Cloud Kitchen Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

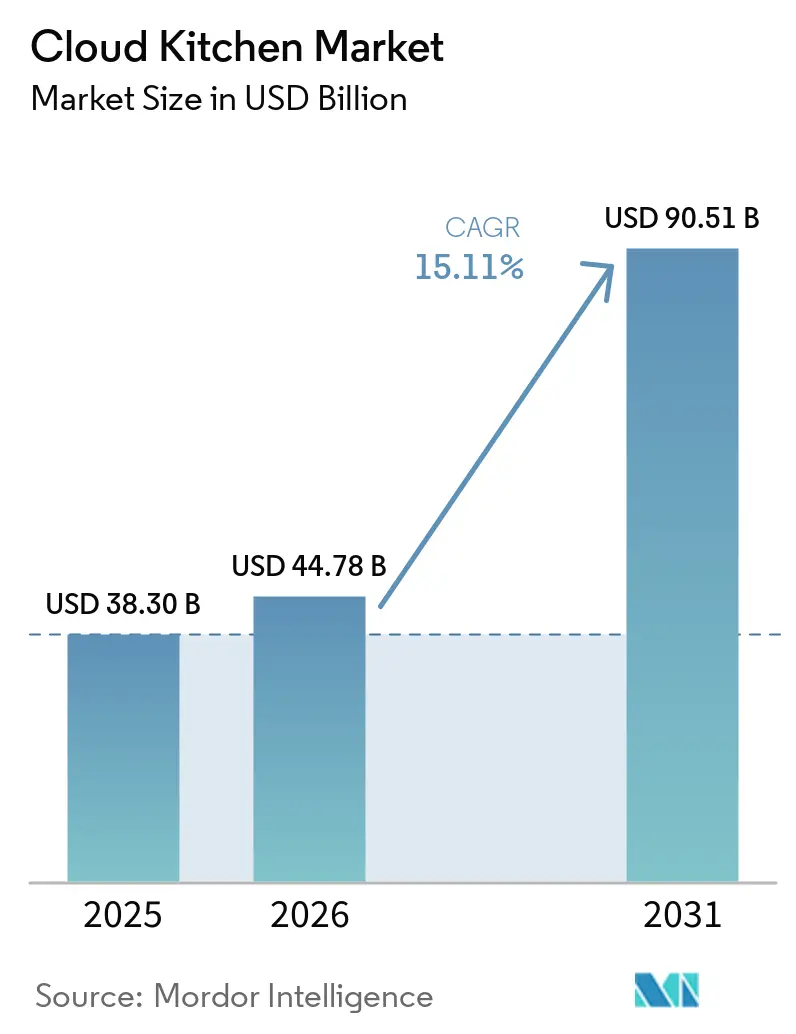

| Market Size (2026) | USD 44.78 Billion |

| Market Size (2031) | USD 90.51 Billion |

| Growth Rate (2026 - 2031) | 15.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cloud Kitchen Market Analysis by Mordor Intelligence

The Cloud Kitchen Market size is expected to grow from USD 38.30 billion in 2025 to USD 44.78 billion in 2026 and is forecast to reach USD 90.51 billion by 2031 at 15.11% CAGR over 2026-2031. The increasing preference for app-based ordering, rapid urbanization, and sustained venture funding are driving this growth. Mature regions are transitioning from network expansion to focusing on unit-level profitability, maintaining growth momentum. The competitive landscape in the cloud kitchen market is shifting as vertically integrated operators consolidate, emphasizing the importance of owning the ordering interface rather than relying on third-party aggregators.

Automation across the cloud kitchen market, previously in the pilot phase, is now being implemented on a larger scale. High-throughput assembly robots and AI-powered demand forecasting are reducing labor costs and minimizing inventory waste. Additionally, Tier-2 cities in the Asia-Pacific and Latin America regions offer significant growth opportunities for the cloud kitchen market. Rising smartphone penetration in these areas enables direct-to-consumer ordering, bypassing the fixed costs associated with dine-in formats and expanding the total addressable market for cloud kitchens. In Europe and certain U.S. regions, sustainability regulations are driving the adoption of recyclable or compostable packaging. While this adds cost pressures, it also creates opportunities for operators to position themselves as premium brands by meeting strict environmental standards.

Key Report Takeaways

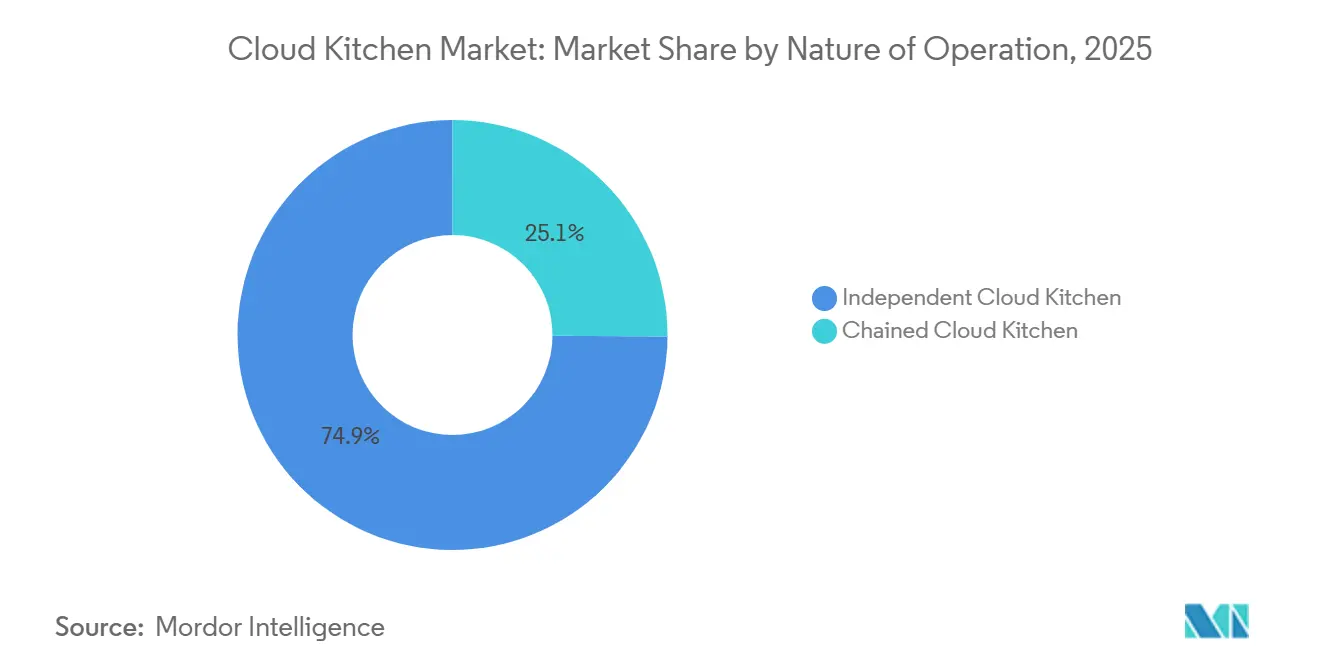

- By nature of operation, independents led with 74.88% of cloud kitchen market share in 2025, while chained operators are forecast to advance at a 17.58% CAGR through 2031.

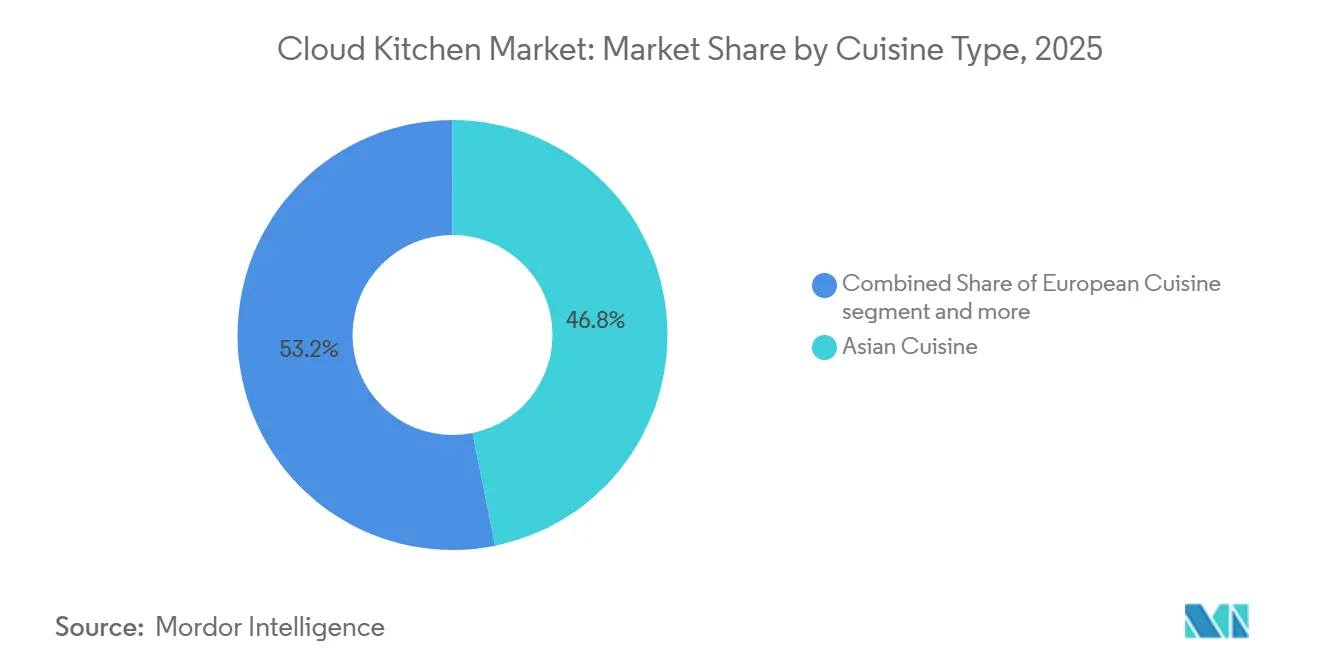

- By cuisine type, Asian cuisine accounted for 48.41% share of the cloud kitchen market size in 2025 and European cuisine is projected to expand at a 17.69% CAGR between 2026-2031.

- By ordering model, third-party aggregators held 62.24% share of the cloud kitchen market in 2025, whereas subscription meal plans are pacing the field with a 17.09% CAGR through 2031.

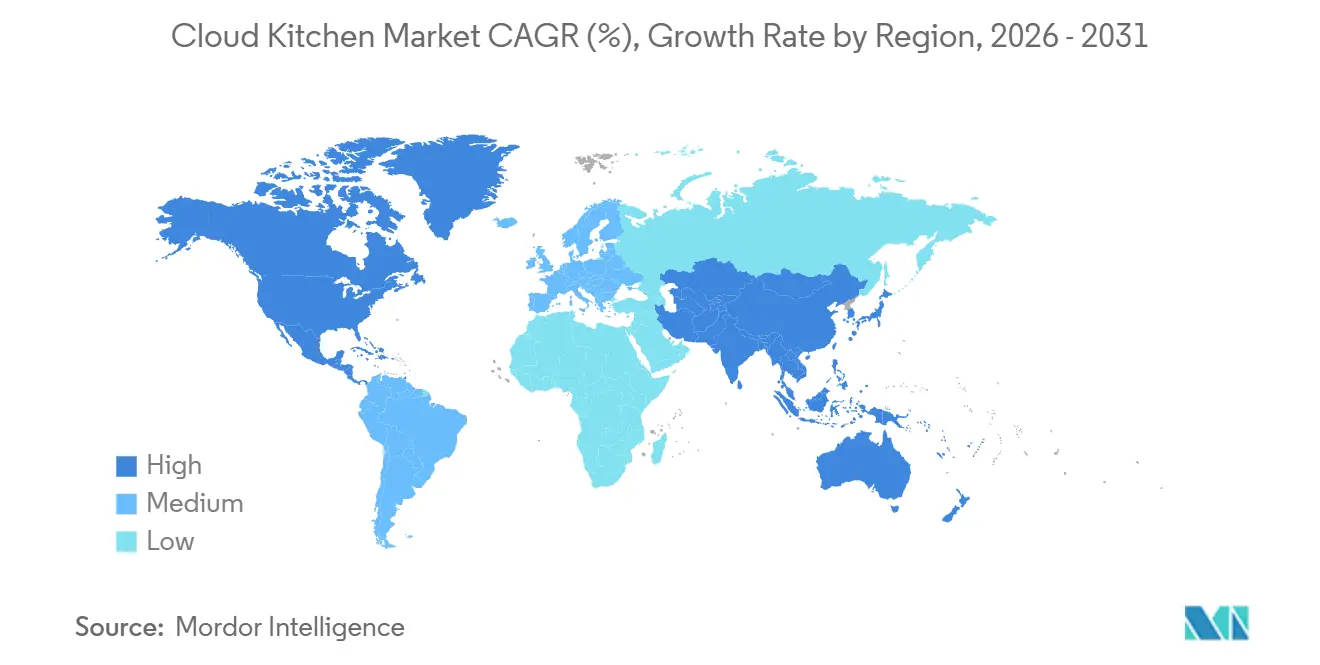

- By geography, Asia-Pacific commanded 41.22% of 2025 global revenue and is expected to grow at an 18.24% CAGR to 2031, outstripping every other region in the cloud kitchen market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cloud Kitchen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Widespread adoption of food delivery apps and online platforms | +3.2% | Global, with peak penetration in Asia-Pacific (India, China, Southeast Asia) and mature North American markets | Medium term (2-4 years) |

| Lower operational costs compared to traditional restaurants | +4.1% | Global, strongest in high-rent urban cores (New York, London, Mumbai, São Paulo) | Short term (≤ 2 years) |

| Technology-enabled ordering and mobile penetration | +2.8% | Asia-Pacific and Middle East lead; Africa emerging | Medium term (2-4 years) |

| Urbanization and changing lifestyles | +2.5% | Asia-Pacific (India, Indonesia, Vietnam), Middle East (Saudi Arabia, UAE), Latin America (Brazil, Mexico) | Long term (≥ 4 years) |

| Emergence of virtual brands and multi-concept kitchens | +2.0% | North America and Europe early adopters; Asia-Pacific scaling rapidly | Medium term (2-4 years) |

| Dark-kitchen co-location within retail fulfillment centers | +1.6% | North America (Kroger, Walmart partnerships), Europe (Tesco, Carrefour pilots) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Widespread adoption of food delivery apps and online platforms

In 2025, 74% of the global population was using the internet, an increase from 71% in 2024. This equates to 6 billion users, up from 5.8 billion the previous year, according to the International Telecommunication Union[1]Source: International Telecommunication Union, "Internet Use", itu.int. Platform networks within the cloud kitchen market create a competitive advantage for dominant players: those with high order density on a single platform gain favorable algorithm placements. This reduces customer acquisition costs per order and enhances price competitiveness, which smaller kitchens find difficult to match. In 2024, Deliveroo expanded its operations by adding approximately 3,000 merchant sites and reducing sales-weighted markups by 20% in the UK and Ireland through its Value Programme.

This initiative compressed margins for independent operators who lack the scale to negotiate similar commission reductions. The practice of stacked orders, where a single driver picks up multiple orders from nearby kitchens, improves delivery efficiency but concentrates volume in high-density kitchen clusters, disadvantaging isolated operators. The trend toward hyperlocal optimization has made platform success in the cloud kitchen market dependent on neighborhood-level kitchen density rather than citywide coverage, benefiting operators located in aggregator-preferred zones. Additionally, the growing use of mobile phones supports the food delivery market. Mobile devices provide significant convenience for food ordering. For example, in 2025, 82% of individuals aged 10 and older globally own a mobile phone, as reported by the International Telecommunication Union[2]Source: International Telecommunication Union, " Mobile Phone Ownership", itu.int.

Lower operational costs compared to traditional restaurants

Businesses operating in the cloud kitchen market reduce real estate costs by 40% to 60% by operating in industrial or secondary locations. Labor costs, which account for 25% to 35% of revenue in traditional restaurants, drop to 20% to 25% in delivery-only models. Profit margins for ghost kitchens range from 8% to 15%, significantly higher than the 3% to 9% margins of conventional restaurants, even after including platform commissions. European operators report cutting overhead costs by 30% to 50% by eliminating front-of-house staff, décor, and customer-facing real estate expenses. Kitopi, with over 200 locations in five GCC markets, achieved profitability by centralizing procurement and standardizing kitchen layouts, highlighting how scale delivers cost efficiencies unavailable to single-unit operators. This cost advantage strengthens the cloud kitchen market, particularly in high-rent urban areas such as New York, London, and Mumbai, where prime retail spaces are significantly more expensive than industrial warehouse rents. This creates a structural benefit for cloud kitchens that traditional restaurants cannot achieve without sacrificing foot traffic.

Technology-enabled ordering and mobile penetration

By 2025, nearly 45% of professional kitchens are expected to adopt artificial intelligence tools. These tools will support inventory forecasting and demand planning, effectively reducing food waste. Predictive restocking not only minimizes waste but also enhances gross margins. Unified point-of-sale and kitchen display systems are optimizing operations across the cloud kitchen market by consolidating orders from multiple delivery platforms into a single dashboard. This integration resolves the issue of "tablet hell" and reduces order errors, which often result in refunds and re-fires. In February 2025, Rebel Foods introduced QuickiES, an innovative 15-minute delivery service. By utilizing AI-driven demand forecasting, QuickiES strategically positions inventory in micro-fulfillment centers, cutting delivery times to below the industry standard of 30 to 45 minutes. Kitopi's SKOS platform is transforming order management by integrating menu management, order routing, and business analytics. This enables operators to update menus across all delivery platforms from a single interface and instantly pause sold-out items. The shift from reactive to predictive operations signifies a major change in the cloud kitchen market. Kitchens now prepare high-probability orders before customers place them. This change not only converts fixed labor costs into variable ones but also increases throughput per square foot.

Urbanization and changing lifestyles

Urban areas, bustling with activity, are propelling market growth in the cloud kitchen market. In 2024, the World Bank reported that 58% of the global population lived in urban regions[3]Source: World Bank, "Urban Population", worldbank.org. Saudi Arabia's cloud kitchen market is expected to grow, driven by the Vision 2030 urbanization strategy, which aims to concentrate populations in Riyadh, Jeddah, and NEOM. In Q2 2024, Brazil recorded BRL 61.4 billion in spending on out-of-home and delivery meals, reflecting a shift toward convenience dining as dual-income households increasingly reduce home cooking. Swiggy operates 1,102 dark stores across 128 cities in India, combining cloud kitchens with grocery micro-fulfillment. This integration of food delivery and quick commerce infrastructure generates economies of scope: a single dark store can handle restaurant orders, grocery deliveries, and subscription meal kits, spreading fixed costs across multiple revenue streams and improving returns on invested capital.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food quality and consistency challenges | -2.3% | Global, acute in markets with weak food safety enforcement (India, Southeast Asia, parts of Latin America) | Short term (≤ 2 years) |

| Aggregator commission squeeze on operator margins | -3.5% | Global, most severe in North America and Europe where DoorDash, Uber Eats, Deliveroo dominate | Short term (≤ 2 years) |

| Complex logistics and last-mile delivery issues | -1.8% | Emerging markets with fragmented delivery infrastructure (Africa, parts of Latin America, Southeast Asia) | Medium term (2-4 years) |

| Packaging and sustainability concerns | -1.2% | Europe (GDPR, Extended Producer Responsibility mandates), California, select Asian cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Food quality and consistency challenges

Environmental health officers in the UK, supported by a study from the National Institute for Health Research, identified the "invisibility" of dark kitchens, frequently operating under multiple trading names, from unregistered premises, and with irregular hours, as the primary obstacle to effective inspections. Operators in the cloud kitchen market noted a significant issue: delivery platforms may take up to two days to update allergen or ingredient information. This delay creates a risk, enabling customers with allergies to unknowingly order unsafe items. High staff turnover and understaffing further intensify these risks. Temporary workers, often lacking adequate food safety training, may fail to adhere to essential HACCP protocols, compromising temperature control, cross-contamination prevention, and allergen segregation. Research from CloudKitchens indicates that nearly 70% of diners prefer ordering from restaurants with physical locations. This finding highlights a trust gap that ghost kitchens must address by focusing on professional branding, transparent sourcing, and proactive review management.

Aggregator commission squeeze on operator margins

DoorDash and Uber Eats typically charge commissions ranging from 15% to 30%. However, when factoring in marketing fees, chargebacks, and payment processing, the effective take rates soar to between 40% and 50%. This adjustment means operators ultimately retain 60% to 70% of the gross order value. Consider a financial model for a single-brand ghost kitchen: with an average order value of USD 22 and handling 80 orders daily, it rakes in a monthly gross revenue of USD 52,800. Yet, after accounting for a 25% platform commission (USD 13,200), 30% food costs (USD 15,840), packaging (USD 2,640), labor (USD 10,560), rent (USD 3,000), and utilities (USD 2,500), the net profit stands at USD 3,560, translating to a 6.7% margin.

However, a mere three-dollar dip in average order value, a 15% decrease in order volume, or a five-percentage-point hike in commission can push the business into the red. To counteract commission pressures, operators in the cloud kitchen market are increasingly establishing direct-order channels via proprietary websites and apps, negotiating reduced rates based on volume, and tactically pricing higher on aggregator platforms while providing discounts for direct orders. In a move underscoring the trend, Wonder Group acquired Grubhub for a whopping USD 650 million in 2025, highlighting vertical integration as a means to sidestep platform fees and harness the full customer lifetime value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nature of Operation: Independents Hold Sway While Chains Accelerate

In 2025, independent operators commanded a significant 74.88% share of the cloud kitchen market revenue, underscoring the allure of the cloud kitchen market for entrepreneurs, thanks to its low capital entry barriers and flexible menu options. This trend persists in suburbs and Tier-2 cities, where the ability to swiftly adapt to local tastes offers independents an edge over larger players. Yet, as food safety audits tighten and packaging compliance costs rise, these independents face squeezed margins, resulting in higher closure rates compared to their chained counterparts. Moreover, with digital branding being paramount, independents find themselves pouring more into paid search efforts just to maintain visibility against chains favored by algorithms, subsequently inflating their customer acquisition costs relative to sales.

Chained cloud kitchens are set to outpace the market, expanding at a robust 17.58% CAGR from 2026 to 2031, thanks to their corporate purchasing power and ability to maintain standardized processes. For instance, Rebel Foods, with its expansive network of 450 kitchens, utilizes centralized prep hubs to batch-produce sauces and gravies. This strategy not only minimizes ingredient variance but also enhances consistency across its offerings. Furthermore, the brand's recognition eases the journey for first-time users, boosting both conversion rates and customer lifetime value. In a strategic move, chains have begun negotiating flat-rate contracts with aggregators, securing deals below the 20% mark. This shift narrows the cost disparity between aggregator and direct channels. As a result, with the compounding effect of operating leverage, the market share of cloud kitchens attributed to these chains is on track to more than double by 2031.

By Cuisine Type: Asian Staples Dominate, European Concepts Premiumize

In 2025, Asian cuisine captured a 48.41% share of the cloud kitchen market, driven by high-turnover items like fried rice and ramen, which maintain quality during delivery. Ingredient synergies streamlined inventory and reduced spoilage, while bold flavor profiles effectively masked minor temperature changes. In the GCC countries, where expatriates account for over a third of the population, rising demand increased average daily order counts and strengthened forward volume pipelines.

Between 2026 and 2031, European cuisine is anticipated to grow at a strong 17.69% CAGR, primarily due to its premium focus on artisanal pasta and bistro dishes. With average order values around EUR 30, operators can incorporate sustainable packaging surcharges without significantly affecting demand. Chef-led branding and customized wine pairings help operators capture discretionary spending in mature Western markets. However, the need for advanced compartmentalized containers to preserve delicate plating raises packaging costs per order, potentially impacting net margins unless offset by strategic pricing. These factors are critical in shaping competitive strategies within the cloud kitchen market.

By Ordering Model: Aggregators Reign but Subscriptions Build Stickiness

In 2025, third-party aggregators processed 62.24% of the global order volume, utilizing their extensive user bases and advanced recommendation systems. Kitchens that achieve top-tier prep times can increase their basket size by 12% compared to median performers, benefiting from algorithmic prioritization. However, fee structures reduce profitability and amplify dependency risks, prompting larger chains to integrate or acquire delivery capabilities, thereby transforming the cloud kitchen market.

While subscription meal plans remain a smaller channel, they are expanding at a strong 17.09% CAGR and exhibit high retention rates. In 2025, HelloFresh Factor launched in Germany, combining heat-and-eat entrées with meal kits and achieving a quarterly churn rate of less than 5%. Predictable demand enables operators to optimize labor scheduling, minimize forecasting errors, and batch-produce core menu items, reducing unit costs. This model also avoids reliance on discretionary algorithm changes by aggregator platforms, presenting a strategic advantage for growth-stage players.

Geography Analysis

In 2025, the Asia-Pacific region led the cloud kitchen market, accounting for a 41.22% revenue share. The region is expected to grow at a robust 18.24% CAGR through 2031. India, Indonesia, and China are at the forefront, with smartphone adoption exceeding 80% among urban adults and digital wallets enabling seamless payments. Companies such as Rebel Foods and Swiggy are driving growth by combining large-scale dark stores with rapid grocery fulfillment. This approach diversifies revenue streams while maximizing the utilization of fixed assets. Additionally, Saudi Arabia's Vision 2030 and NEOM city's urban planning initiatives are supporting the regional cloud kitchen market by allocating specific zones for delivery-only facilities.

North America, a mature market, is defined by aggregator dominance and stricter labor regulations. The Wonder Group is expanding vertically integrated hubs along the east coast, strategically located near densely populated residential areas to ensure faster deliveries and maintain food quality. Similarly, Kitchen United's store-within-store model in Kroger supermarkets highlights a shift in retailers' roles from tenants to collaborative partners. This strategy not only creates new revenue opportunities but also builds consumer trust through physical presence. In California, sustainability regulations have increased compliance costs but have also driven innovation in compostable packaging, setting trends that are being adopted in Europe.

South America, the Middle East, and Africa are in earlier stages of development but show significant growth potential. In 2024, Brazil's off-premise dining market reached BRL 61.4 billion, with Mexico following a similar growth pattern due to fintech advancements facilitating the transition from cash to digital payments. GCC markets benefit from strong purchasing power and a cosmopolitan workforce, while Sub-Saharan Africa faces challenges due to fragmented cold-chain infrastructure. However, strategic franchising and mobile-first ordering solutions are helping bridge these gaps, positioning emerging economies as critical demand centers in the next phase of the global cloud kitchen market.

Competitive Landscape

The cloud kitchen market remains fragmented, driven by established players, delivery aggregators, and a growing number of startups. Leading companies such as Rebel Foods, CloudKitchens, Kitopi, and Grab Holdings Limited (GrabKitchen) are solidifying their positions by leveraging multi-brand portfolios, proprietary technology platforms, and strategies for international expansion. Simultaneously, delivery aggregators like Zomato, Swiggy, DoorDash, and Meituan are strengthening their foothold by launching or investing in cloud kitchen networks, thereby gaining tighter control over the value chain.

Traditional restaurant chains, including Wendy’s and Pizza Hut, are also joining the competition by introducing delivery-only outlets to reduce overhead costs. However, as the competition escalates, independent operators are entering the market, attracted by relatively low entry barriers. To compete effectively in this crowded space, many players are adopting AI-driven kitchen management, robotics, and virtual brand partnerships to improve operational efficiency and expand their consumer reach. The competitiveness of this market is characterized by the relentless drive for scale, speed, and technology-driven differentiation.

Cloud kitchen operators are increasingly utilizing advanced data analytics to optimize menu offerings based on real-time consumer preferences and regional tastes. Innovations in contactless delivery and automated order fulfillment are accelerating service times and enhancing customer satisfaction. Partnerships with food tech startups and ingredient suppliers are enabling faster product development cycles. As consumer awareness grows, sustainability initiatives—such as eco-friendly packaging and energy-efficient kitchen operations—are becoming critical differentiators. Together, these strategies enable cloud kitchens to remain agile and competitive in the global market.

Cloud Kitchen Industry Leaders

-

CloudKitchens

-

Rebel Foods

-

Kitopi Catering Services LLC

-

Everybody Eats (C3)

-

Grab Holdings Limited (GrabKitchen)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Tollywood star Akkineni Naga Chaitanya launched Scuzi, a new cloud kitchen in Hyderabad offering global comfort food, showcasing celebrity-led cloud kitchen expansions in regional markets. This venture follows the success of his pan-Asian cloud kitchen, Shoyu. Scuzi focuses on comfort food with a global twist, offering dishes like burgers, pizzas, pastas, and more, available for delivery through platforms like Swiggy and Zomato.

- March 2025: CloudKitchens rolled out the Otter POS platform, consolidating multi-channel orders with kitchen display support. The company uses Otter POS to manage orders from various sources, like in-store point-of-sale, online ordering platforms, and delivery apps, through a single, unified interface. This centralized system helps streamline operations and reduce errors.

- February 2025: Rebel Foods, a cloud kitchen unicorn, has launched "QuickiES," a standalone app aimed at the 15-minute food delivery market, positioning itself to rival giants like Zomato and Swiggy. In its pilot phase, QuickiES is focusing on specific pin codes in Mumbai, offering deliveries from over 45 brands.

- October 2024: Public company Fruitas Holdings acquired Fly Kitchen Inc., adding four kitchens and expanding its multi-brand delivery capabilities in Metro Manila.

Global Cloud Kitchen Market Report Scope

A cloud kitchen (also known as a ghost, dark, or virtual kitchen) is a delivery-only restaurant business that operates without a physical dining area or storefront. The cloud kitchen market report is segmented by nature of operation, cuisine type, ordering model, and geography. By nature of operation, the market is segmented into independent cloud kitchens and chain cloud kitchens. By cuisine type, the market is segmented into Asian cuisine, European cuisine, Middle Eastern cuisine, Mexican cuisine, North American cuisine, and other cuisine types. By ordering model, the market is segmented into third-party aggregator platforms, direct-to-consumer websites/apps, and subscription meal plans. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, the Middle East and Africa. For each segment, the market forecasts are provided in terms of value (USD).

| Independent Cloud Kitchen |

| Chained Cloud Kitchen |

| Asian Cuisine |

| European Cuisine |

| Middle Eastern cuisine |

| Mexican Cuisine |

| North American Cuisine |

| Other Cuisine Types |

| Third-Party Aggregator Platforms |

| Direct-to-Consumer Websites/Apps |

| Subscription Meal Plans |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Nature of Operation | Independent Cloud Kitchen | |

| Chained Cloud Kitchen | ||

| By Cuisine Type | Asian Cuisine | |

| European Cuisine | ||

| Middle Eastern cuisine | ||

| Mexican Cuisine | ||

| North American Cuisine | ||

| Other Cuisine Types | ||

| By Ordering Model | Third-Party Aggregator Platforms | |

| Direct-to-Consumer Websites/Apps | ||

| Subscription Meal Plans | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the cloud kitchen market by 2031?

The sector is expected to reach USD 90.51 billion by 2031, reflecting robust consumer adoption and continued venture funding.

Which region is growing fastest in cloud kitchen deployments?

Asia-Pacific leads with an 18.24% CAGR forecast through 2031, supported by high smartphone penetration and favorable urbanization policies.

How do aggregator commissions affect kitchen profitability?

Effective commission rates can climb above 40%, cutting operator margins to single digits unless mitigated by direct-to-consumer channels or vertical integration strategies.

Why are subscription meal plans gaining traction?

Subscriptions provide predictable demand and higher customer lifetime value, allowing kitchens to optimize labor scheduling and batch production for cost savings.

Page last updated on: