North America Automotive Heat Shield Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

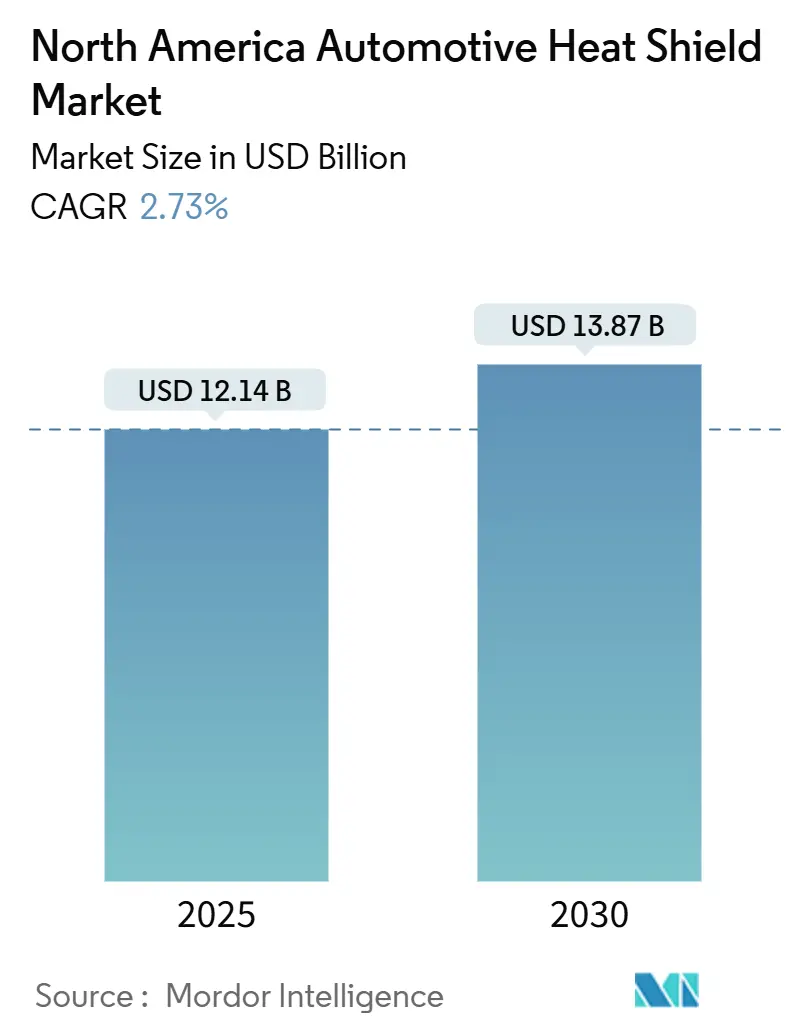

| Market Size (2025) | USD 12.14 Billion |

| Market Size (2030) | USD 13.87 Billion |

| Growth Rate (2025 - 2030) | 2.73% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Automotive Heat Shield Market Analysis by Mordor Intelligence

The North America automotive heat shield market was valued at USD 12.14 billion in 2025 and is projected to reach USD 13.87 billion by 2030, reflecting a 2.73% CAGR. Demand stability arises from conventional exhaust and turbocharger shielding in internal-combustion vehicles, while electrification creates incremental revenue through battery thermal-runaway barriers and power-electronics protection.

Key Report Takeaways

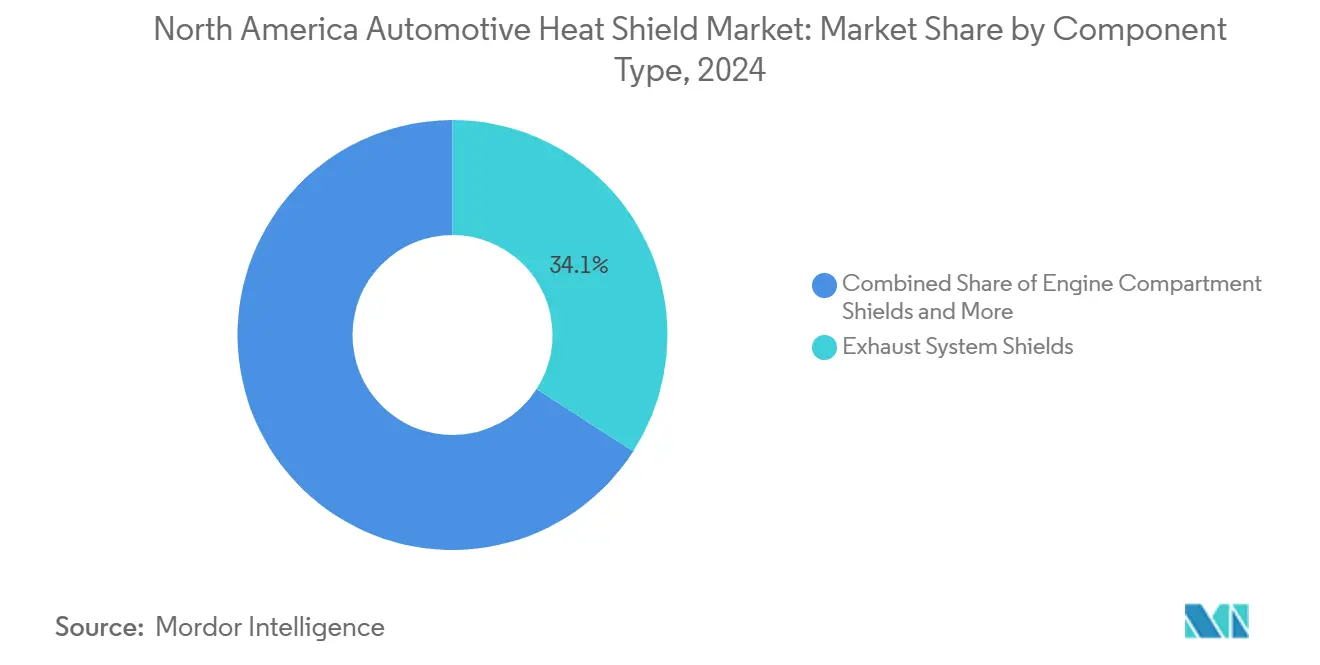

- By component, exhaust system shields led with 34.09% of North America automotive heat shield market share in 2024, while battery and power-electronics shields posted the highest projected CAGR at 13.84% through 2030.

- By material, metallic solutions accounted for 72.14% share of the North America automotive heat shield market size in 2024, whereas non-metallic composites are forecast to expand at a 14.53% CAGR to 2030.

- By product structure, single-shell shields commanded 51.07% of the North America automotive heat shield market size in 2024, but sandwich composites exhibit the quickest growth at 15.28% CAGR over the same period.

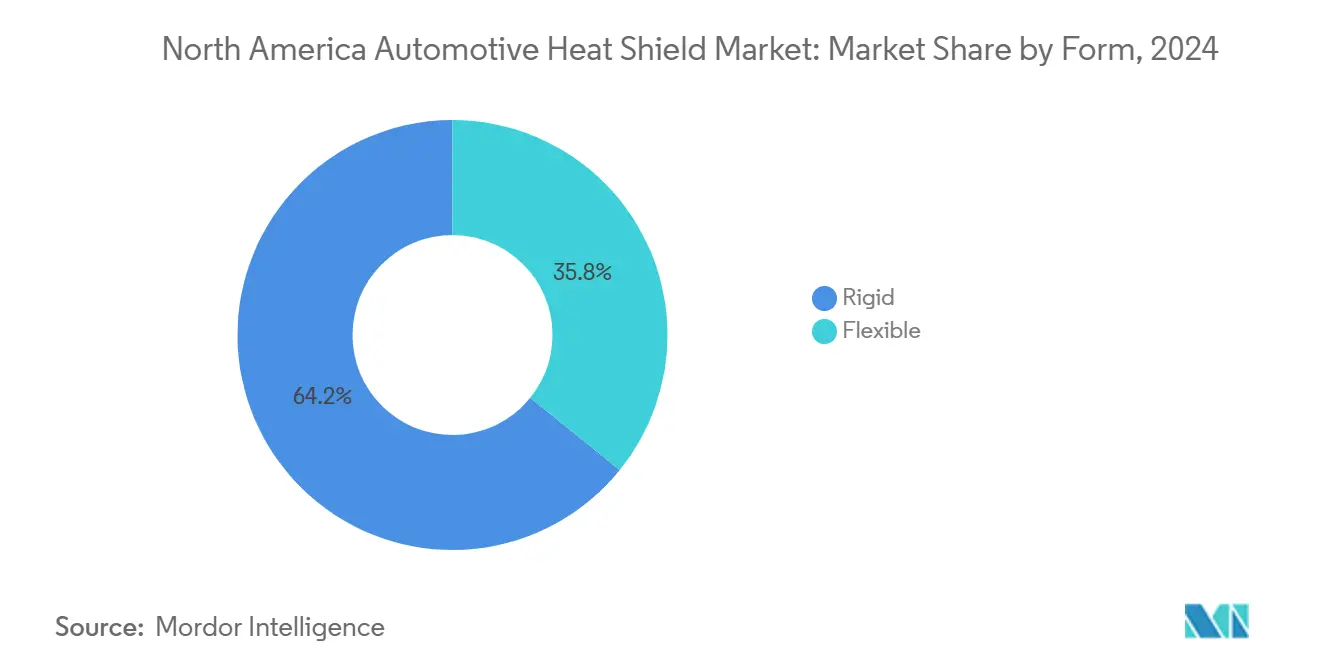

- By form, rigid shields held 64.22% revenue share in 2024, with flexible shields advancing at a 14.06% CAGR through 2030.

- By vehicle propulsion, ICE platforms represented 68.31% share of the North America automotive heat shield market size in 2024, yet battery electric vehicles deliver the strongest 18.47% CAGR outlook.

- By sales channel, OEMs captured 79.36% revenue in 2024, but the aftermarket is set to grow at a 7.82% CAGR on account of an aging vehicle parc.

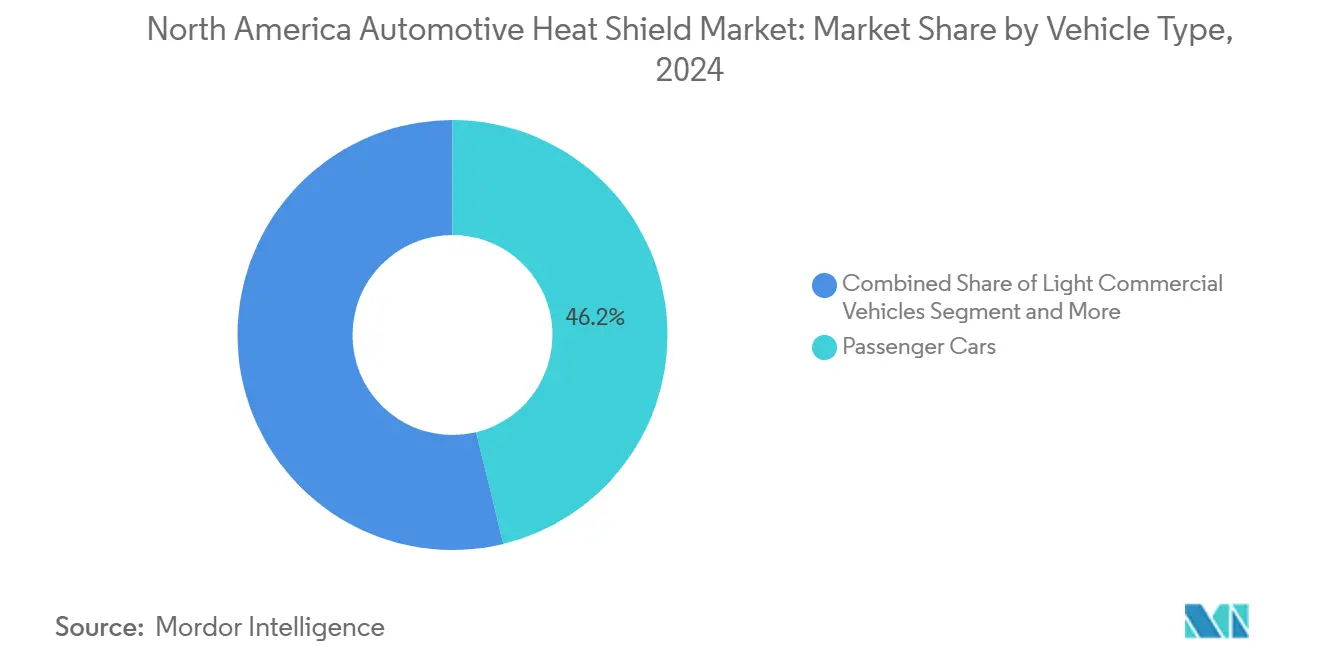

- By vehicle type, passenger cars generated 46.18% of 2024 market value, whereas off-highway and agricultural machinery record the fastest 9.24% CAGR to 2030.

- By geography, the United States dominated with a 58.27% 2024 share, while Canada shows the fastest regional CAGR at 7.15% through 2030.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on automotive heat shield market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Automotive Heat Shield Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Emission and Noise Regulations | +1.4% | North America; strongest in California and CARB states | Medium term (2-4 years) |

| Engine Downsizing With Turbocharging | +0.8% | U.S. light-vehicle segment | Short term (≤2 years) |

| Increased SUV and Light-Truck Sales | +0.7% | United States with spillover to Canada | Short term (≤2 years) |

| Battery Enclosure Shields for EV Runaway | +0.5% | EV manufacturing hubs | Long term (≥4 years) |

| Lightweight Sandwich-Composite Adoption | +0.3% | United States for CAFE compliance | Medium term (2-4 years) |

| Shale-Gas–Driven HD-Truck Demand Boost | +0.2% | Energy-corridor states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Emission and Noise Regulations

Regulatory tightening under CAFE standards and state-level emission mandates drives heat shield demand through multiple pathways beyond traditional exhaust applications. Engine bay thermal management requirements intensify as manufacturers pursue aggressive downsizing strategies to meet 40.5 mpg fleet averages by 2026, necessitating enhanced turbocharger and intake manifold shielding to protect adjacent components from elevated heat loads. The regulatory cascade effect extends to brake particulate emissions, where Euro 7-aligned standards anticipated for North America by 2027 require thermal management solutions for brake dust mitigation systems. IATF 16949:2016[1]"IATF 16949:2016," aiag.org. certification requirements ensure heat shield suppliers maintain quality management systems aligned with automotive industry standards, creating barriers to entry while consolidating market share among certified manufacturers.

Engine Downsizing with Turbocharging

Turbocharger adoption rates exceeding 35% in North American light vehicles by 2024 create concentrated thermal management challenges that traditional naturally aspirated engines never encountered. Exhaust gas temperatures reaching 1,050°C in turbocharged applications versus 850°C in naturally aspirated engines demand advanced shielding materials and designs to protect surrounding components from thermal degradation. The trend toward integrated exhaust manifolds and turbocharger housings compounds heat density, requiring multi-layer composite shields with enhanced thermal conductivity management rather than simple metallic barriers. OEMs increasingly specify sandwich composite constructions combining metallic outer shells with ceramic fiber cores to achieve thermal performance while meeting weight reduction targets under CAFE regulations.

Lightweight Sandwich-Composite Adoption for CAFE Targets

CAFE compliance strategies drive material substitution from traditional steel and aluminum shields toward advanced composites offering 40-60% weight reductions without thermal performance compromise. Polyimide-aerogel combinations such as Blueshift Materials' AeroZero demonstrate 85% air content while maintaining structural integrity under vibration loads, enabling thin-profile applications previously impossible with conventional materials. The regulatory imperative creates a cost-performance inflection point where composite premium pricing becomes justified by fuel economy credits, particularly in premium vehicle segments where CAFE penalties exceed material cost differentials. Manufacturing scalability remains constrained by limited composite processing capacity, creating supply chain bottlenecks that favor established suppliers with dedicated composite production lines.

Battery Enclosure Shields for EV Thermal-Runaway

EV battery thermal runaway protection represents the market's highest-growth application, driven by safety regulations and insurance requirements rather than traditional performance optimization. Thermal runaway events can reach 800-1,000°C within minutes, requiring specialized barrier materials that maintain structural integrity while preventing fire propagation between battery modules. Advanced aerogel composites offer superior thermal diffusivity control compared to traditional metallic shields, enabling thinner barrier designs that preserve battery pack energy density while meeting safety requirements. The application demands materials certification under UL 2580 and ISO 26262 functional safety standards, creating technical barriers that consolidate market share among specialized suppliers with battery-specific expertise.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gradual ICE Production Decline | -0.6% | North America; fastest drop in California and ZEV states | Long term (≥4 years) |

| Volatility in Metal Prices | -0.4% | North America; steel and aluminum inputs | Short term (≤2 years) |

| Lack of Composite Shield Test Standards | -0.2% | North America; certification delays | Medium term (2-4 years) |

| Ceramic-Fiber Supply-Chain Disruptions | -0.3% | Global sourcing with NA assembly | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Gradual ICE Production Decline

ICE vehicle production trajectories in North America show accelerating decline rates, with light vehicle ICE share dropping from 68.31% in 2024 toward a projected 45% by 2030 as EV mandates intensify across key states. The transition creates demand displacement where traditional exhaust system shields, representing 34.09% of the current market value, face volume contraction while EV thermal management applications remain nascent in revenue contribution. Regional variations compound the challenge, with California's Advanced Clean Cars II regulation requiring 100% zero-emission light vehicle sales by 2035, creating geographic pockets of accelerated ICE demand destruction. Supply chain optimization becomes critical as manufacturers balance declining ICE shield volumes against uncertain EV thermal management ramp rates, potentially creating capacity utilization challenges for specialized exhaust shielding production lines.

Volatility in Metal Prices

Steel and aluminum price volatility directly impacts metallic heat shield margins, with 72.14% market share concentrated in metal-based solutions vulnerable to commodity price swings. Recent steel price fluctuations exceeding 25% annually create margin compression for fixed-price OEM contracts, while aluminum pricing volatility affects lightweight shield applications targeting CAFE compliance. The constraint intensifies under potential trade policy changes, where steel tariffs reaching 50% and aluminum tariffs at 25% could reshape North American supply chains toward domestic sourcing at premium pricing. Material cost pass-through mechanisms remain limited in automotive contracts, forcing suppliers to absorb volatility through operational efficiency improvements or strategic inventory management rather than pricing adjustments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Battery Shields Drive Electrification Transition

Exhaust system shields hold the largest 34.09% market share in 2024, while battery and power-electronics shields emerge as the fastest-growing component segment at 13.84% CAGR through 2030. The growth divergence reflects the automotive industry's electrification pivot, where traditional exhaust applications face volume decline while EV thermal management creates entirely new component categories requiring specialized materials and designs. Turbocharger and intake-manifold shields benefit from engine downsizing trends, maintaining steady demand as naturally aspirated engines transition to forced induction configurations. Underbody and floor-pan shields experience moderate growth driven by lightweighting initiatives and enhanced thermal management requirements for both ICE and EV applications.

Other component shields, encompassing transmission, differential, and auxiliary system applications, demonstrate resilience through diversified end-use exposure spanning both conventional and electric powertrains. The segment's stability stems from thermal management requirements that persist across propulsion technologies, particularly in commercial vehicle applications where duty cycles generate consistent heat loads regardless of powertrain configuration. Advanced materials adoption accelerates across all component types, with polyimide-aerogel composites offering thermal performance improvements while meeting weight reduction mandates under CAFE regulations.

By Material: Composites Gain Traction Despite Metallic Dominance

Metallic heat shields dominate with 72.14% market share in 2024, while non-metallic and composite heat shields accelerate at 14.53% CAGR through 2030 as lightweighting pressures intensify under CAFE compliance requirements. The material transition reflects performance advantages where advanced composites achieve equivalent thermal protection at 40 to 60% weight reduction compared to traditional steel and aluminum constructions. Insulation blankets and multi-layer solutions occupy a specialized niche serving high-temperature applications where rigid shields prove inadequate, particularly in turbocharger and exhaust manifold proximity installations.

Metallic heat shields maintain leadership through cost advantages and established manufacturing infrastructure, yet face margin pressure from commodity price volatility affecting steel and aluminum inputs. The segment's resilience stems from proven performance in traditional automotive applications and supplier familiarity with metallic fabrication processes, creating switching costs that slow composite adoption despite performance benefits. Regulatory compliance increasingly favors composite solutions where weight reduction directly contributes to CAFE credit generation, creating economic incentives that offset material cost premiums in premium vehicle segments.

By Product Structure: Sandwich Composites Emerge for Performance Applications

Single shell designs retain 51.07% market share in 2024, while sandwich composite structures demonstrate the fastest growth at 15.28% CAGR through 2030, targeting applications where thermal performance and weight reduction justify premium pricing. The structural evolution reflects engineering optimization where traditional single-layer shields prove inadequate for modern thermal management challenges, particularly in turbocharged engines and EV battery applications requiring enhanced thermal diffusivity control. Double shell configurations serve intermediate applications, balancing performance and cost considerations, maintaining steady demand in commercial vehicle segments where durability outweighs weight optimization priorities.

Manufacturing complexity increases with structural sophistication, creating supply chain advantages for established suppliers with composite processing capabilities while limiting market entry for traditional metallic shield manufacturers. The trend toward integrated thermal management systems drives demand for engineered structures combining thermal barriers, acoustic dampening, and mechanical protection in unified assemblies. Advanced manufacturing techniques, including automated fiber placement and resin transfer molding, enable cost-effective production of complex sandwich structures previously limited to aerospace applications.

By Form: Flexible Solutions Address Complex Geometries

Rigid shields lead with 64.22% market share in 2024, while flexible heat shields accelerate at 14.06% CAGR through 2030, addressing installation challenges in modern vehicle architectures where space constraints and complex geometries limit rigid shield applications. The form factor advantage becomes critical in EV battery pack applications where thermal barriers must conform to irregular cell configurations while maintaining thermal performance under mechanical stress. Flexible materials enable post-installation shaping and adjustment, reducing manufacturing complexity and inventory requirements compared to precision-formed rigid shields requiring exact dimensional specifications.

Material innovations drive flexible shield performance improvements, with advanced fiber constructions maintaining thermal properties while enabling conformability to complex surfaces. The segment benefits from simplified installation procedures, reducing assembly time and labor costs, creating total cost advantages that offset material premium pricing. Applications expand beyond traditional automotive uses into adjacent markets, including off-highway equipment and industrial machinery, where flexible thermal management solutions address unique packaging constraints.

By Vehicle Propulsion: EVs Transform Thermal Management Requirements

ICE vehicles dominate with 68.31% market share in 2024, while battery electric vehicles represent the fastest propulsion segment growth at 18.47% CAGR through 2030. The growth differential reflects fundamental thermal management requirement changes where EV applications demand specialized battery thermal runaway protection, power electronics cooling, and charging system thermal management rather than traditional exhaust and engine bay shielding. Hybrid electric vehicles occupy an intermediate position requiring dual thermal management systems serving both ICE and electric powertrains, creating complexity that drives premium pricing for integrated solutions.

EV thermal management applications demand materials certification under UL 2580 and ISO 26262 functional safety standards, creating technical barriers that favor suppliers with battery-specific expertise over traditional automotive heat shield manufacturers. The propulsion transition creates supply chain disruption where established exhaust shield suppliers face declining volumes while EV-focused thermal management specialists capture emerging applications. Regional variations in EV adoption rates compound market dynamics, with California and ZEV states driving accelerated demand for electric vehicle thermal solutions while traditional automotive regions maintain ICE-focused requirements.

By Vehicle Type: Off-Highway Segment Drives Specialized Applications

Passenger cars dominate with 46.18% market share in 2024, while off-highway and agricultural vehicles emerge as the fastest-growing vehicle segment at 9.24% CAGR through 2030. The segment's growth stems from increasing equipment sophistication and emission compliance requirements, extending automotive-grade thermal management solutions to construction, mining, and agricultural applications. Light commercial vehicles maintain steady demand through e-commerce delivery growth and last-mile logistics expansion, while medium and heavy commercial vehicles face mixed dynamics from freight demand growth offset by gradual electrification adoption.

Agricultural equipment electrification creates unique thermal management challenges where battery systems must operate in harsh environmental conditions while maintaining safety standards, driving demand for ruggedized thermal barrier solutions exceeding automotive specifications. The segment benefits from longer equipment lifecycles and aftermarket replacement demand, creating revenue stability compared to passenger vehicle applications subject to rapid technology transitions. Specialized applications command premium pricing due to limited competition and customized engineering requirements, supporting margin expansion for suppliers with off-highway expertise.

By Sales Channel: Aftermarket Resilience Amid OEM Transition

OEMs lead with 79.36% market share in 2024, while the aftermarket channel accelerates at 7.82% CAGR through 2030, demonstrating resilience as aging vehicle fleets require thermal management component replacement. Aftermarket demand benefits from extended vehicle lifecycles averaging 12.8 years in the United States, creating sustained replacement demand for heat shields subject to thermal degradation and mechanical wear. The channel's growth reflects increasing vehicle complexity, where thermal management failures require specialized replacement components rather than generic solutions, supporting premium pricing for OEM-equivalent aftermarket shields.

Distribution dynamics favor established suppliers with broad product portfolios serving multiple vehicle platforms, while specialized EV thermal management applications remain concentrated in OEM channels due to safety certification requirements and limited aftermarket demand. The U.S. automotive aftermarket projects 5.1% growth in 2025, reaching USD 664 billion by 2028, creating favorable market conditions for heat shield replacement demand across aging ICE vehicle populations. Regional variations in vehicle age and maintenance practices influence aftermarket penetration, with northern climates driving accelerated thermal component replacement due to harsh operating conditions.

Geography Analysis

The United States contributed USD 7.07 billion, or 58.27%, in 2024. Tightening CAFE requirements and SUV popularity maintain elevated shield content per vehicle. California’s zero-emission mandate accelerates battery-shield volumes, favoring suppliers with EV expertise. Regional production clusters in Michigan and the Southeast anchor tier-1 footprints, allowing just-in-time deliveries and mitigating logistics costs. Potential 50% steel and 25% parts tariffs would shift sourcing to domestic mills, boosting U.S. metallic shield cost structures but improving timeline reliability.

Canada delivered USD 1.25 billion in 2024 and is on track for 7.15% CAGR. Assembly plants in Ontario benefit from federal and provincial EV incentives, which stimulate battery enclosure projects. Cold-weather durability requirements spur demand for higher-spec thermal solutions, especially in light-duty trucks and off-road equipment. The EV push toward Quebec’s battery-materials corridor opens opportunities for local composite suppliers to integrate into North American value chains.

Rest of North America, primarily Mexico, supplied USD 3.82 billion in 2024. Nearshoring trends under USMCA encourage tier-1s to expand capacity near Monterrey and Saltillo for cost-competitive stamping and composite processing. Labor-cost advantages boost metallic shield exports to the United States, although advanced composite capability remains limited by skill availability and resin supply-chain maturity. Upgrades to rail and port infrastructure will dictate future capacity ramps.

Competitive Landscape

Market fragmentation is moderate, with the top five companies controlling about 55% of 2025 revenue. Dana, Tenneco, and Autoneum leverage global production footprints and cross-platform R&D to defend share. Materials-driven firms such as Morgan Advanced Materials and ElringKlinger cater to high-value composites for EV battery packs. ElringKlinger’s 2024 divestiture of two shielding plants to Certina Group reallocates capital toward cell contacting systems[2]"ElringKlinger hones its corporate profile and divests itself of two Group companies," ElringKlinger Newsroom, elringklinger.de.. Tenneco’s Low Emission Brake launch exemplifies portfolio pivoting to emissions-oriented thermal solutions. Autoneum’s Pure line upgrades align with OEM net-zero goals and secure premium SUV contracts.

Certification under IATF 16949:2016[3]"IATF Rules 6th Edition: Key Changes," SGS, sgs.com. remains a qualifying gate for OEM sourcing, and the stricter 6th-Edition rules effective 2025 will tighten vendor pools. Suppliers owning both metallic stamping and composite molding assets are best placed to fulfill dual propulsion needs. Emerging competitors may target niche EV segments, yet entry barriers include capital-intensive tooling and lengthy validation cycles.

North America Automotive Heat Shield Industry Leaders

-

Dana Incorporated

-

Tenneco Inc.

-

Autoneum Holding AG

-

ElringKlinger AG

-

Lydall Inc. (Unifrax)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Tenneco introduced Low Emission Brake technology for light and commercial vehicles, targeting Euro 7 brake particulate limits effective 2026 and anticipated China 7 standards. The technology utilizes natural materials and recycled content to reduce brake particulate emissions while achieving 15-35% manufacturing-related GHG reductions, with selection confirmed for upcoming European OEM passenger models and supply relationships established with major Chinese OEMs, including Chery-Huawei, GAC, Geely, and XPeng.

- December 2024: Autoneum optimized the environmental performance of its sustainable Pure technologies for the Renault Emblème vehicle as part of net-zero initiatives. The development focuses on reducing CO2 footprint across vehicle lifecycles through advanced acoustic and thermal management components, positioning Autoneum's Pure product line as a sustainable heat shielding solution for modern vehicle applications.

North America Automotive Heat Shield Market Report Scope

| Engine Compartment Shields |

| Exhaust System Shields |

| Turbocharger and Intake-Manifold Shields |

| Underbody and Floor-pan Shields |

| Battery and Power-Electronics Shields |

| Other Component Shields |

| Metallic Heat Shields |

| Non-metallic/Composite Heat Shields |

| Insulation Blankets/Multi-layer |

| Single Shell |

| Double Shell |

| Sandwich Composite |

| Rigid |

| Flexible |

| ICE Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Off-Highway and Agricultural Vehicles |

| OEMs |

| Aftermarket |

| United States |

| Canada |

| Rest of North America |

| By Component Type | Engine Compartment Shields |

| Exhaust System Shields | |

| Turbocharger and Intake-Manifold Shields | |

| Underbody and Floor-pan Shields | |

| Battery and Power-Electronics Shields | |

| Other Component Shields | |

| By Material | Metallic Heat Shields |

| Non-metallic/Composite Heat Shields | |

| Insulation Blankets/Multi-layer | |

| By Product Structure | Single Shell |

| Double Shell | |

| Sandwich Composite | |

| By Form | Rigid |

| Flexible | |

| By Vehicle Propulsion | ICE Vehicles |

| Hybrid Electric Vehicles | |

| Battery Electric Vehicles | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | |

| Off-Highway and Agricultural Vehicles | |

| By Sales Channel | OEMs |

| Aftermarket | |

| By Country | United States |

| Canada | |

| Rest of North America |

Key Questions Answered in the Report

What is the current value of the North America automotive heat shield market?

It reached USD 12.14 billion in 2025.

How fast will battery and power-electronics shields grow?

They are forecast to advance at 13.84% CAGR through 2030.

Which material segment is expanding the quickest?

Non-metallic composites lead with a 14.53% CAGR outlook.

Why is Canada the fastest-growing regional market?

Manufacturing expansion and cold-weather thermal requirements drive a 7.15% CAGR.

What impact do CAFE standards have on material choice?

They encourage lightweight composites that cut shield mass by 40-60%, supporting fuel-economy compliance.

How will the shift to EVs affect traditional exhaust shielding demand?

Exhaust shield volumes will decline as ICE share falls toward 45% by 2030, but battery shielding offsets some of the loss.

Page last updated on: