Vitiligo Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

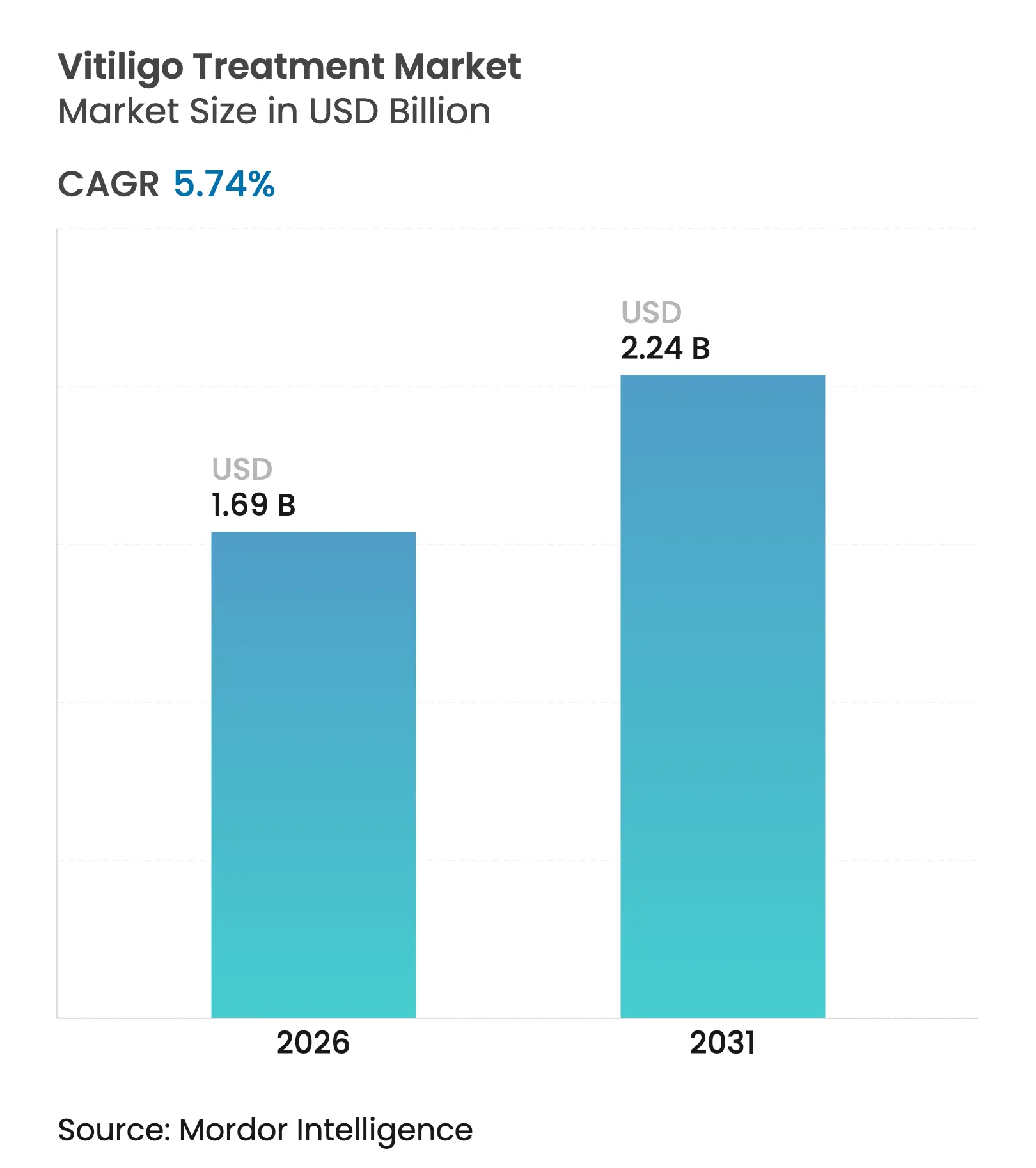

| Market Size (2026) | USD 1.69 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 5.74 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Vitiligo Treatment Market Analysis by Mordor Intelligence

The vitiligo treatment market size is expected to grow from USD 1.60 billion in 2025 to USD 1.69 billion in 2026 and is forecast to reach USD 2.24 billion by 2031 at 5.74% CAGR over 2026-2031. This steady rise traces back to the first FDA-approved topical JAK inhibitor, growing patient awareness, and improved access to handheld phototherapy devices. Topical ruxolitinib cream collected USD 508 million revenue in 2024, showing strong early adoption. Non-segmental vitiligo remains the clinical priority because it affects larger patient pools, while segmental vitiligo gains momentum through targeted surgical innovations. Biologic therapies, now in late-stage pipelines, add precision treatment options that move beyond older steroid-based regimens. Asia-Pacific grows at double-digit pace as regulatory partnerships accelerate technology transfer and premium drug launches.

Key Report Takeaways

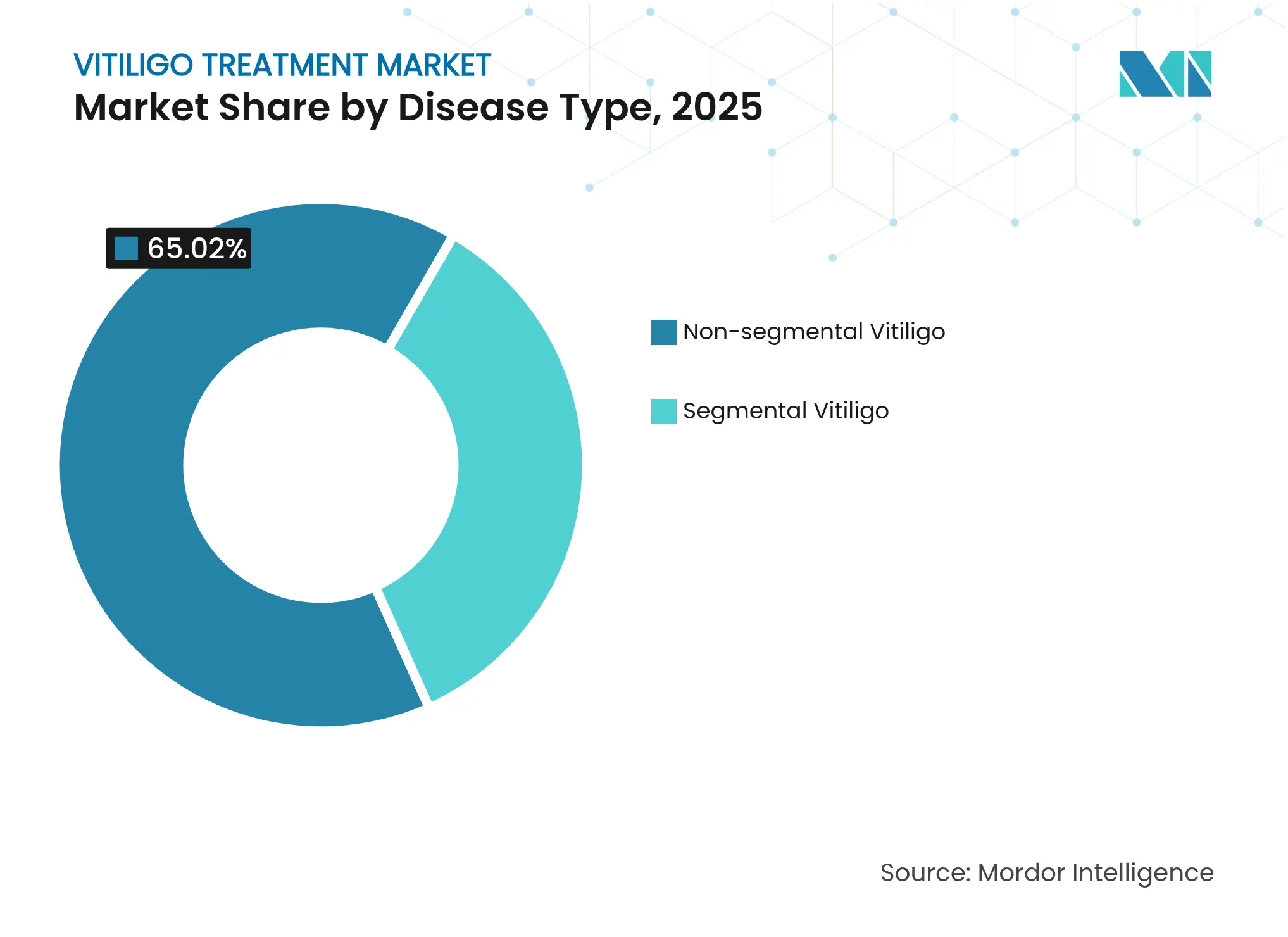

- By disease type, non-segmental vitiligo held 65.02% vitiligo treatment market share in 2025; segmental vitiligo is projected to expand at an 7.98% CAGR through 2031.

- By therapy, topical treatment commanded 45.92% of the vitiligo treatment market size in 2025, while biologic therapies are on track for a 15.56% CAGR to 2031.

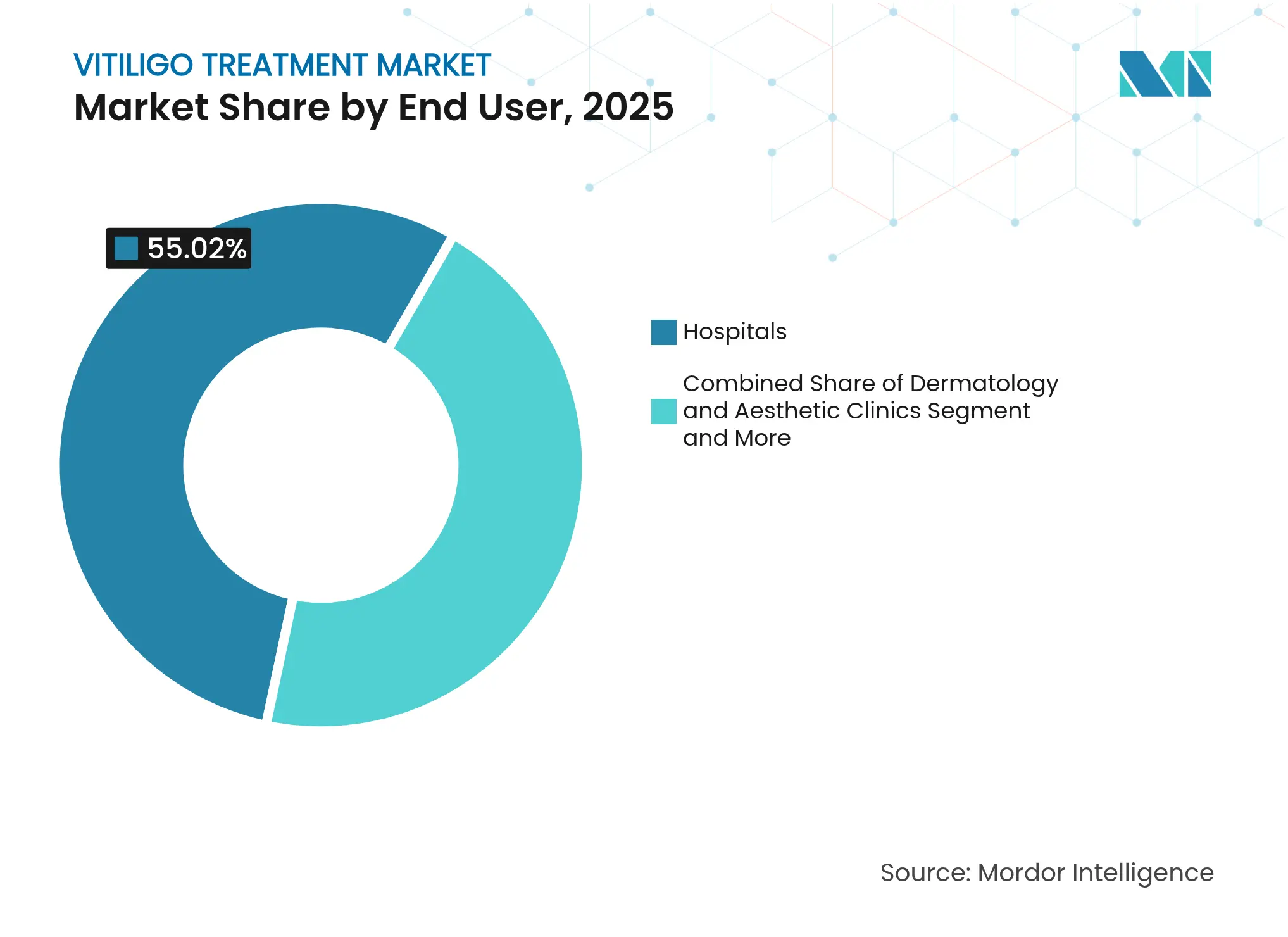

- By end user, hospitals retained 55.02% revenue share in 2025; home-care settings show the fastest growth at 10.71% CAGR through 2031.

- By distribution channel, hospital pharmacies led with 38.11% share of the vitiligo treatment market size in 2025, and online pharmacies are rising at a 12.58% CAGR.

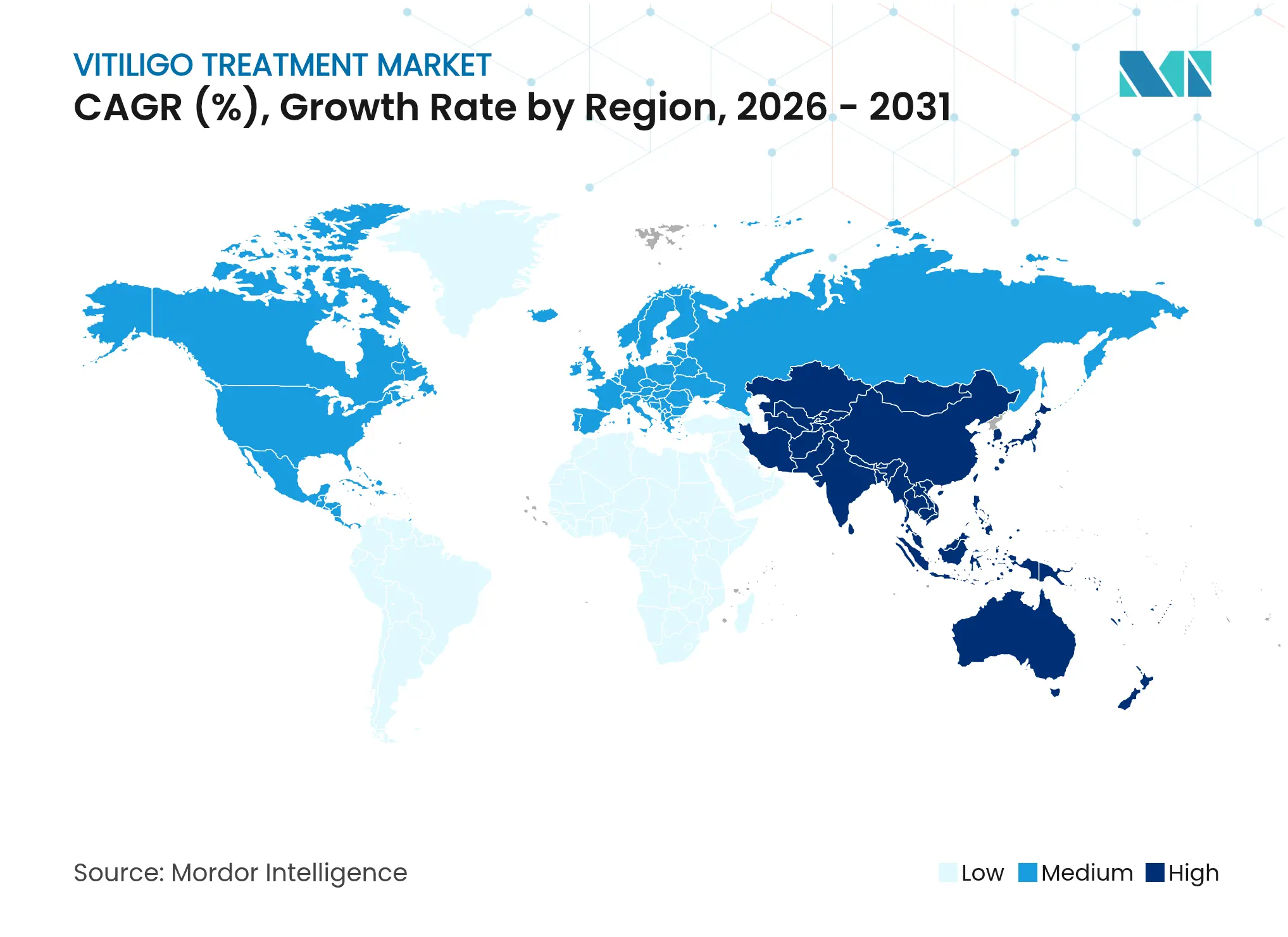

- By geography, North America captured 41.88% revenue in 2025, whereas Asia-Pacific is advancing at a 12.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Vitiligo Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence and growing public-health awareness

Rising prevalence and growing public-health awareness

| +1.2% | Global, highest in Asia-Pacific and MEA | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.2%

| Geographic Relevance:

Global, highest in Asia-Pacific and MEA

| Impact Timeline:

Medium term (2-4 years)

|

Regulatory incentives for orphan dermatology drugs

Regulatory incentives for orphan dermatology drugs

| +0.8% | North America & EU, spill-over to Asia-Pacific | Short term (≤ 2 years) | |||

Breakthrough approvals of topical JAK-inhibitor creams

Breakthrough approvals of topical JAK-inhibitor creams

| +1.5% | Global, early lead in North America and Europe | Short term (≤ 2 years) | |||

Technology advances in targeted and handheld phototherapy

Technology advances in targeted and handheld phototherapy

| +0.7% | Developed markets worldwide | Medium term (2-4 years) | |||

Aesthetic dermatology demand in emerging markets

Aesthetic dermatology demand in emerging markets

| +0.9% | Asia-Pacific core, spread to MEA and South America | Long term (≥ 4 years) | |||

AI-powered dermatology diagnostics

AI-powered dermatology diagnostics

| +0.6% | North America and Europe first | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Increasing prevalence of vitiligo and public-health awareness

Middle East and Africa studies report 3% prevalence, pushing health systems to embed vitiligo screening into routine dermatology visits. Awareness campaigns in Egypt and Palestine now reach communities where 62.8% of participants recognize vitiligo as treatable, boosting clinic visits. Higher visibility of effective therapies reduces stigma and encourages early presentation. Skin-of-color populations gain particular benefit, creating fresh demand for culturally competent care. Expanded patient pools support sustained revenue growth for device and drug makers.

Regulatory incentives for orphan / dermatology drugs

The FDA granted ruxolitinib cream orphan status and accelerated approval, shortening development cycles and providing seven-year exclusivity[1]Food and Drug Administration, “Drug Trials Snapshots: LITFULO,” fda.gov. Similar European pathways synchronize multi-region launches, raising initial uptake. Patent extensions on dermatology formulations protect revenue streams that fund next-generation molecules. These incentives motivate large and mid-size firms to prioritize vitiligo pipelines despite modest total patient counts.

Breakthrough approvals of topical JAK-inhibitor creams

Ruxolitinib cream moved the treatment paradigm from broad immunosuppression to targeted JAK-STAT inhibition, with 30% of patients achieving at least 75% facial repigmentation after 24 weeks. Topical delivery curbs systemic exposure, easing safety concerns. Pipeline agents such as povorcitinib and ritlecitinib follow close behind, generating competitive tension and preparing multi-agent combination protocols that promise deeper, more durable repigmentation.

Technology advances in targeted & handheld phototherapy

FDA-cleared handheld narrowband UVB devices extend treatment outside clinics and improve adherence[2]Zerigo Health, “NB UVB Light Therapy for Vitiligo at Home,” zerigohealth.com. Excimer lasers at 308 nm deliver high-precision therapy for lesions covering less than 10% body surface. Device miniaturization and smartphone pairing enable dose tracking and clinician oversight, addressing past compliance obstacles. Adoption peaks first in wealthier economies, then diffuses through emerging markets as costs fall.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Lack of standardized long-term protocols

Lack of standardized long-term protocols

| -0.4% | Global, highest in developing areas | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:

-0.4%

| Geographic Relevance:

Global, highest in developing areas

| Impact Timeline:

Long term (≥ 4 years)

|

Limited reimbursement in developing regions

Limited reimbursement in developing regions

| -0.8% | Asia-Pacific, MEA, South America | Medium term (2-4 years) | |||

High cost of biologics and JAK inhibitors

High cost of biologics and JAK inhibitors

| -0.6% | Global, sharper in price-sensitive markets | Short term (≤ 2 years) | |||

Safety concerns around off-label immunosuppressants

Safety concerns around off-label immunosuppressants

| -0.3% | North America and Europe | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Lack of globally-standardized long-term treatment protocols

European surveys find many patients believe vitiligo is untreatable when exposure exceeds 200 sessions without clear targets. Pediatric guidelines vary widely, limiting phototherapy uptake despite strong safety signals. Inconsistent outcome metrics hamper cross-study comparisons and delay evidence-based refinements.

Limited reimbursement coverage in developing regions

Classifying vitiligo therapy as cosmetic leaves patients with high out-of-pocket costs. Medicaid covers tretinoin for acne in 45 states, yet only 10 states reimburse for pigment disorders[3]Priya Manjaly, “Disparities in State Medicaid Coverage,” pubmed.ncbi.nlm.nih.gov. Opzelura’s USD 2,094 wholesale cost per tube restricts uptake where insurance gaps persist. Prior authorization hurdles further curb timely access.

Segment Analysis

By Disease Type: Non-segmental dominance drives stability

Non-segmental vitiligo accounted for 65.02% of the vitiligo treatment market in 2025. Broad prevalence, bilateral presentation, and predictable response to systemic or topical therapy support consistent demand. Segmental vitiligo, while affecting fewer patients, advances fastest at an 7.98% CAGR through 2031, aided by graft-based procedures and localized phototherapy innovations. Combination regimens pairing cellular grafting with JAK inhibitors increase repigmentation rates and shorten treatment windows. Pharmaceutical pipelines now explore disease-type-specific formulations that match differing immunologic profiles, improving efficacy and limiting overtreatment.

These dynamics stabilize the vitiligo treatment market size because high-volume non-segmental cases sustain baseline sales, while high-growth segmental cases provide margin expansion opportunities. Device makers refine spot-targeted excimer lasers to meet segmental needs, whereas systemic developers concentrate on autoimmune modifiers more relevant to non-segmental disease heterogeneity.

Note: Segment shares of all individual segments available upon report purchase

By Therapy: Biologics spark next wave of precision care

Topical treatments retained 45.92% share in 2025, buoyed by ruxolitinib’s global rollout. Yet biologic therapies race ahead with a 15.56% CAGR through 2031 as monoclonal antibodies and BET inhibitors move through late-stage trials. Narrowband UVB and excimer laser light therapy hold steady, integrated increasingly as adjuncts to topical JAK inhibitors to maximize pigment return. Surgical procedures cater to stable, localized cases and benefit from incremental improvements in graft survival and donor-site healing. Emerging modalities, stem cells, gene editing, and antioxidant nanocarriers, fill the “others” bracket and foreshadow further diversification. These trends enlarge the vitiligo treatment market size for biologic pipelines and raise the bar for combination regimens that address both immune drivers and melanocyte regeneration.

By End User: Home-care shift reshapes delivery

Hospitals controlled 55.02% of revenues in 2025 due to complex cases requiring surgical or multi-modal phototherapy. Nonetheless, home-care settings grow 10.71% yearly as patients embrace discreet, convenient regimens. Dermatology clinics act as hubs for protocol design, then transition patients to handheld UVB devices and topical JAK inhibitors for maintenance. Research institutes drive validation of novel approaches, ensuring continuous flow of evidence-based updates. Teledermatology platforms support adherence, widen specialist reach, and underpin the home-care surge that lifts the vitiligo treatment market.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Digital access accelerates uptake

Hospital pharmacies supplied 38.11% of prescriptions in 2025, yet online pharmacies outpace others at a 12.58% CAGR. Digital channels meet privacy preferences and facilitate recurring orders for chronic therapy. Retail pharmacies maintain relevance through in-person guidance and simple refills. Specialty services handle high-cost biologics, offering personalized adherence coaching. Mail-order models gain share among stable, long-term users who value automated logistics. These shifts diversify revenue streams and lower overall distribution costs inside the vitiligo treatment market.

Geography Analysis

North America generated 41.88% of global revenue in 2025 due to rapid adoption of FDA-approved JAK inhibitors and strong reimbursement structures. Insurers in the United States reimburse phototherapy and topical ruxolitinib under clear clinical criteria, supporting high initiation rates. Academic medical centers run multi-arm trials testing next-generation antibodies and oral JAKs, keeping the region at the forefront of innovation.

Europe follows with established dermatology service lines and synchronized EMA approvals that reduce launch lags. Cross-border reference pricing and centralized health-technology assessments, however, can slow formulary inclusion of premium biologics. Still, EU centers lead graft technique refinement, making the bloc influential in surgical best practices.

Asia-Pacific represents the fastest-growing bloc at a 12.44% CAGR. China’s 14 million reported cases create a major addressable pool, and regulatory reforms speed up approvals of imported targeted therapies. Partnerships, such as Incyte with CMS Holdings, maximize distribution reach across mainland China and Southeast Asia. India adds volume through growing middle-class spending and expanding tele-dermatology networks, while Japan and South Korea push high-tech phototherapy adoption.

Middle East and Africa show rising diagnoses amid campaigns to destigmatize skin disorders. National health strategies integrate vitiligo into chronic disease management, encouraging procurement of handheld UVB devices. South American markets remain under-penetrated but achieve incremental gains as public insurers revise cosmetic classifications and foreign manufacturers set up local subsidiaries.

Collectively, these regional trends amplify the vitiligo treatment market size through 2030 while balancing volume and price considerations across income tiers.

Competitive Landscape

Market Concentration

The vitiligo treatment market is moderately fragmented. Incyte leads topical JAK inhibition, posting USD 508 million Opzelura sales in 2024, and extends its franchise by acquiring Villaris Therapeutics for USD 1.43 billion to add an IL-15Rβ monoclonal antibody. Pfizer develops oral ritlecitinib, now in Phase 3, targeting both hair loss and vitiligo indications, thereby leveraging economies of scale across autoimmune segments.

Device manufacturers such as STRATA Skin Sciences win regulatory clearances for excimer lasers in Japan and pursue smaller-footprint designs for home settings. Start-ups like Zerigo Health integrate cloud-based dose tracking to differentiate in an increasingly competitive handheld UVB niche. Venture capital supports new entrants: Alys Pharmaceuticals launched with USD 100 million funding to aggregate dermatology assets and accelerate clinical timelines.

Strategic partnerships bridge capability gaps. Incyte licenses povorcitinib to CMS Holdings for greater Asia-Pacific reach, while Organon acquires VTAMA topical rights to diversify its women’s health-centric portfolio. These moves signal a maturing field where targeted acquisitions and regional alliances answer distinct market needs.

Intellectual-property landscapes remain fluid. Orphan exclusivity grants incumbents a runway, yet biosimilar pathways loom as patents expire. Firms invest in combination protocols that pair in-house drugs with third-party devices, locking in ecosystem value and raising switching costs for prescribers. Overall, head-to-head competition hinges on efficacy, safety profile, and payer negotiations rather than on brand awareness alone.

Vitiligo Treatment Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Clinuvel Pharmaceuticals completed Phase III enrollment for afamelanotide (CUV105) systemic repigmentation therapy.

- January 2025: VYNE Therapeutics finalized Phase 2b enrollment for BET inhibitor VYN201 in non-segmental vitiligo.

Table of Contents for Vitiligo Treatment Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increasing Prevalence Of Vitiligo & Public-Health Awareness

- 4.2.2Regulatory Incentives For Orphan / Dermatology Drugs

- 4.2.3Breakthrough Approvals Of Topical Jak-Inhibitor Creams

- 4.2.4Technology Advances In Targeted & Handheld Phototherapy

- 4.2.5Rising Demand For Aesthetic Dermatology In Emerging Markets

- 4.2.6AI-Powered Dermatology Diagnostics Accelerating Early Treatment

- 4.3Market Restraints

- 4.3.1Lack Of Globally-Standardized Long-Term Treatment Protocols

- 4.3.2Limited Reimbursement Coverage In Developing Regions

- 4.3.3High Cost Of Biologics & JAK-Inhibitor Therapies

- 4.3.4Safety Concerns Around Off-Label Systemic Immunosuppressants

- 4.4Porter's Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitute Products

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Disease Type

- 5.1.1Non-segmental Vitiligo

- 5.1.2Segmental Vitiligo

- 5.2By Therapy

- 5.2.1Topical Treatment

- 5.2.1.1Corticosteroids

- 5.2.1.2Calcineurin Inhibitors

- 5.2.1.3JAK Inhibitors

- 5.2.1.4Depigmentation Agents

- 5.2.2Light Therapy

- 5.2.2.1Narrowband-UVB

- 5.2.2.2Excimer Laser

- 5.2.2.3PUVA

- 5.2.3Surgical Procedures

- 5.2.3.1Skin-Grafting

- 5.2.3.2Cellular-Grafting

- 5.2.3.3Micropigmentation

- 5.2.4Biologic Therapies

- 5.2.5Others

- 5.3By End User

- 5.3.1Hospitals

- 5.3.2Dermatology & Aesthetic Clinics

- 5.3.3Home-care Settings

- 5.3.4Research Institutes

- 5.4By Distribution Channel

- 5.4.1Hospital Pharmacies

- 5.4.2Retail Pharmacies

- 5.4.3Online Pharmacies

- 5.5Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2Europe

- 5.5.2.1Germany

- 5.5.2.2United Kingdom

- 5.5.2.3France

- 5.5.2.4Italy

- 5.5.2.5Spain

- 5.5.2.6Rest of Europe

- 5.5.3Asia-Pacific

- 5.5.3.1China

- 5.5.3.2Japan

- 5.5.3.3India

- 5.5.3.4South Korea

- 5.5.3.5Australia

- 5.5.3.6Rest of Asia-Pacific

- 5.5.4Middle East and Africa

- 5.5.4.1GCC

- 5.5.4.2South Africa

- 5.5.4.3Rest of Middle East and Africa

- 5.5.5South America

- 5.5.5.1Brazil

- 5.5.5.2Argentina

- 5.5.5.3Rest of South America

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1AbbVie Inc.

- 6.3.2Ahammune Biosciences Pvt. Ltd.

- 6.3.3Almirall S.A.

- 6.3.4Astellas Pharma Inc.

- 6.3.5Dr. Reddy's Laboratories Ltd.

- 6.3.6Edesa Biotech Inc.

- 6.3.7Incyte Corporation

- 6.3.8Merck & Co., Inc.

- 6.3.9Pfizer Inc.

- 6.3.10STRATA Skin Sciences Inc.

- 6.3.11Eli Lilly and Company

- 6.3.12Sun Pharmaceutical Industries Ltd.

- 6.3.13Dermavant Sciences

- 6.3.14Bristol-Myers Squibb Co.

- 6.3.15Clinuvel Pharmaceuticals Ltd.

- 6.3.16Lumenis Ltd.

- 6.3.17Cutera Inc.

- 6.3.18Alma Lasers (Sisram Medical)

- 6.3.19Fotona d.o.o.

- 6.3.20Glenmark Pharmaceuticals Ltd.

- 6.3.21MedUV Inc.

- 6.3.22Amgen Inc.

- 6.3.23Stiefel Dermatology (GSK)

- 6.3.24Regeneron Pharmaceuticals Inc.

- 6.3.25Johnson & Johnson (NeoStrata/Aveeno)

- 6.3.26La Roche-Posay Laboratoire Dermatologique

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Vitiligo Treatment Market Report Scope

Vitiligo is a chronic skin condition characterized by the loss of pigment-producing cells called melanocytes, leading to the development of white patches on the skin. These patches can appear anywhere on the body, including the face, hands, and other areas exposed to the sun, as well as in the mucous membranes and the retina of the eyes.

The vitiligo treatment market is segmented by disease type (non-segmental vitiligo and segmental vitiligo), therapy (topical treatment, light therapy, surgical procedures, and others), end user (hospital, aesthetic clinics, and others), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The report offers the value (USD) for all the above segments.