Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 19.65 Billion |

| Market Size (2031) | USD 31.57 Billion |

| Growth Rate (2026 - 2031) | 9.95% CAGR |

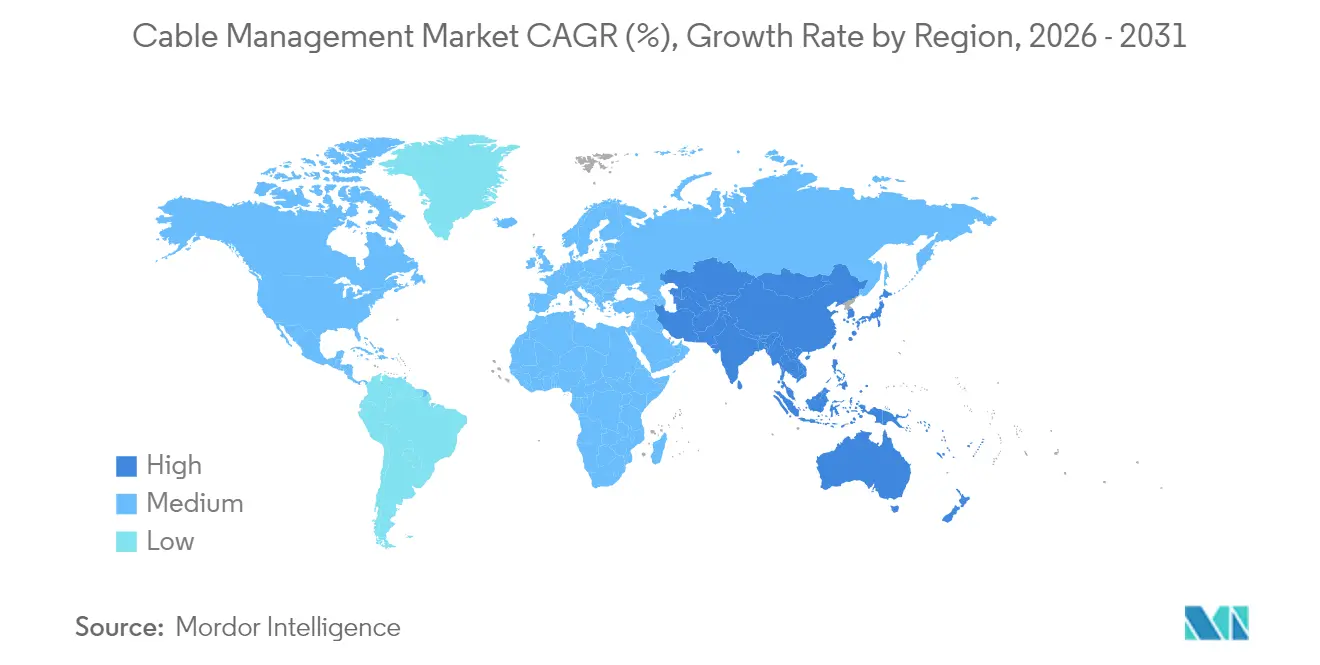

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

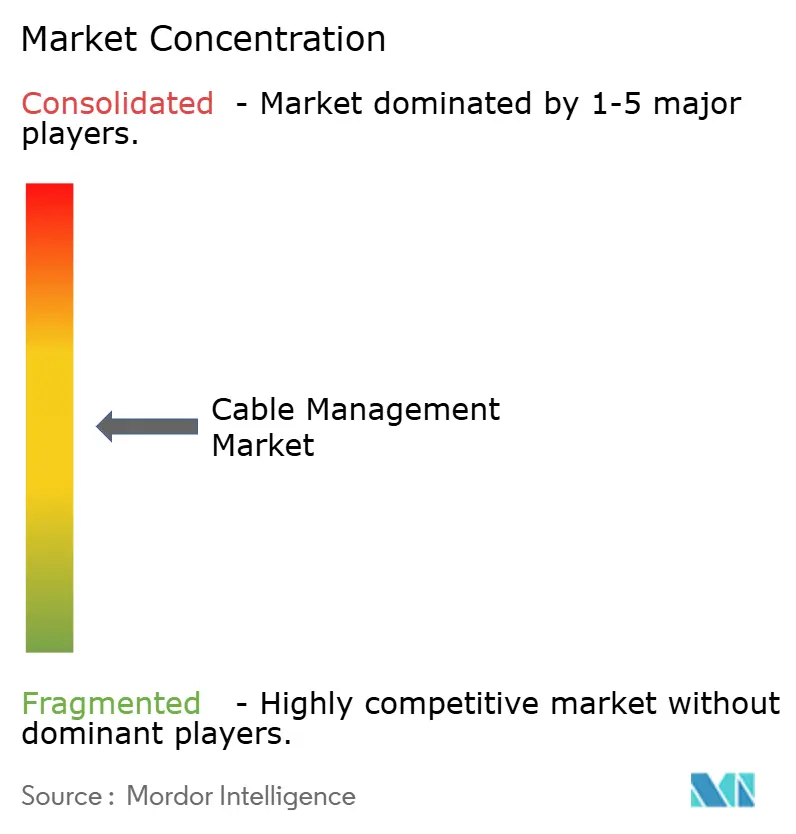

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cable Management Market Analysis by Mordor Intelligence

The cable management market size is expected to grow from USD 17.87 billion in 2025 to USD 19.65 billion in 2026 and is forecast to reach USD 31.57 billion by 2031 at 9.95% CAGR over 2026-2031. Increasing electrification of renewable-energy assets, hyperscale data-center construction, and industrial automation programs underpin this expansion. Higher power densities in 800 V EV-charging networks, convergence of data and control cabling within smart buildings, and modular off-site construction practices further intensify demand for advanced routing, protection, and identification solutions. Competitive activity centers on portfolio digitization and distribution-channel consolidation as suppliers race to integrate predictive maintenance features and shorten time-to-install. Supply-chain pressure from galvanized steel and PVC price swings persists, yet productivity gains from smart manufacturing and standard-modular product designs partially offset margin risk.

Key Report Takeaways

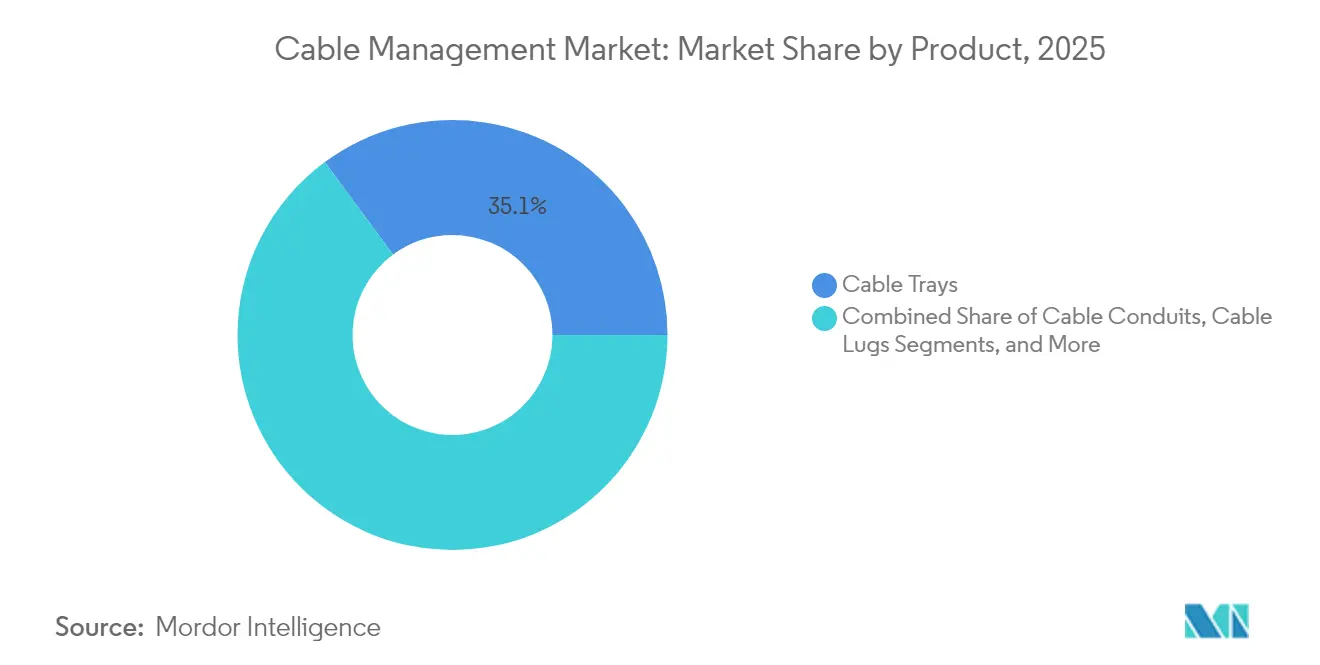

- By product, cable trays captured 35.12% revenue share in 2025, while cable connectors and glands led growth with a 10.52% CAGR through 2031.

- By end-user industry, IT and telecommunications held 28.24% of the cable management market share in 2025; data centers advance fastest at a 10.21% CAGR to 2031.

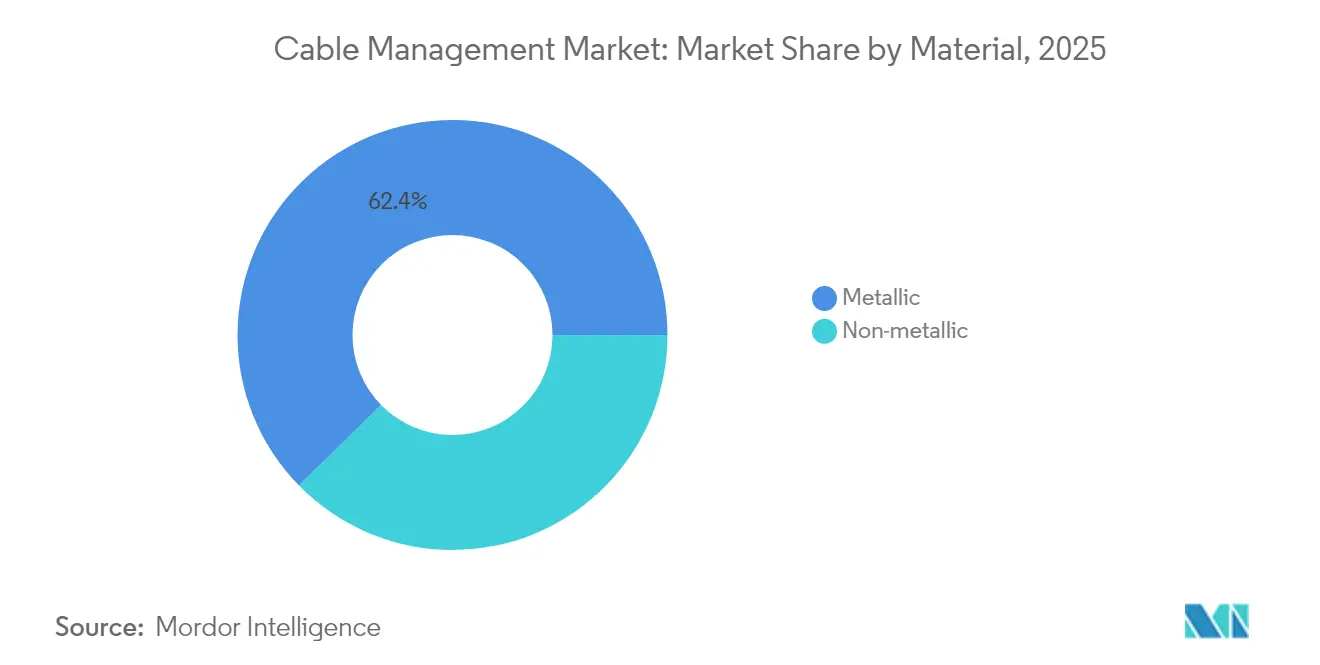

- By material, metallic solutions accounted for 62.35% share of the cable management market size in 2025, yet non-metallic alternatives are projected to expand at 10.97% CAGR between 2026-2031.

- By installation channel, overhead and ceiling systems led with 37.05% share in 2025 in the cable management market, while underground and buried systems record the highest forecast CAGR at 10.48% through 2031.

- By geography, North America commanded 39.02% of the cable management market in 2025; Asia Pacific is the fastest-growing region at an 10.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cable Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated renewable-energy build-outs | +2.1% | Global, with concentration in Asia Pacific and North America | Medium term (2-4 years) |

| Proliferation of hyperscale data centers | +2.8% | North America and EU, expanding to Asia Pacific | Short term (≤ 2 years) |

| Smart-building mandates in OECD economies | +1.7% | North America and EU, selective Asia Pacific markets | Medium term (2-4 years) |

| Electrification of industrial processes | +1.9% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Modular off-site construction methods | +1.2% | North America and EU, emerging in Asia Pacific | Medium term (2-4 years) |

| 800V EV-charging infrastructure rollout | +1.4% | Global, led by China, EU, and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Hyperscale Data Centers

Hyperscale expansion represents the strongest single catalyst for the cable management market. NVIDIA DGX SuperPOD installations now specify cable pathways that house 400 G and 800 G fiber links plus liquid-coolant hoses in confined footprints, doubling the volume of trays and connectors per rack when compared with enterprise facilities. AFL’s vertical cable-manager designs raise usable rack space by 40% and cut airflow losses, supporting power densities beyond 70 kW per rack. It is expected that GPU clusters require three times the routing hardware per rack, pressuring project managers to pre-order components 16 weeks ahead of build start dates. Specialized connector supply is tight, lengthening project lead times and amplifying the value of modular kits that reduce field terminations. Vendors incorporating RFID tags and thermal sensors into trays gain share as operators seek predictive maintenance to avoid downtime.

Accelerated Renewable-Energy Build-Outs

Utility-scale solar and onshore wind sites impose unique environmental and longevity requirements on cable management systems. The U.S. Department of Energy outlines 25-year service-life standards that reward UV-stable polymers, thermal-expansion joints, and corrosion-proof fasteners.[1]U.S. Department of Energy, “Solar Installation Best Practices,” energy.gov Panduit delivers cable ties rated from -40 °C to +90 °C, limiting annual maintenance truck rolls across desert plants. CAB Solar’s modular hangers reduce install labor by 60% and virtually eliminate sand ingress, lowering O&M cost per megawatt. Wind-turbine applications favor flexible carriers that tolerate continual tower sway and rotation, maintaining insulation integrity for 20 years. Hybrid solar-plus-storage sites add routing complexity because DC arrays, AC grid interconnects, and battery circuits must remain segregated to satisfy safety codes.

Smart-Building Mandates in OECD Economies

Revisions to the EU Energy Performance of Buildings Directive obligate developers to install structured cabling that supports IoT sensor networks, centralized lighting control, and PoE endpoints.[2]European Commission, “Energy Performance of Buildings Directive,” ec.europa.eu Eland Cables calculates a 40% bump in cabling density for smart offices versus traditional builds. Integrated pathways that combine power and data reduce ceiling-grid clutter while meeting IEEE 802.3bt’s 90 W power-over-ethernet ceiling. MC Technologies embeds temperature and humidity probes inside trays, alerting facility teams when de-rating thresholds approach.[3]MC Technologies, “Smart Building Platforms,” mctechnologies.com Paradoxically, widespread wireless adoption pulls more structured cabling because each access point requires reliable power and fiber backhaul.

Electrification of Industrial Processes

Manufacturers replacing pneumatic or hydraulic actuators with electric variants drive fresh investment in high-capacity tray systems that mitigate electromagnetic interference around variable-frequency drives. Rockwell Automation architecture guidelines separate operational-technology networks from corporate IT lines, doubling ladder-tray runs in brownfield retrofits. Prysmian’s quick-connect harnesses trim installation time by 30% while delivering chemical resistance for harsh process areas. Far East Cable leverages analytics to predict cable-bend fatigue and cuts maintenance budgets by 25% in smart factories. RFID-tagged harnesses feed asset-management systems, easing line reconfiguration and reducing unplanned downtime.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of galvanized steel and PVC | -1.8% | Global, with acute impact in cost-sensitive markets | Short term (≤ 2 years) |

| Lengthy certification cycles for flame-retardant plastics | -1.1% | North America and EU regulatory markets | Medium term (2-4 years) |

| Growing adoption of wireless/PoE solutions | -0.7% | North America and EU, expanding to Asia Pacific | Medium term (2-4 years) |

| Miniaturization reducing copper cable volumes | -0.5% | Global, concentrated in electronics manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Galvanized Steel and PVC

Spot prices for galvanized steel and PVC swung 15% in early 2025 as regional supply imbalances and energy-cost spikes hit procurement budgets. ADS Sheet Metal’s forecasts show aluminum hovering near USD 2,763 per ton, further complicating cost assumptions. Cable management suppliers shorten quote validity to 14 days and index contracts to commodity benchmarks, shifting risk to end users. Volatility encourages substitution: fiber-reinforced plastic trays see accelerated interest, yet their adoption is tethered to longer qualification cycles. Some EPC contractors lock in bulk raw-material hedges, but smaller installers absorb direct hits to profitability.

Lengthy Certification Cycles for Flame-Retardant Plastics

UL 2556 and UL 94 testing adds 18-24 months to new product launches, slowing the flow of innovative halogen-free polymers.[4]UL Solutions, “Flame Retardant Testing Standards,” ul.com nVent PYROTENAX research indicates potential tightening of UL 2196 requirements, signaling even longer lead times for approvals. Benvic reports certification outlays topping USD 500,000 per variant, a hurdle for startups diversifying beyond standard PVC. EU Construction Products Regulation forces multi-language declarations of performance, escalating paperwork for cross-border sales. Manufacturers maintain parallel product lines, legacy PVC for cost-sensitive projects, and HFFR for regulated sectors, straining inventory management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Infrastructure Density Drives Specialization

Cable trays retained a 35.12% share of the cable management market in 2025, reflecting their broad applicability, while cable connectors and glands are projected to grow at a 10.52% CAGR through 2031. Elevated rack densities in hyperscale data centers and renewable inverters amplify demand for high-ampacity lugs, strain-relief glands, and multi-tier trays that separate power and fiber circuits. The cable management market size for connectors is set to widen as modularity shortens installation windows and limits site labor exposure. Junction boxes and carriers post steady gains, with dynamic-motion carriers finding niche uptake in robotic welding cells. Premium vendors add RFID tagging and asset-tracking software to differentiate offerings and lock in service contracts, supporting hybrid CAPEX-plus-OPEX revenue models.

Ties, covers, and fasteners accumulate incremental revenue thanks to maintenance cycles that replace UV-aged components in solar farms. Innovations in snap-in channel covers reduce assembly time, and color-coded clips boost troubleshooting efficiency. High-current lugs suited for 1,500 V solar strings command ASP premiums, buttressing margins within the cable management market. As copper and aluminum price spreads fluctuate, dual-material lugs enter designs, combining aluminum bodies with copper-plated contacts to manage galvanic corrosion without heavy cost penalties.

By End-User Industry: Data Centers Accelerate Growth

IT and telecommunications held 28.24% of the cable management market share in 2025, yet data centers represent the fastest-growing end-user at 10.21% CAGR through 2031. Artificial-intelligence clusters, liquid-cooled servers, and battery-backed UPS architectures multiply pathway requirements per square foot. The cable management market size for data centers is therefore expected to capture a rising revenue slice as operators standardize on wider rung ladders and double-stacked basket trays to accommodate hybrid copper-fiber topologies.

Construction firms adopting modular prefabrication embed trays within wall panels, enabling hours-rather-than-days rack hall builds. Energy and utilities sectors push for corrosion-resistant solutions in offshore wind substations and hydrogen electrolyzer plants, sustaining metallic-tray demand. Manufacturing embraces flexible plug-and-play harnesses to support Industry 4.0 line changes, while healthcare facilities prioritize smooth, wipe-down surfaces and antimicrobial coatings. Across sectors, IT-OT convergence drives integrated raceways that preserve network segmentation yet promote data exchange for condition monitoring.

By Material Type: Non-Metallic Solutions Gain Momentum

Metallic options, principally steel and aluminum, commanded 62.35% of the cable management market size in 2025 owing to structural rigidity and fire performance. Non-metallic systems, however, show a stronger 10.97% CAGR on the back of corrosion-resistance mandates in chemical processing and weight-saving imperatives in aerospace. Hybrid assemblies combine steel backbones with FRP covers, delivering load-bearing strength while trimming weight by 25%.

Recycled-content quotas in EU public-procurement contracts spur suppliers to certify post-consumer content, complicating melt-chemistry but unlocking bids. Halogen-free flame-retardant formulations penetrate transport infrastructure where smoke-toxicity limits tighten. Marine and offshore energy segments pivot toward glass-reinforced polyester trays, which cut maintenance cycles in salt-spray zones. Supply continuity for specialty resins becomes critical, leading OEMs to dual-source from regional compounders.

By Installation Channel: Underground Systems Drive Growth

Overhead and ceiling installations led revenue with 37.05% share in 2025, but underground and buried systems outpace at 10.48% CAGR amid grid-hardening and EV-charging corridor rollouts. The cable management market supports multi-duct trenches integrating power, fiber, and control in shared civil works, trimming lifecycle costs. Under-floor raceways flourish in hyperscale data-center halls, enabling rapid rack row reconfigurations without ceiling work.

Basket trays remain favored in retrofits for ease of access, while wall-mounted ladders suit constrained industrial corridors. Nexans reports modular underground systems that splice in 70% less field time and deliver 80% safety gains, accelerating adoption in dense urban renewal projects. Regulatory divergence in burial depth, grounding, and fire-barrier practice challenges multinational suppliers to maintain adaptable product catalogs.

Geography Analysis

North America retained 39.02% of the cable management market in 2025, anchored by data-center megacampus construction across Virginia, Ohio, and Alberta. Federal incentives for renewable generation and transmission, together with grid-resilience funds, lift underground-system uptake. Mexico’s near-shoring boom stimulates cable-tray manufacturing footprints, evidenced by Panduit’s USD 50 million plant that serves both data-center and solar-farm demand.

Asia Pacific leads growth at an 10.71% CAGR through 2031. China’s smart-factory programs and India’s high-voltage transmission upgrades fuel large tenders favoring domestic suppliers equipped to navigate local certification. Japan and South Korea innovate miniaturized fiber-tray solutions for semiconductor cleanrooms, while Southeast Asia attracts foreign direct investment into battery gigafactories that specify heavy-duty non-metallic conduits. Regional content rules encourage joint ventures, such as ABB-Niedax’s North American tray JV blueprint now replicated in ASEAN markets.

Europe progresses steadily as smart-building codes and renewable-energy targets hold spending levels, though complex CPR documentation extends pre-bid phases. Germany’s automotive-line electrification demands flexible drag-chain carriers, and the U.K.’s London-edge data-center cluster invests in compact under-floor solutions. Eastern European wind corridors present new revenue pools, albeit with price-sensitive specifications that favor galvanized ladder trays over composites.

Competitive Landscape

The cable management market exhibits moderate concentration: the top five vendors collectively control around 45%, balanced by a long tail of regional specialists. Established majors such as ABB, Schneider Electric, Eaton, and Legrand deploy vertical integration and digital SaaS overlays to defend share. Distributor consolidation accelerates; Sonepar’s 17 acquisitions in 2024 added EUR 2.2 billion in sales and broadened shelf presence for preferred OEM brands.

Joint ventures and tuck-in acquisitions extend product breadth, ABB and Niedax integrate automation know-how with tray expertise, while Legrand’s purchase of VASS expands fiber management for hyperscale clients. Technology disruptors focus on smart trays with embedded sensors and cloud dashboards; early deployments show mean-time-to-repair falling 30% as faults pinpoint faster.

Patent filings cluster around composite-material blends and clip-in accessory modules, hinting at future differentiation through installation speed. Regional challengers leverage proximity, tailored codes, and shorter lead times to chip at incumbents, especially in Asia. Market leaders counter by localizing fabrication and offering BIM libraries that integrate with contractor workflows.

Cable Management Industry Leaders

Schneider Electric SE

Eaton Corporation plc

ABB Ltd.

HellermannTyton Group PLC

Chatsworth Products, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Legrand completed acquisition of VASS to enhance high-density fiber and power distribution offerings for hyperscale facilities.

- February 2025: TE Connectivity finalized its USD 2.3 billion purchase of Richards Manufacturing, adding aerospace and defense cable management capabilities.

- January 2025: Schneider Electric launched EcoStruxure Cable Management, embedding IoT sensors for tray-condition monitoring.

- December 2024: Prysmian closed its USD 4.2 billion acquisition of Encore Wire to expand renewable-energy portfolio.

Global Cable Management Market Report Scope

Cable management refers to managing electrical or optical cables in a cabinet. Products such as cable trays, ladders, and cable baskets support a cable through cabling routes.

The cable management market is segmented by product (cable trays, cable raceways, cable conduits, cable connectors and glands, cable carriers, cable lugs, and junction/distribution boxes), end-user industry (IT and telecommunication, construction, energy and utility, manufacturing, commercial), and geography (North America, Europe, Asia-Pacific, Rest of the World (Latin America and Middle East and Africa)). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product

| Cable Trays |

| Cable Raceways |

| Cable Conduits |

| Cable Connectors and Glands |

| Cable Carriers |

| Cable Lugs |

| Junction / Distribution Boxes |

| Ties, Covers, Fasteners, Clips |

By End-user Industry

| IT and Telecommunications |

| Construction |

| Energy and Utilities |

| Manufacturing |

| Commercial |

| Healthcare Facilities |

By Material Type

| Metallic (Steel, Aluminum) |

| Non-metallic (PVC, HDPE, FRP) |

By Installation Channel

| Overhead and Ceiling |

| Under-floor |

| Wall-mounted |

| Underground / Buried |

By Geography

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product | Cable Trays | ||

| Cable Raceways | |||

| Cable Conduits | |||

| Cable Connectors and Glands | |||

| Cable Carriers | |||

| Cable Lugs | |||

| Junction / Distribution Boxes | |||

| Ties, Covers, Fasteners, Clips | |||

| By End-user Industry | IT and Telecommunications | ||

| Construction | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Commercial | |||

| Healthcare Facilities | |||

| By Material Type | Metallic (Steel, Aluminum) | ||

| Non-metallic (PVC, HDPE, FRP) | |||

| By Installation Channel | Overhead and Ceiling | ||

| Under-floor | |||

| Wall-mounted | |||

| Underground / Buried | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What growth rate is projected for the cable management market through 2031?

The market is forecast to grow at a 9.95% CAGR between 2026 and 2031.

Which region will add demand most quickly over the forecast period?

Asia Pacific is projected to record the fastest expansion at an 10.71% CAGR to 2031.

Which product category is expected to grow fastest?

Cable connectors and glands are anticipated to expand at 10.52% CAGR through 2031.

What end-user vertical holds the largest share today?

IT and telecommunications commanded 28.24% share in 2025.

How are raw-material price swings affecting suppliers?

Volatility in galvanized steel and PVC pricing compresses margins, leading vendors to shorten quote validity and explore composite alternatives.

Why are underground installations gaining traction?

Grid-hardening and renewable-energy transmission projects favor buried systems, which are forecast to grow at 10.48% CAGR.

Page last updated on: