South Korea Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

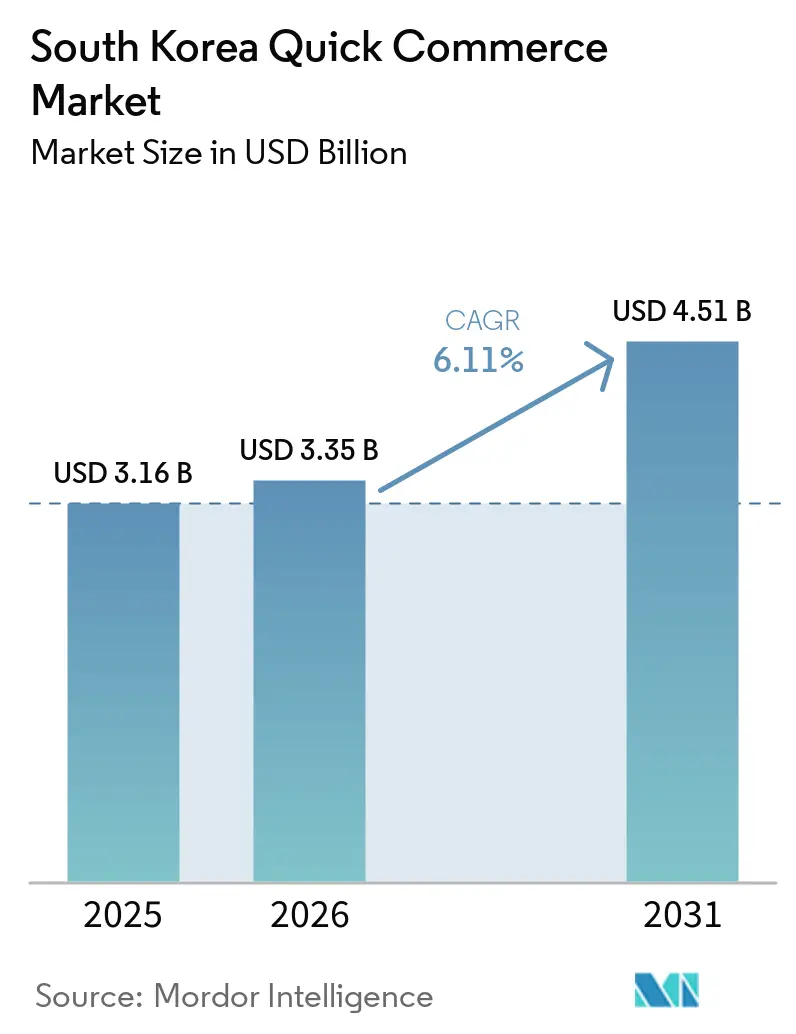

| Base Year Market Size (2025) | USD 3.16 Billion |

| Market Size (2026) | USD 3.35 Billion |

| Market Size (2031) | USD 4.51 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

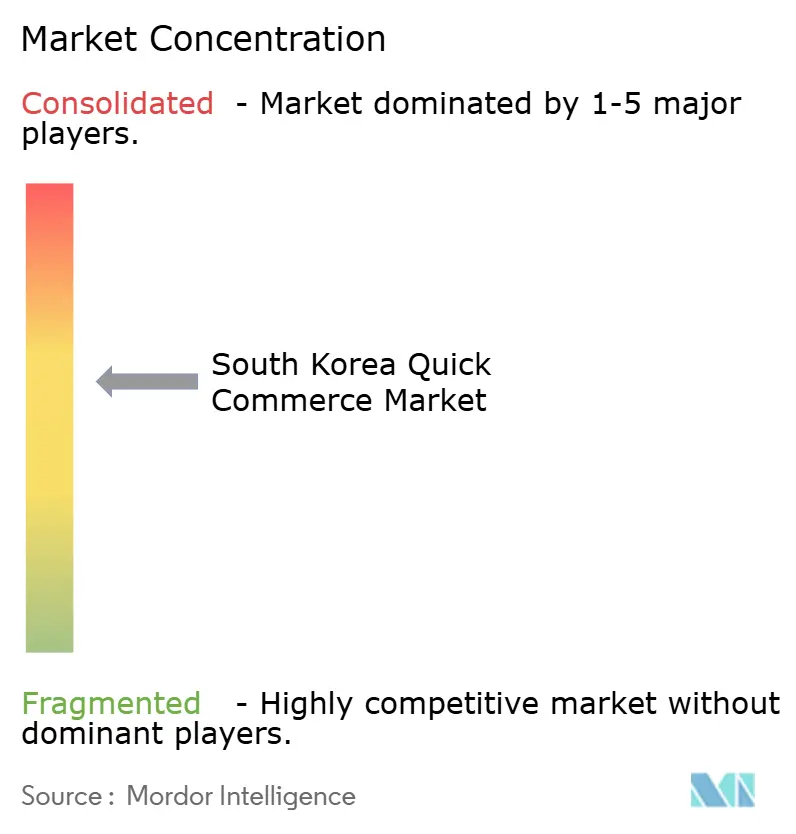

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Quick Commerce Market Analysis by Mordor Intelligence

The South Korea quick commerce market size was valued at USD 3.16 billion in 2025 and estimated to grow from USD 3.35 billion in 2026 to reach USD 4.51 billion by 2031, at a CAGR of 6.11% during the forecast period (2026-2031). The South Korea quick commerce market is being shaped by mobile-first buying behavior, very short urban delivery routes, and rising reliance on on-demand grocery fulfillment in daily life. The Seoul Metropolitan Area gives South Korea's quick commerce market an unusual operating base because dense neighborhoods let platforms serve many households within a tight delivery radius. Demand is also moving beyond occasional convenience purchases, as single-person and dual-income households use fast delivery for routine replenishment and restocking of fresh food. The clearest openings now lie in secondary cities, automation-led fulfillment, and asset-light partnerships that leverage existing store networks rather than expanding dark-store footprints alone.

Key Report Takeaways

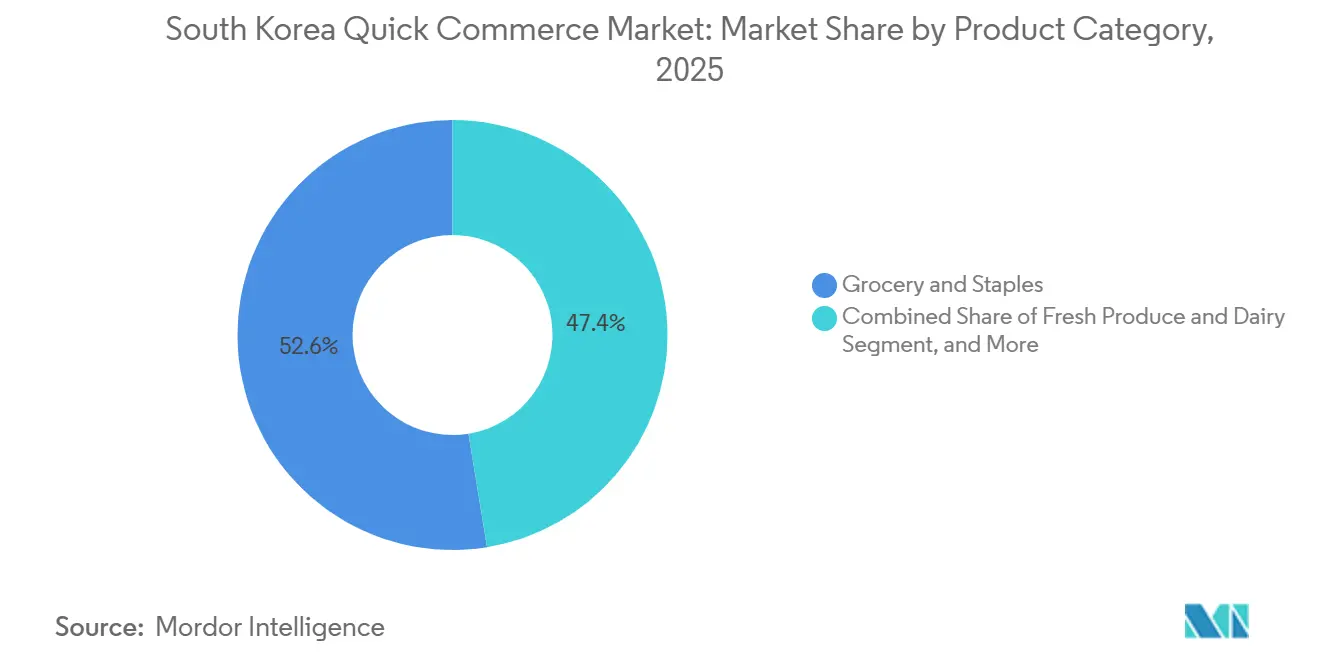

- By product category, Grocery and Staples led with a 52.56% share in the South Korean quick commerce market in 2025, while Electronics and Accessories are projected to expand at a 6.54% CAGR through 2031.

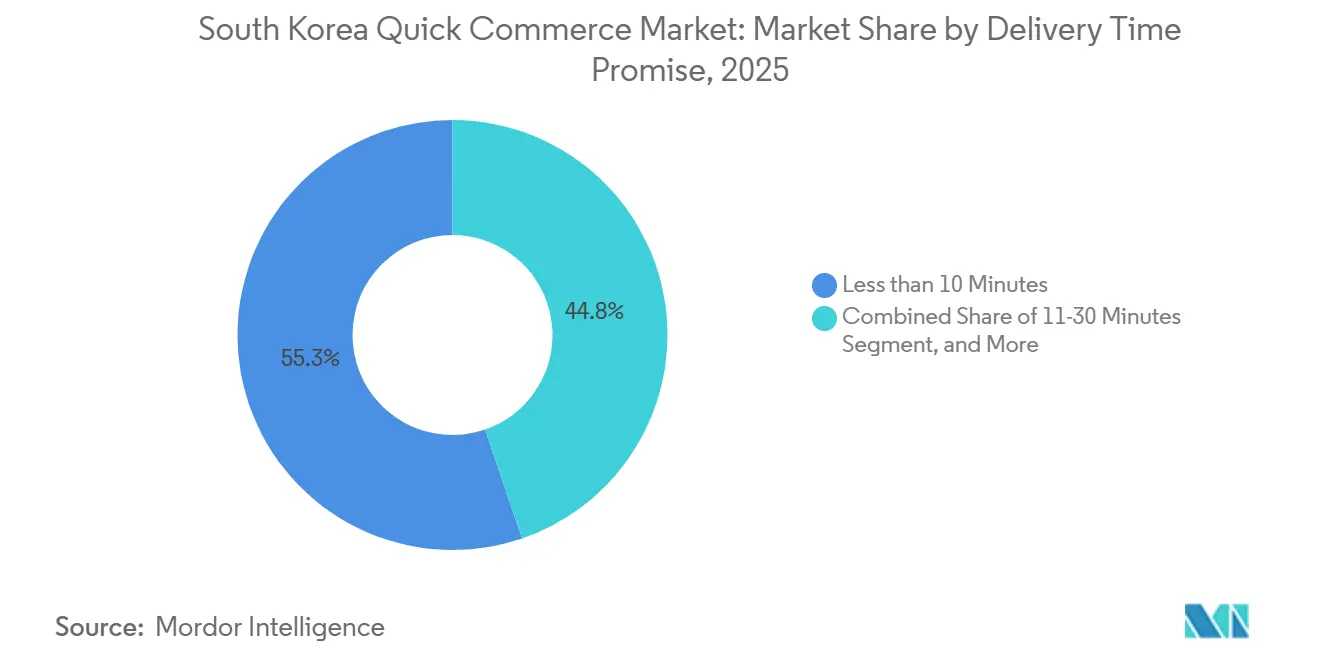

- By delivery time, Less Than 10 Minutes held 55.25% share in 2025, while the 11-30 Minutes tier is forecast to grow at a 6.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Smartphone and Mobile-Payment Penetration | +1.8% | National, concentrated in Seoul, Busan, Incheon | Short term (≤ 2 years) |

| Dense Urban Population Enabling One-Hour Fulfillment | +1.5% | Tier I Metros, Seoul, Busan, Incheon, Daegu | Short term (≤ 2 years) |

| Rising Single-Person and Dual-Income Households Seeking Convenience | +1.2% | National, highest density in Seoul, 39.9%, and Daejeon, 39.8% | Medium term (2-4 years) |

| Retailer-Delivery-App Alliances Expanding Micro-Fulfillment Coverage | +0.9% | National, early gains in Seoul metro and Tier II cities | Medium term (2-4 years) |

| Government Smart-Logistics Incentives and Tax Credits for Automation | +0.5% | National, focused initially on Seoul metro and Busan | Medium term (2-4 years) |

| Super-App Integration of Quick Commerce With Ride-Hailing and Messaging Platforms | +0.4% | National, early gains in Seoul, Gyeonggi, Busan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Smartphone And Mobile-Payment Penetration

Mobile payments give the South Korea quick commerce market one of its strongest demand foundations. Daily mobile card payments reached KRW 1.7 trillion (USD 1.25 billion) in 2025, and mobile accounted for 54.3% of all card spending in the country.[1]Dong-hun Han, “Mobile Payments Hit Record 1.7 Trillion Won Per Day in 2025,” Seoul Economic Daily, en.sedaily.com That scale matters because quick commerce works best when the full purchase path, from search to payment, is handled on the phone in a few steps. The South Korea quick commerce market therefore benefits from a buying pattern that already fits super-app ordering and repeat low-ticket purchases. This keeps checkout friction low and supports frequent use of fast delivery for everyday baskets.

Dense Urban Population Enabling One-Hour Fulfillment

Urban density remains a basic operating advantage for the South Korea quick commerce market. Seoul has a population density of close to 16,000 persons per km², while 42.7% of the country’s single-person households are concentrated in Seoul and Gyeonggi. A Journal of Korea Planning Association study showed that Seoul’s living-logistics parcel volume reached 1.68 million parcels per day in 2020 and is projected to rise to 2.69 million by 2030, showing how dense urban demand keeps building on itself.[2] Seoul’s July 2024 city planning revision also allowed micro-fulfillment placement in Type 2 General Residential Areas, which widened the legal path for urban site deployment. For the South Korea quick commerce market, this means operators with early access to residential fulfillment sites still hold a clear location advantage that later entrants will struggle to match.

Rising Single-Person and Dual-Income Households Seeking Convenience

Household structure is widening the everyday use case for the South Korea quick commerce market. Single-person households reached 8.045 million in 2024 and represented 36.1% of all households, the highest share on record, with projections pointing to continued growth through 2032. Statistics Korea reported average annual income of KRW 34.23 million (USD 25,330) for single-person households in 2024, up 6.2% year over year, which shows that this group is not defined only by budget pressure.[3]Statistics Korea, “2024 Statistics of One-Person Households,” Statistics Korea, mods.go.kr The same source showed that video viewing was the most common weekend activity, which fits a consumer pattern that values time savings, small baskets, and short delivery windows. The South Korea quick commerce market also benefits from high employment among single-person households, which shifts grocery planning away from large weekly stock-ups and toward fast, just-in-time purchasing.

Retailer-Delivery-App Alliances Expanding Micro-Fulfillment Coverage

Retailer-platform partnerships are changing how the South Korea quick commerce market is expanding. Naver launched Now Delivery on May 15, 2025, with 3,000 CU stores, then added more than 1,000 GS25 stores from June 11 and 190 E-Mart Everyday stores from June 16, all using a local delivery radius instead of new proprietary facilities. This model reduces capital requirements because platforms can use existing store inventory and lease footprints to enter more neighborhoods. The South Korea quick commerce market is therefore moving away from dark-store-only fulfillment toward a hybrid model that blends supermarkets, convenience stores, and app traffic. That change matters even more after the convenience store count fell for the first time in 38 years in 2025, pushing chains to monetize existing space through delivery revenue rather than new stores.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Price Wars Eroding Unit Economics | -0.8% | National, most acute in Seoul metro where competition density is highest | Short term (≤ 2 years) |

| Courier Labor Shortage and Rising Minimum-Wage Regulations | -0.5% | National, early legislative pressure concentrated in Seoul and Gyeonggi | Medium term (2-4 years) |

| Municipal Zoning Pushback on Dark Stores in Residential Areas | -0.3% | Seoul, Busan, Incheon, spill-over to Daegu, Daejeon | Medium term (2-4 years) |

| Volatile Fresh-Food Waste Rates Undermining Profitability in Sub-Ten-Minute Models | -0.2% | Tier I Metros, most severe in high-density dark-store zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Price Wars Eroding Unit Economics

Price competition is putting direct pressure on margins across the South Korea quick commerce market. Coupang Eats expanded free delivery to Coupang Wow members in March 2024, and rivals responded with lower-cost subscription offers that reduced per-order revenue across the sector. The cost of that strategy became clearer in 2025, when Woowa Brothers’ consolidated operating profit declined to KRW 592.9 billion (USD 429.6 million), even as revenue increased 22.2%. Higher spending on discounts, rider hiring, and service expansion absorbed the added top line instead of turning into stronger profit. At the same time, policy debate around commission caps and tighter rules on exclusive contracts could narrow the revenue room that platforms use to fund promotions. In the South Korea quick commerce market, that combination makes scale more valuable and raises the risk that smaller operators will struggle to keep matching subsidy-led competition.

Courier Labor Shortage And Rising Minimum-Wage Regulations

Labor is becoming a larger structural cost issue for the South Korea quick commerce market. The 2026 minimum wage was set at KRW 10,320 (USD 7.60) per hour, up from KRW 10,030 (USD 7.40) in 2025, while labor groups were already pushing for another 7-8% increase for 2027. Seoul Economic Daily also reported in January 2026 that 8.7 million gig, freelance, and platform workers could be drawn into a framework with employee-like protections, which would raise exposure to minimum wage, overtime, and social insurance obligations. The breakdown of delivery labor talks in April 2026 showed how difficult it is for operators to keep current service levels while accepting tighter working-hour limits. In response, Coupang expanded automation and AI-led routing, including an NVIDIA-linked logistics initiative in March 2026 and more than USD 84 million in AI startup investments announced in April 2026. This shift shows that the South Korea quick commerce market is starting to substitute capital and software for labor where possible, but that transition will take time.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Grocery Dominance Drives Market Maturation

Grocery and Staples held 52.56% of South Korea quick commerce market share in 2025, which kept this category at the center of daily order frequency and repeat demand. In December 2025, Baedal Minjok’s Baemin Jangbogi and Shopping service posted a 15.4% month-on-month rise in orders and 30% growth in new customers, while milk and instant noodle volumes increased 17.2% and 14.2% from the prior month. That pattern shows the South Korea quick commerce industry still depends most on routine household replenishment rather than one-off emergency buying. Fresh food and staple items keep baskets moving because compact urban homes have less pantry space and need more frequent restocking.

Electronics and Accessories is projected to grow at a 6.54% CAGR through 2031, the fastest pace among product categories, as platforms widen beyond groceries into accessories, stationery, flowers, and pet-related orders. Fresh Produce and Dairy remains more sensitive to delivery quality, and Kurly Now’s cumulative orders grew 2.5 times year over year in January and February 2026 through temperature-controlled hubs in Seoul’s DMC, Dogok, and Seocho districts. Personal Care and OTC Pharma is also gaining weight, with CJ Olive Young handling 15.04 million Today Dream deliveries in 2024 and raising its urban MFC count from 18 to 22 while operating its 38,000 m² Gyeongsan Logistics Center. Across snacks, home supplies, and pet care, operators with direct inventory sourcing still hold an advantage on assortment and margin, which explains why B Mart’s product sales reached KRW 781.1 billion (USD 566 million) in 2025.

By Delivery Time: The 11-30 Minute Tier Builds A Lower-Cost Growth Path

Less Than 10 Min captured 55.25% of South Korea's quick commerce market size in 2025, reflecting the early strength of dark-store-led fulfillment in the densest urban districts. This model works by keeping inventory close to demand, but it also requires heavy fixed investment in micro-fulfillment space and enough local order density to keep each site productive. The South Korean quick commerce industry has relied on that structure to demonstrate demand, especially through Baedal Minjok’s urban pickup-and-pack network. That advantage is strongest in central Seoul, where short delivery radii and concentrated demand still support very fast service promises.

The 11-30 minute tier is projected to grow at a 6.65% CAGR through 2031, making it the fastest-growing delivery window in the South Korean quick commerce market. Retailer-platform partnerships support this shift by leveraging neighborhood store inventory and reducing the need for new dark-store capital. Coupang’s August 2025 decision to end its direct-purchase Eats Mart model and move toward brokerage-based fulfillment through neighborhood merchants within 30-60 minutes reinforced that cost logic at scale. The 31-60 minute and above tier is likely to stay relevant in secondary and smaller cities, where consumers accept slightly longer waits in exchange for broader assortment and more stable pricing. Naver’s current one-hour service model fits that pattern and shows how the South Korea quick commerce market can grow without matching the capital intensity of sub-10-minute delivery in every city.

Geography Analysis

The Seoul Metropolitan Area remains the operational core of the South Korea quick commerce market because it combines very high density with concentrated household demand. Seoul’s population density is near 16,000 persons per km², and 42.7% of the country’s single-person households are concentrated in Seoul and Gyeonggi. That concentration lets a single fulfillment node cover many order points within a tight radius, keeping rider travel time low and helping platforms meet fast service promises. Baedal Minjok’s urban picking-and-packing footprint stayed heavily Seoul-focused, while SSG Corp. expanded Baro Quick to 83 hubs by March 2026 and planned to reach 90 by Q2 2026. Seoul’s July 2024 planning revision widened legal room for urban fulfillment facilities, but the national Logistics Facilities Act still capped MFC floor area at 500 m² and restricted placement within 200 meters of schools or care facilities.

Secondary metro areas are becoming the clearest growth corridor for the South Korea quick commerce market. Busan stands out because Lotte Shopping, BGF Retail, and Coupang Eats all expanded logistics or service coverage there during 2025 and 2026, while Lotte’s planned AI-equipped center is designed to serve 2.3 million households across the Yeongnam region. Daejeon’s 39.8% single-person household share suggests that demand conditions are already strong even though dedicated quick commerce infrastructure is still thinner than in Seoul. Gwangju and Ulsan are still being served more through broader network expansion and convenience store partnerships than through heavy dark-store investment.

Smaller cities and rural areas remain outside the most efficient radius for dedicated sub-30-minute models in the South Korea quick commerce market. Without a dense cluster of households inside a short delivery circle, fixed site costs rise faster than order volume. Convenience store chains therefore act as the working delivery grid in non-metropolitan areas, with GS25 at close to 18,000 stores, CU at close to 18,500, and Seven-Eleven Korea at close to 7,000 participating stores through delivery partnerships. Harim’s OddGrocer adds a different regional model, using a KRW 150 billion (USD 108.7 million), fulfillment center in Iksan connected directly to its food production plants to support fresh delivery beyond the main metro networks.

Competitive Landscape

The South Korea quick commerce market is moderately concentrated at the platform level, with Baedal Minjok and Coupang setting the pace while retailer-led and category-led services compete in narrower lanes. Baedal Minjok retained around 60% of the delivery platform user share, and Coupang Eats reached 12.3 million monthly active users in October 2025, up 32% year over year, which narrowed the gap with Baedal Minjok’s 21.7 million users. Naver entered with a structurally lighter model, building Now Delivery through CU, GS25, and E-Mart Everyday within weeks, rather than funding its own micro-fulfillment network. Kurly Now, SSG. Corps’s Baro Quick, and Homeplus Express’s Magic Now continue to compete in premium fresh-food and grocery use cases, which prevents the South Korea quick commerce market from becoming a simple two-brand story. Naver’s additional KRW 33 billion (USD 23.6 million) investment in Kurly in May 2026, which lifted its stake to 6.2%, showed that major digital platforms still want direct access to high-quality grocery supply and fulfillment capabilities.

Technology and automation are becoming the main tools for defending position in the South Korea quick commerce market. Coupang’s March 2026 AI factory collaboration with NVIDIA improved GPU utilization from 65% to 95% in fulfillment center stocking and delivery routing. In April 2026, Coupang also disclosed more than USD 84 million in AI startup investments, including work with Contoro Robotics on autonomous container unloading at Korean logistics sites. Kakao Mobility applied Google Gemini Flash AI to Kakao T quick delivery in February 2025, cutting delivery-request completion time by 24% and lifting new-user application completion by 13.39% points.

The next contest in the South Korea quick commerce market will likely depend on which players can connect demand, supply, and labor economics more effectively. Baedal Minjok has leaned on proprietary infrastructure and selective exclusive franchise deals, including its February 2026 Baemin Only pilot with Cheogajip Yangnyeom Chicken at a reduced 3.5% commission rate for participating stores. Coupang has moved toward brokerage and neighborhood merchant coverage, which gives it a wider low-capital path in cities where dark-store density is harder to justify. Naver is tying delivery more closely to a broader membership and mobility ecosystem after its October 2025 partnership with Uber for Naver Plus users. There is still room in regulated pharmacy delivery, premium fresh categories, and foreign-resident oriented assortments, but scale and cost discipline will matter more than speed claims alone.

South Korea Quick Commerce Industry Leaders

Woowa Brothers Corp. (Baemin, B Mart)

Coupang Corp.

Kurly Inc. (Market Kurly, Kurly Now)

Yogiyo Co., Ltd.

GS Retail Co., Ltd. (GS25, GS The Fresh)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Naver Corp. completed an additional KRW 33 billion (USD 23.6 million) third-party capital increase in Kurly Inc., raising its stake from 5.1% to 6.2% to fund logistics infrastructure expansion and strengthen the Kurly N Mart offering on Naver Plus Store; Naver Plus Store's monthly active users surged 45.1% from 5.77 million in November 2025 to 8.38 million by April 2026, driven partly by the strategic alliance with Kurly.

- April 2026: Coupang Inc. announced investments exceeding USD 84 million in the United States and global AI tech startups since 2023, including a collaboration with Texas-based Contoro Robotics to develop autonomous container-unloading robots for Coupang's Korean logistics sites, aligned with the United States-Korea Tech Prosperity Deal and directly addressing the delivery labor cost challenge.

- April 2026: Coupang and Kurly rejected the Democratic Party's proposed 48-hour weekly cap for night delivery workers; the Ministry of Land, Infrastructure, and Transport forwarded the unresolved issues to the National Assembly, raising legislative risk for platform cost structures.

- March 2026: Coupang Corp. announced its AI factory collaboration with NVIDIA, using the Coupang Intelligent Cloud and NVIDIA DGX SuperPOD to optimize fulfillment center stocking and delivery routing, increasing GPU utilization from 65% to 95% and positioning Coupang as the second-ranked retailer on Fast Company's 2025 list of the world's most innovative companies.

South Korea Quick Commerce Market Report Scope

The South Korea Quick Commerce Market refers to the rapidly growing segment of the retail and e-commerce industry in Saudi Arabia that focuses on ultra-fast delivery of consumer goods, typically within 30 minutes to a few hours, leveraging technology-driven platforms, localized warehouses, and efficient logistics networks.

The South Korea Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and More), and Delivery Time Promise (Less than 10 Minutes, 11-30 Minutes, and 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less Than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less Than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More |

Key Questions Answered in the Report

What is the current size and growth outlook for quick commerce in South Korea?

The South Korea quick commerce market was worth USD 3.16 billion in 2025, is estimated at USD 3.35 billion in 2026, and is forecast to reach USD 4.51 billion by 2031 at a 6.11% CAGR.

Which product category generates the most demand in South Korea quick commerce?

Grocery and Staples led with 52.56% share in 2025, showing that routine household replenishment remains the main driver of order frequency.

Which delivery window is expanding the fastest in South Korea?

The 11-30 minute tier is projected to grow at a 6.65% CAGR through 2031 because it offers a better balance between speed and cost than sub-10-minute delivery in many locations.

Why is Seoul so important for fast delivery platforms?

Seoul combines high residential density, short travel distances, and a large concentration of single-person households, which supports high order density and better last-mile economics.

Who are the main competitors in this space?

Baedal Minjok and Coupang are the two dominant platform players, while Naver, Kurly, and other retailer-linked services compete through partnerships and category specialization.

What is the biggest challenge for operators over the next few years?

Profitability remains the main pressure point as price wars, rising labor costs, and tighter regulatory scrutiny make it harder to sustain fast delivery at low consumer prices.

Page last updated on: