Automotive Chromium Finishing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.23 Billion |

| Market Size (2030) | USD 5.28 Billion |

| Growth Rate (2025 - 2030) | 4.53% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Chromium Finishing Market Analysis by Mordor Intelligence

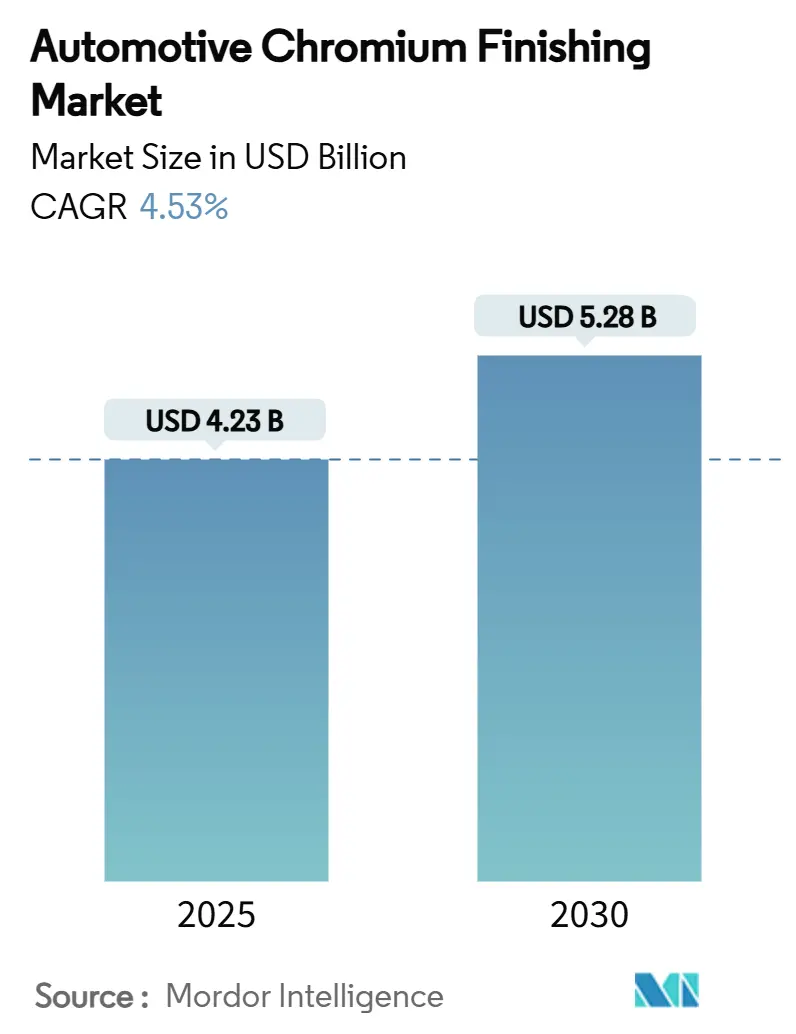

The automotive chromium finishing market size stood at USD 4.23 billion in 2025 and is forecast to touch USD 5.28 billion in 2030, advancing at a 4.53% CAGR over the period 2025-2030. Robust vehicle output recovery, rising electric-vehicle (EV) production, and mandatory shifts toward trivalent chromium systems collectively propel this steady expansion. Automakers continue to specify premium brightwork on exteriors and interiors because chrome remains the most powerful visual cue of craftsmanship and brand identity. Parallel adoption of physical vapor deposition (PVD) allows manufacturers to meet tightening regulations while retaining the signature mirror-like appearance that consumers associate with luxury. Growth headwinds include chromium price swings, capital-intensive equipment upgrades, and the accelerated regulatory timeline in California and the European Union.

Key Report Takeaways

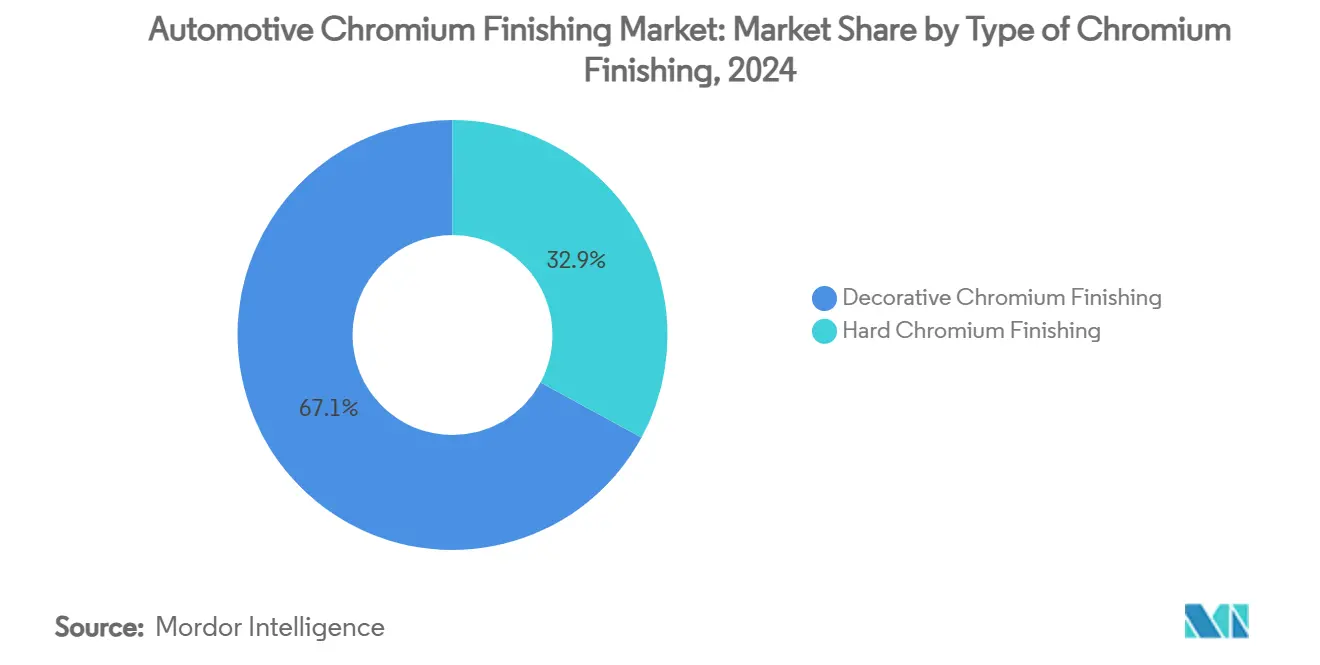

- By chrome finishing type, decorative chromium held 67.13% of automotive chromium finishing market share in 2024. Hard chromium is projected to grow at a 4.95% CAGR to 2030.

- By application, automotive exteriors accounted for a 46.17% share of the automotive chromium finishing market size in 2024, and will show the fastest expansion at 5.18% CAGR through 2030.

- By substrate material, plastics captured 46.81% of the automotive chromium finishing market size in 2024, whereas aluminum substrates register the highest 6.14% CAGR to 2030.

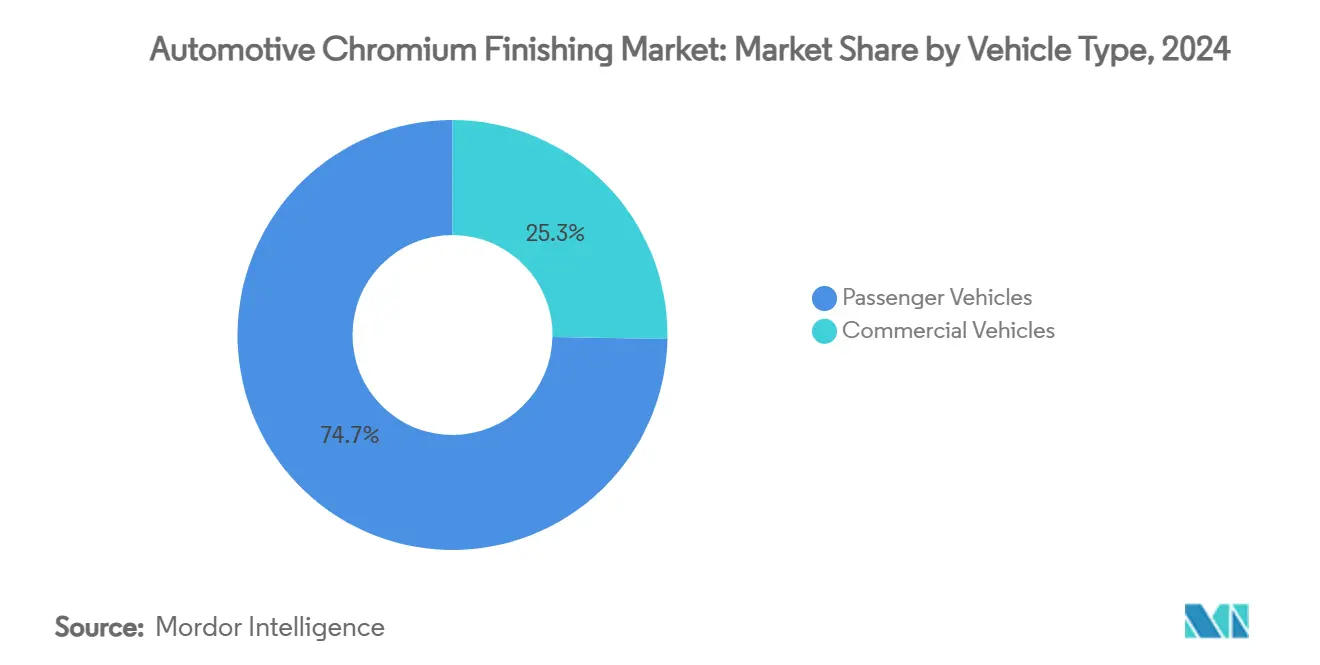

- By vehicle type, passenger cars led with 74.66% of automotive chromium finishing market share in 2024; and will post a 5.34% CAGR over the forecast window.

- By technology, electroplating-hexavalent held 68.24% share in 2024, yet electroplating-trivalent is the quickest-rising sub-segment with a 6.48% CAGR to 2030.

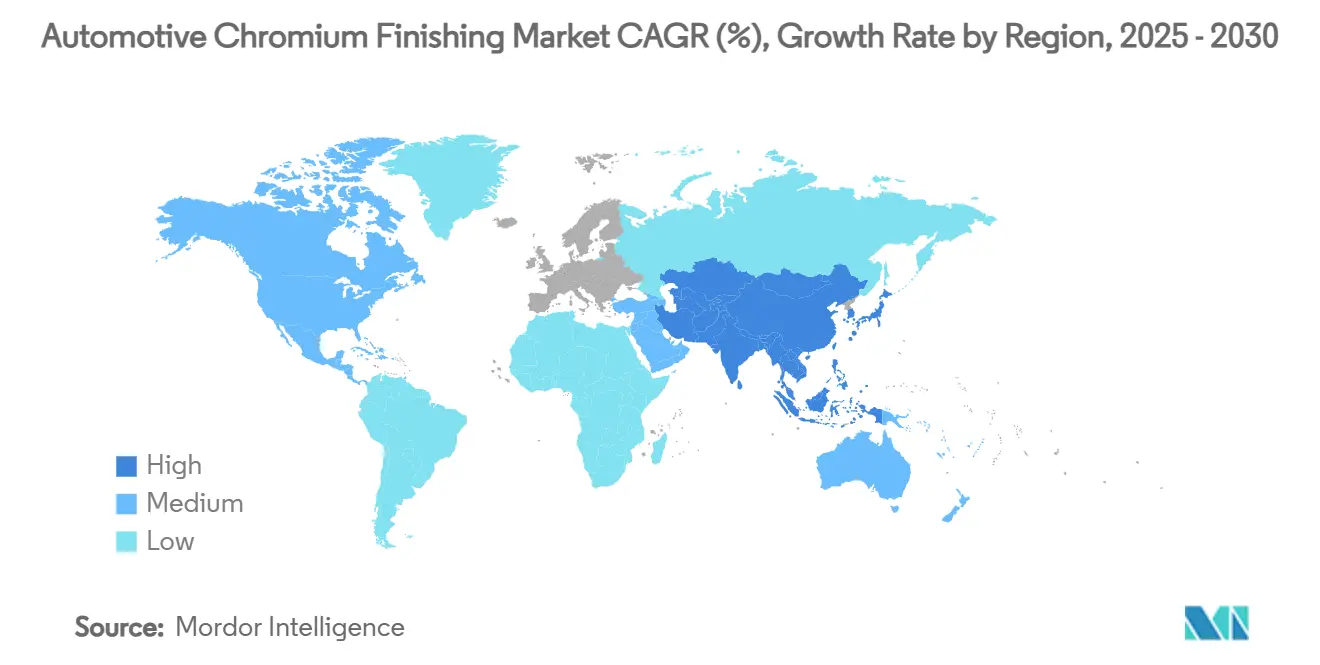

- By geography, Asia-Pacific held 43.86% of the share in 2024, and is expected to witness the fastest growth of 5.83% CAGR through 2030.

Global Automotive Chromium Finishing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium-Grade Exterior Aesthetics | +1.0% | North America and Europe | Medium term (2-4 years) |

| OEM Mandates for Trivalent Cr and PVD | +0.7% | North America and EU | Medium term (2-4 years) |

| Lightweight Plated Plastics in OEM Trims | +0.6% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Post-Pandemic Rebound in Vehicle Builds | +0.4% | Global, led by Asia-Pacific | Short term (≤ 2 years) |

| Illuminated Chrome Trims for EVs | +0.4% | Global EV hubs, early in premium segments | Long term (≥ 4 years) |

| Chrome-Finished Sensor Housings for L3+ ADAS | +0.3% | North America, EU, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Premium-Grade Exterior Aesthetics

Chrome brightwork continues to elevate vehicle perception and allows automakers to justify premium pricing. Luxury brands specify multi-layer trivalent stacks that reduce metal usage but preserve deep reflectivity, and mass-market OEMs add selective chrome in grilles and window surrounds to lift perceived value. Post-pandemic purchasing patterns skewed toward higher-trim models, which lifted per-vehicle chrome content even as regulators restricted legacy electrolytes. Laser-enhanced treatments such as Huf Group’s Signocrom enable brand-specific hues within a chrome layer, demonstrating that innovation is incremental rather than disruptive [1]“Signocrom Process Enables Multicolor Chrome,” Huf Group, huf-group.com. Resilient aesthetic demand therefore underwrites volume stability while the sector undergoes technology change.

OEM Mandates for Trivalent Cr and PVD (PFAS-Free Interiors)

California’s updated Airborne Toxic Control Measure blocked new hexavalent permits from 2024 and forces decorative shops to convert to trivalent by 2030 [2]“Chrome Plating Airborne Toxic Control Measure,” California Air Resources Board, carb.ca.gov. The EU published draft restrictions that target a 17-tonne annual emissions cut, and major vehicle groups have internal cut-off dates between 2025 and 2027. MacDermid Enthone’s PFAS-free trivalent platform delivers corrosion resistance exceeding 120 hours neutral-salt-spray, alleviating previous OEM quality concerns. Suppliers possessing proven trivalent and PVD programs enjoy preferred-supplier status, while legacy shops risk exclusion from global sourcing lists.

Light-Weight Plated Plastics Adoption in OEM Trims

Switching from die-cast zinc or steel to plated ABS or PC-ABS saves several kilograms per vehicle, directly improving fuel economy or EV range. Advanced adhesive-promoter chemistry combined with vacuum flashing achieves adhesion strengths on par with metal substrates. Automakers now integrate complex, single-piece interior bezels that require multiple metal parts, streamlining assembly and cost. DuPont’s Ecoposit CF-800 eliminates hexavalent chromium during etch, addressing both sustainability and worker-safety mandates. Lightweight benefits are amplified in EVs where battery mass dominates vehicle weight budgets, ensuring plastics remain a long-term substrate of choice.

Post-Pandemic Rebound in Global Vehicle Builds

World motor-vehicle production climbed above 95 million units in 2024, surpassing pre-COVID benchmarks and restoring baseline chrome-trim demand [3]“2024 Production Results,” International Organization of Motor Vehicle Manufacturers, oica.net. Asia-Pacific led the rebound as Chinese assembly plants ran at high utilization, while North America and Europe stabilized after chip shortages eased. OEMs prioritized high-spec models to defend margins, which translated into greater chrome finishing per unit. Chrome content is now embedded in baseline specification books rather than relegated to optional appearance packages, giving finishers clearer volume visibility for capacity planning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global Bans on Hexavalent Chromium | -0.9% | California, EU, UK | Short term (≤ 2 years) |

| Chromium Price Volatility and Ferrochrome Risk | -0.5% | Global, cost-sensitive segments | Medium term (2-4 years) |

| Self-healing Clear-Coat Substitutes | -0.4% | North America, Europe, premium models | Long term (≥ 4 years) |

| High CAPEX for Energy-Intensive PVD Lines | -0.3% | Global, impacts smaller suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening Global Bans on Hexavalent Chromium

California and the UK each enacted outright prohibitions on new hexavalent capacity in 2024. The EU’s upcoming REACH amendment would classify many existing decorative baths as Substances of Very High Concern, triggering authorization sunset dates. Stellantis publicized plans to delete all chrome brightwork from future platforms based on worker-safety assessments. While large platers can finance conversions, hundreds of small job shops face closure, curtailing total available capacity and tempering market expansion in the near term.

Chromium Price Volatility and Ferrochrome Supply Risk

Benchmark chromium prices jumped 18% between 2024 and 2025 after power disruptions in South Africa squeezed ferrochrome output. Because material costs comprise roughly 40% of decorative plating inputs, sudden spikes compress margins or force re-quotations. OEM contracts increasingly shift commodity-price clauses to tier-twos that lack hedging tools. Uncertain price trajectories complicate the business case for multi-million-dollar PVD cells, prolonging payback horizons.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Chromium Finishing: Decorative Dominance Drives Aesthetic Premium

Decorative chrome retained 67.13% of automotive chromium finishing market share in 2024 and is slated to rise at a 4.95% CAGR to 2030, underscoring its central role in exterior branding language. The segment directly benefits from continuous grille-size expansion on SUVs and the migration of lighting into brightwork, which increases surface area requirements. Finishing houses deploy pulse-reverse rectification to lower metal thickness while delivering sharper micro-roughness, preserving luster under harsh daylight. Hard chromium, though smaller, services piston rods, bearing races, and battery-cooling plates where tribological performance governs selection. Innovations in micro-cracked hard chrome elevate fatigue life by 25%, widening acceptance in next-generation e-axle shafts.

Decorative suppliers are merging to add in-house design services and color-tune PVD stacks that mimic copper or anodized aluminum at thin layers. This capability attracts EV startups that seek novel signature finishes but lack paint-shop investments. Meanwhile, hard-chrome specialists chase diversification, bundling repair-replate services for remanufactured driveline parts to counter slower ICE volumes. Both niches jointly reinforce the automotive chromium finishing market, though decorative balancing of aesthetics and sustainability keeps it the value engine of the supply chain.

By Application: Exteriors Lead Premium Positioning Strategy

Automotive exteriors represented 46.17% of automotive chromium finishing market size in 2024 and will post a 5.18% CAGR, propelled by SUV grille proliferation and the rise of illuminated fascia bars. Suppliers ship pre-plated large ABS grilles that integrate radar windows, reducing downstream sub-assemblies for OEMs. Coat-within-mold hybrid techniques spray chromium onto warm plastic inserts, eliminating extra tooling and cut steps. Interior brightwork follows with console knobs, air-vent rings, and shifter bezels now mandated even on mainstream crossovers, lifting chrome grams per cabin.

Component-level chrome also expands as battery thermal plates and hair-pin stators demand thin, hard coatings against dielectric coolants. Weight parity with aluminum is critical, so trivalent hard-chrome overlays provide corrosion resistance at 50% lower thickness compared to conventional hard chrome, freeing package space. Collectively, the perseverance of decorative exterior trim and emergence of functional electric-powertrain needs guarantee application diversity within the automotive chromium finishing market.

By Substrate Material: Plastics Dominance Meets Aluminum Innovation

Plastic substrates kept 46.81% share of automotive chromium finishing market size in 2024, delivering unbeatable design freedom. Finishing houses employ low-temperature sputtering so ABS substrates avoid heat-induced warpage, sustaining spec significance. Yet aluminum’s 6.14% CAGR signals its strategic place in battery enclosures, motor housings, and structural strut bars where conductivity and mass savings co-exist. Suppliers like JFE Steel rolled out heat-treatable aluminum sheet that accepts trivalent adhesion layers without chromic acid etch, reducing prep time by 15%.

Steel retains utility in large bumper reinforcements; however, its share slides as OEMs seek kilogram savings ahead of Euro 7 emissions. Composite and glass-fiber substrates emerge in roof rails and spoiler lips, metallized via plasma activation to meet a 720-hour salt-spray target. The wider materials palette rewards applicators that combine flexible racks, multi-chemistry tanks, and automated optical inspection in one cell.

By Vehicle Type: Passenger Vehicles Dominate and Lead Growth

Passenger models consumed 74.66% of automotive chromium finishing market share in 2024 and are projected to expand at the fastest 5.34% CAGR through 2030, with volume anchored in compact SUVs that use chrome headlamp brows and C-pillar spears to convey upscale character. EV sedans add illuminated rocker accents, pushing per-car chrome usage up 8% year on year. Commercial vans, while lower in numbers, embrace hard chromium inside suspension kingpins and power-take-off shafts to extend fleet uptime. As regional legislation promotes zero-emission freight, e-trucks integrate chrome cooling plates that stabilize battery temperature under heavy load, expanding functional demand.

Future growth in commercial EV buses will call for decorative chrome delete in favor of colored PVD bands aligned with city-branding, moderating aesthetic volumes but adding higher-margin specialty coatings. Overall segment interplay indicates passenger vehicles will continue to dictate decorative trends, whereas commercial platforms pull hard-chrome innovation forward.

By Technology: Trivalent Transition Accelerates Despite Hexavalent Dominance

Electroplating-hexavalent still commanded 68.24% of automotive chromium finishing market share in 2024 due to entrenched lines and unmatched color uniformity. The regulatory clock, however, has catalyzed a 6.48% CAGR for trivalent baths. Modern formulations exhibit 0.5-micron deposits that pass CASS corrosion tests, meeting OEM Class-A specs without lead anodes. Tier-ones retrofit existing cells with anode cages and revised filtration instead of greenfield investment, curbing paybacks. PVD, meanwhile, grows double digits off a small base as LEDs in chrome parts mandate optical edge-sharpness only sputtering can deliver.

Some finishers blend chemistries, laying a trivalent strike then sealing with a sputtered clear topcoat to add fingerprint resistance. Future deployments may pair aqueous trivalent lines for high-volume small parts and PVD for oversized trims, preserving scalability while satisfying cosmetic targets. Hexavalent dominance erodes by mid-decade, yet it remains irreplaceable for high-throw deep cavities until additive-based trivalent chemistries advance.

Geography Analysis

Asia-Pacific anchored 43.86% of global demand in 2024 and is forecast to see a 5.83% CAGR through 2030. China’s production above 30 million units supplies local and export programs, ensuring multi-shift loading of decorative ABS plating cells in Guangdong and Jiangsu. Japanese tiers pioneer micro-crack hard chrome for hydraulic rods, funneling innovations downstream to ASEAN contract shops. India’s corridor of paint-and-plating industrial parks near Pune attracts both domestic brands and Western EV newcomers who seek localized trim supply. Public policies blend environmental guardrails with pragmatic conversion grants, so plating plants can adopt trivalent baths without shutdown.

North America remains technology-driven. California mandates accelerate trivalent cut-over, and Canadian suppliers now pre-qualify PFAS-free chemistries to secure Detroit Three sourcing awards. Chrysler parent Stellantis cancelled chrome on future passenger brands, but RAM and Jeep trucks still demand substantial brightwork, creating a split product strategy. The United States also hosts new chrome raw-material investments such as AMG’s approved domestic plant that will offset import dependency. Europe operates under the strictest regulatory lens. Draft REACH revisions threaten blanket SVHC classification for hexavalent Cr decorative uses. German coaters therefore install multi-million-euro PVD cells in concert with energy-recovery modules to meet carbon budgeting. Scandinavian OEMs experiment with chrome-delete styling themes, yet demand persists in traditional premium sedans. Eastern Europe offers cost-competitive plating clusters that feed Germany and France, though access to EU-backed modernization funds requires proven trivalent compliance.

Middle East and Africa’s car build grows from a small base; Turkish suppliers provide chrome grilles to both local assembly and Western European spares. South America stabilizes after chip-shortage slowdowns, and Brazilian finishers shift to trivalent after local regulators aligned with EU norms. Collectively, region-specific regulatory pacing and vehicle-mix evolution shape disparate opportunities in the automotive chromium finishing market.

Competitive Landscape

The automotive chromium finishing market remains moderately fragmented, yet consolidation is accelerating. SRG Global, Atotech, and MacDermid Enthone collectively hold a significant share of the automotive chromium finishing market size. Each company differentiates by turnkey conversion kits and embedded metallurgical labs. Quaker Houghton spent USD 153 million to buy Dipsol in 2024, strengthening trivalent electrolyte portfolios and gaining Asian market entry. Axalta paid USD 285 million for the CoverFlexx Group to add specialty PVD and paint-over-chrome capabilities, demonstrating that scale and surface-engineering breadth define future competitiveness.

Technology roadmaps center on PFAS-free wet processes and large-area sputtering. MacDermid Enthone issued a technical guide in January 2025 affirming that its new PFAS-free trivalent line matches legacy hexavalent ASTM corrosion specs, winning rapid OEM endorsement. Oerlikon invested in 2.5-meter-diameter chambers with AI-controlled thickness mapping, compressing cycle time by 20%.

Smaller regional shops face capital barriers; many seek joint ventures with chemistry suppliers that offer financing bundles. AMG’s US ferrochrome plant signals upstream integration trends that stabilize raw inputs for captive plating networks. Disruptive entrants from the paint sector push high-gloss clear coats as chrome alternatives, but optical parity and luxury cachet still favor genuine metallic layers. Overall, competitive intensity is governed by regulatory readiness, customer proximity, and chemistry-equipment ecosystems rather than price alone.

Automotive Chromium Finishing Industry Leaders

SRG Global

Atotech (MKS Instruments)

MacDermid Enthone Industrial Solutions

AkzoNobel

PPG Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: AMG approved a US chrome manufacturing plant to bolster domestic supply for automotive and industrial demand.

- October 2024: PROTO launched a chrome plating service aimed at the restoration and aftermarket customization community, promising durability and mirror-grade gloss for vintage vehicles.

Global Automotive Chromium Finishing Market Report Scope

| Decorative Chromium Finishing |

| Hard Chromium Finishing |

| Automotive Interiors |

| Automotive Exteriors |

| Automotive Components |

| Steel |

| Aluminum |

| Plastics |

| Other Materials |

| Passenger Vehicles |

| Commercial Vehicles |

| Electroplating – Hexavalent |

| Electroplating – Trivalent |

| Physical Vapour Deposition (PVD) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Type of Chromium Finishing | Decorative Chromium Finishing | |

| Hard Chromium Finishing | ||

| By Application | Automotive Interiors | |

| Automotive Exteriors | ||

| Automotive Components | ||

| By Substrate Material | Steel | |

| Aluminum | ||

| Plastics | ||

| Other Materials | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| By Technology | Electroplating – Hexavalent | |

| Electroplating – Trivalent | ||

| Physical Vapour Deposition (PVD) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the automotive chromium finishing market?

The automotive chromium finishing market size reached USD 4.23 billion in 2025 and is projected to rise to USD 5.28 billion by 2030.

Which region leads the automotive chromium finishing market?

Asia-Pacific holds 43.86% share and posts the fastest 5.83% CAGR thanks to large-scale vehicle production and integrated supply chains.

Why are automakers shifting toward trivalent chromium?

Trivalent electrolytes meet stringent California and EU regulations, eliminate hexavalent carcinogenic risks, and now match legacy corrosion performance.

Which substrate is growing fastest for chrome finishing?

Aluminum parts register a 6.14% CAGR as EV battery housings and motor casings need lightweight, thermally conductive, corrosion-protected surfaces.

Page last updated on: