Baby Toiletries Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 94.99 Billion |

| Market Size (2031) | USD 129.16 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

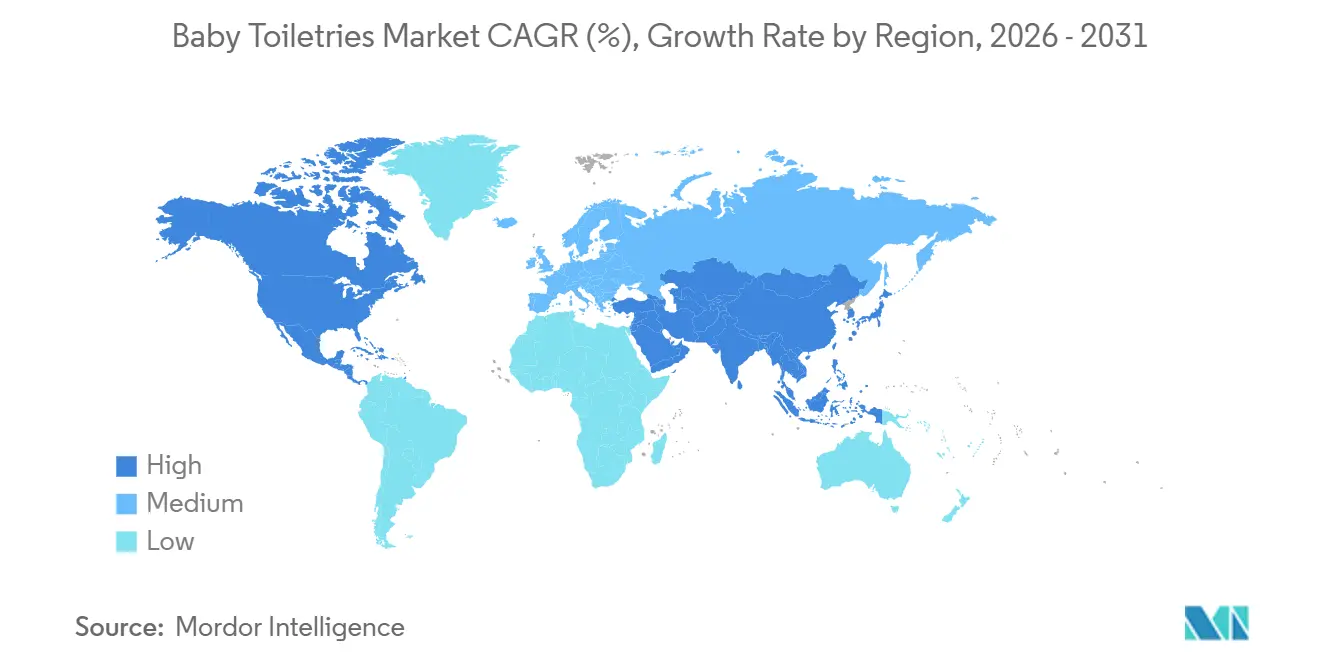

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

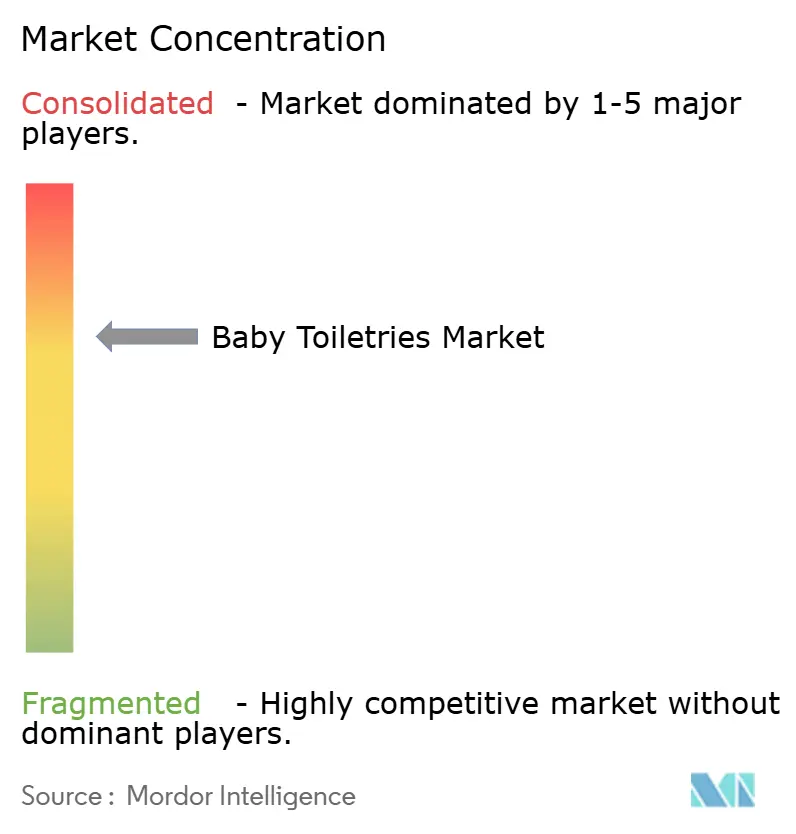

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Baby Toiletries Market Analysis by Mordor Intelligence

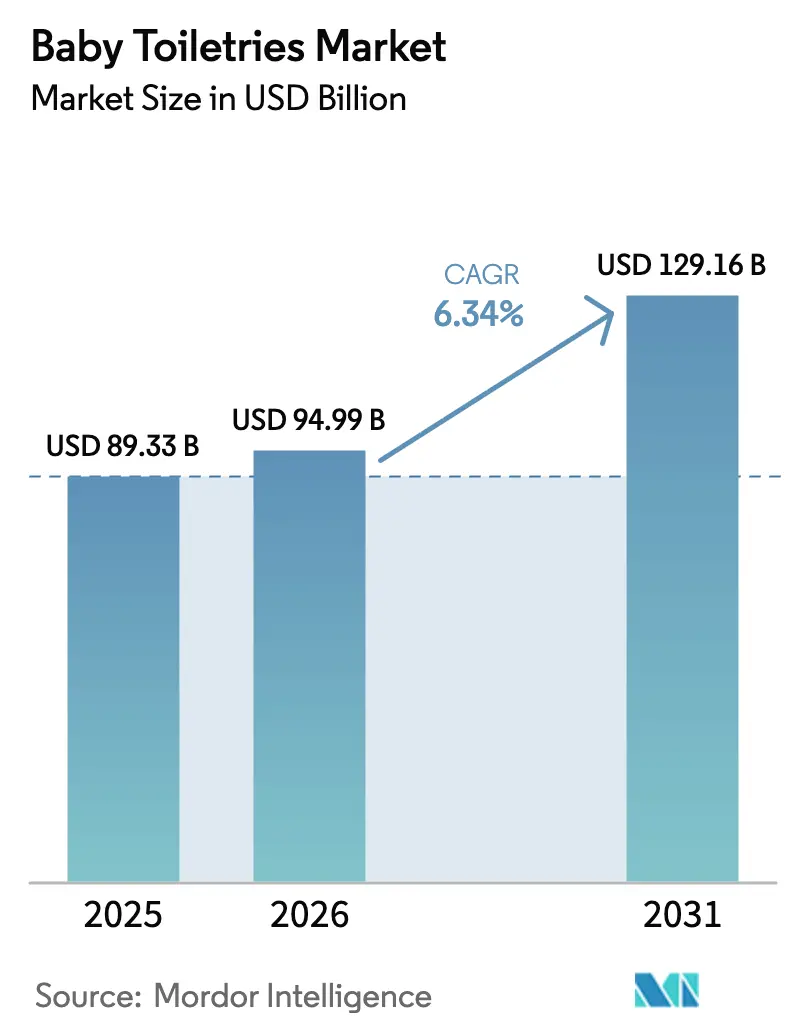

The baby toiletries market size was valued at USD 89.33 billion in 2025 and estimated to grow from USD 94.99 billion in 2026 to reach USD 129.16 billion by 2031, at a CAGR of 6.34% during the forecast period (2026-2031). Continued parental investment in dermatologist-tested formulas, growing adoption of digital retail, and the credibility pediatrician backing lends to online reviews sustain the trajectory. Digital channels convert shoppers faster than traditional media because influencer demonstrations combine product education with real-time safety assurance, an approach that resonates with millennial and Gen Z parents. At the same time, patent-protected absorbent technologies bolster value perception for disposable diapers, while organic certification programs incentivize premium pricing on skin- and hair-care lines. Regional dynamics remain uneven: North America accounts for the largest share of 2025 revenue, but Asia-Pacific is expanding more rapidly as urbanization in India, Indonesia, and the Philippines offsets China’s demographic contraction. Competitive intensity revolves around R&D investments in super-absorbent polymers, microbiome-friendly preservatives, and AI-enabled personalization tools that raise switching costs for caregivers.

Key Report Takeaways

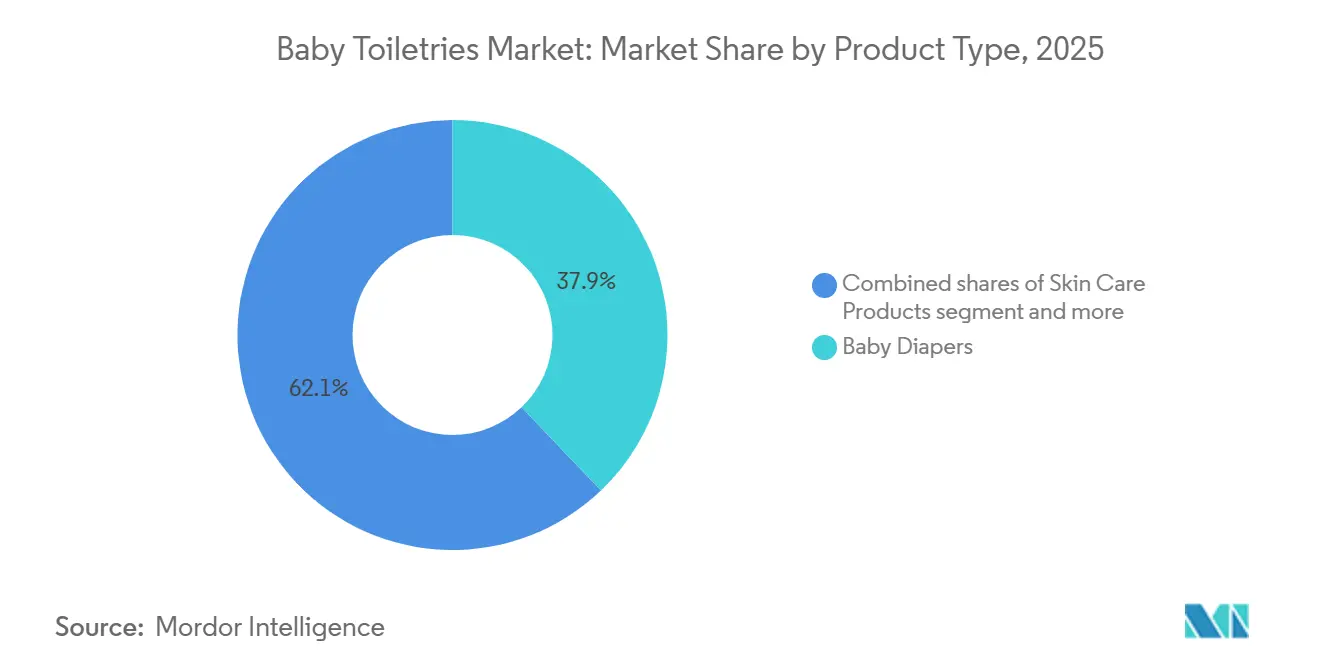

- By product type, baby diapers captured 37.87% of 2025 product-type revenue, whereas skin-care products are forecast to post the fastest 6.77% CAGR to 2031.

- By category, conventional formulations accounted for 78.21% of 2025 sales, while organic and natural variants are projected to grow at a 7.45% CAGR through 2031.

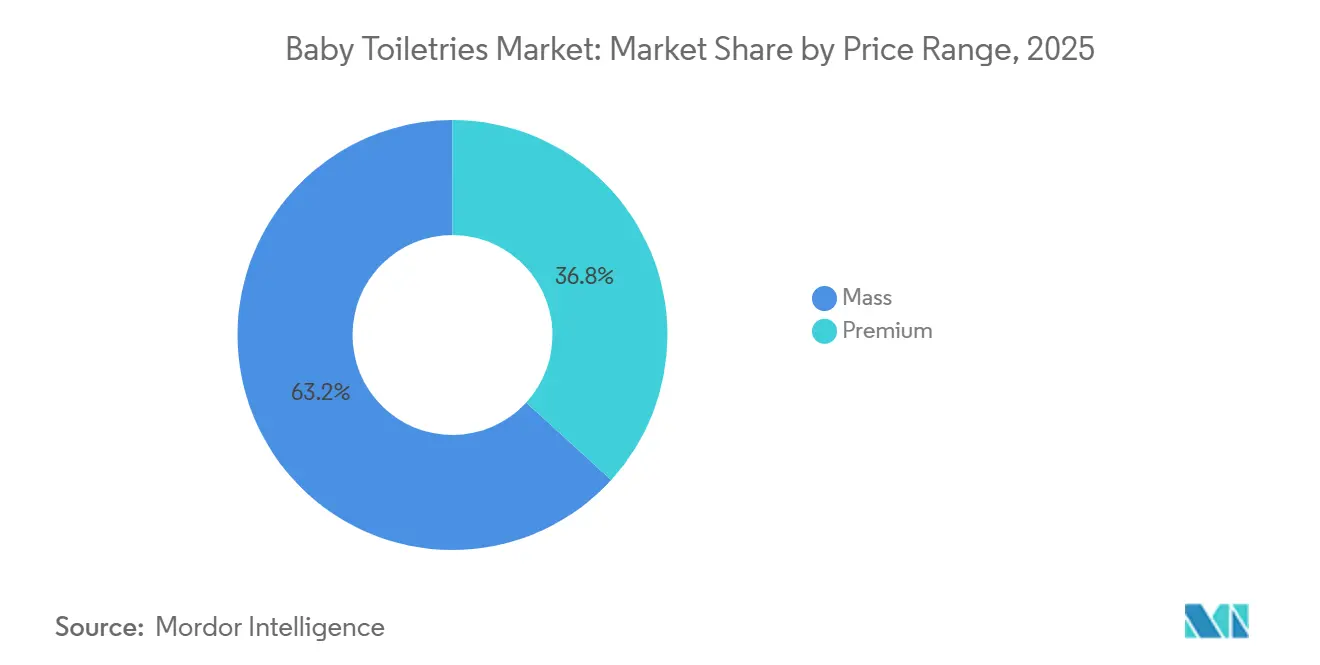

- By price range, mass-market offerings held 63.22% of 2025 revenue; the premium tier is expected to expand at a 7.05% CAGR over the outlook period.

- By distribution channel, supermarkets and hypermarkets led 2025 distribution with 37.21% share, yet online retail stores are on track for a 6.84% CAGR to 2031.

- By geography, North America delivered 34.21% of 2025 global revenue; Asia-Pacific is set to record the highest 7.02% CAGR during the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Baby Toiletries Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing parental awareness of baby hygiene and safety | +1.2% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rising demand for organic and natural formulations | +1.5% | North America, Europe, urban Asia-Pacific | Long term (≥4 years) |

| Rising global birth rates supporting consistent demand | +0.8% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥4 years) |

| Higher parental spending on dermatologist-tested products | +1.1% | North America, Western Europe, affluent Asia-Pacific | Medium term (2-4 years) |

| Collaborations with pediatricians boosting credibility | +0.9% | Global, early gains in North America and Europe | Short term (≤2 years) |

| Strong influence of social media on purchasing decisions | +1.3% | Global, highest in North America and urban Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Organic and Natural Formulations

Organic and natural baby-care lines are expected to outpace conventional products, posting a 7.45% CAGR between 2026 and 2031. Parents focus on certifications such as USDA (United States Department of Agriculture) Organic and COSMOS (COSMetic Organic and Natural Standard) because they provide third-party validation that products exclude parabens, phthalates, and other endocrine disruptors, now flagged by the European Chemicals Agency [1]Source: ECHA (European Chemical Agency), "ECHA takes on additional tasks to strengthen chemical safety in Europe", echa.europa.eu. Major specialty retailers have responded by increasing their organic shelf space; Whole Foods Market reported a significant year-over-year increase in baby-category organic SKUs (Stock Keeping Units) during 2025. Brands that disclose full supply-chain traceability earn Net Promoter Scores 18% higher than competitors relying on generic “gentle” claims. Compliance with the EU Cosmetics Regulation and the U.S. FDA (Food and Drug Administration) Modernization Act 2.0 is accelerating reformulation cycles and pushing manufacturers to invest in botanical-extract standardization alongside ISO 10993 allergen testing.

Strong Influence of Social Media on Purchasing Decisions

Influencer-driven content adds to the overall CAGR, largely because TikTok and Instagram product demonstrations convert at rates 3.5 times higher than banner advertisements. Parenting micro-influencers, those with 10,000 to 100,000 followers, achieve trust scores 40% above celebrity spokespersons, in part due to the authenticity of unedited product trials. Brands now allocate up to 35% of their digital budgets to creators who possess pediatric-nursing credentials or lactation-consultant certifications, a move that bridges marketing and clinical credibility. Hashtag initiatives, such as #BabyCareTruth, generated more than 2 billion impressions in 2025, shaping purchase intent within 48 hours of the campaign launch. The algorithmic preference for short-form video is prompting manufacturers to furnish influencers with dermatologist-validated case studies that verify skin-condition improvements.

Increasing Parental Awareness of Baby Hygiene and Safety

Clinical guidelines from the American Academy of Pediatrics emphasize pH-balanced cleansers and fragrance-free moisturizers, driving product recommendations that flow directly from hospital discharge packs to e-commerce baskets [2]Source: American Academy of Pediatrics, "Fact Checked", aap.org. Telehealth platforms further reinforce evidence-based choices by embedding product links into post-natal care plans, effectively shortening the path to purchase. Recalls of contaminated wipes in 2024 heightened sensitivity to manufacturing quality; ISO 22716 Good Manufacturing Practice certification has since become a baseline retailer requirement in North America and Europe[3]Source: ISO, "ISO: Global standards for trusted goods and services", iso.org. Compliance frameworks such as the Consumer Product Safety Improvement Act mandate third-party verification for heavy metals and phthalates, raising costs for newcomers but elevating overall safety confidence. Collectively, these changes bolster premium spending as parents favor brands that make clinical data public.

Higher Parental Spending on Dermatologist-Tested Products

Dermatologist-tested baby-care SKUs command 15-20% price premiums and add significant share to the sector’s growth. The prevalence of infant atopic dermatitis now ranges between 15% and 20% in developed economies, encouraging health-care providers to recommend hypoallergenic formats that exclude methylisothiazolinone and cocamidopropyl betaine. Manufacturers are channeling USD 50-100 million annually into trials capable of producing peer-reviewed data that satisfy FDA (Food and Drug Administration) Over-the-Counter Monograph requirements for diaper-rash treatments. Co-branding deals with dermatology clinics and children’s hospitals reinforce credibility, while European Medicines Agency guidelines compel age-stratified safety studies that lengthen development cycles but improve product differentiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit or substandard products erode trust | -0.7% | Global, acute in Asia-Pacific and Middle East and Africa | Short term (≤2 years) |

| Stringent regulatory compliance increases costs | -0.9% | Global, highest in European Union and North America | Medium term (2-4 years) |

| Consumer skepticism over ingredient transparency | -0.5% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Limited awareness in rural or developing regions | -0.6% | South Asia, Sub-Saharan Africa, rural South America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Compliance Increases Costs

Divergent safety standards across the European Union, the United States, and China subtract a few percentage points from projected growth. Preparing toxicological dossiers that detail dermal absorption and systemic exposure costs USD 30,000 to USD 80,000 per SKU under the EU (European Union) Cosmetics Regulation. China’s National Medical Products Administration still requires animal testing for certain imports, forcing smaller organic-focused brands to maintain parallel formulations or abandon the market. Although the U.S. FDA Modernization Act 2.0 allows non-animal methods, validating new protocols extends time-to-market by up to 12 months. Retailers have added ISO 22716 accreditation to vendor policies, obliging mid-sized manufacturers to invest USD 0.5-2 million in facility upgrades.

Counterfeit or Substandard Products Erode Trust

E-commerce marketplaces remain vulnerable to counterfeit diapers and wipes as recalls dent brand equity. In 2024, the U.S. FDA issued 47 warning letters for contaminated infant wipes that exceeded microbial limits outlined in USP 61 and 62, prompting widespread consumer alerts. Brands now deploy QR-code authentication and blockchain-enabled traceability, adding USD 0.05-0.15 per unit but restoring confidence among premium shoppers. Regulatory moves such as the EU Market Surveillance Regulation and the U.S. INFORM Consumers Act place responsibility on online platforms to verify seller identities, compelling the integration of AI-driven monitoring systems that flag suspicious listings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Diapers Anchor Revenue While Skin-Care Innovations Accelerate

Diapers represented 37.87% of 2025 revenue, cementing their status as the backbone of the baby toiletries market; advanced super-absorbent polymers now keep skin dry for 12 hours, reducing rash incidence by 30% in clinical trials. Skin-care solutions are projected to deliver a 6.77% CAGR as microbiome-friendly lotions and colloidal oatmeal cleansers gain physician endorsement for atopic-prone infants. Hair-care lines also earn attention, leveraging sulfate-free surfactants that safeguard delicate follicles during the first year of life. Wipes continue to evolve with pH-balanced formulas and biodegradable substrates that comply with flushability standards in Europe and North America. Other categories, such as oral care, sun protection, and insect repellents, remain niche but capture premium price points when formulated without fluoride for infants under 24 months.

Diaper manufacturers increasingly market compostable versions in Europe and parts of North America, a shift spurred by municipal disposal programs and the EU Single-Use Plastics Directive. Although these eco-friendly options cost 20-30% more, surveys show that 40% of affluent parents are willing to pay up for lower landfill impact. The skincare subsegment reflects rising dermatitis prevalence, which now affects one in five infants in high-income regions; products enriched with ceramides and zinc oxide thus command shelf prominence. Regulatory demands under the FDA OTC Monograph and EU Cosmetics Regulation ensure that rash-treatment claims rest on clinical evidence, boosting trust and justifying elevated price tags.

By Category: Conventional Formulations Dominate Yet Organic Variants Surge

Conventional formulas held 78.21% of 2025 sales due to established supply chains and preservative systems that guarantee 36-month shelf lives even in warm climates. Organic-certified alternatives, however, are poised for a 7.45% CAGR as parents scrutinize labels for pesticide residues and heavy-metal contamination. The Environmental Working Group’s public database makes it easy to compare ingredient profiles, encouraging transparent brands to publish third-party audit results. Mass retailers have responded: endcaps devoted to certified-organic products rose across U.S. big-box chains in 2025.

Nevertheless, organic formulators face hurdles because natural preservatives such as radish-root ferment offer shorter efficacy windows, forcing companies to conduct frequent ISO 11930 stability tests. Annual audits mandated by the EU Organic Regulation and the USDA National Organic Program add USD 10,000-30,000 to compliance costs but simultaneously create entry barriers that protect incumbents with robust traceability systems. Enhanced scrutiny of “greenwashing” claims by NSF International and OEKO-TEX further polarizes the baby toiletries market between genuinely certified offerings and value-tier synthetics.

By Price Range: Mass Market Holds Volume While Premium Segment Expands

Mass-market SKUs supplied 63.22% of 2025 revenue through high-velocity channels such as hypermarkets and discount chains, benefiting from manufacturing lines that churn out 500-800 units per minute, keeping diaper prices below USD 0.20 each. The premium tier, however, is projected to grow at a 7.05% CAGR, fueled by dual-income households willing to pay 30-40% more for dermatologist-tested or organic credentials. Subscription models blur lines: direct-to-consumer brands now deliver premium diapers at mid-tier prices by bypassing retail markups and capitalizing on automated replenishment.

Private-label premium lines from major retailers erode share from national brands by offering comparable quality at 15-20% lower price points. Clinical validation remains the central differentiator; companies budget up to USD 100 million annually for pediatric dermatology trials that underpin premium positioning. Regulatory guardrails such as the Consumer Product Safety Improvement Act apply across price tiers, ensuring that safety standards remain uniform and limiting the ability of ultra-low-cost entrants to undercut on compliance.

By Distribution Channel: Supermarkets Lead Yet Online Retail Surges

Supermarkets and hypermarkets controlled 37.21% of 2025 distribution revenue, capitalizing on high foot traffic and bulk discounting that trims per-unit costs by as much as 15%. Nevertheless, online retail is forecast to have a 6.84% CAGR, propelled by mobile-first shoppers who appreciate one-click checkout and doorstep delivery. Subscription services reduce acquisition costs by up to 50% while providing brands with first-party data used for demand forecasting.

Omnichannel tactics merge online ordering with in-store pickup, enhancing convenience without sacrificing the tactile reassurance of physical displays. Pharmacy chains and baby specialty stores preserve relevance by offering staff consultations that help first-time parents navigate ingredient lists, a key defense against pure-play e-commerce. Growing enforcement of the EU Digital Services Act and the INFORM Consumers Act forces platforms to verify sellers, improving trust and encouraging repeat online purchases.

Geography Analysis

North America accounted for 34.21% of 2025 revenue, yet its growth lags the global average because U.S. fertility fell to 1.62 births per woman in 2024. Premiumization compensates for lower unit volumes as parents allocate a higher share of disposable income to dermatologist-validated and organic formulations. Canada mirrors the trend, while Mexico benefits from a younger demographic profile that continues to trade up from economy to mid-tier offerings.

Asia-Pacific is expected to chart a 7.02% CAGR, making it the fastest-growing region in the baby toiletries market. India leads volume expansion, combining a 2.0 fertility rate with rising middle-class incomes and public-health campaigns that emphasize evidence-based hygiene. Urban Indonesia and the Philippines add momentum by adopting e-commerce and subscription models at double-digit annual rates. China’s birth rate slipped to 1.09 in 2024, but per-child spending rises as single-child households trade up to imported brands they view as safer, pushing value sales higher even as volume flattens.

Europe presents moderate growth driven by rigorous safety standards and eco-friendly legislation such as the Single-Use Plastics Directive, which accelerates demand for biodegradable diapers and recyclable packaging. South America offers uneven prospects; Brazil and Argentina wrestle with macroeconomic volatility, yet younger populations and rising hygiene awareness underpin gradual category expansion. In the Middle East and Africa, underdeveloped retail infrastructure restrains premium adoption, but urban enclaves in the United Arab Emirates and South Africa demonstrate strong uptake of certified-organic lines. Overall, regional disparities ensure that the baby toiletries market maintains a diversified growth profile through 2031.

Competitive Landscape

The competitive field scores a moderate concentration scale. Procter & Gamble, Kimberly-Clark, and Unilever rely on global supply chains and deep patent portfolios covering super-absorbent polymers, hypoallergenic surfactants, and microbiome-friendly preservative systems that support 15-20% price premiums. Collectively, these incumbents channel USD 200-500 million per year into R&D, safeguarding their positions in diapers, wipes, and skin care.

White-space opportunities persist in organic skin- and hair-care niches, where insurgents such as The Honest Company, Seventh Generation, and Earth Mama Organics collectively hold significant margin by emphasizing USDA Organic credentials and direct-to-consumer distribution. Subscription models lower customer-acquisition costs and generate data that feed rapid formulation tweaks. Established players respond by striking pediatrician co-branding deals, embedding products in neonatal-intensive-care units, and scaling influencer partnerships that convert social-media engagement into basket additions.

Technology adoption is accelerating. AI-enabled mobile apps diagnose skin conditions, recommend personalized regimens, and trigger automated reorders, increasing stickiness and diminishing price sensitivity. Rising compliance hurdles, ISO 22716 audits, FDA OTC Monograph obligations, and EU Cosmetics Regulation documentation raise the fixed-cost threshold, favouring firms with robust quality systems. As a result, the baby toiletries market is expected to remain moderately consolidated while enabling agile disruptors to thrive in specialized niches.

Baby Toiletries Industry Leaders

-

Kimberly-Clark Corporation

-

Beiersdorf AG

-

Unilever

-

Johnson & Johnson

-

Procter & Gamble

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: TAKE ME HOME, an Israeli textile brand, expanded into baby care with its first full baby care line, including baby soap, shampoo, body oil, face cream, and diaper rash cream, available in major local retail outlets; this marks its entry into the baby toiletries space.

- November 2025: Pampers unveiled what it calls the world’s smallest diaper, designed specifically for preemie infants, emphasizing enhanced fit and care for premature babies as part of the brand’s innovation efforts.

- October 2025: Kimberly‑Clark announced enhanced global strategic partnerships with Baby2Baby, Plan International, Project HOPE, and UNICEF to expand access to essential care, including baby diapers and wipes, improving health and sanitation for millions of women and children across multiple countries.

Global Baby Toiletries Market Report Scope

Baby toiletries are products that are essential for bathing the baby, skincare, and other care products. The baby toiletries products market is segmented by product type into diapers, skincare products, hair care products, bathing products, wipes, and other product types. By category, the market is segmented into organic and conventional. By price range, the market is segmented into mass and premium. By distribution channels, the market is segmented into supermarkets/hypermarkets, specialist retailers, health and beauty stores, and other distribution channels. The market is segmented by Geography into North America, Europe, Asia Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Skin Care Products |

| Hair Care Products |

| Baby Diapers |

| Baby Wipes |

| Other Product Types |

| Organic |

| Conventional |

| Mass |

| Premium |

| Supermarkets/Hypermarkets |

| Beauty and Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Product Type | Skin Care Products | |

| Hair Care Products | ||

| Baby Diapers | ||

| Baby Wipes | ||

| Other Product Types | ||

| Category | Organic | |

| Conventional | ||

| Price Range | Mass | |

| Premium | ||

| Distribution Channel | Supermarkets/Hypermarkets | |

| Beauty and Health Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the baby toiletries market in 2026?

The baby toiletries market size is USD 94.99 billion in 2026, and it is projected to reach USD 129.16 billion by 2031.

Which product category is growing fastest?

Skin-care products are forecast to post the quickest 6.77% CAGR through 2031, driven by microbiome-friendly and hypoallergenic innovations.

Why are organic baby-care products gaining momentum?

Certifications such as USDA Organic and COSMOS provide third-party proof that products exclude harmful chemicals, a priority for millennial and Gen Z parents.

How are counterfeit products being addressed?

Brands now use QR-code authentication and blockchain traceability, while new regulations obligate online marketplaces to verify seller identities, reducing counterfeit incidence.

Page last updated on: