Global Caspofungin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

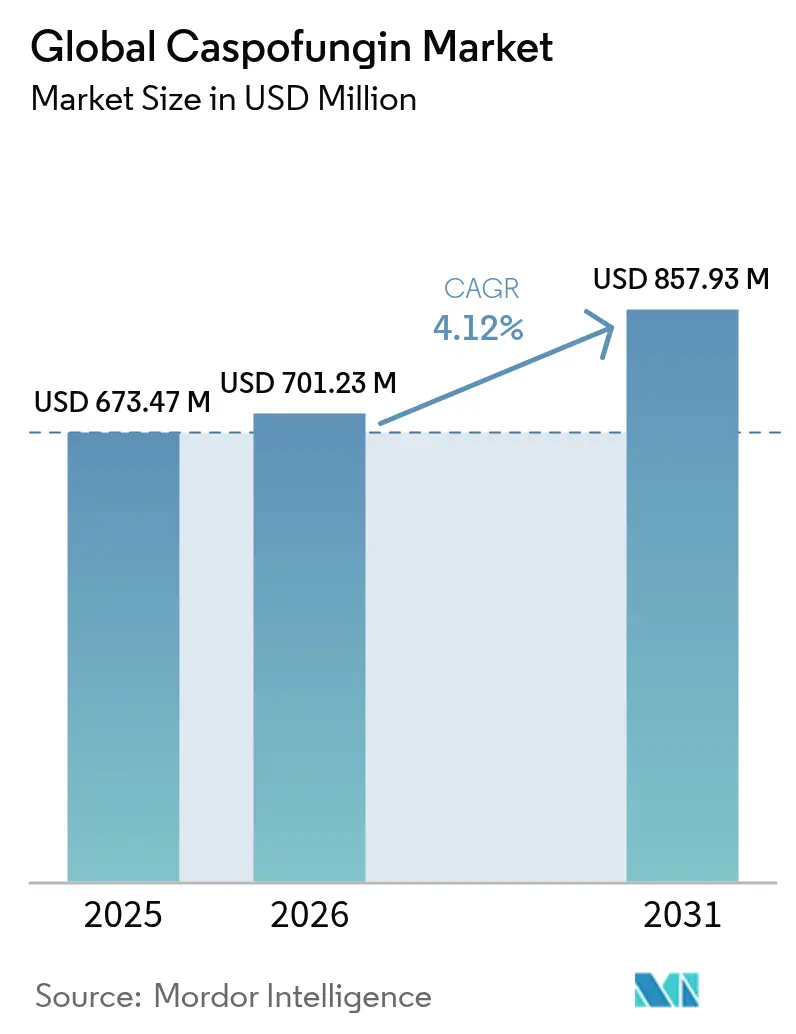

| Market Size (2026) | USD 701.23 Million |

| Market Size (2031) | USD 857.93 Million |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

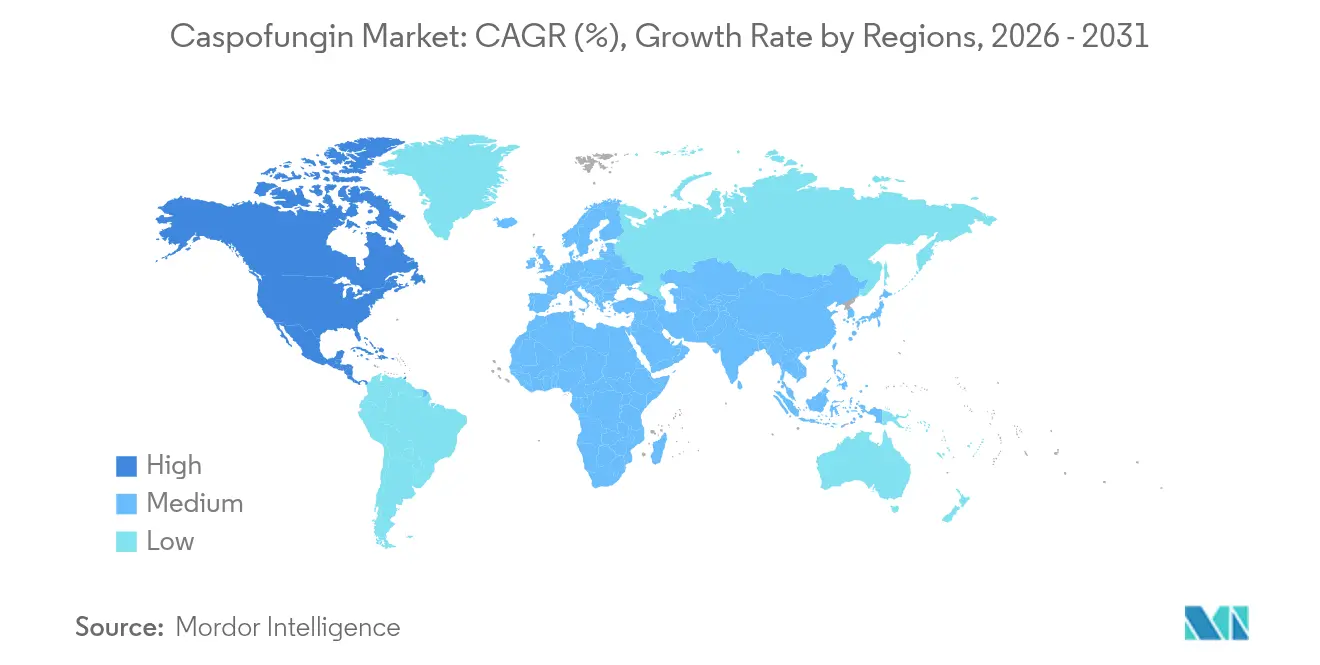

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

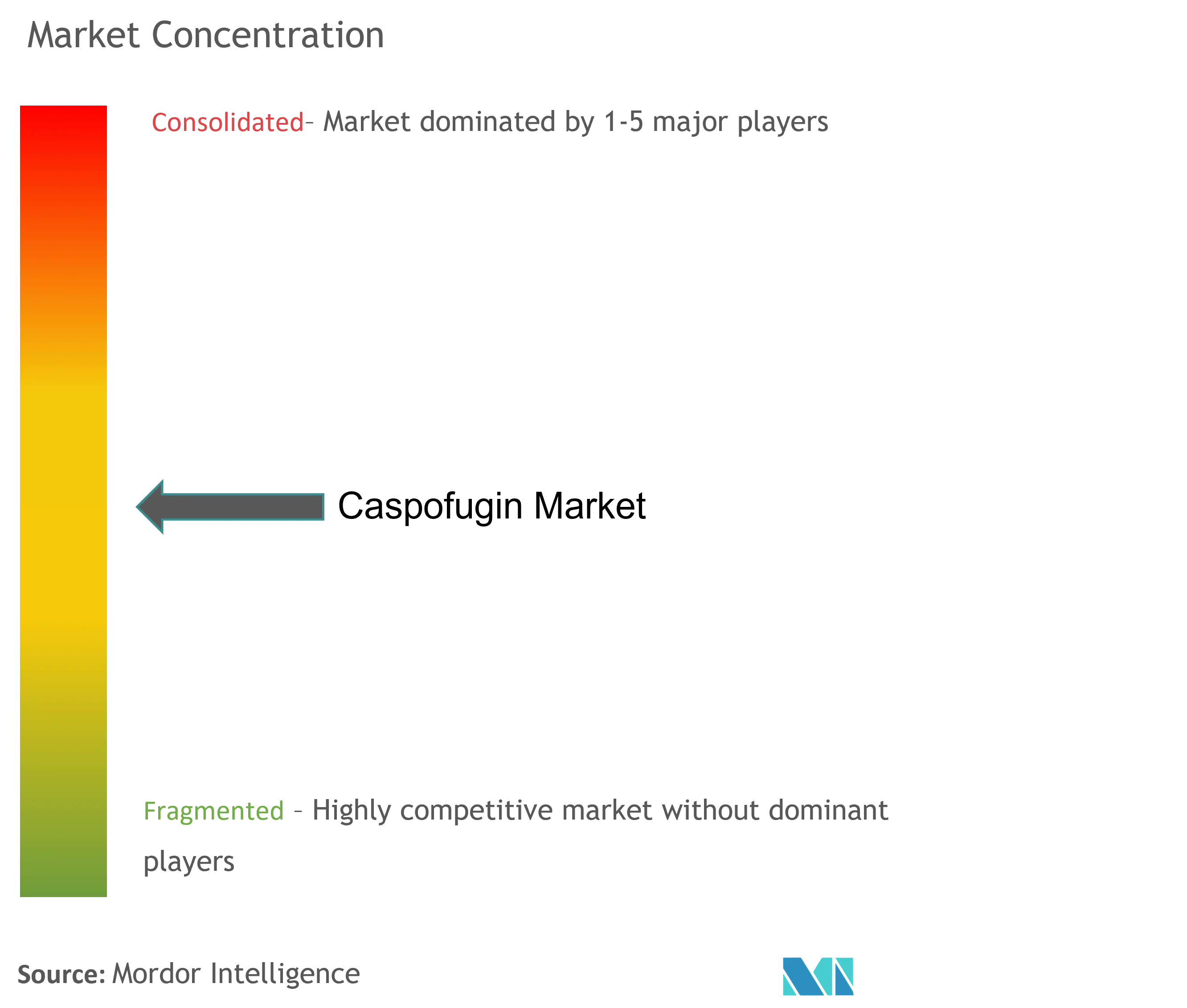

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Caspofungin Market Analysis by Mordor Intelligence

The caspofungin market size was valued at USD 673.47 million in 2025 and estimated to grow from USD 701.23 million in 2026 to reach USD 857.93 million by 2031, at a CAGR of 4.12% during the forecast period (2026-2031). This outlook underscores the drug’s enduring role as a cornerstone echinocandin for invasive candidiasis and aspergillosis in immunocompromised patients despite the arrival of long-acting competitors such as rezafungin. Consistent demand comes from hospitals that value caspofungin’s reliable safety–efficacy balance when azole resistance compromises first-line options. Broader market resilience further reflects rising ICU fungal-infection rates, immunosuppressive transplant volumes, and growing awareness of the high mortality linked with Candida auris outbreaks.

Hospital antimicrobial-stewardship programs now emphasize echinocandin-sparing practices, yet caspofungin prescribing still expands in settings where rapid susceptibility data or azole failure necessitates empirical coverage. Generics approved by the U.S. FDA, the European Medicines Agency, and multiple national regulators are pushing down acquisition prices, promoting wider formulary inclusion even in budget-constrained hospitals. At the same time, clinicians weigh the drug’s IV-only formulation, histamine-mediated infusion reactions, and emerging echinocandin resistance when choosing therapy, creating space for once-weekly alternatives and advanced diagnostics to shape future treatment algorithms.

Key Report Takeaways

- By indication, candidiasis led with 45.24% revenue share in 2025; oropharyngeal thrush is forecast to expand at a 5.61% CAGR through 2031.

- By distribution channel, hospital pharmacies retained 59.74% of the caspofungin market share in 2025, while online pharmacies recorded the fastest projected CAGR at 5.93% through 2031.

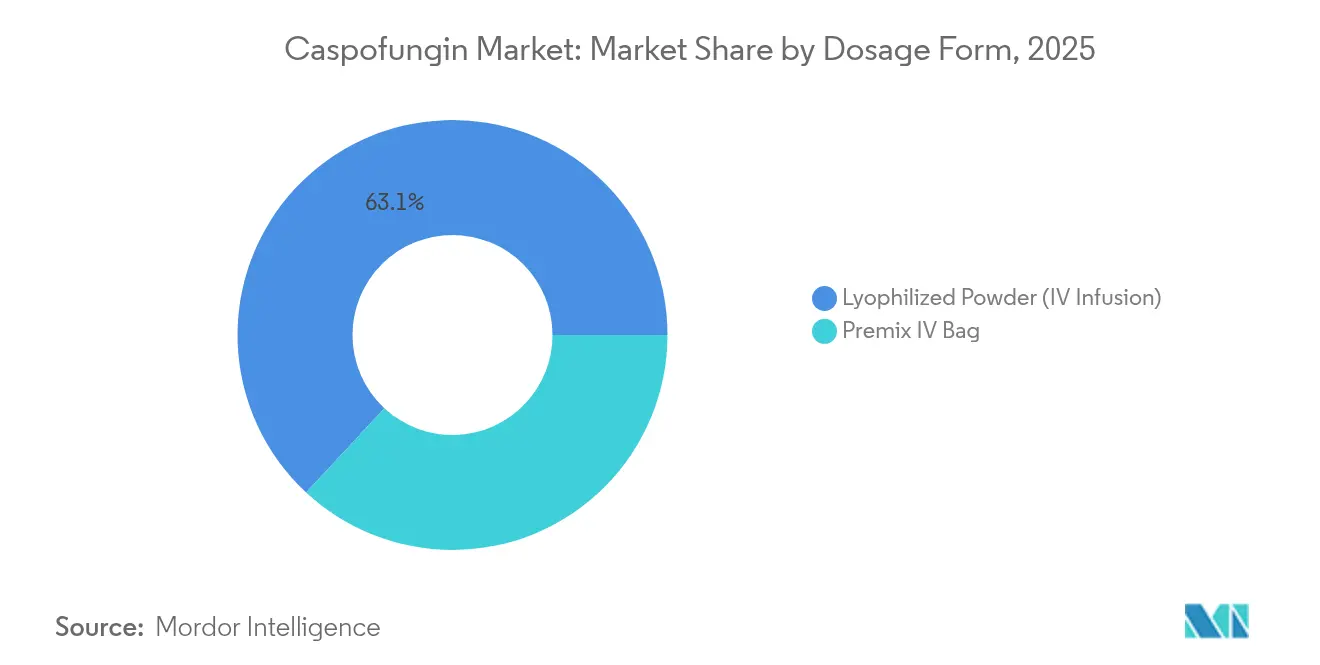

- By dosage form, lyophilized powder accounted for 63.08% share of the caspofungin market size in 2025; premixed IV bags are set to grow at a 5.34% CAGR to 2031.

- By geography, North America captured 39.92% of 2025 revenue; Asia-Pacific is projected to outpace all regions with a 6.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Caspofungin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of invasive candidiasis among ICU patients | +0.8% | Global, notably North America & Europe | Medium term (2-4 years) |

| Expansion of generics post-Cancidas patent expiry | +0.6% | Global, early uptake in emerging markets | Short term (≤ 2 years) |

| Surge in stem-cell & solid-organ transplants | +0.9% | North America & Europe, expanding in APAC | Long term (≥ 4 years) |

| Hospital adoption of echinocandin-sparing stewardship protocols | +0.5% | North America & Europe, gradual APAC adoption | Medium term (2-4 years) |

| Rise of azole-resistant Candida auris outbreaks | +0.7% | Global, hotspots in healthcare-dense regions | Medium term (2-4 years) |

| Development of once-weekly rezafungin | +0.4% | North America & Europe initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Invasive Candidiasis Among ICU Patients

Candidemia incidence climbed to 7.4 cases per 100,000 population across 10 U.S. sentinel sites. COVID-19 further strained infection-control measures, increasing mechanical ventilation and central-line use that heighten fungal-infection risk. Pediatric cardiac ICUs reported 21.8 episodes per 1,000 admissions and 61.1% mortality, reinforcing the clinical impetus for early empiric echinocandin therapy. Length-of-stay analyses show invasive candidiasis patients treated with long-acting echinocandins average 25.2 days versus 28.3 days for traditional caspofungin, though optimization of dosing protocols may narrow this gap. The persistent linkage between ICU complexity and candidemia sustains demand in the caspofungin market, even as hospitals refine antifungal stewardship.

Expansion of Generics Following Cancidas Patent Expiry

FDA-approved manufacturers—including Fresenius Kabi, Sandoz, Sagent Pharmaceuticals, and Alvogen—now offer 50 mg and 70 mg caspofungin acetate vials listed in the Orange Book. U.S. Medicaid claims show declining per-vial reimbursement since 2019, illustrating downward pricing pressure that enhances formulary uptake [1]L. Garcia et al., “Generic Competition and Antifungal Pricing,” mdpi.com. Indian producers such as Senores Pharmaceuticals have registered caspofungin in 43 countries, broadening global supply. While sterile-lyophilized manufacturing remains capital-intensive, generics are easing budget constraints and fostering greater caspofungin industry competition without fully commoditizing the segment.

Surge in Stem-Cell & Solid-Organ Transplants (Immunosuppression)

Hematopoietic stem-cell and solid-organ transplantation volumes continue rising, creating a swelling cohort of profoundly immunocompromised patients vulnerable to fungal infection. ECIL guidelines grade caspofungin B-I for prophylaxis in pediatric hematologic malignancies, underpinning its sustained front-line status. Kidney-transplant recipients face 25-50% mortality when invasive mycoses develop, and Candida species constitute up to 70% of those infections. Early antifungal intervention demonstrably lowers in-hospital mortality and reduces ICU resource utilization, justifying empirical caspofungin expenditures despite generic cost advantages.

Rise of Azole-Resistant Candida auris Outbreaks

Candida auris mortality ranges from 25% to 70%, and clinical cases grew five-fold between 2019 and 2022 in the United States. Italian genomic surveillance documented 503 cases from 2019-2022, revealing independent emergence of echinocandin resistance after prolonged caspofungin exposure. Environmental persistence and under-diagnosis in resource-limited settings obscure the pathogen’s true burden, increasing reliance on broad-spectrum echinocandins. Continuous resistance monitoring has become integral to hospital stewardship strategies, further shaping demand dynamics within the caspofungin market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition cost versus fluconazole & amphotericin B | -0.8% | Global, greatest in LMICs | Short term (≤ 2 years) |

| Adverse events including SJS & histamine reactions | -0.5% | Global, closer scrutiny in developed markets | Medium term (2-4 years) |

| Slow uptake in LMICs due to IV-only formulation | -0.6% | Asia-Pacific, Middle East & Africa, South America | Long term (≥ 4 years) |

| Early resistance signals in C. glabrata & C. parapsilosis | -0.4% | Global, notably high-usage regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition Cost vs. Fluconazole & Amphotericin B

Even with generics, caspofungin’s vial price surpasses fluconazole and conventional amphotericin B, especially impactful in low-income health systems. Cost-effectiveness studies show total treatment expenditure can still favor echinocandins through shorter stays and fewer renal-toxicity events. Nevertheless, many formularies mandate microbiology confirmation or infectious-disease consultation before authorizing therapy, delaying time-to-treatment in critically ill patients and tempering immediate caspofungin market growth.

Adverse Events Including SJS & Histamine-Mediated Reactions

Although safer than azoles in hepatic and QT-prolongation contexts, caspofungin can trigger infusion-related histamine reactions and rare Stevens-Johnson syndrome cases documented in FDA adverse-event reporting 2004-2022 [2]U.S. FDA Adverse Event Reporting System, “Echinocandin Safety Update 2024,” frontiersin.org . Clinical trials show higher treatment-emergent adverse-event rates versus rezafungin, prompting some prescribers to favor once-weekly alternatives where available. Routine liver-enzyme monitoring adds cost and complexity, and the need for reliable IV access limits outpatient applicability, particularly in pediatric or resource-limited environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Candidiasis Dominance Faces Thrush Growth

Candidiasis contributed 45.24% of 2025 revenue, underscoring its status as the principal target for echinocandin therapy amid fluconazole resistance that reached 5.6% in surveillance isolates. Within this setting, the caspofungin market size for candidiasis is forecast to expand at a 3.92% CAGR, benefiting from guideline reinforcement of empiric echinocandin use in non-neutropenic candidemia. Oropharyngeal thrush, though smaller in absolute revenue, is projected to grow 5.61% annually to 2031, buoyed by stem-cell transplant recipients and chronic-obstructive-pulmonary-disease patients on inhaled steroids.

Thrush growth reflects new American Thoracic Society recommendations that prompt earlier empiric antifungal treatment in ventilated patients showing mucosal colonization . Emerging echinocandin tolerance in Candida tropicalis and neonatal dosing uncertainties, however, present hurdles. Combination regimens under evaluation signal potential future label expansion but may also shift demand toward novel modalities should resistance trends accelerate.

By Distribution Channel: Hospital Dominance Meets Online Growth

Hospital pharmacies dispensed 59.74% of caspofungin in 2025, a share anchored in the drug’s IV-only format and the need for close monitoring. The caspofungin market size passing through institutional channels should climb gradually as hospital admissions normalize post-pandemic and transplant volumes rise. Online specialty pharmacies, while representing a modest base today, are predicted to grow 5.93% annually, propelled by home-infusion service integration and coordinated discharge planning to curb inpatient costs.

Digital procurement platforms allow hospitals to lock in bulk prices and emergency stock guarantees, a practice incentivized by the supply shocks experienced during COVID-19. As payers push value-based reimbursement, earlier discharge supported by outpatient IV therapy may tilt volume toward longer-acting echinocandins; nevertheless, widespread generic availability keeps caspofungin a front-line choice for many health systems.

By Dosage Form: Lyophilized Powder Leads Premix Innovation

Lyophilized powder retained 63.08% share in 2025, favored for shelf-life stability and lower unit cost even after accounting for pharmacy compounding labor. Premixed IV bags, growing at 5.34% CAGR, suit rapid-response workflows by eliminating reconstitution and minimizing medication-error risk. Hospitals with large critical-care caseloads highlight time savings as justification for higher acquisition costs.

Recent FDA acceptance of ready-to-use micafungin signals regulatory openness to premixed echinocandin formats, stimulating R&D investment in similar caspofungin presentations. Future liposomal and extended-release technologies could disrupt current volume splits, though sodium load and stability constraints must be resolved before mainstream adoption.

Geography Analysis

North America’s 39.92% revenue lead rests on comprehensive hospital networks, high ICU capacity, and insurance frameworks that reimburse echinocandins despite higher per-vial cost. Use of caspofungin in 49.8% of U.S. candidemia cases between 2017-2021 illustrates entrenched clinical confidence. Rapid adoption of diagnostic-guided stewardship is expected to refine dosing duration without materially shrinking volume because of persistent azole resistance.

Asia-Pacific’s caspofungin market is accelerating on expanding transplant programs, growing ICU capacity, and multicenter surveillance highlighting fungal-infection mortality. The caspofungin market share held by China and India together is projected to climb from 26.20% in 2025 to 31.70% by 2031 as generics lower entry barriers and national guidelines align with international best practice. Government-funded AMR initiatives, such as China’s CFDSS, provide foundational infrastructure for earlier diagnosis and targeted therapy, thereby bolstering demand.

Europe, Latin America, and the Middle East & Africa constitute the remaining demand pool. European antimicrobial-stewardship directives underpin stable usage, whereas Southern Europe monitors C. auris clusters closely after the Italian outbreak, prompting heightened early-warning systems. Latin American hospitals continue shifting from amphotericin B to echinocandins as procurement budgets grow, though IV infrastructure and cold-chain costs temper adoption rates. In Africa, international donor programs and WHO treatment guidelines may stimulate future usage once supply and training improve.

Regulatory Landscape

Caspofungin remains regulated as a prescription-only, sterile injectable across major markets. In the United States, generic entry continues through established pathways that reference the originator Cancidas, with ongoing ANDA activity expanding the set of approved 50 mg and 70 mg caspofungin acetate vials. This includes a July 2025 US FDA approval for Hangzhou Zhongmei Huadong Pharmaceutical for caspofungin acetate injection, while product labeling and listing maintenance in government drug databases supports continued commercialization.

In Europe, caspofungin authorizations and lifecycle changes follow the EMA and national competent authority framework for quality, safety, and efficacy. Generic applications commonly rely on EU legal bases such as Article 10(1) of Directive 2001/83/EC, and post-authorization pharmacovigilance continues to shape labeling and use conditions. UK electronic Medicines Compendium updates (January 2026) also reflect active maintenance of prescribing information and risk communication aligned to current clinical practice.

Value Chain Analysis

The caspofungin value chain typically starts with specialized fermentation and semi-synthetic processing, often using Pneumocandin B0 as a starting material. Complex purification is then used to control closely related analogs and preserve chemical selectivity for a sensitive natural-product-derived molecule. Because thermal instability limits terminal heat sterilization, aseptic filtration and sterile processing are central to quality assurance, and finished-dose manufacture commonly uses lyophilization, increasing dependence on validated fill-finish operations and tight in-process controls.

Downstream distribution is predominantly institutional, given the product is IV-only and is commonly stored and handled under cold-chain conditions (2 to 8 degrees Celsius). This drives higher logistics and inventory-management requirements. The participant set covers originator and generic sterile-injectable manufacturers (including Merck Sharp and Dohme LLC, Fresenius Kabi USA LLC, and Hangzhou Zhongmei Huadong Pharmaceutical), plus API producers such as Jiangsu Hengrui Medicine. GMP and ICH-aligned stability expectations, along with periodic safety updates, particularly in the EU, influence both production planning and hospital procurement continuity.

Competitive Landscape

The caspofungin market shows moderate consolidation. Merck’s original Cancidas retains brand recognition but has ceded significant volume to FDA-approved generic suppliers Fresenius Kabi, Sandoz, Sagent Pharmaceuticals, and Alvogen, alongside rising Asian entrants.

Competition centers on manufacturing reliability, ready-to-use formulation R&D, and bundled stewardship support rather than pure price cuts. Hikma’s injectable-portfolio acquisition and plant expansion highlight the strategic value of sterile manufacturing capacity.

Cidara Therapeutics, via partnership with Mundipharma, positions rezafungin to disrupt hospital stay economics through once-weekly dosing; comparative Phase 3 trials in China pit rezafungin directly against caspofungin. Future white-space opportunities include pediatric dosage forms, oral step-down candidates, and combination regimens targeting emerging resistance.

Global Caspofungin Industry Leaders

Cipla Inc.

Fresenius SE & Co. KGaA (Fresenius Kabi)

Merck & Co., Inc.

Athenex, Inc.

Juno Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hospital stewardship and safety-led updates are creating near-term whitespace around protocol optimization rather than simple volume expansion. In Europe, the EMA issued a DHPC in September 2025 and completed PRAC assessment in November 2025 on treatment failure risk when caspofungin is used with polyacrylonitrile (PAN) membranes during continuous renal replacement therapy. That outcome is pushing hospitals to refine CRRT-compatible antifungal pathways, membrane selection, and pharmacy-informatics alerts. Suppliers that can support education, labeling-aligned order sets, and formulary guidance around ICU use cases, including CRRT workflows, have a direct lever to protect utilization in high-acuity settings.

Product-format and supply reliability remain practical opportunities as well, given the market's reliance on sterile lyophilized powders and the operational burden of IV preparation in hospitals. Expanding access to compliant, consistently supplied generic vials and broadening ready-to-use or ready-to-prepare hospital workflows (including premix where feasible) can reduce compounding time and error risk, while aligning with procurement pressure for dependable availability. Continued maintenance of updated prescribing information, including the January 2026 emc update for Viatris caspofungin in the UK, also signals active lifecycle management that supports institutional confidence and tender participation.

Recent Industry Developments

- January 2026: Fresenius Kabi USA, LLC maintained updated prescribing information for caspofungin acetate for injection in the US DailyMed listing. Keeping labeling current supports uninterrupted wholesaler and hospital purchasing, and reinforces compliance expectations for sterile injectable suppliers competing on reliability as much as price.

- July 2025: Hangzhou Sino-US Huadong Pharmaceutical Co., Ltd. received US FDA approval for an ANDA for caspofungin acetate for injection. The approval added another FDA-cleared generic supply source for 50 mg and 70 mg strengths, increasing competitive intensity in institutional tenders and strengthening supply redundancy for hospital formularies.

- April 2025: Ireland’s Health Products Regulatory Authority published a public assessment report for a caspofungin product authorization, reflecting continued lifecycle activity for caspofungin presentations in European markets. Such updates support ongoing market access across EU procurement channels that rely on current quality and safety documentation for sterile injectables.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks revenue generated from caspofungin (caspofungin acetate) used for systemic fungal infections, measured across the main geographies where it is purchased and administered, largely in hospital and clinic settings.

Scope exclusions: It excludes oral echinocandin pipeline candidates, veterinary uses, compounded substitutes, and standalone API trade flows that do not represent finished-dose patient use.

Segmentation Overview

- By Indication

- Candidiasis

- Thrush (Oropharyngeal)

- Other Indications (Aspergillosis, Febrile Neutropenia)

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Dosage Form

- Lyophilized Powder (IV Infusion)

- Premix IV Bag

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with anchoring the clinical use and approved labeling, then mapping how the medicine moves from supply to patient administration. We rely on public sources such as FDA drug labeling and safety updates, CDC fungal disease guidance, WHO antimicrobial and antifungal stewardship materials, and OECD health statistics to understand treatment settings and demand signals. When needed, peer reviewed journals are used to check trends in invasive candidiasis and aspergillosis burden, and to cross-check changes in resistance and outbreak mentions.

We also use company annual reports, investor presentations, and reputable press coverage to track portfolio changes, launches, and manufacturing shifts that can move supply and pricing. Trade association websites and national procurement portals help confirm tender behavior in hospital channels, especially for injectables. Select paid subscriptions are used for company financials and news screening, patent lookups, and shipment level import export checking where available. These examples are not exhaustive, and many other public sources are reviewed to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focuses on validating what drives caspofungin volumes and realized pricing in routine care, including hospital pharmacists, infectious disease clinicians, procurement teams, and distributors. We also speak with manufacturing and regulatory facing roles to confirm supply continuity, tender timing, and typical discounting patterns, then refine assumptions across APAC, EMEA, and the Americas so the model does not rely on one region's purchasing behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 15% | APAC: 42% |

| Mid tier: 50% | Functional/Unit leaders: 30% | EMEA: 31% |

| Smaller Players: 15% | Managers: 55% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where treatment setting demand is reconstructed from invasive fungal infection signals, hospital activity indicators, and drug utilization patterns that were validated during interviews, then converted into revenue using country level price points. To keep the calculations practical, we use inputs such as ICU and transplant related risk pool trends, antifungal stewardship intensity, hospitalization volumes for severe infections, shares of echinocandin use in relevant protocols, and the typical dosing course length for adult patients. Because caspofungin is mainly an injectable used in acute care, we also check the timing of hospital tenders and any supply interruptions that can temporarily shift volumes.

Results are corroborated with selective bottom-up approximations, such as sampled price per vial multiplied by estimated vials per treatment course, and cross-checked against a small set of supplier and channel checks. Totals are adjusted when these checks show consistent gaps. Where country data is incomplete, nearby markets with similar care pathways are used as proxies, followed by a conservative adjustment based on expert feedback. For forecasting, we apply scenario analysis supported by short variable trends (infection burden and hospital capacity), then layer in expected ASP progression based on generic penetration and tender discount behavior.

Data Validation & Update Cycle

Outputs are validated through multiple checks so unusual jumps are not carried into the final numbers. We compare modeled revenue against independent signals like hospitalization and ICU activity trends, public procurement announcements, and observed price movements for injectable hospital drugs, and we rework outliers before sign off. If a variance is driven by a specific event like a tender reset, a new entrant, or a supply change, the assumption is rechecked and the related country blocks are recalculated.

The report is refreshed annually, and interim updates are triggered when material events occur, such as major pricing changes, notable supply disruptions, or regulatory actions. Before delivery, analysts run a final pass on currency conversion timing, base year price consistency, and the latest public signals so clients receive an up to date view.

Mordor Intelligence's Caspofungin Market Estimate Compared With Other Published Estimates

Published values for caspofungin often differ because the market is small enough that pricing and channel choices can move totals, and because firms do not always use the same year and currency basis. Differences also come from whether calculations focus on hospital purchasing only or try to spread use across broader pharmacy channels.

A refresh led gap is common in this market, since tender resets and generic discounting can change realized ASPs quickly, and even a small change in the FX conversion month can shift USD totals. By locking prices to a constant year, rechecking the latest procurement and utilization signals before sign off, and applying a consistent ASP progression step, Mordor Intelligence reduces drift from one update to the next in a way that is easy to audit back to inputs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 701.23 M (2026) | |

| Global Consultancy A | USD 672.81 M (2026) | Uses a similar forecast start year, but its scope leans more on distribution channel splits and can understate hospital tender discount variability, which affects realized ASPs for injectables. |

| Regional Consultancy B | USD 475.77 M (2025) | Anchors the market on an earlier base year and a lower growth view, and the pricing basis appears less tied to tender timing, which can compress totals when generic price erosion is applied too broadly. |

The table shows that year choice and price construction are the biggest drivers of spread, more than pure volume assumptions. Our approach stays traceable because volumes are tied to treatment setting signals, and pricing is handled with explicit currency timing and discount logic that can be revisited when market conditions change.

Key Questions Answered in the Report

What is the current Global Caspofungin Market size?

The caspofungin market generated USD 701.23 million in 2026 and is projected to reach USD 857.93 million by 2031.

Who are the key players in Global Caspofungin Market?

Cipla Inc., Fresenius SE & Co. KGaA (Fresenius Kabi), Merck & Co., Inc., Athenex, Inc. and Juno Pharmaceuticals are the major companies operating in the Global Caspofungin Market.

What segment shows the fastest growth?

Oropharyngeal thrush is the fastest-growing indication, advancing at a 5.61% CAGR through 2031 amid rising immunosuppressed patient numbers.

Which region has the biggest share in Global Caspofungin Market?

North America held 39.92% of 2025 revenue due to sophisticated hospital infrastructure, broad insurance coverage, and strong stewardship programs.

Page last updated on: