently, direct-to-consumer strategies are becoming increasingly popular, significantly influencing buying habits. The growing penetration of smartphones and affordable internet access in these regions has further accelerated online shopping trends. Furthermore, advancements in logistics and last-mile delivery services are enhancing customer satisfaction and driving sustained growth in this channel.

Geography Analysis

In 2025, North America held a 33.38% share of the baby diaper rash cream market. This was despite declining birth rates, thanks to high per-capita spending and a significant penetration of adult incontinence products. While regulatory leniency on 40% zinc oxide bolstered the market's maximum-strength positioning, private-label brands, driven by retailer data analytics, exerted the most pressure in this region. The growing focus on product innovation and premium offerings has further supported market stability. Additionally, the presence of established players with strong distribution networks ensures consistent product availability.

Asia-Pacific is set to achieve the fastest growth rate, with a projected 5.65% CAGR from 2026 to 2031. This surge is fueled by larger birth cohorts in India and Indonesia, coupled with a trend towards premiumization in urban China. Notably, 53% of mothers in urban China express a preference for natural ingredients. The increasing adoption of e-commerce platforms has also contributed to market expansion, providing consumers with greater access to a variety of products. Moreover, government initiatives promoting maternal and child health in developing countries are expected to further drive demand.

Europe's cosmetic market is on a steady rise, largely due to stringent regulations favoring Ecocert-certified balms and multifunctional liniments. The EU's 25% ceiling on zinc oxide limits brands' differentiation based on potency. In response, brands are now pivoting towards ceramide stacking and securing dermatological seals. The UK's 2024 regulations, effective January 31, 2025, introduced new prohibited and restricted substances, with transitional sell-off deadlines stretching to October 2026[3]Source: Government of the United Kingdom, "The Cosmetic Products (Restriction of Chemical Substances) (No. 2) Regulations 2024", legislation.gov.uk. In Spain, France, and Germany, pharmacies are seeing robust sales for both Bepanthen and up-and-coming local organic brands. Growing consumer awareness about the advantages of organic and dermatologically tested products is influencing buying choices. Additionally, partnerships between manufacturers and pharmacies are bolstering product visibility and fostering consumer trust.

Competitive Landscape

The market exhibits moderate concentration, with Kenvue, Bayer, Beiersdorf, and Prestige Consumer Healthcare leading but ceding ground to retailer private labels. In a significant move, Kimberly-Clark is set to acquire Kenvue for USD 48.7 billion, a deal poised to merge Huggies diapers with Desitin creams, paving the way for innovative cross-category bundles and enhanced data synergies. This acquisition is expected to strengthen Kimberly-Clark's position in the baby care and skincare segments. Additionally, it could create opportunities for leveraging combined distribution networks to enhance market penetration.

Retail giants Amazon, Walmart, and Costco are harnessing the flexibility of private labels to offer lower prices than national brands. Meanwhile, The Honest Company and Babo Botanicals are appealing to the clean-label demographic, boasting endorsements from EWG and OEKO-TEX. These endorsements help build trust among consumers who prioritize safety and transparency in product formulations. Furthermore, private labels are increasingly adopting similar certifications to compete in the clean-label segment, intensifying market competition.

Competition is increasingly shaped by environmental, social, and governance (ESG) factors. Brands that advocate for carbon-neutral production or employ sugarcane-based tubes are enjoying heightened shelf visibility, particularly in Europe and coastal U.S. states. Here, eco-consciousness plays a pivotal role in parental buying choices. The growing demand for sustainable products is also driving innovation in eco-friendly raw materials and manufacturing processes. As a result, companies are forming strategic partnerships with suppliers to secure sustainable inputs and maintain a competitive edge.

Diaper Rash Cream Industry Leaders

-

Prestige Consumer Healthcare

-

Bayer AG (A+D)

-

Johnson & Johnson (Desitin)

-

Beiersdorf AG (Aquaphor)

-

Summer Laboratories (Triple Paste)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CVS Health has unveiled a major packaging overhaul for its health and wellness range, notably including diaper rash creams. The revamped labels prioritize simplicity and clearer product benefits. By 2026, this initiative aims to encompass almost 3,000 products, marking a substantial commitment to bolstering private label competitiveness and elevating the customer experience.

- February 2025: Fixderma, a brand celebrated for its dermatologist-endorsed skincare solutions, has made a foray into the baby care sector with its latest product line, Hoopoe. This initiative highlights Fixderma's strategic pivot, transitioning from adult skincare to meet the escalating global appetite for safe, scientifically formulated baby products.

- January 2025: Sudocrem, the renowned Irish diaper rash cream, has officially launched nationwide on Amazon in the U.S. This marks the first time American households can directly access the celebrated cream, building on its storied legacy in Ireland, the UK, and Canada.

- January 2024: CITTA has bolstered its reputable baby care range by introducing the CITTA Diaper Rash Cream, specifically formulated to alleviate diaper rash in newborns and infants.

Global Diaper Rash Cream Market Report Scope

Diaper rash creams are designed to prevent, soothe, and treat skin irritations in both infants and adults, often caused by prolonged exposure to moisture, friction, and other irritants. By end-user, the market is segmented into baby, adult, and geriatric. Based on the category, the market is segmented into clean label and conventional. By distribution channel, the market is segmented into pharmacies, online retail stores, supermarkets/hypermarkets, and others. The report offers a detailed analysis of major economies across North America, Europe, Asia-Pacific, South America and Middle East, and Africa.

| Baby |

| Adult and Geriatric |

| Mass |

| Premium |

| Organic |

| Convetional |

| Pharmacies and Drug Stores |

| Online Retail Stores |

| Supermarkets/Hypermarkets |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By End User | Baby | |

| Adult and Geriatric | ||

| By Category | Mass | |

| Premium | ||

| By Ingredient | Organic | |

| Convetional | ||

| By Distribution Channel | Pharmacies and Drug Stores | |

| Online Retail Stores | ||

| Supermarkets/Hypermarkets | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the diaper rash cream market?

The diaper rash cream market size reached USD 1.86 billion in 2026 and is forecast to hit USD 2.46 billion by 2031 at a 5.39% CAGR.

Which region leads the diaper rash cream market?

North America led with 33.38% revenue share in 2025 due to premium product uptake and strong retail infrastructure.

Which segment is growing fastest within the diaper rash cream market?

The adult-geriatric end-user segment is projected to post the highest 6.14% CAGR during 2026-2031, driven by rising incontinence prevalence.

How is e-commerce influencing diaper rash cream sales?

Online channels will record a 5.76% CAGR through 2031 as subscription models and direct-to-consumer strategies boost accessibility and brand loyalty.

Page last updated on: