Automotive Sun Visor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

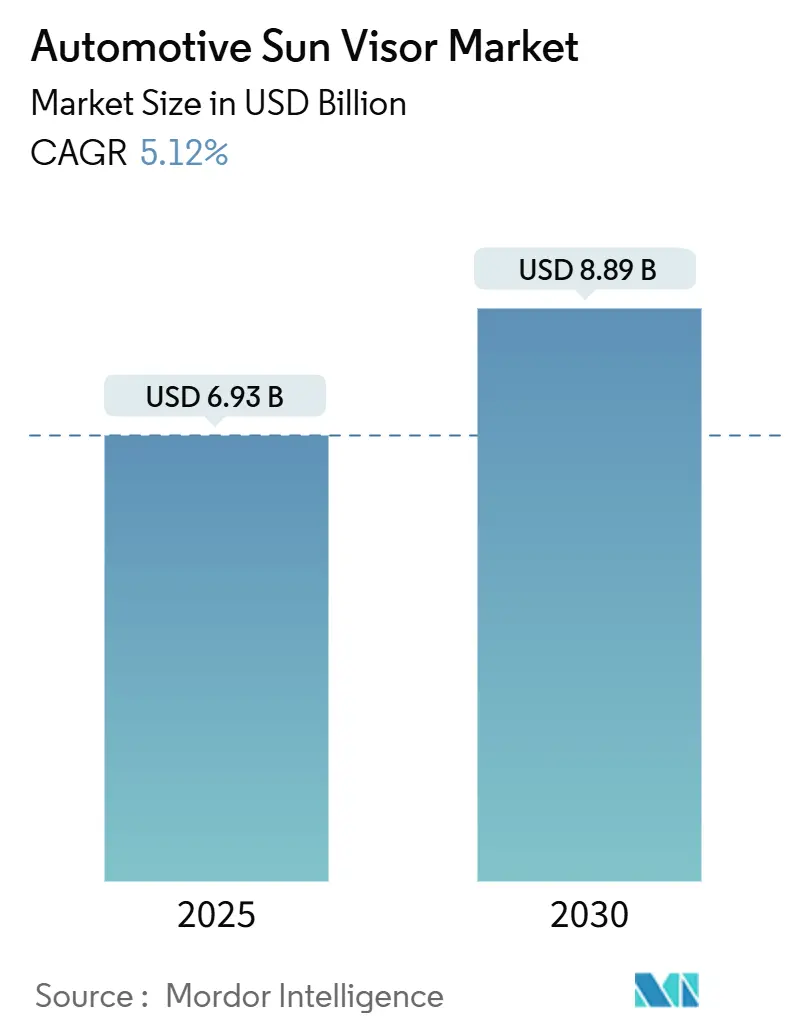

| Market Size (2025) | USD 6.93 Billion |

| Market Size (2030) | USD 8.89 Billion |

| Growth Rate (2025 - 2030) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Sun Visor Market Analysis by Mordor Intelligence

The Automotive Sun Visor Market size is estimated at USD 6.93 billion in 2025, and is expected to reach USD 8.89 billion by 2030, at a CAGR of 5.12% during the forecast period (2025-2030). Passenger vehicle premiumization, rising smart cockpit penetration, and regulatory pressure for sustainable interiors collectively raise procurement volumes and average selling prices. LCD visor programs move from pilot scale in luxury trims toward broader mid-segment adoption, encouraging tier-1 suppliers to invest in dedicated electronic assembly lines. Supply-chain consolidation intensifies bargaining leverage for large global vendors that can guarantee long-term material compliance under evolving PFAS and VOC rules. Aftermarket demand expands as ride-hailing operators replace high-wear interior parts more frequently than private owners, stimulating growth beyond the OEM channel.

Key Report Takeaways

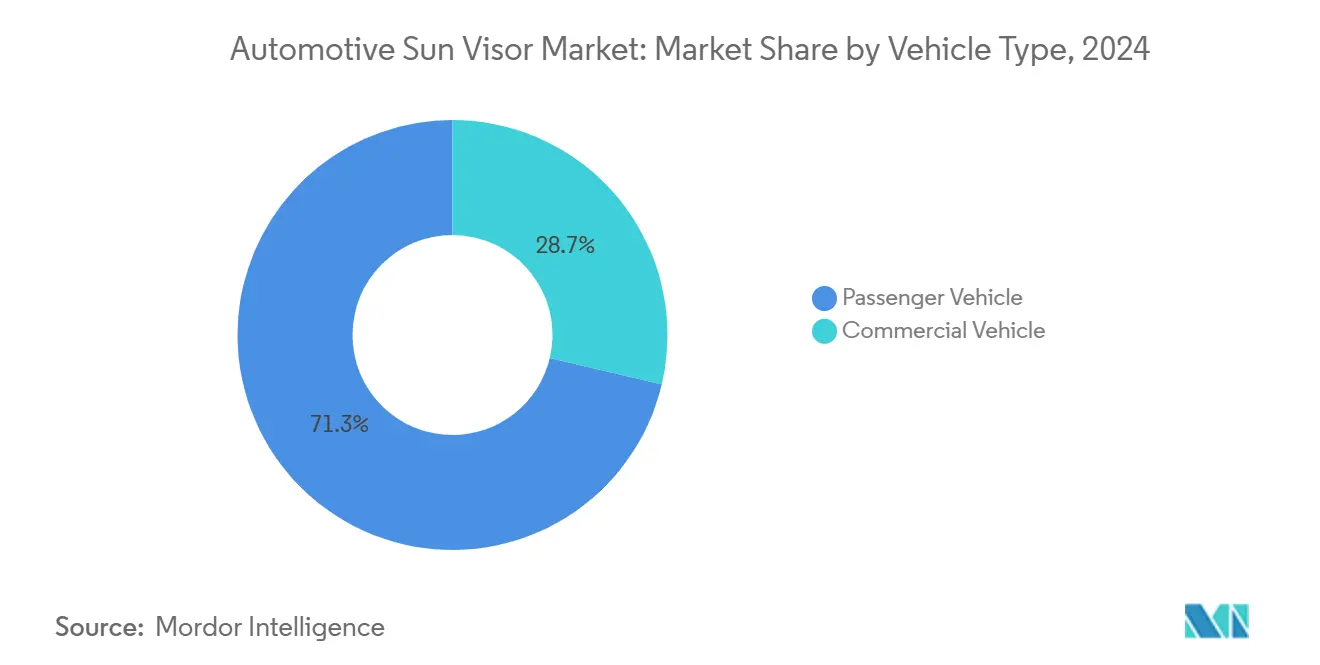

- By vehicle type, passenger vehicles held 71.29% of the automotive sunvisor market share in 2024, and the segment also posted a 5.16% CAGR outlook to 2030.

- By material, vinyl commanded a 47.63% of the automotive sunvisor market share in 2024, whereas fabric alternatives are forecast to advance at a 5.18% CAGR between 2025 and 2030.

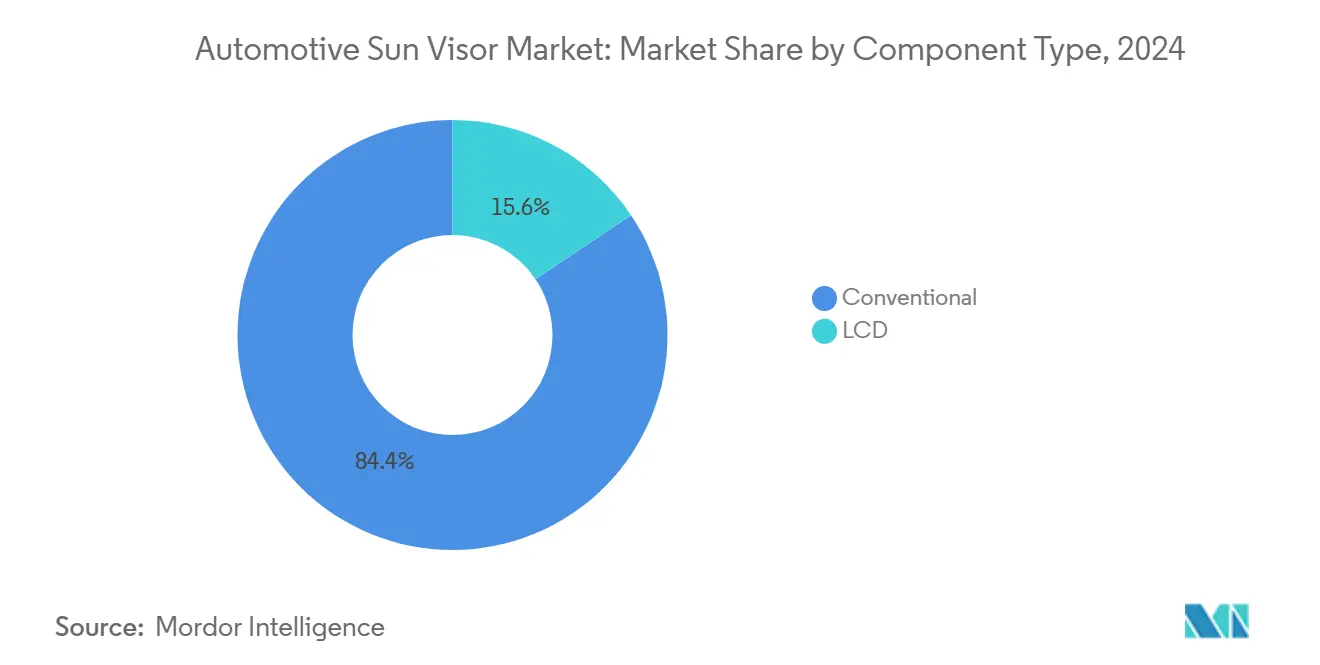

- By component, conventional visors contributed 84.41% of the automotive sunvisor market share in 2024; LCD-integrated systems are the fastest-growing segment, with a 5.22% CAGR through 2030.

- By sales channel, OEM deliveries accounted for 87.73% of the automotive sunvisor market share in 2024, and the aftermarket is primed for a 5.15% CAGR from 2025 to 2030.

- By region, Asia-Pacific led with 37.91% of the automotive sunvisor market share in 2024 and is projected to expand at 5.19% CAGR to 2030.

Global Automotive Sun Visor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Demand | +1.2% | North America and EU premium segments, expanding to Asia Pacific | Medium term (2-4 years) |

| LCD / Smart-Visor Integration | +1.1% | North America and EU early adoption, Asia Pacific following | Long term (≥ 4 years) |

| OEM Adoption Of Illuminated | +0.9% | Global, concentrated in premium vehicle lines | Medium term (2-4 years) |

| Rising Global Vehicle-Production Rebound | +0.8% | Global, with Asia Pacific leading recovery | Short term (≤ 2 years) |

| Shift To Lightweight, Sustainable Visor Materials | +0.7% | EU regulatory-driven, expanding globally | Long term (≥ 4 years) |

| After-Sales Demand From Ride-Hailing Fleets | +0.5% | Urban centers globally, concentrated in Asia Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand for Premium Interiors

U.S. and European shoppers increasingly select trims that bundle illuminated visors, ambient LEDs, and stitched soft-touch materials, prompting mid-segment brands to replicate luxury cues [1]“Car Interior Materials Explained,” J.D. Power, jdpower.com. Interior differentiation now outweighs powertrain attributes in several buyer-perception studies, which forces OEMs to allocate more of their budget to cabin components. Suppliers respond with modular visor platforms that accept add-on lighting, mirrors, and electronics to span multiple price points. This modularity reduces tooling amortization and quickens launch cycles. As premium features migrate downward, visor electronic control modules standardize, reducing per-unit cost and boosting penetration.

LCD / Smart-Visor Integration for Driver-Assist

Mercedes-Benz piloted a transparent LCD sun visor that darkens only where sunlight strikes the driver’s eyes, projecting navigation cues when glare subsides [2]“Transparent LCD Sun Visor,” Daimler AG, daimler.com. The technology exploits ambient-light sensors and head-tracking cameras already present for ADAS, minimizing incremental bill-of-materials. Early deployments appear in luxury sedans, yet volume expansion is forecast for premium crossovers by 2027 as panel costs decline roughly one-tenth annually. European regulatory bodies allow dynamic opacity glass under UNECE R46 amendments, clearing a legal path for broader market rollout. Suppliers with interior and ADAS portfolios gain an advantage in system integration contracts.

OEM Adoption of Illuminated & Extendable Visors

Brands such as BMW and Lexus install extendable visor rails and color-matched LED vanity mirrors, turning a once-basic glare shield into a focal design element. The integration aligns with broader ambient-lighting packages that reach A-pillars and headliners. Engineering teams require visor electronics to handshake with body-control modules, creating cross-functional sourcing decisions that favor full-service interior suppliers. Cost per unit has fallen slightly since 2023 as shared harness architectures proliferate. Customer satisfaction surveys cite improved glare coverage in SUVs with large panoramic roofs, reinforcing OEM commitments to the feature.

Rising Global Vehicle-Production Rebound

Global assembly volumes recovered from pandemic lows in 2024, with China posting minimum year-over-year growth while North American and European plants normalized semiconductor supply. Higher build schedules translate to firm visor order books and improved supplier capacity-planning visibility. OEMs temporarily prioritize supply security over cost, rewarding long-standing tier-1 partners that can scale quickly. Asia-Pacific plants contribute the bulk of incremental units, though premium North American platforms lift visor value per vehicle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Price Volatility | -0.6% | Global, with particular impact on cost-sensitive segments | Short term (≤ 2 years) |

| Tier-1 Supply Consolidation | -0.5% | Global, with concentrated impact in mature automotive markets | Long term (≥ 4 years) |

| Low Replacement Cycle | -0.4% | North America and EU mature markets | Long term (≥ 4 years) |

| Glare-Safety Regulations | -0.4% | North America and EU regulatory markets, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Raw-Material Price Volatility

Spot vinyl quotes rose, propelled by refinery outages and freight surcharges. Fabric mills in Southeast Asia faced cotton-poly blend shortages after weather-related crop damage, hiking textile costs. Smaller visor manufacturers lack hedging tools, forcing quarterly price renegotiations with OEMs that prefer annual contracts. Margin swings threaten R&D budgets, slowing the transition to smart visors among capital-constrained players. To counter, Magna and Grupo Antolin signed multi-year resin supply deals indexed to Brent crude, dampening volatility through 2026.

Low Replacement Cycle in Mature Car-PARC

Average vehicle age in the United States reached 12.8 years in 2024, yet visor components often remain functional for the car's life, limiting aftermarket volume. Owners of decade-old sedans prioritize drivetrain and safety repairs over cosmetic upgrades, keeping visor replacement rates below 1% annually. Suppliers experiment with retrofit kits that add LEDs or antimicrobial fabric to aging visors, but adoption remains niche. Long product lifespans also weigh on revenue forecasts in Europe, where scrappage rates slowed amid economic uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Passenger Dominance Drives Premium Integration

Passenger vehicles represented 71.29% of the automotive sunvisor market share in 2024 and are forecast to retain leadership through 2030, growing at a robust CAGR of 5.16%. Demand stems from growing middle-class expectations for enriched cabin features and OEM efforts to defend pricing power with technology-laden interiors. LCD prototypes debut first in luxury sedans but cascade to compact SUVs as panel costs decline, elevating visor value per unit.

Commercial vehicles continue to prioritize durability and cost control, selecting fabric-wrapped polypropylene cores over heavier vinyl to handle higher daily mileages. Fleet operators have been slow to adopt illuminated mirrors because downtime for electrical retrofits outweighs the perceived benefit. Nonetheless, ride-hailing companies are carving out a lucrative retrofit niche that could partially offset this conservatism. Suppliers market modular assemblies that swap into existing clips without rewiring, a tactic that may raise penetration in vans and urban logistics vehicles by the decade’s end.

By Material Type: Vinyl Leadership Faces Sustainable Pressure

Vinyl accounted for 47.63% of the automotive sunvisor market 2024 due to its abrasion resistance and low cost. EU PFAS removal targets tighten from 2026 onward, creating risk for traditional vinyl chemistries and accelerating bio-based PVC programs. Fabric alternatives log the fastest CAGR at 5.18% because they align with OEM carbon-neutral pledges and boast premium tactile qualities valued by high-income buyers.

Recycled PET textiles adopt antimicrobial coatings that maintain colorfastness despite intense UV exposure at the windshield level. Bio-PVC blends shave one-tenth from part weight, contributing directly to OEM emissions credits under EU Regulation 2019/631. In North America, the regulatory push is softer, yet brand marketing around eco interiors nudges Ford and GM to pilot soy-based vinyl. Material innovation and lifecycle assessment certification become key award criteria in RFQs issued after 2025.

By Component Type: LCD Innovation Disrupts Conventional Dominance

Conventional visor assemblies still captured 84.41% of the Automotive Sunvisor market share in 2024, but LCD smart visors post a robust 5.22% CAGR to 2030. Early adopters Tesla and Mercedes integrate dynamic-darkening panels that selectively block sunlight without hiding traffic signals. Their success sets performance benchmarks that mainstream brands plan to meet before 2028.

LCD modules require tight thermal management near the roof header, so suppliers collaborate with HVAC teams to prevent overheating. The complexity strengthens the moat around incumbents supplying head-up displays and cluster screens. Capital expenditure for clean-room coating lines is high, deterring new entrants. Over time, cost-down curves may mirror infotainment screens, positioning LCD visors as a new revenue pillar once hardware standardization matures.

By Sales Channel: OEM Dominance Reflects Integration Complexity

OEM purchasing comprised 87.73% of the Automotive Sunvisor Market's revenue in 2024 because visors are fitted during cabin trim build-up and must align with wiring and safety protocols. Tier-1 suppliers integrate visor software into body-control modules at the factory, an effort infeasible for mass aftermarket installers today.

The aftermarket remains promising, advancing at a 5.15% CAGR as gig-economy fleets target quick upgrades that refresh cabin appeal between high-mileage service intervals. E-commerce channels gain traction, with Amazon Business listing universal visor kits that require only a screwdriver for replacement. Warranty regulations in the EU recently clarified that non-safety interior parts do not void OEM coverage, further lowering adoption barriers for DIY enthusiasts.

Geography Analysis

Asia-Pacific led the Automotive Sun Visor Market with a 37.91% revenue share in 2024, riding on a swift rebound of Chinese production and expanding Indian assembly capacity [3]“Production and Sales Report,” China Association of Automobile Manufacturers, caam.org.cn. The region posts a 5.19% CAGR to 2030 as Japanese and Korean OEMs localize sourcing to mitigate freight volatility. Joint-venture plants in Vietnam and Indonesia bring new demand, and suppliers set up satellite molding centers to shorten lead times. Government incentives under China’s “Made in China 2025” and India’s PLI Automotive scheme strengthen localization economics.

Despite lower unit volumes, North America remains the largest profit pool because premium SUV mixes elevate visor ASPs. New United States tariffs of up to one-fourth on selected Chinese components, announced in 2024, spur near-shoring of visor sub-assemblies to Mexico and the U.S. Midwest. Lear and Magna break ground on electronics bonding lines in Michigan to serve General Motors' smart-visor launch slated for late 2026. OEM-supplier proximity trims program-management cycles, a critical advantage for electronic visor iterations.

Europe sees modest volume but significant technology pull as stringent PFAS rules kick in. Suppliers like Grupo Antolin pilot hemp-fiber composite cores certified for recyclability under the EU End-of-Life Vehicle Directive amendments finalized in 2025. Mercedes and Stellantis request lifecycle analyses in all RFQs, nudging the supply base toward transparent environmental disclosures. The region’s mature aftermarket relies on value-added upgrades rather than basic replacements, with Audi offering dealer-installed illuminated visor kits for vehicles up to seven years old.

Competitive Landscape

The Automotive sunvisor industry exhibits moderate concentration, with Magna, Grupo Antolin, Toyota Boshoku, and Kasai Kogyo controlling significant OEM sourcing. Vertical integration strategies accelerate; Magna’s 2025 acquisition of a Korean visor substrate plant secures vinyl supply and yields minimal cost savings on raw materials [4]“2025 Investor Presentation,” Magna International, magna.com . Grupo Antolin invests in automated sewing robots to raise fabric visor throughput and cut labor variance.

Technology alliances intensify. Continental and Gentex co-developed a visor camera that feeds driver-monitoring analytics to seat belt tensioners, bundling safety and convenience into one module. Smaller firms pivot to retrofit kits for ride-share fleets, leveraging agile design and lower overhead.

Sustainability is now a core battleground. Toyota Boshoku’s 2025 Kenaf fiber visor cores launch achieved one-third weight saving and attracted Lexus and Subaru nominations. In response, Kasai Kogyo announces a closed-loop vinyl recycling plant in Tennessee capable of processing 1,200 tons annually, promising OEM carbon-credit offsets. These moves show how environmental credentials intertwine with procurement scoring matrices, shifting competition beyond simple cost metrics.

Automotive Sun Visor Industry Leaders

Grupo Antolin

Yanfeng Automotive Interior Systems

IAC Group

Toyota Boshoku Corporation

Magna International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hyundai Motor Group and POSCO Group signed a USD 5.8 billion pact to build an electric-arc-furnace steel mill in Louisiana with 2.7 million metric tons annual capacity from 2029.

- April 2025: Celanese and Li Auto began commercializing Hostaform POM XAP3, an ultra-low-emission polymer for visors and other cabin parts.

- February 2025: Lear Corporation integrated ComfortMax Seat technology into General Motors platforms starting Q2 2025, illustrating cabin-wide comfort strategies that complement advanced visor systems.

Global Automotive Sun Visor Market Report Scope

| Passenger Vehicle |

| Commercial Vehicle |

| Fabric |

| Vinyl |

| Others |

| Conventional |

| LCD |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Vehicle | |

| Commercial Vehicle | ||

| By Material Type | Fabric | |

| Vinyl | ||

| Others | ||

| By Component Type | Conventional | |

| LCD | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Automotive Sun Visor Market in 2030?

The market is forecast to reach USD 8.89 billion by 2030.

Which vehicle segment leads visor demand?

Passenger cars hold 71.29% market share, reflecting higher premium-feature adoption.

Which component type is growing fastest?

LCD smart visors are advancing at a 5.22% CAGR through 2030.

Why is the Asia-Pacific critical for suppliers?

The region contributes 37.91% revenue and offers low-cost, high-volume production hubs in China and India.

How are sustainability rules influencing materials?

EU PFAS restrictions accelerate the shift from traditional vinyl toward bio-based PVC and recycled fabrics.

What CAGR is expected for the aftermarket channel?

The aftermarket is set to grow at a 5.15% CAGR during 2025-2030, driven by ride-hailing fleet replacements.

Page last updated on: