United Kingdom Full Service Restaurants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

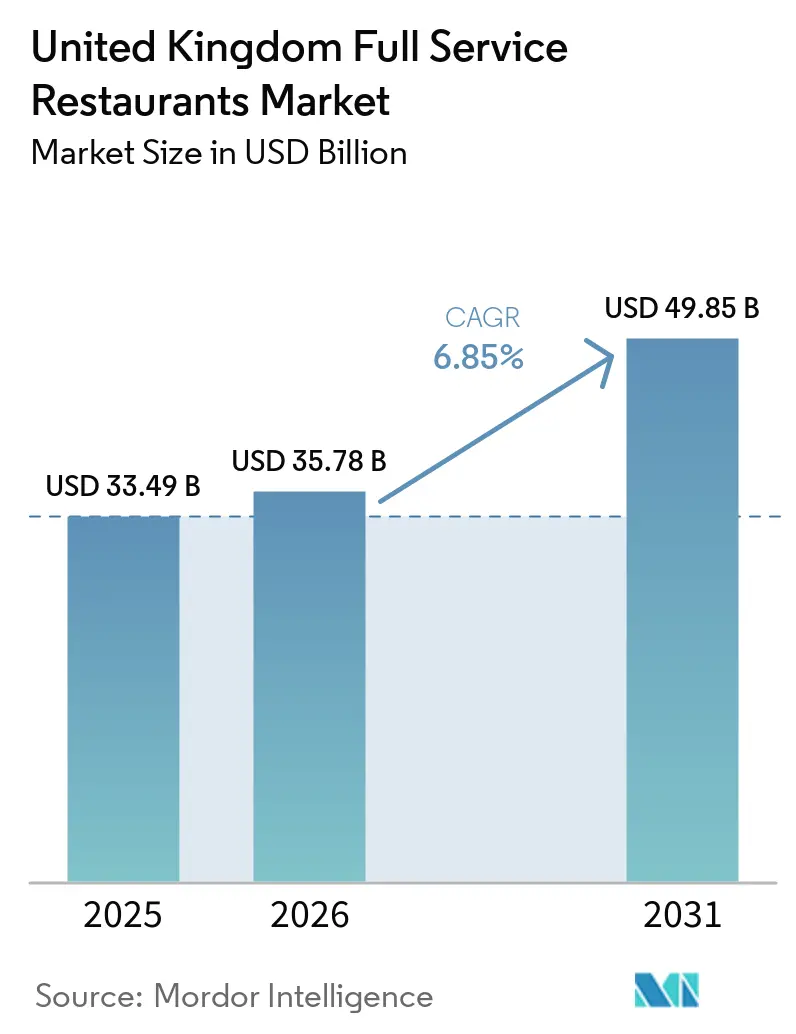

| Base Year Market Size (2025) | USD 33.49 Billion |

| Market Size (2026) | USD 35.78 Billion |

| Market Size (2031) | USD 49.85 Billion |

| Growth Rate (2026 - 2031) | 6.85% CAGR |

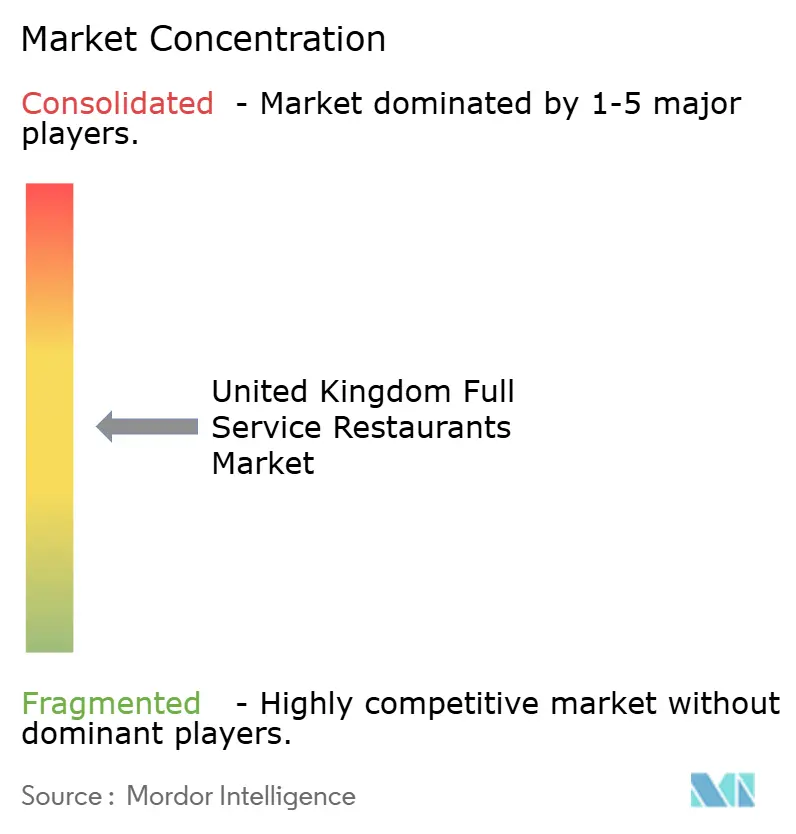

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Full Service Restaurants Market Analysis by Mordor Intelligence

The United Kingdom full service restaurant market size was valued at USD 33.49 billion in 2025 and estimated to grow from USD 35.78 billion in 2026 to reach USD 49.85 billion by 2031, at a CAGR of 6.85% during the forecast period (2026-2031). Digital ordering, experience-led dining, and sustained menu innovation are reshaping competitive dynamics as operators pivot from location-driven models to omnichannel engagement. Independent venues still dominate footfall, yet chained concepts accelerate faster by leveraging scale in data analytics, procurement, and labor scheduling. Consumers increasingly favor restaurants that embed sustainability in sourcing and operations, rewarding brands that disclose carbon metrics and invest in energy-efficient kitchens. At the same time, regulatory cost pressure from a higher National Living Wage and elevated National Insurance contributions to margin compression, sharpening focus on automation and dynamic pricing. Technology partnerships spanning AI-enabled point-of-sale, reservation, and loyalty platforms give adopters a measurable edge in maximizing revenue per labor hour.

Key Report Takeaways

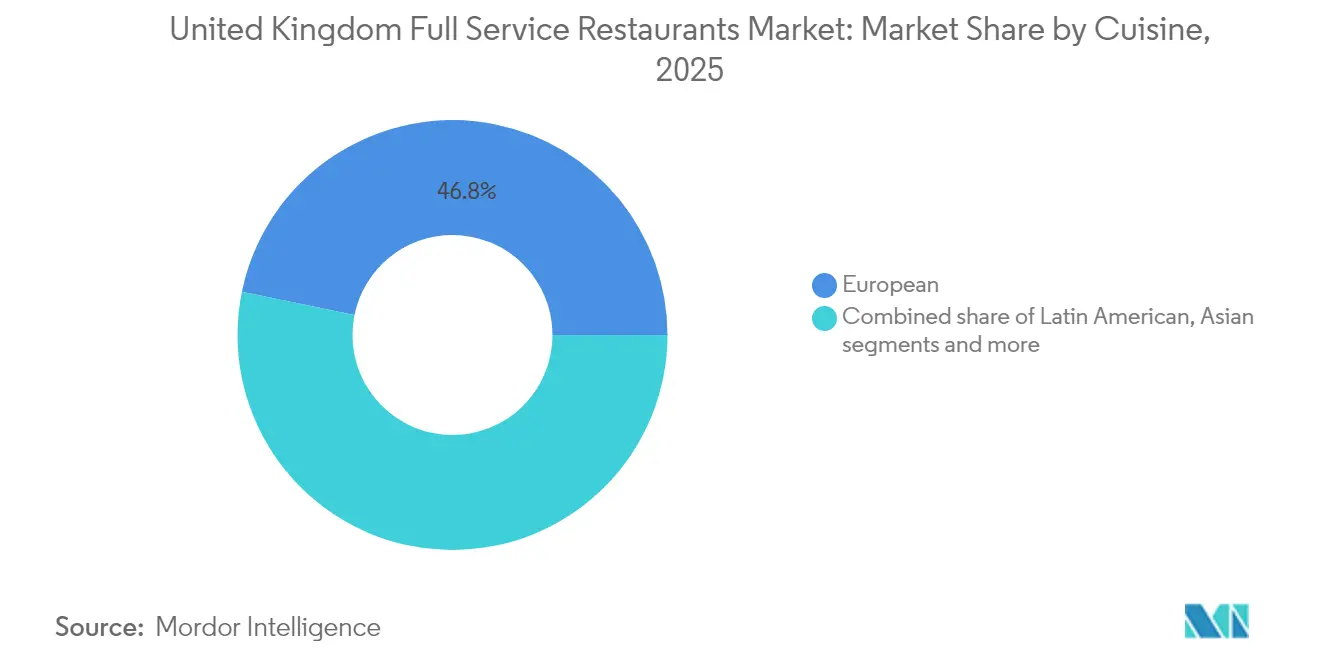

- By cuisine, European dishes led with 46.78% revenue share in 2025, while Latin American cuisine is projected to expand at an 7.79% CAGR through 2031.

- By outlet, independent outlets accounted for 66.85% of spending in 2025, whereas chained counterparts are advancing at a 7.52% CAGR to 2031.

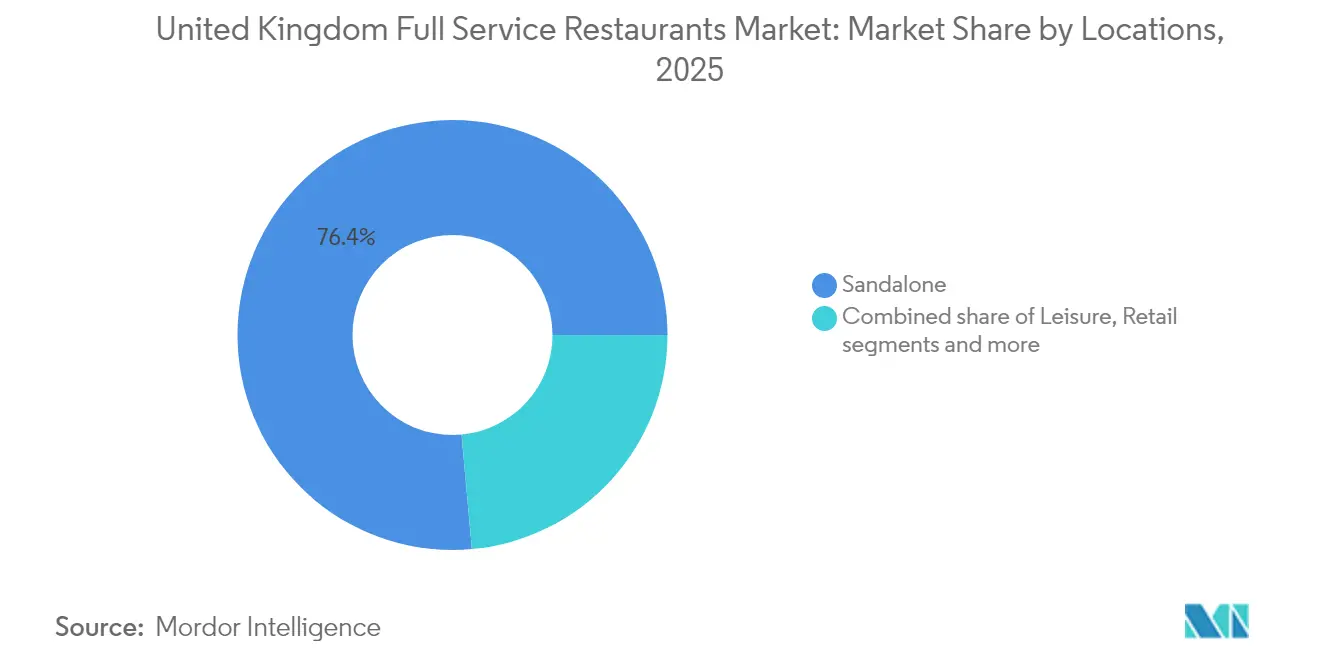

- By location, standalone restaurants captured a 76.44% share in 2025, with lodging-based venues forecast to grow at a 10.23% CAGR over the period.

- By service type, dine-in visits made up 68.92% of revenue in 2025, yet delivery formats are set to rise at a 8.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Full Service Restaurants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising popularity of international cuisines | +1.5% | National, with concentration in London, Manchester, Birmingham | Medium term (2-4 years) |

| Increasing consumer demand for healthier and plant-based menu options | +0.8% | National, strongest in urban centers and affluent suburbs | Long term (≥ 4 years) |

| Growth in food tourism enhancing demand for authentic dining experiences | +1.2% | National, with premium impact in tourist destinations | Medium term (2-4 years) |

| Expansion of hotel and lodging businesses supporting in-premise dining | +0.9% | National, concentrated in business districts and tourist areas | Long term (≥ 4 years) |

| Digital reservation and loyalty platforms boost visit frequency | +1.1% | National, with faster adoption in metropolitan areas | Short term (≤ 2 years) |

| Government rate relief and targeted hospitality support | +0.7% | National, with enhanced benefits for smaller operators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising popularity of international cuisines

Cultural diversity and the growing popularity of international cuisines are driving significant changes in the United Kingdom's full-service restaurant industry. Operators are increasingly innovating menus to cater to consumers seeking authentic global flavors. VisitBritain research highlights the enduring appeal of iconic British dishes alongside a rising curiosity for international fare among locals and visitors, creating opportunities for hybrid concepts that merge local and global culinary traditions. The University of Birmingham’s findings emphasize the role of restaurants as cultural bridges, where exposure to diverse cuisines influences social attitudes and reduces anti-immigrant biases, fostering cohesion in multicultural communities [1]Source: University of Birmingham, "Eating Food from Different Cultures Reduces Anti-immigrant Attitudes - Study", birmingham.ac.uk . Latin American restaurants are particularly capitalizing on this trend, achieving a CAGR of 8.23%, driven by unique flavor profiles and visually appealing dishes that resonate on social media platforms. Brands like Las Iguanas exemplify this approach with vibrant, Instagram-friendly presentations and accessible formats. The Food Standards Agency’s "Our Food 2023" report highlights regional variations, with cosmopolitan Londoners embracing international options, while Northern England maintains a preference for traditional British classics. These geographic differences enable operators to strategically tailor expansion plans and menu localization to align with regional preferences. By addressing consumer demand for novel dining experiences and contributing to social integration, the restaurant industry reinforces its commercial and societal relevance in a rapidly evolving foodservice landscape.

Increasing consumer demand for healthier and plant-based menu options

Consumer demand for healthier and plant-based menu options has reshaped the competitive dynamics of full-service restaurants in the United Kingdom, with plant-based offerings evolving from niche products to key revenue drivers. For example, Wagamama partnered with THIS to introduce the plant-based "vegatsu" in 2024, targeting health-conscious consumers while retaining loyal customers seeking familiar flavors. Similarly, Pizza Express achieved carbon-neutral status in 2024 and launched vegan "PiNO" cheese across all UK locations, showcasing how sustainability initiatives can drive menu innovation and differentiation. Regulatory support from Public Health England, including partnerships focused on calorie reduction, has positioned the development of healthier menus as a strategic advantage rather than a compliance obligation. The Vegan Society reported that the number of vegans in Great Britain increased to approximately 2 million (3% of the population) in 2024, highlighting a growing market segment that restaurants are addressing with diverse plant-based offerings [2]Source: The Vegan Society, "Nationwide Trends Highlight Growing Shift Toward Plant-Based Diets", vegansociety.com. These trends reflect broader health and sustainability priorities, encouraging restaurants to adopt plant-forward menus that cater not only to vegans but also to flexitarians and environmentally conscious diners. This shift drives menu diversification, strengthens brand appeal, and establishes a new benchmark for competitive positioning. Brands like Wagamama and Pizza Express exemplify how innovation, partnerships, and sustainability initiatives can align to meet the increasing consumer demand for plant-based and healthier dining options in the UK.

Growth in food tourism enhancing demand for authentic dining experiences

Food tourism significantly drives the demand for authentic dining experiences, serving as a key motivator for both domestic and international travelers in the United Kingdom. According to the House of Commons Library, overseas residents made 42.5 million visits to the UK in 2024, an increase from 38 million in 2023, highlighting the growth of inbound tourism, which directly benefits the hospitality sector [3]Source: House of Commons Library, "Tourism: Statistics and Policy", commonslibrary.parliament.uk . The Department for Business & Trade’s hospitality strategy identifies food and drink as central to the UK’s tourism appeal, with initiatives such as the "Food is GREAT" campaign, in collaboration with DEFRA, promoting British culinary excellence on a global scale. Also, OpenTable’s Top 100 UK restaurants showcase a geographic distribution of popular, authentic local dining experiences beyond major cities, where such establishments achieve premium pricing and higher customer loyalty compared to standardized chains, reflecting strong consumer demand for regional authenticity. Additionally, Airbnb's GBP 1 million "Best of British" fund supports restaurants that emphasize local culinary heritage and cultural storytelling, creating investment opportunities that enhance differentiated service offerings. These factors collectively illustrate how the integration of food tourism with the UK’s culinary heritage creates opportunities for full-service restaurants to capitalize on authentic experiences for commercial growth while contributing to the broader tourism economy. This trend fosters the sustainable development of regional gastronomic offerings, attracts diverse consumer segments from both tourism and domestic markets, and strengthens the sector’s competitive positioning and resilience.

Expansion of hotel and lodging businesses supporting in-premise dining

The expansion of hotel and lodging businesses is significantly influencing the market by repositioning food and beverage operations as essential profit centers rather than supplementary guest amenities. The British Institute of Innkeeping reports that hotel restaurants in Northern England are experiencing a 2.4% site growth in 2023, outperforming Southern markets and highlighting regional opportunities for lodging-based dining concepts. Besides, VisitEngland occupancy surveys indicate that the recovery of business travel is driving weekday demand in hotel restaurants, while leisure travel sustains weekend patronage, resulting in more balanced and resilient revenue streams compared to standalone restaurants. Furthermore, Deloitte’s hotel investment data identifies London and Edinburgh as prime destinations for hospitality capital, where elevated food and beverage quality serves as a critical differentiator amid room rate ceilings. This dynamic is exemplified by hotel brands such as The Hoxton, which leverage upscale dining to enhance guest experiences while appealing to both local and business diners. Collectively, these trends underscore how the growth of integrated dining within lodging properties fosters new revenue opportunities, better customer segmentation, and competitive advantages in the UK full-service restaurant market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing competition from quick service and casual dining segments | -1.2% | National, with intensified pressure in suburban and retail locations | Medium term (2-4 years) |

| High operational costs including staffing and ingredient procurement | -0.8% | National, with acute impact on independent operators | Short term (≤ 2 years) |

| Complex regulatory requirements related to health, safety, and food standards | -0.6% | National, with enhanced compliance burden on smaller operators | Long term (≥ 4 years) |

| Challenges with maintaining consistent quality and service standards | -0.4% | National, with particular impact on multi-site chain operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing competition from quick service and casual dining segments

Full-service restaurants in the United Kingdom face significant challenges due to increasing competition from quick-service and casual dining segments. These competitors are expanding into traditionally full-service domains by enhancing menu quality, upgrading service models, and adopting premium positioning, which blurs traditional category distinctions. This competitive pressure is particularly evident in suburban and retail locations, where full-service restaurants directly compete with fast-casual alternatives offering comparable food quality with faster service and lower price premiums. The doubling of energy costs since 2022 has disproportionately impacted full-service establishments due to longer customer dwell times and higher facility demands, creating structural cost disadvantages compared to quick-service models optimized for rapid turnover and minimal space usage. Additionally, food inflation forces full-service operators to either absorb rising costs or increase prices, narrowing the perceived value gap with casual dining. Independent restaurants are particularly affected, as they lack the bulk purchasing power of larger chains. The rise of delivery-optimized restaurant formats further intensifies competition by offering restaurant-quality food without the labor costs associated with full-service operations. This trend compels full-service operators to justify their premium pricing through superior customer experiences rather than food quality alone. Brands such as Honest Burgers illustrate how fast-casual formats can deliver elevated dining experiences at accessible prices, increasing competitive pressure on full-service restaurants. These factors collectively require full-service restaurants to innovate in both experience and value to maintain differentiation in a market increasingly shaped by the efficiency and convenience of quick-service models.

High operational costs including staffing and ingredient procurement

High operational costs are a significant challenge for operators in the full-service restaurant industry in the United Kingdom. Labor cost inflation, driven by recent increases in the National Living Wage and employer National Insurance Contributions, has substantially raised wage bills across the industry. These pressures are further intensified by severe staffing shortages, with many hospitality businesses reporting conditions approaching financial collapse as they struggle to maintain service levels amidst rising labor expenses. Ingredient procurement is also impacted by supply chain disruptions and commodity price volatility, both of which contribute to higher food costs. Additionally, energy expenses have doubled since 2022, further compressing profit margins. These cost pressures are prompting restaurants to explore strategies such as menu engineering, portion control, and operational efficiencies to sustain profitability. Independent operators are particularly vulnerable due to their limited purchasing power and difficulties in spreading fixed costs across multiple locations. This has driven consolidation trends, favoring larger chains that benefit from economies of scale. For instance, some chains have utilized their scale to negotiate more favorable supplier contracts and optimize labor costs. Moreover, increasing competition from quick-service and delivery-focused formats has added to the profitability challenges faced by full-service restaurants. To remain viable, these establishments must focus on operational excellence and strategic positioning to justify premium pricing and sustain their presence in the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cuisine: European Heritage Meets Latin Innovation

European cuisine holds a dominant 46.78% market share in 2025, reflecting the UK's strong cultural connection to Mediterranean, French, and Italian dining traditions. Latin American cuisine, however, is the fastest-growing segment, with an impressive 7.79% CAGR projected through 2031. This growth is driven by increasing consumer demand for bold flavors, visually appealing dishes, and authentic cultural experiences that stand out from mainstream offerings. Asian cuisine benefits from the UK's multicultural demographic and established supply chains, while Middle Eastern cuisine gains popularity due to its health-conscious positioning and innovative flavors. In contrast, North American cuisine faces challenges from market saturation in burger and barbecue concepts, prompting operators to shift toward premium positioning and experiential differentiation.

Research from the University of Birmingham highlights the societal value of diverse dining experiences, noting that exposure to various cuisines reduces cultural barriers and fosters social cohesion. This supports long-term demand for international offerings. Regional data from the Food Standards Agency reveals geographic differences in cuisine preferences: London leads in adopting international flavors, while Northern England shows a stronger preference for traditional European dishes. These insights present opportunities for operators who tailor their strategies to regional taste profiles. Additionally, the "Other FSR Cuisines" category encompasses emerging fusion concepts and plant-based innovators, signaling ongoing fragmentation and specialization within the broader market structure.

By Outlet: Independent Resilience Versus Chain Efficiency

Independent outlets hold a dominant 66.85% market share in 2025, yet chain operators are set to achieve faster growth with a strong 7.52% CAGR through 2031. This reflects a notable shift toward operational standardization and economies of scale, which favor multi-unit operators. Independent restaurants capitalize on local market knowledge, flexible menus, and authentic experiences to build customer loyalty. However, they face increasing challenges from rising operational costs and complex regulations, which disproportionately impact smaller operators. The sector-wide increase in the National Living Wage to GBP 12.21 per hour adds a significant cost burden, threatening the sustainability of independent businesses. In contrast, chain operators leverage their purchasing power and operational efficiencies to absorb these cost pressures effectively.

Technology adoption is driving competitive advantages for chain operators, who are implementing standardized POS systems, integrating delivery platforms, and utilizing customer relationship management tools. These technologies enable data-driven decision-making and operational optimization. According to the SevenRooms platform data, 74% of restaurant operators in the UK are expected to use artificial intelligence for operational improvements by 2025, with chain operators leading the way due to their investment capabilities and streamlined implementation processes. Independent operators are increasingly collaborating with technology providers and delivery platforms to access advanced operational tools. At the same time, they maintain their differentiation by focusing on personalized service, local sourcing, and menu innovation, areas that chain operators find difficult to replicate at scale.

By Locations: Standalone Dominance Faces Lodging Disruption

Standalone restaurants dominate the UK Full Service Restaurants market in 2025, holding a 76.44% share. Their success is attributed to location flexibility, brand independence, and strong community integration, which foster customer loyalty and a unique local appeal. However, this dominance is being challenged by lodging-based restaurants, which are growing at a robust 10.23% CAGR through 2031. Hotels increasingly treat food and beverage operations as profit centers rather than guest amenities, creating new competitive dynamics. Retail locations benefit from increased footfall and extended operating hours, while travel-based restaurants leverage captive audiences in airports and transport hubs to command premium pricing, capitalizing on convenience and location advantages. Standalone operators are responding to rising commercial rents and operational cost pressures by exploring partnerships with retail, lodging, and entertainment venues to access complementary customer flows and shared efficiencies, balancing the evolving competitive landscape. Brands such as The Hoxton exemplify successful integration of lodging and dining, combining upscale experiences that attract both hotel guests and local diners.

Simultaneously, leisure-oriented locations capture increased weekend and holiday demand through experiential positioning, which helps diversify revenue streams beyond traditional patterns. Standalone restaurants, with their agility and community ties, maintain a competitive edge in delivering personalized experiences, yet they face mounting pressure from lodging and retail establishments growing steadily through strategic investments and evolving consumer behavior. As lodging-based dining grows faster, it reshapes the market by offering diversified and scalable food and beverage models, compelling standalone operators to innovate through collaborations and enhanced customer engagement. This shift underscores a market transition where location dynamics, operational models, and consumer expectations intersect, requiring full service restaurant operators to adapt strategically to sustain growth and profitability in a competitive and evolving UK market.

By Service Type: Dine-In Evolution Meets Delivery Innovation

Delivery services are anticipated to grow at a CAGR of 8.88% through 2031. In 2025, dine-in services are expected to hold a significant 68.92% market share. These trends underscore a shift in consumer behavior, transitioning from pandemic-driven necessities to a preference for convenience. Restaurants are increasingly integrating with delivery platforms. By partnering with companies such as Deliveroo, Uber Eats, Stuart, and Otter, they are creating omnichannel experiences. This approach prioritizes maximizing revenue per kitchen hour over traditional seat-based metrics. Takeaway services occupy a strategic position, combining elements of the dine-in experience with the convenience of delivery. They appeal to customers who value food quality and speed while maintaining direct relationships with restaurants, avoiding third-party platform commissions.

The evolution of dine-in services focuses on delivering differentiated experiences. Ambiance, service quality, and social interaction are key factors that distinguish dine-in from delivery and takeaway formats. This compels operators to justify premium positioning through intangible value creation rather than relying solely on food quality. Updated food safety guidelines from the Food Standards Agency ensure consistent quality across all service formats. These guidelines also establish compliance frameworks that favor operators with robust operational systems. Technology is driving the adoption of hybrid service models, enabling restaurants to optimize kitchen utilization across dine-in, takeaway, and delivery channels. Tools such as POS systems and inventory management solutions facilitate real-time resource allocation, guided by demand patterns and profitability analysis.

Geography Analysis

Regional economic conditions, demographic composition, and cultural preferences significantly influence the performance of full-service restaurants across the UK. In 2024, Northern England leads with a +6.2% growth in hospitality spending, surpassing the South's +4.8% increase. This growth is attributed to lower operational costs, the emergence of food tourism destinations, and a demographic shift favoring authentic dining experiences, as reported by UK Hospitality. Cities such as Liverpool, Chester, and Sheffield, each experiencing a +2.4% growth in new restaurant sites, reflect a regional economic recovery that supports restaurant expansion beyond the traditional London-centric investment focus. The British Institute of Innkeeping highlights that Northern hospitality businesses exhibit greater resilience and growth potential compared to their Southern counterparts, who face challenges like higher commercial rents and operational cost pressures.

London retains its status as the UK's leading restaurant destination, with Deloitte's hotel investment surveys identifying the capital and Edinburgh as top locations for hospitality capital deployment. However, London faces unique challenges, including rising commercial rents, regulatory complexities, and intense competition. These factors create barriers for independent operators while favoring chain concepts with established operational systems. According to Food Standards Agency regional data, cuisine preferences and food safety compliance vary geographically. Metropolitan areas lead in adopting international cuisines, while rural and Northern regions show stronger preferences for traditional British fare. Scotland stands out with its integration of whisky and food tourism, offering premium positioning opportunities for restaurants that emphasize local heritage and authentic experiences.

Wales and Northern Ireland present emerging opportunities for restaurant expansion, supported by government initiatives aimed at developing the hospitality sector and increasing recognition of food tourism. The VisitBritain "Food is GREAT" campaign, in partnership with DEFRA, enhances international awareness of British culinary diversity, promoting regional specialties and encouraging operators to prioritize local sourcing and cultural authenticity. Regional economic development programs further support hospitality businesses, creating favorable conditions for restaurant growth in areas previously underserved by full-service dining options.

Competitive Landscape

The competitive landscape of the United Kingdom Full Service Restaurants market is characterized by moderate fragmentation, creating both intense competition and consolidation opportunities as operators vie across various dimensions such as cuisine authenticity, service quality, technological sophistication, and operational efficiency. Successful players differentiate themselves through vertical integration, robust technology adoption, and sustainability commitments, leveraging economies of scale while maintaining sensitivity to local market preferences, an advantage that independent operators find challenging to replicate consistently. This strategic balance enables market leaders to thrive amid diverse consumer demands.

Emerging disruptors are reshaping traditional competitive boundaries by introducing delivery-optimized formats, ghost kitchens, and technology-enabled service models that reduce reliance on labor while maintaining quality standards akin to full service. The sector’s regulatory environment, governed by Food Standards Agency guidelines, raises entry barriers favoring established operators with robust compliance systems, thereby protecting market quality and consumer safety. Concurrently, the rise of hybrid service models that integrate physical and digital customer touchpoints presents growth potential, especially when combined with innovation in plant-based cuisine and regional market expansion.

Technology adoption in the UK full service restaurants sector is evolving rapidly, with operators increasingly utilizing artificial intelligence for operational optimization. Leading competitors leverage data analytics for enhanced customer relationship management and inventory control, translating into operational excellence and sustainable competitive advantages across multiple segments. For instance, innovative brands are deploying AI-driven personalized marketing and seamless online ordering systems to enrich guest experiences. This integration of technological advancements with strategic market positioning underpins resilience and fuels growth in the competitive landscape.

United Kingdom Full Service Restaurants Industry Leaders

-

Mitchells & Butlers PLC

-

The Restaurant Group PLC

-

The Azzurri Group

-

Whitbread PLC

-

Greene King Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Wagamama officially opened at Preston's new Animate leisure complex. At Wagamama Preston, customers experienced the brand's latest summer menu, introduced in May. Key offerings included pho noodle soups featuring a clear yuzu broth and konjac noodles, available with chicken thigh, hoki fish, or king oyster mushroom. The menu also included fresh salads, such as sweet chilli chicken or tofu options, and a pad Thai-inspired salad.

- July 2025: Marston’s, a prominent local pub group, introduced Woodie’s, a new family-oriented pub concept. Each renovated venue included designated family-friendly areas, such as Woodie’s Den, a woodland-themed space designed for children to engage in creative activities like games, crafts, and special events, including discos, karaoke, and quizzes. These areas also featured Marston’s proprietary event system, allowing content to be streamed directly to integrated TVs.

- September 2024: PizzaExpress opened a new restaurant at The ICC in Birmingham, which marked the first location outside London to include a record store. This development followed the earlier opening of three stores in London that year. The record store offered vinyl and CDs from artists under the brand’s PX Records label. Customers had the opportunity to purchase records from UK soul group Mamas Gun, keyboardist Matt Johnson (Jamiroquai), and acclaimed British singer-songwriter Jack Garratt, all of whom recorded at PizzaExpress Live's iconic venues.

United Kingdom Full Service Restaurants Market Report Scope

Asian, European, Latin American, Middle Eastern, North American are covered as segments by Cuisine. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Asian |

| European |

| Latin American |

| Middle Eastern |

| North American |

| Other FSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Sandalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| By Cuisine | Asian |

| European | |

| Latin American | |

| Middle Eastern | |

| North American | |

| Other FSR Cuisines | |

| By Outlet | Chained Outlets |

| Independent Outlets | |

| By Locations | Leisure |

| Lodging | |

| Retail | |

| Sandalone | |

| Travel | |

| By Service Type | Dine-in |

| Takeaway | |

| Delivery |

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms