Car Door Latch Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

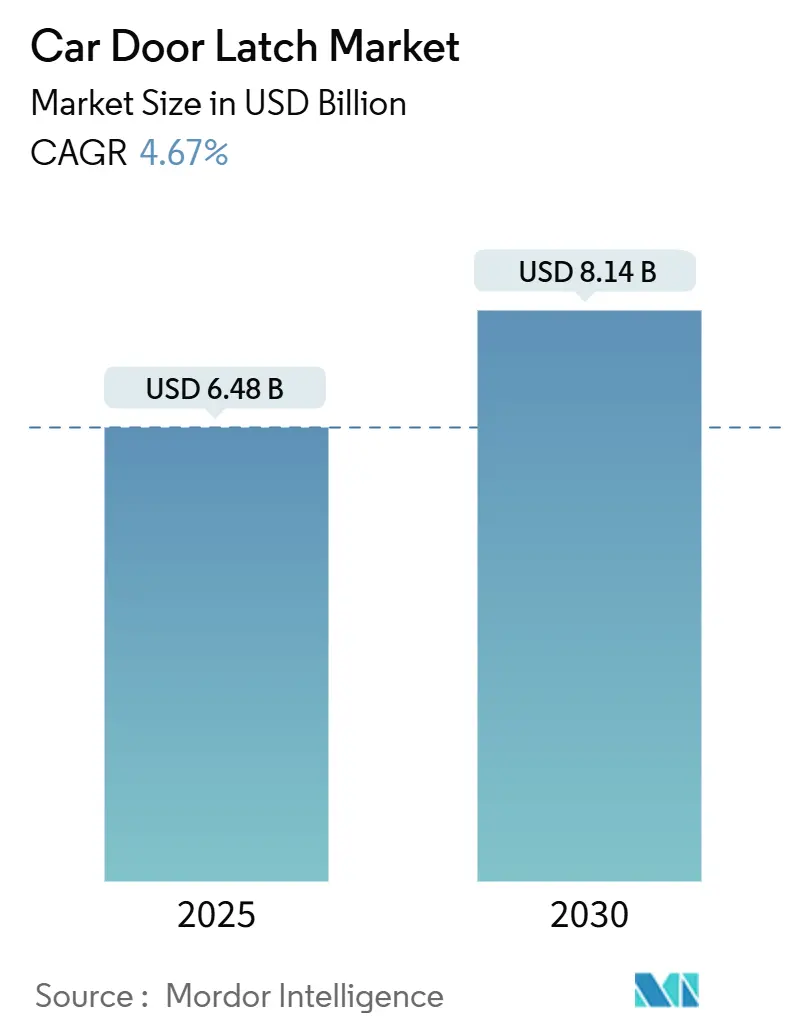

| Market Size (2025) | USD 6.48 Billion |

| Market Size (2030) | USD 8.14 Billion |

| Growth Rate (2025 - 2030) | 4.67% CAGR |

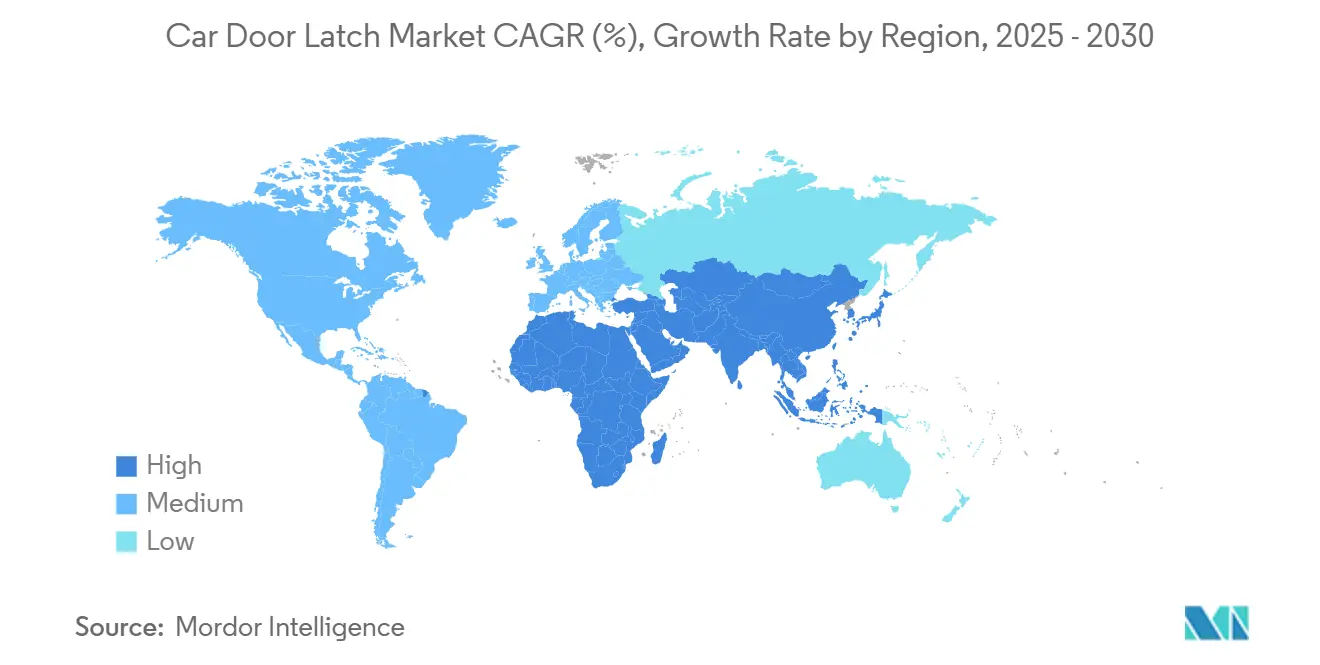

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Car Door Latch Market Analysis by Mordor Intelligence

The global car door latch market size is USD 6.48 billion in 2025 and is forecast to reach USD 8.14 billion by 2030 at a at 4.67% CAGR during the forecast period (2025-2030). Growth accelerators include rising electronic latch fitment rates across electric and autonomous platforms, intensifying safety mandates, and OEM appetite for software-defined access systems that unlock predictive maintenance revenues. Electronic latches led the car door latch market share in 2024 as automakers pivot to fully networked closures that integrate seamlessly with keyless entry and biometric authentication. Asia-Pacific leads global demand owing to sustained vehicle production expansions in China and India, while North America sees heightened aftermarket activity following large recall campaigns. Although raw-material cost volatility and cybersecurity validation requirements temper near-term margins, suppliers with vertically integrated actuator and control-module capabilities are positioned to outpace the wider car door latch market through value-added service models and regional supply-chain diversification.

Key Report Takeaways

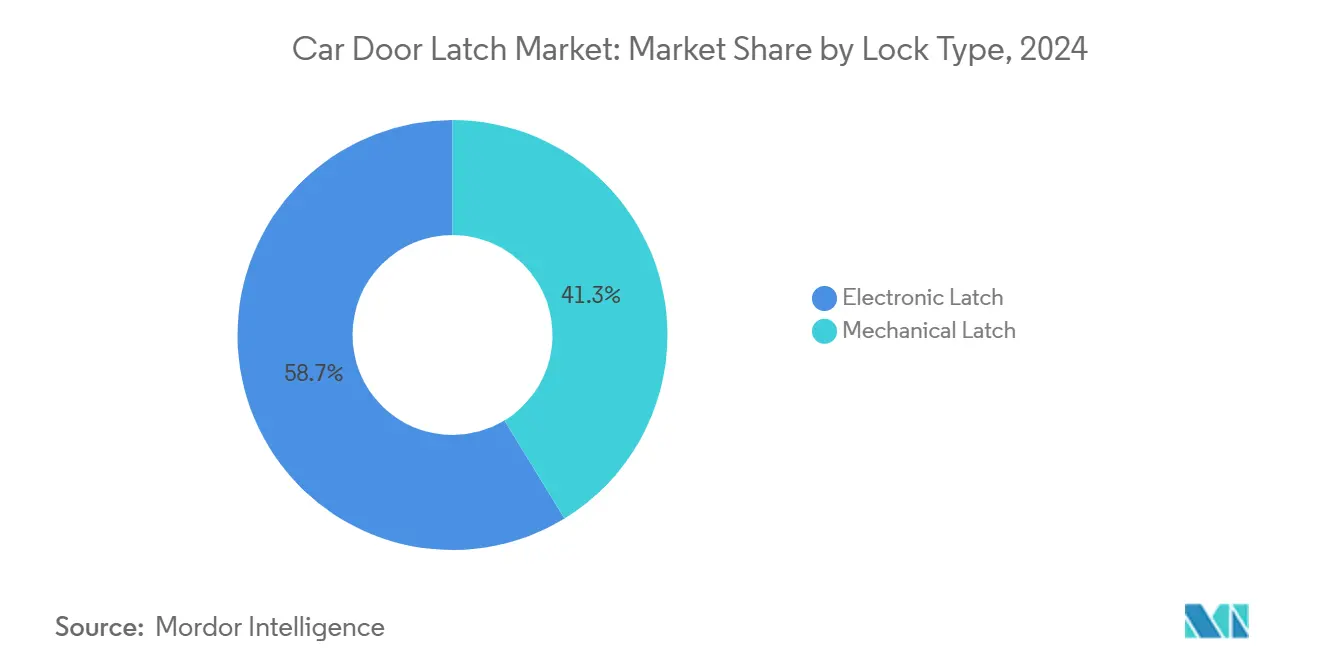

- By lock type, electronic latches led with 58.71% revenue share of the car door latch market in 2024 and are projected to expand at a 6.64% CAGR during the forecast period (2025-2030).

- By vehicle type, SUV/MUV captured 63.77% of the car door latch market size in 2024 and is projected to grow at a 4.94% CAGR during the forecast period (2025-2030).

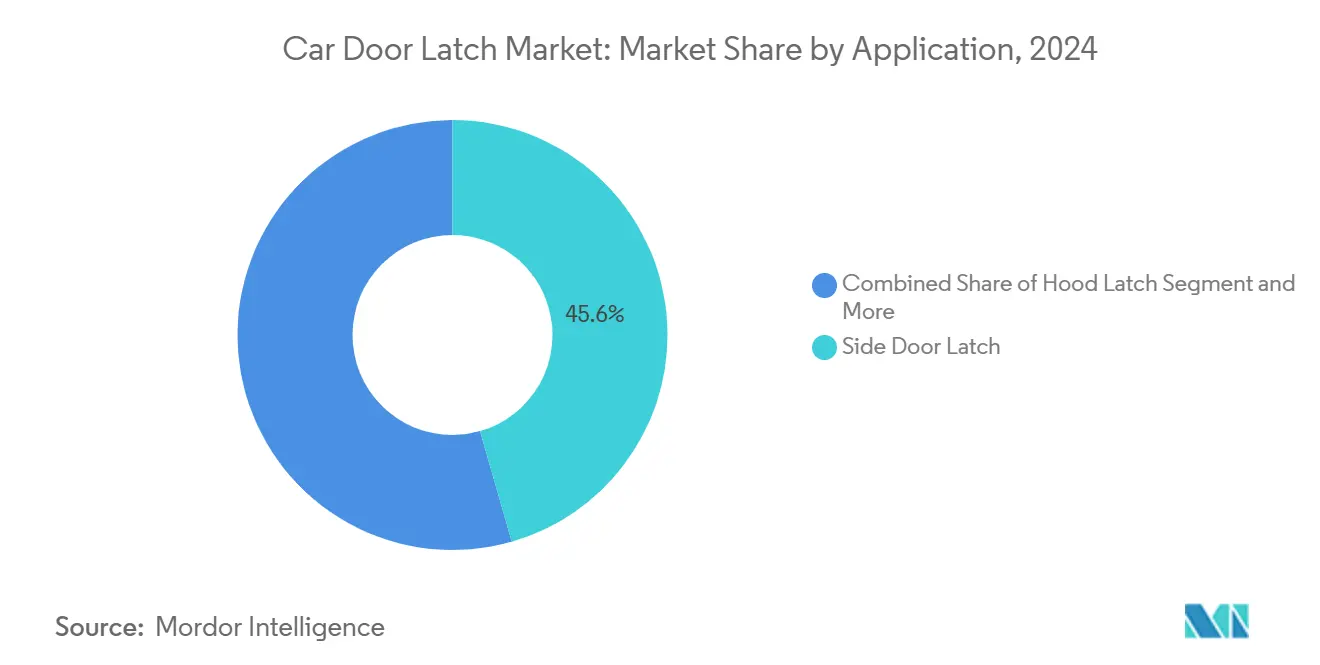

- By application, side door latches accounted for 45.55% of the car door latch market size in 2024, whereas tailgate latches are projected to advance at a 5.29% CAGR during the forecast period (2025-2030).

- By distribution channel, the OEM segment held 71.87% share of the car door latch market in 2024, yet the aftermarket is projected to record the highest projected CAGR at 6.44% during the forecast period (2025-2030).

- By geography, Asia-Pacific captured 46.57%share of the car door latch market in 2024 and is projected to be the fastest growing region at 5.33% CAGR during the forecast period (2025-2030).

Market Trends and Insights

Drivers Impact Analysis of Car Door Latch Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electronic and Smart Latches | +1.2% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Rising Vehicle Production | +0.9% | Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Stringent Vehicle-Safety Regulations | +0.7% | Global, with Europe and North America driving compliance | Short term (≤ 2 years) |

| Aftermarket Replacement Demand | +0.5% | North America and Europe primarily | Short term (≤ 2 years) |

| Standardized Global Platform Doors | +0.4% | Global, with OEM platform consolidation | Medium term (2-4 years) |

| OTA-Driven Predictive-Maintenance Models | +0.3% | North America, Europe, premium segments in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Demand for Electronic and Smart Latches for EVs/Autonomous Vehicles

Automakers are embedding fully electronic latching mechanisms to harmonize with digital key, over-the-air update, and autonomous-parking requirements. Tesla’s redesign of its door system illustrates the delicate balance between sleek flush handles and emergency egress mandates, underscoring the supplier's need for dual-path mechanical backups[1]Sean O’Kane, “Tesla Is Redesigning Its Door Handles Following Safety Probe,” TechCrunch, techcrunch.com. Premium OEMs favor compact 48 V-ready actuators that lower current draw while supporting swift unlatching times compatible with automated valet features. The trend rewards suppliers able to miniaturize motor-zone controllers and certify software to the latest functional-safety standards. As EV unit volumes accelerate, economies of scale are driving electronic latch average selling prices down, widening addressable penetration in mid-price passenger cars.

Rising Global Vehicle Production in Emerging Markets

Asia-Pacific assembly plants are scaling output across multi-energy platforms, prompting Tier-1 latch makers to add localized capacity. India’s component sector forecasts robust revenue growth for FY 2025-26, reflecting pent-up demand and import substitution initiatives that favor competitively priced latch modules. Inteva Products’ expansion in Pune aims at window-regulator and latch units annually by 2026, confirming that regionalization is critical to margin preservation amid freight-cost inflation. Modular kit strategies that adapt to multiple door architectures without tooling redesign shorten OEM launch cycles, translating to incremental volumes that add 0.9 percentage points to the compound growth of the car door latch market.

Stringent Vehicle-Safety Regulations (FMVSS 206, UNECE R-11, etc.)

Global rulebooks tighten minimum load-bearing thresholds, anti-intrusion metrics, and cybersecurity clauses, forcing rapid technology refreshes. Europe’s UNECE R-155 and R-156 demand secure firmware-over-the-air workflows, compelling latch makers to invest in encryption protocols and incident-response playbooks. North American FMVSS updates now reference electronic latch latency during crash events, raising validation mileage and test-bench hours. The financial burden favors top-tier vendors with accredited labs, while smaller firms risk exclusion from global sourcing panels. These mandates enhance replacement cycles for legacy fleets and underpin a positive CAGR contribution inside the car door latch market.

Growing Aftermarket Replacement Demand Driven by Large-Scale Recall Campaigns

Field-failure spikes across electronically actuated closures are triggering unprecedented recall volumes. Ford’s 2025 Mustang Mach-E campaign affects over 197,000 vehicles, elevating dealer-parts throughput and independent garage demand[2]Lurah Lowery, “Ford Recalls Nearly 200,000 Mustang Mach-Es Over Potentially Trapping Passengers,” Repairer Driven News, repairerdrivennews.com. Recalls deliver short-cycle revenue bursts to suppliers as OEMs place expedited orders for redesigned latch sub-assemblies. However, heightened media scrutiny reinforces the imperative for zero-defect process capability. For suppliers with established remanufacturing networks, warranty parts also provide cores for circular-economy initiatives.

Restraints Impact Analysis of Car Door Latch Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost and Integration Complexity | -0.6% | Global, particularly affecting cost-sensitive segments | Short term (≤ 2 years) |

| Price Volatility | -0.4% | Global, with supply chain concentration in APAC | Medium term (2-4 years) |

| OEM-Controlled Vehicle Data | -0.3% | North America and Europe primarily | Long term (≥ 4 years) |

| Cyber-Security Concerns | -0.2% | Global, with stricter requirements in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost and Integration Complexity of Electronic Latches

Electronic latch systems bundle micro-actuators, hall-effect sensors, and controller firmware, elevating bill-of-materials by USD 50–100 per vehicle relative to mechanical units. Development programs now span electromagnetic-compatibility, cyber-security penetration, and fail-safe validation, stretching timelines by up to 18 months. Shape-memory-alloy actuators and three-position solenoids introduce single-source dependencies that magnify sourcing risk should geopolitical or capacity disruptions arise. Adoption, therefore, lags in cost-sensitive A- and B-segment cars despite regulatory pushes, shaving 0.6 percentage points off aggregate car door latch market growth in the near term.

Price Volatility of Steel, Engineered Plastics and Semiconductors

Steel dominates latch assemblies, while engineered plastics hold a significant share. Semiconductor foundry limitations continue to constrain the availability of microcontrollers. Suppliers are increasingly adopting hedging strategies or renegotiating terms due to fluctuations in raw material costs, especially steel and silicon. Original Equipment Manufacturers (OEMs) frequently resist pricing models linked to market indices, shifting financial risk onto suppliers. This shift encourages stockpiling, raising working capital requirements. Such persistent volatility pressures profitability, prompting some smaller suppliers to exit the market and slightly dampening the industry's overall growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Car Door Latch Market Segment Analysis

By Lock Type:

Electronic Dominance AcceleratesElectronic latches secured a commanding 58.71% of the car door latch market share in 2024 and are forecast to widen their lead at a 6.64% CAGR during the forecast period (2025-2030). This leadership stems from OEMs embedding digital keys, proximity-based unlocking, and autonomous-door actuation that mesh seamlessly with software-defined vehicle ecosystems. Mechanical designs still populate entry-level cars where rugged simplicity offsets feature scarcity, yet even these platforms increasingly adopt hybrid electro-mechanical back-ups to satisfy emerging safety mandates.

Competitive intensity in the electronic cohort centers on actuator miniaturization and current-draw optimization to align with 48 V architectures. Vendors are also differentiating through firmware-level diagnostics that feed predictive-maintenance dashboards. Conversely, mechanical suppliers refine engineered-plastic housings and corrosion-resistant coatings to cut mass and extend service life. The dual-track innovation landscape keeps overall lock-type diversity vibrant, reinforcing the broad revenue canvas driving the car door latch market.

By Vehicle Type:

SUVs/MUVs Gain MomentumSUVs and MUVs held 63.77% of the car door latch market revenue in 2024. Shoppers keep gravitating toward these larger models, and automakers are equipping them with electronic latches, soft-close doors, and power tailgates. That mix pushes SUVs and MUVs to the top of the growth chart, with latch sales for this group rising at a 4.94% CAGR during the forecast period (2025-2030). Passenger cars continue to need high-spec latches for premium sedans and hatchbacks, but growth there is flatter. Commercial platforms, by contrast, call for rugged hardware that survives frequent door cycles and harsh fleet duty.

Hatchbacks and sedans still play an important role in the car door latch market, especially in premium models where advanced electronic latches and safety features are in demand. Hatchbacks generally lean toward cost-effective mechanical or basic electronic systems, while sedans often incorporate more sophisticated solutions like central locking and child safety locks. On the other hand, SUVs and MUVs clearly lead the way, not just in market share but also in growth, owing to their higher latch count per vehicle and the growing popularity of features like hands-free tailgate operation. This shift reflects a broader consumer trend toward larger, feature-rich vehicles that prioritize convenience and safety.

By Application:

Tailgate Latches SurgeSide-door latches commanded 45.55% of the car door latch market's revenue in 2024 as every vehicle mandates at least two such mechanisms, and electronic-child-lock regulations heighten complexity. Tailgate latches are expected to accelerate at a 5.29% CAGR during the forecast period (2025-2030), mirroring global demand for crossovers, and SUVs with powered liftgates. Modern tailgate systems now incorporate pinch-sensor arrays and soft-close motors, raising per-unit ASPs and attracting specialist suppliers.

Hood and back-seat latches retain steady volume anchored in regulatory requirements for secondary restrainers and ISOFIX-compatible child-seat anchors. Sliding-door applications in premium minivans and urban-delivery vans present niche but profitable opportunities due to high actuator content and demanding duty cycles. Suppliers employing condition-monitoring algorithms to pre-empt latch-pin wear are well positioned to capture share as application-specific digital services proliferate within the broader car door latch market.

By Distribution Channel:

Aftermarket AcceleratesThe OEM channel captured 71.87% of car door latch market's 2024 sales as door latches integrate directly into body-in-white build sequences and must meet PPAP validation alongside adjacent sheet-metal. Nonetheless, aftermarket demand is slated for a robust 6.44% CAGR during the forecast period (2025-2030), because widespread recalls and extended vehicle lifespans inflate replacement volumes. Electronic latch complexity also raises failure incidence rates after warranty expiration, funneling revenue to independent distributors stocking refurbished modules.

Yet data-access constraints impede some aftermarket gains, prompting entrepreneurial suppliers to develop CAN-bus-agnostic diagnostic dongles and universal latch harnesses. E-commerce platforms streamline part identification, enabling do-it-yourself owners to source genuine or pattern replacements quickly. As repairability emerges as a brand loyalty factor, OEMs weigh parts-pricing strategies that balance profit margins with consumer satisfaction, underscoring the dynamic channel interplay shaping the car door latch market.

Geography Analysis

APAC Car Door Latch Market

Asia-Pacific dominated the landscape with a 46.57% 2024 revenue share of the car door latch market and is set to compound at 5.33% through 2030. The region’s output boom stems from China’s electric-vehicle surge and India’s quest for higher localization levels. Inteva Products’ Pune facility, designed for latch and window-regulator units annually by 2026, typifies how global Tier-1s co-locate with expanding OEM clusters. Government incentives that reward advanced-safety content further encourage the adoption of electronic latches in domestic models, reinforcing Asia-Pacific’s role as the growth engine of the car door latch market.

North America Car Door Latch Market

North America shows a more mature posture but still benefits from regulatory-driven aftermarket pulls, exemplified by Ford’s 197,000-unit Mustang Mach-E recall that flooded service bays with replacement latch orders. Steadfast investment in cyber-security compliance and over-the-air readiness sustains higher average selling prices, partially offsetting slower 2.89% regional CAGR. Meanwhile, Mexico’s manufacturing corridor captures incremental programs diverted from Asia to mitigate geopolitical risk, injecting fresh momentum into North American supply chains.

EMEA, Russia and Oceania Car Door Latch Market

Europe faces saturated new-car volumes, yet adoption of UNECE-mandated cyber-secure closures supports a 3.63% CAGR. Suppliers leverage local R&D outposts to navigate stringent homologation protocols, though many shift series production to cost-advantaged Central-Eastern plants. Smaller markets in Western Asia and Africa realize faster unit growth, albeit from modest bases, as CKD assembly networks multiply. Conversely, Russia’s subdued economic outlook and Oceania’s limited vehicle output restrict latch-demand upticks, underlining divergent geographic tapestries within the car door latch market.

Competitive Landscape

The car door latch market exhibits moderate concentration with fragmented supplier base creating opportunities for technological differentiation and regional expansion. While dominant in high-volume mechanical assemblies, these incumbents face vigorous competition from electronics-focused specialists providing sealed micro-motor actuators and embedded security firmware. Intellectual-property filings around shape-memory-alloy pins, three-position pawls, and network-firewall algorithms have surged, with TLX Technologies notably advancing hybrid solenoid designs optimized for low-temperature actuation.

Strategic moves in 2025 emphasize vertical integration and near-shoring. Magna is expanding actuator-coil winding in Mexico to hedge semiconductor shortages, whereas Kiekert pilots a cloud-enabled predictive-maintenance suite with a European fleet-management partner. Brose partnered with an Asian EMS provider to localize PCB assembly, reflecting OEM mandates for regional sourcing parity. As over-the-air monetization gains prominence, suppliers that align hardware, firmware, and data analytics offerings strengthen lock-in across vehicle lifecycles.

Emergent disruptors exploit white-space around software-defined latching, bundling API-exposed door modules that integrate with mobility-as-a-service platforms. These newcomers often license core hardware from established stampers while differentiating via cloud-service layers. Established players respond by opening developer portals and offering reference-design kits to preserve platform relevance. Such cross-disciplinary contests, spanning mechanical heft and digital deftness, will shape competitive outcomes through the forecast period in the car door latch market.

Car Door Latch Industry Leaders

Kiekert AG

Aisin Seiki Co. Ltd.

Magna International Inc.

STRATTEC Security Corp.

Brose Fahrzeugteile GmbH

- *Disclaimer: Major Players sorted in no particular order

Car Door Latch Market Companies Covered in this Report

- Kiekert AG

- Aisin Seiki Co. Ltd.

- Magna International Inc.

- STRATTEC Security Corp.

- Brose Fahrzeugteile GmbH

- Mitsui Mining & Smelting Co.

- U-Shin Ltd.

- Minda VAST Access Systems

- Inteva Products LLC

- Valeo SA

- Robert Bosch GmbH

- Denso Corporation

- Lear Corporation

- Grupo Antolin

- Shivani Locks Pvt Ltd.

- Huf Hülsbeck & Fürst GmbH

- Igarashi Motors India Ltd.

- D-La Porte (GmbH and Co.)

- Kongsberg Automotive ASA

- Dorman Products Inc.

- Guala Closures Group (Automotive)

Recent Industry Developments in Car Door Latch Market

- September 2025: Tesla announced plans to redesign emergency-door mechanisms by merging manual and electronic releases to resolve post-crash exit concerns.

- June 2025: Ford recalled 197,432 Mustang Mach-E vehicles (model years 2021-2025) owing to latch failures that could trap occupants, as confirmed by the National Highway Traffic Safety Administration.

Global Car Door Latch Market Report Scope

Segmentation Overview

| Electronic Latch |

| Mechanical Latch |

| Hatchback |

| Sedan |

| SUV/MUV |

| Side Door Latch |

| Hood Latch |

| Tailgate Latch |

| Back Seat Latch |

| Sliding Door Latch |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Lock Type | Electronic Latch | |

| Mechanical Latch | ||

| By Vehicle Type | Hatchback | |

| Sedan | ||

| SUV/MUV | ||

| By Application | Side Door Latch | |

| Hood Latch | ||

| Tailgate Latch | ||

| Back Seat Latch | ||

| Sliding Door Latch | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the car door latch market and its forecast growth?

The market is valued at USD 6.48 billion in 2025 and is projected to reach USD 8.14 billion by 2030, advancing at a 4.67% CAGR.

Which lock type dominates global demand?

Electronic latches hold 58.71% of 2024 revenue and are expanding at a 6.64% CAGR as OEMs migrate toward fully digital closures.

Which vehicle category is the fastest-growing user of advanced latches?

Light commercial vehicles are forecast to grow at 4.94% CAGR through 2030 due to e-commerce logistics expansion and stricter safety rules.

Why is Asia-Pacific the largest regional market?

High vehicle-production volumes in China and India, coupled with increasing electronic-latch content in domestic EVs, give Asia-Pacific a 46.57% share.

How are recalls influencing aftermarket demand?

Large campaigns, such as Ford’s 197,000-unit Mustang Mach-E recall, drive brisk replacement-parts sales and contribute to a 6.44% aftermarket CAGR.

What competitive strategies are suppliers adopting?

Firms focus on actuator miniaturization, cyber-secure firmware, and regionalized production to meet OEM cost and compliance targets.

Page last updated on: