Baby Oral Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

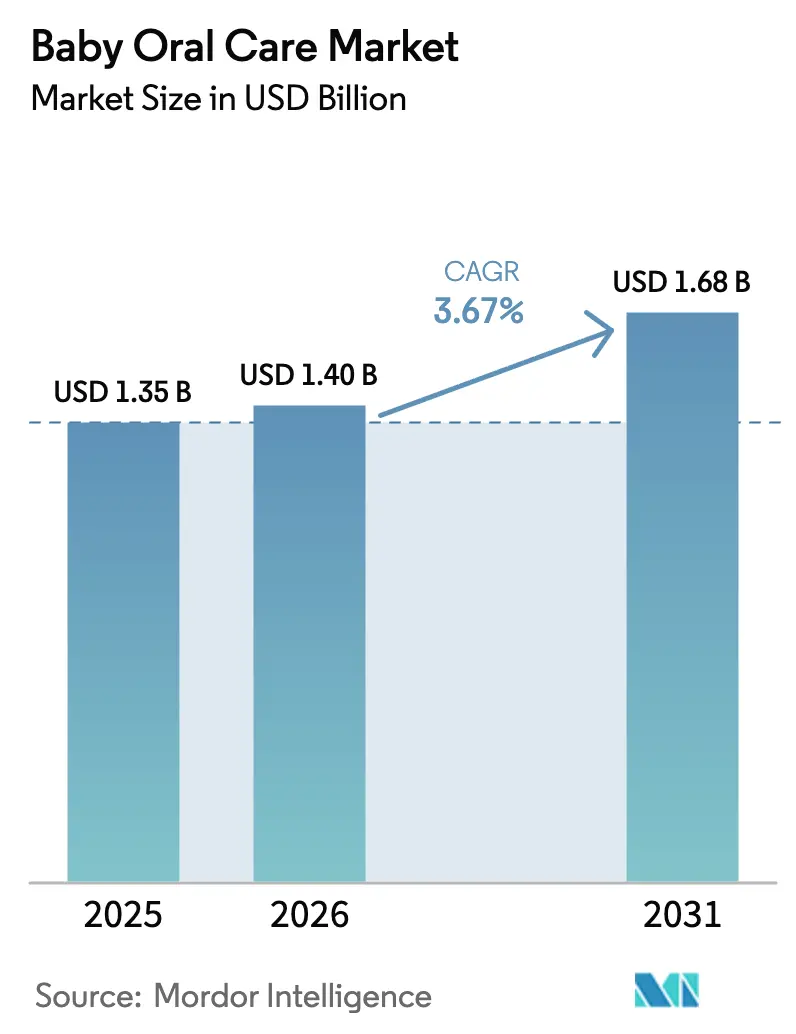

| Market Size (2026) | USD 1.4 Billion |

| Market Size (2031) | USD 1.68 Billion |

| Growth Rate (2026 - 2031) | 3.67% CAGR |

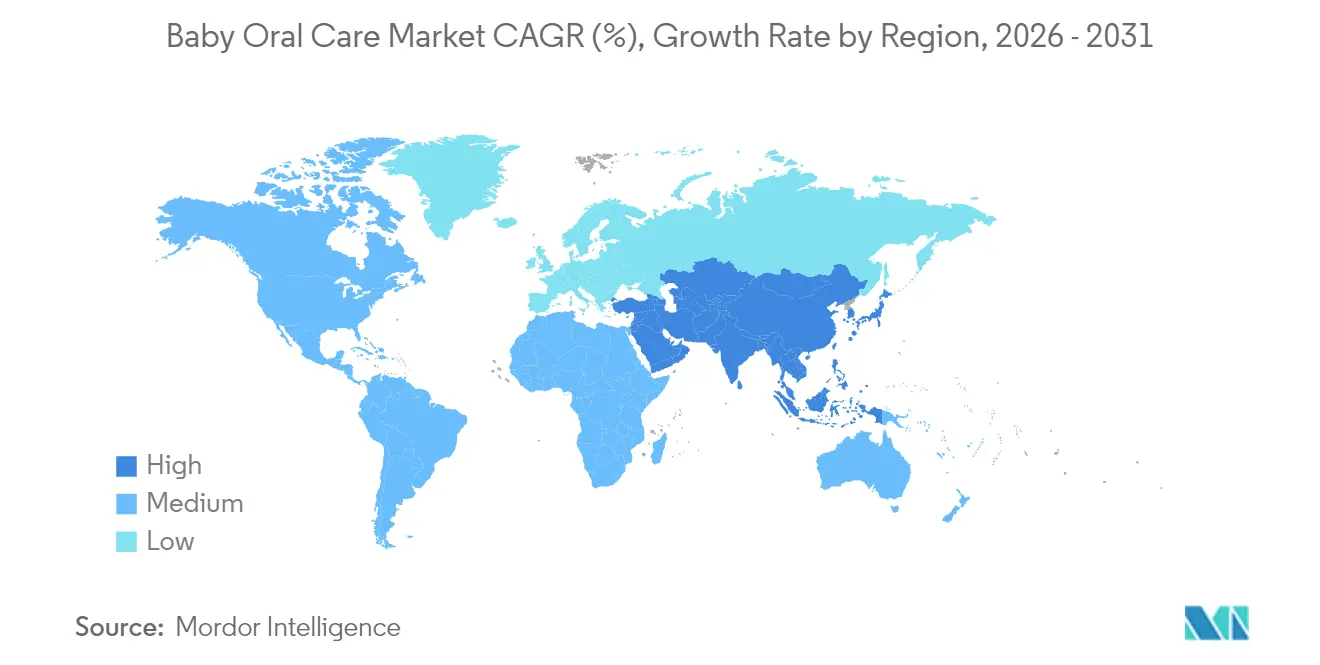

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Baby Oral Care Market Analysis by Mordor Intelligence

The baby oral care market size is expected to grow from USD 1.35 billion in 2025 to USD 1.4 billion in 2026 and is forecast to reach USD 1.68 billion by 2031 at 3.67% CAGR over 2026-2031. Parents are acting sooner to prevent early childhood caries, as the Centers for Disease Control and Prevention reports 11% of U.S. children aged 2-5 exhibiting untreated cavities in their primary teeth in 2024 [1]Source: Centers for Disease Control and Prevention, “Oral Health Surveillance Report,” cdc.gov. Government-funded fluoride-varnish programs, the viral reach of pediatric-dentist guidance on social media, and expanding e-commerce channels are reinforcing demand for specialized brushes, pastes, and wipes that cater to infants and toddlers. Material innovation is another growth catalyst: BPA-free plastics hold the largest share today, yet biodegradable bio-plastics are on track for double-digit growth as millennial and Gen Z parents favor sustainable goods. Regionally, Asia-Pacific anchors the category, while the Middle East registers the fastest sales rise on the back of higher birth rates, premium retail expansion, and rising disposable income.

Key Report Takeaways

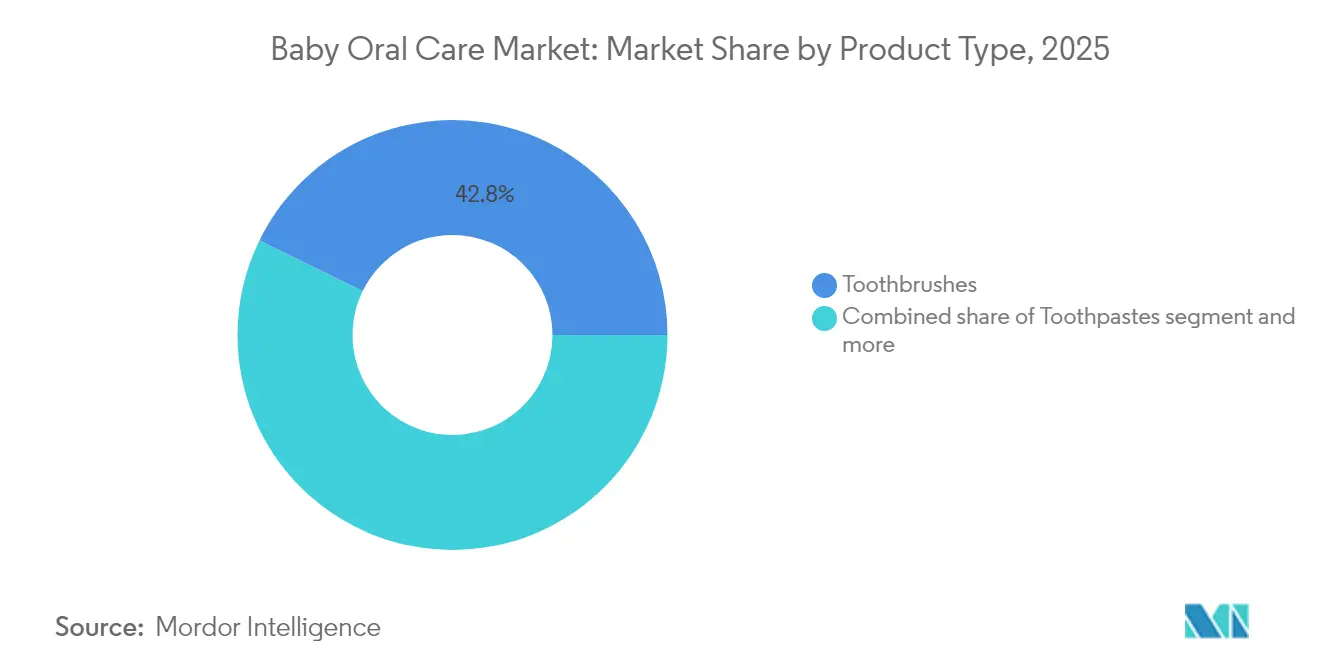

- By product type, toothbrushes led with 42.75% of the baby oral care market share in 2025, while silicone finger brushes are projected to grow at a 10.67% CAGR through 2031.

- By age group, the 1-2 years dominated with a 34.35% share in 2025; the 0-6 months cohort is set to expand at a 9.56% CAGR from 2026-2031.

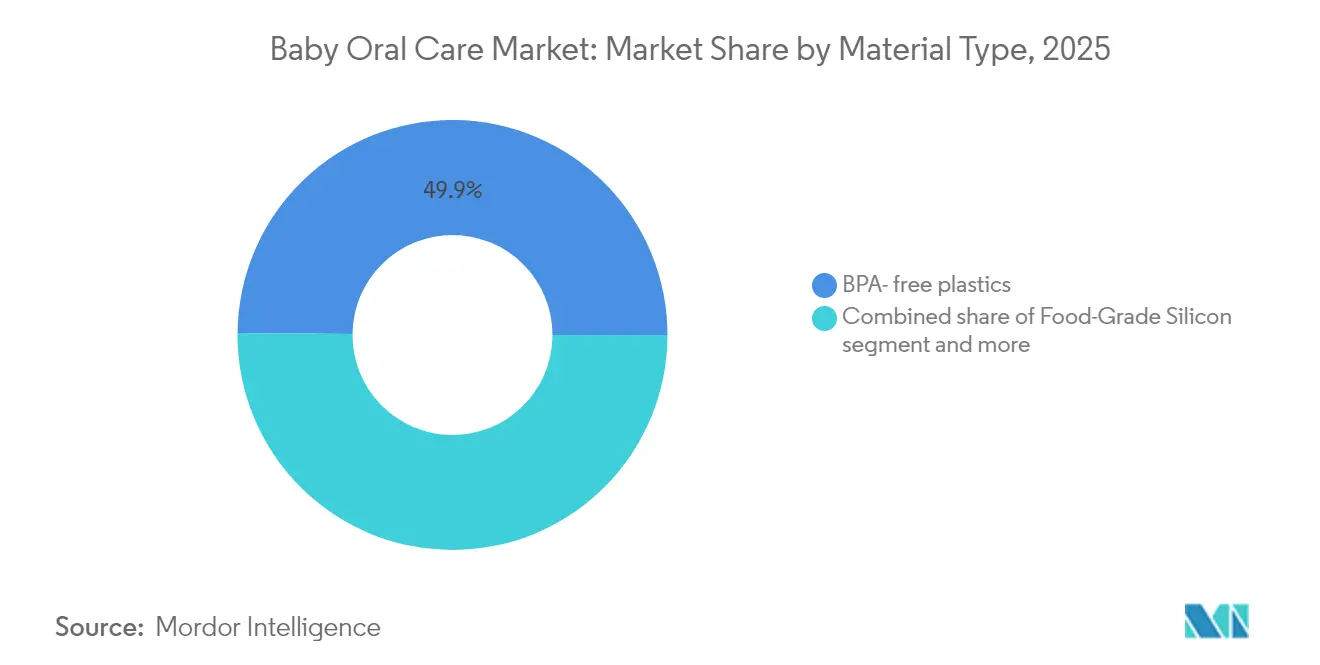

- By material, BPA-free plastics held a 49.85% share in 2025, yet biodegradable bio-plastics are forecast to advance at a 12.25% CAGR to 2031.

- By distribution channel, supermarkets and hypermarkets commanded 38.10% share in 2025, whereas online retail is expected to climb at a 13.11% CAGR.

- By geography, Asia-Pacific accounted for 40.05% of the 2025 share, and the Middle East and Africa are poised for a 9.37% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Baby Oral Care Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Early Childhood Caries Driving Preventive Oral-Care Purchases | +1.0% | Global, with higher impact in Middle East and Asia-Pacific | Medium term (2-4 years) |

| Growing Birth Rate in Developing Countries | +0.8% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Parents Prioritizing Silicone Finger Brushes for Gingival Massage | +0.7% | North America, Europe, and urban centers in Asia-Pacific | Short term (≤ 2 years) |

| Innovative and Natural Products Launches | +0.6% | Global, with higher adoption in North America and Europe | Medium term (2-4 years) |

| Government Fluoride Varnish Programs Boosting Baby Toothpaste Adoption | +0.5% | North America and Europe | Medium term (2-4 years) |

| Pediatric Dentist Recommendations Integrated into Social-Media Influencer Marketing | +0.4% | Global, with higher impact in regions with high social media penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Early Childhood Caries Driving Preventive Oral-Care Purchases

The prevalence of early childhood caries is rising across the world. This alarming rate is prompting parents to invest in preventive oral care products earlier in their children's development, with the American Academy of Pediatric Dentistry's 2024 policy update emphasizing the establishment of a dental home by 12 months of age [2]Source: American Academy of Pediatric Dentistry, “Policy on Early Childhood Oral Health,” aapd.org. The economic burden of treating dental caries, often requiring costly interventions under general anesthesia for young children, is creating a compelling value proposition for preventive products, particularly in regions with limited access to pediatric dental care. Manufacturers are responding by developing age-specific formulations with appropriate fluoride concentrations and incorporating educational components into their packaging to guide proper usage, effectively transforming the purchase decision from discretionary to essential. The National Institute of Dental and Craniofacial Research's 2024 research highlights that tooth decay affects nearly 46% of children in the U.S., underscoring the urgent need for preventive interventions

Parents Prioritizing Silicone Finger Brushes for Gingival Massage

Silicone finger brushes are experiencing rapid adoption, particularly for infants in the 0-6 months age group, as they serve the dual purpose of oral cleaning and teething relief. The material innovation in this category has accelerated, with manufacturers like SmilyMia developing food-grade silicone variants that are BPA-free, phthalate-free, and latex-free, addressing parental concerns about chemical exposure. Pediatric dentists are increasingly recommending these products for early oral hygiene routines, with Dr. Ashley Lerman, a pediatric dentist who developed the Soft Silicone Finger Brush, emphasizing their role in preventing future dental issues by establishing good habits from infancy. The ergonomic design of these brushes also enables better compliance among caregivers, as they provide greater control and comfort during the cleaning process, while their textured surfaces offer effective plaque removal and gum stimulation.

Government Fluoride Varnish Programs Boosting Baby Toothpaste Adoption

Government-sponsored fluoride varnish programs are driving awareness of fluoride's role in cavity prevention and early dental care. As of 2024, 53% of children aged 0-18 have private dental benefits, while 38% are covered by Medicaid or CHIP, according to the American Dental Association's Health Policy Institute. This is boosting demand for fluoride products at home. However, the FDA's planned withdrawal of fluoride supplements for children in May 2025 may shift preferences toward alternatives. Manufacturers are responding with innovations like hydroxyapatite-based toothpastes, identified as safer options in a 2024 fluoride dosing study. The Massachusetts Oral Health Practice Guidelines for Pregnancy and Early Childhood, updated in October 2024, further emphasize the importance of coordinated care between healthcare providers and parents in establishing effective oral hygiene routines

Growing Birth Rate in Developing Countries

In developing countries, sustained population growth is expanding the market for baby oral care products, with elevated birth rates in regions like sub-Saharan Africa, Asia-Pacific, and Latin America. Countries such as India and Nigeria, with growing middle-class populations and high birth rates, offer significant opportunities. The World Health Organization's initiatives are raising awareness of early childhood oral care, driving market growth, and education. Modern retail infrastructure is improving product access and brand recognition, while government health programs support maternal and child health. However, these drivers' full impact will take time, relying on economic growth and shifting healthcare priorities.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Parental Misconceptions Around Fluoride Toxicity Limiting Toothpaste Penetration | -0.6% | Global, with higher impact in regions with active anti-fluoride movements | Medium term (2-4 years) |

| Intense Price Competition from Private-Label Brands in Hypermarkets | -0.4% | Europe and North America | Short term (≤ 2 years) |

| Regulatory Scrutiny Over Sweeteners & Flavorings Delaying Approvals | -0.3% | North America and Europe | Medium term (2-4 years) |

| Lack of Standardized Guidelines | -0.3% | Global, with higher impact in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Parental Misconceptions Around Fluoride Toxicity Limiting Toothpaste Penetration

Parental misconceptions about fluoride safety are hindering the adoption of fluoride toothpaste for infants and toddlers. Ongoing legal challenges, such as the 2025 lawsuit against Colgate-Palmolive, highlight this issue. The lawsuit claims Colgate-Palmolive misleads consumers about the safety of fluoride in their children's toothpaste. Adding to the confusion, the FDA's May 2025 decision to withdraw ingestible fluoride products for children has further muddied the waters. In response, manufacturers are creating fluoride-free alternatives and providing clearer dosing instructions. However, educating consumers remains a daunting task, especially in areas with strong anti-fluoride sentiments. As the industry strives to regain consumer trust through open communication and product innovation, and as regulatory bodies seek to clarify safe fluoride guidelines for children, these challenges are poised to have a medium-term impact.

Intense Price Competition from Private-Label Brands in Hypermarkets

Private-label brands in hypermarkets are increasing price pressure on the baby oral care market by leveraging scale and direct consumer relationships. This trend is prominent in Europe and North America, where retailers have expanded private label portfolios to include oral care products. Branded manufacturers, especially in the mid-market segment, face margin compression and must invest in innovation or risk losing market share. Price sensitivity is highest in basic toothbrushes and toothpaste, where differentiation is difficult. Premium brands emphasize clinical validation, age-specific features, and sustainable materials to justify higher prices, though success varies by region. Branded manufacturers are adapting their strategies and exploring direct-to-consumer channels to counter private-label growth and maintain margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Silicone Finger Brushes Redefine Infant Oral Care

The toothbrushes segment commanded a dominant 42.75% market share in 2025, reflecting its status as the fundamental tool in baby oral care routines. Within this category, silicone finger brushes are emerging as the fastest-growing sub-segment with a projected CAGR of 10.67% from 2026-2031, driven by their versatility in providing both cleaning and teething relief for infants. Electric training brushes are gaining traction in the 2-3-year age group, with features like musical timers and character designs enhancing compliance among toddlers.

The toothpaste segment is experiencing a shift toward fluoride-free formulations, particularly for the 0-6 months age group, in response to parental concerns about fluoride ingestion. Oral wipes and gum massagers represent a smaller but growing segment, particularly popular for on-the-go use and as complementary products to traditional brushing routines. The overall product landscape is evolving toward more specialized solutions tailored to specific developmental stages and oral health needs, with a growing emphasis on multi-functional designs that address multiple concerns simultaneously.

By Age Group: Early Intervention Drives 0-6 Months Growth

The 1-2 years age group held the largest market share at 34.35% in 2025, representing a critical period when most primary teeth have erupted and structured oral hygiene routines become established. However, the 0-6 months segment is experiencing the fastest growth with a 9.56% CAGR from 2026-2031, reflecting the paradigm shift toward earlier intervention in oral health. This trend is supported by the American Academy of Pediatric Dentistry's 2024 policy update, which emphasizes establishing a dental home by 12 months of age and initiating oral hygiene practices as soon as the first tooth appears . Products designed for this youngest segment focus on gentle cleaning and gum care, with silicone finger brushes and oral wipes dominating the category.

The 6-12 months segment marks the shift from gum care to tooth brushing as primary teeth erupt, with products featuring soft bristles and ergonomic handles. For the 2-3-year age group, the focus is on independent brushing habits, supported by playful designs, timers, and interactive features. The Massachusetts Oral Health Practice Guidelines, updated in October 2024, highlight the need for age-appropriate oral care products. Age-based segmentation reflects the rapid evolution of oral health needs in the first three years, requiring specialized products for each stage.

By Material Type: Biodegradable Bio-Plastics Lead Sustainability Shift

BPA-free plastics dominated the baby oral care market with a 49.85% share in 2025, reflecting the industry's response to consumer concerns about chemical exposure in products that enter infants' mouths. However, biodegradable bio-plastics are emerging as the fastest-growing material category with a projected CAGR of 12.25% from 2026-2031, driven by increasing environmental consciousness among millennials and Gen Z parents. This shift is supported by innovations in material science, with companies like Biobrush developing children's toothbrushes made from wood chips and castor oil-based nylon bristles that are 94% biodegradable.

Food-grade silicone, prized for its flexibility, durability, and hypoallergenic nature, plays a pivotal role, especially in products targeting the 0-6 months age group. To allay parental concerns over material safety, manufacturers spotlight certifications like FDA approval and BPA-free status in their marketing. The sector is witnessing a surge in material innovation, with a keen focus on exploring new biodegradable materials that promise top-notch performance while being environmentally friendly. Additionally, the growing demand for sustainable and safe baby products is driving manufacturers to invest in advanced research and development. This trend aligns with the increasing consumer preference for eco-friendly and non-toxic materials.

By Distribution Channel: Online Retail Disrupts Traditional Sales Models

Supermarkets and hypermarkets maintained the largest market share at 38.10% in 2025, benefiting from their one-stop shopping convenience for parents and their ability to showcase a wide range of baby oral care products. However, online retail is experiencing explosive growth with a 13.11% CAGR projected from 2026-2031, fundamentally reshaping how parents discover and purchase baby oral care products. E-commerce platforms are leveraging content marketing and educational resources to guide purchase decisions, addressing the information gap that often exists at physical retail.

Pharmacies and drug stores represent a significant channel, particularly for premium and medically-positioned products, benefiting from the trust associated with healthcare settings. Specialty baby stores offer curated selections and personalized advice, though their market share varies significantly by region. The "Others" category, including direct-to-consumer models and subscription services, is gaining traction by offering convenience and personalization. The evolution of distribution channels is creating both challenges and opportunities for manufacturers, requiring more sophisticated omnichannel strategies to maintain visibility and influence purchase decisions across increasingly fragmented touchpoints.

Geography Analysis

In 2025, Asia-Pacific commands the baby oral care market, holding a 40.05% share. This dominance is fueled by the region's vast population, rising disposable incomes, and heightened awareness of infant oral health. Within Asia-Pacific, India stands out as a burgeoning market, spurred by urbanization and the swift rise of modern retail formats. Meanwhile, Japan, though smaller in population, boasts a discerning market with significant per-capita spending on baby oral care, underscoring its commitment to product innovation and quality. Additionally, the region enjoys a boost from government policies championing maternal and child health, setting the stage for market growth.

The Middle East and Africa is on a rapid ascent, forecasting a CAGR of 9.37% from 2026-2031. This surge is attributed to high birth rates, a growing health consciousness, and swift retail modernization. Saudi Arabia and the UAE lead the charge, with premium international brands thriving, thanks to the region's affluent, status-driven consumers. The rise of specialized baby product retailers, coupled with e-commerce platforms like Mumzworld, recently acquired by Tamer Group, is bolstering product accessibility and consumer awareness. With a youthful demographic and a pivot towards preventive healthcare, the region is witnessing a sustained appetite for innovative baby oral care solutions.

North America, while mature, is a hotbed of innovation. The U.S. takes the lion's share, bolstered by a robust healthcare framework and a keen emphasis on preventive dental care. The market here is notably segmented, with offerings tailored to distinct age groups and oral health requirements. Europe mirrors this trend, spotlighting the UK, Germany, and France as its frontrunners. However, Europe's market dynamics are notably influenced by stringent regulations, especially concerning chemical ingredients and sustainability, which in turn shape product development and marketing. In South America, Brazil emerges as the frontrunner, buoyed by its sizable population and an expanding middle class. Yet, the region grapples with economic fluctuations and inconsistent dental care access. Still, government initiatives promoting child health present avenues for market growth.

Competitive Landscape

The baby oral care market shows moderate consolidation, with established global companies and specialized brands competing for market share. Companies such as Colgate-Palmolive Company, Kenvue Inc., and Procter & Gamble Company maintain their market positions through extensive research capabilities, strong distribution networks, and significant investments in product development. These companies benefit from their established brand recognition, economies of scale, and ability to invest in advanced manufacturing technologies. However, they face growing competition from specialized startups focusing exclusively on baby care products.

The market demonstrates two distinct strategic approaches: global companies expand through acquisitions, product line extensions, and geographical market penetration, while specialized brands establish market presence through material innovations, targeted product development, and digital marketing campaigns targeting millennial parents who prioritize natural and safe ingredients. Market opportunities exist in three key areas: biodegradable materials, smart connected devices, and products for infants aged 0-6 months. The biodegradable materials segment focuses on developing eco-friendly oral care products that address growing environmental concerns. Smart connected devices incorporate technology to improve oral hygiene habits and monitoring capabilities for parents.

Companies like Brush-Baby Ltd. and Jack N' Jill Kids are gaining market share through focused product innovation, brand authenticity, and the development of specialized oral care solutions for different age groups. Technology adoption is becoming crucial for competitive advantage, as demonstrated by Colgate-Palmolive's sustainability initiatives. The company plans to convert 60% of its toothpaste products to recyclable tubes by 2024, expanding to 100% by 2025, reflecting the industry's broader shift toward sustainable packaging solutions and environmentally responsible manufacturing practices.

Baby Oral Care Industry Leaders

Colgate-Palmolive Company

Kenvue Inc.

The Procter & Gamble Company

GlaxoSmithKline PLC

Pigeon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Pepsodent, Ghana's leading oral care brand, launched a new toothpaste specifically for babies. The products are available in strawberry and orange flavors. The product is formulated to protect teeth from sugar acids, promoting oral health.

- November 2024: Marico Bangladesh Limited introduced a gel baby toothpaste under its Parachute Just for Baby brand in Bangladesh. The product features mango and orange flavors, with the mango variant being the first in the country. The toothpaste is fluoride-free, contains no sugar, and uses safe ingredients.

- September 2023: Edgewell Personal Care acquired Mamamoo Baby, a natural baby care products brand that includes oral hygiene solutions. The acquisition expands Edgewell's baby product portfolio and addresses consumer preferences for natural and chemical-free infant hygiene products.

- July 2023: STIM Oral Care has introduced "Hoppy Kids," a toothbrush designed for children aged 3 to 10 years. The toothbrush features densely packed bristles that clean teeth thoroughly and remove plaque to maintain oral hygiene.

Global Baby Oral Care Market Report Scope

Baby oral care includes products that are intended to cleanse the oral cavity, freshen the breath, and maintain good oral hygiene in infants and toddlers.

The baby oral care market is segmented by product type, age group, material type, distribution channels, and geography. By product type, the market is segmented into toothbrushes, toothpastes, and oral wipes & gum massagers. Toothbrushes are further segmented into silicone finger brushes and electric training brushes. Toothpastes are further segmented into fluoride toothpastes (≤1,000 ppm F) and fluoride-free toothpastes. By age group, the market is segmented into 0–6 months, 6–12 months, 1–2 years, and 2–3 years. The market is segmented by material type into BPA-free plastics, food-grade silicone, and biodegradable bio-plastics. By distribution channels, the market is segmented into supermarkets /hypermarkets, pharmacies & drug stores, specialty baby stores, online retail, and others. The market is segmneted by geography into North America, Europe, Asia Pacific, South America, and Middle East, and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| Toothbrushes | Silicone Finger Brushes |

| Electric Training Brushes | |

| Toothpastes | Fluoride Toothpastes (≤1,000 ppm F) |

| Fluoride-Free Toothpastes | |

| Oral Wipes & Gum Massagers |

| 0–6 Months |

| 6–12 Months |

| 1–2 Years |

| 2–3 Years |

| BPA-Free Plastics |

| Food-Grade Silicone |

| Biodegradable Bio-plastics |

| Supermarkets/Hypermarkets |

| Pharmacies & Drug Stores |

| Specialty Baby Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Toothbrushes | Silicone Finger Brushes |

| Electric Training Brushes | ||

| Toothpastes | Fluoride Toothpastes (≤1,000 ppm F) | |

| Fluoride-Free Toothpastes | ||

| Oral Wipes & Gum Massagers | ||

| By Age Group | 0–6 Months | |

| 6–12 Months | ||

| 1–2 Years | ||

| 2–3 Years | ||

| By Material Type | BPA-Free Plastics | |

| Food-Grade Silicone | ||

| Biodegradable Bio-plastics | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies & Drug Stores | ||

| Specialty Baby Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the baby oral care market?

The market is valued at USD 1.4 billion in 2026 and is projected to reach USD 1.68 billion by 2031.

Which product category leads sales?

Toothbrushes hold 42.75% of revenue, with silicone finger brushes recording the fastest 10.67% CAGR outlook.

Why are biodegradable materials gaining traction?

Millennial and Gen Z parents favor eco-friendly choices, driving biodegradable bio-plastics toward a 12.25% CAGR through 2031.

Which region grows the fastest?

The Middle East and Africa is expected to expand at a 9.37% CAGR owing to high birth rates, premium retail growth and rising health awareness.

Page last updated on: