Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 139.43 Billion |

| Market Size (2031) | USD 187.95 Billion |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

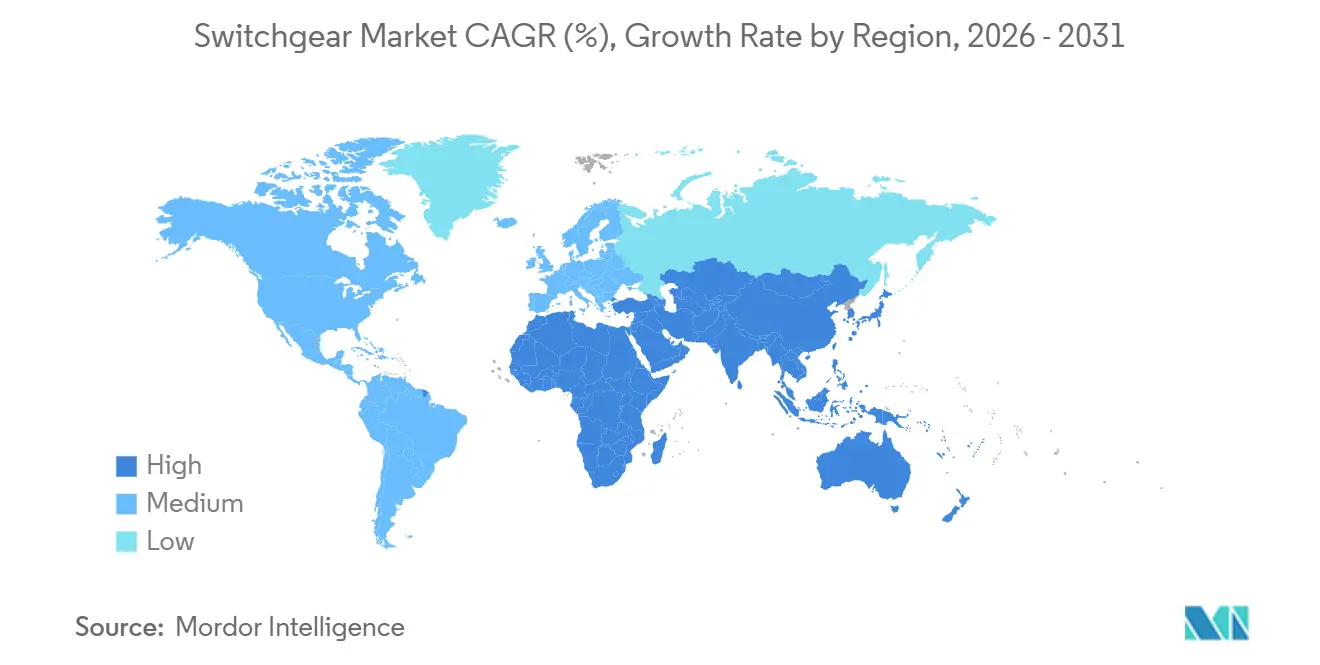

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

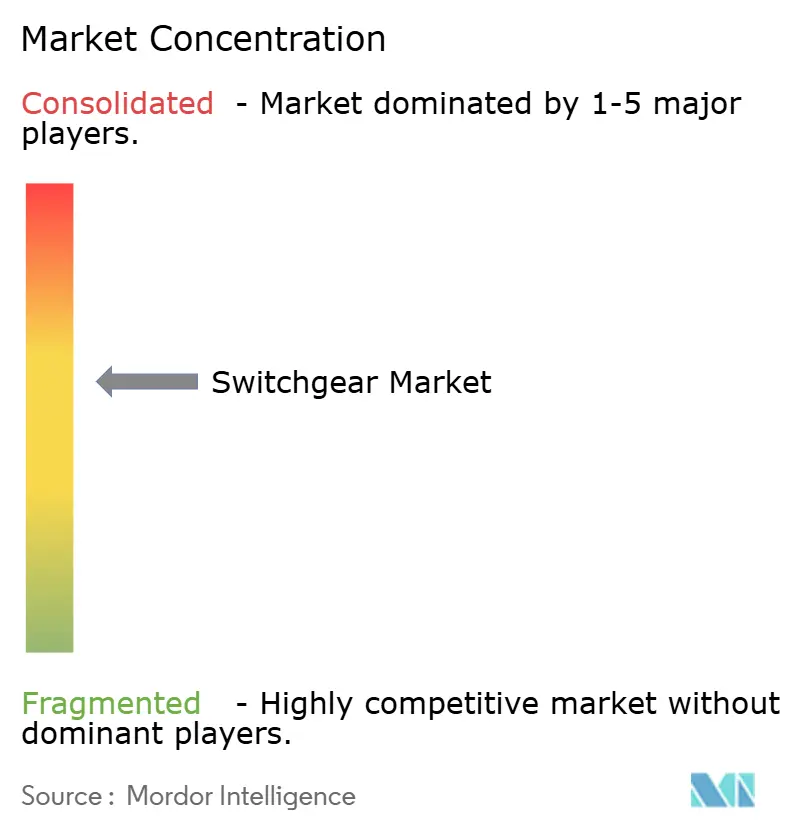

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switchgear Market Analysis by Mordor Intelligence

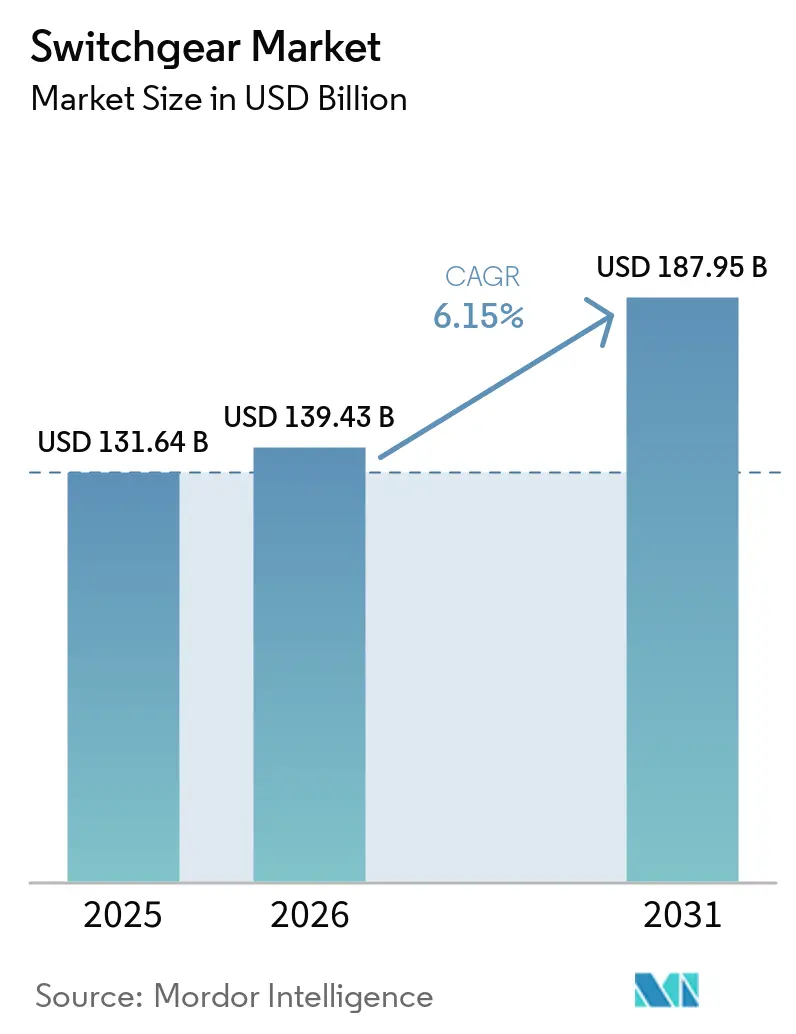

The Switchgear Market size is expected to increase from USD 131.64 billion in 2025 to USD 139.43 billion in 2026 and reach USD 187.95 billion by 2031, growing at a CAGR of 6.15% over 2026-2031.

Growth is supported by rapid data-center electrification, government-funded grid-resilience programs, and the European Union ban on SF₆ in medium-voltage equipment below 24 kV that starts in January 2026.[1]European Commission, “EU Legislation to Control F-Gases,” climate.ec.europa.eu Copper and CRGO steel price swings are pressuring manufacturers to redesign low-voltage busbars, while fluoronitrile supply constraints lengthen lead times for gas-insulated gear. Asia-Pacific leads current demand and is expanding the switchgear market faster than any other region as China builds ultra-high-voltage corridors and India modernizes distribution grids.[2]Ministry of Power, “Revamped Distribution Sector Scheme,” powermin.gov.in Utilities continue to direct the largest share of capital toward switchgear market upgrades that harden networks against extreme weather and integrate renewable generation.

Key Report Takeaways

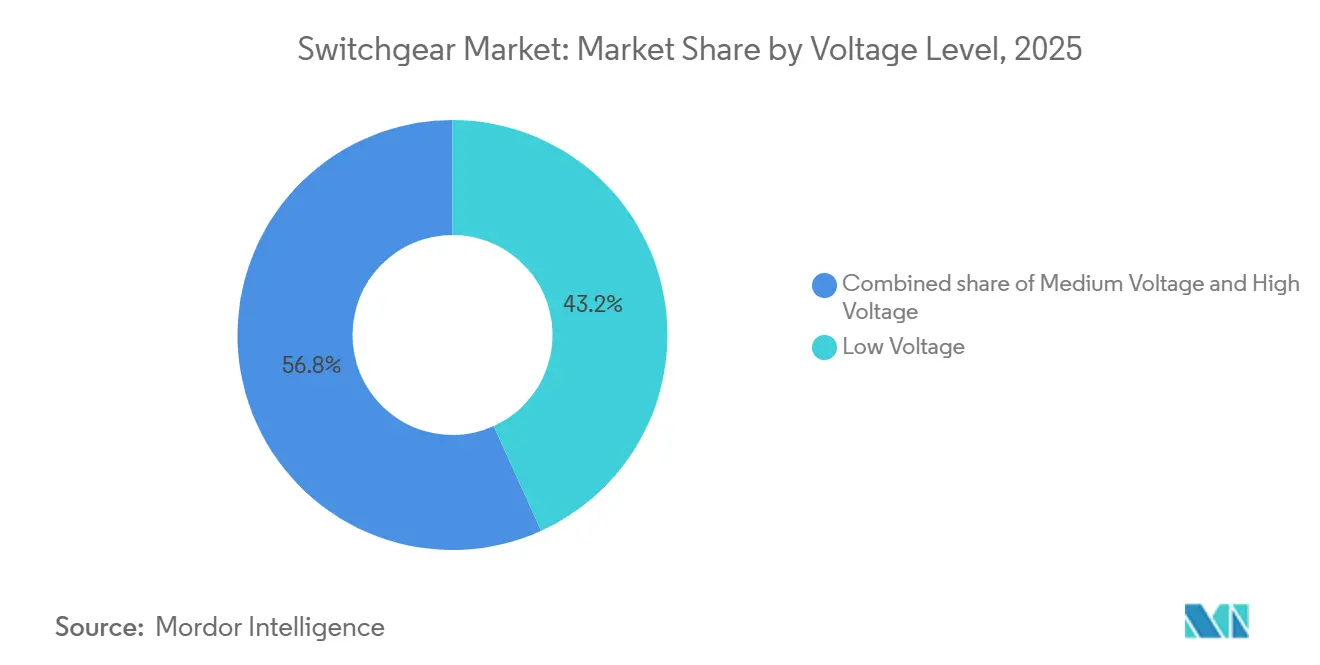

- By voltage, low-voltage equipment led with 43.22% revenue share in 2025, while high-voltage gear is projected to expand at an 8.01% CAGR through 2031.

- By insulation type, air-insulated units commanded 67.79% of 2025 demand; the “others” category, which includes solid-dielectric designs, is expected to grow at a 14.50% CAGR over 2026-2031.

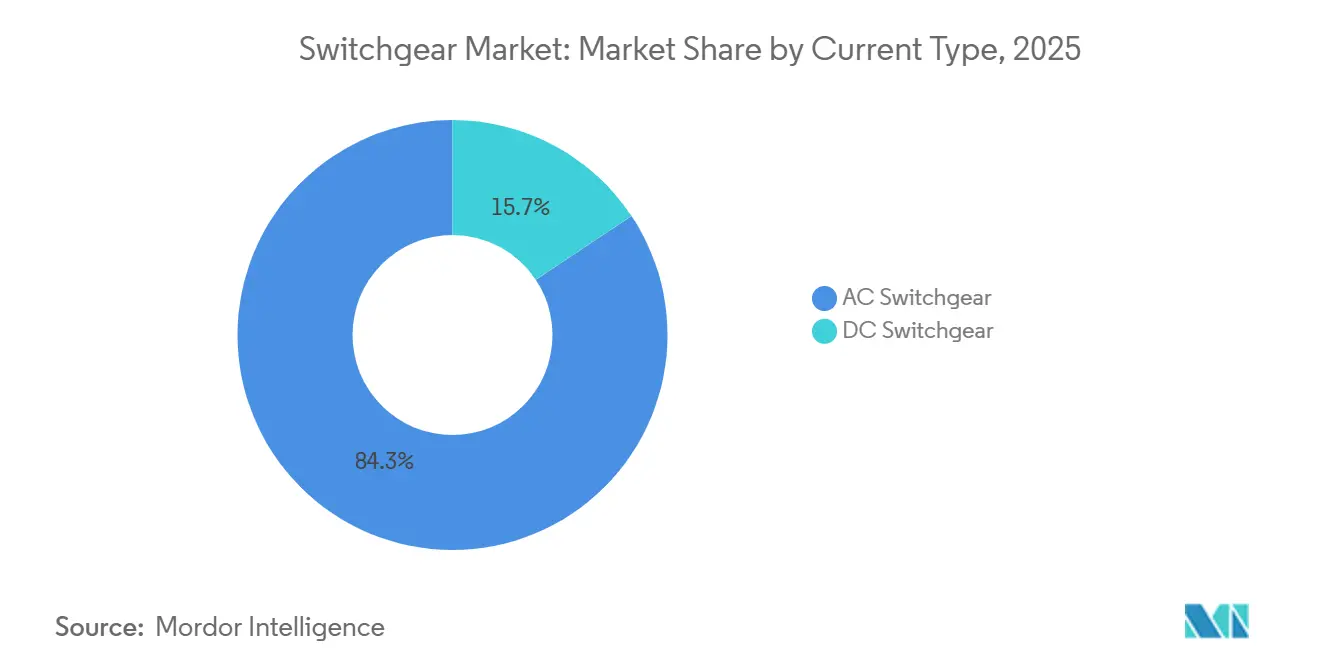

- By current type, AC equipment accounted for 84.34% of 2025 installations, whereas DC switchgear is expected to advance at a 7.11% CAGR on the back of rail and battery-storage projects.

- By installation, indoor configurations held 76.36% of 2025 deployments; outdoor units are expected to advance at an 8.75% CAGR as rural grid-extension programs unfold in the United States.

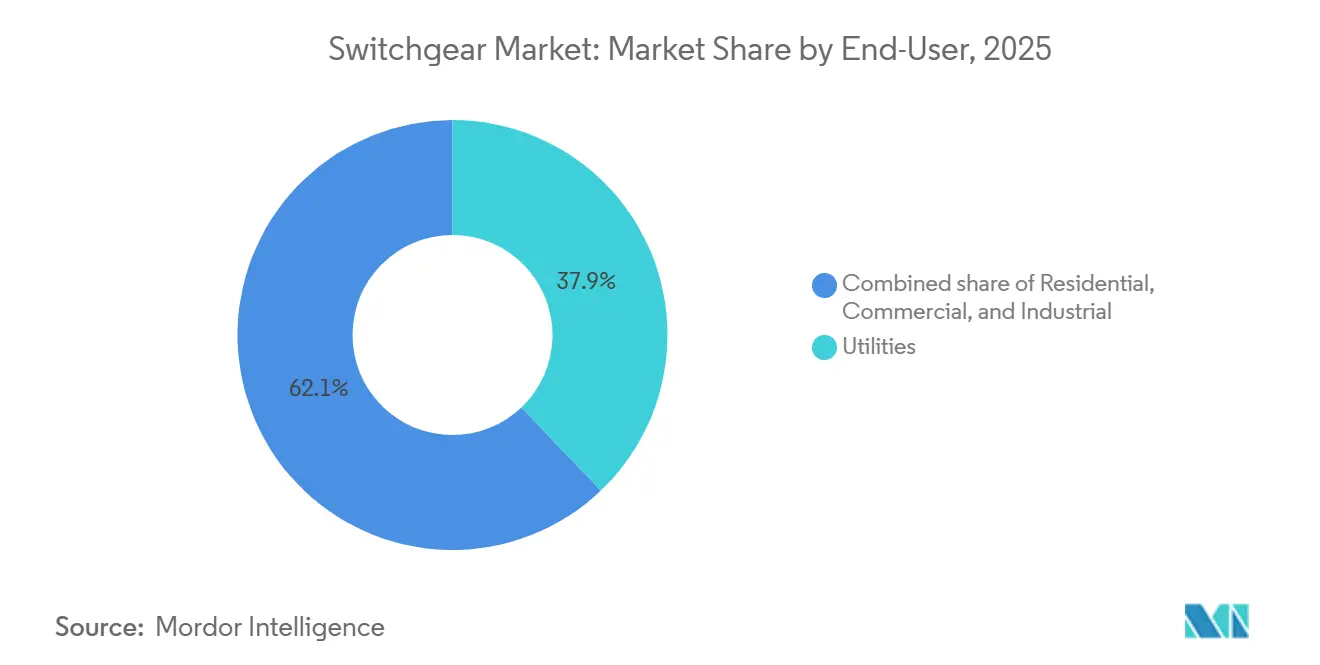

- By end-user, utilities accounted for 37.88% of the 2025 revenue and are also expected to grow at a 6.64% CAGR through 2031.

- By geography, Asia-Pacific led with 47.01% of global revenue in 2025 and is projected to rise at an 8.08% CAGR to 2031 on sustained investment in ultra-high-voltage transmission and smart-meter rollouts.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Data-Center MV Indoor Switchgear Demand in NA and EU | 0.9% | North America & Europe | Medium term (2-4 years) |

| EU F-Gas Phase-Out Accelerating SF₆-Free GIS Procurement | 1.2% | Europe, spill-over to APAC & MEA | Short term (≤ 2 years) |

| India RDSS USD 40 Bn Outlay for Distribution Switchgear 2021-28 | 0.8% | India, with early gains in Uttar Pradesh, Bihar, Rajasthan | Long term (≥ 4 years) |

| Offshore-Wind 66 kV Array-Cable GIS Uptake in East Asia | 0.7% | China, Japan, South Korea | Medium term (2-4 years) |

| US IIJA Grants for Pad-Mounted Grid Modernization | 0.6% | United States, rural & peri-urban areas | Long term (≥ 4 years) |

| GCC Rail Electrification Boosting High-Speed DC Switchgear | 0.5% | Saudi Arabia, UAE, Qatar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Data-Center Medium-Voltage Indoor Switchgear Demand

Hyperscale facilities in Loudoun County and other U.S. hotspots are shifting from 480 V low-voltage panels to 13.8 kV and 34.5 kV line-ups that halve copper mass and cut transformer counts per hall.[3]T&D World, “Data-Center Switchgear Market Analysis,” tdworld.com Schneider Electric’s pure-air SM AirSeT platform removes SF₆ and lowers embodied carbon by 99%, aligning with cloud-provider sustainability targets.[4]Siemens Energy, “Blue GIS Technology,” siemens-energy.com Colocation operators now require IEC 61850 digital interfaces, enabling predictive maintenance that trims unplanned downtime by 30%. The resulting efficiency and sustainability gains accelerate the switchgear market adoption of compact indoor gear across North America and Europe.

EU F-Gas Phase-Out Accelerating SF₆-Free GIS Procurement

Regulation 2024/573 bans SF₆ in new switchgear up to 24 kV from January 2026 and in the 24 kV-52 kV band from 2030. Utilities must replace roughly 1.2 million legacy panels, creating an immediate uptick in the switchgear market for fluoronitrile-based alternatives. ABB secured more than 200 orders for its EconiQ range in 2025, including a 145 kV project that supplies 500,000 Irish households. Siemens Energy’s Blue GIS reached full IEC type approval in 2024 and is now a default requirement in German tenders.

India RDSS USD 40 Billion Outlay for Distribution Switchgear

India’s Revamped Distribution Sector Scheme budgets USD 40 billion to install 250 million smart meters and upgrade 11 kV and 33 kV switchgear by 2028. Aggregate distribution losses fell from 21.91% in FY 2021 to 15.04% in FY 2025, saving roughly 70 billion kWh annually. Local-content rules have driven CG Power to open a plant capable of assembling 1.2 million panels per year, ensuring domestic suppliers capture the expanding switchgear market demand. The grant-loan mix ties disbursements to geotagged milestones, increasing transparency but extending procurement cycles.

Offshore-Wind 66 kV Array-Cable GIS Uptake in East Asia

Developers in China, Japan, and South Korea are moving from 33 kV to 66 kV collection grids that cut resistive losses by up to 15% and reduce the number of required substations. Hitachi Energy supplied a 1 GW Chinese farm with 66 kV SF₆-free GIS in 2025. Japan’s energy ministry now mandates ≥ 66 kV arrays for projects over 500 MW, ensuring alignment with onshore voltages and trimming transformation steps. These standards propel the switchgear market for compact, corrosion-resistant GIS models in marine environments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SF₆-Free Interrupter Capacity Shortage (Lead-Times >72 Weeks) | -0.8% | Global, acute in Europe & North America | Short term (≤ 2 years) |

| Copper and CRGO Price Volatility Pressuring LV OEM Margins | -0.6% | Global, most severe in Asia-Pacific | Medium term (2-4 years) |

| Counterfeit LV Units from Informal Exporters in Africa | -0.3% | Sub-Saharan Africa | Long term (≥ 4 years) |

| Cyber-Security Compliance Costs for IEC 61850 Smart Gear | -0.4% | North America, Europe, APAC utilities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

SF₆-Free Interrupter Capacity Shortage

Lead times for fluoronitrile interrupter chambers now exceed 72 weeks as chemical suppliers scale production under strict environmental permits. Hitachi Energy and Siemens Energy report 18-month backlogs, prompting utilities to pre-order gear 24 months ahead of need and, in some cases, revert to larger air-insulated alternatives despite the footprint penalty. The shortage restrains near-term growth in the switchgear market for SF₆-free GIS even as regulatory bans loom.

Copper and CRGO Price Volatility Pressuring OEM Margins

Copper traded between USD 8,400 and USD 9,500 per ton during 2024-2025, while CRGO steel surpassed USD 3,000 per ton, cutting low-voltage OEM margins by up to 4 percentage points. Manufacturers now renegotiate prices quarterly, and some switch to aluminum busbars for panels under 630 A, accepting a 15% size increase for a 25% cost reduction. Volatility complicates tender pricing and pressures the switchgear market toward designs that minimize raw-material content.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage: High-Voltage Transmission Anchors Long-Distance Renewables

High-voltage equipment is projected to advance at an 8.01% CAGR during 2026-2031, outpacing the 6.15% global switchgear market average. The segment benefits from 132 kV to 765 kV corridors that move renewable power from remote deserts and offshore zones to urban load centers. China commissioned 18 ±800 kV DC lines in 2024-2025, each terminus integrating converter-station breakers with fault-clearing times below 3 ms. In India, 765 kV yards under the Green Energy Corridor Phase II underpin 20 GW of solar and wind integration. Medium-voltage remains the largest revenue contributor, yet its shorter lead times are eroding due to SF₆-free bottle shortages. Low-voltage retains 43.22% of 2025 revenue, though copper volatility narrows margins, prompting simplified designs.

Asia-Pacific favors 220 kV and above to build continental backbones, while North America and Europe retrofit 145 kV and below to modernize aging assets. ABB’s 420 kV live-tank breakers with SF₆-free interrupters entered twelve Scandinavian substations in 2025. Rising reliance on distributed energy resources tempers medium-voltage growth, but the high-voltage tier steadily lifts the overall switchgear market size for transmission applications.

By Insulation: Solid Dielectrics Disrupt Legacy GIS and AIS

Air-insulated switchgear owned 67.79% of 2025 revenue thanks to lower capital cost, yet compact solid-dielectric and vacuum designs are growing at a 14.50% CAGR. Siemens Energy’s 8DJH Blue GIS uses a fluoronitrile-CO₂ mix, occupying 30% less floor area than comparable AIS line-ups. Solid-dielectric switchgear, such as Eaton’s VacClad-W, launched in 2025, eliminates gas handling and achieves IP67 ratings that suit offshore platforms. Lifecycle economics now favor enclosed solutions once real-estate and maintenance savings are tallied, narrowing AIS’s cost edge in the switchgear market. Gas-insulated products face fluoronitrile supply bottlenecks, creating a window for epoxy-resin alternatives, while hybrid configurations mix vacuum interrupters with gas-free busbars to balance cost and footprint.

By Current Type: DC Configurations Gain Traction in Rail and Storage Projects

The AC segment retained 84.34% of 2025 installations, yet DC switchgear is projected to advance at a 7.11% CAGR through 2031 as metro, high-speed rail, battery storage, and data-center operators search for end-to-end direct-current architectures. Gulf Cooperation Council rail corridors specify 1,500 V and 3,000 V breakers able to clear 100 kA faults in 5 ms, while China’s ±800 kV HVDC lines demand metallic-return transfer breakers with highly coordinated protection logic. Rising interest in 380 V server racks is creating proof-of-concept data halls that eliminate one rectification stage and improve power-use effectiveness by 5%. These deployments favor solid-state interrupters that shrink arc-chamber volume and extend mechanical life beyond 30,000 operations. The DC portion of the switchgear market size for rail applications is estimated at USD 3.1 billion in 2026 and is forecast to approach USD 4.7 billion by 2031, equating to an 8.1% CAGR that outpaces the broader market. Hybrid mechanical-electronic breakers lower switching losses to 0.5% of rated current, driving adoption in battery-energy-storage systems that cycle multiple times per day. U.S. data-center pilots in Virginia and Oregon have begun specifying 1,000 A, 380 V DC panels with arc-flash detection that extinguishes faults within 2 ms, a level of performance unattainable with conventional AC gear. Continued rollout of regenerative-braking metro fleets and 150 kW direct-current fast chargers will keep DC growth on a steady upswing in the global switchgear market.

End users still procure AC equipment for grid-connected renewables because synchronous generators and bulk transmission remain overwhelmingly alternating current, but the margin of dominance is narrowing. Manufacturers are responding with dual-rating portfolios in which identical cabinets house either AC or DC interrupters, trimming tooling costs and shortening lead times. The product strategy helps balance factory utilization as order mix evolves. International standards bodies are finalizing coordination rules for 380 V layouts, which should accelerate procurement once codified. As these rules emerge, medium-voltage DC adoption in 10 MW-plus battery parks is expected to surpass 25% of new builds after 2029. This transition sets the stage for a more modular, bidirectional architecture that blurs the historical boundary between substation and load center and enlarges the total addressable switchgear market.

By Installation: Pad-Mounted Units Propel Outdoor Growth

Indoor assemblies held 76.36% of 2025 deployments thanks to compact metal-clad gear in urban substations, commercial towers, and industrial plants. Outdoor configurations are projected to grow at an 8.75% CAGR to 2031, lifted by U.S. undergrounding mandates, India’s rural electrification drive, and Africa’s mini-grid expansion. The United States Infrastructure Investment and Jobs Act earmarked USD 65 billion for grid resilience, enabling municipal utilities in Texas, Florida, and California to replace legacy overhead conductors with underground circuits protected by polymer-housed pad-mounted switchgear rated 15 kV class. Field data show these units cut weather-related outages by 40%, sharply improving service reliability indices and justifying higher up-front cost.

Growth in outdoor systems is also visible in containerized renewable-energy substations, where ISO-frame enclosures integrate a 40 MVA transformer plus 24 kV switchgear and can be commissioned within six weeks, reducing site labor 70% compared with a block-built structure. Asia-Pacific remains the primary market for indoor gear because land scarcity drives utilities to bury 24 kV and 36 kV installations beneath shopping malls and rail stations. Yet even in dense cities, rooftop solar interconnections sometimes require outdoor weather-proofed disconnects that can be retrofitted without structural reinforcement. Rising labor costs are eroding the historical capital-cost gap between air-insulated outdoor yards and gas-insulated indoor halls, nudging procurement managers toward lifecycle evaluations that increasingly favor sealed, factory-assembled pads. As a result, outdoor systems will expand their share of the switchgear market to 28% by 2031, up from 23% in 2025, while indoor growth plateaus.

By End-User: Utilities Double Down on Grid-Hardening Programs

Utilities captured 37.88% of 2025 revenue and are poised to advance at a 6.64% CAGR, slightly above the market average. California’s order to underground 10,000 miles of feeder lines by 2030 drives large lots of 12.47 kV pad-mounted sectionalizers, and similar mandates in Australia and the Philippines will follow. Transmission system operators in Germany and South Korea are specifying IEC 61850 digital bays that link directly to centralized protection schemes, reducing fault-location time from 20 minutes to less than 2 minutes. Residential uptake remains strong in India’s 250 million-unit smart-meter program, which requires service-entrance panels with remote disconnect that trim aggregate technical and commercial losses. Commercial customers raise demand for arc-flash-mitigating molded-case breakers to comply with updated workplace-safety codes, particularly in North America.

Industrial buyers continue modernizing motor-control centers with embedded variable-frequency drives but defer some capital as commodity prices spike, limiting short-term growth. Counterfeit low-voltage imports in parts of Africa slow traction in the formal sector, though recent certification mandates in South Africa and Kenya are expected to restore purchasing confidence. Overall, utilities remain the anchor tenant of the global switchgear market, with spending boosted by government co-funding and climate-resilience budgets. By 2031, the segment is projected to command USD 71.5 billion of annual demand, representing 38% of the switchgear market size, while residential and commercial segments together add another 5 percentage-point share as electrification of heat and transport accelerates.

Geography Analysis

Asia-Pacific accounted for 47.01% of 2025 revenue, and aggressive ultra-high-voltage transmission corridors, smart-meter rollouts, and offshore-wind collection grids keep the region on an 8.08% CAGR path. China energized 18 ±800 kV DC lines through 2025, each terminal requiring converter-station switchgear with 3 ms clearing times, while India’s USD 40 billion RDSS targets 11 kV and 33 kV ring-main replacements across 28 states. Japan and South Korea specify 66 kV subsea GIS for 15 MW turbines, expanding demand for corrosion-resistant, SF₆-free designs. Australia’s 330 kV reinforcements in New South Wales underpin rooftop-solar back-feed management. Altogether, the region will surpass USD 90 billion in annual sales by 2031, strengthening its hold on the global switchgear market share.

Europe ranks second and benefits from Regulation 2024/573, which bans SF₆ in medium-voltage equipment up to 24 kV from January 2026. Utilities must swap roughly 1.2 million panels within five years, ensuring a steady retrofit pipeline. Offshore-wind interconnections in the North Sea, Baltic, and Celtic Sea create incremental 132 kV and 220 kV GIS demand, while HVDC backbones such as NordLink and NeuConnect require ±525 kV DC switch-yards. Southern Europe’s progress is slower as fiscal headroom remains tight, but Iberian solar deployments lift mid-voltage orders. Europe’s overall growth of 5.3% CAGR lags Asia-Pacific yet still adds USD 13 billion in new annual revenue by 2031.

North America grows at 5.9% CAGR, powered by the Infrastructure Investment and Jobs Act’s USD 65 billion grid budget. California alone will install thousands of pad-mounted switchgear cabinets to mitigate wildfire risk, and ERCOT’s 4 GW battery boom mandates 34.5 kV collector systems. Canada’s Atlantic Loop upgrades 230 kV interties, and Mexico seeks 115 kV and 230 kV modernizations to connect 12 GW of renewables, though procurement faces budget and permitting latency. South America rides Brazil’s 3,800 km transmission auction and Chile’s Atacama solar exports, while the Middle East and Africa see localized spikes from GCC rail electrification and South African substation retrofits. Collectively, these regions account for 17% of 2025 revenue and will edge toward 19% by 2031.

Competitive Landscape

Global supply is moderately concentrated: Schneider Electric, Siemens Energy, ABB, Mitsubishi Electric, and Eaton together control about 45% of 2025 revenue. Strategic priorities center on SF₆-free launches, digital-service ecosystems, and vertical integration into fluoronitrile chemistry. Schneider Electric’s purchase of Motivair couples medium-voltage switchgear with liquid cooling, enabling turnkey 100 MW data-hall blueprints that reduce the total cost of ownership 12%. Siemens Energy’s 3M tie-up secures low-GWP gas supply, while ABB’s Ability platform aggregates live condition-monitoring data from 50,000 panels worldwide, cutting unplanned outages 25% and locking utilities into multi-year analytics contracts.

Chinese challengers XD Electric and Pinggao leverage domestic ±800 kV DC experience to export price-competitive breakers to Belt and Road markets. Indian firms CG Power and Havells ramp capacity under local-content mandates, pursuing Middle East tenders that require regionally built 11 kV and 33 kV units. Niche players such as NOJA Power dominate reclosers in Australia, and Powell Industries supplies custom 15 kV metal-enclosed gear to North American petrochemical plants. Compliance with IEC 62351 cybersecurity rules now appears in most utility RFQs, raising entry hurdles for vendors lacking digital-security expertise.

Margin pressure comes from copper and CRGO cost spikes, which sliced 2-4 percentage points off low-voltage product margins in 2025. Suppliers counter with redesigned aluminum busbars and remote-factory-acceptance testing that saves travel costs. Lead-time risk on fluoronitrile interrupters remains a wild card, prompting long-term chemical supply contracts and regional assembly hubs. As a result, merger-and-acquisition chatter surrounds medium-sized firms with solid-dielectric patents that could plug technology gaps for the top five. The switchgear industry is therefore on a consolidation trajectory likely to raise the combined top-five share above 50% by 2028.

Switchgear Industry Leaders

Schneider Electric

Mitsubishi Electric Corporation

Siemens AG

ABB Ltd

Havells India Limited.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: ABB India introduced the ArTu Formula Low Voltage Switchgear, a modular and IEC-compliant solution designed to enhance power distribution across industrial, infrastructure, commercial, and residential applications. This product integrates with ABB’s existing portfolio to improve reliability, safety, and operational control, addressing India’s increasing electrification demands.

- March 2025: nVent Electric announced and subsequently completed the acquisition of the Electrical Products Group from Avail Infrastructure Solutions. This acquisition added critical switchgear, enclosures, and bus systems to nVent’s portfolio, strengthening its position in high-growth power infrastructure sectors such as utilities and data centers.

- March 2025: Avail Infrastructure Solutions’ parent company announced the divestiture of its electrical products division, including switchgear and bus systems, to nVent for USD 975 million. This move reflects consolidation within the switchgear supply chain and enables nVent to expand its product offerings in electrification markets.

- February 2025: Lauritz Knudsen Electrical and Automation (formerly L&T Switchgear) showcased a comprehensive range of switchgear and automation solutions at ELECRAMA 2025. The highlights included advanced air circuit breakers and MCCBs with digital integration, catering to industrial, infrastructure, retail, home, and agricultural applications.

Global Switchgear Market Report Scope

Switchgear plays a pivotal role in safeguarding power systems. It regulates electrical circuits, manages power distribution, and facilitates testing and maintenance by de-energizing equipment. Key components of switchgear include circuit breakers, isolators, relays, switches, fuses, and control panels.

The switchgear market is segmented by voltage (low-voltage, medium-voltage, and high-voltage), insulation (gas-insulated switchgear (GIS), air-insulated switchgear (AIS), and other insulation types), current type (AC and DC), installation (indoor and outdoor), end-user (utilities, residential, commercial, and industrial), and geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Low Voltage |

| Medium Voltage |

| High Voltage |

| Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) |

| Others |

| AC Switchgear |

| DC Switchgear |

| Indoor |

| Outdoor |

| Utilities |

| Residential |

| Commercial |

| Industrial |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Voltage | Low Voltage | |

| Medium Voltage | ||

| High Voltage | ||

| By Insulation | Gas Insulated Switchgear (GIS) | |

| Air Insulated Switchgear (AIS) | ||

| Others | ||

| By Current Type | AC Switchgear | |

| DC Switchgear | ||

| By Installation | Indoor | |

| Outdoor | ||

| By End-User | Utilities | |

| Residential | ||

| Commercial | ||

| Industrial | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of global switchgear demand in 2031?

The switchgear market size is forecast to reach USD 187.95 billion by 2031, expanding at a 6.15% CAGR from 2026.

Which insulation technology is growing fastest?

Solid-dielectric and other SF6-free designs are advancing at a 14.50% CAGR as utilities prioritize compact, environmentally compliant gear.

How will the EU SF6 ban affect procurement?

Regulation 2024/573 forces replacement of about 1.2 million medium-voltage panels, sharply boosting European demand for fluoronitrile or pure-air GIS from 2026 onward.

Why is DC switchgear gaining attention?

Rail electrification, 380 V data-center pilots, and battery storage rely on direct current, pushing DC switchgear orders to a 7.11% CAGR through 2031.

Which region leads growth over the forecast period?

Asia-Pacific, driven by China's ultra-high-voltage lines and India's USD 40 billion RDSS scheme, is slated for an 8.08% CAGR to 2031.

What challenges could restrain near-term expansion?

Lead-times exceeding 72 weeks for SF6-free interrupters and raw-material price volatility hamper the market growth.

Page last updated on: