Cable Assembly Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 197.75 Billion |

| Market Size (2031) | USD 256.48 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

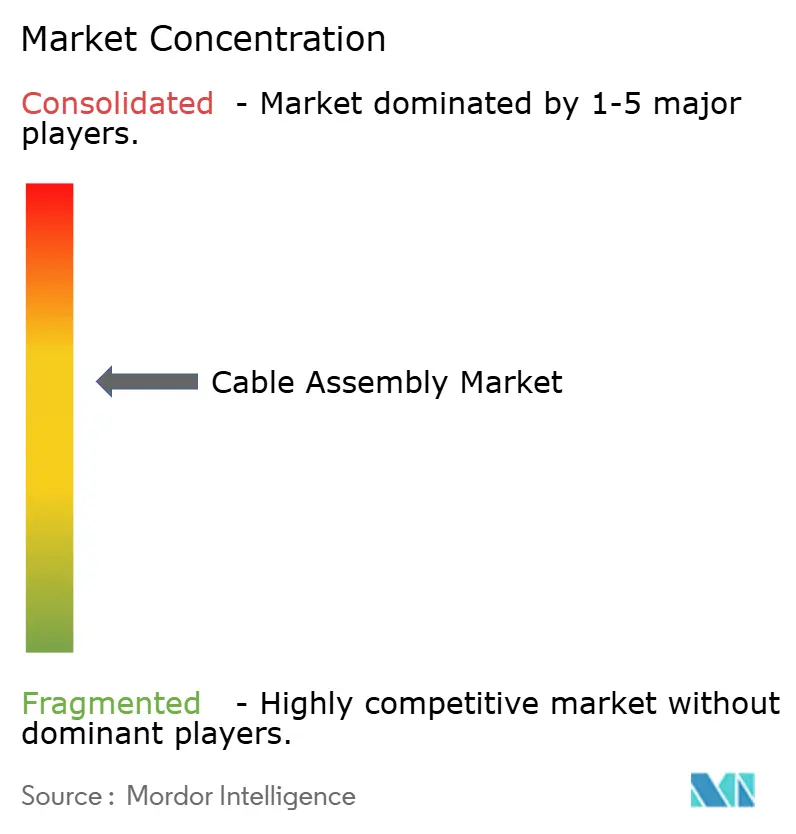

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cable Assembly Market Analysis by Mordor Intelligence

The cable assembly market size is projected to be USD 186.36 billion in 2025, USD 197.75 billion in 2026, and reach USD 256.48 billion by 2031, growing at a CAGR of 5.34% from 2026 to 2031. Robust demand stems from hyperscale data-center refresh cycles that favor 800 Gbps and 1.6 Tbps optics, the electrification of 800-volt vehicle platforms, and 5 G fiber-to-the-home rollouts that increasingly specify pre-terminated drop cables. Suppliers that combine automated polishing, vision-guided crimping, and vertical integration into connectors are compressing lead times below the 8–12-week industry median, while regional players retain share through design-for-manufacturing partnerships and just-in-time kitting. At the same time, recurring copper-price spikes and tightening RoHS or REACH mandates are steering customers toward halogen-free, low-smoke-zero-halogen constructions and aluminum-conductor alternatives. These crosscurrents explain why the cable assembly market continues to favor scale, automation, and materials agility over pure labor-arbitrage advantages.

Key Report Takeaways

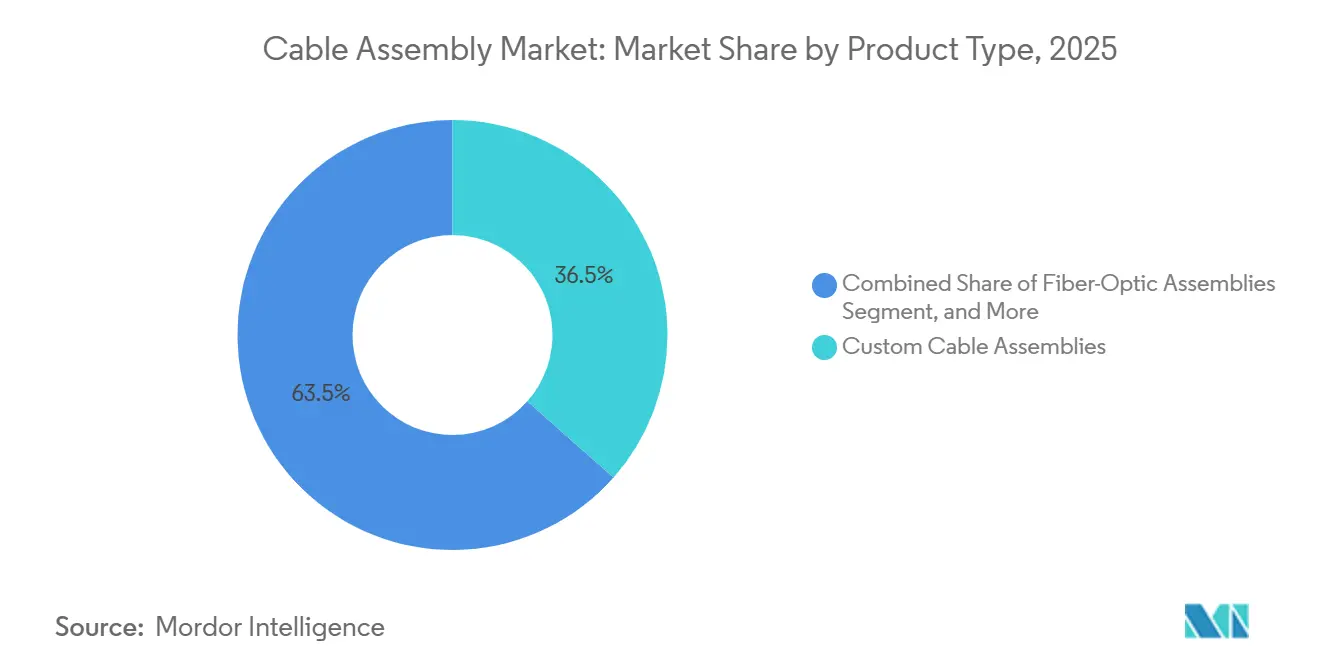

- By product category, fiber-optic assemblies led with 36.54% revenue share in 2025 and are forecast to expand at a 6.06% CAGR to 2031.

- By cable type, fiber-optic configurations commanded 37.72% of the cable assembly market share in 2025, while the same category is projected to grow at a 6.11% CAGR through 2031.

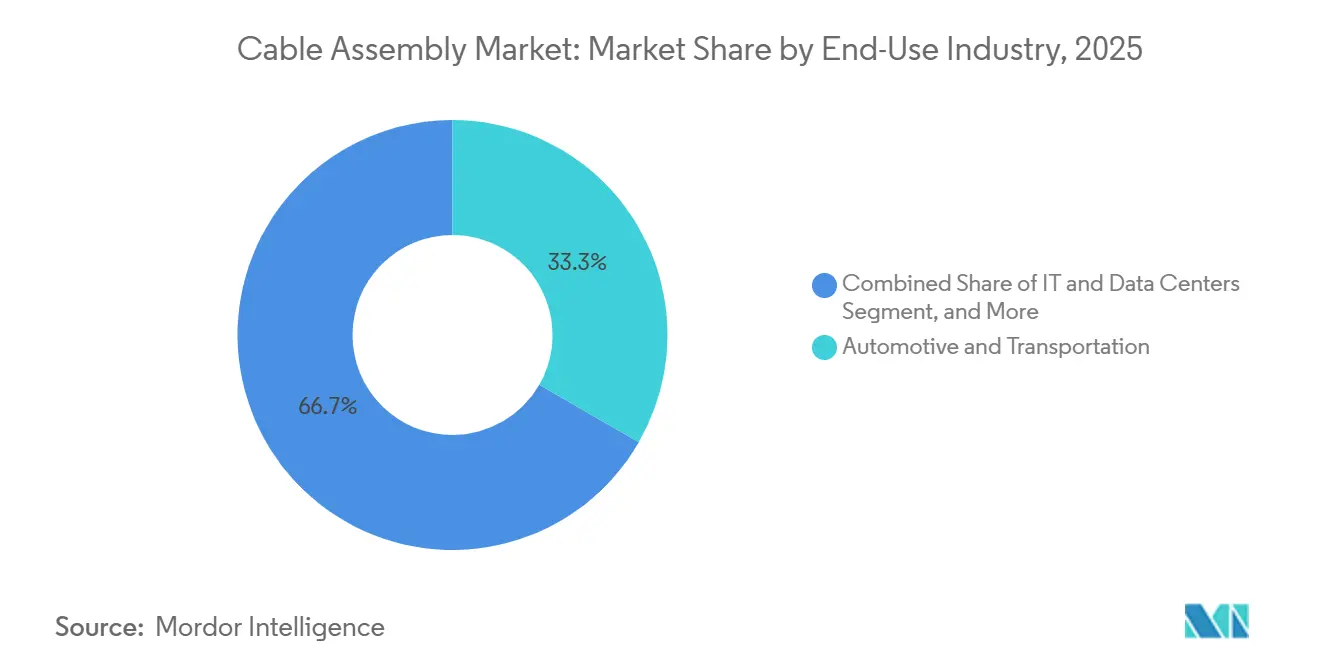

- By end-use industry, automotive and transportation accounted for 33.31% of 2025 revenue, whereas IT and data centers recorded the highest projected CAGR at 5.98% through 2031.

- By application, data communication held 38.76% of 2025 revenue, and high-performance computing interconnects are advancing at a 5.73% CAGR through 2031.

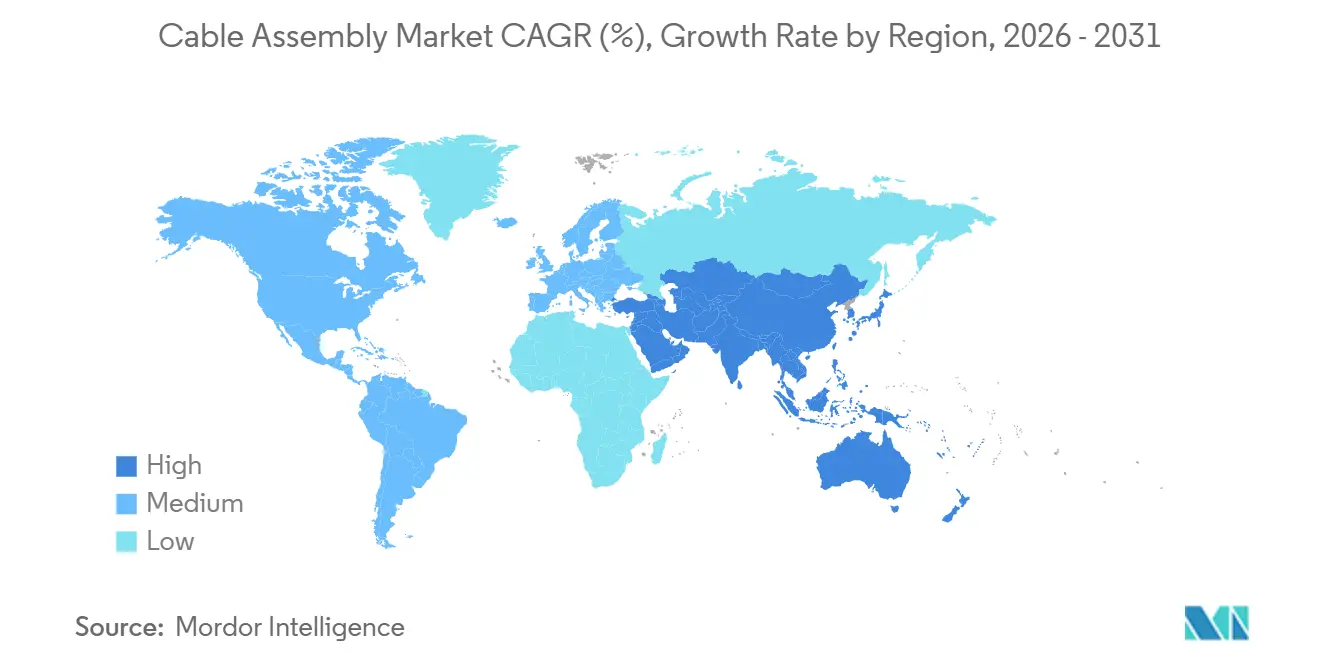

- By geography, Asia-Pacific captured 42.12% of 2025 revenue and is advancing at a 5.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cable Assembly Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in High-Speed Data-Center Interconnect Demand | +1.2% | Global, with concentration in North America and Asia-Pacific hyperscale hubs | Medium term (2–4 years) |

| Expansion of 5G and Fiber-to-the-Home Deployments | +1.0% | Global, led by North America and Asia-Pacific; secondary uptake in Europe and Middle East | Medium term (2–4 years) |

| Electrification and ADAS-Driven Automotive Wiring Complexity | +0.9% | Global, with early adoption in Europe and China; North America following for 800V platforms | Long term (≥4 years) |

| Industrial Automation and Smart-Factory Roll-outs | +0.7% | Asia-Pacific manufacturing corridors, Europe Industry 4.0 zones, selective North America sites | Medium term (2–4 years) |

| Quantum-Computing Cryogenic Cabling Requirements | +0.3% | North America and Europe research clusters; nascent commercial deployments | Long term (≥4 years) |

| eVTOL and Urban-Air-Mobility Modular Power Harnesses | +0.2% | North America and Europe certification pathways; Asia-Pacific prototype testing | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge In High-Speed Data-Center Interconnect Demand

Hyperscale operators are migrating from 400 Gbps to 800 Gbps and 1.6 Tbps optics, compressing refresh cycles to roughly two years and lifting fiber purchases under multi-year supply agreements. Active optical cables dissipate roughly half the port power of direct-attach copper, a difference that favors them in dense GPU racks where a single server can draw 10 kilowatts. Automated polishing lines that certify more than 10,000 termini per shift remain scarce, giving scale players an execution edge. IEEE 802.3’s ratification of 1.6 Tbps Ethernet in early 2026 will accelerate replacement of installed 200 G and 400 G inventories, sustaining double-digit fiber-assembly growth well into the forecast window.[1]Fierce Telecom Staff, “Fiber Broadband Association: 11.8 M homes passed in 2025,” FierceTelecom.com

Expansion Of 5 G And Fiber-To-The-Home Deployments

United States FTTH construction passed 11.8 million additional premises during 2025, absorbing 1.2–1.5 drop-cable assemblies per home as installers pivot from fusion splicing to push-on connectors. Pre-terminated harnesses cost up to 35% more per unit yet cut truck-roll labor by around one-third, an attractive trade-off in markets where field labor exceeds USD 75 per hour. Parallel 5 G mid-band densification boosts demand for hybrid copper-fiber feeder cables that integrate DC power for remote radio heads, while rural fixed-wireless rollouts favor NEMA 4X-rated backhaul assemblies in difficult trench terrain.

Electrification And ADAS-Driven Automotive Wiring Complexity

Moving from 400-volt to 800-volt battery systems doubles charging-station voltage requirements and raises insulation ratings to 1,500 V AC test levels. Each electric vehicle can add 15–25 kg of wiring over 2020 combustion benchmarks, even as zonal architectures push toward copper weight reduction. Automated routing and crimping lines cut touch labor by roughly half and lift first-pass yield beyond 99.5%, numbers essential for tier-one suppliers that must avoid recall risk on safety-critical harnesses. Shielded twisted-pair and coaxial links supporting raw video streams now exceed 6 GHz bandwidth, and European safety rules have rendered ADAS wiring standard equipment on all new passenger cars.

Industrial Automation and Smart-Factory Rollouts

Edge-connected robotics and IIoT sensors are pulling sealed M12 assemblies and Cat6A patch cords into wash-down or high-vibration plant areas once served by pneumatic controls. AI-guided vision cells achieved 98% first-pass quality on mixed-gauge harnesses in 2025 pilots, slashing scrap by up to half and reducing custom lead times to under three weeks. As proprietary fieldbus protocols recede, Industrial Ethernet variants enable multi-vendor interoperability but also invite price pressure that suppliers counterbalance with IP67 sealing, stainless-steel glands, and high-flex jackets rated beyond 5 million bend cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Copper and Specialty Metal Prices | -0.8% | Global, with acute impact in Asia-Pacific and Europe manufacturing hubs | Short term (≤2 years) |

| Stringent RoHS/REACH and Halogen-Free Material Mandates | -0.5% | Europe and North America regulatory zones; cascading to Asia-Pacific export-oriented suppliers | Medium term (2–4 years) |

| Tight Supply of High-Performance Fluoropolymer Dielectrics | -0.3% | Global, concentrated in North America and Europe PFAS regulatory jurisdictions | Medium term (2–4 years) |

| Signal-Integrity Challenges in Ultra-Miniature High-Frequency Connectors | -0.2% | Global, most acute in aerospace, defense, and high-speed data applications | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility In Copper and Specialty Metal Prices

London Metal Exchange copper futures climbed 63% from early 2025 to mid-2026, inflating the raw-material cost of goods by roughly one-fifth for assembly houses. Automotive contracts offer indexed adjustments, yet 60–90-day lags compress gross margin by as much as 400 basis points during rapid spikes. Smaller regional assemblers, lacking hedging or volume rebates on phosphor bronze and beryllium copper, apply surcharges or shift toward aluminum conductors that save 60–70% per kilogram but sacrifice 40% conductivity. Electric-vehicle harnesses averaging 80–100 kg of copper would incur up to USD 1,000 in extra wiring cost at a steady USD 10,000 per metric-ton price, a figure automakers struggle to absorb in full.

Stringent RoHS/REACH And Halogen-Free Material Mandates

Complying with lower lead and cadmium thresholds increases material and documentation costs by roughly 10–20% and forces reformulation of PVC jackets, which often trade off cold-bend performance. Halogen-free low-smoke-zero-halogen constructions, required for rail rolling stock and public-assembly structures, command up to a 50% premium yet need specialized extrusion tooling that only a limited group of global suppliers possess. The European Union’s proposal to classify certain PFAS under REACH Annex XIV complicates future access to PTFE or PFA dielectrics, which are vital for microwave and cryogenic assemblies, keeping compliance costs elevated across the forecast horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fiber Assemblies Capture Data-Center Upside

Fiber-optic assemblies held 36.54% of 2025 revenue and are projected to expand at a 6.06% CAGR, outpacing legacy copper offerings as hyperscale campuses migrate to 800 Gbps optics. The cable assembly market size for fiber products benefits from Meta’s multibillion-dollar Corning agreement, which pre-books capacity and signals confidence in long-term demand. Custom cable assemblies, about 28-30% of sales, underpin automotive, aerospace, and medical projects where just-in-time kitting shrinks’ inventory on original equipment manufacturers’ floors.

Standard off-the-shelf assemblies remain price sensitive, with Chinese contractors routing basic USB-C cables at sub-USD 2-unit costs, compressing margins outside retail-branded niches. Overmolded designs and high-frequency assemblies sustain gross margins near 30% because ingress-protection and insertion-loss guarantees are hard to replicate cheaply. Ribbon and flat-cable formats serve ultrathin consumer devices but face partial substitution from flexible printed circuits that co-laminate signal and power layers.

By Cable Type: Fiber Dominates While Power Conductors Accelerate

Fiber-optic cables accounted for 37.72% of 2025 revenue and will continue to lead at a 6.11% CAGR as single-mode specifications with sub-0.3 dB insertion loss become standard in spine-leaf architectures. Coaxial lines, roughly one-fifth of the cable assembly market size, grow more slowly as 5 G installers prefer lower-loss corrugated designs, yet they stay critical for antenna feeders that exceed 100 meters.

Power cables are gaining momentum from 800-volt vehicle architectures, lifting their share of the cable assembly market by mid-single digits as insulation ratings and current thresholds rise. RF and microwave cables, buoyed by electronic-warfare upgrades, sustain mid-single-digit growth on defense budgets that favour higher-frequency radar. Cat6A and Cat7 twisted-pair lines refresh enterprise campuses, but commoditization tempers growth to the low-single-digit range.

By End-Use Industry: Automotive Largest, IT and Data Centers Fastest

Automotive and transportation held 33.31% of 2025 revenue, underpinned by rising copper weight per electric vehicle and ADAS camera proliferation. Luxshare’s acquisition of Leoni’s wiring division illustrates consolidation that seeks scale and geographic diversification within the cable assembly market. Telecommunications sits near a 23% share as fiber-to-the-home builds and 5 G densification absorb weather-sealed jumpers.

IT and data centers, although just over one-tenth of market volume, advance at the fastest 5.98% CAGR as 1.6 Tbps coherent optics demand high-density fiber harnesses certified for sub-microsecond latency. Consumer electronics trails because longer smartphone refresh cycles cap accessory demand, whereas healthcare harnesses grow steadily on sterilizable silicone jackets. Aerospace and defense sustain mid-single-digit gains from rotorcraft modernization and eVTOL prototypes that need weight-saving assemblies.

By Application: Data Communication Dominant, HPC Rising

Data-communication links represent 38.76% of 2025 revenue, spanning enterprise Ethernet, USB, and FTTH drop lines that anchor the bulk of the cable assembly market. High-performance computing connections, though currently under 10%, are projected to grow at a 5.73% CAGR as AI training clusters mandate sub-nanosecond latency and cryogenic quantum rigs push permittivity stability below 4 K.

Power transmission cables expand on fast-charge stations and residential energy-storage units, while RF and microwave harnesses edge higher on phased-array antenna adoption. Sensor and control wiring profits from IP67-sealed M12 demands in IIoT rollouts and charging, and battery-management leads margin capture in e-mobility ecosystems.

Geography Analysis

Asia-Pacific contributed 42.12% of global 2025 revenue and is set to rise at a 5.78% CAGR as TE Connectivity, Hirose Electric, and Luxshare commit fresh capital to the Philippines, India, and mainland China. Japan and South Korea invest in optical-fiber capacity to serve domestic cloud expansion, whereas Vietnam picks up consumer-electronics programs as brands diversify sourcing beyond China.[2]Nikkei Asia Staff, “TE Connectivity Philippines expansion,” Asia.Nikkei.com

North America sits near 29% share, with reshoring activity accelerating after Nexans’ Electro Cables acquisition and multiple state incentives targeting critical infrastructure supply chains. Mexico advances as a nearshoring hub for harnesses feeding U.S. assembly plants, balancing higher U.S. labor costs.[3]Nexans Newsroom, “Nexans completes Electro Cables acquisition,” Nexans.ca

Europe holds roughly one-fifth of revenue; compliance burdens from RoHS and REACH weigh on smaller shops, yet premium niches such as AI-datacenter fiber and 800-volt vehicle harnesses thrive. Middle East and Africa and South America collectively remain below 10% but log steady orders for submarine links, transit electrification, and regional data-center buildouts.

Competitive Landscape

The cable assembly market shows moderate concentration: the top twenty vendors control roughly 55–60% of global revenue, leaving substantial room for regional specialists. Commodity USB-C and Cat6A assemblies face sub-USD 2 pricing that cramps gross profit, whereas aerospace or medical contracts attain 25–35% margins due to stringent qualification. Vertical integration into connector moulding and automated crimping helps TE Connectivity, Rosenberger, and Yazaki cut cycle time and control quality from resin to finished harness.

White-space opportunities emerge in eVTOL modular power harnesses, millikelvin cryogenic assemblies for quantum processors, and halogen-free LSZH cables that meet stricter IEC fire mandates. AI-driven inspection replaces manual checking, raising first-pass quality to 98% and slashing scrap. Connector innovation also shifts the playing field; Samtec’s 800-position AcceleRate HP series enables 112 Gbps PAM4 in PCIe 6.0 backplanes, spurring adjacent cable-assembly demand.

Capital intensity continues to escalate plants in the Philippines and Hungary exceed USD 60 million per site as suppliers add automated polishers, laser strippers, and optical backscatter testers. Certification to ISO 9001, AS9100, IATF 16949, and ISO 13485 remains an entry ticket for global bids, while integrated traceability systems become indispensable for regulated medical and defense programs.

Cable Assembly Industry Leaders

TE Connectivity Ltd.

Amphenol Corporation

Molex LLC

LuxShare Precision Industry Co., Ltd.

Yazaki Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Aptiv announced the spin-off of its Electrical Distribution Systems unit as Versigent, supported by a USD 1.6 billion notes offering.

- March 2026: Samtec expanded its AcceleRate Slim cable portfolio for mixed-impedance AI servers.

- January 2026: Amphenol posted record FY 2024 revenue of USD 15.2 billion after closing purchases of Carlisle Interconnect Technologies and Luetze.

Global Cable Assembly Market Report Scope

The Cable Assembly Market Report is Segmented by Product Type (Custom Cable Assemblies, Standard/Off-the-Shelf Assemblies, Overmolded Cable Assemblies, Fiber-Optic Assemblies, Ribbon/Flat-Cable Assemblies, High-Speed and High-Frequency Assemblies), Cable Type (Coaxial, Fiber-Optic, Ribbon/Flat, Twisted-Pair/Networking, RF and Microwave, Power), End-Use Industry (Automotive and Transportation, Telecommunications, Consumer Electronics, Industrial Automation and Robotics, Healthcare and Medical Devices, Aerospace and Defense, IT and Data Centers, Energy and Power, Rail and Mass Transit), Application (Data Transfer and Communication, Power Transmission, RF/Microwave Signal, High-Performance Computing, Sensor and Control, Charging and Battery Management, Lighting and Display), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Custom Cable Assemblies |

| Standard / Off-the-Shelf Assemblies |

| Overmolded Cable Assemblies |

| Fiber-Optic Assemblies |

| Ribbon / Flat-Cable Assemblies |

| High-Speed and High-Freq Assemblies |

| Coaxial |

| Fiber-Optic |

| Ribbon / Flat |

| Twisted-Pair / Networking |

| RF and Microwave |

| Power |

| Automotive and Transportation |

| Telecommunications |

| Consumer Electronics |

| Industrial Automation and Robotics |

| Healthcare and Medical Devices |

| Aerospace and Defense |

| IT and Data Centers |

| Energy and Power |

| Rail and Mass Transit |

| Data Transfer and Communication |

| Power Transmission |

| RF / Microwave Signal |

| High-Performance Computing |

| Sensor and Control |

| Charging and Battery Management |

| Lighting and Display |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Custom Cable Assemblies | |

| Standard / Off-the-Shelf Assemblies | ||

| Overmolded Cable Assemblies | ||

| Fiber-Optic Assemblies | ||

| Ribbon / Flat-Cable Assemblies | ||

| High-Speed and High-Freq Assemblies | ||

| By Cable Type | Coaxial | |

| Fiber-Optic | ||

| Ribbon / Flat | ||

| Twisted-Pair / Networking | ||

| RF and Microwave | ||

| Power | ||

| By End-Use Industry | Automotive and Transportation | |

| Telecommunications | ||

| Consumer Electronics | ||

| Industrial Automation and Robotics | ||

| Healthcare and Medical Devices | ||

| Aerospace and Defense | ||

| IT and Data Centers | ||

| Energy and Power | ||

| Rail and Mass Transit | ||

| By Application | Data Transfer and Communication | |

| Power Transmission | ||

| RF / Microwave Signal | ||

| High-Performance Computing | ||

| Sensor and Control | ||

| Charging and Battery Management | ||

| Lighting and Display | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the cable assembly market be by 2031?

It is forecast to reach USD 256.48 billion, reflecting a 5.34% CAGR over 2026-2031.

Which product type is expanding fastest within cable assemblies?

Fiber-optic assemblies are projected to grow at 6.06% CAGR, ahead of copper-based offerings.

What end-use segment is growing most quickly?

IT and data centers post the highest CAGR at 5.98% as hyperscale operators adopt 1.6 Tbps optics.

Which region leads global revenue in cable assemblies?

Asia-Pacific accounted for 42.12% of 2025 revenue and maintains the fastest 5.78% CAGR outlook.

How are raw-material price swings affecting suppliers?

A 63% copper-price surge between 2025 and 2026 cut gross margins by up to 400 basis points for assemblers lacking indexed contracts.

What new opportunities are emerging for specialty cable makers?

Growth pockets include eVTOL power harnesses, cryogenic quantum-computing cables, and halogen-free LSZH assemblies for rail.

Page last updated on: