Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.17 Billion |

| Market Size (2031) | USD 2.80 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

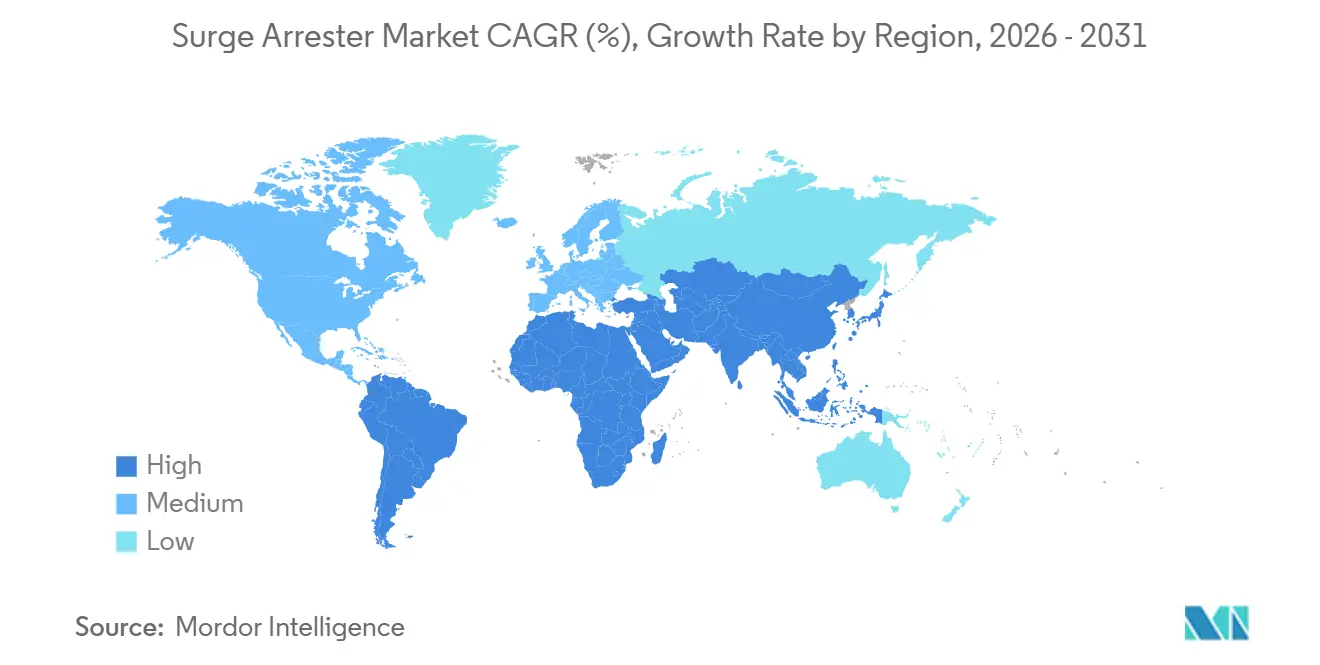

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Surge Arrester Market Analysis by Mordor Intelligence

The Surge Arrester market size is expected to grow from USD 2.06 billion in 2025 to USD 2.17 billion in 2026 and is forecast to reach USD 2.8 billion by 2031 at 5.23% CAGR over 2026-2031.

Rising grid modernization investments, aggressive renewable integration, and stricter reliability targets are keeping the Global surge arrester market on a firm expansion path. Digitization trends now require arresters with built-in health monitoring, while supply-chain resilience remains a top-level priority following recent price swings of metal-oxide varistors. Utilities in North America and Europe are adopting digital twin models to optimize replacement cycles, whereas utilities in the Asia-Pacific region are pushing extra- and ultra-high-voltage deployments that stretch product performance envelopes. Competitive moves center on product differentiation, higher energy ratings, compact footprints, and IoT connectivity, yet OEMs must also counter the rising tide of counterfeit devices entering price-sensitive economies.

Key Report Takeaways

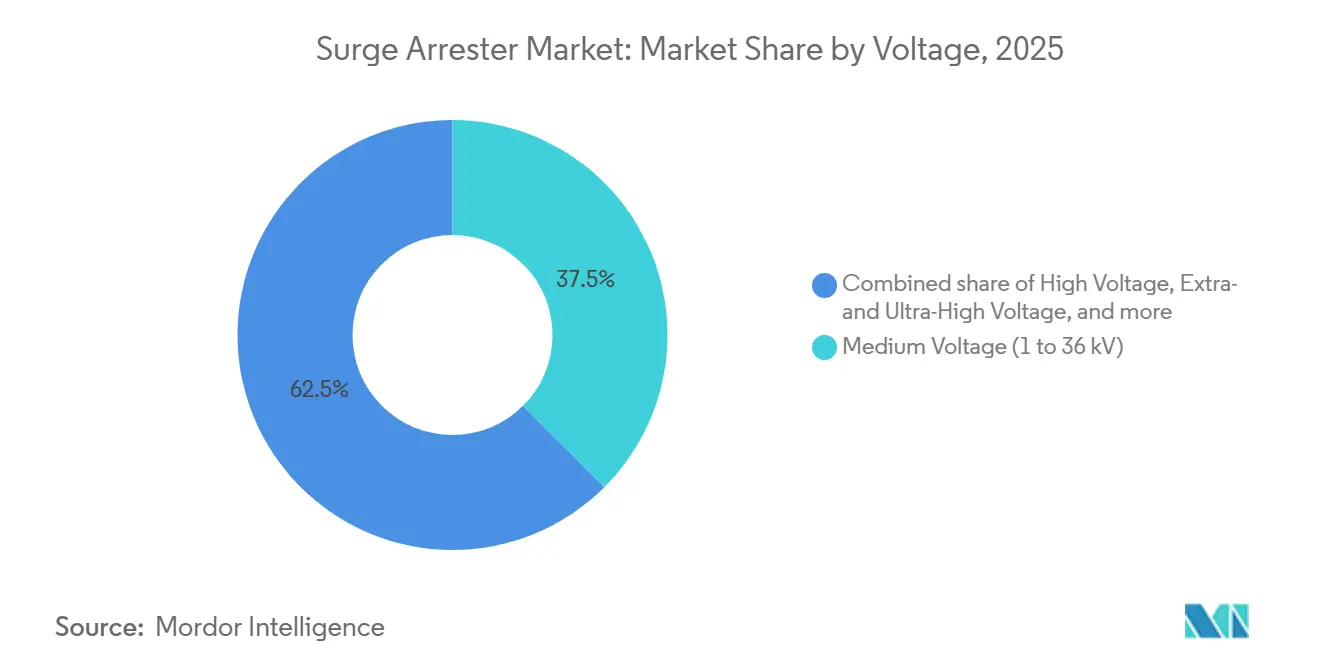

- By voltage rating, medium-voltage arresters held a 37.52% market share of the surge arrester market in 2025. Extra- and ultra-high-voltage arresters are projected to expand at a 6.74% CAGR between 2026-2031.

- By product type, station-class units accounted for a 41.95% revenue share of the surge arrester market size in 2025. Line arresters represent the fastest-growing product category, advancing at a 7.18% CAGR through 2031.

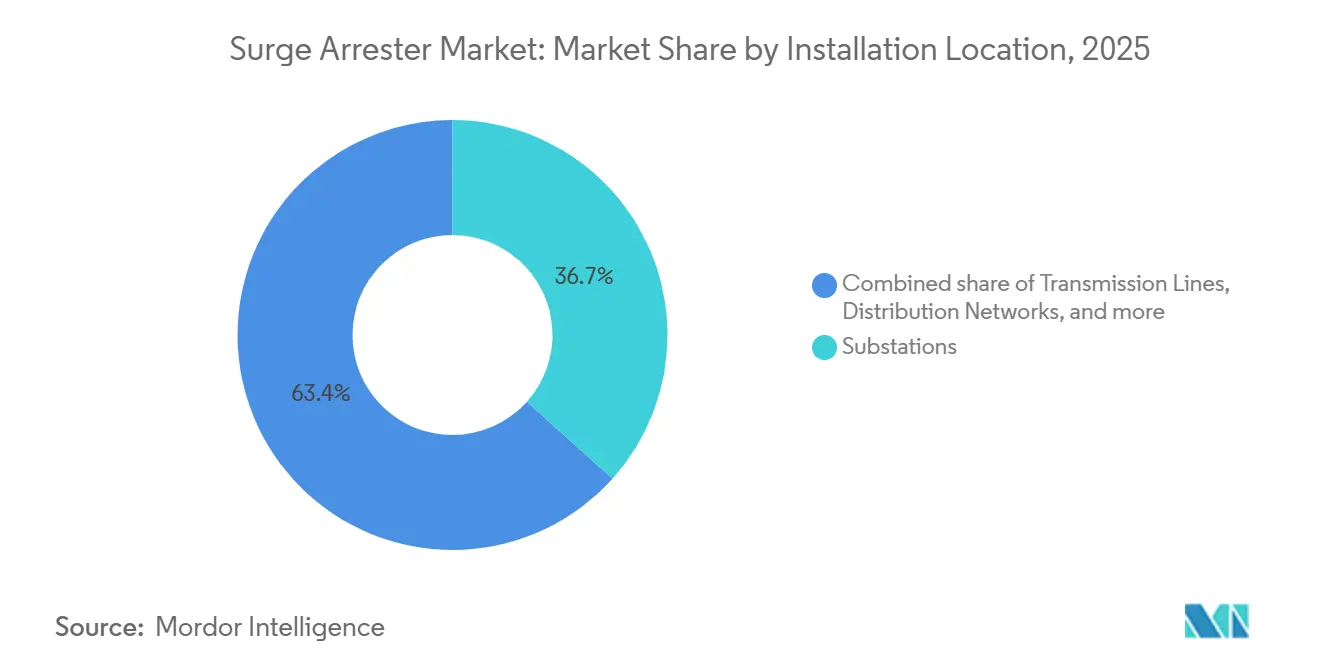

- By installation location, substations accounted for 36.65% of the surge arrester market size in 2025, whereas transmission lines are expected to expand at a 6.92% CAGR.

- By application, the utilities segment captured 53.35% of the surge arrester market size in 2025, while the residential segment is projected to grow at a 6.12% CAGR.

- By geography, the Asia-Pacific region commanded 41.05% of the Global surge arrester market in 2025 and is expected to post a 5.82% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Surge Arrester Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid modernisation programmes in North America & EU | 1.20% | North America & EU | Medium term (2-4 years) |

| Utility-scale renewable capacity additions requiring over-voltage protection | 1.00% | Global, concentration in APAC & EU | Long term (≥ 4 years) |

| Electrification of industrial processes in emerging Asia | 0.80% | APAC, spill-over to MEA | Medium term (2-4 years) |

| Rapid build-out of EV fast-charging corridors | 0.60% | Global, early adoption in North America & EU | Short term (≤ 2 years) |

| Surge arrester retrofits in offshore wind substations | 0.40% | North America & EU coastal regions | Medium term (2-4 years) |

| Digital twin-enabled asset-health monitoring boosting replacement demand | 0.30% | Global, led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid Modernisation Programmes in North America & EU

Utility regulators across both regions allocate multibillion-dollar budgets to harden aged grids against severe weather, elevating demand for station-class arresters with online condition sensors. Projects such as Entergy Texas’s USD 335 million line-reinforcement scheme pair surge-protection upgrades with federal resilience funding, illustrating how reliability mandates translate directly into purchase orders. Predictive maintenance, powered by leakage-current analytics, now informs arrester replacement schedules, enabling utilities to avoid catastrophic failures while managing capital expenditures. At the same time, the increasing use of renewable interconnections escalates switching-surge frequency, forcing tighter coordination between arresters, breakers, and shunt reactors. As a result, the Global surge arrester market receives a pronounced boost from digital-ready hardware aligned with North American and European grid-code updates.[1]“Entergy Texas Strengthens Lines,” T&D World, tdworld.com

Utility-Scale Renewable Capacity Additions Requiring Over-Voltage Protection

Wind and solar developers specify arresters across collection systems, substations, and export cables to safeguard inverters and transformers from lightning and switching surges. Offshore wind farms pose a heightened risk; measured temporary overvoltages can reach levels that threaten cable insulation unless mitigated. Technical studies show arresters cut those overvoltages by 68.3%, with even greater reductions when paired with pre-insertion resistors, underscoring the need for coordinated protection schemes. As governments double their renewable targets to meet 2030 climate goals, medium-voltage switchgear and the associated surge-protection hardware are experiencing double-digit growth. Consequently, component suppliers scaling high-energy MOV technologies capture an additional share of the Global surge arrester market.[2]B. De Andrade et al., “Temporary Over-Voltage Mitigation in Offshore Wind Farms,” IEEE Access, ieee.org

Electrification of Industrial Processes in Emerging Asia

Manufacturers transitioning from fossil-fuel boilers to electric heaters often encounter frequent voltage fluctuations, resulting in production losses that can exceed USD 25,000 per month for some plants. Surge-protection retrofits, therefore, migrate from optional to critical-path investments. China’s automation push drives demand for medium-voltage arresters that handle high-frequency transients generated by variable-frequency drives, while India’s incentive programs foster electronics clusters that require low-pollution, corrosion-resistant devices. Suppliers able to package arresters with filters and isolation transformers gain an edge. These orders underpin the Global surge arrester market outlook for industrial segments across ASEAN and South Asia.[3]Reinhausen, "Asian industry uses voltage regulation distribution transformers in the fight against fluctuating grids," reinhausen.com

Rapid Build-Out of EV Fast-Charging Corridors

Public DC fast chargers are susceptible to lightning, grid-switching, and internal fault surges on both the AC input and DC output. Standards lag equipment rollouts, giving arrester makers a window to define best practice. Device launches such as Bourns’ 1500 VDC Class I+II modules illustrate product adaptation to higher-voltage DC. Thermal-disconnect designs and compact footprints suit roadside enclosures, aiding safe uptime. As charging-corridor density rises, tailored protection shifts more revenue into the Global surge arrester market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| Volatile prices of metal-oxide varistors | -0.80% | Global, concentrated in manufacturing regions |

| Fragmented IEC & IEEE testing standards across regions | -0.50% | Global, affecting multinational manufacturers |

| Project delays in long-distance UHV transmission lines | -0.40% | APAC core, spill-over effects globally |

| Counterfeit low-cost products eroding OEM margins | -0.30% | Emerging markets, particularly Asia & MEA |

| Source: Mordor Intelligence | ||

Volatile Prices of Metal-Oxide Varistors

Zinc oxide accounts for the majority of varistor weight, so fluctuations in mine output and tighter environmental regulations drive cost swings that squeeze margins, especially on low-voltage units sold through competitive tenders. Some OEMs redesign formulations to reduce ZnO content; however, qualification cycles are still lengthy. Short-term volatility, therefore, trims profitability, modestly slowing procurement across the Global surge arrester market.

Fragmented IEC & IEEE Testing Standards Across Regions

Parallel compliance regimes force dual design and test programs. IEC 61643-01 emphasizes lightning-impulse performance, whereas IEEE C62.11 focuses on switching-surge energy ratings. Multinational suppliers often need to maintain duplicate product lines, which inflates costs and extends the time-to-market. Until greater harmonization emerges, this complexity restricts economies of scale within the Global surge arrester market.[4]“Surge Protective Device Standards,” International Electrotechnical Commission, iec.ch

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage: Driving UHV Technical Innovation

Extra- and ultra-high-voltage arresters are projected to grow at the fastest rate, with a 6.74% CAGR, as interregional renewable transfers demand voltages of ±800 kV and above. Medium-voltage devices still anchor 37.52% of the Global surge arrester market in 2025, providing backbone protection for distribution feeders that serve industrial parks and dense urban loads. Complex varistor stacks and silicone housings designed for 330 kV-plus duties continue to trickle down into lower-voltage offerings, improving thermal stability across the board. China’s 1,901 km ±800 kV UHVDC line underscores technical feasibility and stimulates export interest in similar corridors across South Asia and Africa.

By Product Type: Line Arresters Gain Transmission Traction

Station-class arresters delivered 41.95% of the revenue in 2025, while line arresters advanced at a 7.18% CAGR as utilities quantified outage reductions that outweighed the installation cost. Gapless polymer-housed designs, combined with vibration-resistant clamps, speed up retrofit campaigns on existing 220 kV lines. Field data from CIGRE confirms significant lightning-outage cuts, reinforcing the adoption curve across the Global surge arrester market.

By Installation Location: Transmission Lines Accelerate Adoption

Substations retained a 36.65% share in 2025, but transmission-line applications expanded at a 6.92% CAGR due to renewed reliability focus. Remote monitoring modules now relay arrester temperature and leakage current via cellular links, enabling helicopter-free inspections on mountain spans. Such advances widen opportunity size within the Global surge arrester market, particularly in regions with long overhead corridors.

By Application: Residential Segment Powers Smart-Home Growth

Utility networks held a 53.35% share in 2025; nonetheless, residential adoption posted a brisk 6.12% CAGR as smart-home electronics grew. Insurance data highlighting USD 825 million in lightning damage to U.S. households catalyzes code revisions that mandate the use of Type 1 or Type 2 devices at service entrances. That policy backdrop injects fresh momentum into the Global surge arrester market for low-voltage units.

Geography Analysis

The Asia-Pacific region led with a 41.05% share of the Global surge arrester market in 2025 and is predicted to expand at a 5.82% CAGR. China’s State Grid alone invested over 500 billion yuan in smart-grid rollouts during 2024, with UHV lines absorbing a sizeable arrester budget. India’s electrification drives add medium-voltage demand, while Japan’s long record of 66-1100 kV installations supplies application know-how.

North America registers steady gains as federal-state grid-modernization alliances release funding tranches tied to resilience metrics. Offshore-wind buildouts along the Atlantic spur marine-grade arrester purchases, and Canada’s USD 1.4 trillion grid-upgrade roadmap secures long-term replacement cycles, each reinforcing North America’s contribution to the Global surge arrester market.

Europe emphasizes digital monitoring and harmonized protection practices under EN 50539, and Mediterranean offshore wind cables add a challenging salt-spray environment. South America, plus the Middle East & Africa, comprise emerging pockets; mining and petrochemical projects create site-specific surges, but procurement often favors ruggedized, proven models over feature-rich units, moderating yet not negating growth within the Global surge arrester market.

Competitive Landscape

The market remains moderately consolidated. ABB, Siemens Energy, and Hitachi Energy continue to dominate high-voltage niches by pairing deep R&D pipelines with global service fleets. These leaders integrate IoT sensors into polymer-housed arresters to shore up differentiation. Mid-tier players like Eaton and TE Connectivity expand their portfolios through targeted acquisitions: TE’s November 2024 acquisition of Harger adds lightning-grounding breadth that complements its arrester line. Counterfeit proliferation, particularly in certain parts of Asia, pressures pricing at the lower end and compels OEMs to invest in traceability and QR-coded product passports. Strategic alliances between EPC contractors and renewable developers are increasingly influencing contract awards, nudging the Global surge arrester market toward ecosystem-based competition.

Surge Arrester Industry Leaders

-

ABB Ltd

-

Siemens AG

-

Hitachi Energy Ltd.

-

Eaton Corporation plc

-

DEHN SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: China has completed its ±800 kV Jinsha River–Hubei UHVDC line, which transmits 36 billion kWh annually and necessitates specialized high-energy arresters.

- November 2024: TE Connectivity acquired Harger to deepen its grounding and lightning-protection expertise.

- August 2024: Bourns launched 1,500 VDC Class I+II surge-protective devices designed for EV charging stations.

- July 2024: Construction began on the Gansu-Zhejiang flexible ±800 kV UHVDC link valued at USD 4.82 billion.

Global Surge Arrester Market Report Scope

The surge arrester market report include:

By Voltage

| Low Voltage (Up to 1 kV) |

| Medium Voltage (1 to 36 kV) |

| High Voltage (36 to 330 kV) |

| Extra and Ultra High Voltage (Over 330 kV) |

By Product Type

| Station-Class Arresters |

| Distribution-Class Arresters |

| Intermediate-Class Arresters |

| Line Arresters |

By Installation Location

| Substations |

| Transmission Lines |

| Distribution Networks |

| Power-Generation Facilities |

| Industrial Machinery and Process Plants |

By Application

| Utilities |

| Industrial |

| Commercial |

| Residential |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Voltage | Low Voltage (Up to 1 kV) | |

| Medium Voltage (1 to 36 kV) | ||

| High Voltage (36 to 330 kV) | ||

| Extra and Ultra High Voltage (Over 330 kV) | ||

| By Product Type | Station-Class Arresters | |

| Distribution-Class Arresters | ||

| Intermediate-Class Arresters | ||

| Line Arresters | ||

| By Installation Location | Substations | |

| Transmission Lines | ||

| Distribution Networks | ||

| Power-Generation Facilities | ||

| Industrial Machinery and Process Plants | ||

| By Application | Utilities | |

| Industrial | ||

| Commercial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Global surge arrester market?

The market reached USD 2.17 billion in 2026 and is forecast to grow to USD 2.8 billion by 2031.

Which region leads surge arrester demand?

Asia-Pacific held 41.05% share in 2025, driven by China’s ultra-high-voltage projects and India’s distribution upgrades.

Which product segment is expanding fastest?

Line arresters are projected to grow at 7.18% CAGR through 2031 owing to their effectiveness in cutting lightning-induced outages.

How will renewable energy integration influence arrester purchases?

Utility-scale wind and solar sites require extensive over-voltage protection, adding roughly 1.0 percentage point to overall market CAGR.

Why are counterfeit surge arresters a concern?

They erode OEM pricing power and pose safety risks, especially in emerging markets, trimming expected market growth by an estimated 0.3 percentage point.

Page last updated on: