Market Overview

| Study Period | 2021 - 2031 |

|---|---|

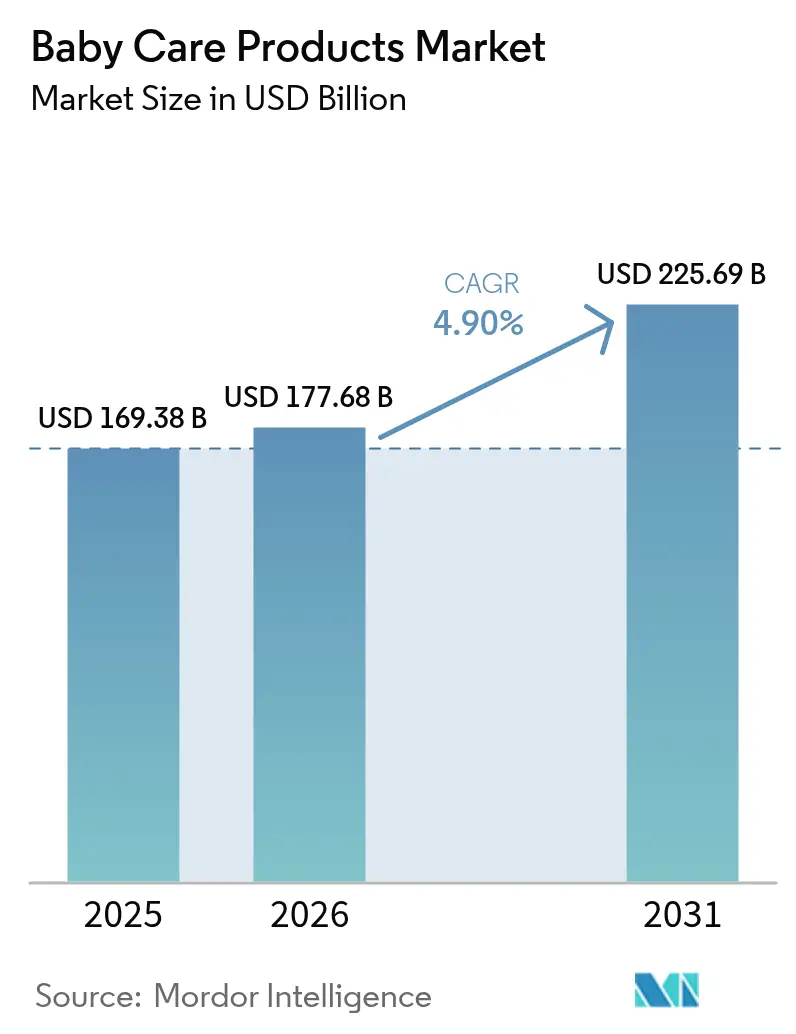

| Market Size (2026) | USD 177.68 Billion |

| Market Size (2031) | USD 225.69 Billion |

| Growth Rate (2026 - 2031) | 4.90% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Baby Care Products Market Analysis by Mordor Intelligence

The baby care products market size in 2026 is estimated at USD 177.68 billion, growing from 2025 value of USD 169.38 billion with 2031 projections showing USD 225.69 billion, growing at 4.90% CAGR over 2026-2031. Established market leaders are enhancing their operating margins by launching clean-label product extensions that cater to the growing consumer demand for transparency and safety. Meanwhile, new entrants are leveraging social commerce platforms to effectively engage with first-time parents, creating personalized and interactive shopping experiences. Parents are placing an increasing emphasis on their babies' health, hygiene, and safety, driving the demand for natural, premium-quality baby care products that comply with stringent regulatory standards. Confidence in government safety frameworks, such as the FDA's updated regulations for infant formula, is raising industry-wide quality benchmarks and encouraging investments in clinical validation to ensure product efficacy and safety. The rising number of working mothers has further amplified the need for convenient, ready-to-use baby care solutions that save time and simplify daily routines. To remain competitive amidst pricing pressures, the market is witnessing significant ingredient innovations, combining plant-based substrates with biotech-derived actives to deliver effective and sustainable solutions. Additionally, the adoption of an omnichannel purchasing model, which includes subscription-based diaper services and same-day grocery deliveries, is transforming inventory management practices and marketing strategies, enabling companies to meet evolving consumer expectations more efficiently.

Key Report Takeaways

- By product type, Baby Food and Beverages led with 42.72% of the baby care products market share in 2025, while Baby Skin Care is expanding at a 6.57% CAGR through 2031.

- By ingredient type, Conventional/Synthetic formulations accounted for 72.90% share of the baby care products market size in 2025, whereas Organic/Natural products are projected to rise at a 6.35% CAGR to 2031.

- By age group, the Toddler segment held 62.10% of the baby care products market size in 2025, and the Infant segment is set to grow at a 5.52% CAGR during the forecast window.

- By distribution channel, Supermarkets/Hypermarkets captured 36.55 of % baby care products market share in 2025, while Online Retail Stores recorded the highest 6.62% CAGR through 2031.

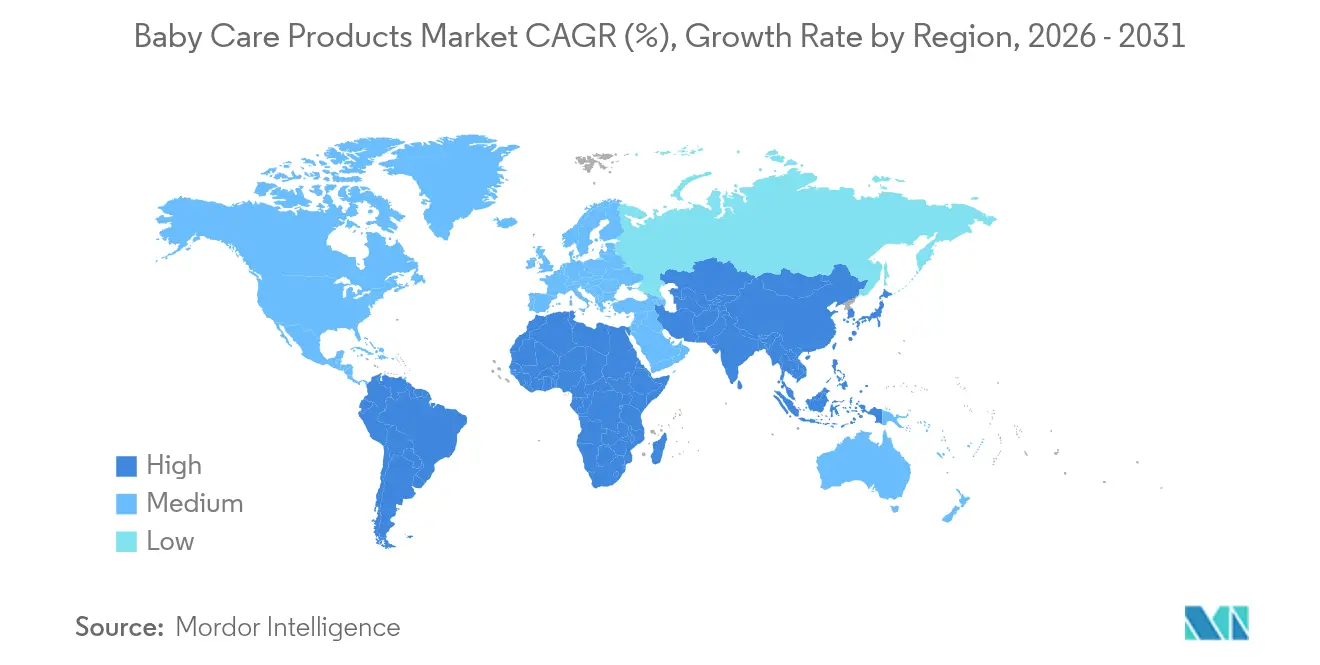

- By geography, North America accounted for 35.20% revenue share in 2025; Asia-Pacific is forecast to advance at a 5.35% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Baby Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concerns over infant hygiene and health | +1.2% | Global, highest in North America and Europe | Medium term (2-4 years) |

| Premiumization of baby care SKUs | +0.8% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Growing infant population | +0.6% | Asia-Pacific, Sub-Saharan Africa, Middle East and Africa | Long term (≥ 4 years) |

| Preference for organic and chemical-free products | +0.9% | North America, European Union, emerging-market metros | Medium term (2-4 years) |

| Innovations in product offerings | +0.7% | Global, fastest in developed markets | Short term (≤ 2 years) |

| Digital parenting influence | +0.5% | Global, linked to high internet penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Concerns over infant hygiene and health

Parents' growing awareness of infant vulnerabilities is driving demand for products with superior safety features and clinical validation. The FDA has implemented stricter regulations on infant formulas, requiring enhanced testing protocols, nutritional adequacy, and facility registrations. These regulations, detailed under 21 CFR Parts 106 and 107, have enhanced industry standards. This regulatory rigor benefits manufacturers with strong quality systems while creating challenges for smaller players. According to the Consumer Product Safety Commission, scrutiny of infant products has increased, with new safety standards for nursing pillows and infant support cushions highlighting a broader focus on safety. "Safety Standards for Infant Products." 2024. Additionally, pediatric healthcare providers are increasingly recommending specific product categories, shifting consumer decisions from being price-driven to recommendation-based. In high-mortality regions, infections such as sepsis, diarrhea, and pneumonia, often caused by inadequate hygiene and sanitation, remain leading causes of infant deaths. In 2024, the CIA - The World Factbook reported an infant mortality rate of 53.7 deaths per thousand live births in Nigeria during the first year of life [1]Source: CIA - The World Factbook, "The World Factbook", cia.gov. This highlights the critical need for educational initiatives, safe baby care products, clean birthing practices, and broader public health reforms to prevent infection-related deaths.

Premiumization of baby care SKUs

Parents are increasingly prioritizing baby care products that emphasize safety, efficacy, and high-quality, often organic or plant-based ingredients. Their readiness to invest more in premium formulations is driving growth across categories like skin care, toiletries, and baby food. By adopting premium positioning strategies, brands are reaping higher margins, as parents willingly pay a premium for perceived quality and safety. This trend is underscored by organic certifications, claims of clinical testing, and initiatives in sustainable packaging, all justifying price premiums of 20-40% over conventional options. The premiumization effect is especially notable in developed markets, buoyed by disposable income levels that allow for discretionary spending on infant care. For instance, per capita personal income in the United States was USD 108,233 in 2024, according to the US Department of Commerce [2]Source: US Department of Commerce, "Regional Data - GDP and Personal Income", bea.gov. A case in point is Bobbie Labs, which, in April 2025, rolled out the first USDA organic whole milk infant formula, catering to parents leaning towards organic over conventional options. Market dynamics are increasingly favoring brands that effectively communicate scientific validation and ingredient transparency, fostering brand loyalty and encouraging repeat purchases.

Growing infant population

The arrival of every new child drives demand for baby care products, including those for hygiene, health, and nutrition. The growing global population of infants and children is prompting brands to enhance their investments in distribution, product innovation, and marketing. Despite declining fertility rates in developed regions, demographic growth in key emerging markets continues to support volume expansion. Sub-Saharan Africa and parts of Asia maintain birth rates above replacement levels, ensuring consistent demand for essential infant care products. According to the United Nations Economic and Social Commission for Asia and the Pacific, India's total fertility rate in 2024 was 2 live births per woman [3]Source: United Nations Economic and Social Commission for Asia and the Pacific, "Population Trends and Demographic Dividend in Asia-Pacific." 2024. asiapacific.unfpa.org. Infant population growth is increasingly concentrated in specific regions rather than driving broad global expansion, highlighting the importance of targeted market entry and distribution strategies. This trend not only increases global access to baby care products but also expands the variety available. The rising infant population drives consistent demand for a wide range of baby care products, supporting market growth and strengthening the industry's focus on innovation, distribution, and product category diversification.

Preference for organic and chemical-free products

The growing preference for organic and chemical-free baby care products is driving rapid category growth, fostering higher innovation rates, and shifting market share toward brands that prioritize health, transparency, and sustainability. Regulatory frameworks supporting organic claims provide structured pathways for product differentiation and premium pricing. The USDA's National Organic Program establishes clear standards for organic baby food and personal care products, covering ingredient sourcing, processing methods, and labeling compliance. This regulatory clarity enables manufacturers to confidently invest in organic product lines while offering consumers trusted certification standards. The trend toward organic products is accelerating as millennial and Gen Z parents emphasize ingredient transparency and environmental sustainability. Currently, market penetration is concentrated in higher-income demographics and urban centers, indicating significant growth potential as organic supply chains mature and cost structures improve.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Potential health concerns related to chemical residues | -0.4% | Global, higher in European Union and North America | Medium term (2-4 years) |

| Stringent regulatory environment | -0.3% | European Union, North America, mirrored elsewhere | Long term (≥ 4 years) |

| Falling birth-rates in OECD nations | -0.6% | OECD markets, large urban centers worldwide | Long term (≥ 4 years) |

| Complexity of ingredient formulations | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Potential health concerns related to chemical residues

Growing consumer concerns over chemical residues, coupled with heightened regulatory scrutiny, are significantly restricting market growth, particularly in conventional product categories. A notable example is the European Chemicals Agency's classification of borate and talc as Category 1B carcinogens, which has led to their planned ban in cosmetic products by 2027. This regulatory action underscores how safety concerns can render entire ingredient categories obsolete. As a result, manufacturers are compelled to reformulate their products, which involves substantial costs for additional testing and navigating disruptions across their supply chains. The rise of social media platforms and advocacy group campaigns has further amplified consumer awareness of the potential risks associated with chemical residues. This growing awareness is driving demand for cleaner and safer product formulations, often pressuring manufacturers to act even before regulatory mandates are enforced. For established brands with legacy formulations, these developments pose significant challenges. They must invest heavily in research and development to meet evolving consumer expectations and regulatory standards, while also facing the risk of losing market share during the transition period. The shift toward cleaner formulations is not only reshaping product development strategies but also redefining competitive dynamics within the market.

Falling birth-rates in OECD nations

Demographic declines in high-value markets are significantly reducing the size of the addressable market, intensifying competition as companies vie for a shrinking consumer base. In OECD countries, fertility rates have consistently fallen below replacement levels, creating far-reaching implications that extend beyond immediate volume reductions to fundamentally reshape market structures over time. This demographic trend forces businesses to shift their focus from relying on category growth to aggressively pursuing market share, which, in turn, escalates competitive pressures and compresses profit margins. The decline in birth rates is particularly severe in developed Asian markets such as South Korea and Japan, where a combination of cultural norms and economic challenges has led to persistently low fertility rates. To mitigate these challenges, companies are increasingly adopting geographic diversification strategies, targeting emerging markets with more favorable demographic profiles. However, this approach presents its own set of obstacles, as businesses must adapt their products and distribution models to align with varying economic conditions and navigate complex regulatory environments in these new markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Food Dominance Meets Care Innovation

Baby Food and Beverages hold a 42.72% market share in 2025, highlighting parents' focus on ensuring nutritional security over discretionary care products. This segment's dominance is driven by essential purchasing patterns and regulations that enforce specific nutritional standards for infant formulas and complementary foods. On the other hand, Baby Skin Care is the fastest-growing segment, with a 6.57% CAGR projected through 2031. This growth is propelled by premiumization trends and increased awareness of infant skin sensitivities. The rise in skin care reflects a broader shift in consumer preferences, as parents increasingly acknowledge the specialized needs of their infants' skin development. Baby Hair Care continues to grow steadily, supported by gentle formulations and the use of natural ingredients. Meanwhile, Baby Toiletries includes both high-volume staples like diapers and premium bath products, with the latter offering higher profit margins.

The regulatory environment plays a critical role in shaping product development across categories. For example, FDA requirements for nutritional adequacy in infant formulas not only ensure product safety but also create barriers for new entrants. Within toiletries, Bath and Fragrances capitalize on sensory marketing and gift-giving occasions, enabling premium pricing. Diapers and Wipes represent the largest volume segment in toiletries, with subscription models and sustainability initiatives addressing environmental concerns. Innovation trends vary significantly across product categories: food and beverages focus on organic certifications and nutritional improvements, while care products emphasize gentle formulations and dermatological testing. These dynamics indicate a continued division between essential nutrition products with stable demand and premium care products experiencing accelerated growth.

By Ingredient Type: Conventional Scale Versus Organic Acceleration

Conventional and synthetic ingredients hold a 72.90% market share in 2025. Their dominance is driven by established supply chains, cost efficiencies, and a proven safety record, ensuring accessibility for the mass market. This leadership highlights the practicalities of global manufacturing scale and regulatory processes that favor well-documented synthetic ingredients over emerging natural options. Meanwhile, organic and natural ingredients are experiencing growth, with a 6.35% CAGR projected through 2031. This trend reflects a steady shift in consumer preferences toward cleaner formulations, despite their higher costs. The United States Department of Agriculture National Organic Program certification standards further support this growth by providing regulatory clarity and enhancing consumer confidence in product claims.

Conventional ingredients excel in product consistency, shelf stability, and manufacturing efficiency, which are critical for global distribution. Synthetic ingredients range from traditional chemical compounds to advanced biotechnology-derived components, both offering superior performance. Organic and natural alternatives face challenges such as supply chain constraints and seasonal availability, which limit scalability. However, they command premium pricing that offsets higher raw material costs. The distinction between ingredient segments is increasingly blurred as manufacturers develop hybrid formulations that combine synthetic base ingredients with organic active compounds. These innovations deliver products that balance performance, safety, and natural appeal. Regulatory compliance also plays a significant role in ingredient selection. For example, the European Union's restrictions on certain synthetic compounds have accelerated the adoption of natural ingredients in European markets.

By Age Group: Toddler Volume Meets Infant Growth Potential

Toddlers hold a significant 62.10% share of the market in 2025, driven by extended product usage and a wider range of offerings designed for children aged 1-3. This segment's dominance is primarily due to longer consumption cycles for food and diapers, along with the growing availability of developmental and educational toys. Parents are increasingly open to experimenting with products and opting for premium alternatives to cater to their toddlers' changing preferences. On the other hand, the infant segment, though smaller, is expected to grow at a 5.52% CAGR through 2031, propelled by new parents' concerns, which lead to higher demand for premium products and specialized care for the 0-1 age group.

Purchasing behaviors vary significantly between the two age groups. Infant products emphasize safety and often rely on medical endorsements, while toddler products focus on developmental benefits and convenience. Strict nutritional regulations for infant formulas limit opportunities for product differentiation. In contrast, toddler food products offer more flexibility in formulation and flavor variety. Distribution strategies also differ by age group: infant products often require recommendations from healthcare providers, whereas toddler products benefit from peer recommendations and social media marketing.

By Distribution Channel: Traditional Retail Stability Versus Digital Disruption

Supermarkets and Hypermarkets hold a 36.55% market share in 2025, leveraging consumer trust, enabling product trials, and offering a convenient one-stop shopping experience that appeals particularly to time-pressed parents. Their dominance highlights the importance of immediate product availability and the ability to physically compare products before purchasing. On the other hand, Online Retail Stores are experiencing the fastest growth, with a 6.62% CAGR projected from 2026 to 2031. This growth is driven by the adoption of subscription models, access to specialized products, and competitive pricing, which strongly attract digital-native parents. The acceleration of e-commerce, influenced by pandemic-driven behavioral changes, is further supported by improved last-mile delivery capabilities that cater to parents' convenience needs.

Pharmacies and Drug Stores play a critical role in providing product recommendations and medical endorsements, particularly for sensitive skin products and specialized nutritional formulations. Other Distribution Channels include specialty baby stores, direct-to-consumer brands, and emerging platforms like social commerce, which leverage influencer-driven sales. This evolving distribution landscape has significant implications for brand positioning. Traditional retail channels must focus on broad appeal and competitive pricing, while online channels allow for niche targeting and premium positioning. Subscription models are particularly effective in the baby care segment, benefiting from predictable consumption patterns and parents' need to avoid stockouts of essential products. The distribution landscape increasingly favors omnichannel strategies, combining the convenience of online shopping with the tactile benefits of offline product trials.

Geography Analysis

North America holds a leading 35.20% market share in 2025, reflecting its high disposable incomes, strong preference for premium products, and a regulatory framework that effectively balances innovation with consumer protection. The region's advanced healthcare systems not only endorse products but also support a well-established retail infrastructure that caters to both traditional and modern distribution channels. Increasing consumer sophistication drives demand for organic certifications, clinical testing validations, and sustainable packaging, all of which command premium pricing. The FDA's oversight of infant formulas and the CPSC's safety standards for infant products ensure product quality, fostering consumer trust while creating significant entry barriers. Digital parenting trends are particularly prominent in North America, where high internet penetration and widespread social media usage drive online product discovery and the growth of direct-to-consumer brands.

Asia-Pacific is experiencing rapid growth, with a projected 5.35% CAGR through 2031, fueled by strong demographic and economic factors. The region's massive population of 4.3 billion, representing 60% of the global total, offers a substantial market opportunity despite varying fertility rates across subregions. Accelerating urbanization is driving lifestyle changes that favor packaged baby care products over traditional alternatives, while a growing middle class increases purchasing power for premium products. The region's technological adoption trends favor smart baby products and e-commerce, with countries like China and South Korea leading the way in digital integration, influencing global product development priorities.

Europe remains strategically significant, not only as a market but also as a regulatory leader, shaping global product standards and driving demand for organic and sustainable products, particularly in the premium segment. The European Chemicals Agency's proactive stance on chemical safety, including restrictions on talc and microplastics, underscores the region's focus on compliance and safety. Europe's emphasis on environmental sustainability drives innovation in biodegradable packaging and natural ingredient formulations, which are subsequently adopted in global markets. Meanwhile, South America and the Middle East and Africa present emerging opportunities, supported by favorable demographics. However, these regions face challenges such as diverse economic conditions, distribution infrastructure limitations, and regulatory complexities. While urbanization trends and demographic dividends offer growth potential, issues like product affordability and supply chain development influence market entry strategies and product positioning.

Competitive Landscape

The baby care products market is moderately consolidated, with established multinational corporations maintaining leadership positions due to their scale advantages, extensive distribution networks, and decades of brand recognition. Companies such as The Procter and Gamble Company, Kimberly-Clark Corp., Unicharm Corp., Kenvue, and Nestlé SA benefit from diversified product portfolios that cover multiple categories and geographic markets, enabling cross-selling opportunities and risk mitigation. However, the competitive landscape is evolving as direct-to-consumer brands like Mamaearth and The Honest Company disrupt traditional market dynamics with digital-first strategies, clean-label products, and targeted appeals that resonate with millennial parents.

Strategic differentiation increasingly focuses on technology integration, sustainability initiatives, and regulatory compliance, which create competitive advantages. New entrants and challenger brands can gain traction by targeting specific product categories or market segments with unique value propositions centered on natural ingredients, sustainability, or technological innovation. Success factors include building strong digital marketing capabilities, creating authentic brand narratives, and establishing efficient supply chain networks. Companies must address growing regulatory scrutiny regarding product safety and labeling while managing substitution risks from homemade alternatives and traditional practices. Long-term success in the market will depend on building consumer trust through transparency in ingredients and manufacturing processes while maintaining competitive pricing. The most successful baby care brands will be those that effectively balance innovation with consumer trust.

White-space opportunities are emerging in personalized nutrition, biodegradable packaging solutions, and AI-powered monitoring systems that address specific parental concerns about infant development and safety. Regulatory compliance is becoming a competitive advantage, as companies with robust quality systems can navigate complex approval processes more efficiently than smaller competitors, particularly in areas like infant formula and organic certification requirements. The competitive landscape favors companies that successfully balance investments in innovation with operational efficiency while maintaining brand trust through consistent product quality and safety standards.

Baby Care Products Industry Leaders

-

Nestlé S.A.

-

Kimberly-Clark Corporation

-

The Proctor and Gamble Company

-

Unicharm Corp

-

Kenvue

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Bobbie Labs has launched the first USDA organic whole milk infant formula in the U.S., aiming to provide parents with organic alternatives to conventional formulas. This launch addresses the increasing demand for organic baby nutrition while skillfully navigating the complex FDA regulations for infant formula production and labeling.

- February 2024: MamyPoko Pants launched Extra Absorb Pants with 30+ patented technologies. The diapers are claimed to be up to 60% absorbent.

- January 2024: Pampers launched a new Pampers Premium Care Diaper – a 360-degree coverage all-in-one diaper for babies. It has an inbuilt anti-rash blanket and lotion with aloe vera to protect the baby's delicate skin from rashes.

- January 2024: The Procter and Gamble Korea, a subsidiary of the global giant Procter and Gamble Company, unveiled its latest product: Pampers Baby-Dry Pants, a diaper crafted for superior absorbency.

Global Baby Care Products Market Report Scope

Baby care products like skin care, hair care, and toiletries are specially designed for infants as per their requirements.

The baby care products market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into baby skin care, baby hair care, baby toiletries, and baby food and beverage. Baby toiletries are further sub-segmented into baby bath products and fragrances and baby diapers and wipes. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, pharmacies/drug stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa.

For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Product Type

| Baby Skin Care | |

| Baby Hair Care | |

| Baby Toiletries | Bath and Fragrances |

| Diapers and Wipes | |

| Baby Food and Beverages |

By Ingredient Type

| Organic / Natural |

| Conventional / Synthetic |

By Age Group

| Infants (0-1 Year) |

| Toddlers (1-3 Years) |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Pharmacies / Drug Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Baby Skin Care | |

| Baby Hair Care | ||

| Baby Toiletries | Bath and Fragrances | |

| Diapers and Wipes | ||

| Baby Food and Beverages | ||

| By Ingredient Type | Organic / Natural | |

| Conventional / Synthetic | ||

| By Age Group | Infants (0-1 Year) | |

| Toddlers (1-3 Years) | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Pharmacies / Drug Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the baby care products space in 2026?

The segment reached USD 177.68 billion in 2026 and is set to rise to USD 225.69 billion by 2031 on a 4.90% CAGR.

Which product category captures the biggest share?

Baby Food and Beverages hold 42.72% share, reflecting parents’ focus on core nutrition purchases.

What drives the fastest-growing distribution channel?

Online Retail Stores post a 6.62% CAGR thanks to subscription models, same-day delivery, and influencer-led discovery.

Why are organic labels gaining traction?

USDA-certified formulations earn consumer trust, letting brands command 20–40% price premiums over conventional options.

Page last updated on: