Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

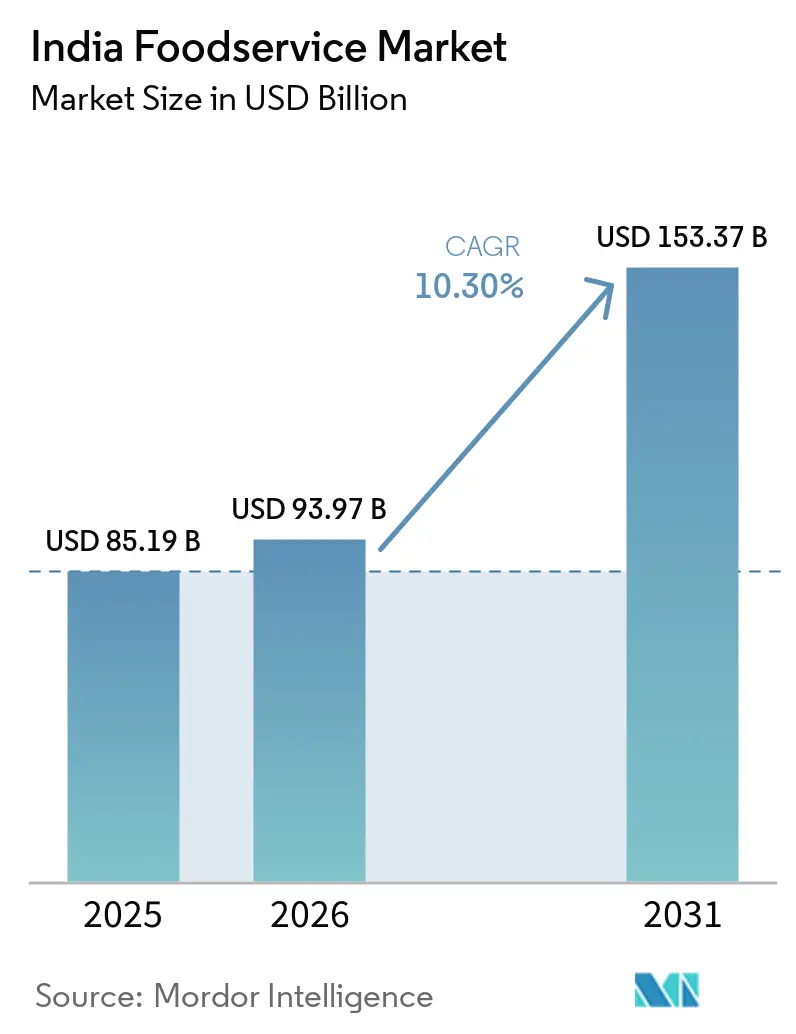

| Base Year Market Size (2025) | USD 85.19 Billion |

| Market Size (2026) | USD 93.97 Billion |

| Market Size (2031) | USD 153.37 Billion |

| Growth Rate (2026 - 2031) | 10.30% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Foodservice Market Analysis by Mordor Intelligence

The India foodservice market size is expected to grow from USD 85.19 billion in 2025 to USD 93.97 billion in 2026 and is forecast to reach USD 153.37 billion by 2031 at 10.3% CAGR over 2026-2031. The expansion of digital payments, urban migration, and the steady rise of working women are reshaping household consumption, steering demand toward prepared meals and technology-enabled ordering. The India foodservice market continues to split between experience-oriented full-service outlets and convenience-led delivery models, while cloud kitchens win share through lower overheads and data-driven menu optimization. Growing domestic tourism, improved highway infrastructure, and airport upgrades broaden the India foodservice market footprint beyond metropolitan cores. Meanwhile, aggregator platforms deepen penetration in tier-2 and tier-3 cities, catalyzing franchise investments and widening the market’s geographic base. Heightened FSSAI (Food Safety and Standards Authority of India) scrutiny pushes operators to formalize hygiene protocols, raising barriers for unorganized vendors and nudging them toward licensing compliance

Key Report Takeaways

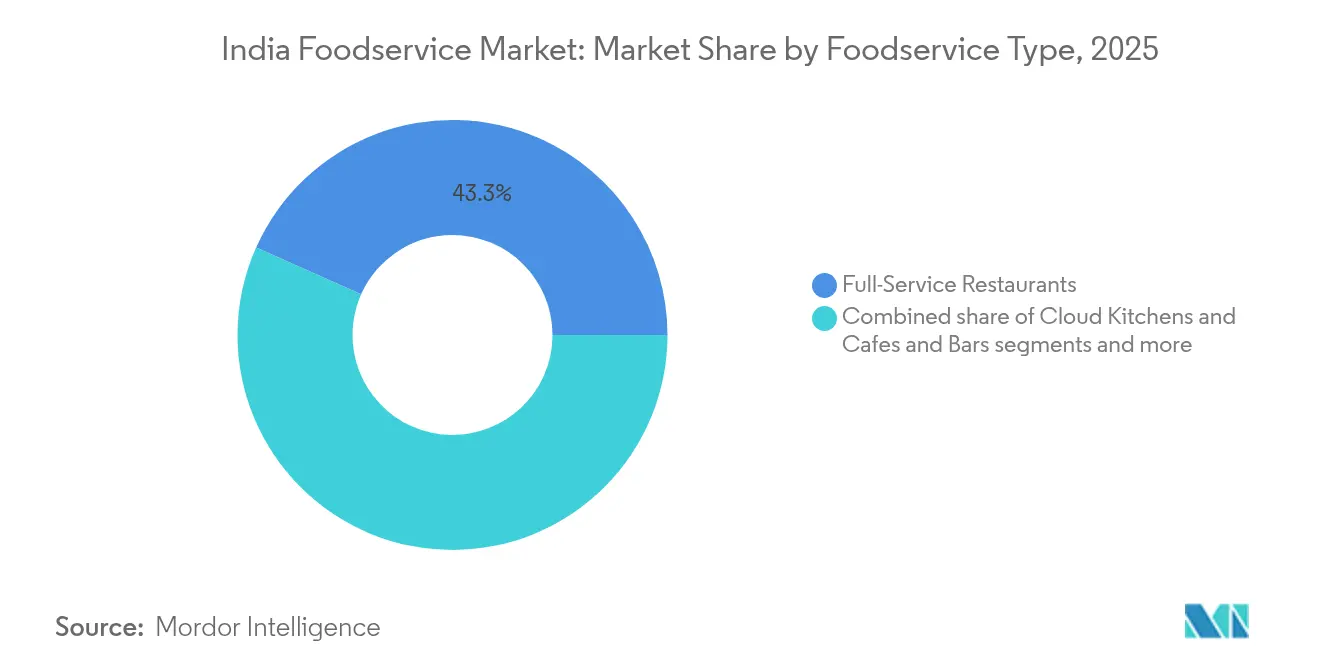

- By foodservice type, full-service restaurants led with 43.33% of India foodservice market share in 2025; cloud kitchens are advancing at an 18.29% CAGR through 2031, the fastest pace among all formats.

- By outlet, independent players controlled 64.76% of the India foodservice market size in 2025; chained concepts are forecast to grow at a 10.78% CAGR through 2031.

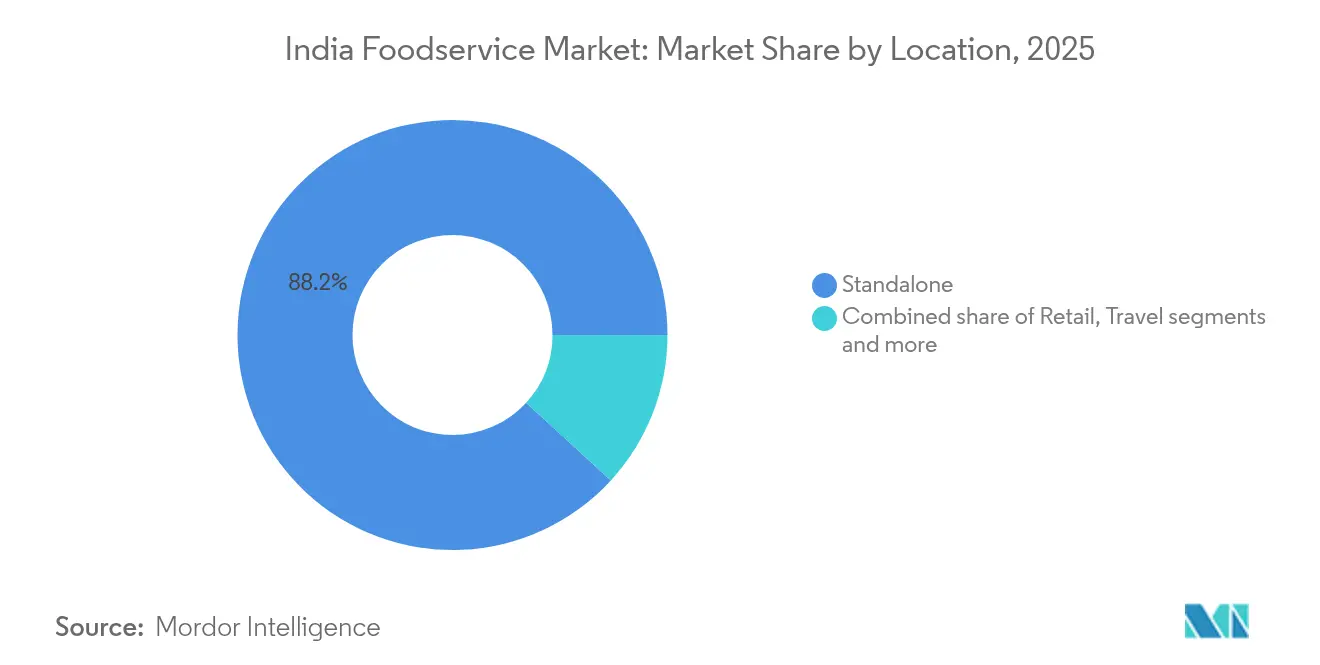

- By location, standalone outlets held 88.18% of India foodservice market share in 2025; travel hubs recorded the highest growth trajectory at a 14.13% CAGR through 2031.

- By service type, dine-in accounted for 59.49% of India foodservice market; delivery channels are expanding at a 12.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing dining out and convenience food consumption | +2.5% | National, with concentration in metro and tier-1 cities | Medium term (2-4 years) |

| Increasing westernization and food variety preferences | +1.8% | Urban centers, tier-1 and tier-2 cities | Long term (≥ 4 years) |

| Growing tourism and business travel boosting demand for hotels and restaurants | +1.5% | Travel hubs (airports, railway stations), tourist destinations | Medium term (2-4 years) |

| Investments in infrastructure and government support for the hospitality sector | +1.2% | National, with emphasis on tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Rising number of working women and dual-income households | +2.0% | Urban areas, particularly metros and tier-1 cities | Short term (≤ 2 years) |

| Increasing penetration of smartphones facilitating online ordering and delivery | +2.2% | National, accelerating in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing dining out and convenience food consumption

Rising dining-out frequency and growing consumption of convenience foods are key structural drivers of India’s foodservice market, as urban consumers balance longer working hours, commuting time and nuclear family living with higher disposable incomes and aspirational lifestyles. Eating out has shifted from an occasional treat to a routine social and lifestyle activity, especially among millennials and Gen Z, boosting demand for quick-service restaurants, cafés, casual dining and food courts in malls and transit hubs. In parallel, strong growth in convenience formats ready‑to‑eat and ready‑to‑cook meals, frozen snacks and delivery‑friendly items supports foodservice operators by enabling faster turnarounds, standardized quality and efficient delivery and takeaway models, including cloud kitchens and aggregator-led online ordering. Together, these shifts expand average transaction frequency, increase per‑capita spend on out‑of‑home food, and encourage rapid chain expansion into tier 2 and tier 3 cities, underpinning robust double‑digit growth expectations for India’s foodservice industry over the medium term.

Growing tourism and business travel boosting demand for hotels and restaurants

Growing tourism and business travel have significantly boosted demand for hotels and restaurants in India, with the country recording approximately 56 lakh Foreign Tourist Arrivals (FTAs) till August 2025 according to the Press Information Bureau, Ministry of Tourism[1]Press Information Bureau, "World Tourism Day", pib.gov.in. This influx of international visitors has fueled the expansion of the foodservice market as hotels, resorts, and standalone restaurants experience increased patronage. Culinary tourism, where travelers seek authentic local food experiences, has become a key attraction, encouraging establishments to offer region-specific cuisines and immersive dining. The surge in travel not only raises demand for quality food and beverage services but also stimulates economic growth by creating jobs and supporting local food ecosystems. India's strategic focus on combining culinary experiences with tourism continues to enhance the overall appeal of the foodservice industry through vibrant gastronomic offerings and hospitality excellence.

Investments in infrastructure and government support for the hospitality sector

Investments in infrastructure and strong government support are crucial drivers of India’s foodservice market growth. The government has allocated substantial funds to tourism infrastructure in the 2025-26 budget, including over INR 2,500 crore for developing top tourist destinations in partnership with states[2]Press Information Bureau, "Tourism as a Key Driver for Employment and Growth Budget 2025-26 Focuses on Infrastructure, Medical Tourism, and Heritage Conservation", pib.gov.in, aiming to enhance tourism-driven economic growth. Initiatives like Swadesh Darshan 2.0, improved air connectivity under schemes such as UDAN (Ude Desh ka Aam Nagrik), streamlined e-visa facilities, and infrastructure status granted to hotels have collectively improved ease of doing business and investor confidence in the hospitality sector. These efforts, along with rapidly expanding regional airports, highways, and air routes, are boosting connectivity to tier II and tier III cities, enabling wider access to emerging tourism circuits. This infrastructure growth, coupled with government incentives such as tax breaks and simplified approvals, is stimulating hotel and restaurant investments, expanding capacity, and improving service quality across urban and rural areas, solidifying the foundation for sustained foodservice market expansion in India.

Increasing penetration of smartphones facilitating online ordering and delivery

The rising penetration of smartphones has significantly accelerated the digital transformation of India’s foodservice market, enabling a seamless shift towards online food delivery and ordering. This digital growth is fueled by the increasing availability of affordable smartphones and robust internet connectivity, which supports a broader consumer base adopting app-based food delivery platforms. Notably, as of March 2024, India had an extensive internet subscriber base of approximately 954.4 million, with 556.05 million in urban and 398.35 million in rural areas, contributing to a tele-density of 85.7%[3]Invest India, "India’s internet surge: Catalyzing change in the telecom landscape", investindia.gov.in. This widespread digital access has empowered consumers across urban and rural regions to embrace the convenience of online food services, driving the rapid expansion of cloud kitchens and virtual brands optimized for delivery. Technology integration, including AI-driven personalization and digital payment solutions, further enhances the customer experience, reinforcing this trend and enabling foodservice operators to scale efficiently in an increasingly digital market landscape.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent food safety and hygiene regulations | -0.8% | National, with stricter enforcement in metro cities | Medium term (2-4 years) |

| Inconsistent quality and supply chain issues | -1.0% | National, more acute in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| Intense competition among unorganized and organized players | -1.2% | National, particularly in urban centers | Short term (≤ 2 years) |

| Cultural and regional food preferences limiting standardization | -0.6% | Regional, varying by state and community | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent food safety and hygiene regulations

Stringent food safety and hygiene regulations pose a significant restraint to the growth of India’s foodservice market, as compliance demands can be complex and costly for operators. The Food Safety and Standards Authority of India (FSSAI) enforces rigorous standards covering hygiene, sanitation, food handling, labeling, and packaging to protect public health and ensure quality. All food businesses, from street vendors to large restaurant chains, must obtain an FSSAI license, prominently display their license details, and adhere to detailed requirements such as temperature controls, allergen management, and regular inspections. While these regulations build consumer trust and safeguard health, the evolving and stringent compliance landscape also increases operational challenges and entry barriers for many foodservice providers, particularly smaller players.

Intense competition among unorganized and organized players

Intense competition between unorganized and organized players is a significant restraint in the India foodservice market, creating challenges for market stability and growth. The unorganized sector, comprising small roadside eateries, street vendors, and local food stalls, continues to dominate large parts of the market due to its low cost and accessibility. Meanwhile, organized players such as branded quick-service restaurants (QSRs), café chains, and fine-dining establishments are expanding rapidly, leveraging strong brand recognition, superior service quality, and technology integration. This competitive landscape results in price wars, margin pressures, and high customer acquisition costs for many operators. Additionally, smaller unorganized players often struggle to comply with increasing regulations and quality standards, complicating efforts to scale or formalize. The coexistence of these divergent market segments intensifies rivalry, limits pricing power, and raises operational complexities for all players, thereby restraining the overall market’s efficiency and profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Disrupt Traditional Formats

Full-service restaurants (FSRs) dominated the India foodservice market, holding the largest market share of 43.33% in 2025. This segment’s leading position is driven by its ability to offer a comprehensive dining experience that combines a comfortable ambiance, personalized waiter service, and an extensive variety of cuisines. FSRs appeal to a broad customer base, including families, business professionals, and social groups who seek leisurely and upscale dining occasions. The growth of this segment is also fueled by rising disposable incomes and increasing urbanization across India, encouraging consumers to dine out more frequently. Furthermore, FSRs generate higher revenues per customer due to multi-course meals and significant beverage sales, positioning them as a premium segment within the market. Their adaptability in providing both traditional regional dishes and international cuisines allows them to cater to India’s culturally diverse population, ensuring sustained demand and growth.

The cloud kitchen segment represents the fastest-growing foodservice format in India, advancing at an impressive compound annual growth rate (CAGR) of 18.29% through 2031. This rapid expansion is primarily driven by the surge in demand for convenient, on-demand food delivery enabled by the widespread adoption of digital ordering platforms and mobile apps. Cloud kitchens benefit from lower operational costs compared to traditional dine-in restaurants since they operate without storefronts, focusing exclusively on food preparation and delivery. Investors and food tech companies are actively fueling growth in this sector, especially in metropolitan areas with tech-savvy consumers. Additionally, cloud kitchens allow foodservice operators to experiment with diverse menus and niche cuisines without the heavy investment usually required for physical outlets. This agility combined with the increasing preference for home delivery among younger demographics positions cloud kitchens as a transformational force reshaping the Indian foodservice landscape.

By Outlet: Chained Formats Scale Through Aggregator Partnerships

Independent players dominated the India foodservice market by outlet type, controlling a substantial 64.76% share in 2025. This segment's dominance is largely attributed to its deep roots in local communities and its ability to offer personalized dining experiences that resonate with regional tastes and preferences. Independent outlets typically showcase a diverse range of cuisines, often experimenting with fusion and innovative dishes tailored to local palates. These establishments benefit from their flexibility in menu design, pricing strategies, and rapid responsiveness to consumer trends and feedback. Being often owner-managed, independent outlets provide attentive customer service and cultivate strong customer loyalty. Additionally, their relatively lower overhead costs compared to chained counterparts allow them to operate competitively across both urban and rural areas, supporting their strong market presence.

On the other hand, chained concepts represent the fastest-growing segment within the Indian foodservice market, forecasted to expand at a CAGR of approximately 10.78% through 2031. This growth surge is fueled by increasing brand awareness, standardization of food quality, and efficient operational models that resonate with the evolving urban consumer’s preference for consistent and convenient dining options. Chain outlets, including quick-service restaurants (QSRs) and limited-service formats, are rapidly expanding their footprint beyond metropolitan areas into tier-2 and tier-3 cities, tapping into new consumer bases driven by rising disposable incomes and changing lifestyles. The scalability and marketing prowess of chained players enable them to leverage technology platforms effectively, enhancing customer engagement through loyalty programs and digital ordering. The ongoing urbanization, lifestyle shifts, and preference for branded, hygienic food options further accelerate the adoption and growth of the chained segment.

By Location: Travel Hubs Capture Premium Pricing Power

Standalone outlets dominated the India foodservice market by location in 2025, accounting for a substantial 88.18% share. These outlets have established their stronghold largely due to their strategic presence in high-traffic and easily accessible areas. Standalone outlets encompass a wide variety of foodservice formats such as local restaurants, cafes, and quick-service establishments, appealing to consumers seeking convenient and personalized dining experiences. Their widespread presence in residential, commercial, and mixed-use zones allows them to cater to a diverse clientele with varied dining preferences. The flexibility of these outlets to offer customized menus, competitive pricing, and local specialties further strengthens their market position. Additionally, standalone outlets are benefiting from the rising popularity of food delivery services, which have expanded their reach beyond physical locations, boosting their overall market dominance.

In contrast, travel hubs represent the fastest growing segment in the Indian foodservice industry, projected to grow at a CAGR of 14.13% through 2031. This high growth trajectory is driven by increasing domestic and international travel, alongside expanding airport, railway, and highway infrastructure improvements, which have led to a surge in demand for foodservice outlets in these transit areas. Travel hub foodservice providers cater to a dynamic mix of travelers seeking quick, quality meals during their journeys, favoring formats that emphasize speed, convenience, and hygiene. The increasing penetration of branded quick-service restaurants and cafes within airports and railway stations has raised consumer expectations and preferences for standardized dining experiences in these locations. Moreover, private sector investments and government initiatives aimed at upgrading travel infrastructure and enhancing passenger amenities are fueling the expansion of foodservice outlets in travel hubs.

By Service Type: Delivery Channels Reshape Economics

The dine-in service type held the largest share of the India foodservice market, accounting for 59.49% in 2025. This segment’s dominance is fueled by the cultural and social significance of dining out in India, where it is often regarded as a communal activity that encourages social interaction. Dine-in establishments provide consumers with the advantages of controlled food quality, personalized service, and the opportunity to enjoy food in an ambient setting, enhancing the overall dining experience. Moreover, this segment includes a wide range of formats such as full-service restaurants, cafes, and casual dining joints, offering diverse culinary options that cater to the varied preferences of Indian consumers. The growth of urban middle-class consumers with rising disposable incomes and a penchant for exploring different cuisines has further solidified the dominance of dine-in services.

Conversely, delivery channels represent the fastest-growing segment in the India foodservice market, expanding at a CAGR of 12.52% through 2031. This rapid growth is driven by the increasing adoption of digital food delivery platforms and mobile applications, which provide consumers with unparalleled convenience and access to a wide variety of dining options from the comfort of their homes. The delivery model has gained significant traction among urban and tech-savvy populations, especially millennials and Gen Z, who prioritize speed and convenience in food consumption. The COVID-19 pandemic accelerated the shift towards delivery services, introducing new consumer behaviors that persist as long-term trends. Furthermore, cloud kitchens and restaurant delivery expansions have enhanced the scalability and reach of this segment by minimizing operational costs associated with dine-in facilities.

Geography Analysis

In India, the foodservice market divides into four main regions: West, North, South, and East, with each region contributing uniquely to the market's dynamics. The West leads as the dominant player, driven by metropolitan giants like Mumbai, Pune, and Ahmedabad. High urbanization, increasing disposable incomes, and a rich culinary heritage that blends local and fusion cuisines propel this region's growth. Mumbai, often referred to as India's "food capital," showcases a vibrant dining scene that ranges from bustling street food stalls to upscale international restaurants, firmly establishing its critical role in the foodservice sector.

North India significantly influences the market, with urban centers like Delhi, Gurugram, and Chandigarh fostering strong foodservice demand. Rapid urbanization, rising affluence, and a cosmopolitan population drive this growth. The region supports a variety of foodservice formats, including quick-service restaurants (QSRs), casual dining, and fine dining, catering to the diverse preferences of its consumers. Additionally, the increasing adoption of digital food delivery platforms strengthens the foodservice ecosystem in the North, providing consumers with greater access and convenience.

South India experiences fast-paced growth, led by technology hubs like Bengaluru and Hyderabad. A young and dynamic workforce fuels demand for quick, affordable, and varied dining options. To meet these evolving consumer preferences, cloud kitchens and fast-casual dining formats are expanding rapidly. Meanwhile, East India, with Kolkata at the forefront, grows steadily, supported by increasing urbanization and economic development. Together, these regions create a vibrant Indian foodservice landscape, reflecting regional culinary diversity, strong urban demand, and a seamless blend of traditional and modern dining experiences.

Competitive Landscape

The competitive landscape of the India foodservice market is highly fragmented, characterized by a diverse mix of global chains, domestic players, and numerous small local operators. Major international brands such as McDonald's, Starbucks, Domino's, KFC, and Yum! Brands hold significant market share, leveraging their global brand recognition and standardized operating models. Alongside these giants, prominent Indian players like Jubilant FoodWorks, Barbeque Nation Hospitality, and Haldiram's cater deeply to local tastes and preferences, adding to the competitiveness by blending regional flavors with scalable business models.

Fragmentation also stems from the coexistence of traditional family-owned eateries and modern chain restaurants across various segments including full-service restaurants, quick-service restaurants (QSRs), cafes, and the rapidly expanding cloud kitchen sector. This diversity creates intense competition as each segment targets different consumer groups from budget-conscious customers to premium diners. Cloud kitchens, in particular, are gaining momentum due to their low overhead costs and ability to rapidly scale via digital food delivery platforms, intensifying competition especially in urban and tier-2 cities.

Innovation and operational agility are critical for sustaining competitiveness in this fragmented market. Companies focus on menu localization, tech integration such as digital ordering and kitchen automation, and strategic partnerships with food delivery platforms to expand market reach and enhance customer experience. The franchise model dominates expansion strategies, supporting rapid growth into newer markets while managing operational costs. Overall, the competitive dynamics in India's foodservice market reflect a vibrant ecosystem driven by consumer diversity, regional variation, and a blend of traditional and cutting-edge business models fostering continuous evolution and market penetration.

India Foodservice Industry Leaders

-

Jubilant FoodWorks Limited

-

McDonald's Corporation

-

Yum! Brands, Inc.

-

Coffee Day Enterprises Ltd

-

Barista Coffee Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Subway experienced rapid expansion in India during the first quarter of FY26, opening 33 new stores across 17 cities and raising its total store count in the country to over 900 outlets. This growth followed Subway's addition of 15 stores in the previous quarter, with ambitions to exceed 100 new openings by the fiscal year's end.

- July 2025: India's speciality coffee chain, Third Wave Coffee unveiled 11 new cafes in Delhi, Hyderabad, Chennai, Mumbai, and Mysuru on a single day. These openings brought the brand's total to 165 cafes spanning 12 cities, showcasing its stronghold in both emerging and established markets.

- March 2025: Jubilant FoodWorks announced an ambitious target to expand its Domino's Pizza store network to 3,000 outlets by 2028, up from approximately 2,100 in 2024, while scaling Popeyes from 60 to 200-250 outlets within 3 years.

- March 2025: Chai Kings received a Rs 24 crore investment to expand their tea-centric cafe concept across North India. The initiative focused on integrating traditional chai culture with a modern presentation and ambiance, aiming to cater to a broader audience.

India Foodservice Market Report Scope

Cafes & Bars, Cloud Kitchen, Full Service Restaurants, Quick Service Restaurants are covered as segments by Foodservice Type. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.

By Foodservice Type

| Cafés and Bars | Bars and Pubs |

| Cafés | |

| Juice/Smoothie/Dessert Bars | |

| Specialist Coffee and Tea Shops | |

| Cloud Kitchens | |

| Full-Service Restaurants | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other FSR Cuisines | |

| Quick-Service Restaurants | Bakeries |

| Burger | |

| Ice-cream | |

| Meat-based Cuisines | |

| Pizza | |

| Other QSR Cuisines |

Outlet

| Chained Outlets |

| Independent Outlets |

Location

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

Service Type

| Dine-in |

| Takeaway |

| Delivery |

| By Foodservice Type | Cafés and Bars | Bars and Pubs |

| Cafés | ||

| Juice/Smoothie/Dessert Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchens | ||

| Full-Service Restaurants | Asian | |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick-Service Restaurants | Bakeries | |

| Burger | ||

| Ice-cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines | ||

| Outlet | Chained Outlets | |

| Independent Outlets | ||

| Location | Leisure | |

| Lodging | ||

| Retail | ||

| Standalone | ||

| Travel | ||

| Service Type | Dine-in | |

| Takeaway | ||

| Delivery | ||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms