Atelocollagen Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

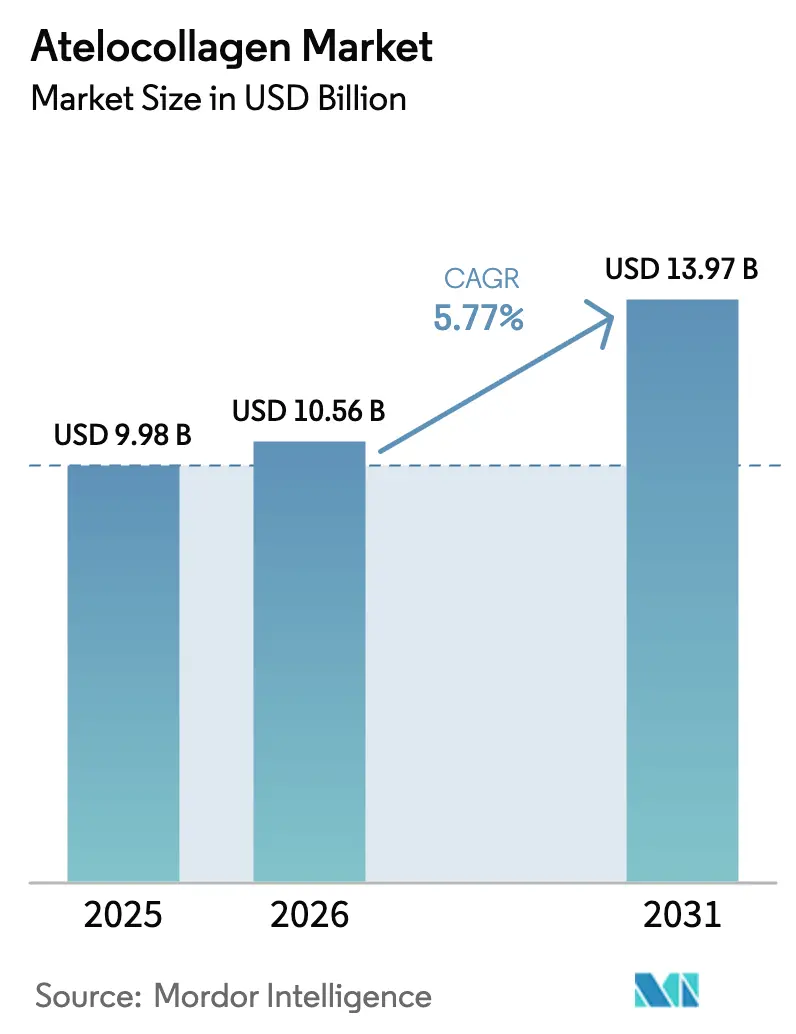

| Market Size (2026) | USD 10.56 Billion |

| Market Size (2031) | USD 13.97 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

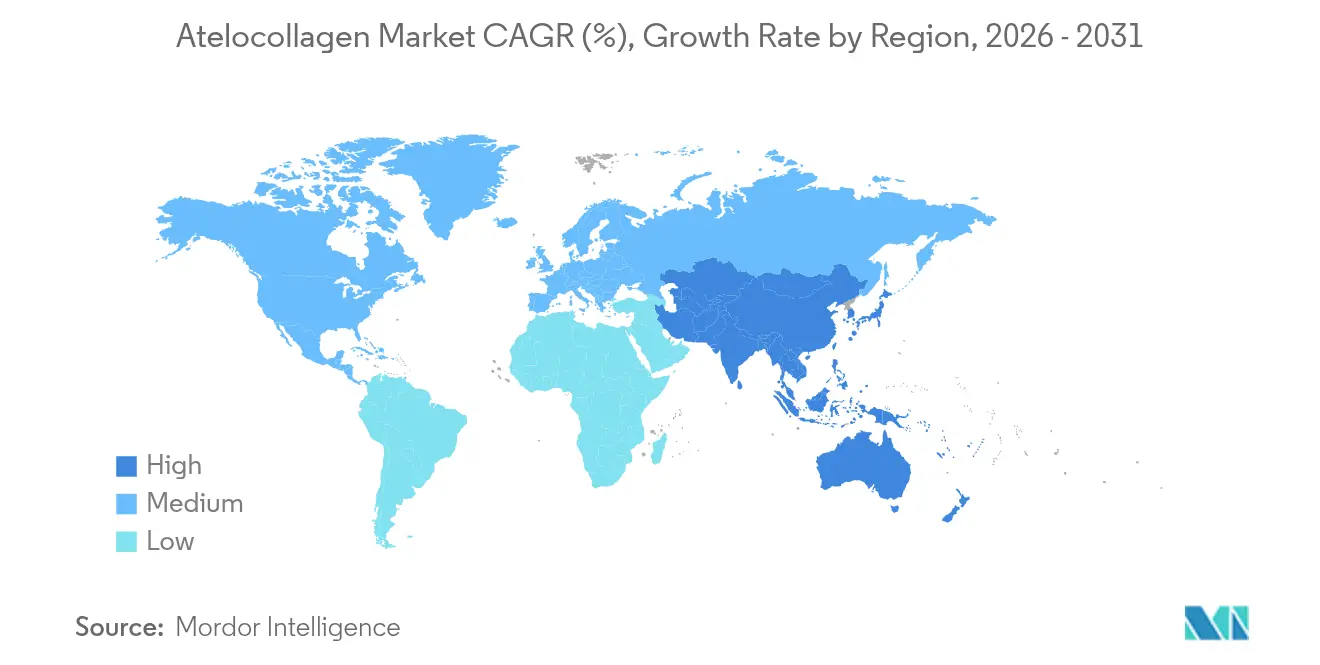

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

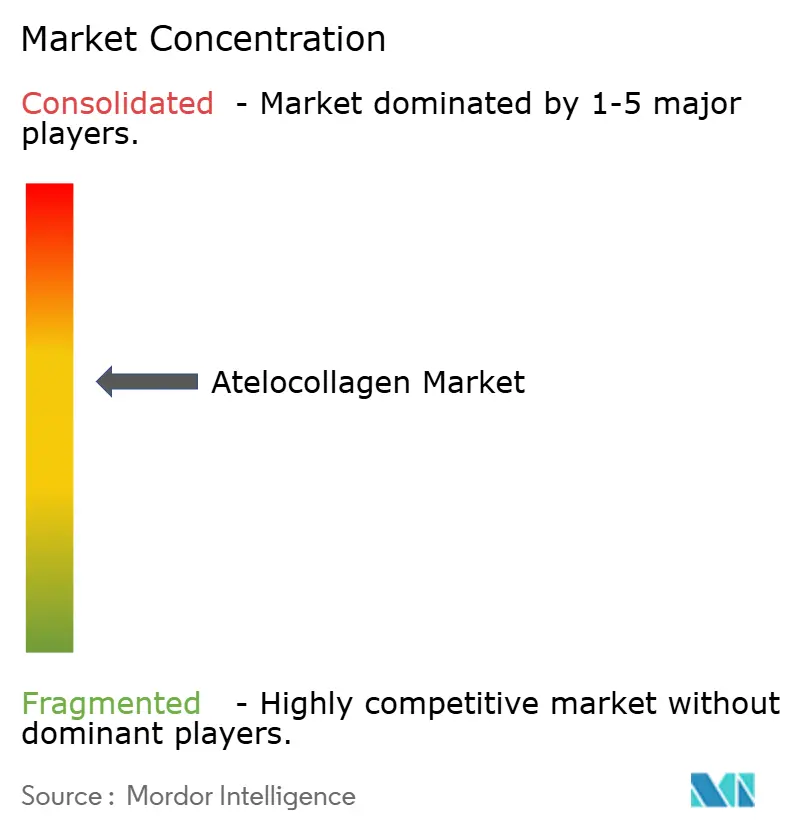

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Atelocollagen Market Analysis by Mordor Intelligence

The atelocollagen market size is expected to grow from USD 9.98 billion in 2025 to USD 10.56 billion in 2026 and is forecast to reach USD 13.97 billion by 2031 at 5.77% CAGR over 2026-2031. Uptake is strongest in regenerative medicine, aesthetic injectables, and advanced wound care, where enzymatic de-telopeptidation minimizes immunogenicity and improves biomechanical fidelity. Clinical trials confirm that atelocollagen up-regulates Sox9, type II collagen, and aggrecan during chondrogenic differentiation, strengthening its role in cartilage reconstruction[1]Scientific Reports Editorial Team, “Atelocollagen boosts chondrogenic differentiation markers in human adipose-derived MSCs,” nature.com. FDA clearance of Symvess, an acellular collagen vessel, signals regulatory confidence in next-generation matrices, while fast-growing 3-D bioprinting and marine sourcing diversify supply and cut zoonotic-risk concerns[2]FDA Communications Office, “FDA clears Symvess acellular vessel for vascular trauma,” fda.gov. Strategic partnerships—such as Evonik’s vegan-collagen alliance with Jland Biotech—shorten development cycles and widen geographic reach.

Favorable reimbursement, growing medical-tourism hubs, and social-media-driven aesthetic demand keep the atelocollagen market on a resilient trajectory despite inflationary cost pressure and logistics complexity. Fermentation platforms, plant-based recombinant formats, and continuous-processing lines are poised to compress unit costs, raising margins for suppliers that master scale-up engineering.

Key Report Takeaways

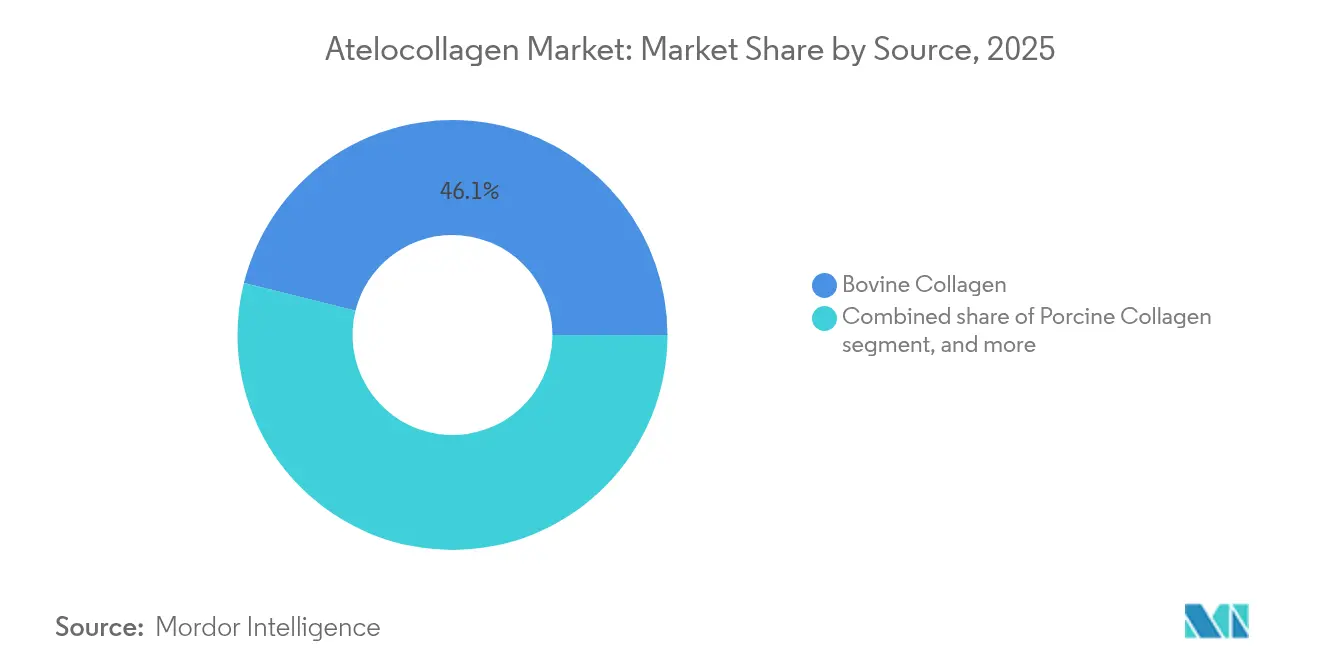

- By source, bovine collagen held 46.12% of the atelocollagen market share in 2025, while fish/marine formats are projected to post a 7.12% CAGR through 2031.

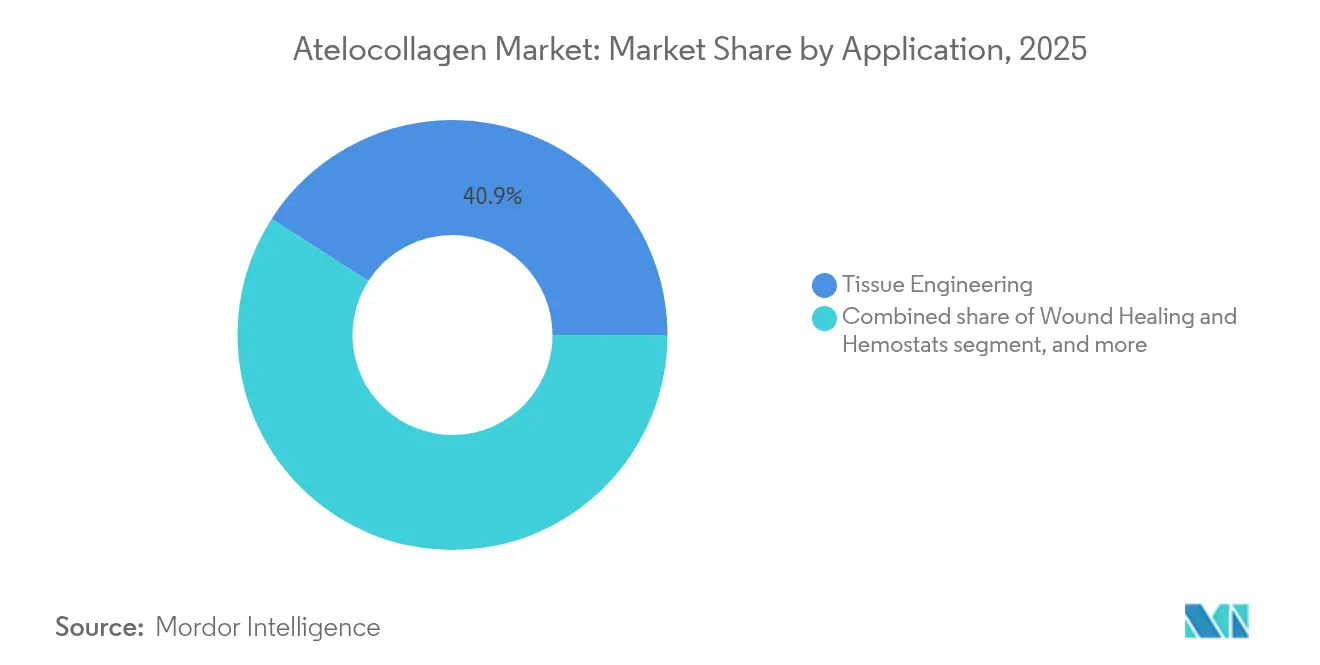

- By application, tissue engineering captured 40.92% of 2025 revenue; drug-delivery and cell-carrier systems will grow the fastest at 7.55% CAGR to 2031.

- By end user, pharmaceutical and biotechnology companies consumed 38.05% in 2025, whereas aesthetic clinics and hospitals show the highest 8.05% CAGR outlook.

- By geography, North America led with 42.85% revenue in 2025; Asia-Pacific is forecast to expand at 6.32% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Atelocollagen Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancing Regenerative Medicine Approvals | +1.2% | Global; early adoption in North America & EU | Medium term (2-4 years) |

| Rapid Growth in Cosmetic Procedures | +0.9% | North America & APAC core; spill-over to EU | Short term (≤ 2 years) |

| Strategic Industry Partnerships and Licensing Deals | +0.7% | Global | Medium term (2-4 years) |

| Surge in Marine Collagen Adoption | +0.8% | APAC core; expanding to North America & EU | Long term (≥ 4 years) |

| Expansion of 3-D Bioprinting Applications | +0.6% | North America & EU; emerging in APAC | Long term (≥ 4 years) |

| Favorable Regulatory Classifications for Collagen Implants | +0.5% | Global; led by FDA & EMA frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advancing Regenerative-Medicine Approvals

Regulators now fast-track collagen devices that present robust safety dossiers. The FDA’s December 2024 Symvess decision—67% primary patency at 30 days—sets a precedent for acellular vascular implants. Similar rigor applies to orthopedics, where bilayer atelocollagen scaffolds achieve hyaline cartilage integration in 12-week animal trials. Retrospective studies on paraspinal injections report statistically significant pain relief, widening musculoskeletal indications. China’s Class II/III framework for recombinant collagen offers predictable dossiers and reduces approval latency[3]PubMed Central Editors, “Class II and III designation for recombinant collagen devices in China,” ncbi.nlm.nih.gov. Collectively, these milestones expand the atelocollagen market into vascular, spinal, and chondral niches that demand high biocompatibility.

Rapid Growth in Cosmetic Procedures

The global medical-aesthetics sector is rising from USD 20 billion toward USD 27 billion by 2028, with injectables logging 12–14% annual growth. New cross-linked porcine dermal fillers show zero hypersensitivity, eliminating traditional pre-test delays. Younger consumers pursue preventive regimens, driving repeat visitation and product-tier diversification. An upcoming FDA advisory panel will evaluate decolletage filler indications, expanding collagen’s usable anatomy. Social-media micro-influencers and clinic-locator apps now funnel traffic to regional providers, sustaining volume even amid economic cycles—an effect that reinforces the atelocollagen market’s defensive characteristics.

Strategic Industry Partnerships and Licensing Deals

Cross-sector partnerships shorten time-to-market and share scale economics. Evonik’s vegan-collagen partnership with Jland Biotech delivers fermentation-derived material with superior dermal diffusion. Brenntag’s distribution pact with Cambrium introduces NovaColl to the UK, Ireland, and France, leveraging logistics expertise to penetrate the cosmetics supply chain. Darling Ingredients’ Nextida platform extends collagen peptides into metabolic-health supplements, demonstrating scope for cross-category synergies. PlantForm’s Nicotiana-based recombinant collagen points toward agricultural bioprocessing that could upend animal sourcing. These alliances inject technology and market-access capital that enlarges the atelocollagen market footprint.

Surge in Marine Collagen Adoption

Sustainability, cultural acceptance, and reduced zoonotic risk fuel marine sourcing. Thai Union’s USD 30 million tuna-skin plant yields 200 tonnes annually, aimed at premium Asian nutraceuticals. Clinical data show marine di- and tri-peptides raise skin hydration and elasticity in 8-week cohorts. Enzymatic extraction enhances thermal stability, allowing marine atelocollagen to survive broader processing windows and reach distant markets without denaturation. As fisheries monetize by-products, the circular-economy narrative resonates with consumers, strengthening brand equity while expanding the atelocollagen market across supplements, cosmetics, and biomedical devices.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production Cost and Complex Processing | -0.8% | Global; particularly affecting emerging markets | Short term (≤ 2 years) |

| Availability of Alternative Biomaterials | -0.6% | Global; with varying regional preferences | Medium term (2-4 years) |

| Cold-Chain and Storage Challenges | -0.4% | Global; acute in regions with limited infrastructure | Short term (≤ 2 years) |

| Regulatory Uncertainty for Novel Recombinant Collagen | -0.3% | Global; with regional regulatory variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Cost and Complex Processing

Manufacturers balance triple-helix integrity, sterility, and scalable yields. Recombinant systems often lack prolyl-hydroxylation capacity, requiring co-expression of human-like enzymes or costly post-processing. Fed-batch fermentation can reach 19 g/L but needs capital-intensive bioreactors and sophisticated oxygen control. Animal-sourced atelocollagen demands cold-chain isolation, pepsin de-telopeptidation, and multi-stage purification, inflating cost of goods on a per-gram basis. Freeze–thaw optimization can enhance elasticity but adds handling steps that lengthen cycle time. These factors compress margins in price-sensitive geographies and slow penetration into publicly funded health systems, tempering near-term expansion of the atelocollagen market.

Availability of Alternative Biomaterials

Chitosan hemostats such as HemCon and Celox outperform collagen pads in high-flow trauma via rapid ionic clot formation. PDLLA biostimulators deliver long-lasting dermal volumization, appealing to patients seeking fewer retreatments. Gelatin-methacrylate fibrin glues gel within 2 seconds on wet tissue, surpassing collagen sealants in adhesion strength. Reactive kaolin composites achieve arterial hemostasis in 30 seconds, beating traditional collagen sponges. Such alternatives siphon share where price or speed outrank long-term biocompatibility, capping the upper bound of atelocollagen market adoption in selected indications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine Innovation Drives Sustainability

Bovine collagen retained 46.12% revenue in 2025 thanks to abundant raw supply and broad clinical precedent. Yet fish-derived formats are expanding at 7.12% CAGR as processors valorize waste streams and capitalize on cultural acceptance. Thai Union’s ThalaCol tuna-skin line anchors Asia-Pacific growth, while cod-skin matrices enter EU wound-care tenders. Recombinant human collagen platforms such as Evonik’s Vecollan address supply-chain variability and eliminate animal-origin risk. Plant-derived constructs from Nicotiana benthamiana promise carbon-light footprints once downstream purification reaches scale. Porcine collagen remains essential in certain dental and cardiac meshes where mechanical compliance matches native tissue.

The atelocollagen market size for marine formats is projected to cross USD 2.23 billion by 2031, a leap reflecting sustainability branding, enhanced peptide bioactivity, and supportive government recycling targets. While bovine supply remains cost-competitive, climate-linked zoonotic threats and cultural dietary shifts push formulators toward fish and recombinant options, broadening the total addressable atelocollagen market.

By Application: Drug-Delivery Systems Accelerate Growth

Tissue engineering led demand with 40.92% share in 2025, underpinned by nerve conduits, orthopedic fillers, and periodontal membranes. Bilayer atelocollagen scaffolds restore articular cartilage by fostering hyaline-like regeneration within three months. Drug-delivery and cell-carrier systems register the quickest trajectory, growing 7.55% CAGR on the back of nucleic-acid duplex formation and sustained-release microbeads. The atelocollagen market size for drug-delivery systems is projected to hit USD 2.19 billion by 2031, as ophthalmic gels, oncologic depots, and vaccine adjuvants shift toward collagen-stabilized formats.

Aesthetic fillers sustain steady escalation alongside rising procedure volumes. Zero hypersensitivity porcine fillers, free of pre-testing, now treat facial and hand rejuvenation with confidence. Wound-healing and hemostats continue to penetrate trauma centers where collagen scaffolds accelerate re-epithelialization and reduce hospital stays versus synthetic foams. Emerging 3-D bioprinting implants for breast and soft-tissue reconstruction foreshadow multi-modal device revenues converging on the atelocollagen market.

By End User: Aesthetic Clinics Drive Adoption

Pharmaceutical and biotech firms absorbed 38.05% of consumption in 2025, leveraging GMP-grade atelocollagen for clinical-trial substrates and commercial drug conjugates. Research institutes and CROs rely on consistent batch performance to interpret pre-clinical efficacy. Yet aesthetic clinics and hospitals advance at 8.05% CAGR as consumer appetite for minimally invasive treatments broadens across age cohorts. Clinic chains deploy digital booking engines and bulk-buy contracts, stabilizing offtake volumes and reinforcing the atelocollagen market’s services component.

Orthopedic and wound-care centers represent incremental upside as collagen meniscal implants like RejuvaKnee gain FDA clearance and dermal matrices such as Cohealyx show 7-day wound-bed integration. Specialty surgical facilities experiment with collagen-based adhesives that reduce intra-operative bleeding, shortening stay lengths and generating pay-for-performance incentives. As payer systems reimburse outcome-linked bundles, atelocollagen suppliers that document faster recovery will win formulary preference, deepening institutional penetration.

Geography Analysis

North America commanded 42.85% of global revenue in 2025. FDA clearances for Symvess and RejuvaKnee illustrate a regulatory culture that rewards robust clinical evidence. Domestic manufacturers also benefit from a mature reimbursement environment and a deep technical workforce. Market-share realignment is underway, however, as compliance lapses—such as recent warnings on production quality—create space for new entrants with automated, paperless manufacturing lines.

Europe maintains a strong foothold, backed by MDR 2017/745 and harmonized standards for collagen characterization. Precision-fermented NovaColl debuted across the UK, Ireland, and France, reflecting consumer demand for vegan and skin-identical inputs. National-level tendering for advanced wound care favors suppliers with CE-marked, evidence-backed products, sustaining predictable procurement cycles even amid broader economic volatility.

Asia-Pacific exhibits the highest growth, at 6.32% CAGR to 2031, as expanding healthcare budgets and medical-tourism corridors enlarge the patient base. Government support for biomanufacturing, combined with regulatory clarity for recombinant collagen, reduces entry barriers. Local firms leverage cost-effective production to supply domestic demand and export worldwide, often through joint ventures that marry international quality standards with regional logistics agility. The atelocollagen market share in Asia-Pacific is expected to rise by 3.9 percentage points by 2031, driven principally by marine-source output and aesthetic-clinic expansion.

Latin America, the Middle East, and Africa account for smaller proportions today but represent untapped growth pools. Infrastructure upgrades and skill-transfer programs are laying foundations for future collagen processing hubs, particularly in fisheries-rich coastal economies. Multinationals are piloting distribution partnerships to ensure cold-chain reliability and localized regulatory filings, positioning themselves for demand inflection as disposable incomes rise.

Competitive Landscape

Moderate fragmentation characterizes the atelocollagen market, with platform innovators competing alongside vertically integrated incumbents. Top suppliers safeguard quality through in-house enzymatic de-telopeptidation, medical-grade purification, and ISO-compliant documentation. Evonik’s Vecollan fermentation platform reduces batch-to-batch variability, positioning the firm for high-end device contracts. CollPlant differentiates through recombinant human collagen suitable for 3D printing, entering co-development deals with implant manufacturers.

Strategic acquisitions target technology gaps: ingredient leaders buy marine-collagen processors to secure sustainable supply, while device companies license plant-based rhCollagen to hedge against livestock-borne pathogens. Distribution alliances such as Brenntag-Cambrium ensure geographic reach for vegan offerings without duplicating infrastructure. Quality systems are emerging as pivotal: recent FDA enforcement actions against manufacturers that failed GMP obligations shifted hospital tenders toward compliant rivals.

Digitally enabled personalization is gaining prominence. Firms integrate AI-driven dosing models and tele-consultation support to enhance therapy adherence, particularly in aesthetics and chronic wound management. From a financial perspective, investor focus remains on cost-reduction technologies—continuous bioprocessing, single-use fermenters, and automated lyophilization—that can compress margin-pressure cycles and sustain long-term profitability.

Atelocollagen Industry Leaders

KOKEN Co., Ltd.

Advanced BioMatrix (BICO)

DSM-Firmenich

Nitta Gelatin Inc.

Rousselot (Darling Ingredients)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Thai Union invested USD 30 million in a marine collagen plant with 200-tonne annual capacity, releasing ThalaCol tuna-skin collagen for premium Asian markets.

- April 2025: AVITA Medical unveiled Cohealyx, a collagen dermal matrix accelerating wound-bed formation within 7 days compared with incumbent products.

- January 2025: Brenntag and Cambrium launched NovaColl in the UK, Ireland, and France, delivering 100% skin-identical collagen via precision fermentation.

- April 2025: Evonik introduced Vecollan, a commercial-scale, non-animal, fermentation-derived collagen targeting medical devices.

- March 2024: Evonik partnered with Jland Biotech to supply vegan collagen to cosmetic formulators, enhancing skin absorption profiles.

Global Atelocollagen Market Report Scope

As per the scope of the report, atelocollagen is a type of collagen that undergoes a specific process of removing the telopeptides from the collagen molecule, resulting in reduced antigenicity. It has a wide range of applications in tissue culture research, clinical medicine, and cosmetics.

The atelocollagen market is segmented by source, application, end user, and geography. By source, the market is segmented into bovine collagen, porcine collagen, and other sources. The other sources segment includes mouse collagen and rat collagen. By application, the market is segmented into tissue engineering, wound healing, cosmetics, and other applications. By end user, the market is segmented into pharmaceutical and biotechnology companies, research institutes and laboratories, and other end users. The report also covers the market size and forecasts for the atelocollagen market in 17 countries across major regions. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Bovine Collagen |

| Porcine Collagen |

| Fish / Marine Collagen |

| Recombinant Human Collagen |

| Other Sources |

| Tissue Engineering |

| Wound Healing & Hemostats |

| Aesthetic & Dermal Fillers |

| Drug Delivery & Cell Carrier Systems |

| Other Applications |

| Pharmaceutical & Biotechnology Companies |

| Research Institutes & CROs |

| Aesthetic Clinics & Hospitals |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Bovine Collagen | |

| Porcine Collagen | ||

| Fish / Marine Collagen | ||

| Recombinant Human Collagen | ||

| Other Sources | ||

| By Application | Tissue Engineering | |

| Wound Healing & Hemostats | ||

| Aesthetic & Dermal Fillers | ||

| Drug Delivery & Cell Carrier Systems | ||

| Other Applications | ||

| By End User | Pharmaceutical & Biotechnology Companies | |

| Research Institutes & CROs | ||

| Aesthetic Clinics & Hospitals | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the atelocollagen market in 2026?

The atelocollagen market is valued at USD 10.56 billion in 2026 and is forecast to grow at a 5.77% CAGR to 2031.

Which source segment leads the atelocollagen market?

Bovine collagen leads with 46.12% revenue share in 2025, while fish/marine collagen is the fastest growing at 7.12% CAGR.

What is driving demand for atelocollagen in drug-delivery systems?

Rising interest in controlled release therapies and cell-carrier platforms is pushing drug-delivery applications to expand at a 7.55% CAGR through 2031.

Which region is expected to grow fastest?

Asia-Pacific shows the highest projected growth at 6.32% CAGR, supported by healthcare spending increases and marine collagen investments.

How are regulators influencing market growth?

The FDA’s clearance of novel collagen implants and the EU’s MDR 2017/745 provide clear pathways, encouraging device approvals and clinical uptake.

What major technological trend is shaping future opportunities?

3D bioprinting of pure collagen bioinks is enabling patient-specific implants that gradually degrade while fostering natural tissue regeneration.

Page last updated on: