Baby Carrier Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

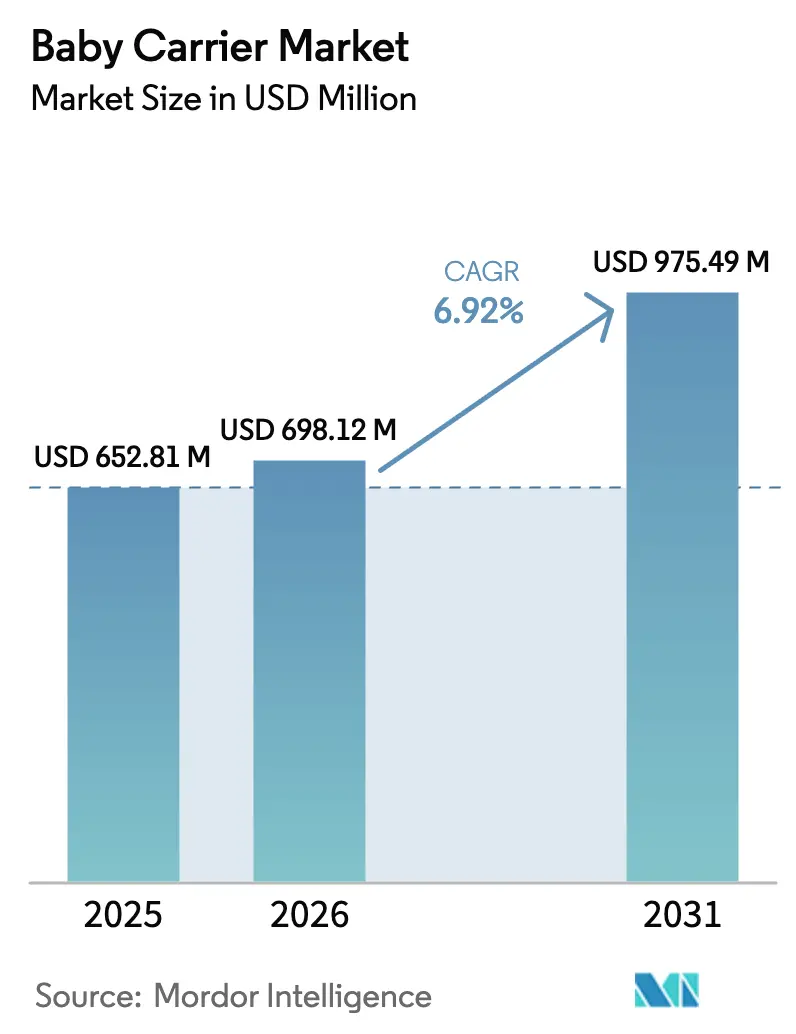

| Market Size (2026) | USD 698.12 Million |

| Market Size (2031) | USD 975.49 Million |

| Growth Rate (2026 - 2031) | 6.92% CAGR |

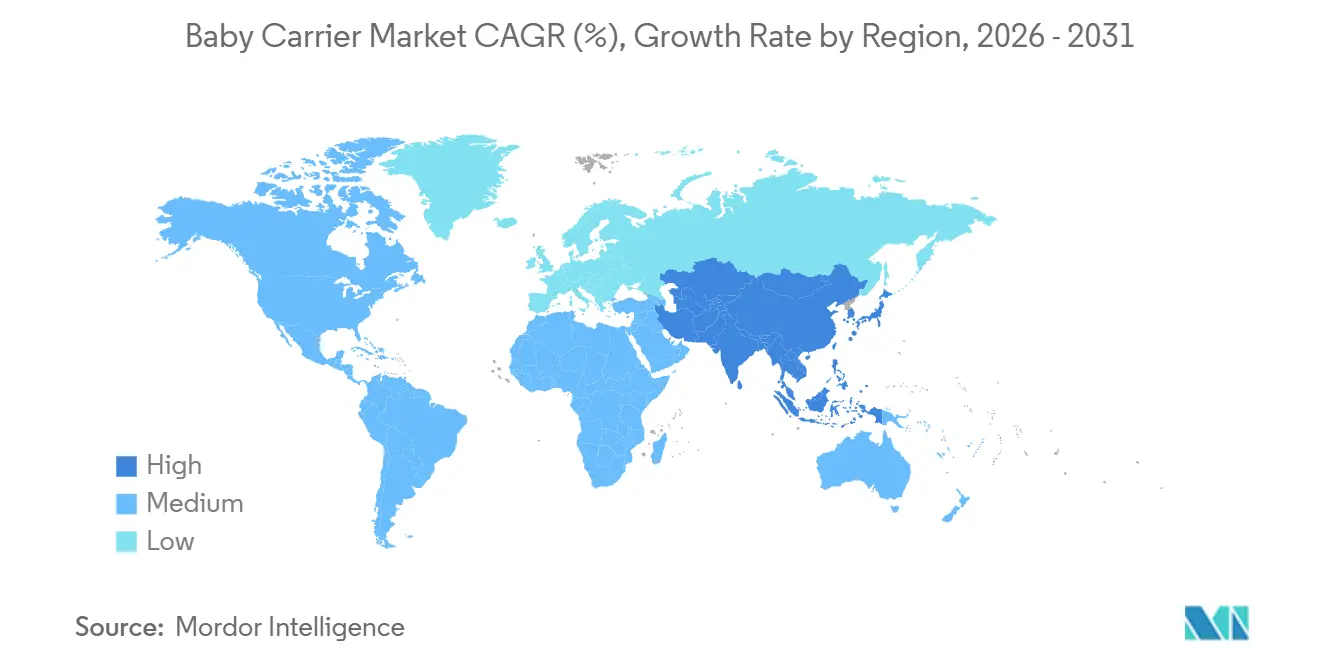

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Baby Carrier Market Analysis by Mordor Intelligence

The Baby Carrier Market size was valued at USD 652.81 million in 2025 and estimated to grow from USD 698.12 million in 2026 to reach USD 975.49 million by 2031, at a CAGR of 6.92% during the forecast period (2026-2031). While population growth plays a role, evolving lifestyles are a key source of demand. Notably, 68.3% of U.S. mothers with kids under 6 are in the labor force, underscoring the heightened need for hands-free mobility, as highlighted by the U.S. Bureau of Labor Statistics. Parents are increasingly gravitating toward premium brands, especially those that combine ergonomic certifications with eco-friendly materials. This trend is further supported by omni-channel distribution, which simplifies product discovery. Since February 2025, the stringent enforcement of 16 CFR Part 1226 has made safety a pivotal competitive edge, leading some smaller, import-only brands to reconsider their market presence. Meanwhile, social media platforms have amplified product visibility, with influencer endorsements swaying 44% of maternal purchasing choices, giving direct-to-consumer brands a significant platform.

Key Report Takeaways

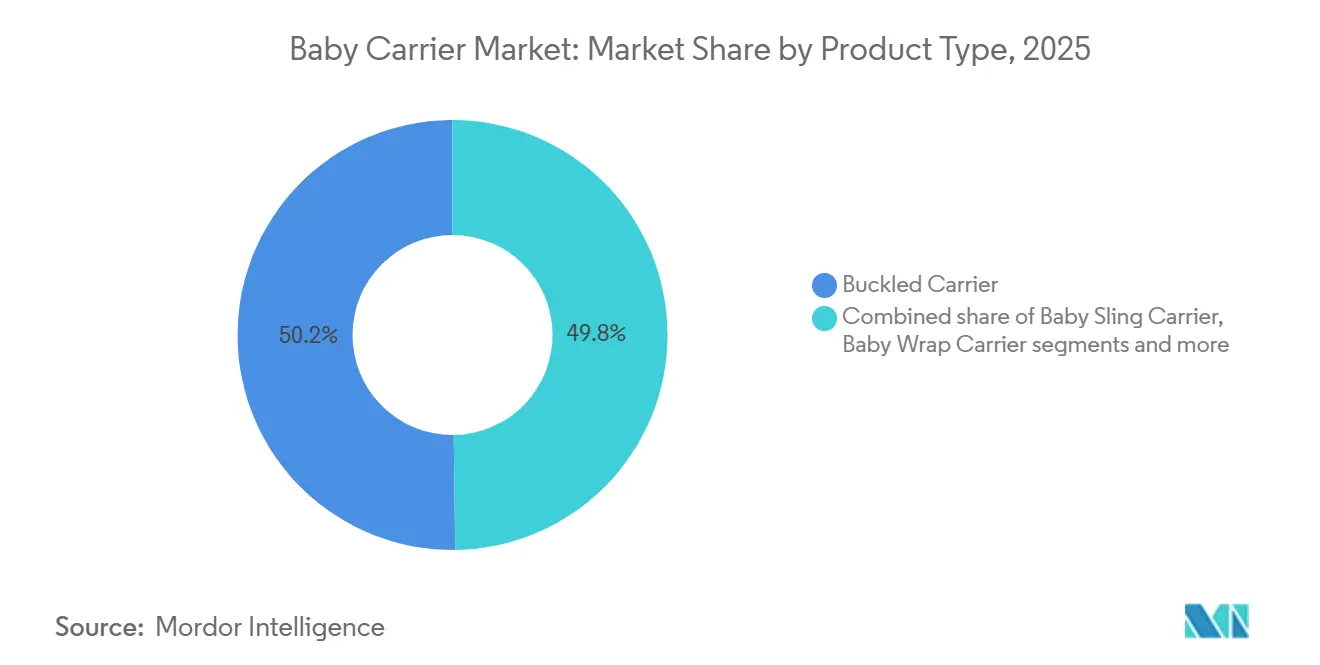

- By product type, buckled baby carriers led with 50.21% of the baby carrier market share in 2025, while baby sling carriers posted the fastest projected 5.88% CAGR through 2031.

- By price range, the mass tier commanded 67.51% share of the baby carrier market in 2025, whereas the premium tier advances at an 8.41% CAGR to 2031.

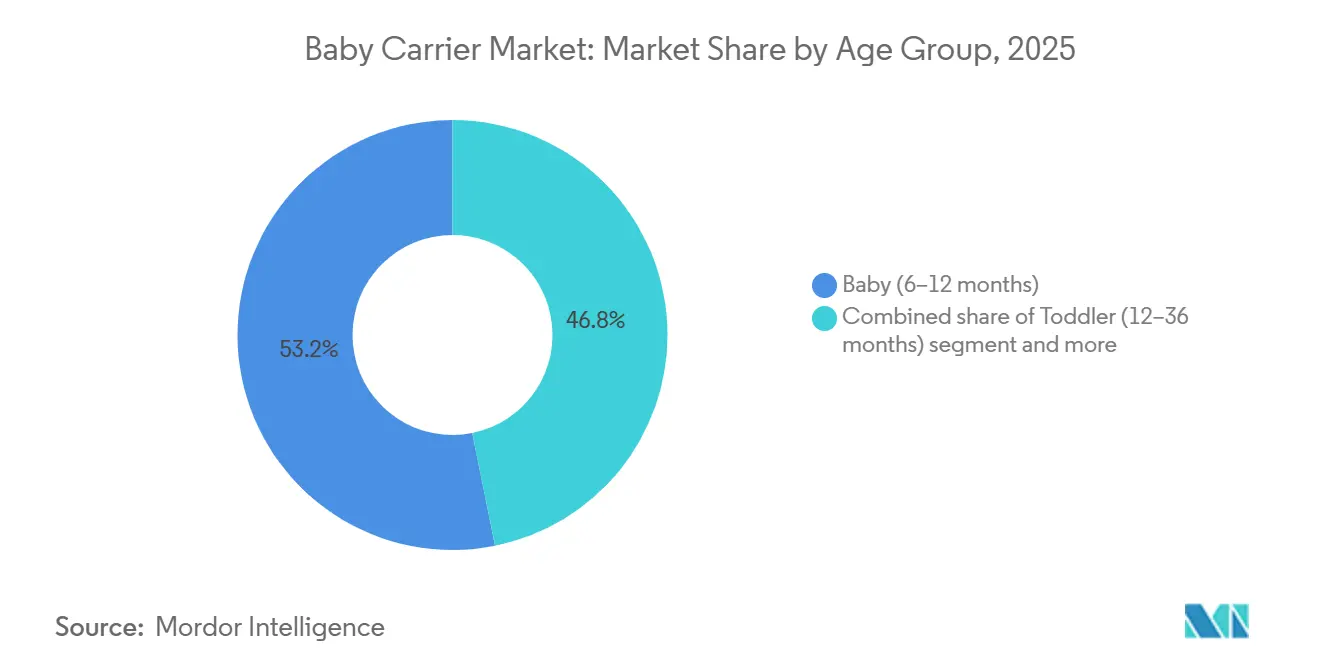

- By age group, baby carriers designed for infants aged 6–12 months captured a 53.17% share in 2025, and the toddler segment is forecast to expand at a 6.13% CAGR to 2031.

- By distribution channel, offline retail outlets accounted for 44.50% of sales in 2025, while online retail is projected to grow at a 7.11% CAGR through 2031.

- By geography, North America held a 37.05% share in 2025; the Asia-Pacific region records the fastest growth at 5.92% CAGR for the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Baby Carrier Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban millennial adoption of baby-wearing | +1.2% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Omni-channel expansion of DTC premium brands | +0.9% | North America, EU core, Asia-Pacific metros | Short term (≤ 2 years) |

| Post-pandemic outdoor and travel boom | +0.8% | North America, Europe, Australia/New Zealand | Short term (≤ 2 years) |

| Rising birth rates in emerging economies | +1.1% | India, Indonesia, Nigeria, Egypt, South America | Long term (≥ 4 years) |

| Increasing number of working parents | +1.3% | Global, strongest in North America, Northern Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Influence of social-media parenting networks | +0.7% | Global, leader North America, Europe, rapidly growing Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Urban millennial adoption of baby-wearing culture

Millennial parents, now the dominant cohort of first-time buyers, treat baby-wearing as a lifestyle statement rather than a utilitarian choice, driving demand for aesthetically differentiated products that signal attachment-parenting values. The U.S. Bureau of Labor Statistics reported that 68.3% of mothers with children under 6 participated in the labor force in 2024, creating a structural need for hands-free caregiving solutions that integrate into commuting and errand routines[1]Source: U.S. Bureau of Labor Statistics, “Employment Characteristics of Families, 2024,” bls.gov. Ergobaby's 2024 launch of the Embrace Cozy Newborn Carrier, emphasizing soft-structured design for skin-to-skin contact, reflects manufacturers' pivot toward products that blend ergonomic function with emotional resonance. Urban density amplifies this trend, as public-transit navigation and apartment living favor compact, wearable solutions over bulky strollers. The International Hip Dysplasia Institute's endorsement of specific carrier models further legitimizes baby-wearing within pediatric circles, converting clinical recommendations into purchase triggers.

Omni-channel expansion of DTC premium brands

Direct-to-consumer brands bypass traditional retail intermediaries, capturing 25-35% gross margins versus 15-20% for wholesale-dependent peers, and reinvest savings into content marketing and influencer partnerships that drive online conversion rates above 3.5%. Walmart and Kohl's both launched baby registries in 2024-2025 with omni-channel fulfillment, enabling customers to order online and pick up in-store within hours, a capability that premium DTC entrants like BabyBjörn and Ergobaby now replicate through partnerships with specialty retailers. Amazon's dominance in baby products, capturing an estimated 40% of U.S. online baby-gear sales, forces brands to maintain Amazon storefronts while simultaneously building owned e-commerce channels to protect pricing integrity. The shift to omni-channel also reduces inventory risk, as brands can test new SKUs online before committing to retail shelf space, accelerating product-development cycles from 18 months to under 12.

Rising birth rates in emerging economies

India and Indonesia together account for over 40 million annual births, sustaining absolute volume growth even as fertility rates edge downward from historical peaks, and rising disposable incomes in these markets shift demand from unbranded wraps to structured carriers priced at USD 30-60. India's birth rate of 16.8 per 1,000 population in 2024, combined with a median age of 28, creates a demographic tailwind that offsets declines in East Asia and Southern Europe[2]Source: World Bank, “Crude Birth Rate” and “Total Fertility Rate,” worldbank.org. Indonesia's expanding middle class, projected to reach 135 million households by 2030, drives demand for international brands that signal quality and safety, with Goodbaby's Cybex label gaining traction in Jakarta and Surabaya through partnerships with premium department stores. Nigeria and Egypt in the Middle East and Africa region exhibit similar dynamics, with birth rates above 25 per 1,000 sustaining market entry for mass-tier brands. However, distribution infrastructure remains fragmented, and brands must navigate import tariffs ranging from 15-35% depending on the country of origin and product classification.

Increasing number of working parents

Labor-force participation among mothers with children under 6 reached 68.3% in the United States in 2024, and OECD data shows similar trends across Northern Europe, where maternal employment rates exceed 70% within two years of childbirth. This structural shift creates demand for carriers that enable multitasking, grocery shopping, commuting, and household chores, while maintaining infant proximity, a need that buckled carriers address more effectively than wraps due to faster on-off cycles. Employers' adoption of on-site childcare and lactation rooms, mandated under updated U.S. Department of Labor guidelines in 2024, further normalizes baby-wearing in professional settings, expanding the use case beyond weekends and errands. Ergobaby's Omni Breeze Plus, launched in 2024 with four carrying positions and breathable mesh, explicitly targets working parents who cycle between forward-facing, hip, and back carries throughout the day. The trend also benefits sling carriers, which offer discreet nursing access in public spaces, a feature increasingly valued as return-to-office mandates reduce remote-work flexibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented regional safety standards | -0.6% | Global, acute in cross-border trade between North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Persistently low birth rates in East Asia and Southern Europe | -0.9% | East Asia (Japan, South Korea, China), Southern Europe (Italy, Spain, Greece) | Long term (≥ 4 years) |

| High costs of premium carriers | -0.5% | Global, most pronounced in price-sensitive emerging markets | Short term (≤ 2 years) |

| Proliferation of counterfeit/low-quality products | -0.4% | Asia-Pacific, Middle East and Africa, South America; e-commerce platforms globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistently low birth rates in East Asia and Southern Europe regions

In 2024, Japan's fertility rate stands at 1.2, while South Korea's is even lower at 0.7. These figures highlight a persistent demographic decline in both nations, one that policy interventions have yet to reverse. According to the World Bank, this trend narrows the addressable market in two regions that have historically been deemed high-value. Italy and Spain, also hovering around a fertility rate of 1.2, are on a similar path. Their aging populations further curtail the household spending typically directed towards baby products. Meanwhile, China's fertility rate, recorded at 1.0, continues to reflect the challenges posed by urbanization and escalating education costs. Despite China's 2021 reversal of its one-child policy, these factors have effectively deterred many from considering second or third births. Highlighting the impact of these domestic challenges, Goodbaby International reported a notable 7.9% decline in revenue for the first half of 2024, emphasizing how local headwinds can overshadow potential international growth[3]Source: Goodbaby International Holdings, “Interim Report 2024,” goodbaby.com. Furthermore, these markets are characterized by strong brand loyalty, posing significant challenges for newcomers aiming to displace established players. Compounding this challenge is a trend of distribution consolidation among major retailers, which has led to a diminished shelf space for niche or emerging brands. Looking ahead, this demographic drag is poised to intensify until 2031. As cohorts, born during previous low-fertility periods, reach their prime childbearing years, the cycle is set to perpetuate.

Proliferation of counterfeit/low-quality products

In fiscal 2024, U.S. Customs and Border Protection seized a staggering USD 5.4 billion worth of counterfeit goods, with a notable 90% of these fakes hailing from China and Hong Kong[4]Source: U.S. Customs and Border Protection, “Fiscal Year 2024 Seizures,” cbp.gov. Baby products, due to their high margins and perceived low risk of enforcement, constituted a significant portion of the counterfeit goods. These counterfeit items, frequently sold by third-party sellers on platforms like Amazon and AliExpress, are often priced 50-70% lower than genuine brands. However, they lacked safety certifications and were made from subpar materials, posing a risk of failure under load. This not only exposed platforms to potential liabilities but also diminished consumer trust in online shopping. A loophole in the system allowed 97% of the seized counterfeits to infiltrate the U.S. via de minimis shipments, which are packages valued under USD 800 that can sidestep formal customs entry. Despite proposed legislative reforms aimed at closing this loophole, they face pushback from e-commerce lobbyists. While brands are turning to anti-counterfeiting strategies like serialized QR codes and blockchain authentication, these measures come at an added cost of USD 2-5 per unit. This poses a challenge for smaller brands that lack the scale for such investments. The issue is particularly pronounced in the Asia-Pacific and Middle East regions, where regulatory enforcement is lax. Here, consumers often remain oblivious to the authenticity of products until a safety-related incident brings the counterfeit nature to light.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Buckled Carriers Dominate Through Ease of Use

Buckled baby carriers accounted for 50.21% of the 2025 market share, driven by their user-friendly clip-and-adjust design, which appeals to first-time parents who prioritize convenience over the learning curve associated with wraps. In contrast, baby sling carriers are expected to grow at the fastest rate, with a 5.88% CAGR through 2031, as millennial consumers increasingly embrace traditional baby-wearing techniques promoted by lactation consultants and doulas. Notable products like Ergobaby's Omni Breeze Plus and BabyBjörn's Harmony Carrier, both launched in 2024, address common issues such as back pain through features like padded shoulder straps and lumbar support, which distribute weight more effectively compared to earlier models. Back pain, a key factor in legacy products' abandonment rates exceeding 30%, has been a significant challenge for the market. Meanwhile, baby wrap carriers, though requiring practice to use effectively, attract attachment-parenting advocates who value skin-to-skin contact and customizable fits for newborns under 10 pounds, a demographic underserved by buckled carriers. The "Other Product Type" category, which includes frame carriers and hybrid designs, remains a niche segment but benefits from the growing popularity of outdoor recreation. Brands such as Osprey and Deuter have expanded distribution through retailers like REI and specialty hiking stores, capitalizing on this trend. Additionally, compliance with ASTM F2236-24, effective February 2025, has increased testing costs for buckled carriers by USD 5,000-10,000 per SKU, leading to market consolidation favoring brands with the financial resources to meet third-party certification requirements mandated by the U.S. Consumer Product Safety Commission.

The 5.88% CAGR of baby sling carriers reflects their positioning as a secondary purchase for parents who already own a buckled carrier but seek a lightweight, portable option for short outings or nursing in public. Brands such as WildBird and Kol Kol differentiate themselves through premium fabric options, including linen, organic cotton, and cashmere blends, which command price points ranging from USD 100 to 200. These carriers appeal to consumers who view them as both functional and fashionable. The segment also benefits from influencer marketing, as sling carriers are visually appealing and perform well on platforms like Instagram and TikTok, generating organic reach that buckle carriers, with their more utilitarian design, struggle to achieve. However, sling carriers face challenges related to safety concerns, as improper positioning can obstruct infant airways. Compliance with the CPSC's 16 CFR Part 1228 requires warning labels and instructional videos, adding to production costs as mandated by the U.S. Consumer Product Safety Commission. Baby wrap carriers, despite their steep learning curve, maintain a loyal customer base among experienced parents and those influenced by attachment-parenting philosophies. These carriers are particularly valued for their ability to provide skin-to-skin contact and a customizable fit for newborns. However, their growth lags behind buckled and sling carriers due to limited retail availability and a reliance on direct-to-consumer sales channels. This restricted distribution model poses a challenge to broader market penetration, limiting their appeal to a niche audience.

Note: Segment shares of all individual segments will be available upon report purchase

By Price Range: Premium Segment Outpaces Mass Market

The mass price segment accounted for 67.51% of the market share in 2025, reflecting consumer preferences for carriers priced between USD 50-80, where functionality takes precedence over brand prestige. However, the premium segment is projected to grow at a CAGR of 8.41% through 2031, surpassing the overall market growth rate of 6.92%. This growth is driven by affluent parents opting for features such as organic fabrics, International Hip Dysplasia Institute certification, and lifetime warranties, which emphasize durability. In early 2025, tariff-driven inflation increased baby-gear prices by 20%, reducing affordability for mass buyers and creating a bifurcated market. Premium brands like BabyBjörn and Ergobaby retained pricing power, while mass-tier competitors such as Infantino and Baby K'tan absorbed margin losses to maintain volume. Additionally, premium buyers increasingly demand transparency regarding labor practices and environmental impact. Brands unable to substantiate sustainability claims face risks of social media backlash, where accusations of greenwashing can quickly damage long-established brand equity.

The resilience of the mass segment is attributed to its strong presence in emerging markets, where median household incomes remain below USD 10,000 annually, making carriers priced above USD 100 aspirational purchases. Goodbaby's Cybex brand, positioned in the premium segment, gained traction in urban markets in India and Indonesia through partnerships with premium department stores. However, Goodbaby International reported a 7.9% revenue decline in H1 2024, as macroeconomic challenges in China offset gains in other regions. Mass-tier brands benefit from omni-channel distribution through retailers such as Walmart, Target, and Amazon. These channels capture impulse purchases from parents who may not have planned to buy a carrier but are drawn by competitive pricing and same-day pickup options.

By Age Group: Baby Segment Dominates, Toddler Grows Fastest

Carriers designed for babies aged 6-12 months accounted for 53.17% of the market share in 2025. This age group represents the peak usage period, as infants have outgrown newborn-specific carriers but are still light enough for extended wear. Meanwhile, the toddler segment (12-36 months) is expected to grow at a CAGR of 6.13% through 2031. This growth is driven by parents extending baby-wearing beyond traditional timelines to manage tantrums and maintain mobility in crowded environments. The infant segment (0-6 months), while critical for first-time buyers, faces challenges due to safety concerns related to airway obstruction. Additionally, the CPSC's 16 CFR Part 1228 regulation requires warning labels and instructional videos for sling carriers, which are the most commonly used in this age group. BabyBjörn's Mini Carrier, launched in 2024, targets the infant segment with a simplified design that eliminates adjustable straps, reducing setup time to under 30 seconds and addressing concerns about complexity that deter adoption among sleep-deprived new parents.

The toddler segment's 6.13% CAGR reflects a shift in usage patterns, as parents increasingly rely on carriers for crowd control in environments such as airports, theme parks, and urban festivals, rather than as a primary mobility solution. In response, brands are designing products with weight capacities of up to 45 pounds and reinforced stitching to withstand the lateral forces generated by active toddlers. Ergobaby's Omni Breeze Plus, rated for children up to 45 pounds, is positioned as a long-term investment, eliminating the need for separate infant and toddler carriers. This value proposition appeals to cost-conscious buyers. Despite its smaller market share, the infant segment remains strategically important for establishing brand loyalty, which influences subsequent purchases. Brands are heavily investing in hospital partnerships and endorsements from lactation consultants to capture first-time buyers. However, growth in this segment is limited by shorter usage periods, as most infants transition to the baby segment by six months, and competition from bassinets and swaddles that address overlapping needs during the newborn phase.

Note: Segment shares of all individual segments will be available upon report purchase

By Distribution Channel: Online Retail Gains at Offline's Expense

Offline retail stores accounted for 44.50% of the market share in 2025, driven by consumers' preference to physically test products before purchase and the ability of retailers to provide immediate gratification through same-day pickup. However, online retail channels are projected to grow at a compound annual growth rate (CAGR) of 7.11% through 2031, surpassing offline channels. This growth is fueled by direct-to-consumer brands that bypass traditional markups and leverage influencer partnerships, achieving conversion rates exceeding 3.5%. Amazon dominates the baby products segment, capturing an estimated 40% of U.S. online baby-gear sales. This compels brands to maintain Amazon storefronts while simultaneously developing their own e-commerce platforms to safeguard pricing integrity. Amazon's Prime membership, which offers free two-day shipping, reduces the friction that previously favored brick-and-mortar purchases. Walmart and Kohl's introduced baby registries in 2024-2025 with omni-channel fulfillment options, allowing customers to order online and pick up in-store within hours. This capability blurs the distinction between online and offline channels, creating a hybrid shopping experience that benefits both formats.

Specialty baby stores and supermarkets/hypermarkets, categorized under offline retail, face margin pressures due to rising rents in high-traffic locations and pricing competition from e-commerce platforms, which undercut prices by 15-25%. The "Other Distribution Channels" category, which includes direct sales, pop-up shops, and hospital gift shops, remains niche but benefits from experiential marketing. For instance, brands like Ergobaby and BabyBjörn host in-person baby-wearing workshops, converting attendees at rates exceeding 20%, which is double the conversion rate of online advertising. The 7.11% CAGR of online retail also reflects challenges such as the proliferation of counterfeit products, which undercut authentic brands by 50-70% and erode consumer trust when safety incidents occur. Platforms are under increasing pressure to implement authentication measures, such as serialized QR codes and blockchain-based verification, as recommended by the U.S. Customs and Border Protection. Despite these challenges, the shift to online retail benefits smaller, direct-to-consumer brands that lack the capital for retail distribution. These brands effectively reach niche audiences through targeted Facebook and Instagram advertising, achieving customer acquisition costs below USD 50 per buyer.

Geography Analysis

North America accounted for 37.05% of the 2025 market share, supported by the enforcement of 16 CFR Part 1226 by the U.S. Consumer Product Safety Commission (CPSC) in February 2025. This regulation mandates third-party testing for soft infant carriers, creating barriers for non-compliant importers and favoring brands with the resources to fund CPSC-accredited lab testing, which costs USD 5,000-10,000 per SKU. The region benefits from high disposable incomes, with median household income exceeding USD 70,000 in the United States and CAD 85,000 in Canada. This supports an 8.41% CAGR in the premium segment, as consumers increasingly opt for organic fabrics and products certified by reputable organizations, such as the International Hip Dysplasia Institute. In Mexico, the expanding middle class, projected to reach 40 million households by 2030, drives demand for mass-tier carriers priced between USD 30 and USD 60. Brands like Infantino and Baby K'tan are expanding their distribution through retailers such as Walmart and Soriana. However, tariff-driven inflation in early 2025 increased baby-gear prices by 20%, reducing affordability for mass-market buyers while creating opportunities for domestic manufacturers marketing "Made in USA" products. Additionally, the region's 68.3% labor-force participation rate among mothers with children under six sustains demand for hands-free caregiving solutions. Employers' adoption of on-site childcare, following updated U.S. Department of Labor guidelines in 2024, has further normalized baby-wearing in professional settings, as reported by the U.S. Bureau of Labor Statistics.

The Asia-Pacific region is the fastest-growing, with a 5.92% CAGR projected through 2031. This growth is driven by high birth rates in India (16.8 births per 1,000 population) and Indonesia (15.9 births per 1,000 population), which sustain absolute birth volumes despite China's declining total fertility rate of 1.0. Rising disposable incomes in urban centers are shifting consumer preferences from unbranded wraps to structured carriers that emphasize quality and safety, according to the World Bank. Goodbaby's Cybex brand has gained traction in Jakarta and Surabaya through partnerships with premium department stores. However, the company's 7.9% revenue decline in H1 2024 highlights how macroeconomic challenges in China offset gains in other markets. Japan and South Korea, with total fertility rates of 1.2 and 0.7, respectively, face structural demographic declines that have not been reversed by policy interventions, shrinking the addressable market in these historically high-value regions. Southeast Asia's rapid urbanization and growing middle class provide a demographic tailwind; however, fragmented distribution infrastructure and import tariffs ranging from 15% to 35% pose significant challenges. Australia and New Zealand, though smaller markets, exhibit high per-capita spending on baby products and strong consumer preference for safety-certified carriers, benefiting brands like BabyBjörn and Ergobaby that comply with voluntary Australian standards.

Europe's market reflects maturity, characterized by high safety awareness and stringent compliance with the EN 13209-1:2021 standards. Germany, the United Kingdom, and France account for the majority of regional demand, while Southern Europe, including Italy and Spain, faces demographic challenges due to declining birth rates, with total fertility rates near 1.2, as reported by the World Bank. Sustainability is a key driver in the region, with demand for organic cotton and recycled materials on the rise. Brands unable to substantiate environmental claims risk backlash on social media, where accusations of greenwashing can spread rapidly. Poland and Sweden, though smaller markets, show above-average growth due to rising incomes and government childcare subsidies that support household spending on baby products. South America and the Middle East and Africa remain emerging markets. In South America, countries such as Brazil, Argentina, and Colombia exhibit birth rates above 13 per 1,000 population, but face challenges due to fragmented retail infrastructure and import tariffs that add 15-35% to landed costs. In the Middle East, the United Arab Emirates and Saudi Arabia lead regional demand, driven by high expatriate populations and disposable incomes. In Africa, countries like Nigeria and Egypt sustain volume growth with birth rates exceeding 25 per 1,000 population, though affordability constraints limit penetration in the premium segment.

Competitive Landscape

The global baby carrier market exhibits moderate concentration, with key players such as Goodbaby International, Artsana Group, Ergobaby, Thrive International, and BabyBjörn holding significant but not dominant positions. No single company commands more than a 15% market share, creating opportunities for agile direct-to-consumer brands. These emerging players utilize influencer partnerships and omnichannel distribution strategies to effectively capture niche segments. Goodbaby International experienced a 7.9% revenue decline in the first half of 2024. While its Cybex premium label gained traction in urban Asia-Pacific markets, macroeconomic challenges in China offset international growth. Additionally, the company's reliance on wholesale channels exposes it to risks such as retailer consolidation and margin pressures. Ergobaby and BabyBjörn focus on product innovation to differentiate themselves. For instance, the Omni Breeze Plus and Harmony Carrier, both launched in 2024, feature breathable mesh and organic cotton materials, with price points ranging from USD 150 to USD 200. These companies also invest heavily in compliance with standards such as ASTM F2236-24 and EN 13209-1:2021, creating barriers for smaller competitors that lack the capital for third-party testing.

White-space opportunities exist in the toddler segment (12-36 months), which is growing at a compound annual growth rate (CAGR) of 6.13% but remains underserved by legacy brands that primarily focus on infant carriers. Additionally, emerging markets such as India and Indonesia present growth potential, as fragmented distribution infrastructure and local manufacturers' ability to undercut imports by 30-40% through domestic sourcing create unique market dynamics. Emerging disruptors like WildBird and Baby K'tan are gaining market share through social media marketing, achieving engagement rates exceeding 5%, which is double the effectiveness of traditional advertising. Their direct-to-consumer models eliminate retail markups, allowing them to offer competitive pricing despite their premium positioning. Technology adoption is also a key trend, with brands utilizing e-commerce platforms, mobile apps featuring augmented reality for virtual try-ons, and blockchain-based authentication to combat counterfeiting. Counterfeit products accounted for USD 5.4 billion in U.S. Customs seizures during fiscal 2024, with 90% originating from China and Hong Kong.

Brands are increasingly investing in sustainability certifications such as GOTS for organic cotton and Oeko-Tex for chemical safety. These certifications help differentiate products in a market where 44% of mothers report making purchases influenced by brand endorsements emphasizing environmental responsibility. However, incumbents face challenges such as margin pressures from tariff-driven cost inflation, which increased baby gear prices by 20% in early 2025. Additionally, Amazon's dominance in online baby product sales forces brands to maintain Amazon storefronts while simultaneously building their own e-commerce channels to protect pricing integrity.

Baby Carrier Industry Leaders

Goodbaby International Holdings Limited

Artsana Group

Ergobaby Inc.

Thrive International, Inc. (Moby Wrap, Inc)

BabyBjörn AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hippychick expanded its Hipseat baby carrier range with the launch of a new Denim Mocha colour variant, combining ergonomic support with fashion-forward design to appeal to style-conscious parents.

- February 2025: Ergobaby launched the Omni Deluxe All-in-One Baby Carrier, featuring enhanced breathability and an innovative ergonomic design that supports four carrying positions, addressing the growing consumer demand for versatile carriers that adapt to different stages of child development.

- August 2024: Bc Babycare announced its participation in Kind + Jugend 2024, where it showcased its upgraded Free Decompression Baby Carrier, reflecting the company's focus on innovation and expansion in the global baby carrier market. The company serves over 50 million users globally, indicating its significant market presence.

- April 2024: Rebelstork and Ergobaby have formed a strategic partnership to launch new products under The ReLuvable Collective. This collaboration aims to expand both companies' markets and promote sustainable practices by addressing environmental concerns related to product returns.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the baby carrier market as all wearable devices purpose-built to secure an infant or toddler to a caregiver's body, including structured buckle carriers, wraps, slings, hip seats, and backpack carriers, sold new through any retail or direct channel worldwide. Our study measures annual sell-through value in U.S. dollars at producer-level price points.

Scope exclusion: second-hand sales, stroller travel systems, and infant car seats are not covered.

Segmentation Overview

- By Product Type

- Buckled Baby Carrier

- Baby Wrap Carrier

- Baby Sling Carrier

- Other Product Type

- By Price Range

- Mass

- Premium

- By Age Group

- Infant (0–6 months)

- Baby (6–12 months)

- Toddler (12–36 months)

- By Distribution Channel

- Supermarkets/Hypermarkets

- Specialty Baby Stores

- Online Retailers

- Other Distribution Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

- Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews were conducted with regional distributors, specialty baby-store managers, and product engineers across North America, Europe, and Asia Pacific. These conversations validated adoption triggers, price corridors, and channel mark-ups and helped us adjust early desk assumptions before triangulating the final model.

Desk Research

Analysts began with population, birth, and female labor-force statistics from tier-one agencies such as the United Nations DESA, World Bank, Eurostat, and the U.S. National Center for Health Statistics, which anchor potential user pools. Trade flows from COMTRADE and Volza shipment data clarified cross-border supply, while patent families pulled via Questel highlighted innovation pacing. Industry associations like the Juvenile Products Manufacturers Association and Baby Products Association offered safety standard timelines that affect replacement cycles.

Company 10-K filings, investor decks, and retailer scans supplied average selling prices and product mix signals, and D&B Hoovers provided revenue splits for privately held manufacturers. The desk sources listed here are illustrative; many additional open and paid references informed data checks and context building.

Market-Sizing & Forecasting

The model starts with a top-down build that links live birth cohorts and urban caregiver penetration to typical carrier ownership rates, then layers channel margin ladders to translate unit demand into producer value. Select bottom-up cross-checks, supplier roll-ups, and sampled ASP × volume from five leading brands align the totals. Key variables tracked include fertility trends, dual-income household share, average selling price drift, e-commerce share in durable nursery goods, regulatory recall events, and fabric cost indices, each stress-tested for elasticity. Forecasts apply a multivariate regression that blends these drivers with three scenario weights discussed with primary experts, after which outlying growth streaks are tempered by historical replacement intervals.

Data Validation & Update Cycle

Outputs pass variance screens against independent shipment tallies and retailer sell-out dashboards; anomalies trigger re-contacts with sources. Two analyst reviews precede release. Reports refresh annually, and material recalls or regulatory shifts prompt interim updates, ensuring clients receive the most current baseline.

Why Mordor's Baby Carrier Baseline Earns Trust

Published estimates often differ because firms pick unmatched product bundles, divergent ASP assumptions, and distinct update cadences.

Key gap drivers in this market include whether slings and hip seats are bundled with broader 'travel systems,' how markdown periods are treated in ASP progression, and the refresh frequency that catches recall-driven demand dips. By selecting a focused wearable definition, validating ASPs quarterly, and revisiting variables each year, Mordor supplies a balanced, transparent anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 652.81 M (2025) | Mordor Intelligence | - |

| USD 2.26 B (2024) | Regional Consultancy A | Includes strollers and car seats, limited primary validation |

| USD 1.30 B (2024) | Trade Journal B | Uses retailer markup values, no cross-border shipment adjustment |

| USD 1.23 B (2024) | Industry Association C | Aggregates sling segment only, excludes backpack carriers |

The comparison shows that wide swings stem from scope creep or narrow segmentation. Mordor's disciplined variable set and yearly refresh cadence give decision-makers a dependable, reproducible baseline.

Key Questions Answered in the Report

What is the current value of the baby carrier market?

The baby carrier market size is USD 698.12 million in 2026 with a forecast value of USD 975.49 million by 2031.

Which product type holds the largest share?

Buckled carriers lead the category with 50.21% of 2025 sales.

Which region is growing the fastest?

Asia-Pacific posts the highest 5.92% CAGR through 2031, driven by sustained birth volumes in India and Indonesia.

Why are premium models expanding faster than mass ones?

Premium growth at 8.41% CAGR is fueled by demand for organic fabrics, ergonomic certification, and influencer-driven brand storytelling.

What role do online channels play in category growth?

Online retail records a 7.11% CAGR, outpacing offline as fast shipping, registry integration, and influencer content lower purchase barriers.

Page last updated on: