Infectious Disease Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

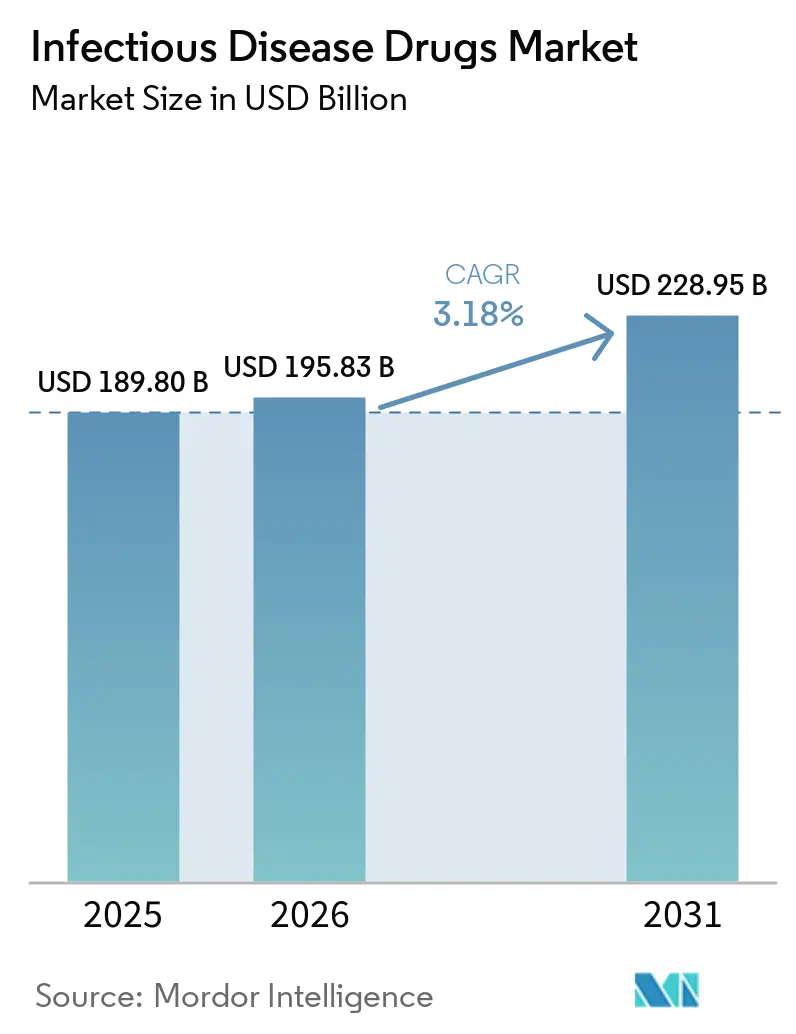

| Market Size (2026) | USD 195.83 Billion |

| Market Size (2031) | USD 228.95 Billion |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Infectious Disease Drugs Market Analysis by Mordor Intelligence

The Infectious Disease Drugs Market size was valued at USD 189.80 billion in 2025 and is estimated to grow from USD 195.83 billion in 2026 to reach USD 228.95 billion by 2031, at a CAGR of 3.18% during the forecast period (2026-2031).

Tight cost-containment policies, stronger pharmacovigilance rules, and value-based purchasing models keep growth steady rather than explosive. At the same time, artificial-intelligence drug-discovery tools shorten lead-time from target to candidate, giving developers a realistic path to replenish portfolios emptied by resistance. Major pharmaceutical companies are pairing with tech firms to offset scientific risk, while governments add milestone payments that de-risk late-stage R&D. Heightened anxiety over active-ingredient shortages—67% of antimicrobial API Drug Master Files sit in India and China—has led regulators to talk openly about reshoring. Taken together, the infectious disease drugs market is moving from volume-driven expansion to resilience-driven innovation.

Key Report Takeaways

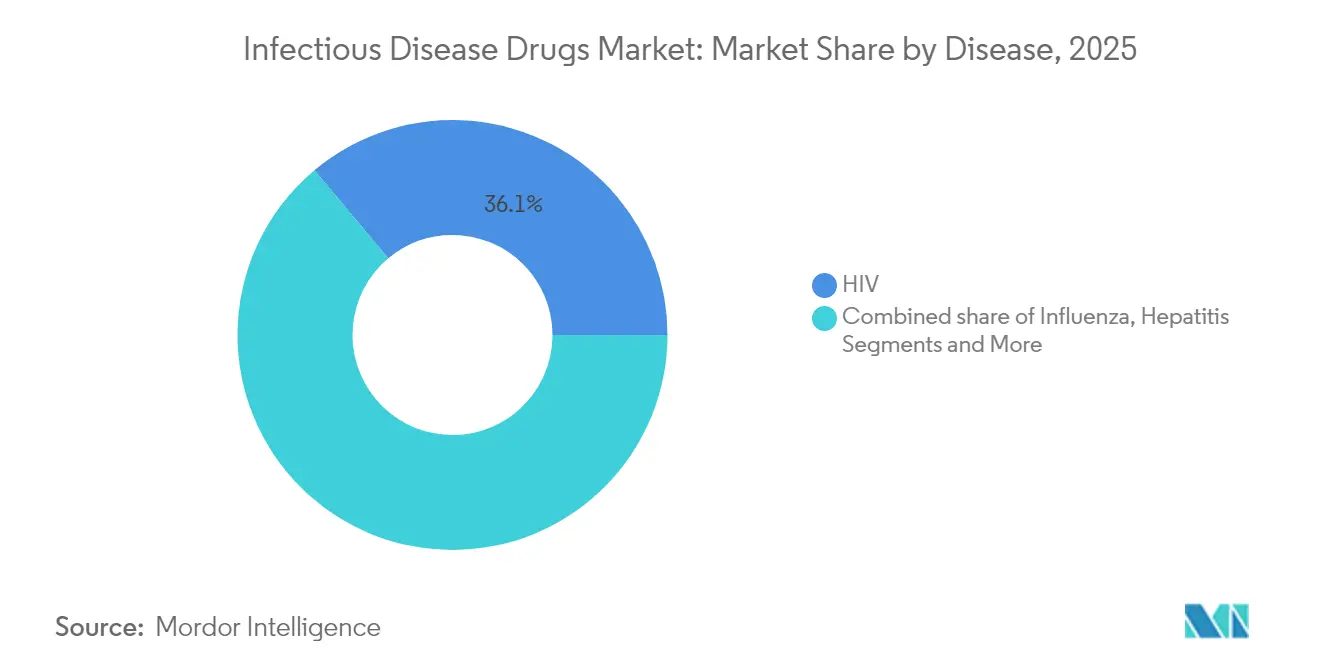

- By disease, HIV therapies led with 36.10% of the infectious disease drugs market share in 2025, while hepatitis drugs are forecast to grow the fastest at a 3.98% CAGR to 2031.

- By treatment class, antivirals accounted for 40.80% of the infectious disease drugs market share in 2025; phage and CRISPR therapies are projected to expand at a 5.41% CAGR through 2031.

- By drug type, small molecules controlled 62.90% of the infectious disease drugs market size in 2025, yet biologics and monoclonal antibodies are expected to post a 5.96% CAGR from 2026 to 2031.

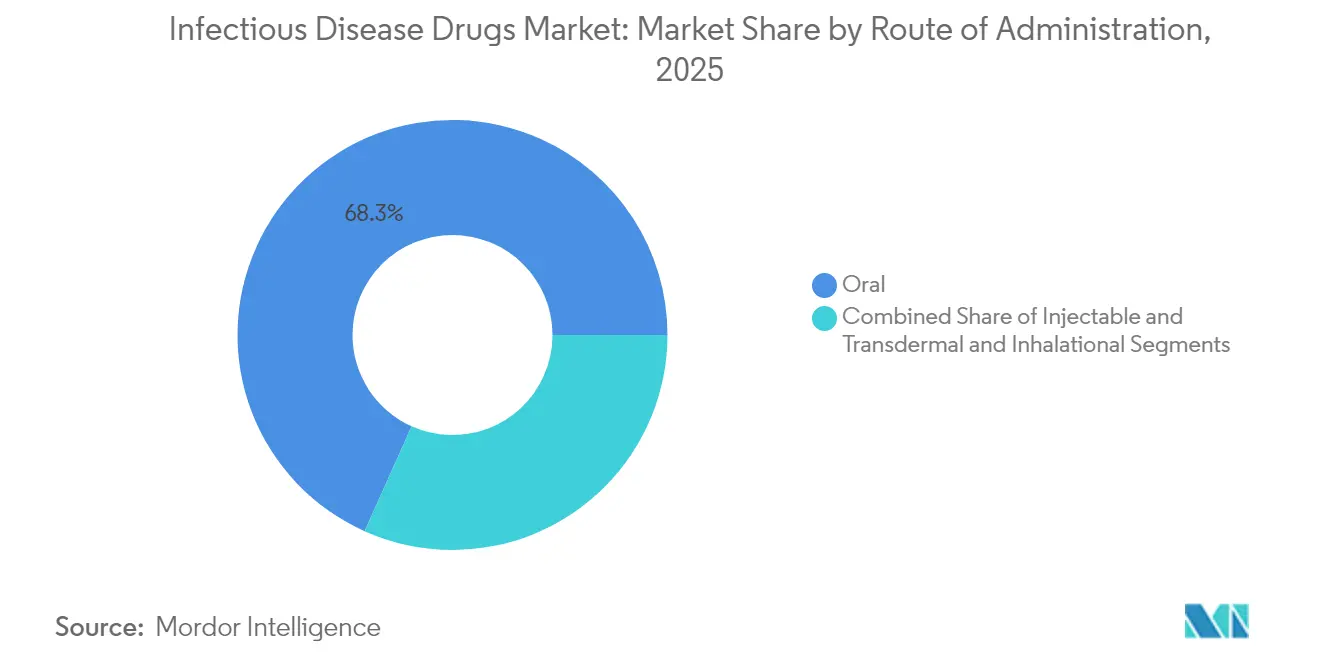

- By route of administration, oral products dominated with 68.30% of the infectious disease drugs market share in 2025, while injectables are forecast to advance at a 6.18% CAGR through 2031.

- By distribution channel, hospital pharmacies held 52.05% of the infectious disease drugs market share in 2025; online pharmacies are set to climb at an 7.85% CAGR over the outlook period.

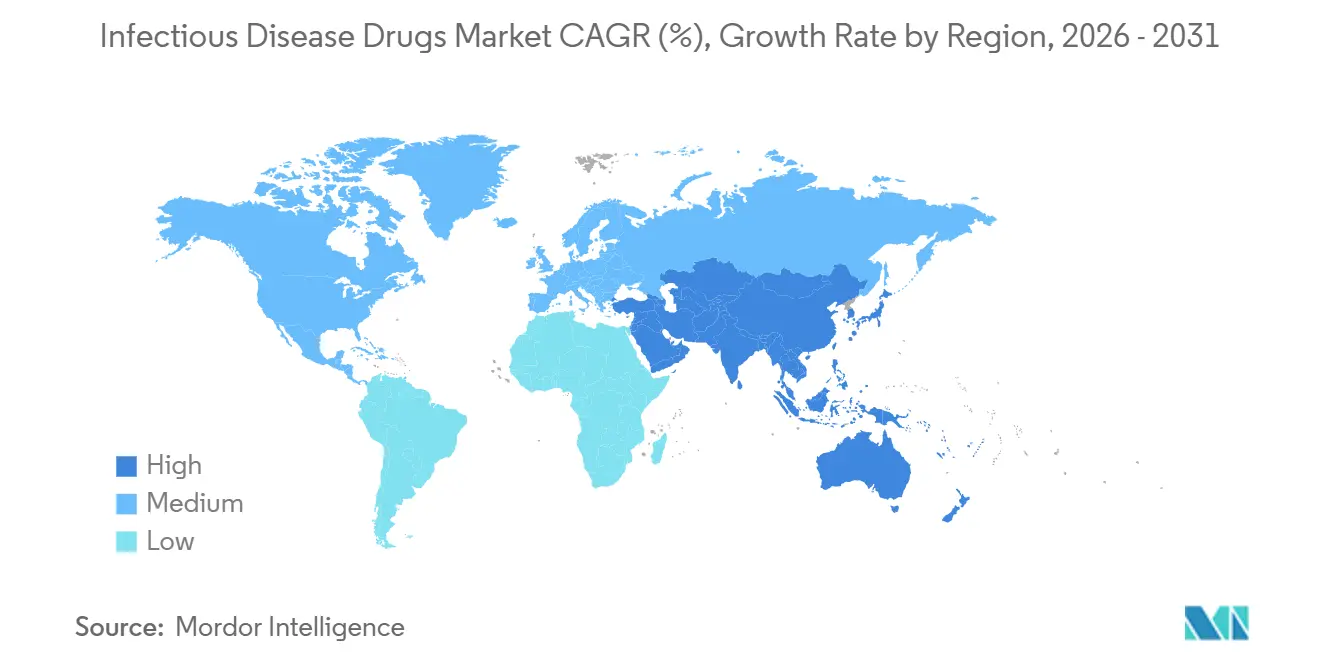

- By region, North America captured 36.20% of the infectious disease drugs market share in 2025; Asia-Pacific is positioned to lead growth at a 7.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Infectious Disease Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising awareness initiatives by governments & NGOs | +0.8% | Sub-Saharan Africa, Southeast Asia | Medium term (2-4 years) |

| Growing prevalence of infectious diseases | +0.9% | APAC, MEA | Long term (≥ 4 years) |

| Expanding funding & R&D investments | +0.7% | North America, EU | Medium term (2-4 years) |

| Accelerated regulatory pathways post-COVID-19 | +0.6% | US, EU, Japan | Short term (≤ 2 years) |

| Long-acting injectables boosting adherence | +0.5% | High-income markets | Medium term (2-4 years) |

| AI-driven antimicrobial discovery platforms | +0.4% | North America, EU, China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Infectious Diseases

Drug-resistant pathogens claim around 700,000 lives every year, underscoring a structural demand for better medicines. Tuberculosis now affects 10.8 million people, with resistant strains spreading quickly.[1]B. Zhao et al., “Targeting de Novo Purine Biosynthesis for Tuberculosis Treatment,” Nature, nature.comArtemisinin-resistant malaria has been confirmed in Rwanda and Tanzania, jeopardizing earlier public-health gains.[2]T. A. Ndikumana et al., “Emergence of Artemisinin Partial Resistance in Africa: How Do We Respond?” The Lancet Infectious Diseases, thelancet.com Surveillance in Uganda shows 11% of children harbor partial resistance to front-line malaria therapy. Aging populations, cancer-related immunosuppression, and climate-shifted vector habitats layer further demand on the infectious disease drugs market. Collectively, these epidemiological pressures sustain mid-single-digit growth for specialized therapies despite stewardship curbs.

AI-Driven Antimicrobial Discovery Platforms

Machine-learning engines now sift chemical libraries in weeks, not years. Eli Lilly’s USD 100 million pact with OpenAI illustrates pharma’s largest single AI commitment to tackle resistance. CRISPR-optimized phage LBP-EC01 is entering Phase 2 trials with USD 23.9 million in BARDA funding. SNIPR Biome dosed the first volunteers with a genome-edited antibiotic that spares commensal flora. Predictive algorithms flag resistance pathways early, guiding chemists toward compounds less likely to fail in vivo. As platform proof points accumulate, capital flows tilt toward AI-native pipeline builders, reshaping the infectious disease drugs market’s innovation map.

Expanding Funding & R&D Investments

The AMR Action Fund seeks two to four fresh antibiotics by 2030 and counts Lilly’s USD 100 million among its largest tickets. GSK pledged USD 45 million to the Fleming Initiative in London. The Novo Nordisk Foundation expanded early-stage help through CARB-X, while BARDA supplied multiple USD 20 million-plus grants to platform innovators. These injections push biotech firms to pursue high-risk targets that big pharma once avoided. As capital hurdles drop, a broader slate of candidates feeds the infectious disease drugs market pipeline.

Accelerated Regulatory Pathways Post-COVID-19

The FDA cleared cefepime–enmetazobactam for complicated UTIs under GAIN Act incentives that add five years of exclusivity. Rezzayo won approval for invasive candidiasis after a priority review. China’s NMPA signed off on 32 new drugs in a single month, many targeting resistant infections. Breakthrough Therapy and PRIME designations now favor antimicrobials that address clear unmet need. Shorter review clocks mean revenue arrives earlier, partially offsetting historically low net-present-value scores for antibiotics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low diagnosis & treatment penetration in developing regions | -0.7% | Sub-Saharan Africa, Southeast Asia, rural Latin America | Long term (≥ 4 years) |

| Adverse side-effects & toxicity profiles | -0.5% | Global | Medium term (2-4 years) |

| Antimicrobial stewardship curbing prescriptions | -0.6% | North America, EU, rising in APAC | Short term (≤ 2 years) |

| API supply-chain fragility & geopolitics | -0.8% | US, EU, global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Antimicrobial Stewardship Curbing Prescriptions

Hospitals now require pre-authorization for broad-spectrum antibiotics, cutting usage by up to 30% in some systems. Remote telehealth visits, however, escape many controls, prompting fresh audit tools. The European Union blueprint is spreading worldwide, formalizing daily-dose caps and treatment-length ceilings. While stewardship slows units sold, it is catalyzing demand for narrow-spectrum therapies positioned as resistance-sparing, thus reshaping revenue composition inside the infectious disease drugs market.

API Supply-Chain Fragility & Geopolitics

Two-thirds of antimicrobial API registrations sit in India and China, exposing pharmaceutical companies to single-region shocks. China’s 2023 Anti-Espionage Law halted several quality inspections, threatening Europe-bound shipments. Forty percent of cephalosporin APIs already face shortage notices, forcing buyers into premium spot contracts. Western governments are discussing strategic stockpiles and on-shore incentives, yet capital build-out remains slow. In the interim, manufacturers diversify toward Mexico and Southeast Asia, but the transition timeline stretches risk into the forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: HIV Dominance Faces Hepatitis Acceleration

HIV therapies held 36.10% of 2025 revenue, giving the infectious disease drugs market a core cash generator that funds riskier pipeline bets. Long-acting cabotegravir–rilpivirine autoinjectors, administered every two months, improved real-world viral suppression rates, lifting lifetime adherence and revenue consistency. In contrast, hepatitis treatments are projected to grow at a 3.98% CAGR, courtesy of bulevirtide’s 90% sustained virologic response in hepatitis D trials.Eliminating chronic hepatitis outcomes is a priority for payers aiming to curb organ-transplant costs. Tuberculosis therapies ride policy urgency as PurF inhibitor JNJ-6640 posts potent activity against multidrug-resistant strains. Malaria portfolios focus on triple combination regimens to offset artemisinin resistance documented in East Africa. Influenza antivirals gain from surveillance systems built during COVID-19, while opportunistic infection drugs rise with cancer-therapy-driven immunosuppression.

The hepatitis surge widens therapy choice, attracting regional generic entrants faster than in HIV, yet intellectual-property cliffs in 2028 could reshape pricing. Meanwhile, pipeline assets for tuberculosis and malaria often rely on nonprofit co-funding, implying slower commercialization but high public-health value. For HIV, the challenge is next-generation broadly neutralizing antibodies that aim to cut dosing to twice yearly, a shift with potential to defend market incumbency. Collectively, disease-specific dynamics keep the infectious disease drugs market balanced between cash-rich chronic segments and fast-rising acute segments.

By Treatment Class: Novel Therapeutics Challenge Antiviral Leadership

Antivirals generated 40.80% of 2025 revenue, reflecting entrenched HIV and hepatitis franchises. Yet novel phage and CRISPR-enabled treatments are on track for a 5.41% CAGR, racing to clinical proof via adaptive trials that measure rapid microbiological outcomes. Locus Biosciences’ LBP-EC01 achieved significant bacterial load reduction in urinary tract infections within 24 hours. Antibacterials find fresh life through long-acting glycopeptides that permit outpatient dosing, appealing to payers eager to cut hospital stays. Antifungals like fosmanogepix address the surge in Aspergillus resistance among transplant recipients. Antiparasitics counter emergent mutations with triple-drug blends now in Phase 3.

The infectious disease drugs market size for novel classes remains small today, yet pipeline density suggests rapid upside as regulators validate surrogate endpoints. Success will depend on companion diagnostics that confirm pathogen identity, ensuring narrow-spectrum agents reach the right patients and qualify for value-based contracts. In short, the competitive field is widening beyond chemical antivirals to include precision biological modalities.

By Drug Type: Biologics Surge Challenges Small-Molecule Dominance

Small molecules still command 62.90% of 2025 sales, but biologics and monoclonal antibodies are growing at a 5.96% CAGR, reflecting a decisive swing toward precision immunology. Nirsevimab reduced RSV respiratory infections by 70.1% with a single dose lasting five months. YUMAB’s platform screens 100 billion antibody sequences in under three months, allowing companies to progress from concept to IND quickly. For investors, biologics offer premium pricing, patentable epitopes, and reduced resistance risk.

This uptake raises manufacturing questions, especially for cold-chain logistics in emerging markets, yet mRNA technology promises faster facility builds. As biologics capture complex infection settings such as invasive fungal disease, small-molecule developers pivot toward oral backbones for outpatient use. The infectious disease drugs market size attached to biologics is thus poised to double its 2024 base by 2030 if current trial success holds.

By Route of Administration: Injectable Growth Reflects Precision Delivery Needs

Oral agents accounted for 68.30% of 2025 volume, preferred for adherence and cost. Injectables, however, show the highest growth at 6.18% CAGR, driven by depot technologies that extend therapeutic coverage. MIT’s crystalline depot kept antibiotic concentrations stable for two months in primate models. Weekly rezafungin simplifies invasive candidiasis therapy versus daily echinocandins. Transdermal films and inhaled powders gain traction for pulmonary infections, meeting guidelines that favor site-directed delivery.

The infectious disease drugs market share captured by injectables grows quickest in high-income countries where payers reward shorter hospital stays. Oral generics keep a floor under overall volume, but reimbursement models shifting toward outcome-based payments make long-acting injections financially attractive.

By Distribution Channel: Digital Transformation Accelerates Online Growth

Hospital pharmacies held 52.05% of 2025 revenue thanks to stewardship oversight and parenteral drug handling. Online pharmacies are on course for an 7.85% CAGR as telemedicine normalizes infection care. Same-day courier chains and data-logging smart packs reassure regulators about temperature-sensitive biologics. Retail chains integrate point-of-care antigen testing that informs immediate dispensing choices, trimming diagnostic delays.

This blended distribution future forces manufacturers to design packaging suitable for both shelf and courier routes. It also expands the infectious disease drugs market’s addressable base by easing access for rural patients who previously lacked specialty inventory. Regulatory bodies are responding with e-pharmacy licensure frameworks aimed at curbing antibiotic overuse in virtual settings.

Geography Analysis

North America retained 36.20% of 2025 sales, powered by BARDA grants that expedite late-stage trials and by insurers willing to reimburse novel mechanisms that reduce hospitalization. Accelerated FDA pathways encourage early launch, while Canada’s priority review vouchers extend the model region-wide. The United States remains exposed to API import risks, pushing federal proposals for tax credits on domestic fermentation plants. Mexico’s inclusion in continental supply chains offers near-shoring relief but still lacks large-scale sterile capacity.

Asia-Pacific is forecast to grow at a 7.28% CAGR, lifted by regulatory modernization and rising middle-class healthcare spend. China’s NMPA is clearing anti-infective NDAs faster than any peer agency, showing policy urgency on resistance. Singapore bankrolls bacteriophage hubs, while South Korea’s digital health ecosystem supports online antibiotic dispensing. India straddles its role as both API exporter and large therapy consumer, making quality assurance a strategic imperative. Japan, faced with the world’s oldest population median, funds infection prophylaxis in elder-care settings, adding steady volume to the infectious disease drugs market.

Europe balances stewardship-driven volume limits with high adoption of premium therapies that prove outcome gains. Germany and the United Kingdom bankroll basic AMR science, exemplified by the Fleming Initiative. EMA and HERA coordinate stockpiles to blunt shortage risk, a response to recent cephalosporin gaps. Eastern European states modernize procurement rules to attract biosimilar antivirals, boosting regional competitive intensity. The continent’s unified regulatory stance simplifies launch sequences, allowing companies to stage pan-EU rollouts that lift the infectious disease drugs market size more efficiently than piecemeal national filings.

Competitive Landscape

Market structure is moderately fragmented. Gilead, GSK, and Pfizer anchor HIV, hepatitis, and pneumococcal portfolios, supplying scale advantages in manufacturing and distribution. Yet specialized biotech challengers such as Locus Biosciences and SNIPR Biome are carving niches in pathogen-specific therapy, often partnering with large firms post-Phase 2 for capital-intensive trials. AI partnerships are the new competitive currency: Eli Lilly’s OpenAI link-up represents a template others aim to replicate.

Portfolio differentiation now hinges on three fronts: resistance-sparing mechanisms, long-acting formulations, and companion diagnostics. Pfizer’s vaccine franchise insulates earnings, while GSK’s RSV antibody opens a defensive moat in pediatrics. Meanwhile, emerging players court value-based contracts, promising reduced ICU days per treated episode. M&A chatter centers on companies holding Phase 2 proof for narrow-spectrum assets that fit stewardship goals.

Competition also manifests in supply-chain investments. Western incumbents commit capex to domestic API plants, seeking first-mover advantage in reliability. Small biotechs leverage contract manufacturing in Singapore and Ireland to sidestep geopolitical bottlenecks. As a result, the infectious disease drugs market is witnessing a blend of consolidation at scale and diversification at the edges.

Infectious Disease Drugs Industry Leaders

AbbVie Inc

Gilead Sciences, Inc.

GlaxoSmithKline plc

F Hoffmann-La Roche, Ltd

Merck & Co, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: University of Otago researchers mapped the full structure of a key Mycobacterium tuberculosis efflux pump, opening routes for resistance-bypassing drugs.

- May 2025: Roche advanced zosurabalpin into Phase 3 for carbapenem-resistant Acinetobacter baumannii, the first novel Gram-negative agent in 50 years.

- May 2025: Gilead reported that 36% of chronic hepatitis D patients kept viral RNA undetectable nearly two years after stopping bulevirtide.

- April 2025: Johns Hopkins showed navitoclax cut tuberculosis lung necrosis by 40% when paired with first-line antibiotics.

Research Methodology Framework and Report Scope

Market Definition and Key Coverage

Our study defines the infectious disease drugs market as global revenue from prescription-only pharmacological agents, namely antivirals, antibacterials, antifungals, and antiparasitics, that treat or prophylactically suppress human infections across every clinical setting. We count finished-dose products sold through hospital, retail, and online pharmacies; pipeline compounds, vaccines, and veterinary therapeutics are outside the quantified scope.

Scope Exclusion: Sales of stand-alone vaccines, diagnostic kits, and over-the-counter antimicrobial creams are excluded to maintain comparability.

Segmentation Overview

- By Disease

- HIV

- Influenza

- Hepatitis (A, B, C, D & E)

- Tuberculosis

- Malaria

- Opportunistic & other infections

- By Treatment Class

- Antiviral

- Antibacterial

- Antiparasitic

- Antifungal

- Novel phage & CRISPR-based therapeutics

- By Drug Type

- Small-molecule

- Biologic / mAb

- Vaccine-derived therapeutics

- By Route of Administration

- Oral

- Injectable (IV, IM, SC)

- Transdermal & Inhalational

- By Distribution Channel

- Hospital Pharmacies

- Retail & Chain Pharmacies

- Online Pharmacies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts engage infectious-disease physicians, hospital pharmacy directors, reimbursement advisors, and regulators across North America, Europe, Asia-Pacific, and Latin America. Interviews and structured surveys refine therapy adoption rates, treatment duration, and discounting practices, filling gaps that desk work leaves open.

Desk Research

We begin by collecting baselines from the WHO, CDC, ECDC, and national health ministries that publish incidence, treatment coverage, and antimicrobial consumption data. Country prescription audits, tariff records, and customs codes from sources such as IQVIA MIDAS, UN Comtrade, and OECD Health Accounts shape initial demand curves. Our team then taps financial filings, pipeline disclosures, and white papers from the International Federation of Pharmaceutical Manufacturers, while Mordor's paid D&B Hoovers and Dow Jones Factiva portals enrich revenue splits and price corridors. These sources illustrate the mix; many additional documents are screened to reconcile anomalies.

Market-Sizing & Forecasting

We construct a top-down model starting with country prevalence and standard-of-care treatment rates, building drug consumption volumes that are priced using blended ex-manufacturer averages. Select bottom-up checks, including supplier roll-ups for five key molecule classes and sampled average selling price times volume, calibrate totals. Key variables like HIV and hepatitis treated patient pools, multi-drug-resistant bacterial case growth, average defined daily doses, generic erosion curves, and healthcare spend per capita feed a multivariate regression that projects values through 2030. Regional proxy ratios bridge molecule-level gaps before final aggregation.

Data Validation & Update Cycle

Model outputs undergo algorithmic variance checks, peer analyst challenge sessions, and senior analyst sign-off. We refresh results annually, and material events such as patent cliffs, guideline shifts, or pandemics trigger interim recalculations so clients always receive the latest calibrated view.

Why Our Infectious Disease Drugs Baseline Commands Confidence

Published estimates often diverge because firms apply different therapy baskets, pricing points, and update cadences.

Key gap drivers emerge when others count only branded hospital injectables, embed vaccine revenue, or lock exchange rates at outdated parity, whereas Mordor aligns scope to all prescription therapeutics, converts at rolling annual averages, and refreshes each year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 189.8 B (2025) | Mordor Intelligence | |

| USD 84.9 B (2024) | Global Consultancy A | excludes antivirals and retail channel, uses static incidence inputs |

| USD 243.4 B (2024) | Industry Data Provider B | combines vaccines and veterinary sales, applies list prices without discount factors |

| USD 239.2 B (2025) | Regional Consultancy C | aggregates drugs plus diagnostics spend, projects with single-factor CAGR |

Taken together, the comparison shows that our disciplined scope, live currency treatment, and dual-path validation deliver a balanced baseline clients can track, replicate, and defend in strategic discussions.

Key Questions Answered in the Report

What is the current size of the infectious disease drugs market?

The infectious disease drugs market was valued at USD 195.83 billion in 2026 and is projected to reach USD 228.95 billion by 2031.

Which disease segment holds the largest share?

HIV therapies led with 36.10% of 2025 revenue, making them the largest segment within the infectious disease drugs market.

Why are biologics growing faster than small molecules?

Biologics deliver pathogen-specific action with lower resistance potential, helping them grow at a 5.96% CAGR compared with the wider market’s 3.18% pace.

How do stewardship programs influence market growth?

Stewardship rules trim broad-spectrum antibiotic use by up to 30%, slowing unit growth but pushing demand toward precision therapies that satisfy resistance-reduction goals.

What regions will drive future demand?

Asia-Pacific is forecast to post a 7.28% CAGR through 2031 thanks to regulatory acceleration, rising incomes, and high infectious-disease burden.

How is AI changing antimicrobial development?

AI platforms cut discovery timelines from years to months, exemplified by Eli Lilly’s OpenAI collaboration to identify candidates targeting drug-resistant bacteria.

Page last updated on: