Electrical Fuses Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.55 Billion |

| Market Size (2030) | USD 5.78 Billion |

| Growth Rate (2025 - 2030) | 4.92% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrical Fuses Market Analysis by Mordor Intelligence

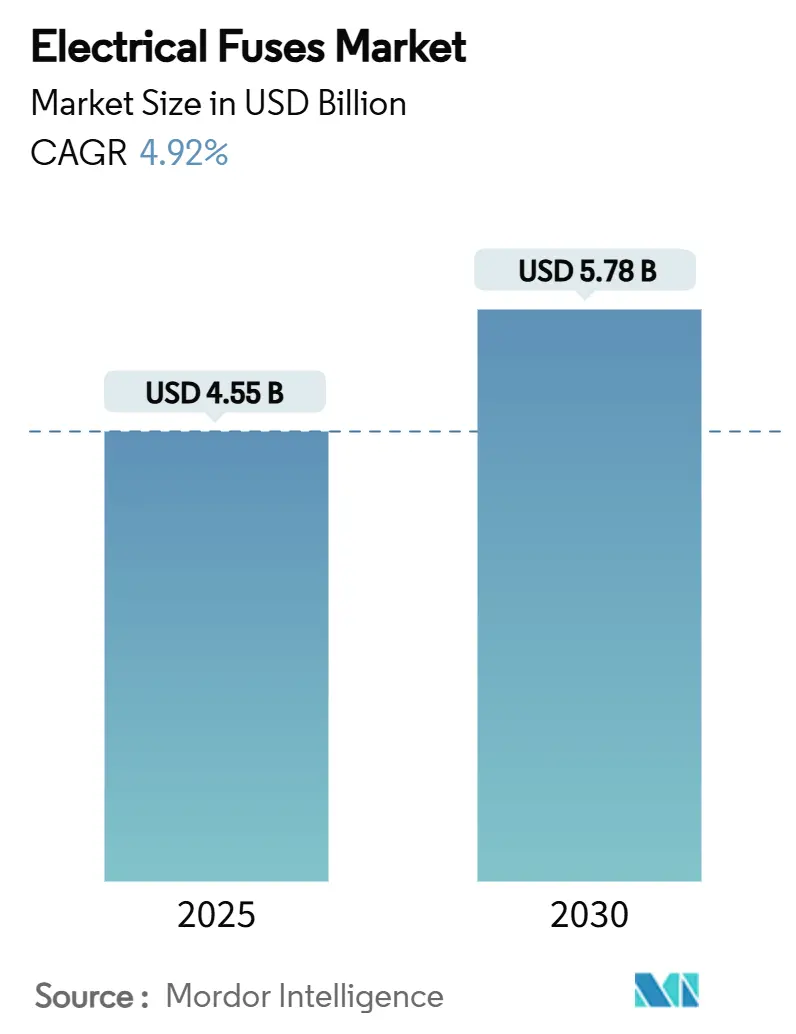

The electrical fuses market size is estimated at USD 4.55 billion in 2025 and is projected to reach USD 5.78 billion in 2030, growing at a 4.92% CAGR, underscoring healthy long-term momentum for circuit-protection products. The shift from conventional one-time protection toward intelligent, application-specific solutions is reshaping competitive dynamics. Grid modernization programs, the surge in electric vehicle platforms, and accelerated renewable energy deployments collectively expand the electrical fuses market, while supply chain stress favors manufacturers with diversified footprints. Self-resetting PTC technologies, semiconductor-grade fast-acting designs, and IoT-enabled status monitoring differentiate premium offerings. Meanwhile, established low-voltage products maintain volume leadership, reflecting the need to serve legacy installations even as high-voltage applications grow at a faster rate.

Key Report Takeaways

- By product type, power fuses and fuse links led with 33.7% revenue share in 2024, while resettable PTC devices are advancing at a 5.8% CAGR to 2030, reshaping the electrical fuses market share profile.

- By voltage class, low-voltage devices (<1 kV) accounted for 46.5% of the electrical fuses market size in 2024; high-voltage designs (>69 kV) posted the fastest CAGR at 5.6% through 2030.

- By end-user, utilities held 26.9% of the 2024 electrical fuses market, whereas the transportation sector is expanding at a 6.1% CAGR, driven by EV adoption.

- By fuse speed, time-delay products captured 46.3% of the electrical fuses market share in 2024, while semiconductor-grade fast-acting fuses are growing at a 6.2% CAGR.

- By form factor, blade fuses dominated with a 41.20% share in 2024; however, SMD chip fuses are scaling at a 5.60% CAGR, reflecting the trend of electronics miniaturization.

- By geography, the Asia Pacific region dominated the electrical fuses market with a 42.60% share in 2024; North America is poised for a 5.70% CAGR through 2030.

Global Electrical Fuses Market Trends and Insights

Driver Imapct Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Modernization Investments | +1.2% | North America, Asia-Pacific, Europe | Medium term (2-4 years) |

| Electronics Content in EVs and Chargers | +1.5% | China, North America, Europe | Short term (≤2 years) |

| Renewable-Energy Capacity Additions | +0.9% | Asia-Pacific, Europe | Long term (≥4 years) |

| Data-Centre HV-DC Architectures | +0.8% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Smart Self-Resetting Fuse Technologies | +0.6% | Developed markets globally | Long term (≥4 years) |

| Electrification of Off-Grid Micro-Utilities | +0.3% | Sub-Saharan Africa, broader Middle East and Africa | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Investments in Grid Modernisation

Utilities are upgrading aging networks to manage bidirectional power flows from renewables and distributed resources, which elevates demand for high-reliability overcurrent protection. The International Energy Agency reports that transformer prices climbed 75% and cable costs doubled since 2021, extending asset-replacement cycles and raising the criticality of robust fusing solutions. Smart-grid rollouts increasingly specify fuses equipped with condition-monitoring interfaces to coordinate with digital relays. Government infrastructure budgets in the United States and India sustain multi-year procurement pipelines, supporting predictable growth for the electrical fuses market.

Surging Electronics Content in EVs and xEV Chargers

Battery-electric vehicles rely on compact 500–1,000 V DC fuses rated up to 50 kA, while charging stations demand fast-acting devices tailored to Level 3 400 A outputs[1]Aite Fuse editorial team, “What Is EV Fuse and What Is the Fuse Size for an Electric Car Charger,” Aite Fuse, Jun 5, 2024, aitefuse.com. Automakers are shifting toward 800 V platforms to cut charging time, drive heightened adoption of semiconductor-grade fuses such as Littelfuse’s EV1K series. This dynamic accelerates the electrical fuses market as OEMs seek purpose-built circuit protection that balances thermal limits with compact footprints.

Accelerated Renewable-Energy Capacity Additions

Photovoltaic arrays now incorporate 1,500 V strings, prompting demand for DC-rated fuses like Bourns’ POWrFuse high-power series. Wind-farm inverters and battery-energy-storage integrations complicate fault-current profiles, spurring utilities to specify adaptive protection curves. As renewables scale, specialized fuses become essential in safeguarding inverters against reverse-current damage, boosting premium demand within the electrical fuses market.

Expansion of Data-Centre HV-DC Architectures

Hyperscale facilities migrate to 380 V DC buses to trim conversion losses, necessitating ultra-fast DC interrupting devices that suppress high-energy arcs without natural zero-crossings. ABB’s July 2025 SACE Emax 3 breaker launch illustrates how OEMs incorporate cybersecurity into protection hardware for mission-critical loads. Such requirements elevate average selling prices and widen the addressable electrical fuses market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Resettable Breakers in LV Panels | -0.8% | Developed markets globally | Medium term (2-4 years) |

| Delays in Large Grid-Upgrade Projects | -0.5% | North America, Europe | Short term (≤2 years) |

| Thermal-Management Limits from Miniaturisation | -0.3% | Global electronics sector | Long term (≥4 years) |

| Proliferation of Counterfeit, Low-Quality Parts | -0.2% | Emerging markets, online channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Resettable Breakers in LV Panels.

Industrial and commercial users increasingly select electronic breakers that trip and reset remotely, cutting labor costs linked to fuse replacement. Siemens’ SENTRON ECPD device, introduced in March 2024, operates up to 1,000 times faster than traditional overcurrent gear while offering diagnostic connectivity. Such capabilities erode low-voltage volume prospects for the electrical fuses market, though the inherent speed and cost advantages of fuses retain relevance in high-fault scenarios.

Project Delays in Large Grid-Upgrade Programs

Complex permitting processes and disjointed inter-regional planning are hindering the timely execution of grid upgrades, subsequently disrupting the procurement cycles for electrical fuses. As the U.S. aims for expansion in its transmission capacity to achieve net-zero targets, regulatory hurdles are undermining the certainty of these schedules. Such delays lead to unpredictable demand fluctuations, complicating inventory management and production forecasting for manufacturers and suppliers of electrical fuses in utility-centric markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Resettable devices upend power-fuse dominance

The electrical fuses market size for power fuses and fuse links was bolstered by their 33.7% share in 2024, reflecting established use in utility switchgear and industrial drives. Despite stable unit demand, revenue growth is moderate because buyers increasingly evaluate total-lifecycle cost rather than replacement price alone. Resettable PTC fuses, expanding at a 5.8% CAGR, cater to consumer electronics and EV subsystems where downtime carries a premium. This segment benefits from polymer-science improvements, delivering narrower trip tolerances and faster reset times. Specialty surface-mount fuses extend design flexibility, enabling OEMs to meet space constraints in power-dense modules without sacrificing interrupting ratings. The co-existence of disposable and self-healing technologies positions the electrical fuses market for balanced growth across legacy and emerging applications.

Power fuse producers defend their share through materials innovations such as sand-filled ceramic barrels that enhance arc-quenching efficiency. Yet margin pressure persists because customers weigh replace-once strategies against breaker retrofits. In contrast, PTC suppliers pitch eco-credentials, emphasizing reduced waste and lower field-service emissions. The juxtaposition of these value propositions underscores a two-track evolution inside the electrical fuses market.

By Voltage Range: High-voltage surge starts to challenge LV supremacy

Low-voltage products retained 46.5% of the electrical fuses market share in 2024, anchored in residential panels, commercial buildings, and machinery control centers. Growth moderates as construction cycles plateau in mature economies, but refurbishment and safety-code updates sustain baseline demand. Medium-voltage fuses, integral to 1–69 kV feeders, capture incremental upside from substation digitalization projects that call for coordinated protection schemes. High-voltage (>69 kV) devices grow 5.6% CAGR through 2030, benefiting from HVDC links connecting offshore wind parks and long-haul renewable corridors. The high-price, low-volume nature of these fuses elevates revenue contribution disproportionate to unit shipments, improving average selling prices across the electrical fuses market size landscape.

Technical complexity in >69 kV applications favors incumbents with vertical integration of silver-alloy elements and precision ceramic processing. Qualification cycles exceeding two years and stringent utility test protocols deter new entrants, reinforcing competitive moats. Nevertheless, rising grid-interconnection mandates enlarge the accessible pool, gradually diluting low-voltage dominance in the electrical fuses market.

By End-User Industry: Transportation speeds ahead

Utilities continued to represent the single-largest buying center at 26.9% in 2024, yet the 6.1% CAGR posted by transportation signals structural rebalancing. Electric-vehicle platforms adopt multiple fuse nodes-battery pack, inverter input, on-board charger, and auxiliary circuits-multiplying unit demand per vehicle. Rail electrification and metro-line expansions add further impetus, with suppliers such as Mersen providing integrated fuse boxes and collector assemblies[2]T&D World staff, “ABB to Invest USD 120 Million in U.S. to Expand Production Capacity of Low Voltage Electrification Products,” T&D World, Mar 5, 2025, tdworld.com. Industrial manufacturing maintains steady ordering to protect drives and robotics, while residential and commercial retrofit programs create consistent low-voltage pull-through. Renewable power plants introduce specialized DC fuse needs, though volumes remain niche. Collectively, these dynamics diversify the electrical fuses market and insulate participants from single-sector downturns.

Automotive tier-ones increasingly co-design fuses with OEM power-electronics teams to tailor ultra-fast clearing characteristics that safeguard silicon-carbide devices. This collaborative model accelerates design-win cycles and tightens supply relationships, establishing transportation as a technology catalyst within the electrical fuses market.

By Fuse Speed/Class: Semiconductor-grade devices gain altitude

Time-delay fuses, with 46.3% share in 2024, stay indispensable for motor circuits where inrush currents exceed rated load. Nonetheless, fast-acting and semiconductor fuses rising at a 6.2% CAGR mirror the proliferation of high-frequency inverters. These products demand precise element geometries to interrupt faults within microseconds, limiting thermal propagation that can destroy power modules.

Hybrid solutions integrating pyroswitches extend clearing performance into the sub-millisecond domain, though cost considerations confine adoption to high-value assets. Over the forecast horizon, the electrical fuses market anticipates blend-and-extend portfolios that pair traditional slow-blow SKUs with fast-acting derivatives to address mixed-load panels.

By Form Factor: Blade still rules, but SMD is the fast riser

Blade fuses comprising 41.20% share remain standard in automotive wiring harnesses thanks to easy field replacement and automated insertion capabilities. Yet SMD chip fuses, growing 5.60% CAGR, reflect the relentless march of miniaturization in consumer electronics and compact power adapters. These surface-mount devices cut assembly steps and enable double-sided PCB population, shrinking product footprints.

Bolt-down NH fuses retain a foothold in industrial switchgear demanding high-current, vibration-resistant connections, while cylindrical designs sustain aftermarket needs in specialty machinery. The resulting form-factor diversity ensures the electrical fuses market serves both legacy and forward-looking applications.

Geography Analysis

Asia-Pacific commanded 42.60% of global revenue in 2024, buoyed by China’s renewable roll-out and India’s grid upgrades. Regional electronics clusters in Shenzhen, Suwon, and Tokyo foster high-value demand for semiconductor-grade protection devices. Local manufacturing cost advantages allow large-scale production runs, sustaining price competitiveness across standardized SKUs in the electrical fuses market. Government incentives targeting solar build-outs result in continuous orders for 1,500 V DC fuses, while Japan’s focus on quality drives the adoption of premium designs with extended endurance cycles.

North America is projected to grow at a rate of 5.70% through 2030, driven by reshoring and data center construction. Schneider Electric’s USD 700 million U.S. capacity expansion through 2027 exemplifies strategic positioning to capture infrastructure spend. Concurrently, ABB’s USD 120 million investment raises low-voltage output by 50%, cementing domestic supply security.[3]Mersen, “Power Transfer for Rail Vehicles – Rolling Stock,” Mersen, Jun 1, 2017, mersen.com Federal infrastructure grants and state-level clean energy mandates underpin demand for electrical fuses across utility, EV charging, and industrial segments.

Europe sustains mid-single-digit growth amid mature utility capex cycles. High-renewable penetration in Germany complicates protection coordination, spurring procurement of adaptive fuses that tolerate inverter-dominant fault currents. Automotive electrification in Germany, France, and the Nordics enhances transportation-sector volumes. Supply-chain realignment post-Brexit incentivizes local fuse manufacturing in Eastern Europe to serve continental OEMs efficiently, maintaining resilience in the electrical fuses market.

Competitive Landscape

The electrical fuses market shows moderate concentration. Littelfuse reported USD 554 million in net sales for Q1 2025, indicating steady demand despite macroeconomic volatility.

Technology differentiation rather than sheer scale drives advantage. ABB’s acquisition of Siemens' wiring accessories arm in China expands its distribution reach to 230 cities and strengthens its smart-building portfolio. Eaton leverages vehicle-specific EV fuses to deepen penetration with automotive tier-ones.

Investment in smart fuse R&D, such as wireless status reporting and real-time temperature monitoring, enables premium pricing while locking in replacement cycles. Patent filings covering intelligent fault-detection circuitry protect intellectual property moats[4]Google Patents, “Intelligent Circuit Breakers with Detection Circuitry Configured to Detect Fault Conditions,” US Patent 11 170 964 B2, Dec 19 2019, patents.google.com. However, price competition persists in the commodity blade and cartridge segments, where Asian OEMs have a competitive advantage due to their low-cost manufacturing. Strategic alliances with PCB assemblers, switchgear builders, and EV-battery integrators become critical to sustain share in the evolving electrical fuses market.

Electrical Fuses Industry Leaders

Littelfuse Inc.

Mersen

ABB Ltd.

Schneider Electric SE

Eaton Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bourns, Inc. introduced the 1,500 V DC POWrFuse series for photovoltaic arrays, targeting installers migrating to higher-voltage strings for lower balance-of-system costs.

- March 2025: Schneider Electric committed USD 700 million to expand U.S. manufacturing capacity, aligning production with domestic infrastructure funding and strengthening its electrical fuses market footprint.

- March 2025: ABB completed the USD 150 million purchase of Siemens’ wiring-accessories business in China, deepening market access and broadening smart-building offerings.

- January 2025: ABB launched the SACE Emax 3 air circuit breaker with IEC 62443 Security Level 2 certification to serve AI data-centre and advanced-manufacturing loads, reinforcing its cyber-resilient portfolio strategy.

Global Electrical Fuses Market Report Scope

| Power Fuse and Fuse Link |

| Cartridge and Plug Fuse |

| Distribution Cut-out |

| Resettable (PTC) Fuse |

| Specialty / Surface-mount Fuse |

| Low Voltage (<1 kV) |

| Medium Voltage (1–69 kV) |

| High Voltage (>69 kV) |

| Utilities | |

| Industrial and Manufacturing | |

| Residential and Commercial Buildings | |

| Transportation | Automotive |

| Rail | |

| Metro | |

| Renewable Power Plants |

| Fast-acting Fuse |

| Time-delay / Slow-blow Fuse |

| Blade Fuse |

| Bolt / NH Fuse |

| Cylindrical Fuse |

| SMD / Chip Fuse |

| Other Form Factor (Axial, Radial, Square-body) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | Power Fuse and Fuse Link | ||

| Cartridge and Plug Fuse | |||

| Distribution Cut-out | |||

| Resettable (PTC) Fuse | |||

| Specialty / Surface-mount Fuse | |||

| By Voltage Range | Low Voltage (<1 kV) | ||

| Medium Voltage (1–69 kV) | |||

| High Voltage (>69 kV) | |||

| By End-User Industry | Utilities | ||

| Industrial and Manufacturing | |||

| Residential and Commercial Buildings | |||

| Transportation | Automotive | ||

| Rail | |||

| Metro | |||

| Renewable Power Plants | |||

| By Fuse Speed/Class | Fast-acting Fuse | ||

| Time-delay / Slow-blow Fuse | |||

| By Form Factor | Blade Fuse | ||

| Bolt / NH Fuse | |||

| Cylindrical Fuse | |||

| SMD / Chip Fuse | |||

| Other Form Factor (Axial, Radial, Square-body) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the electrical fuses market?

The electrical fuses market size totals USD 4.55 billion in 2025, with a projected value of USD 5.78 billion by 2030 at a 4.92% CAGR.

Which fuse type is growing the fastest?

Resettable PTC fuses lead growth at a 5.8% CAGR thanks to rising use in consumer electronics and electric-vehicle subsystems.

How will transportation influence future demand?

Transportation applications, particularly EV platforms and rail electrification, expand at 6.1% CAGR, making them the fastest-growing end-user group for fuses.

Which region offers the highest growth rate?

North America posts an 5.70% CAGR through 2030, driven by reshoring, data-centre construction, and federal infrastructure investments.

Page last updated on: