Vietnam Quick Commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

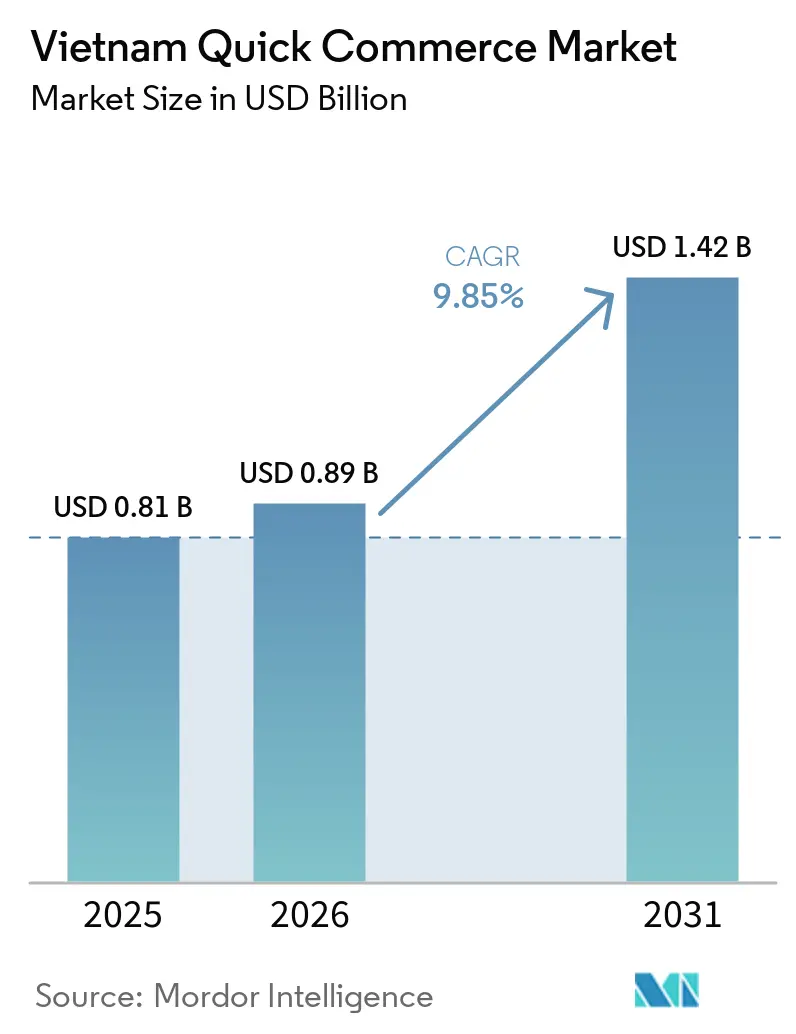

| Base Year Market Size (2025) | USD 0.81 Billion |

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 9.85% CAGR |

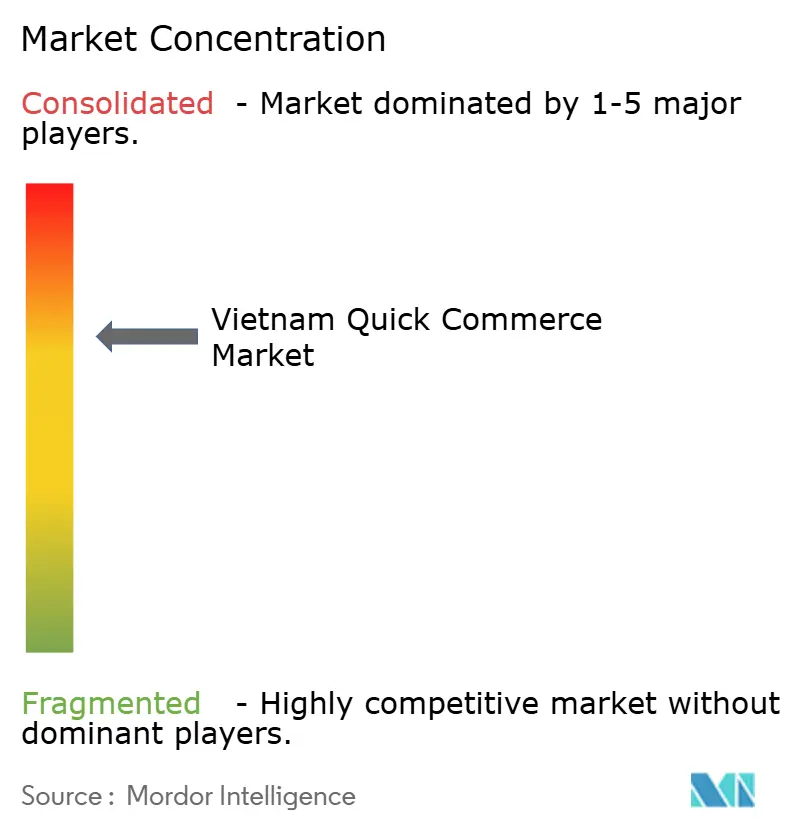

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Quick Commerce Market Analysis by Mordor Intelligence

The Vietnam quick commerce market size was valued at USD 0.81 billion in 2025 and estimated to grow from USD 0.89 billion in 2026 to reach USD 1.42 billion by 2031, at a CAGR of 9.85% during the forecast period (2026-2031). A sustained boom in mobile wallets, dark-store roll-outs and supportive Ministry of Industry and Trade policies are reshaping the Vietnam quick commerce market into an embedded part of daily urban life. Platforms now process high-frequency orders that arrive every three to five minutes during evening peaks, and the average basket already carries 15% to 20% higher spend than traditional e-commerce checkouts. Grocery subscriptions dominate repeat volumes, but fresh produce is closing the gap as cold-chain investments cut spoilage. At the same time, commission-heavy platform economics are accelerating vertical integration by retail conglomerates that want to protect margins, while price-sensitive Tier II households spur geographic expansion that tests last-mile cost discipline.

Key Report Takeaways

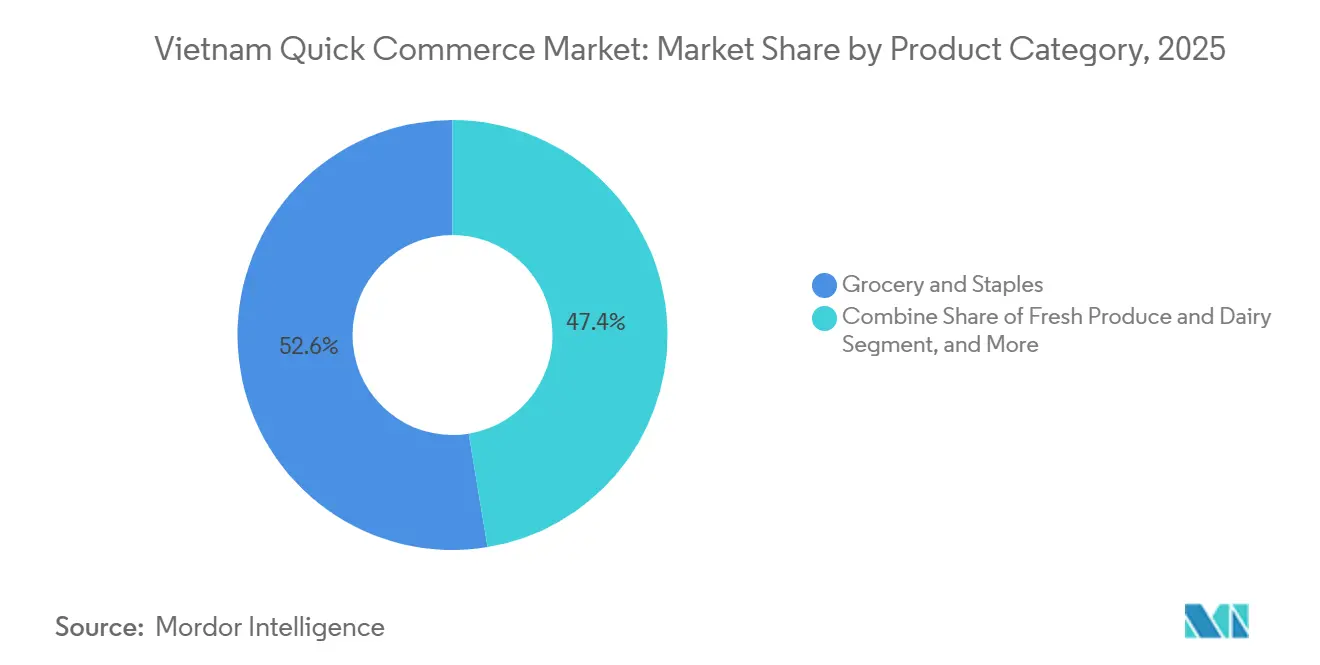

- By product category, Grocery and Staples led with 52.61% of the Vietnam quick commerce market share in 2025, while Fresh Produce and Dairy are projected to expand at a 9.92% CAGR through 2031 and therefore stand out as the fastest-growing segment.

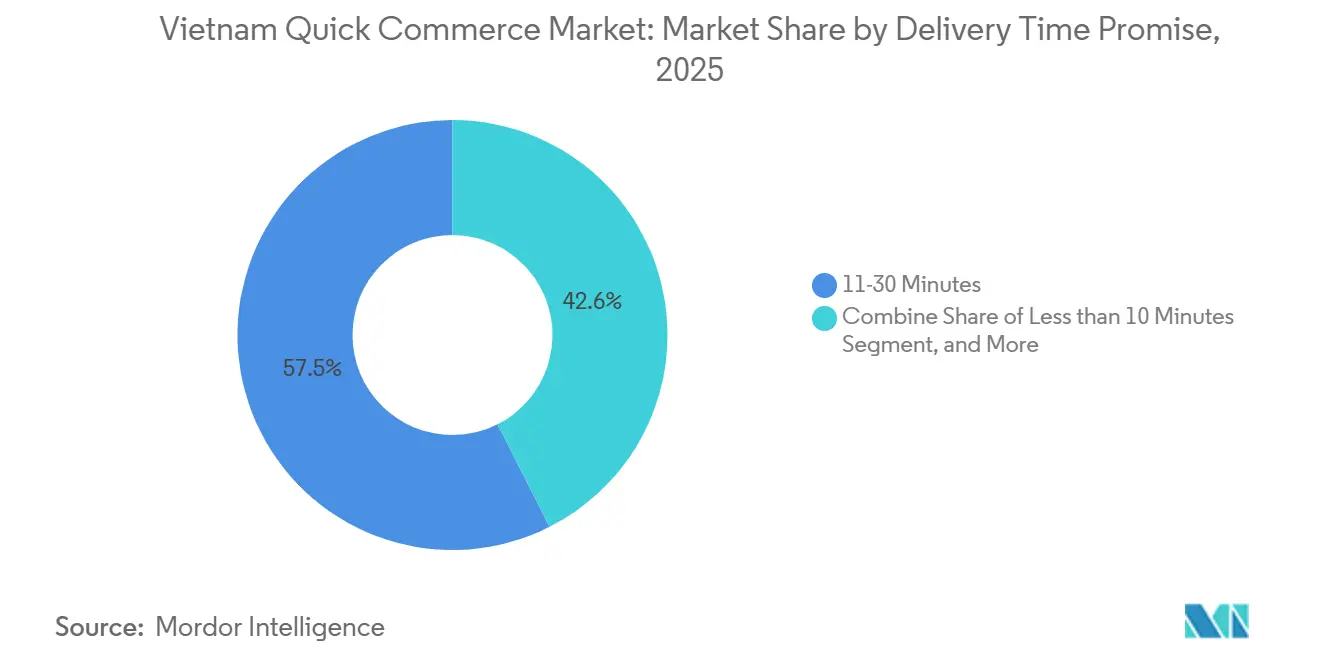

- By delivery time promise, the 11-30 Minutes window captured 57.45% of the Vietnam quick commerce market share in 2025 and remains the operational sweet spot, whereas Less than 10 Minutes is forecast to post the highest 10.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Quick Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding Mobile Wallet Adoption Across Urban Vietnam | +2.1% | Tier I Metros, expanding to Tier II cities | Short term (≤ 2 years) |

| Rising Demand for Hyper-Convenience Among Gen Z Shoppers | +1.8% | National, highest in major metros | Medium term (2-4 years) |

| Growth of Domestic Dark-Store Networks Backed by Retail Conglomerates | +1.5% | Tier I, selective Tier II | Medium term (2-4 years) |

| Government E-Commerce Roadmap Incentives Through 2026 | +1.2% | National | Long term (≥ 4 years) |

| Embedded Finance Integration Driving Higher Basket Sizes | +0.9% | High-income urban districts | Short term (≤ 2 years) |

| Expansion of 24/7 Micro-Fulfillment Centers in High-Density Districts | +0.8% | Core Hanoi and Ho Chi Minh City districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Preference Among Urban Millennials for Hyper-Local Shopping Models

MoMo currently has over 30 million active users, demonstrating its strong presence in the digital payments market. In 2025, QR-code payments experienced a significant growth of 128%, highlighting the increasing adoption of this payment method. This growth has enabled seamless and efficient checkout processes, which have positively impacted businesses by driving higher average order values and encouraging repeat purchases. Digital payment platforms such as ShopeePay and GrabPay, which have incorporated wallet APIs, have successfully reduced cart-abandonment rates. This improvement can be attributed to the fact that 87% of urban shoppers possess linked bank accounts, facilitating a more convenient and integrated payment experience.[1]State Bank of Vietnam, “Digital Banking and Payment Infrastructure Report 2025,” sbv.gov.vn

Rising Demand for Hyper-Convenience Among Gen Z Shoppers

In Vietnam, approximately 19 million Gen Z consumers are now engaging in online shopping on a weekly basis, with a participation rate of 65%. This demographic has shifted its focus from price sensitivity to prioritizing delivery speed, signaling a notable transformation in the traditionally price-driven retail culture of the country. Concurrently, mobile data consumption has risen significantly, reaching an average of 12 GB per month. This increase in data usage has facilitated the adoption of quick commerce applications, which offer curated assortments of approximately 2,000 SKUs. These streamlined assortments are designed to reduce decision fatigue among consumers while simultaneously encouraging impulse purchases, thereby reshaping the online retail landscape in Vietnam.[2]Milieu Insights, “Vietnam Consumer Shopping Behavior Survey 2025,” milieuinsight.com

Growth of Domestic Dark-Store Networks Backed by Retail Conglomerates

During the initial two months of 2026, WinCommerce, a subsidiary of Masan Group, inaugurated 145 small-format outlets. These outlets were strategically positioned within a 10-15 kilometer radius of densely populated residential clusters to maximize accessibility and convenience for consumers. By leveraging dark-store control, the retailer has successfully captured margins across wholesale, retail, and delivery operations, enhancing overall profitability. Concurrently, Viettel Post has implemented advanced robotics at its newly established hub, achieving a remarkable 91% optimization in labor efficiency. This technological advancement underscores the company's commitment to operational excellence and cost efficiency.[3]Masan Group, “WinCommerce Expansion Strategy 2025-2026,” masangroup.com

Government E-Commerce Roadmap Incentives Through 2026

Through Decision 1568, the government is strategically channeling tax incentives and prioritizing expedited land approvals to support the development of fulfillment assets. Concurrently, the 2025 E-Commerce Law introduces a formal regulatory framework for livestreaming activities and enforces mandatory registration for foreign e-commerce platforms operating within the country. Together, these measures are projected to achieve a significant reduction in national logistics costs, estimated at 10-15%, well before the target year of 2028.

Persistently High Last-Mile Logistics Costs in Tier II-III Cities

In Da Nang, Can Tho, and Hai Phong, delivery costs account for 50-53% of total logistics budgets. This significant expenditure is primarily attributed to the low density of orders in these regions, which increases per-unit delivery costs. Additionally, restrictions such as truck bans hinder overnight replenishment operations, further complicating logistics processes. These limitations result in extended delivery times, often exceeding 45 minutes, thereby impacting overall efficiency in the supply chain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently High Last-Mile Logistics Costs in Tier II-III Cities | -1.4% | Tier II and Tier III | Medium term (2-4 years) |

| Limited Cold-Chain Infrastructure for Fresh Produce | -1.1% | Nationwide, acute in rural production zones | Long term (≥ 4 years) |

| Intensifying Price Wars Compressing Gross Margins | -0.8% | National, most severe in Tier I | Short term (≤ 2 years) |

| Regulatory Uncertainty Around Gig-Worker Classification | -0.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Profitability challenges driven by persistent consumer preference for cash-on-delivery payments.

COD persists despite cashless penetration, forcing additional delivery attempts, security protocols, and administrative reconciliation that inflate last-mile costs. Slow cash recovery strains working capital and complicates inventory procurement cycles. Decree No. 52/2024/ND-CP moves to widen digital payment acceptance through tighter payment-service-provider standards, yet behavioral inertia outside tier-one cities tempers near-term relief for Vietnam quick commerce market operators.

Limited Cold-Chain Infrastructure for Fresh Produce

In Vietnam, 90% of the 117 cold-storage facilities are allocated to seafood and meat storage, leaving limited capacity for fresh produce. This imbalance in cold-storage allocation results in significant post-harvest losses for fresh produce, estimated at 20-40%, which equates to an annual financial loss of up to USD 4 billion. To address this challenge, businesses operating in this space face a critical decision: either invest in optimizing their own refrigerated fleet operations to reduce spoilage or accept higher levels of product wastage, which directly impacts their profit margins and operational efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Grocery Dominance Meets Fresh Produce Acceleration

Grocery and Staples delivered the largest share of the Vietnam quick commerce market size in 2025, reinforcing their role as reliable repeat-purchase anchors. Yet Fresh Produce and Dairy is projected to advance at a 9.92% CAGR, fueled by incremental cold-chain capacity and 1-hour delivery pilots that shrink spoilage windows. Snacks and Beverages gain from impulse demand that thrives in sub-30-minute delivery slots, while Pet Care sees double-digit revenue growth among affluent urban owners.

ShopeeMart’s 1-hour express launch in Q1 2026, backed by FamilyMart and Farmers Market alliances, earned 99.5% five-star reviews and validates that freshness perception improves retention. JioMart Vietnam’s 30-minute service undercuts incumbents on basket minimums, stepping up competitive intensity in the Vietnam quick commerce market. Electronics and Accessories still post longer decision cycles, but same-day handoff through AEON’s omnichannel system keeps the category in the convenience game.

By Delivery Time Promise: Mid-Range Windows Dominate, Ultra-Fast Gains Momentum

With 57.45% 2025 share, the 11-30 Minutes bracket suits fleet routing economics and customer tolerance thresholds, securing the biggest slice of Vietnam quick commerce market size across metros. Less than 10 Minutes is gaining steam at a forecast 10.10% CAGR as dense micro-fulfillment grids form in District 1, District 3 and Ba Dinh, though costs escalate sharply below 20 minutes.

GrabMart’s renewables-powered hubs push 30-minute guarantees, and Xanh SM Ngon’s no-batching pledge sells a 1-to-1 delivery premium to time-starved households. Conversely, the 31-60 Minutes option retains relevance for bulk beverages and cleaning supplies where weight, not speed, sets the economic threshold.

Geography Analysis

Tier I metros, led by Ho Chi Minh City and Hanoi, dominate the market and are expected to maintain steady growth over the forecast period. These cities are characterized by high population density and strong consumer demand for quick commerce services. Key districts in these metros contribute significantly to national sales, as households frequently place multiple weekly top-up orders. In Hanoi, areas such as the Old Quarter and Ba Dinh benefit from high dark-store saturation, supported by advanced logistics infrastructure enabling rapid doorstep deliveries. The combination of urban convenience and efficient supply chain networks makes Tier I metros the primary drivers of the quick commerce market.

Tier II cities, including Da Nang, Can Tho, and Hai Phong, are anticipated to expand at a faster pace. These cities are witnessing growing adoption of quick commerce services due to increasing urbanization and rising disposable incomes. Early roll-outs by major players demonstrated significant demand, though challenges such as lower order values and higher delivery costs continue to impact profitability. Local constraints, including narrow alleys, truck restrictions, and cold-chain limitations, necessitate inventory buffers, increasing working capital requirements. Despite these challenges, Tier II cities hold strong potential for growth as infrastructure and operational efficiencies improve.

Tier III and smaller regions remain a long-term opportunity, contributing a smaller share to the market. These areas are characterized by lower population density and limited access to quick commerce services, making them a challenging yet promising segment. Hybrid convenience formats with extended delivery windows are being tested in rural areas to address specific regional needs. Advancements in automated logistics are also reducing inter-city lead times, improving service feasibility in these regions. As 5G coverage and smartphone penetration expand in the coming years, the quick commerce market in Vietnam is expected to achieve a broader national presence, unlocking opportunities in underserved areas.

Competitive Landscape

ShopeeFood and GrabFood dominated the Vietnam quick commerce market in 2025, each holding an equal share after competitors Baemin, Gojek, and Loship exited. Their commission structure, which includes a percentage-based fee along with advertising charges, significantly impacts merchants' margins. This has prompted retailers to explore vertical integration as a strategy to regain profitability and reduce dependency on third-party platforms. The departure of key competitors has further consolidated the market, allowing these two players to strengthen their foothold. However, the high commission rates continue to challenge smaller merchants, pushing them to innovate or collaborate to sustain operations.

WinCommerce responded by rapidly expanding its network, adding a substantial number of new outlets in early 2026, demonstrating the scalability of a captive fulfillment model. This aggressive expansion highlights the company's commitment to increasing its market presence and meeting growing consumer demand. Bach Hoa Xanh achieved significant revenue growth in 2025 and is aggressively pursuing further expansion to solidify its position in the market. Meanwhile, Xanh SM Ngon is leveraging an all-electric fleet to stand out with eco-friendly delivery and direct-to-consumer services. These strategies underline the importance of sustainability and operational efficiency in gaining a competitive edge.

Opportunities remain in cold-chain logistics, as a small portion of storage capacity is dedicated to fresh produce, creating potential for platforms willing to invest in refrigerated micro-fulfillment centers. The lack of sufficient cold-chain infrastructure presents a significant gap that innovative players can address to capture unmet demand. Robotics is also transforming the market, with Viettel Post achieving significant manpower reductions and GHN enhancing parcel processing efficiency. These advancements in automation are reshaping operational models, signaling that technology will play a critical role in determining long-term success in the Vietnam quick commerce market. Companies that prioritize innovation and infrastructure development are likely to emerge as leaders in this evolving landscape.

Vietnam Quick Commerce Industry Leaders

Grab Holdings Inc.

ShopeeFood (Sea Ltd.)

GoJek Group

Tiki Corporation

Loship JSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mobile World Investment Corporation, Vietnam's leading retailer, officially introduced its Bach Hoa Xanh grocery chain in Hanoi, entering one of the country's most competitive consumer markets. The first store, located in Yen Tang village of Da Phuc commune on the outskirts of Hanoi, is strategically positioned near Bac Ninh province, where the retailer currently operates 12 outlets.

- March 2026: WinCommerce said it would open 1,000-1,500 new stores this year to help Masan Group reach USD 40 million in retail profit.

- March 2026: Shopee unveiled ShopeeMart in Ho Chi Minh City and Hanoi with 1-hour grocery delivery that recorded 99.5% five-star reviews in 60 days.

- February 2026: WinCommerce’s network hit 4,737 stores, posting VND 7.9 trillion (USD 316 million) revenue in the first two months, up 32.2% year-on-year.

Vietnam Quick Commerce Market Report Scope

The Vietnam Quick Commerce Market refers to the rapidly growing segment of the retail and e-commerce industry that focuses on ultra-fast delivery of consumer goods, typically within 30 minutes to a few hours, leveraging technology-driven platforms, localized warehouses, and efficient logistics networks.

The Vietnam Quick Commerce Market Report is Segmented by Product Category (Grocery and Staples, Fresh Produce and Dairy, Snacks and Beverages, Personal Care and OTC Pharma, Home and Cleaning Supplies, Electronics and Accessories, Pet Care, Flowers and Gifts, and Other Product Categories), Delivery Time Promise (Less than 10 Minutes, 11-30 Minutes, 31-60 Minutes and More). The Market Forecasts are Provided in Terms of Value (USD).

| Grocery and Staples |

| Fresh Produce and Dairy |

| Snacks and Beverages |

| Personal Care and OTC Pharma |

| Home and Cleaning Supplies |

| Electronics and Accessories |

| Pet Care |

| Flowers and Gifts |

| Other Product Categories |

| Less than 10 Minutes |

| 11-30 Minutes |

| 31-60 Minutes and More |

| By Product Category | Grocery and Staples |

| Fresh Produce and Dairy | |

| Snacks and Beverages | |

| Personal Care and OTC Pharma | |

| Home and Cleaning Supplies | |

| Electronics and Accessories | |

| Pet Care | |

| Flowers and Gifts | |

| Other Product Categories | |

| By Delivery Time Promise | Less than 10 Minutes |

| 11-30 Minutes | |

| 31-60 Minutes and More |

Key Questions Answered in the Report

What is the current Vietnam quick commerce market size and its expected growth by 2031?

The Vietnam quick commerce market size is USD 0.89 billion in 2026 and is projected to reach USD 1.42 billion by 2031, reflecting a 9.85% CAGR during 2026-2031.

Which product category is expanding the fastest inside Vietnam's quick commerce space?

Fresh Produce and Dairy is the fastest-growing segment with a forecast 9.92% CAGR through 2031, outpacing the overall market.

How rapidly are Tier II cities embracing quick commerce formats?

Tier II cities such as Da Nang, Can Tho and Hai Phong are projected to post a 10.45% CAGR between 2026 and 2031 as coverage widens and disposable incomes rise.

Who currently dominates Vietnam's quick commerce platforms?

ShopeeFood and GrabFood together hold 96% share, confirming a highly concentrated competitive landscape.

Which delivery window attracts the highest order volumes?

The 11-30 Minutes promise captured 57.45% of spending in 2025, making it the most popular delivery speed among Vietnamese users.

What is the biggest enabler behind rising digital checkout conversion?

Exploding mobile-wallet adoption-now exceeding 30 million active users-removes payment friction and increases repeat purchase rates, especially among Gen Z shoppers.

Page last updated on: