Catering Services Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

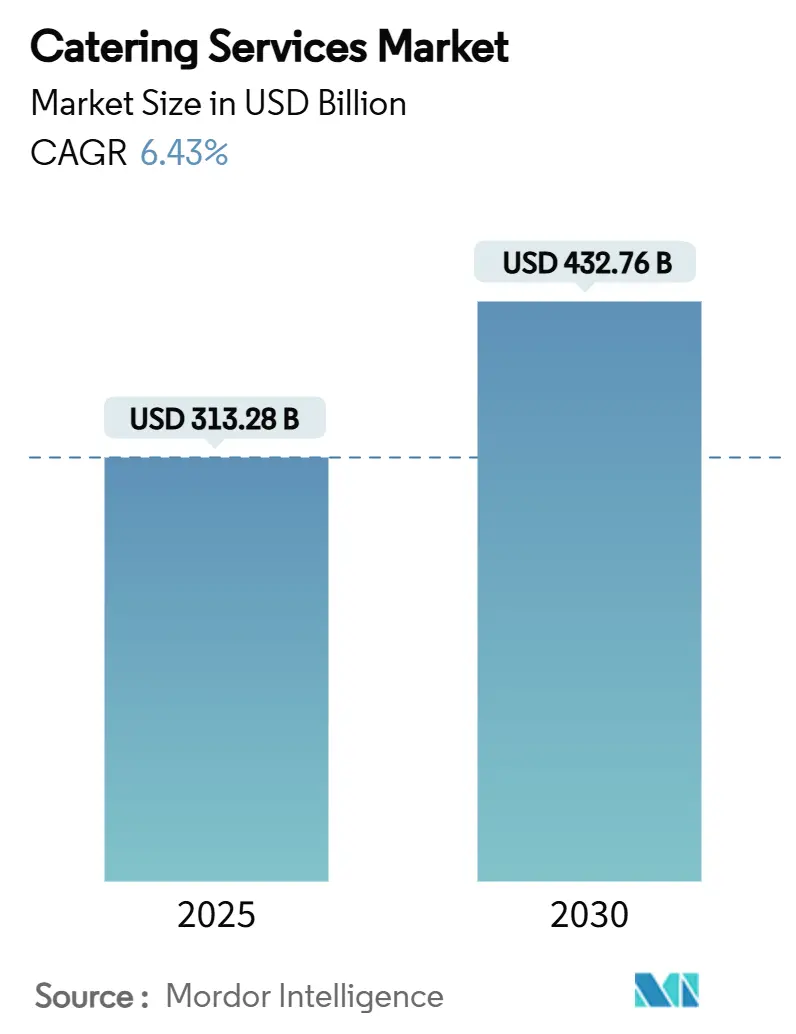

| Market Size (2025) | USD 313.28 Billion |

| Market Size (2030) | USD 432.76 Billion |

| Growth Rate (2025 - 2030) | 6.43% CAGR |

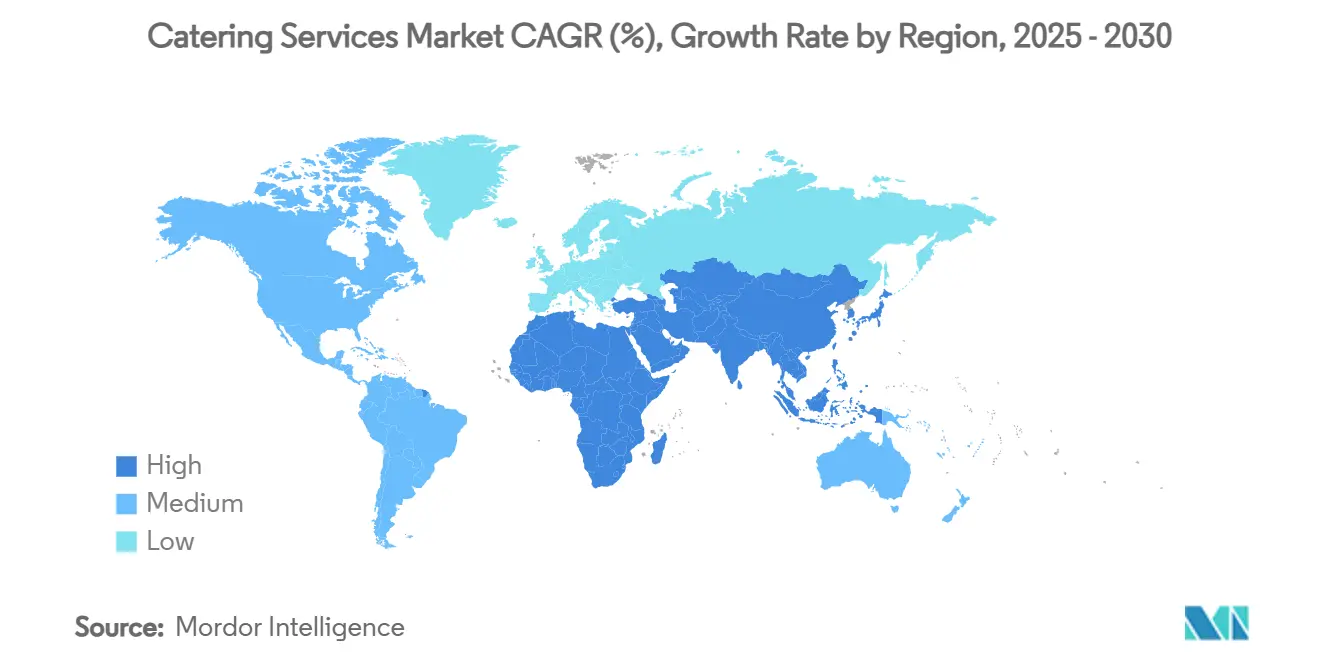

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Catering Services Market Analysis by Mordor Intelligence

The catering services market size reached USD 313.28 billion in 2025 and is forecast to touch USD 432.76 billion by 2030, delivering a 6.43% CAGR over the period; this line-up of figures positions the catering services market size for a solid multi-year expansion. Several forces sustain this upward curve. First, corporate clients have re-focused workplace dining on employee wellness, driving steady contract renewals even as hybrid work trims daily footfall. Second, cloud-kitchen infrastructure cuts fixed costs and unlocks new “drop-off” service lines that appeal to cost-sensitive accounts. Third, investments in predictive inventory software and temperature-tracking IoT devices curb waste and enhance food-safety compliance, lifting margins. Finally, steady outsourcing by hospitals and universities injects long-term revenue, giving operators confidence to scale into new geographies.

Key Report Takeaways

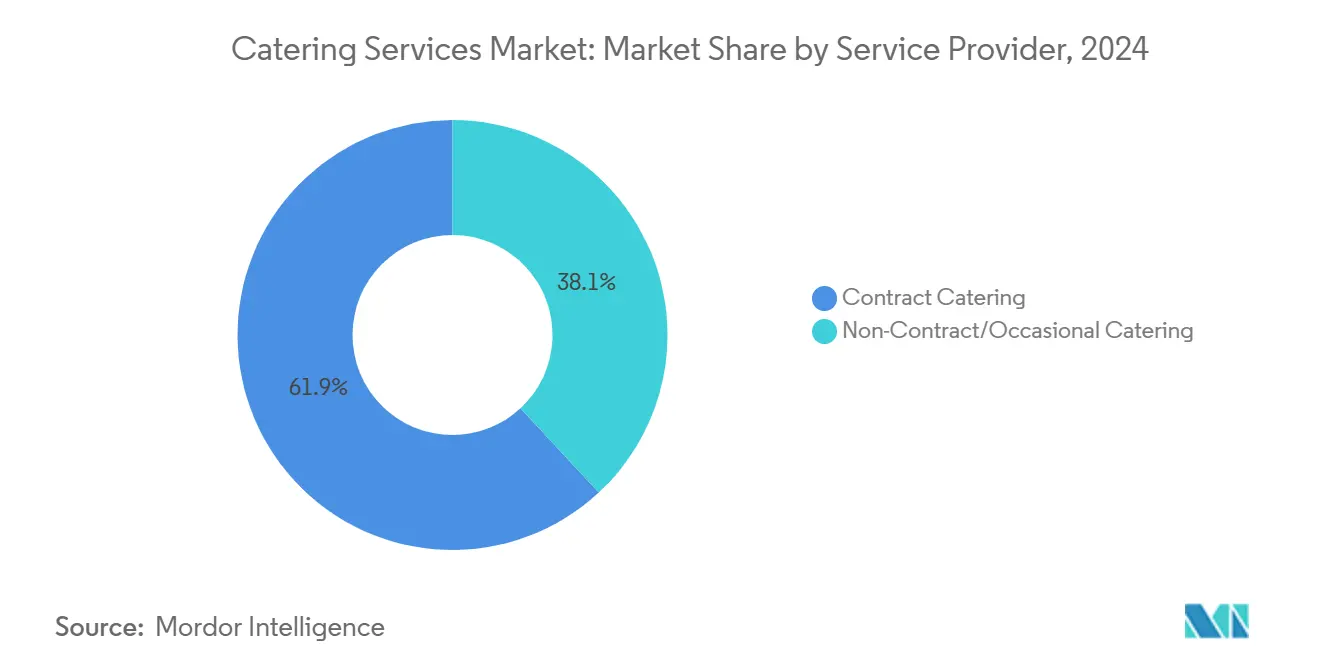

- By service provider type, contract catering led with 61.91% revenue share in 2024, while non-contract catering is projected to expand at a 7.01% CAGR through 2030.

- By catering type, corporate catering accounted for 34.08% of the catering services market share in 2024, and is advancing at a 6.72% CAGR to 2030.

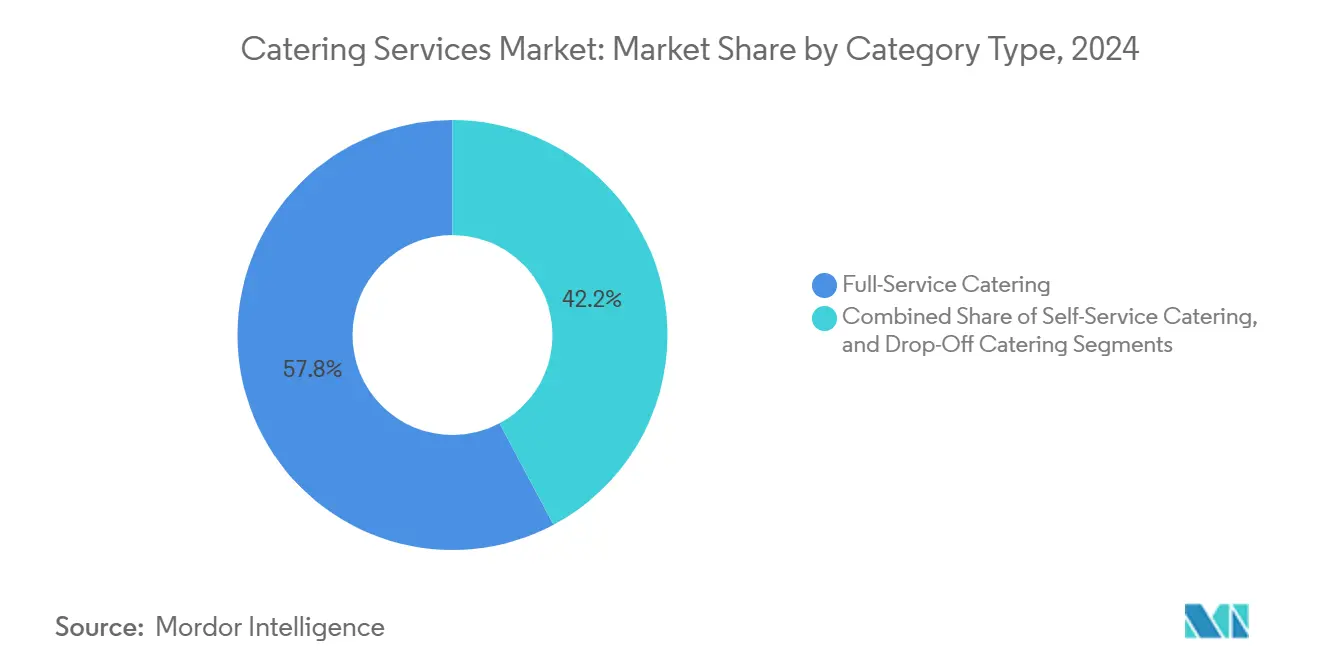

- By category, full-service formats captured 57.79% of the catering services market size in 2024, while drop-off options are recording faster growth with 7.34%.

- By geography, North America held 36.25% of global revenue in 2024; Asia-Pacific is set to post the highest regional CAGR of 7.79% through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Catering Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate Wellness and Workplace Dining Initiatives | +1.2% | North America & Europe core, expanding to APAC | Medium term (2-4 years) |

| Growth of Cloud Kitchens and Hybrid Catering Models | +0.8% | Global, with concentration in urban centers | Short term (≤ 2 years) |

| Technological Integration in Operations | +0.7% | North America & Europe lead, APAC following | Medium term (2-4 years) |

| Rise in Outsourcing by Healthcare and Institutional Sectors | +1.1% | Global, accelerated in developed markets | Long term (≥ 4 years) |

| Menu Innovation and Culinary Diversity | +0.5% | Global, with regional customization | Short term (≤ 2 years) |

| Shift to Healthier, Plant-Forward Menus | +0.9% | North America & Europe primary, global expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Corporate Wellness and Workplace Dining Initiatives

Corporate wellness programs now include comprehensive workplace dining strategies that influence employee retention and productivity. According to McKinsey's 2024 healthcare analysis, organizations with employee wellness infrastructure report 23% higher profit margins than those offering basic benefits. Companies now view on-site dining as a strategic tool for talent acquisition rather than a cost center. Corporate catering contracts increasingly include nutritional analytics and personalized meal planning, moving away from traditional volume-based models. Modern workplace dining programs use biometric screening data to tailor menu offerings, establishing a connection between food service and measurable health outcomes to support higher pricing.

Growth of Cloud Kitchens and Hybrid Catering Models

The integration of cloud kitchens into traditional catering operations has transformed service delivery economics. This model enables providers to serve multiple client locations from centralized production facilities without full-service infrastructure costs. Cloud kitchens are particularly effective for drop-off catering, where food quality and delivery efficiency take precedence over on-site presentation, contributing to the segment's 7.34% CAGR. Companies implementing hybrid models that combine cloud kitchen production with strategic full-service locations can optimize costs while maintaining service flexibility. The technology supports real-time demand forecasting and inventory optimization, reducing food waste by up to 30% compared to traditional on-site preparation. These operational efficiencies create pricing advantages, especially for corporate clients aiming to reduce facilities management costs while maintaining food service quality.

Technological Integration in Operations

AI-powered demand forecasting systems align production quantities with real-time order patterns, reducing food waste by 30% and decreasing capital tied to perishable inventory. IoT temperature monitoring systems throughout the distribution chain create digital records that comply with the FDA's 2024 traceability requirements and reduce audit time by 40%. Catering companies that implement predictive analytics, automated inventory systems, and customer behavior analysis gain competitive advantages in service delivery. Digital ordering systems and mobile apps have become crucial customer interaction points, with effective implementations increasing order frequency and average transaction values by 15-20%. IoT sensors for food safety and temperature monitoring generate compliance records that meet regulatory standards while lowering compliance expenses. Process control systems and sensor networks help catering operations maintain food quality standards across multiple locations, solving a key operational challenge in the industry.

Rise in Outsourcing by Healthcare and Institutional Sectors

Healthcare institutions are increasingly outsourcing their food services to focus on core medical operations. The sector's growing profit margins enable investment in premium catering services. This outsourcing addresses specialized dietary needs, therapeutic nutrition programs, and infection control protocols that require expert management. Educational institutions also benefit from professional food service management, which improves student satisfaction while reducing administrative workload. Strict regulatory requirements in healthcare create entry barriers that favor established catering companies with proven institutional service experience. The long-term contracts in these sectors provide stable revenue streams, allowing catering companies to invest in specialized equipment and staff development, which strengthens their market position.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour Shortages and Rising Wage Floors | -1.8% | Global, acute in developed markets | Short term (≤ 2 years) |

| Fluctuating Food Prices & Supply Chain Disruptions | -1.3% | Global, with regional variations | Medium term (2-4 years) |

| Seasonal Demand Fluctuations | -0.6% | Global, weather-dependent regions more affected | Short term (≤ 2 years) |

| Stricter Food-Safety Traceability Mandates | -0.9% | North America & Europe lead, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Labour Shortages and Rising Wage Floors

The catering industry faces significant staffing challenges, with more than 50% of hospitality workers hesitant to return to service roles, according to Bloomberg's workforce surveys[1]International Caterers Association, “Global Catering Workforce Survey 2024,” internationalcaterers.org. Labor shortages have compelled catering companies to offer enhanced compensation packages, including paid time off, benefits, and team-building programs, increasing operational costs by 15-25% compared to pre-pandemic levels. The shortage affects skilled positions, particularly chefs and food safety specialists, where training requirements constrain the available talent pool. Companies are adopting automation and technology to maintain service levels with fewer staff, though initial investments strain smaller operators' cash flow. While the industry has established partnerships with culinary schools and apprenticeship programs, these initiatives require 2-3 years to substantially increase the workforce.

Stricter Food-Safety Traceability Mandates

In 2024, the FDA rolled out a supplement to its 2022 Food Code, introducing stricter traceability and food defense measures[2]U.S. Food and Drug Administration, “2024 Food Code Supplement,” fda.gov. These changes are driving up compliance costs for catering operations. Meanwhile, the USDA has bolstered its Listeria monitoring protocols and broadened testing requirements. This adds layers of operational complexity, especially for facilities catering to vulnerable groups like healthcare patients and school children. As a result of these regulatory shifts, mid-sized catering firms now face annual costs ranging from USD 50,000 to 200,000. These costs stem from the need for detailed record-keeping, staff training, and facility upgrades. Navigating compliance across various jurisdictions gives larger operators, with their dedicated compliance teams, a competitive edge. In contrast, smaller firms find themselves under pressure, facing the tough choices of consolidation or market exit. While advanced food safety management systems are becoming crucial investments, they also offer a silver lining: the ability to command premium prices from clients seeking certified compliance documentation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Provider Type: Contract Dominance Meets Flexible Growth

Despite contract catering holding a dominant 61.91% market share in 2024, the non-contract catering sector is projected to grow at a 7.01% CAGR through 2030. This growth signals a shift towards more flexible service models, catering to the demands of hybrid work patterns and event-driven needs. The rise in occasional catering services is largely driven by corporate clients seeking scalable solutions, aligning costs with actual usage rather than being tied to fixed capacities. In response, contract catering providers are adopting flexible pricing tiers and hybrid service models, blending guaranteed base services with variable capacity options. This shift in segmentation highlights a move away from traditional long-term contracts towards performance-based agreements, prioritizing service quality and adaptability over mere volume commitments.

Within the realm of contract catering, providers boasting technology-driven service delivery and expertise across multiple locations are gaining a competitive edge. A testament to this trend is Compass Group's USD 600 million acquisition of CH&CO, underscoring how industry leaders are consolidating specialized capabilities to cater to a diverse array of client needs across various business sectors[3]Compass Group PLC, “Acquisition of CH&CO,” compass-group.com. While non-contract providers enjoy the advantages of lower capital demands and enhanced pricing flexibility, they grapple with the challenge of scaling operations to compete effectively in food procurement and deliver standardized services. Given the segment's growth trajectory, it's evident that successful catering companies will need to forge hybrid business models, marrying the reliability of contract services with the nimbleness of occasional catering.

By Catering Type: Corporate Leadership Drives Innovation

Corporate catering, commanding a 34.08% market share and boasting a 6.72% CAGR, stands out as the industry's chief innovator. This is underscored by corporate investments in premium services, driven by workplace wellness and enhanced employee experience initiatives. While industrial catering enjoys consistent demand from the manufacturing and energy sectors, its growth lags behind the corporate segment. This is attributed to the former's conservative spending habits and a preference for standardized services. Demand for event catering remains erratic, swayed by economic fluctuations and seasonal trends. Notably, corporate events have rebounded more robustly than social ones in the wake of the pandemic.

Segmentation highlights the unique demands of various client types, shaping service innovations and pricing strategies. Corporate clients are leaning towards tailored nutrition programs, insist on documentation for sustainable sourcing, and favor tech-driven ordering systems that sync with employee wellness platforms. Meanwhile, sports and entertainment venues are on the lookout for adept logistics and the ability to handle high-volume services, presenting a niche for catering firms with event management prowess. On the other hand, the education and government sectors emphasize cost-effectiveness and adherence to regulations, gravitating towards providers with a track record in institutional services and standardized protocols. This broad spectrum of client needs allows catering firms to pursue growth while adeptly managing associated risks.

By Category Type: Service Models Reshape Market Dynamics

Cost-conscious clients are increasingly opting for premium food experiences through drop-off catering, which has seen a 7.34% CAGR acceleration. This trend challenges the traditional belief that higher service levels are a necessity. Meanwhile, full-service catering commands a significant 57.79% market share, underscoring a sustained demand for comprehensive event management. However, the growth rates hint at a maturation phase for these conventional service formats. Straddling the line, self-service catering offers a balance: it provides cost savings over full-service options while ensuring greater engagement than drop-off services.

These shifts in catering categories mirror evolving client expectations and the changing economics of operations. Drop-off catering is reaping the benefits of cloud kitchen integrations and streamlined delivery logistics. This allows providers to efficiently serve multiple locations without compromising food quality. Moreover, technology plays a pivotal role in the success of drop-off catering. Features like mobile ordering and real-time tracking not only enhance service but also set providers apart in a competitive landscape. In response, full-service catering is upping its game, spotlighting experiential elements like live cooking demos and bespoke menu development. Such specialized offerings help justify their premium pricing. As the landscape evolves, it's clear that thriving catering companies will need to cultivate versatile capabilities, tailoring their services to meet diverse client needs and budgetary constraints.

Geography Analysis

In 2024, North America commands a 36.25% share of the market, underscoring its entrenched outsourcing culture and significant corporate investments in employee wellness. However, this dominance also signals a saturation point in traditional service categories. Growth in the region is pivoting from mere market expansion to a focus on service innovation and tech adoption. Notably, companies like Compass Group have harnessed strategic acquisitions and operational efficiencies to post a commendable 10.6% organic revenue growth. While outsourcing in healthcare and education ensures a steady demand, corporate wellness initiatives pave the way for premium service offerings. Furthermore, the regulatory landscape, shaped by FDA food safety updates and USDA compliance mandates, tends to favor established players adept at navigating these complexities.

Asia-Pacific stands out as the region with the most rapid growth, boasting a 7.79% CAGR, largely fueled by the expansion of China's catering industry. This growth trajectory is bolstered by urbanization, rising disposable incomes, and a growing embrace of Western-style corporate dining. Companies are heavily investing in technology infrastructure, recognizing the importance of digital transformation and supply chain optimization for their multi-location operations. Notably, markets in India, Japan, and Southeast Asia are poised for a surge in first-time outsourcing, especially in healthcare and education.

Europe experiences consistent growth, with a pronounced focus on sustainability and regulatory compliance shaping service differentiation. This emphasis on environmental stewardship offers a competitive edge to catering firms that prioritize sustainable sourcing and waste reduction. For instance, Aramark's ambitious goals of halving food waste by 2030 and achieving net-zero greenhouse gas emissions by 2050 highlight the strategic advantage of sustainability in Europe[4]Aramark, “ESG Progress Report 2025,” aramark.com. Meanwhile, South America and the Middle East/Africa regions, though exhibiting moderate growth, are witnessing new opportunities in institutional catering, spurred by infrastructure development and economic diversification.

Competitive Landscape

The catering services market is highly fragmented, presenting significant opportunities for consolidation among companies adept at acquisitions and those with operational scale advantages. Some of the key players in the catering services market include Compass Group PLC, Sodexo SA, Aramark Corporation, Elior Group, and Delaware North. Market leaders leverage their geographic reach, specialized expertise, and tech-driven service models, setting them apart from smaller competitors who struggle to replicate these advantages cost-effectively. A case in point is Compass Group's strategic USD 600 million acquisition of CH&CO, underscoring how industry giants are consolidating specialized capabilities to cater to diverse client needs across various sectors.

Technology adoption stands out as a pivotal competitive edge. AI-driven automation and digital ordering platforms not only enhance operational efficiency but also offer advantages in pricing and service quality. Here, stringent regulatory compliance and specialized knowledge act as formidable entry barriers. While emerging disruptors champion tech-driven service models and sustainable sourcing to attract eco-conscious clients, their limited scale hampers their bid for major institutional contracts.

As the catering services market continues to evolve, the emphasis on sustainability and health-conscious offerings is becoming paramount. Catering firms are increasingly curating menus that prioritize organic ingredients, locally sourced produce, and environmentally friendly packaging. This shift not only caters to the growing demand for healthier dining options but also aligns with global sustainability goals. Furthermore, partnerships with nutritionists and wellness experts are becoming commonplace, ensuring that offerings are not just delicious but also nutritionally balanced. Such initiatives not only enhance brand reputation but also foster deeper client relationships, especially in sectors like corporate events and healthcare, where wellness is a top priority.

Catering Services Industry Leaders

Compass Group PLC

Sodexo SA

Aramark Corporation

Elior Group

Delaware North Companies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: In a bid to bolster public safety, the USDA's Food Safety and Inspection Service rolled out enhanced measures against Listeria monocytogenes. These include expanded testing protocols, upgraded inspector training, and tighter oversight of regulated entities. Such measures have direct implications for catering operations catering to vulnerable groups, necessitating substantial compliance investments.

- October 2024: Sodexo celebrated a robust Q1 Fiscal 2024, marking an 8.2% organic revenue surge, culminating in consolidated revenues of 6.3 billion euros. The food services segment led the charge with a 10.0% organic growth, fueled by pricing strategies, new contract activations, and a rebound in volumes across corporate and educational sectors.

- January 2024: Compass Group PLC has set its sights on acquiring CH and CO, a premium contract and hospitality service provider based in the UK and Ireland, with an initial enterprise value pegged at USD 600 million. This strategic move bolsters Compass Group's offerings across various sectors, including Business and Industry, Sports and Leisure, Education, and Healthcare. Notably, CH and CO boast annual revenues nearing USD 570 million.

Global Catering Services Market Report Scope

| Contract Catering |

| Non-Contract/Occasional Catering |

| Corporate Catering | |

| Industrial Catering | |

| Event Catering | Corporate Events |

| Sports Events | |

| Government Events | |

| Education Events | |

| Social Events | |

| Entertainment Events |

| Full-Service Catering |

| Self-Service Catering |

| Drop-Off Catering |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Service Provider Type | Contract Catering | |

| Non-Contract/Occasional Catering | ||

| By Catering Type | Corporate Catering | |

| Industrial Catering | ||

| Event Catering | Corporate Events | |

| Sports Events | ||

| Government Events | ||

| Education Events | ||

| Social Events | ||

| Entertainment Events | ||

| By Category Type | Full-Service Catering | |

| Self-Service Catering | ||

| Drop-Off Catering | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the catering services market?

The catering services market size stood at USD 313.28 billion in 2025 and is projected to reach USD 432.76 billion by 2030.

Which region grows fastest in catering services?

Asia-Pacific leads with a forecast 7.79% CAGR to 2030, supported by strong expansion in China’s commercial food-service sector.

How are cloud kitchens influencing catering economics?

Cloud-kitchen hubs cut front-of-house costs and enable drop-off services, helping operators lower delivered-meal prices and expand margins.

What major regulatory trends will shape the market?

The FDA’s 2024 traceability supplement and USDA’s tighter Listeria protocols require digital record-keeping and enhanced hazard monitoring, raising compliance stakes for all operators.

Page last updated on: