Temporary Power Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

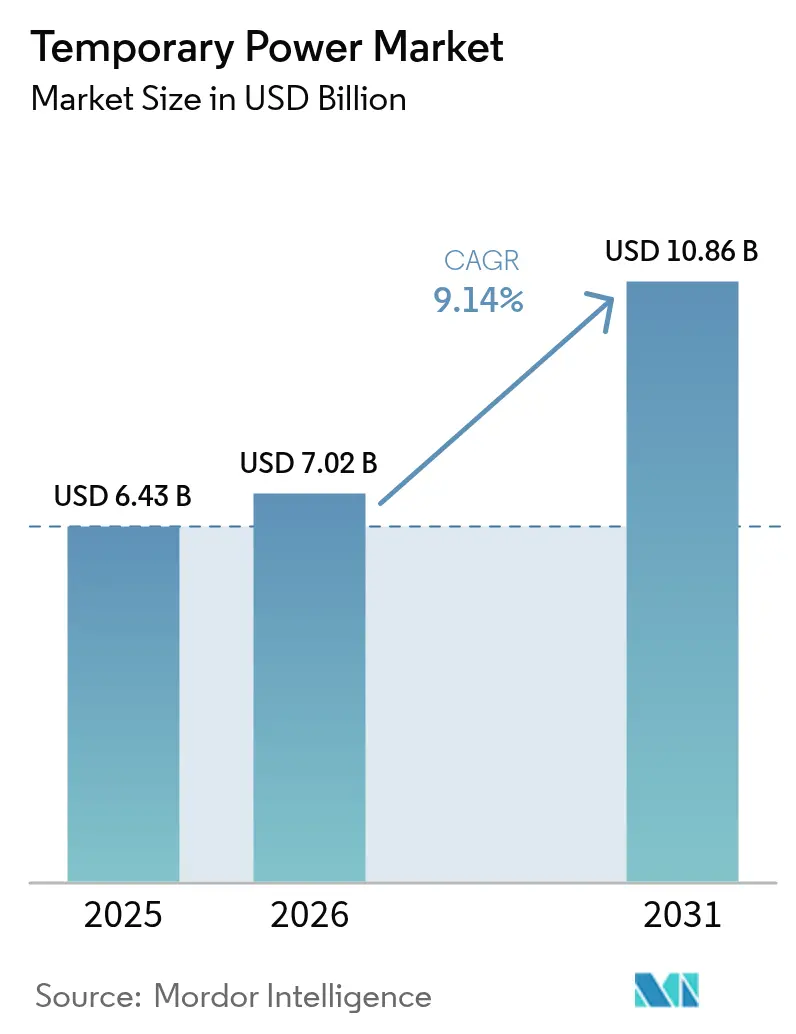

| Market Size (2026) | USD 7.02 Billion |

| Market Size (2031) | USD 10.86 Billion |

| Growth Rate (2026 - 2031) | 9.14% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Temporary Power Market Analysis by Mordor Intelligence

Temporary Power market size in 2026 is estimated at USD 7.02 billion, growing from 2025 value of USD 6.43 billion with 2031 projections showing USD 10.86 billion, growing at 9.14% CAGR over 2026-2031.

Growth is propelled by grid‐modernization programs, extreme-weather disruptions, and accelerating data-center construction, all elevating the need for reliable bridging power. Diesel units retain a sizeable installed base, yet regulatory pressure and ESG targets are spurring hybrid fleet investments. Data-center developers, utilities, and large construction firms anchor demand, while rapid deployment expectations sharpen competition on service capability rather than equipment ownership. North America remains the revenue leader regionally, but Asia-Pacific contributes the greatest absolute volume growth as industrial expansion and infrastructure spending intensify.

Key Report Takeaways

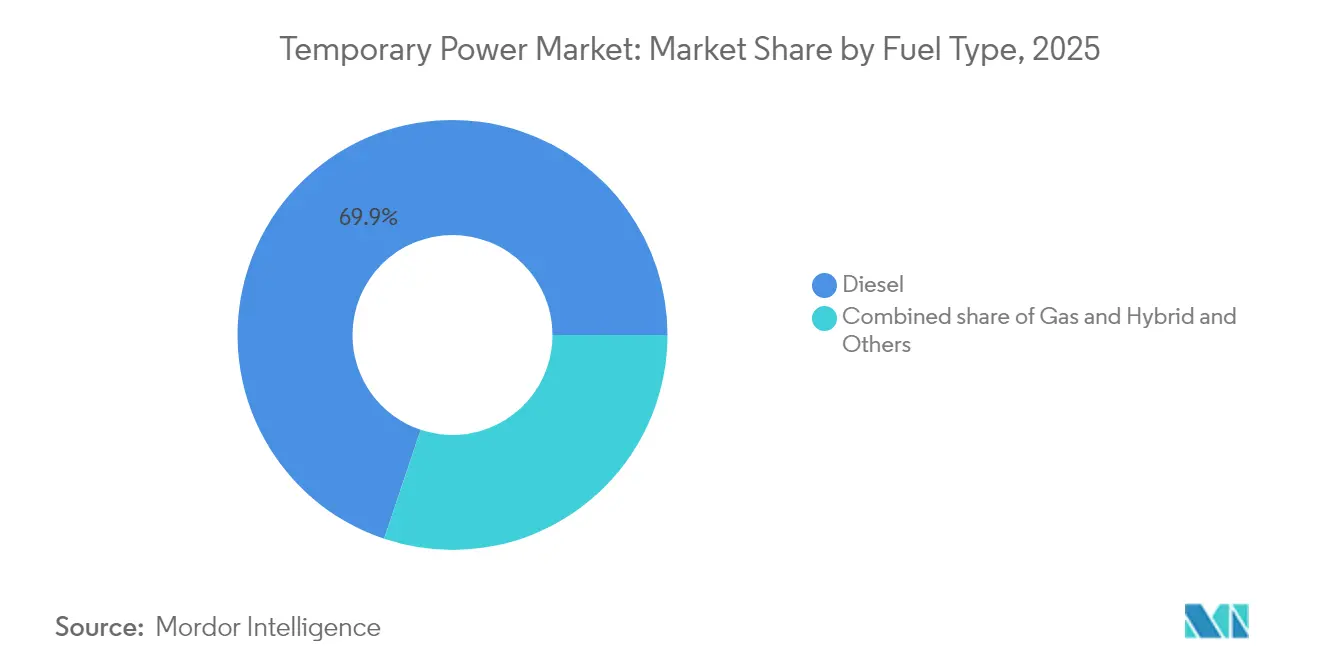

- By fuel type, diesel generators commanded 69.85% of 2025 revenue; hybrid and renewable solutions are forecast to expand at 15.05% CAGR through 2031.

- By power rating, the 501-2,000 kW class led with 32.35% temporary power market share in 2025; units exceeding 2,000 kW are projected to advance at 11.02% CAGR to 2031.

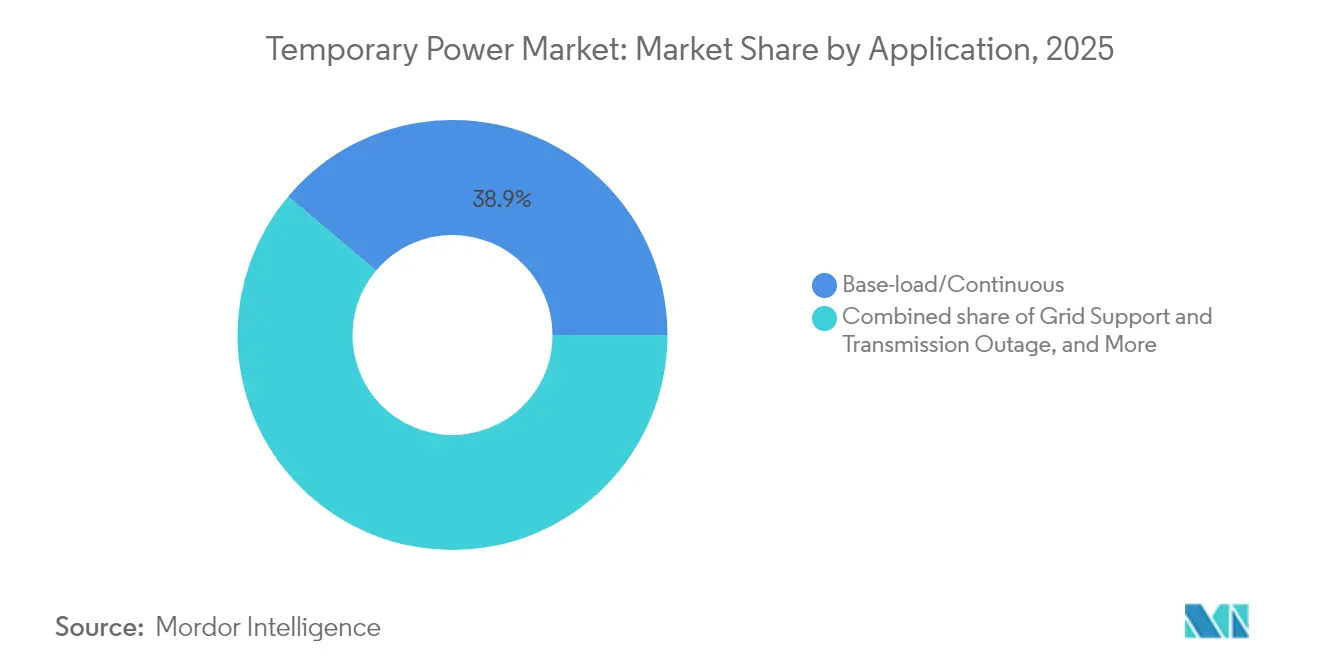

- By application, base-load service held 38.85% of 2025 revenue; grid-support deployments are expected to grow at 10.55% CAGR over the same horizon.

- By end-user industry, utilities captured 31.70% of revenue in 2025; data-center and ICT users are set to record a 12.26% CAGR through 2031.

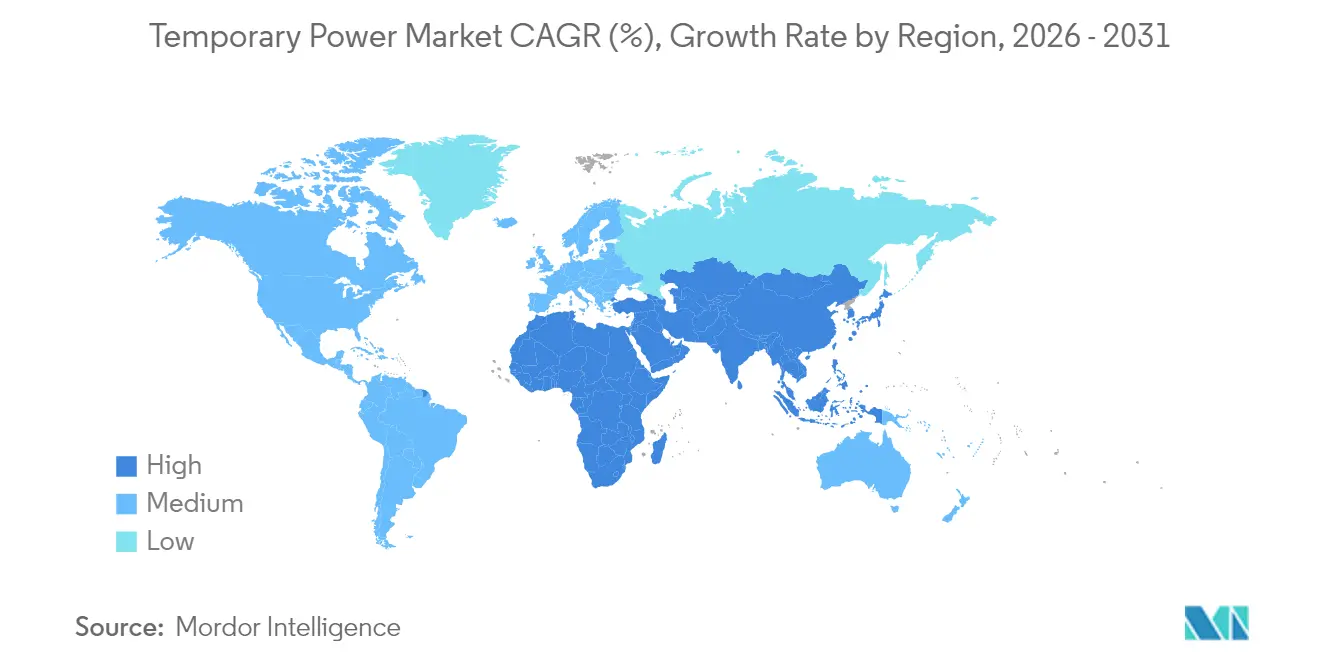

- By geography, North America accounted for 35.05% of revenue in 2025, while Asia-Pacific is anticipated to post a 11.94% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Temporary Power Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising frequency of extreme-weather outages | +2.1% | Global, with acute effects in North America, Europe | Short term (≤ 2 years) |

| Industrialisation & construction booms in emerging markets | +1.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Ageing grid infrastructure & planned maintenance shutdowns | +1.5% | North America & EU, expanding to developed APAC | Long term (≥ 4 years) |

| Multi-gigawatt data-centre "utility-gap" demand | +2.3% | Global, concentrated in major data center hubs | Short term (≤ 2 years) |

| Renewable integration requiring flexible peaking capacity | +1.2% | Europe, North America, progressive APAC markets | Medium term (2-4 years) |

| ESG-driven shift toward low-emission & hybrid rental fleets | +0.9% | Global, led by Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Frequency of Extreme-Weather Outages

Hurricanes, heat waves, wildfires, and monsoon floods are triggering longer and more frequent grid failures, causing emergency generator rentals to spike immediately after each event. Utilities and municipal authorities now pre-stage rental fleets ahead of storm seasons, allowing suppliers to reposition assets and optimize pricing. Insurance underwriters increasingly insist on on-site backup for hospitals, telecom nodes, and cold-chain warehouses. These contractual safeguards convert what was once sporadic, disaster-driven revenue into predictable seasonal demand. As climate variability intensifies, emergency power services have become an embedded line item in North America and Europe's resilience budgets.

Industrialisation & Construction Booms in Emerging Markets

Megaproject pipelines in India, Indonesia, and the Gulf Cooperation Council nations require high-capacity generators to run cranes, concrete plants, and dewatering pumps when grid feeds are absent or unstable. Local rental providers typically supply ≤ 500 kW units, but multinational contractors now prefer bundled packages of 1 MW and above to lower per-kilowatt logistics costs.[1]Sekhar, Metla, "Construction site generators: Types & features of generators used at construction sites," The Economic Times, economictimes.indiatimes.com The resulting scale shift allows global fleets to deliver containerized plants on accelerated timelines. Government stimulus for roads, ports, and industrial corridors further widens the user base, supporting steady multi-year contracts rather than one-off rentals.

Ageing Grid Infrastructure & Planned Maintenance Shutdowns

The average power transformer in the United States has operated for 38 years, and replacement lead times now exceed two years for large units. Utilities mitigate the risk of prolonged outages by leasing multi-megawatt mobile generators during scheduled tie-line or substation upgrades. Rental agreements often span several months, providing suppliers with high utilization and stable cash flows. In Europe, similar modernization drives under the “Fit for 55” package require temporary power during switchgear retrofits, further institutionalizing the service model.

Multi-Gigawatt Data-Center “Utility-Gap” Demand

New hyperscale campuses often face multi-year waits for permanent grid interconnection. Developers bridge the gap by leasing 1.5 MW diesel or gas sets clusters, sometimes exceeding 100 MW aggregate on a single site.[2]Rich Miller, “Diesel Waivers for Data Centers,” Data Center Frontier, datacenterfrontier.com Regulators in Virginia and Dublin have granted waivers allowing temporary generators to operate during grid emergencies, demonstrating official acknowledgement of supply constraints. The accelerated adoption of artificial-intelligence workloads, which carry five-to-six-times higher power density, magnifies the opportunity for rental operators willing to engineer bespoke solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diesel-price volatility & fuel-logistics disruptions | -1.4% | Global, acute in remote and island markets | Short term (≤ 2 years) |

| Stricter global & local emission standards on gensets | -0.8% | Europe, North America, expanding to APAC | Medium term (2-4 years) |

| Battery storage & micro-grids eroding genset demand | -0.6% | Global, concentrated in urban and grid-connected areas | Long term (≥ 4 years) |

| Generator-component supply-chain bottlenecks | -0.9% | Global, with acute effects in North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Global & Local Emission Standards on Gensets

EU Stage V rules oblige particulate filters on 19-560 kW engines; India’s forthcoming CPCB IV+ will extend coverage to 800 kW sets, while California is drafting Tier 5 proposals likely to surpass European stringency.[3]DieselNet, “India CPCB IV+ Emission Limits,” dieselnet.com Each tightening cycle raises capital costs and compresses residual values of legacy fleets, lowering return on invested capital for rental operators. Urban authorities also deploy low-emission zones that limit runtime hours, constraining traditional diesel utilization in core city projects. Although cleaner technologies can offset lost volumes, the transition demands funding and technical retraining.

Diesel-Price Volatility & Fuel-Logistics Disruptions

Global distillate prices experienced three double-digit swings between 2022 and 2024, complicating rental bid formulas that often hold fixed rates for six to twelve months. Supply‐chain bottlenecks extend generator-package lead times beyond 90 weeks and gas-turbine backlogs beyond five years, creating allocation dilemmas for fleet managers.[4]Heatmap News, “Gas-Turbine Backlog Stretches to 2029,” heatmap.news Remote mining and island grids face additional marine-delivery risks, heightening the attractiveness of propane, renewable, or battery-hybrid alternatives despite higher capital intensity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Diesel Dominance Faces Hybrid Challenge

Diesel sets generated 69.85% of 2025 revenue, reflecting ubiquitous service infrastructure, high energy density, and rapid response capabilities that remain indispensable on disaster sites and off-grid projects. Nevertheless, the temporary power market is pivoting toward hybrid formats that combine solar arrays, battery packs, or propane engines, a category forecast to compound at 15.05% annually through 2031. Aggreko’s Martin County microgrid, built around five 1.3 MW gas generators, illustrates the scaling potential for cleaner fuels in oilfield operations. Construction firms adopting electric excavators also request low-noise solar-battery generators, signaling how equipment electrification ripples through the broader temporary power industry. As cost curves fall, hybrid packages shift from pilot deployments to core rental offerings, redesigning procurement specifications across Europe and North America.

By Power Rating: Large-Scale Dominance Driven by Data Centers

Sets in the 501-2,000 kW band held 32.35% of 2025 revenue, serving industrial processes and sizeable construction jobs that value transportability alongside capacity. Above-2,000 kW machines deliver the highest forecast growth at 11.02% CAGR, underpinned by hyperscale data-center commissioning schedules that now demand 100 MW-plus bridging solutions. Aggreko’s rollout of eight 1.5 MVA gensets for a Malaysian data-center complex exemplifies how modular design lets operators match rising load profiles without extended downtime. Meanwhile, the up-to-50 kW niche retains relevance for residential and small commercial backup, but its share erodes as telecom towers and clinics migrate to solar-battery kits.

By Application: Base-Load Leadership Meets Grid-Support Growth

Base-load and continuous use cases held 38.85% of 2025 revenue, including long-term power for remote mines, bottling plants, and island hospitality assets. Yet grid-support deployments will outpace all others at 10.55% CAGR, amplified by scheduled transmission upgrades and peak-shaving programs. CenterPoint Energy’s plan to install 15 mobile generation units totaling 450 MW for summer 2025 grid stability typifies how utilities now embed mobile assets into reliability strategies. The convergence of emergency, maintenance, and peaking services erodes traditional application silos, broadening the opportunity for suppliers that offer turnkey engineering and remote monitoring.

By End-User Industry: Utilities Lead as Data Centers Surge

Utilities contributed 31.70% of 2025 rental revenue, driven by planned maintenance at substations, transformer replacements, and hurricane-season contingencies. The data-center segment, however, is set to log a 12.26% CAGR to 2031 as AI-training clusters push power density beyond grid‐connection timelines. Cummins reported a 24% rise in power-generation sales in Q3 2024, attributing growth largely to this customer class. Oil-and-gas clients maintain a stable demand for offshore drilling, gas-lift compression, and decommissioning, while event organizers favor low-noise, Stage V-compliant units for urban festivals.

Geography Analysis

North America’s leadership in the temporary power market rests on a sophisticated rental ecosystem, deep OEM–dealer partnerships, and disciplined asset-management practices. United Rentals alone operates 1,591 locations and manages a USD 21.4 billion equipment fleet, enabling rapid mobilization when storms threaten Gulf Coast refineries or when Midwest utilities announce transformer change-outs. The United States accounts for most regional demand, while Canada supplements with LNG plant builds and hydro dam refurbishments. Mexico adds volume through nearshoring-driven factory expansions.

Asia-Pacific supplies the highest growth trajectory as governments channel multi-year funding into roads, airports, and urban transit. China drives headline volumes but faces policy-induced caps on diesel runtime in tier-1 cities, accelerating migration toward gas and hybrid sets. India adopts similar standards under CPCB IV+ yet remains a diesel stronghold for rural electrification and construction. ASEAN economies, Vietnam, Indonesia, and the Philippines, present diverse grid resiliency challenges, favoring mid-scale containerized solutions. Japanese and Korean contractors specify Stage V-equivalent engines, anchoring premium demand in the region.

Europe’s market centres on emission compliance and renewable-grid integration. Germany, France, and the United Kingdom purchase large fleets of Stage V gensets paired with battery pods for low-noise urban applications. The region also pioneers hydrogen-ready mobile turbines to balance offshore wind intermittency in the North Sea. Southern and Eastern European countries grow more modestly but exhibit episodic spikes tied to hydro-dam refurbishments and gas-pipeline expansions. Across the continent, city authorities incentivize hybrid rental packages by granting low-emission‐zone access, thereby shaping fleet renewal cycles.

Competitive Landscape

Competitive intensity remains moderate as the top five suppliers account for about 60% of global rental revenue, leaving ample space for regional specialists. Aggreko leverages its global footprint and application engineering to capture multi-site, multi-megawatt contracts in data centers, utilities, and mining. Caterpillar and Cummins monetize deep vertical integration, engine, alternator, and control systems, offering faster lead times in markets with volatile demand. Atlas Copco expands its Specialty Rental arm via bolt-on acquisitions in New Zealand and South Africa, signalling a strategy to build localized hubs rather than centralized megafleets.

Consolidation gathers pace in North America. Herc Holdings proposed a USD 5.3 billion merger with H&E Equipment Services, aiming for USD 300 million in annual synergies and enhanced access to industrial clientele. Deutz’s acquisition of Blue Star Power Systems diversifies its engine business into packaged generators and is expected to add USD 100–150 million in annual revenue. Technology-oriented deals also rise: Generac’s purchase of PowerPlay Battery Energy Storage Systems arms the company with commercial BESS capacity up to 7 MWh, complementing its generator lineup for hybrid offerings.

Differentiation increasingly hinges on emissions performance, digital monitoring, and turnkey service capability rather than equipment count alone. United Rentals markets solar-battery generator sets for urban construction sites, while Caterpillar pilots Dynamic Energy Transfer platforms that automatically balance diesel, solar, and battery inputs on remote mines. Smaller regional players carve niches by tailoring fleets to extreme climates, arctic oilfields, tropical mining camps, or high-altitude construction, where global firms may lack localized engineering. Suppliers that invest in telemetry and analytics gain a pricing edge as customers demand outcome-based contracts, measured in uptime percentages or fuel-savings guarantees.

Temporary Power Industry Leaders

-

Aggreko plc

-

Cummins Inc.

-

APR Energy Ltd

-

Caterpillar Inc.

-

United Rentals Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Generac announced a 320,000 sq ft manufacturing plant in Beaver Dam, Wisconsin, slated to employ 350–400 workers and expand industrial-generator output.

- February 2025: CenterPoint Energy secured ERCOT approval for 15 emergency mobile generators totaling 450 MW, with first deployments scheduled for Summer 2025.

- January 2025: Herc Holdings proposed a USD 5.3 billion merger with H&E Equipment Services, targeting USD 300 million EBITDA synergies and creating North America’s third-largest rental fleet.

- January 2025: Generac’s Pramac unit acquired a majority stake in India’s Captiva Energy Solutions to strengthen its presence in one of the world’s fastest-growing generator markets.

Global Temporary Power Market Report Scope

The temporary power market report includes:

| Diesel |

| Gas |

| Hybrid and Others |

| Up to 50 kW |

| 51 to 280 kW |

| 281 to 500 kW |

| 501 to 2,000 kW |

| Above 2,000 kW |

| Base-load/Continuous |

| Grid Support and Transmission Outage |

| Disaster Relief and Emergency |

| Remote-area Electrification |

| Utilities and Power |

| Oil and Gas |

| Construction and Mining |

| Manufacturing and Industrial |

| Events and Entertainment |

| Data Centres and ICT |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Fuel Type | Diesel | |

| Gas | ||

| Hybrid and Others | ||

| By Power Rating | Up to 50 kW | |

| 51 to 280 kW | ||

| 281 to 500 kW | ||

| 501 to 2,000 kW | ||

| Above 2,000 kW | ||

| By Application | Base-load/Continuous | |

| Grid Support and Transmission Outage | ||

| Disaster Relief and Emergency | ||

| Remote-area Electrification | ||

| By End-User Industry | Utilities and Power | |

| Oil and Gas | ||

| Construction and Mining | ||

| Manufacturing and Industrial | ||

| Events and Entertainment | ||

| Data Centres and ICT | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the temporary power market?

The temporary power market size reached USD 7.02 billion in 2026 and is forecast to hit USD 10.86 billion by 2031.

Which segment is growing fastest within the temporary power market?

Hybrid and renewable-fuel generators are projected to expand at 15.05% CAGR through 2031, outpacing traditional diesel sets.

Why are data centers important to temporary power demand?

Hyperscale campuses often face multi-year grid-connection delays, requiring 100 MW-plus temporary power installations to bridge the “utility gap.”

How do emission regulations affect rental fleets?

EU Stage V and forthcoming U.S. Tier 5 rules mandate advanced particulate control, increasing capital costs and accelerating hybrid‐fleet adoption.

Which region will add the most new temporary power capacity?

Asia-Pacific is set to record a 11.94% CAGR to 2031, driven by infrastructure investment in China, India, and Southeast Asia.

What technologies are emerging alongside diesel generators?

Mobile gas turbines capable of burning hydrogen blends, battery-integrated solar systems, and propane-hybrid generators are all gaining traction for low-emission deployments.

Page last updated on: