Thailand Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

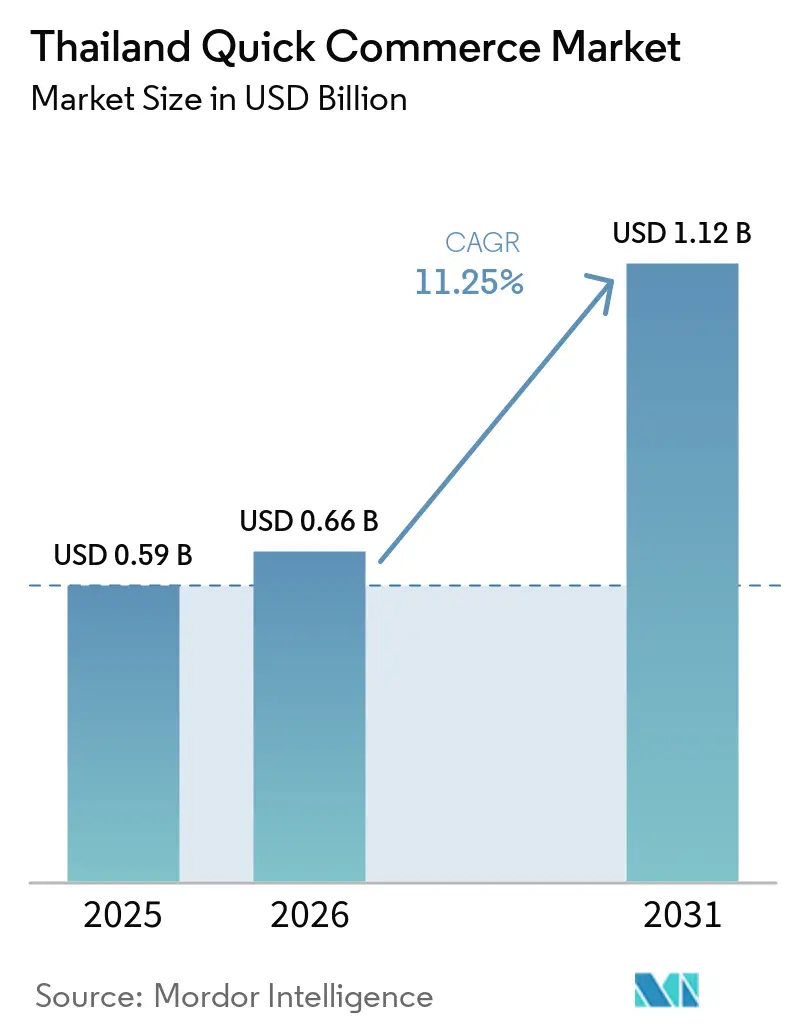

| Base Year Market Size (2025) | USD 0.59 Billion |

| Market Size (2026) | USD 0.66 Billion |

| Market Size (2031) | USD 1.12 Billion |

| Growth Rate (2026 - 2031) | 11.25% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Quick Commerce Market Analysis by Mordor Intelligence

The Thailand quick commerce market size was valued at USD 0.59 billion in 2025 and estimated to grow from USD 0.66 billion in 2026 to reach USD 1.12 billion by 2031, at a CAGR of 11.25% during the forecast period (2026-2031). The Thailand quick commerce market is being supported by the rapid build-out of on-demand delivery networks across Bangkok and nearby urban clusters, where dense rider coverage and store proximity have made short delivery windows more dependable. Mobile broadband depth and digital payment use have reduced checkout friction for low-ticket and repeat orders, which matters because this format depends on fast order cycles and low cash handling. Consumer demand is also moving beyond restaurant delivery into groceries, health-related purchases, and small daily-use items, which is widening the order mix and giving platforms more ways to raise basket value. The Thailand quick commerce market is also becoming harder for smaller entrants to penetrate because scaled platforms and large retailers already control rider density, app traffic, and store-based fulfillment points.

Key Report Takeaways

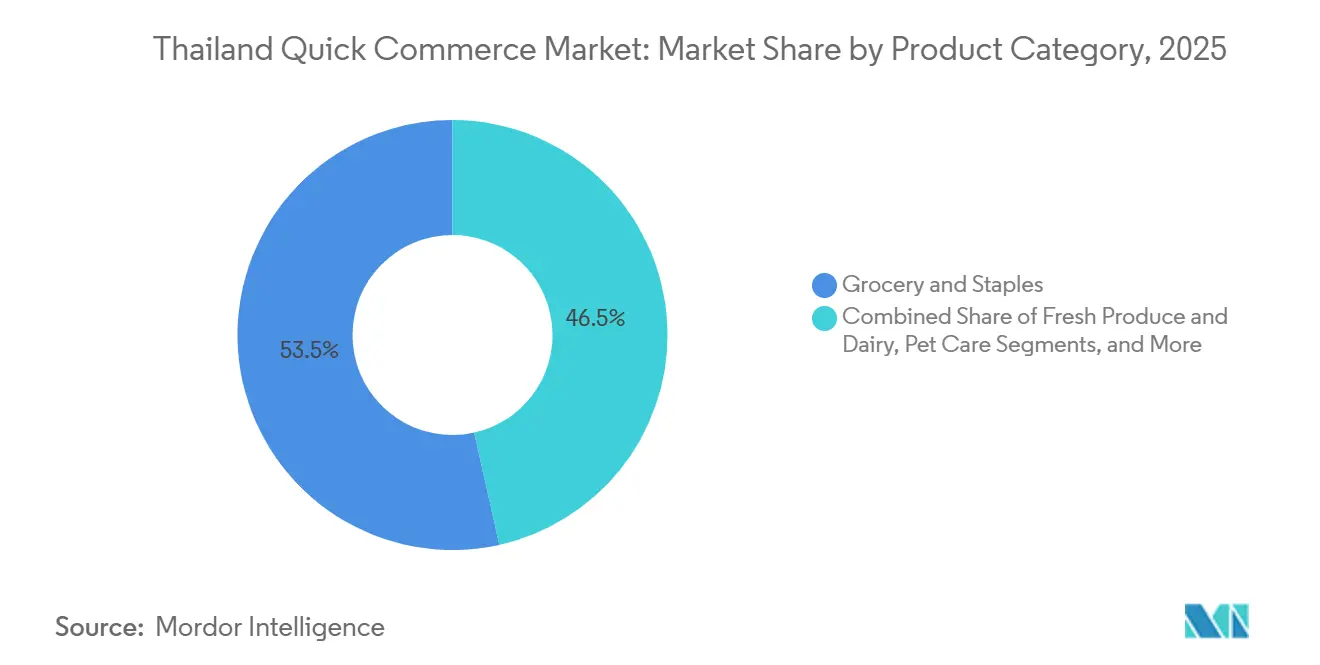

- By product category, Grocery and Staples held 53.48% of the Thailand quick commerce market share in 2025, while Personal Care and OTC Pharma is forecast to expand at an 11.56% CAGR through 2031.

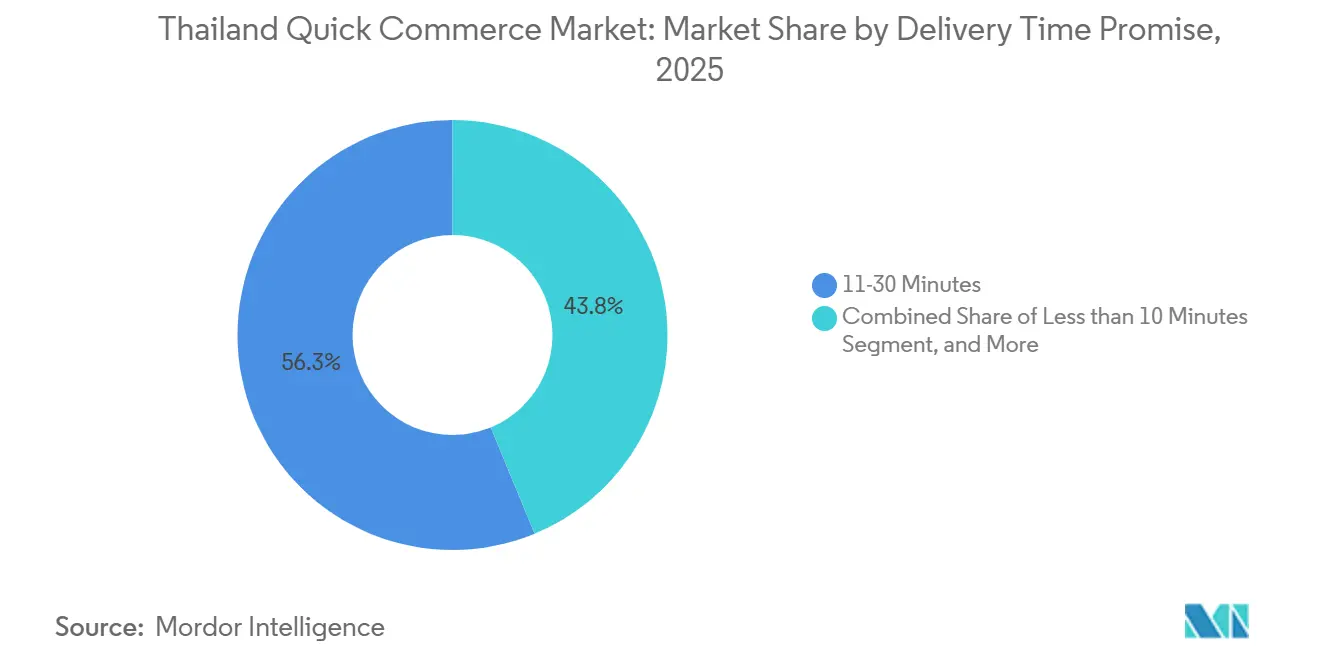

- By delivery time promise, 11-30 Minutes accounted for 56.25% share of the Thailand quick commerce market size in 2025, while Less than 10 Minutes is projected to grow at an 11.77% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Smartphone Penetration and High Mobile Broadband Coverage | +2.5% | National, strongest in Bangkok, Chiang Mai, and Phuket | Short term (≤ 2 years) |

| Growing Urban Millennial and Gen Z Consumer Base in Bangkok and Tier II Cities | +2.1% | National, with core demand originating from Bangkok and Tier II metros | Medium term (2-4 years) |

| Rising Investor Interest in Dark-Store Infrastructure Build-Outs | +1.8% | Bangkok core, with early spill-over to Chiang Mai and Phuket | Medium term (2-4 years) |

| Partnership Momentum Between Convenience Chains and Delivery Apps | +1.5% | National, highest density in Bangkok and Chonburi | Medium term (2-4 years) |

| Expansion of Instant Payment Rails Through PromptPay | +1.2% | National, aligned with Bank of Thailand national e-Payment Master Plan rollout | Short term (≤ 2 years) |

| Surge in Corporate Lunch-Hour Basket Orders From CBD Offices | +0.8% | Bangkok CBD, Silom, Sathorn, Sukhumvit, and Rama IX | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Smartphone Penetration and High Mobile Broadband Coverage

The Thailand quick commerce market rests on a mobile-first ordering base that is already broad and stable. Thailand recorded 4G population coverage at 98% and active mobile broadband subscriptions at 122 per 100 inhabitants, which gives platforms the connectivity depth needed for app-led ordering and live dispatch.[1]International Telecommunication Union, “Digital Development Dashboard BETA - Thailand,” International Telecommunication Union, itu.int The GSMA Mobile Connectivity Index 2025 also placed Thailand among the stronger upper-middle performers in Southeast Asia on infrastructure and consumer readiness, which supports wider use of app-based retail services. This level of network quality matters because quick commerce relies on location tracking, instant order confirmation, and continuous rider communication during every trip. The same connectivity also lets rider fleets operate as connected logistics nodes, which improves route reassignment and favors larger platforms with stronger dispatch systems.

Growing Urban Millennial and Gen Z Consumer Base In Bangkok and Tier II Cities

The Thailand quick commerce market is also benefiting from a younger urban customer base that uses digital services as part of everyday spending. LINE MAN Wongnai served more than 10 million monthly users and listed more than 700,000 restaurants across all 77 provinces, which shows how deeply app-based ordering is already embedded in consumer behavior.[2]LINE MAN Wongnai, “LINE MAN Wongnai Acquires JERA Cloud, Expanding Beyond Restaurants Into Beauty and Wellness,” LINE MAN Wongnai, lmwn.com Shopee Thailand stated in April 2026 that it was expanding faster delivery options, including a premium 1-hour tier, which points to willingness among younger users to pay more for speed in selected use cases. That matters for the Thailand quick commerce market because speed premiums are easier to monetize when users already treat apps as their default buying channel for daily needs. It also increases the value of multi-service ecosystems, where grocery, food delivery, payments, and financial products can reinforce each other inside the same app environment.

Rising Investor Interest in Dark-Store Infrastructure Buildouts

The Thailand quick commerce market is moving closer to a model where fulfillment infrastructure matters as much as rider speed. Freshket raised USD 8 million in January 2025 to support expansion, new product lines, and stronger supply chain partnerships across Thailand's large food service base, which signals investor confidence in infrastructure linked to fast inventory movement and cold handling. LINE MAN Wongnai also disclosed that Wongnai POS processed THB 176 billion (USD 5.3 billion), in annual transactions as of early 2026, which gives platforms more demand data to improve inventory planning and cut stock mismatch. That matters because the fastest delivery tiers cannot scale without micro-fulfillment points that sit very close to dense residential demand. As dark-store investment rises, competition in the Thailand quick commerce market shifts toward site selection, stock depth, and spoilage control, where established retailers and well-funded platforms hold a clear structural edge.

Partnership Momentum Between Convenience Chains and Delivery Apps

The Thailand quick commerce market is being reinforced by partnerships that turn existing store networks into fulfillment nodes. CP All reported 15,945 7-Eleven stores across Thailand in 2025, and its O2O channels, 7Delivery and All Online, accounted for 11% of total consolidated sales that year. That store density provides the market with a distributed inventory base that many peer countries lack, especially in urban and near-urban areas. Grab reported that its Kon La Krueng Plus campaign generated more than 1 million orders within days and lifted average merchant sales by 3 times, which shows how app, merchant, and policy alignment can accelerate order frequency. LINE MAN Wongnai's April 2026 partnership with the Bangkok Metropolitan Administration brought digital payment terminals, hygiene equipment, and rider staging support to more than 100 street food vendors at Hawker Center Suan Lumphini, which widened the orderable supply base without requiring new dark-store investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Margin Pressure From Extensive Rider Incentive Programs | -2.2% | National, most acute in Bangkok and Chonburi | Short term (≤ 2 years) |

| Intensifying Regulatory Scrutiny on Gig-Worker Welfare | -1.8% | National, governed by Thailand's Labour Department and proposed Independent Workers Protection Act | Medium term (2-4 years) |

| High Per-Order Logistics Cost Outside Bangkok Metropolitan Region | -1.4% | Tier II and Tier III cities, particularly in Northern and Northeastern provinces | Long term (≥ 4 years) |

| Limited Cold-Chain Capacity For Fresh Produce In Tier III Cities | -0.9% | Tier III and Below, with structural gaps in Northern and Northeastern provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Margin Pressure From Extensive Rider Incentive Programs

The Thailand quick commerce market faces its clearest near-term pressure in rider incentives and last-mile costs. Bangkok Post reported that rider incentive costs exceeded 35% of ticket value during peak hours for Bangkok-based operators, which shows how quickly margins can narrow when platforms compete for rider availability. In April 2026, Kerry Express, Flash Express, and J&T Express raised shipping fees by THB 3 (USD 0.08) per shipment, citing higher fuel costs and a move away from subsidized pricing. This changes the cost base for the Thai quick-commerce market because low-fee delivery has supported basket conversion even when order values are small. Platforms with subscriptions, stronger route optimization, or in-house rider networks are better placed to absorb this pressure than operators that still depend on high promotional spending.

Intensifying Regulatory Scrutiny on Gig-Worker Welfare

The Thailand quick commerce market is also moving into a more regulated labor environment. Thailand's Labour Protection Act, No. 9, B.E. 2568 was published in the Royal Gazette on November 7, 2025 and took effect 30 days later, expanding protections for workers under digital platform service contracts. Fairwork Thailand Ratings 2025 found that none of the 7 assessed platforms scored above 2 out of 10 on fair-work principles, which adds reputational pressure to the legal shift already underway. The draft Independent Workers Protection Act remains relevant because it would add minimum remuneration, health and accident insurance, and access to a joint welfare structure for riders. These changes could force operators in the Thailand quick commerce market to rebalance pricing, incentives, and service levels over the medium term, especially if they rely heavily on variable-pay rider models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Grocery Commands Share, But Health And Wellness Leads Growth

Grocery and Staples retained a 53.48% share of the Thailand quick commerce market in 2025, which made it the largest product category by a clear margin. This lead came from habitual daily and weekly replenishment behavior, which aligns with dark-store stocking and repeat-order planning. LINE MAN Wongnai's 2025 year-end data showed strong recurring food demand, while Grab also reported very high ordering volumes for core daily-consumption items, which supports the role of routine consumption in maintaining high order frequency.[3]Grab Thailand, “Grab Unveils 2025's Highlights in Ride-Hailing and Food Delivery Services,” Grab Thailand, grab.com The category also benefits from convenience-store integration, as store-based fulfillment makes it easier to serve frequent baskets without bearing the full inventory costs of a dedicated dark-store network.

Fresh Produce and Dairy, Snacks and Beverages, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and other smaller lines all add to basket expansion and category diversification. Shopee Thailand's 2026 move into fresh flower delivery via ShopeeFood riders shows that platforms are expanding the quick-delivery catalog to include purchases that were not historically part of the same-day grocery trip. Personal Care and OTC Pharma is forecast to grow at an 11.56% CAGR through 2031, the fastest pace across product categories, as speed and convenience matter more for health-adjacent buying decisions. The Thailand quick commerce industry also gains from the overlap between grocery and health-related fulfillment, because both can benefit from stronger cold handling, tighter inventory control, and denser local delivery coverage. This gives the Thailand quick commerce market a practical route to category expansion without needing a completely separate operating model for each new product line.

By Delivery Time Promise: Speed Stratification Reshapes Platform Competition

The 11-30 minutes window accounted for 56.25% of the Thailand quick commerce market in 2025, making it the primary operating standard for the sector. That lead reflects the reality that this time band is fast enough to create a premium convenience proposition, but still achievable within Bangkok traffic conditions when platforms use store hubs and dense rider fleets. In the Thailand quick commerce market, this middle band also matches the current maturity of most fulfillment networks better than extreme speed promises do. The 31-60 Minutes and More segment remains relevant in cities where rider density and inventory placement are still developing, thereby continuing to support provincial coverage even when premium delivery windows are not yet reliable.

Less than 10 Minutes is projected to grow at a 11.77% CAGR through 2031, making it the fastest-expanding delivery promise tier. This growth path shows that competition is moving toward hyper-local rider staging and micro-fulfillment placement in high-density parts of Bangkok. It also suggests that future differentiation in the Thailand quick commerce market will depend less on basic app availability and more on whether platforms can support premium speed without eroding margins. Shopee Thailand's 2026 testing of a 1-hour express model supports that direction, because it signals a stepwise move toward shorter delivery windows on selected items and in selected zones. The result is a more stratified market, where speed tiers are becoming a tool for revenue mix, consumer segmentation, and local infrastructure investment rather than a simple service promise.

Geography Analysis

Bangkok supports the densest cluster of riders, dark-store assets, and convenience-led fulfillment points, which is why it still sets the service standard for the rest of the country. CP All reported 15,945 7-Eleven stores in Thailand in 2025, and this network gives Bangkok and nearby urban corridors an unusual advantage in store-based order preparation and dispatch. LINE MAN Wongnai's April 2026 partnership with the Bangkok Metropolitan Administration also showed that local public infrastructure is increasingly supporting platform operations in the capital.

Tier II cities present a more mixed picture for the Thailand quick commerce market. Demand is building in Chiang Mai, Phuket, Hat Yai, Khon Kaen, and Pattaya, but service quality still depends heavily on how quickly rider density and local inventory points improve. Phuket stands out because its high tourist concentration and stronger spending patterns give it demand characteristics closer to Bangkok than to those of a typical provincial city. Chiang Mai appears to be moving through the dark-store build-out stage, where weekly grocery replenishment can start to create the repeat economics needed for broader category scaling.

PromptPay's national scale reduces one of the largest historic barriers to rural and provincial digital commerce because it normalizes low-ticket electronic payment behavior across the country. The harder issue is that per-order costs rise when route distances stretch and order density stays low, especially for fresh and temperature-sensitive categories. For that reason, the Thailand quick commerce market will likely expand in smaller cities through gradual density gains, broader basket sizes, and more flexible fulfillment models rather than through immediate replication of Bangkok's speed-led format.

Competitive Landscape

The Thailand quick commerce market is consolidating around a duopoly, with Grab and LINE MAN Wongnai now holding the clear strategic advantage after Foodpanda ended operations in Thailand in May 2025. Bangkok Post reported that Grab and LINE MAN Wongnai together accounted for 80-90% of platform delivery transaction volume in 2026, while ShopeeFood remained the main third-place challenger after raising its position in 2025. This concentration has raised barriers for new entrants because scale now depends on rider density, consumer traffic, merchant reach, and payment familiarity all at once. It also means the Thailand quick commerce market is moving away from open-ended subsidy competition and toward models built on ecosystem depth, merchant tools, and fulfillment control.

Leading firms are responding by widening their role beyond delivery alone. Grab's March 2026 strategy introduced the AI-powered Basket Builder for GrabMart, a merchant content feed, and Grab Quick Cash personal loan pilots, which shows how the platform is using quick commerce as an entry point into consumer finance and higher-value retention. LINE MAN Wongnai acquired JERA Cloud in 2025, extending its merchant digitization reach into beauty and wellness locations and adding another data and workflow layer around partner retention. CP All's 7-Delivery model shows another route, where a physical retailer uses its nationwide store network as a built-in fulfillment grid rather than relying only on pure-play delivery economics. Together, these moves show that competitive strength in the Thailand quick commerce market now comes from control over inventory, merchant systems, financial tools, and local distribution points, not from delivery speed alone.

White space still exists, but it is narrow and selective. Health-adjacent delivery, beauty and wellness fulfillment, and B2B supply support for Thailand's large food service base remain areas where platforms can build deeper specialization. Freshket's January 2025 funding round underscores that supply-chain-linked models can still attract capital when they solve real procurement and inventory problems rather than just consumer-facing delivery. Smaller community-led apps are also testing low-fee models in local markets, but compliance, data governance, and rider welfare requirements all favor larger operators with stronger legal and operating capacity. That keeps the Thailand quick commerce market concentrated, even though new niches continue to appear around underserved geographies, category specialization, and more localized service formats.

Thailand Quick Commerce Industry Leaders

Grab Holdings Ltd.

LINE MAN Wongnai (Thailand) Co., Ltd.

Shopee Thailand Ltd.

Lazada Group S.A. (Lazada Express Quick Commerce)

Siam Makro Public Company Limited (Makro Quick)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Shopee Thailand confirmed the expansion of its 1-hour express delivery service across selected Bangkok zones and announced plans to extend its Shopee Global Sales program to 3 additional ASEAN countries in 2026, targeting further markets for Thai SME exports, leveraging quick-commerce logistics infrastructure for cross-border commerce development.

- March 2026: Grab Thailand unveiled its "Winning with Purpose Together" 2026 strategy, introducing the AI-powered "Basket Builder" feature for GrabMart, enabling order additions via voice, text, or photo, the "Discover" merchant content feed, and the "Grab Quick Cash" consumer personal loan pilot offering up to THB 20,000 (USD 550) per user repayable over 6 months, marking Grab's first consumer-facing financial product in Thailand.

- November 2025: Thailand's Labour Protection Act, No. 9, B.E. 2568 was published in the Royal Gazette on November 7, 2025, taking effect 30 days later, with expanded coverage to workers under digital platform service contracts and new employer obligations on remuneration floors, leave entitlements, and annual employment reporting to the Department of Labor Protection and Welfare.

- October 2025: Grab Thailand launched the "GrabFood x Kon La Krueng Plus" campaign with a THB 200 million (USD 6 million), marketing investment, participating merchants recorded average sales increases of 3 times within days of the November 3, 2025 campaign launch, with the highest-performing vendor reporting an 18-fold sales surge, the largest single government co-payment-driven demand event recorded on the platform to date.

Thailand Quick Commerce Market Report Scope

The Thailand Quick Commerce Market refers to the rapidly growing segment of the retail and e-commerce industry in Saudi Arabia that focuses on ultra-fast delivery of consumer goods, typically within 30 minutes to a few hours, leveraging technology-driven platforms, localized warehouses, and efficient logistics networks.

The Thailand Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and More), and Delivery Time Promise (Less than 10 Minutes, 11-30 Minutes, and 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More |

Key Questions Answered in the Report

How large is the Thailand quick commerce market in 2026 and what is the outlook to 2031?

The Thailand quick commerce market stands at USD 0.66 billion in 2026 and is forecast to reach USD 1.12 billion by 2031, growing at a CAGR of 11.25% over 2026-2031.

Which product category generates the most revenue in Thailand quick commerce?

Grocery and Staples was the largest category in 2025 with a 53.48% share, supported by frequent household replenishment and strong fit with dark-store and convenience-led fulfillment.

Which segment is growing the fastest in Thailand quick commerce?

Less than 10 Minutes is the fastest-growing delivery time tier at an 11.77% CAGR through 2031, while Personal Care and OTC Pharma is the fastest-growing product category at an 11.56% CAGR.

Why is Bangkok still the core demand center for fast delivery in Thailand?

Bangkok combines the highest rider density, the deepest store network, stronger office-worker demand, and the most mature fulfillment infrastructure, which helped Tier I Metros hold 52.76% of market value in 2025.

How is competition changing in Thailand's quick commerce space?

Competition is tightening around Grab and LINE MAN Wongnai after Foodpanda's exit, and leading firms are now differentiating through merchant tools, financial services, store-based fulfillment, and better inventory control rather than price alone.

Page last updated on: