Automotive Heat Shield Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

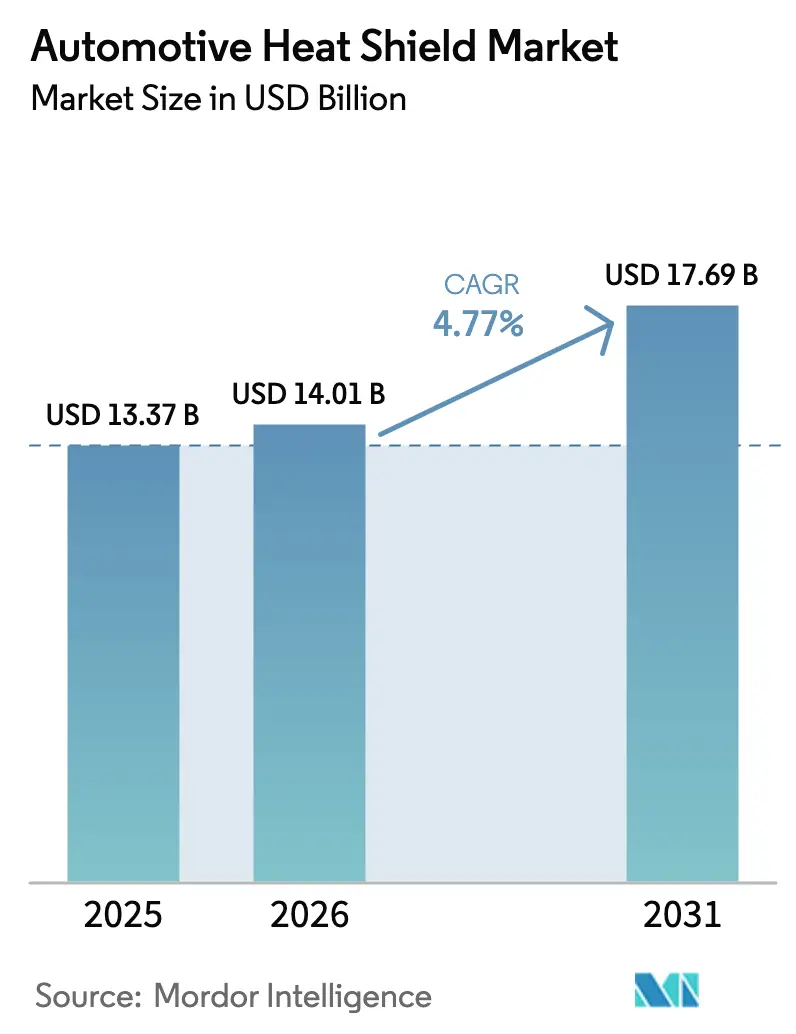

| Market Size (2026) | USD 14.01 Billion |

| Market Size (2031) | USD 17.69 Billion |

| Growth Rate (2026 - 2031) | 4.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

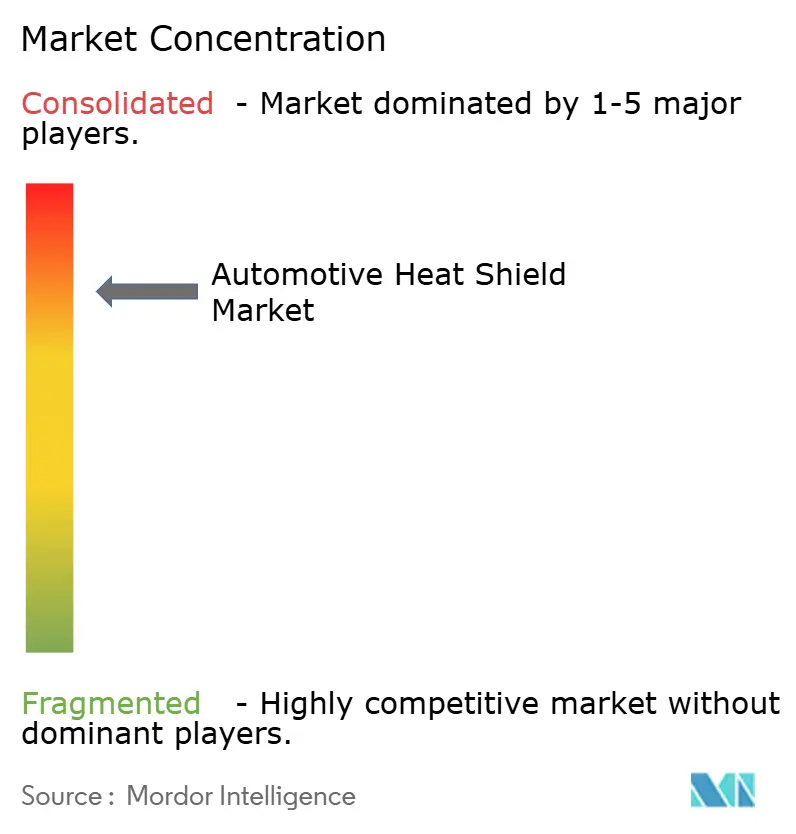

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Heat Shield Market Analysis by Mordor Intelligence

The Automotive Heat Shield Market size was valued at USD 13.37 billion in 2025 and estimated to grow from USD 14.01 billion in 2026 to reach USD 17.69 billion by 2031, at a CAGR of 4.77% during the forecast period (2026-2031). Stricter emissions regulations and a swift pivot to electric powertrains are shaping the industry's trajectory. Across all vehicle classes, automakers prioritize thermal protection, driven by battery safety mandates, lightweighting goals, and innovative materials. They're adopting composite materials and smart sensors to reduce weight, maintain catalytic converter efficiency, and protect lithium-ion batteries during quick charges. Concurrently, larger tier-one suppliers leverage scale benefits, diversify their material portfolios, and employ hedging strategies.

Key Report Takeaways

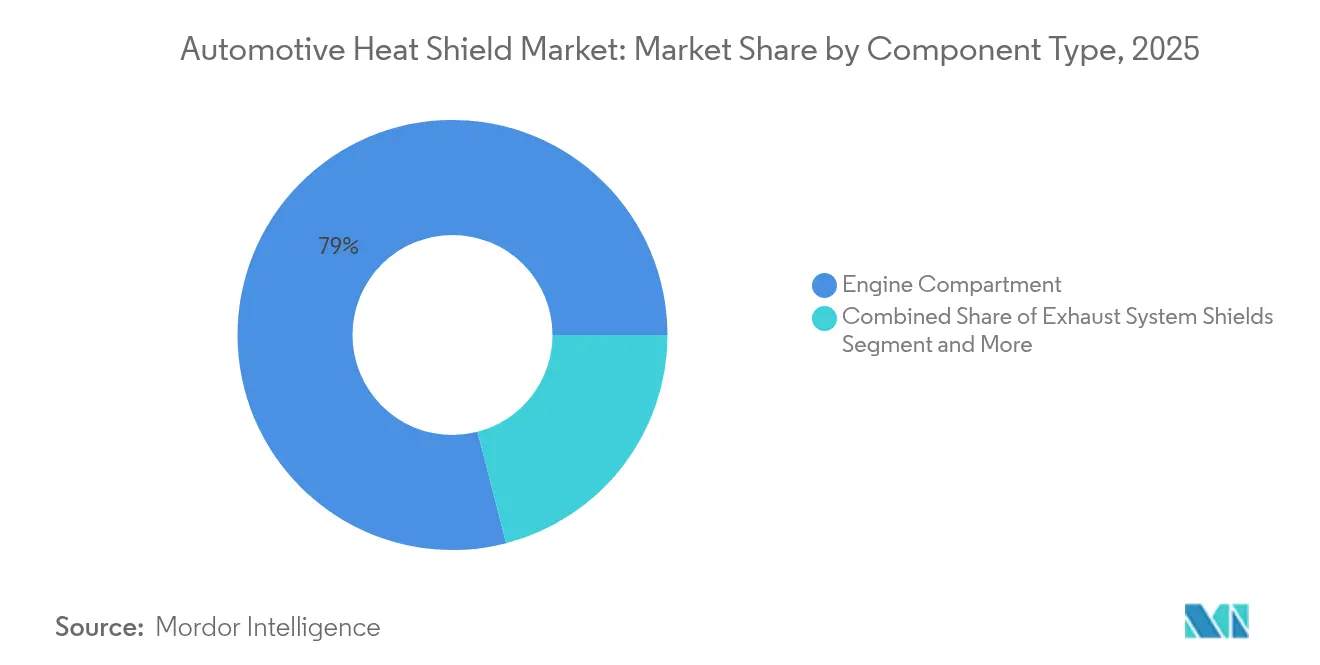

- By component type, Engine Compartment Shields held 79.02% of the automotive heat shield market share in 2025, while Battery & Power-Electronics Shields are projected to expand at a 11.62% CAGR through 2031.

- By sales channel, OEM deliveries commanded an 84.05% share of the automotive heat shield market in 2025, whereas the aftermarket is advancing at an 7.72% CAGR through 2031.

- By vehicle type, passenger cars accounted for 62.58% of the automotive heat shield market size in 2025, and light commercial vehicles posted the fastest growth with 13.86% CAGR during the 2026-2031 period.

- By material, Metallic Heat Shields accounted for 86.45% of the automotive heat-shield market in 2025, while Non-metallic/Composite Heat Shields are projected to grow the fastest, at an 8.18% CAGR through 2031.

- By product structure, Single-Shell designs dominated with a 55.52% share in 2025, whereas Sandwich-Composite shields are expected to register the quickest expansion, rising at a 6.98% CAGR to 2031.

- By form, Rigid heat shields captured roughly 68.84% of 2025 revenues, while Flexible formats are forecast to outpace them, advancing at a 6.08% CAGR over the same period.

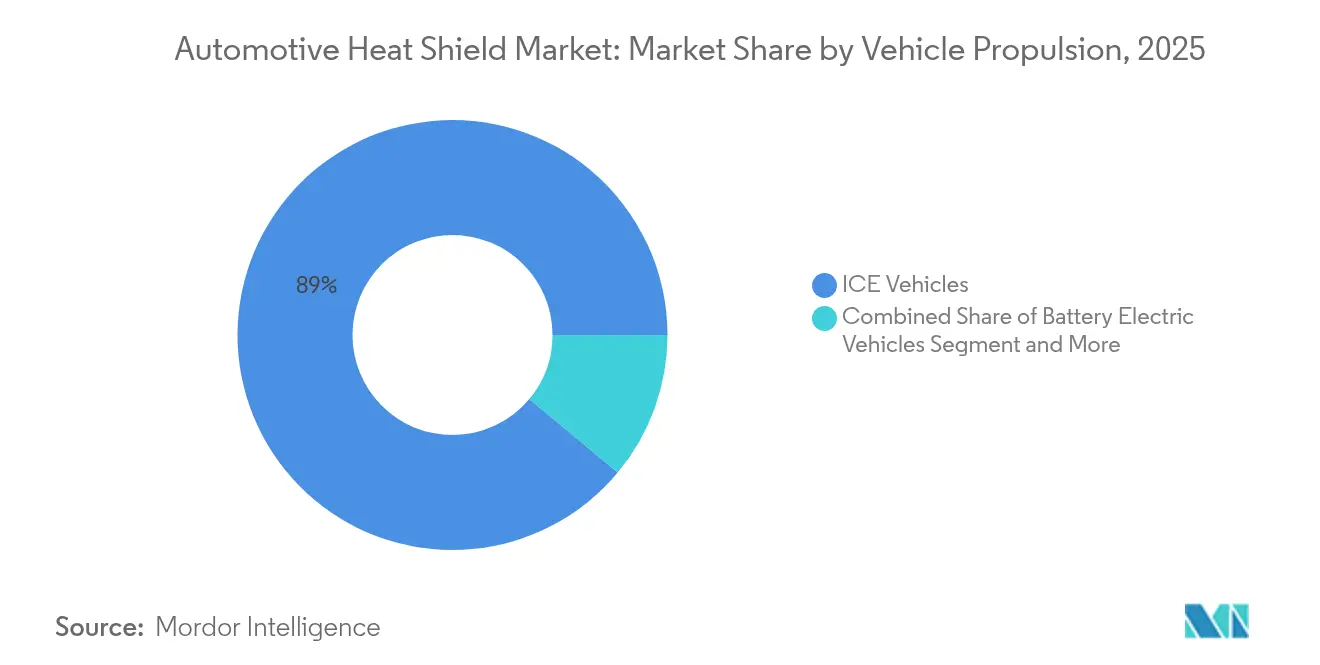

- By vehicle propulsion, ICE-powered vehicles still led with about 88.95% of heat-shield demand in 2025, but Battery-Electric-Vehicle applications are set to surge ahead with a 13.72% CAGR through 2031.

- By region, Asia-Pacific captured 46.48% revenue share of the automotive heat shield market in 2025; the same region is projected to grow at a 9.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Heat Shield Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Emission & Fuel Economy Rules | +1.2% | North America & Europe, with spillover to China & India | Medium term (2-4 years) |

| Hybrid / EV Thermal Demand Surge | +1.8% | Global, with concentration in Europe & China | Long term (≥ 4 years) |

| Lightweight Aluminum & Composites Adoption | +0.9% | Global, led by North America & Europe | Medium term (2-4 years) |

| Rising APAC Vehicle Output | +1.4% | China, India, Japan, South Korea | Short term (≤ 2 years) |

| Active / Smart Heat Shields Emergence | +0.7% | North America, Europe, Japan | Long term (≥ 4 years) |

| ELV Aluminum Upcycling for Low-Carbon Shields | +0.5% | Europe, North America, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Emission & Fuel-Economy Regulations

Current EPA rules push CO₂ limits for new passenger models toward 85 g / mile by 2032, compelling automakers to operate engines hotter and keep catalytic converters at optimal light-off temperatures. Multi-layer metallic shields that capture radiant exhaust heat are pivotal to meeting emissions and corporate average fuel-economy targets. Higher-margin premium shields are seeing the fastest uptake in California, Western Europe, and Japan, whereas cost-driven variants dominate emerging markets with looser rules but converging deadlines.

Surge in Hybrid & EV Battery-Thermal-Management Demand

Lithium-ion packs run safest between 20-40 °C, and containment structures must withstand events exceeding 1,000 °C. New ceramic-fiber and intumescent layers inside battery enclosures limit propagation during thermal runaway, while embedded cooling channels and phase-change inserts handle rapid-charge spikes. Automakers treating thermal shields as safety-critical hardware drive double-digit growth, especially in China and Germany, where electric models launch at the unprecedented cadence.

Lightweight Aluminum & Composite Material Adoption

High-Mg aluminum forgings and sandwich composites trim 40-60% mass versus steel while reflecting more infrared energy. Gigacasting now compresses sizable underbody panels—including exhaust tunnel shields—into single shots, saving welding steps and improving heat dissipation. Aerogel-loaded laminates cut thermal transfer by another 35% and allow thinner profiles, opening cramped EV skateboard layouts for larger cell modules.

Rising Vehicle Production in APAC

Asia-Pacific output eclipses global peers, raising near-term demand for cost-effective yet regulatory-ready thermal shields. Chinese EV lines specify ceramic-fiber battery wraps at scale, Japanese hybrids adopt ultra-thin multi-layer engine shields for NVH and weight perks, and Indian plants request simplified punched-aluminum formats that meet value thresholds while preserving 500,000-km durability targets.[1]“Integrated Report 2024,” Nippon Steel Corporation, nipponsteel.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility (Al, SS) | -0.8% | Global, with higher impact in import-dependent regions | Short term (≤ 2 years) |

| Durability Issues With Non-Metallic Shields | -0.6% | Global, with concentration in regions with extreme climates | Medium term (2-4 years) |

| Compliance Costs From Cartel Probes | -0.4% | Europe, North America, Japan | Medium term (2-4 years) |

| Diesel Vehicle Phase-Down in Europe | -0.7% | Europe, with spillover effects in global export markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility (Al, SS)

Aluminum prices spiked 15% in early 2025 following bauxite disruptions in Australia and power outages in Yunnan, squeezing margins for stamped-sheet suppliers whose bill-of-materials can exceed 70% metal content. Tier-ones hedge on futures exchanges, but many tier-threes lack credit lines, prompting accelerated R&D into polymer or ceramic alternatives with steadier cost curves.

Durability Challenges of Non-Metallic Shields

Certain polymer composites lose up to 40% tensile strength after 5,000 h at 200 °C, prompting warranty fears for turbocharger or under-floor locations. Freeze-thaw cycling in Canada, Scandinavia, and the Himalayas induces micro-cracks that can propagate during vibration, steering OEMs toward hybrid metal–ceramic sandwiches or reinforcing scrim fabrics until higher-temperature resins mature.[2]“Sustainability Roadmap 2050,” Morgan Advanced Materials, morganadvancedmaterials.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Battery Shields Disrupt Traditional Hierarchy

Engine Compartment Shields controlled 79.02% of the automotive heat shield market in 2025, reflecting the longstanding need to protect wiring, plastic reservoirs, and passenger footwells from engine block and exhaust manifold radiation. Evolving turbo and downsized cylinder heads run hotter, so multilayer aluminum-with-glass-mat designs stay central. Battery & Power-Electronics Shields, though smaller in revenue, are advancing at 11.62% CAGR as every additional kilowatt-hour of energy density raises containment stakes. Flexible ceramic papers and intumescent foams line battery frames, while copper-mesh spreaders move hotspots away from cells during DC-fast-charge phases.

Exhaust System Shields remain the second-largest sub-segment at 15.34%, driven by Euro 7 and EPA after-treatment temperature windows. These assemblies often carry double-shell construction and dimpled patterns to hold boundary-layer air and slash surface temps by 40 °C. Turbocharger & Intake-Manifold Shields follow, registering 9.29% CAGR thanks to global turbo-gasoline adoption. Underbody & Floor-pan Shields couple thermal and acoustic layers to cut drivetrain hum by up to 3 dB and resist stone impacts in off-road SUVs.

By Material: Composites Challenge Metallic Dominance

Metallic solutions, hold 86.45% of the market share in 2025—chiefly three xxx aluminum sheet and 409 stainless—still comprise the bulk of automotive heat shield market shipments because of well-known forming, joining, and recycling streams. Variable-thickness hydroforming and laser-perforation now shave weight while venting trapped exhaust heat.

Non-metallic and composite alternatives are seizing share, leveraging 40-60% mass savings and 35% insulation drops. Aerogel-filled blankets push conductivity down to 0.015 W/mK, allowing 2 mm sandwiches that rival 6 mm aluminum shells. Aspen Aerogels’ PyroThin® panels surround EV cell groups, confining runaway events to single modules and giving pack designers valuable cooling headroom.

By Product Structure: Sandwich Designs Gain Traction

Single-shell stampings hold 55.52% of the market share in 2025, remaining popular for splash zones and moderate-heat brackets because their one-piece geometry limits tooling outlay. Yet rising under-bonnet peak temperatures expose their 200 °C ceiling. Double-shell forms insert an air gap that blocks up to 40% radiative flux, meeting stricter cabin soak targets without redesigning firewall geometry.

The fastest growth lies in sandwich composites that pair an aluminum skin with a microporous ceramic center. Morgan Advanced Materials now supplies multi-layer mats that trim 70% of the weight compared with earlier steel pans while holding exhaust-gas ducts at or below 450 °C during hill-climb duty cycles.

By Form: Flexible Solutions Address Complex Geometries

Rigid shields command a dominant 68.84% share of the automotive heat shield market in 2025, primarily catering to big-volume orders. Automated presses are busy producing uniform parts for ICE manifolds and under-floor tunnels. With continuous 600-ton transfers, manufacturers maintain a cost parity, keeping expenses below USD 3 per part for mid-size sedans.

However, the market is shifting towards flexible foils and quilted mats as EVs integrate power-electronics bays with tightly packed wiring, coolant lines, and charge ports. Projections indicate a burgeoning flexible sub-category, expected to reach USD 5.85 billion by 2031, with an annual growth rate of 6.08%. Notably, when bonded to aluminum foil, aramid-glass cloths offer a unique advantage: they can be hand-fitted post-assembled, effectively sealing gaps around high-voltage junction boxes and significantly reducing rework time.

By Vehicle Propulsion: Electrification Drives Specialized Solutions

ICE models dominate the market, commanding an 88.95% share in 2025. These models require shields to maintain catalytic substrates above 400 °C for effective emissions conversion and prevent scorch damage during high-grade ascents. Meanwhile, hybrid electric vehicles are incorporating secondary insulation to shield traction batteries from surges in the engine bay. This move broadens the thermal zone, now encompassing inverters and DC-DC converters.

The automotive heat shield market is witnessing the fastest growth in the battery electric segment, projected at a 13.72% CAGR through 2031. This surge is driven by OEMs adopting double-wall steel tubs filled with ceramic blankets, engineered to endure thermal events of up to 1,100 °C, in line with UN ECE R100 fire testing standards.

By Vehicle Type: Passenger Cars Lead, Commercial Fleets Follow

Passenger cars generated 62.58% of revenue in 2025, with mid-range sedans and crossovers adopting composite encapsulation around turbo scrolls to meet idle-stop restart timing. Light commercial vans saw a 24.18% share, prioritizing durability for multi-shift logistics routes; perforated steel tunnels paired with fiberglass-needled liners extend life to 300,000 km.

Heavy commercial rigs leverage thicker 409 SS sheet and ceramic wrap-around diesel particulate filters for uptime demands topping 1 million km. Off-highway tractors integrate reinforced basalt cloth shields that resist mud impact and wash-down chemicals.

By Sales Channel: OEMs Dominate, Aftermarket Accelerates

OEM contracts represented 84.05% of the automotive heat shield market revenue in 2025, thanks to early-phase design integration and validation requirements that lock suppliers into multi-year platforms. Platform lifecycles now include EV skateboard architectures, demanding requalification of shield performance under new thermal maps.

The aftermarket grows 7.72% annually as owners retrofit aluminized glass cloth to vintage turbo projects or replace corroded OE parts in high-salt regions. Specialty tuners offer polished stainless wraps that double as aesthetic upgrades while cutting under-hood intake temps by 8°C.

Geography Analysis

Asia-Pacific retained a 46.48% share of the automotive heat shield market in 2025 and is expanding at a 9.21% CAGR. Chinese EV assembly hubs in Guangdong and Jiangsu specify ceramic-fiber battery isolators, while Japanese OEMs ship multi-layer acoustic-thermal hybrids that lower drivetrain noise and cabin soak simultaneously. India’s localized suppliers produce cost-optimized punched-aluminum forms, meeting small-car price targets while ensuring 500,000-km durability in monsoon climates. South Korean firms specialize in high-density battery pack cooling shields for export SUVs, leveraging domestic cell technology leadership.

Europe followed at 27.34% share, where Euro 7 exhaust rules and stringent OEM lightweighting quotas spur demand for composite and recycled-aluminum designs. German luxury brands pay premiums for ultra-thin titanium-aluminide heat blankets that safeguard turbo housings. French mid-segment programs experiment with end-of-life aluminum feedstock that cuts embedded CO₂ by up to 95%. British low-volume performance builders choose 3D-printed Inconel shields for complex turbine scrolls, illustrating the region’s appetite for additive manufacturing.

North America contributed 18.09% of 2025 revenue. United States pickup and SUV lines consume traditional stamped aluminum shields in large lots, yet Tesla, GM, and Ford EV platforms drive rapid growth in battery-compartment protection. Canada’s freeze-thaw climate elevates durability testing thresholds, pushing composite suppliers toward hybrid metal-ceramic architectures. Mexico’s maturing supplier base now molds aerogel-filled flexible wraps for export to Michigan and Ontario assembly plants, diversifying the regional sourcing map.

Mordor Intelligence provides coverage of the automotive heat shield market across other key regional markets, including North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The top five suppliers—Autoneum, Dana, ElringKlinger, Tenneco, and Sumitomo Riko—collectively owned majority of 2024 global shipments, reflecting moderate consolidation. Larger tier-ones leverage multi-regional plants and hedged aluminum contracts to buffer commodity swings, while specialist newcomers tackle high-growth EV niches with aerogel or intumescent chemistries. Aspen Aerogels licenses its PyroThin® technology to multiple module integrators, creating cross-brand safety commonalities. Dana’s 2025 acquisition of a composite molding line in Slovakia underscores a strategy to blend metallic and polymer expertise.

Price pressure weighs on legacy metallic parts as stamping know-how commoditizes, whereas EV-specific shields maintain higher gross margins through patent-protected chemistries. Additive manufacturing firms such as EOS help premium OEMs print lattice-cooling structures in thin-wall Inconel, cutting mass and easing under-bonnet airflows. Strategic white-space resides in integrated thermal-acoustic panels that consolidate NVH foam, heat reflection, and water-ingress barriers in one install step, especially appealing to skateboard-style EV frames.

Smaller suppliers without global hedging capacity face raw-material cost exposure, driving merger talks and joint ventures. Tier-twos that master hybrid aluminum-composite layups win share when OEMs demand combined lightweighting and high-temperature tolerance, notably in Asia, where production volumes reward fast tooling cycles. Market entry barriers revolve around material IP, capital-intensive forming presses, and validation protocols that stretch from -40 °C Arctic tests to 1,200 °C thermal runaway firewalls.

Automotive Heat Shield Industry Leaders

ElringKlinger AG

Dana Incorporated

Autoneum Holding AG

Tenneco Inc. (Federal-Mogul)

Sumitomo Riko Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Brookfield acquired Chemelex, a leader in electric heat-trace systems, expanding its capabilities in temperature regulation technologies applicable to automotive thermal management.

- November 2024: Autoneum inaugurated a new Research & Technology (R&T) Center in Shanghai, China, targeting New Mobility and bolstering its foothold in the region. This center is set to aid in the development and production of components and materials tailored for e-mobility.

- September 2024: Zircotec unveiled new high-performance coatings for electric vehicle battery enclosures and cooling plates.

Global Automotive Heat Shield Market Report Scope

The Automotive Heat Shield Market report covers the latest trends and developments. The Automotive Heat Shield Market is segmented by Component Type, Vehicle Type, and Geography. The report also covers the market share of major players in volume USD billions.

Based on Component Type, the market is segmented as Engine Compartment, Exhaust Compartment, and Other Types. By Vehicle Type, the market is segmented as Passenger Cars and Commercial Vehicles. By Sales Channel, the market is segmented as OEMs and Aftermarket, and based on Geography, the market is observed as North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

| Engine Compartment Shields |

| Exhaust System Shields |

| Turbocharger & Intake-Manifold Shields |

| Underbody & Floor-pan Shields |

| Battery & Power-Electronics Shields |

| Other Component Shields |

| Metallic Heat Shields |

| Non-metallic / Composite Heat Shields |

| Insulation Blankets / Multi-layer |

| Single Shell |

| Double Shell |

| Sandwich Composite |

| Rigid |

| Flexible |

| ICE Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Off-Highway & Agricultural Vehicles |

| OEMs |

| Aftermarket |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| APAC | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of APAC | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Component Type | Engine Compartment Shields | |

| Exhaust System Shields | ||

| Turbocharger & Intake-Manifold Shields | ||

| Underbody & Floor-pan Shields | ||

| Battery & Power-Electronics Shields | ||

| Other Component Shields | ||

| By Material | Metallic Heat Shields | |

| Non-metallic / Composite Heat Shields | ||

| Insulation Blankets / Multi-layer | ||

| By Product Structure | Single Shell | |

| Double Shell | ||

| Sandwich Composite | ||

| By Form | Rigid | |

| Flexible | ||

| By Vehicle Propulsion | ICE Vehicles | |

| Hybrid Electric Vehicles | ||

| Battery Electric Vehicles | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Heavy Commercial Vehicles | ||

| Off-Highway & Agricultural Vehicles | ||

| By Sales Channel | OEMs | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| APAC | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of APAC | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the automotive heat shield market?

The automotive heat shield market size is USD 14.01 billion in 2026, projected to reach nearly USD 17.69 billion by 2031.

Which component segment holds the largest share?

Engine Compartment Shields lead with 79.02% of global revenue in 2025 due to their long-standing role in managing under-bonnet heat.

Why are battery-specific heat shields growing so quickly?

Battery and power-electronics Shields are advancing at an 11.62% CAGR because electric vehicle packs require sophisticated thermal barriers that prevent thermal runaway and maintain optimal operating temperatures.

Which region contributes the most to demand?

Asia-Pacific commands 46.48% of global sales thanks to high vehicle production in China, India, Japan, and South Korea, and it is also the fastest-growing region at 9.21% CAGR.

How are raw-material price swings affecting suppliers?

Volatile aluminum and stainless prices compress supplier margins by up to 0.8 points of CAGR, forcing larger players to hedge and prompting smaller firms to explore polymer or ceramic substitutes.

What innovative materials are shaping future heat shields?

Aerogel-filled composites, intumescent foams, and multi-layer aluminum-ceramic sandwiches enable thinner, lighter shields that withstand temperatures above 1,000 °C while meeting automaker lightweighting targets.

Page last updated on: