Aircraft Circuit Breakers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

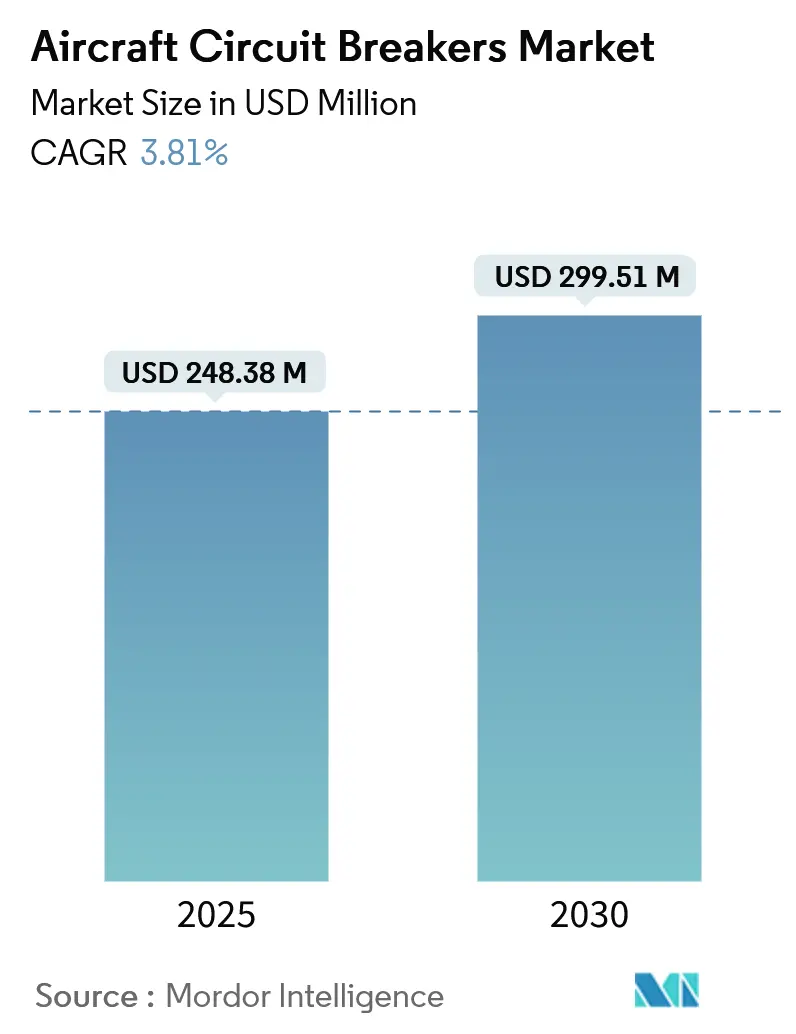

| Market Size (2025) | USD 248.38 Million |

| Market Size (2030) | USD 299.51 Million |

| Growth Rate (2025 - 2030) | 3.81% CAGR |

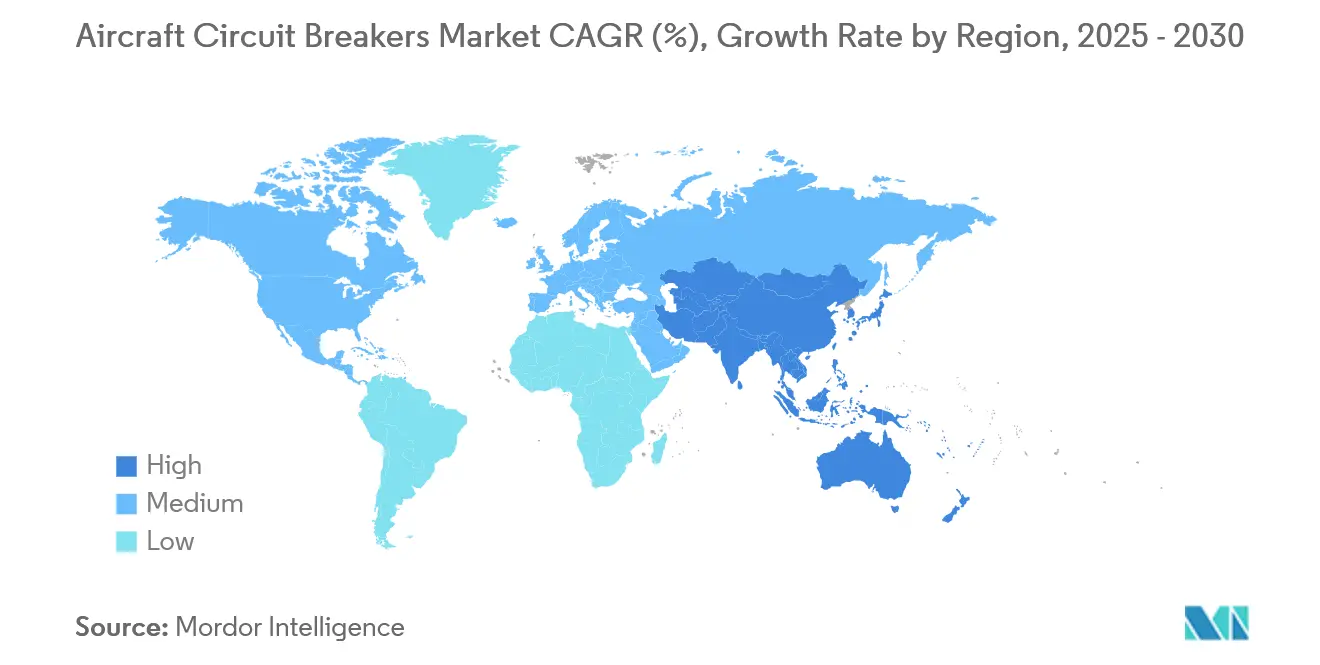

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Circuit Breakers Market Analysis by Mordor Intelligence

The aircraft circuit breakers market size stood at USD 248.38 million in 2025 and is forecasted to reach USD 299.51 million by 2030, translating into a 3.81% CAGR. Airlines, airframers, and system suppliers are steadily replacing hydraulic and pneumatic subsystems with electrical alternatives, which multiplies the number of protected feeders on every platform and sustains long-run demand for reliable circuit breakers. Weight-saving mandates from original-equipment manufacturers (OEMs), the maturation of silicon-carbide (SiC) switching devices, and certification progress on electric vertical-take-off-and-landing (eVTOL) aircraft collectively lift near-term order pipelines. At the same time, qualified thermal-magnetic breakers enjoy entrenched positions in retrofit programmes where operators value interchangeability over novel features. Regional defence budgets aimed at high-energy radar and directed-energy payloads further expand the addressable base, even as intermittent semiconductor shortages cap upside potential on the supply side.[1]Source: RTX Corporation, “RTX reports Q2 2025 results,” Rtx.com

Key Report Takeaways

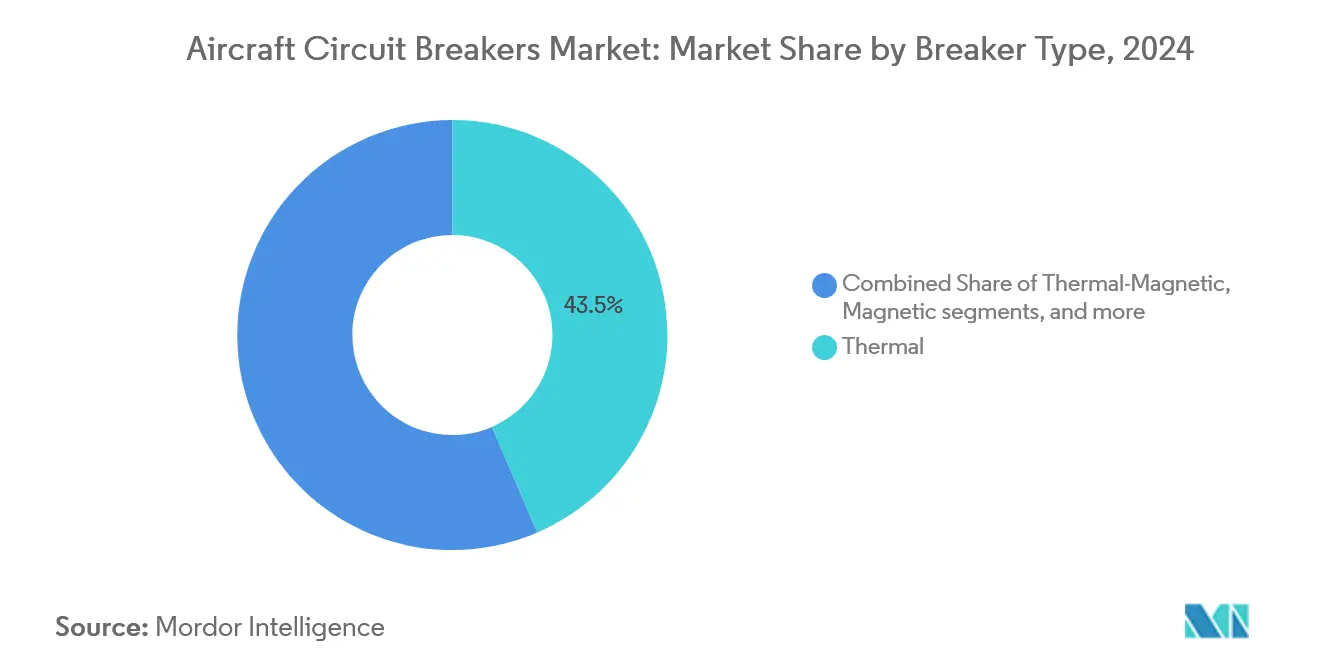

- By breaker type, thermal units commanded 43.54% of the aircraft circuit breakers market share in 2024, while electronic circuit breaker units are accelerating at 6.41% CAGR through 2030.

- By aircraft type, fixed-wing platforms held 65.89% revenue share in 2024; advanced air mobility programs deliver a 7.98% CAGR to 2030 as eVTOL certifications progress.

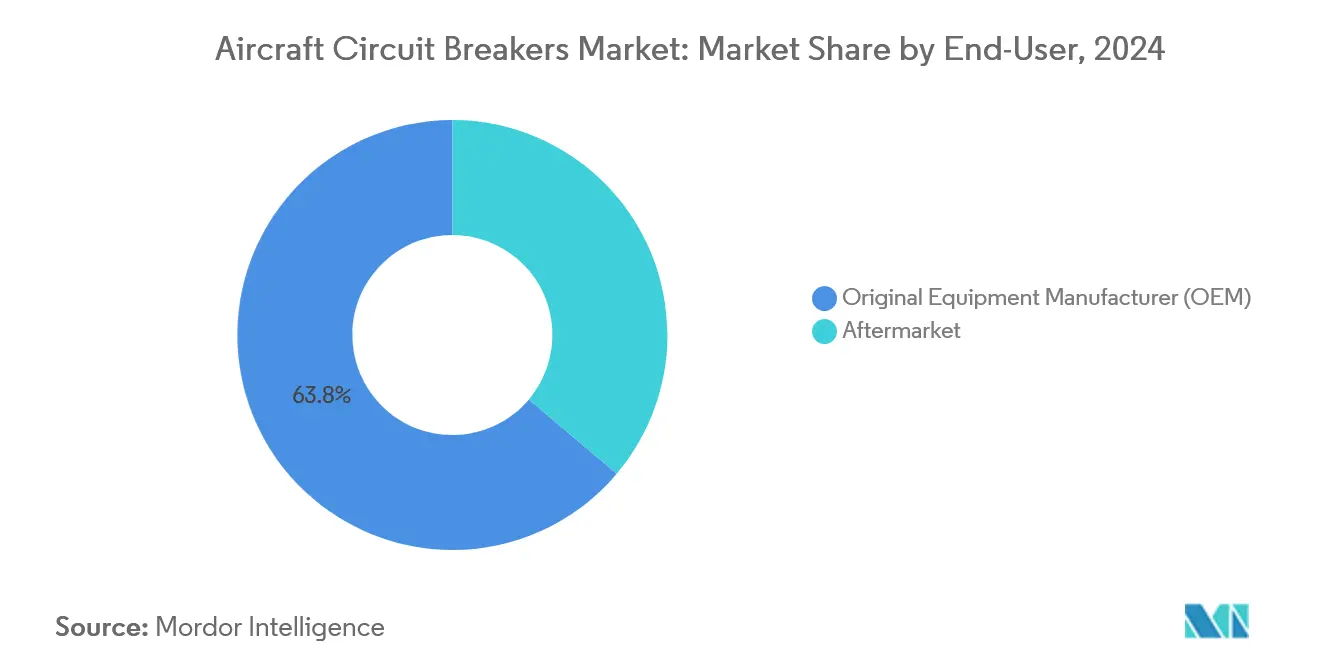

- By end-user, OEMs accounted for 63.78% of the aircraft circuit breakers market in 2024 and are expanding at a 4.36% CAGR due to narrowbody production ramp-ups.

- By voltage range, low-voltage feeders represented 35.87% share in 2024, yet high-voltage applications are pacing growth at 5.21% CAGR as 270 V DC architectures proliferate.

- By geography, North America maintained a 39.60% share in 2024, while Asia-Pacific is projected to register the fastest 5.65% CAGR through 2030.

Global Aircraft Circuit Breakers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated shift to “More-Electric Aircraft” architectures | +1.2% | Global, early adoption in North America and EU | Long term (≥ 4 years) |

| Rising retrofit demand for solid-state circuit protection in ageing commercial fleets | +0.8% | North America and EU core, spill-over to APAC | Medium term (2-4 years) |

| Ramp-up of narrowbody production (A320neo, B737 MAX) boosting installed base | +0.7% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Military modernization budgets favoring high-power DC distribution | +0.5% | North America, EU, APAC defence markets | Medium term (2-4 years) |

| OEM push for weight-saving components in eVTOL and UAM prototypes | +0.4% | North America and EU first movers, APAC followers | Long term (≥ 4 years) |

| Airline focus on predictive-maintenance ready components (self-monitoring breakers) | +0.3% | Global, led by major airline hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Shift to “More-Electric Aircraft” Architectures

The migration toward 270 V DC and higher voltages expands every electrical load on board, boosting the installed base of protection devices per aircraft. Boeing 787 and parallel military demonstrators already use megawatt-class electrical subsystems, arc-fault-tolerant, low-loss breakers to operate in unpressurised bays.[2]Source: National Aeronautics and Space Administration, “Development of a Thermal Management System for Electrified Aircraft,” Ntrs.nasa.gov Safran’s GENeUSGRID energy-management line integrates solid-state disconnects that achieve 99.5% efficiency, underscoring OEM appetite for integrated power and protection modules. Because each hydraulic actuator replacement typically spawns several new electrical feeders, the multiplier effect materially expands the aircraft circuit breakers market over the long term. Programme-level commitments such as Airbus ZeroE and the US Navy’s Next-Generation Air-Dominance (NGAD) road-map confirm the durability of this shift. Therefore, the aircraft circuit breakers market tracks broader electrification trends rather than isolated sub-system upgrades.

Rising Retrofit Demand for Solid-State Circuit Protection in Ageing Fleets

Commercial operators are extending asset life cycles while tightening dispatch-reliability targets, which positions predictive-maintenance-ready breakers as an immediate upgrade path. Incidents linked to wiring faults have heightened regulatory scrutiny, prompting carriers to substitute mechanical breakers with electronic units that offer embedded health monitors. Astronics reports 20-fold reliability improvements and 30% wiring-weight reductions on its electronic circuit breaker unit retrofit kits, savings that feed directly into fuel burn and turnaround metrics.[3]Source: Astronics, “Aircraft Power Distribution,” Astronics.com Because these kits install within existing panel footprints, airlines avoid wholesale rewiring and circumvent lengthy supplemental type-certificate cycles. As a result, the retrofit channel provides a counter-cyclical buffer that smooths revenues during OEM build-rate fluctuations and underpins the medium-term expansion of the aircraft circuit breakers market.

Ramp-up of Narrowbody Production Boosting Installed Base

Airbus aims for 89 A320neo airframes a month by 2025, and Boeing targets steady-state B737 MAX output at 31 units, translating into several hundred new shipments of sets of breakers every four weeks. Each narrowbody contains 200-300 protection devices across 28 V DC, 115 V AC, and emerging 270 V DC buses, so incremental production lifts aggregate demand in lock-step. Tier-one suppliers with line-fit positions secure multiyear frame contracts, locking in ship-set pricing and capacity reservations. Because the single-aisle segment captures most new route openings, the aircraft circuits market benefits directly from the shift toward fuel-efficient narrowbody fleets operated on high-frequency schedules.

Military Modernization Budgets Favoring High-Power DC Distribution

Directed-energy weapons (DEWs), active electronically scanned array (AESA) radars, and electronic-warfare (EW) pods require kilovolt-ampere power levels delivered through tightly controlled DC buses. US Army UH-60M and US Marine Corps H-1 avionics upgrades embed modular open-systems architectures that specify fault-tolerant, actively monitored protection stages. Bell’s structural power upgrade on the H-1 fleet further illustrates how legacy airframes gain electrical headroom to host future mission payloads. Defence qualification funnels near-term orders toward incumbents with pedigree in high-vibration, high-temperature duty cycles, reinforcing moderate concentration within the aircraft circuit breakers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Certification lag for novel solid-state power controllers | -0.9% | Global, stringent in North America and EU | Long term (≥ 4 years) |

| Heat-dissipation challenges above 270 V DC architectures | -0.6% | Global, acute in high-power applications | Medium term (2-4 years) |

| Limited standardization across OEM platforms inflating qualification cost | -0.4% | Global, fragmented by regional preferences | Long term (≥ 4 years) |

| Persistent supply-chain shortages of high-current MOSFETs and SiC devices | -0.3% | Global, focused on chip-fabrication hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Certification Lag for Novel Solid-State Power Controllers

Federal Aviation Administration Advisory Circular 25.1701-1 mandates rigorous demonstration of wiring and device durability, and DO-160 environmental tests expose new electronic designs to lightning strikes, thermal cycling, and electromagnetic interference. These regimes extend approval cycles to three to five years, during which legacy mechanical breakers continue to win line-fit positions. H55 secured the first European Union Aviation Safety Agency approval for electric-propulsion protection in 2023, proving feasibility but underscoring resource demands on applicants. Certification inertia, therefore, tempers the otherwise quick transition toward digital solutions and subtracts roughly 0.9 percentage points from the aircraft circuit breakers market CAGR assessment.

Heat-Dissipation Challenges Above 270 V DC Architectures

Higher voltages cut conductor weight but multiply I²R losses inside solid-state switches, creating concentrated thermal loads. NASA thermal-management trials show that active liquid cooling or phase-change materials add 15-20% mass to the power-distribution assembly, offsetting some efficiency gains. Military demonstrators using 540 V DC buses report elevated skin-temperature readings that pressure composite panel tolerances. System designers must therefore trade efficiency against added weight budget and maintenance complexity. Until novel wide-bandgap devices become mainstream, these heat-rejection hurdles shave 0.6 percentage points from the expected expansion of the aircraft circuit breakers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breaker Type: Solid-State Solutions Challenge Thermal Dominance

Thermal units held 43.54% of the aircraft circuit breakers market share in 2024, cementing their role as the incumbent choice for line-fit and fleet-age retrofit work scopes. The segment stays attractive because of modest acquisition cost, broad qualification history, and minimal software overhead. Operators value plug-and-play interchangeability that keeps certification changes negligible during heavy checks.

Electronic circuit breaker units record a 6.41% CAGR through 2030 as airlines and OEMs weigh life-cycle economics over purchase price. Embedded current-sensing and data-bus connectivity support predictive maintenance, reducing unscheduled component removals by double-digit percentages. Astronics’ platform, for instance, demonstrates refractory times an order of magnitude quicker than bimetal designs, allowing finer discrimination between transient and sustained overloads. The improved monitoring capabilities expand adoption even in safety-critical feeds, signalling a measured shift in the aircraft circuit breakers market toward semiconductor-based products.

By Aircraft Type: Advanced Air Mobility Drives Electrical Innovation

Fixed-wing models collectively secured 65.89% revenue in 2024 because the global single-aisle backlog exceeds ten thousand units, guaranteeing multi-year production visibility. Fleet-standardisation strategies at major carriers sustain upgrade work scopes for legacy narrowbodies that remain operational beyond 2035.

Advanced air mobility operations, including eVTOL shuttles and cargo drones, expand at a 7.98% CAGR, injecting incremental high-voltage, high-cycle protection hardware. These designs utilise distributed electric propulsion that imposes rapid switching and high-frequency load steps, conditions best served by solid-state breakers with embedded diagnostics. Consequently, platform diversification broadens the aircraft circuit breakers market opportunity outside the historically dominant fixed-wing enclave.

By End-User: OEM Integration Shapes Market Dynamics

OEMs controlled 63.78% of the aircraft circuit breakers market in 2024, with a 4.36% CAGR baked in via backlog-driven production hikes. Because certification ownership stays with the integrator, OEMs tend to single-source breakers with proven reliability records and backward compatibility across model upgrades, locking suppliers into long-term master terms agreements.

While smaller in value, the aftermarket channel offers higher operating margins and steady demand from ageing narrowbodies, turboprops, and regional jets. Predictive maintenance capabilities embedded in electronic breakers shorten troubleshooting cycles and lower no-fault-found events. Airlines re-allocate scheduled maintenance labour to revenue-generating activities, steadily tilting value toward digital units within the broader aircraft circuit breakers market.

By Voltage Range: High-Voltage Systems Drive Innovation

Low-voltage feeders retained a 35.87% share in 2024 because legacy avionics and cabin systems still operate within this envelope. The domain remains a volume play with limited growth.

High-voltage rails push a 5.21% CAGR, propelled by megawatt-grade propulsion experiments and auxiliary power units optimised for efficient transmission. Sensata’s STPS500 PyroFuse operates up to 1,000 V and disconnects in under 1 millisecond, meeting stringent arcing criteria for lithium-ion battery strings and inverters. Silicon-carbide (SiC) MOSFET arrays reduce switching losses, enabling smaller heatsinks and lighter packaging. Their entry underscores how material advances underpin the long-term outlook of the aircraft circuit breakers market.

Geography Analysis

North America preserved 39.60% revenue in 2024, underpinned by mature supply chains in Wichita, Montreal, and the Pacific Northwest and a robust defence modernization cadence. RTX reported USD 21.6 billion Q2 2025 sales and a record USD 236 billion backlog, reinforcing procurement visibility for tier-two component producers. The F-35 enhanced power and cooling programme achieved 80 kW capacity, setting a reference point for high-density protection assemblies. Collective momentum ensures the aircraft circuit breakers market continues benefiting from the region's early-adopter demand.

Asia-Pacific registers the fastest 5.65% CAGR through 2030, supported by passenger traffic resurgence, local aerospace industrialisation, and rising defense budgets in China, Japan, and India. Indigenous semiconductor fabs under construction in Japan and Taiwan are expected to alleviate medium-term chip shortages, tightening the regional ecosystem around circuit-protection value streams. Fleet-age statistics also show older jetliners operating in secondary markets, a factor that sustains retrofit demand and broadens participation across suppliers.

Europe maintains a structurally significant share anchored by Airbus final assembly lines, subsystem champions in France and Germany, and regulatory leadership through the European Union Aviation Safety Agency. Safran posted EUR 7,257 million (USD 8,541.49 million) in the first quarter of 2025 revenue, a 12% year-on-year rise driven by narrow-body engine and equipment volume. Ongoing research into hybrid-electric propulsion qualifies the region as an innovation hub, raising the technical bar inside the aircraft circuit breakers market for integrating smart disconnects, enhanced diagnostics, and recyclable materials.

Competitive Landscape

The aircraft circuit breakers market displays moderate fragmentation. Sensata, RTX subsidiary Collins Aerospace, and Safran guard entrenched line-fit positions by pairing broad catalogues with certification experience spanning multiple airframe generations. Safran’s July 2025 purchase of Collins’ flight-controls business tightened vertical integration around power distribution, electro-mechanical actuation, and protection.

Technology rivalry intensifies around solid-state architectures, where smaller specialists harness fast-switching silicon-carbide devices to deliver weight and reliability advantages. Yet scaling those gains to commercial production volumes demands capital and regulatory resources often lacking in newcomers. Consequently, incumbents acquire niche innovators to accelerate portfolio refresh without exposing themselves to prolonged R&D payback cycles.

Price competition remains secondary to reliability metrics and through-life support. Airlines and defence ministries favour suppliers capable of global field-service coverage and digital twin data integration. This service overlay reinforces the stickiness of existing contracts and shapes future tender evaluations. Overall, switched-reluctance technology, adaptive trip logic, and embedded prognostics are the frontiers defining the next five-year positioning battles within the aircraft circuit breakers market.

Aircraft Circuit Breakers Industry Leaders

Sensata Technologies, Inc.

RTX Corporation

Safran SA

Astronics Corporation

TE Connectivity Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Sensata unveiled its PyroFuse, which significantly advances the high-voltage safety market. The STPS500 series, featuring a compact design and fast interrupt time, addresses the growing need for reliable. It ensures protection in aerospace, ensuring safety against short circuits and electrical shocks in applications up to 1000 V.

- March 2025: Collins Aerospace secured a USD 80.2 million award to modernize UH-60M avionics, embedding a modular open-systems architecture that raises circuit-protection density.

Global Aircraft Circuit Breakers Market Report Scope

| Thermal |

| Thermal-Magnetic |

| Magnetic |

| Electronic Circuit Breaker Units (ECB-Us) |

| Fixed-Wing Aircraft | Commercial | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Military | Fighter Jets | |

| Transport Aircraft | ||

| Special-Mission Aircraft | ||

| General Aviation | Business Jets | |

| Piston and Turboprop Aircraft | ||

| Rotorcraft | Civil Helicopters | |

| Military Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| Advanced Air Mobility (AAM) | ||

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| High |

| Medium |

| Low |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Breaker Type | Thermal | ||

| Thermal-Magnetic | |||

| Magnetic | |||

| Electronic Circuit Breaker Units (ECB-Us) | |||

| By Aircraft Type | Fixed-Wing Aircraft | Commercial | Narrowbody |

| Widebody | |||

| Regional Jets | |||

| Military | Fighter Jets | ||

| Transport Aircraft | |||

| Special-Mission Aircraft | |||

| General Aviation | Business Jets | ||

| Piston and Turboprop Aircraft | |||

| Rotorcraft | Civil Helicopters | ||

| Military Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| Advanced Air Mobility (AAM) | |||

| By End-User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Voltage Range | High | ||

| Medium | |||

| Low | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is global demand for aircraft circuit protection expected to grow to 2030?

It is projected to rise at a 3.81% CAGR, moving from USD 248.38 million in 2025 to USD 299.51 million in 2030.

Which breaker technology is advancing the quickest?

Electronic circuit breaker units lead with a 6.41% CAGR, reflecting airline and OEM preference or predictive-maintenance features.

Why are high-voltage rails important for future aircraft platforms?

Voltages at or above 270 V DC reduce conductor weight and improve distribution efficiency, though they require advanced thermal and protection solutions.

Which region offers the strongest growth outlook?

Asia-Pacific shows the fastest 5.65% CAGR, driven by expanding commercial fleets and rising defence investment.

What factor most restrains rapid solid-state adoption?

Lengthy certification cycles under FAA and EASA rules delay entry of novel solid-state power controllers into commercial service.

Page last updated on: