Baby Diapers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 58.14 Billion |

| Market Size (2031) | USD 76.14 Billion |

| Growth Rate (2026 - 2031) | 5.54% CAGR |

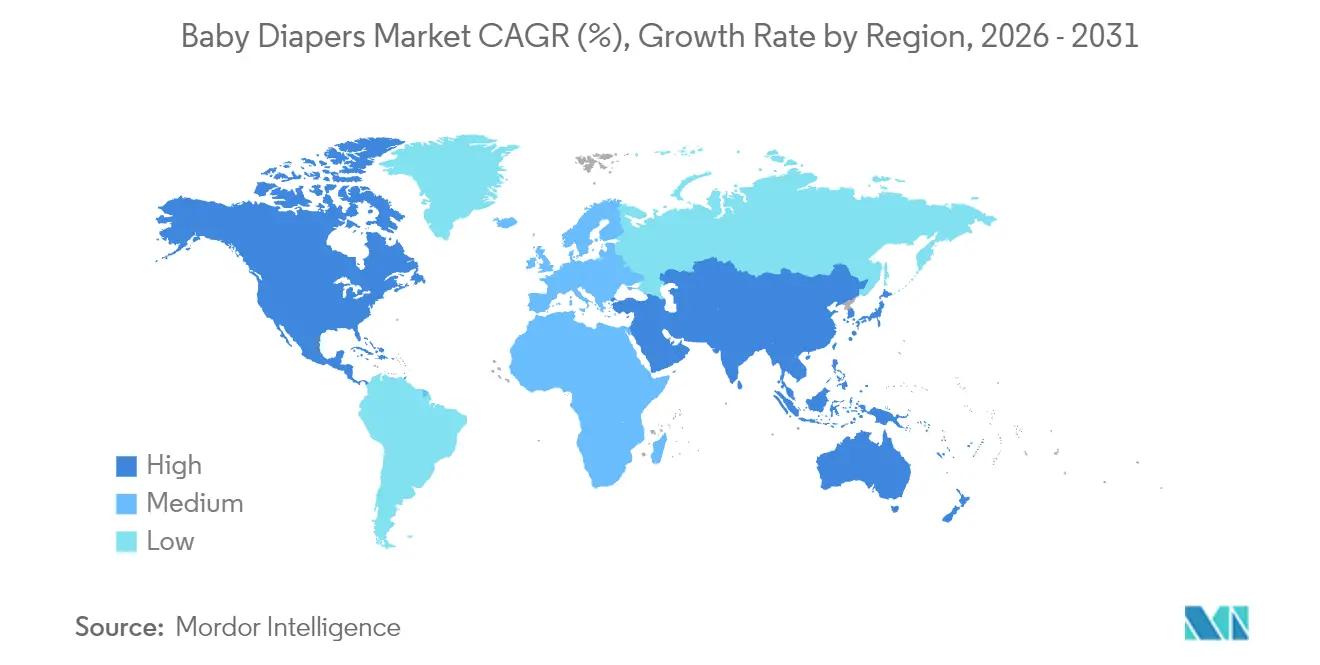

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

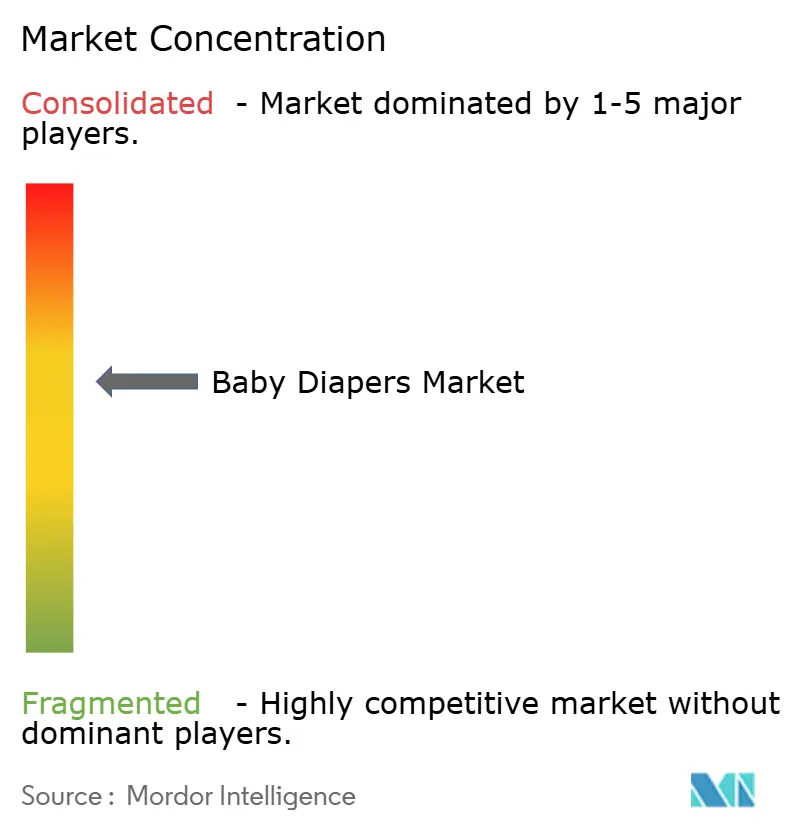

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Baby Diapers Market Analysis by Mordor Intelligence

Baby diapers market size in 2026 is estimated at USD 58.14 billion, growing from 2025 value of USD 55.09 billion with 2031 projections showing USD 76.14 billion, growing at 5.54% CAGR over 2026-2031. Growing awareness among parents regarding the critical importance of hygiene for their babies is driving increased investment in products that ensure cleanliness and comfort. This shift has accelerated the adoption of disposable diapers, which are perceived as more hygienic alternatives to cloth diapers. Key growth drivers now include premiumization, supportive government policies, and the expansion of direct-to-consumer (D2C) retail models, surpassing the influence of birth-rate trends. Industry players are leveraging innovations such as dual-core absorbency, plant-based materials, and subscription-based services to safeguard profit margins and enhance customer retention. Governments in Hong Kong and Singapore are fostering demand through initiatives like newborn bonuses and infant-care subsidies, while the United States is scaling up diaper distribution programs for low-income households. Additionally, advancements in raw materials, particularly biodegradable super absorbents, are transforming sustainability into a strategic revenue opportunity rather than a compliance expense.

Key Report Takeaways

- By product type, disposable diapers held 70.45% of the baby diapers market share in 2025; biodegradable options are forecast to expand at an 8.02% CAGR to 2031.

- By style, pant/pull-up products commanded 57.85% revenue share of the baby diapers market in 2025, while the segment is growing at a 7.05% CAGR through 2031.

- By absorbency technology, standard SAP Core held 55.92% of the baby diaper market share in 2025; dual-core and channel technology forecast 7.55% CAGR through 2031.

- By material type, cotton held 53.02% of the baby diaper market share in 2025, while blended fabrics forecast 7.86% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets led with 42.25% of the baby diaper market size in 2025; online retail is advancing at a 9.95% CAGR to 2031.

- By geography, Asia-Pacific captured 39.10% of the baby diapers market size in 2025, whereas North America records the highest projected CAGR at 9.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Baby Diapers Market*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in birth rates fuels demand for baby diapers | +0.8% | North America, selective Asian markets | Short term (≤ 2 years) |

| Premiumization of baby diapers drives the market | +1.2% | Global, concentrated in developed markets | Medium term (2-4 years) |

| Boom in D2C online-native brands supports market | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Government subsidy programs for infant hygiene | +0.6% | Asia-Pacific, selective European markets | Long term (≥ 4 years) |

| Increasing awareness of infant hygiene drives market growth | +0.7% | Emerging markets, rural penetration focus | Long term (≥ 4 years) |

| Technological advancements in diaper manufacturing enhance product appeal | +1.0% | Global, manufacturing hub concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in birth rates fuels demand for baby diapers

Rising birth rates directly correlate with an increase in the number of potential diaper users, as diapers are a fundamental necessity for infants, typically from birth to the age of three years. This growth in the infant population naturally drives higher diaper consumption. In developed markets, where birth rates have stabilized, demand has shown unexpected resilience, effectively mitigating the impact of demographic challenges. For instance, the United States recorded 3,622,673 births in 2024, reflecting a 1% increase compared to the previous year and marking a reversal of a prolonged decline in birth rates[1]Source: Centers for Disease Control and Prevention, “Births: Provisional Data for 2024”, www.cdc.gov. Additionally, government initiatives, such as Hong Kong's USD 20,000 newborn bonus, highlight how fiscal policies can stimulate artificial demand surges, extending beyond organic population growth trends[2]Source: Chief Secretary for Administration, "Newborn Baby Bonus", www.cso.gov.hk. Companies that strategically adapt their product portfolios, optimize sizing options, and intensify promotional efforts are well-positioned to capitalize on these shifts. In markets where even minor fluctuations in birth rates can significantly influence diaper consumption, such proactive measures can yield substantial competitive advantages.

Premiumization of baby diapers drives the market

Consumers are demonstrating an increasing willingness to pay premium prices for products that offer enhanced performance features, fundamentally altering market dynamics by shifting the focus from volume-driven growth to value-driven strategies. Procter and Gamble's baby care segment serves as a prime example, where a decline in sales volume was offset by revenue stability achieved through the strategic optimization of a premium product mix. This development highlights a critical trend in the market: the ability to capture value through premium offerings is becoming more important than simply driving unit sales. In developed markets, where higher disposable incomes prevail, parents are placing greater emphasis on product efficacy and safety, often prioritizing these attributes over cost considerations. This evolving consumer behavior enables manufacturers to mitigate the impact of rising raw material costs by leveraging pricing power rather than relying solely on volume expansion. Advanced innovations, such as dual-core absorbency technology and the use of organic materials, are commanding significant price premiums that far exceed traditional manufacturing cost differentials. This indicates a strong correlation between the speed of innovation and the potential for margin growth, emphasizing the importance of continuous product development in sustaining competitive advantage.

Boom in D2C online-native brands supports market

Direct-to-consumer (D2C) distribution models are fundamentally transforming traditional retail structures, enabling niche and specialized brands to strategically capture market share through precise positioning and targeted outreach. Online retail channels are experiencing significant growth, far outpacing the growth of traditional supermarket channels. This trend highlights a pronounced consumer preference for the convenience, accessibility, and brand discovery opportunities provided by digital platforms. D2C brands are leveraging innovative strategies, such as subscription-based models and personalized product recommendations, to foster strong customer loyalty while simultaneously reducing customer acquisition costs. These approaches represent a departure from traditional advertising-heavy methods, offering a more cost-efficient and customer-centric alternative. This model is particularly advantageous for eco-friendly and specialty diaper brands, which often face challenges in securing shelf space within conventional retail environments. By utilizing digital marketing techniques and engaging with consumers through social media platforms, these brands can effectively reach their target audience and establish a direct connection with their customer base.

Government subsidy programs for infant hygiene

Policy interventions are driving artificial demand stimuli, enabling market growth to surpass natural demographic limitations. For instance, Singapore's infant care subsidy program provides working families with USD 600 in basic financial support, effectively reducing the economic burden associated with childcare expenses[3]Source: Government of Singapore, “Infant and Child Care Subsidies,” supportgowhere.life.gov.sg , including the cost of diapers. Similarly, the U.S. Department of Health and Human Services has introduced a diaper distribution pilot program, acknowledging that diaper expenses can constitute a significant portion of low-income family budgets and hinder access to childcare services. These initiatives reflect a strategic governmental recognition of diapers as essential commodities rather than discretionary items. Such policy measures have the potential to foster expanded public support, thereby increasing the overall market size beyond the constraints of private consumer purchasing power.

Restraints Impact Analysis of Baby Diapers Market*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent single-use plastic ban legislations | -0.9% | Europe, selective developed markets | Medium term (2-4 years) |

| Volatile SAP and pulp prices compressing margins | -1.1% | Global, manufacturing-dependent regions | Short term (≤ 2 years) |

| High competition among market players | -0.6% | Global, concentrated in mature markets | Long term (≥ 4 years) |

| Limited awareness in emerging economies | -0.4% | Emerging markets, rural focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent single-use plastic ban legislations

Regulatory frameworks targeting plastic waste impose compliance costs and necessitate product reformulations, thereby constraining traditional manufacturing methods. In 2024, the United Kingdom enacted a sweeping ban on plastic-laden wet wipes, granting manufacturers an 18-month window to pivot to plastic-free alternatives. The European Union's Packaging and Packaging Waste Regulation, set to take effect in February 2025, demands that by 2050, all packaging must meet heightened recycling standards and climate neutrality benchmarks. Such regulations compel manufacturers to pivot towards alternative materials and revamped production processes, often leading to heightened initial costs and squeezed profit margins. The Federal Trade Commission mandates scientific backing for claims related to degradability and compostability, curbing manufacturers' tendencies to make unfounded sustainability assertions. As companies navigate these evolving regulatory landscapes, the associated compliance costs and reformulation timelines induce a temporary disruption in the market.

Volatile SAP and pulp prices compressing margins

Volatility in raw material costs exerts significant pressure on profit margins, requiring manufacturers to strategically balance pricing approaches with volume retention in price-sensitive markets. Procter and Gamble's baby care segment reported volume declines due to competitive pricing pressures and rising input costs, highlighting the direct impact of material cost inflation on market dynamics. In diaper production, super absorbent polymer (SAP) and pulp are critical cost drivers, with their price fluctuations influenced by petroleum market trends and disruptions in the forestry supply chain. Manufacturers face a strategic dilemma: absorb cost increases, leading to margin compression, or pass these costs to consumers, potentially reducing demand elasticity. This challenge is particularly pronounced in emerging markets, where high price sensitivity and limited effectiveness of premium positioning strategies complicate decision-making. The exploration of alternative materials, such as hemp-based superabsorbents, offers a pathway to cost stability but necessitates substantial investment in new supply chains and manufacturing infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Baby Diapers Market Segment Analysis

By Product Type:

Biodegradable Innovation Challenges, Disposable DominanceDisposable diapers maintain commanding market leadership with 70.45% share in 2025. Urban parents, often pressed for time, prioritize convenience and hygiene, making disposable diapers their preferred choice over cloth ones. Modern parenting trends lean towards time-saving solutions, and disposable diapers significantly cut down on laundry and associated hassles. Yet, biodegradable alternatives are on a rapid ascent, boasting an impressive 8.02% CAGR growth rate projected through 2031. This surge underscores a pivotal shift in consumer priorities, leaning heavily towards environmental sustainability. The widening growth gap highlights a dual trend: heightened parental awareness of environmental ramifications and technological advancements that bridge the performance divide between traditional and eco-friendly diaper options.

Cloth diapers maintain a niche position in the market, appealing to cost-conscious and environmentally aware consumers despite their higher maintenance requirements. The segment has benefited from innovations in fabric technology and enhanced washing machine efficiency, which have mitigated many of the traditional barriers to adoption. Additionally, the implementation of stringent plastic waste regulations, particularly in European markets where environmental policies are more rigorous, is creating favorable conditions for the increased adoption of non-disposable alternatives.

By Style:

Pull-Up Convenience Drives Market EvolutionIn 2025, pant/pull-up diapers account for 57.85% of the market share and are projected to grow at a 7.05% CAGR through 2031. This performance highlights increasing consumer demand for convenience and features that support child development. The dual leadership in market size and growth indicates a shift toward products designed to facilitate toilet training and improve mobility for active toddlers. This preference aligns with evolving parenting practices that prioritize fostering child independence and achieving developmental milestones over basic containment. Japan's cultural emphasis on early toilet training and child autonomy drives pull-up adoption rates above global averages, despite the country's declining birth rates.

Taped diapers continue to play a critical role in the newborn and early infant segment, where ease of application and secure fit are prioritized over mobility. This segment benefits from advancements in adhesive technology and leak protection, maintaining its competitive position despite a declining market share. Additionally, the manufacturing efficiency of taped designs supports cost optimization, appealing to price-sensitive consumers and institutional buyers such as childcare facilities. This segmentation reflects increasing consumer sophistication, with parents opting for products tailored to specific developmental stages rather than relying on a single solution throughout the diapering period.

By Absorbency Technology:

Dual-Core Systems Redefine Performance StandardsStandard SAP core technology secures a leading 55.92% market share in 2025, driven by cost optimization and economies of scale in manufacturing. Concurrently, dual-core and channel technology innovations, recognized for their advanced liquid distribution and leak prevention features, are projected to achieve a CAGR of 7.55% during the forecast period of 2026-2031. This progression highlights consumers' willingness to pay a premium for performance enhancements that address inconvenience and mitigate potential reputational risks. Advanced absorbency systems now facilitate thinner product designs, enhancing user comfort and discretion while maintaining or exceeding the absorption efficiency of traditional thicker alternatives.

Channel technology emerges as the most rapidly expanding subsegment within absorbency innovations. By integrating strategic liquid distribution mechanisms, it effectively prevents gel blocking and ensures consistent absorption performance over extended usage periods. This advancement resonates particularly with working parents, offering dependable functionality during longer intervals between diaper changes. Additionally, the Consumer Product Safety Commission's stricter safety regulations for infant products further validate the adoption of advanced technologies. Parents increasingly perceive superior product performance as a critical safety feature rather than a convenience factor.

By Material Type:

Natural Fiber Innovation Challenges Synthetic DominanceCotton retains its market leadership with a 53.02% share in 2025, driven by its established performance, economies of scale, and cost competitiveness across various market segments. Meanwhile, blended fabrics are projected to grow at a CAGR of 7.86% during 2026-2031. These fabrics offer a strategic blend of natural fiber benefits and synthetic performance attributes, appealing to consumers who value both sustainability and functionality. Additionally, the segment's manufacturing adaptability supports customization to meet specific performance criteria and cost objectives.

Bamboo and plant-based materials are experiencing accelerated adoption, propelled by increasing environmental awareness and hypoallergenic qualities that resonate with health-conscious parents. This shift aligns with broader consumer preferences for natural and sustainable products. Technological advancements have mitigated previous performance limitations of plant-based alternatives, further driving their adoption. Regulatory developments, such as stricter Federal Trade Commission standards on environmental marketing claims, are also fostering growth in natural material usage, particularly in areas emphasizing biodegradability and compostability. In this competitive landscape, material innovation is a critical differentiator, with intellectual property protection and supply chain management playing pivotal roles in determining market positioning and profitability.

By Distribution Channel:

Digital Transformation Accelerates Market AccessSupermarkets and hypermarkets secure a 42.25% market share in 2025 by leveraging convenience, bulk purchasing options, and immediate product availability to align with routine consumer shopping behaviors. Conversely, online retail demonstrates the highest growth trajectory, with a 9.95% CAGR projected through 2031. This growth highlights a significant transformation in consumer purchasing patterns and brand engagement strategies. The disparity in growth rates indicates that traditional retail strengths are increasingly challenged by the efficiency of digital platforms, subscription-based models, and direct-to-consumer approaches, which deliver personalized product recommendations and flexible delivery options.

Convenience and grocery stores maintain a stable market position, driven by their strategic locations. These stores often serve as the preferred choice for urgent purchases where immediate availability outweighs cost considerations. Pharmacy and drug stores capitalize on a health-oriented market positioning, aligning with the growing consumer perception of products like diapers as health-related necessities rather than basic commodities. According to the U.S. Census Bureau, child day care services experienced significant revenue growth despite a decline in the number of businesses. This trend underscores the strong institutional purchasing power that supports bulk distribution channels.

Geography Analysis

China and APAC Baby Diapers Market

Asia-Pacific accounts for a significant 39.10% market share in 2025, driven by its high population density and the growing purchasing power of the middle class. However, demographic challenges pose risks to sustained long-term growth. In China, the expansion of childcare institutions is driving institutional demand while complementing household consumption. Additionally, government support for childcare infrastructure underscores a strong commitment to fostering market growth.

North America Baby Diapers Market

North America, despite holding a smaller market share, is projected to achieve the highest regional growth at a 9.15% CAGR through 2031. This growth highlights a shift where purchasing power and premiumization trends are becoming more influential than demographic volume in driving market expansion. The region benefits from elevated disposable incomes, early adoption of premium products, and a well-established e-commerce ecosystem that supports direct-to-consumer strategies. Government initiatives, such as the U.S. diaper distribution pilot, reflect policy acknowledgment of diapers as essential goods, potentially expanding the market beyond private purchasing capacity.

EMEA and South America Baby Diapers Market

Europe exhibits consistent market growth, supported by stringent environmental regulations that encourage innovation in sustainable product alternatives. This creates opportunities for premium positioning and technological advancements. Meanwhile, South America and the Middle East and Africa present emerging growth opportunities, driven by urbanization, improvements in healthcare, and increasing disposable incomes. However, infrastructure limitations and price sensitivity are likely to constrain the development of the premium segment in the short term.

Competitive Landscape

The baby diaper market is moderately concentrated, driven by a mix of regional and global players. Leading companies, including Procter & Gamble Company, Kimberly-Clark Corporation, Kao Corporation, and Unicharm Corporation, focus on strategies such as product innovation, market expansion, and mergers and acquisitions. The growing presence of private-label brands is expected to heighten competitive dynamics. Significant investments in research and development are enabling companies to introduce innovative offerings and cater to the increasing consumer demand for sustainable baby products, particularly baby diapers.

Opportunities are emerging in sustainability and direct-to-consumer (D2C) segments. Purdue-licensed hemp-based superabsorbents present new entrants with the potential to challenge established eco-credentials. Digital-first players bypass traditional retail competition by targeting tech-savvy parents with subscription-based bundles and transparent ingredient disclosures. Established players are responding with equity investments, co-development partnerships, and carbon-neutral initiatives to strengthen their market positions.

Competitive differentiation will depend on robust ESG compliance, proprietary absorbency technologies, and seamless omnichannel strategies. Companies lacking scale or innovation capabilities risk being marginalized as regulatory costs rise and consumer expectations evolve. However, regulatory compliance expenses and stringent safety standards continue to act as significant barriers, safeguarding the competitive advantages of established players while limiting the disruptive potential of undercapitalized competitors.

Baby Diapers Industry Leaders

-

Procter & Gamble Company

-

Kimberly-Clark Corporation

-

Kao Corporation

-

Unicharm Corporation

-

Ontex Group NV

- *Disclaimer: Major Players sorted in no particular order

Baby Diapers Market Companies Covered in this Report

- Procter & Gamble Company

- Kimberly-Clark Corporation

- CHIAUS (Fujian) Industrial Development Co.,Ltd.

- Kao Corporation

- Unicharm Corporation

- Ontex Group NV

- Daio Paper Corporation

- Hengan International Group

- WEHOO Hygiene

- Hello Bello

- Babee Greens

- Humble Group AB

- The Honest Company

- Thirsties Inc.

- Nobel Hygiene Pvt. Ltd.

- Mama Bamboo

- Coterie Baby Inc.

- Eco Baby Products Pty

- DYPER Inc.

- Fewer Better Things LLC

Recent Industry Developments in Baby Diapers Market

- May 2025: Ontex Group NV has unveiled a new 360° leak protection system for its baby diapers. This innovative feature ensures comprehensive coverage from front to back and side-to-side, aiming to keep babies comfortable, dry, and secure.

- April 2025: Swara Baby Products, through its Baby Hug Pro brand, introduced India's first tree-free diaper technology, showcasing a breakthrough in sustainable diaper solutions.

- January 2025: Panacea Biotec Pharma, a wholly owned subsidiary of Panacea Biotec, has unveiled its new baby diaper brand, 'NikoMom'. This brand will consolidate the company’s portfolio of diaper products.

- July 2024: Soft N Dry Diapers Corp has launched its innovative tree-free disposable baby diapers in the European market, establishing white label sales and distribution partnerships with retailers in France, Germany, and the UK.

Global Baby Diapers Market Report Scope

A diaper is a piece of toweling or other absorbent material wrapped around a baby's bottom and between its legs to absorb and retain urine and feces.

The baby diapers market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into Cloth Diapers and Disposable Diapers. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, pharmacy/drug stores, online retail channels, and other distribution channels. Also, the study analyzes the dietary supplements market in emerging and established markets worldwide, including North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

Segmentation Overview

| Cloth Diapers |

| Disposable Diapers |

| Biodegradable/Eco-friendly Diapers |

| Taped Diapers |

| Pant/Pull-Up Diapers |

| Standard SAP Core |

| Dual-Core and Channel Technology |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Pharmacy/Drug Stores |

| Online Retail |

| Other Channels |

| Cotton |

| Bamboo and Plant-based |

| Blended Fabrics |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Cloth Diapers | |

| Disposable Diapers | ||

| Biodegradable/Eco-friendly Diapers | ||

| By Style | Taped Diapers | |

| Pant/Pull-Up Diapers | ||

| By Absorbency Technology | Standard SAP Core | |

| Dual-Core and Channel Technology | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Pharmacy/Drug Stores | ||

| Online Retail | ||

| Other Channels | ||

| By Material Type | Cotton | |

| Bamboo and Plant-based | ||

| Blended Fabrics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the baby diapers market by 2031?

The baby diapers market is forecast to reach USD 76.14 billion in 2031, rising from USD 58.14 billion in 2026.

Which region is growing fastest in the baby diapers market?

North America records the highest regional CAGR at 9.15% through 2031, driven by premium product uptake and supportive public programmes.

Why are pull-up diapers gaining share?

Pant-style pull-ups offer convenience for mobile toddlers and support toilet-training transitions, securing 57.85% market share in 2025 and a 7.05% growth rate.

How are regulations influencing product innovation?

Europe and United Kingdom single-use plastic restrictions push brands toward biodegradable materials and recyclable packaging, making sustainability a core design criterion.

Page last updated on: