Aviation Connectors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.14 Billion |

| Market Size (2031) | USD 7.99 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Connectors Market Analysis by Mordor Intelligence

Aviation connectors market size in 2026 is estimated at USD 6.14 billion, growing from 2025 value of USD 5.83 billion with 2031 projections showing USD 7.99 billion, growing at 5.39% CAGR over 2026-2031. This steady rise springs from the industry’s tilt toward More Electric Aircraft architectures, which swap hydraulic and pneumatic subsystems for electric alternatives that multiply connector counts per airframe. Wide adoption of integrated modular avionics, electrified flight-control actuation, and in-flight connectivity keeps high-speed data transmission in focus, therefore lifting demand for fiber optic and high-current power interfaces. Production backlogs that exceed 6,000 aircraft at both Airbus and Boeing ensure multi-year baseline volume even as new Urban Air Mobility platforms add fresh connector content under FAA’s Innovate28 framework. At the same time, elevated raw-material prices and certification bottlenecks tighten supply, so tier-one suppliers with hedging strategies and deep test capabilities maintain pricing leverage.

Key Report Takeaways

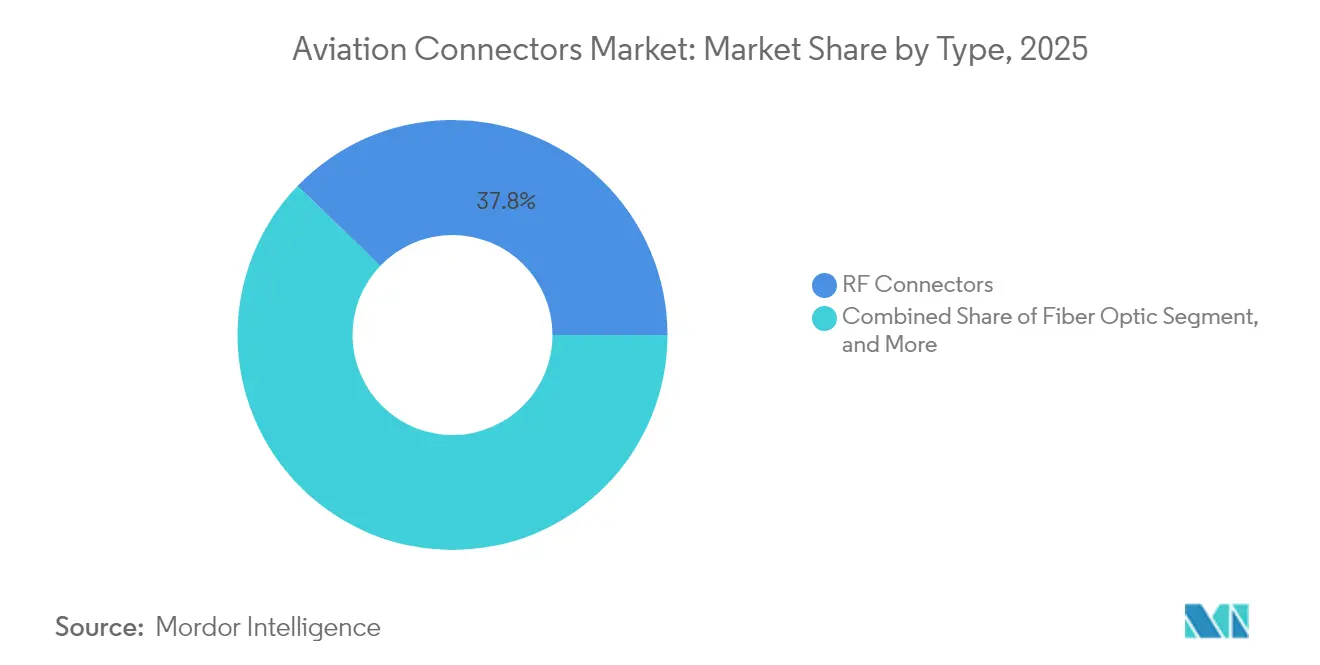

- By type, RF connectors held 37.82% of aviation connectors market share in 2025 while fiber optic connectors are advancing at a 7.41% CAGR through 2031.

- By shape, circular connectors commanded 56.10% revenue in 2025 and are growing at a 6.85% CAGR to the end of the decade.

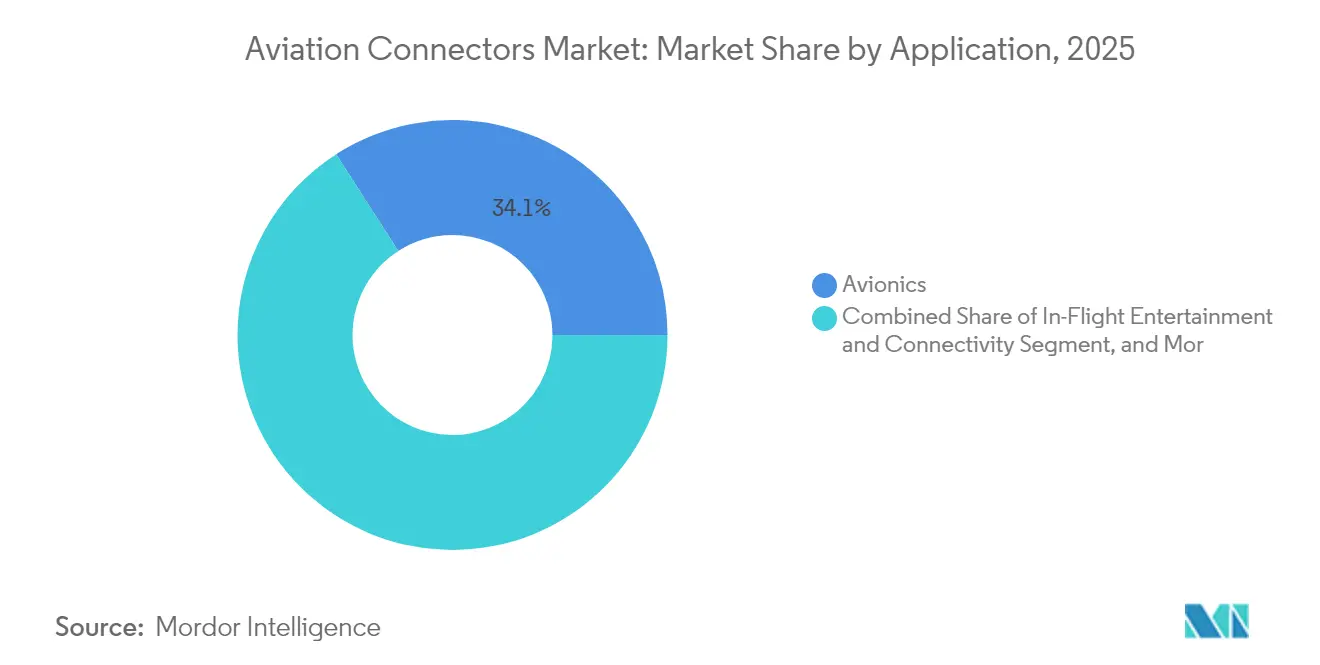

- By application, avionics led with 34.10% revenue in 2025, but in-flight entertainment and connectivity is forecast to post a 7.76% CAGR to 2031.

- By end user, original equipment manufacturers contributed 62.20% of 2025 revenue, whereas the aftermarket segment is set to grow at a 6.74% CAGR through 2031.

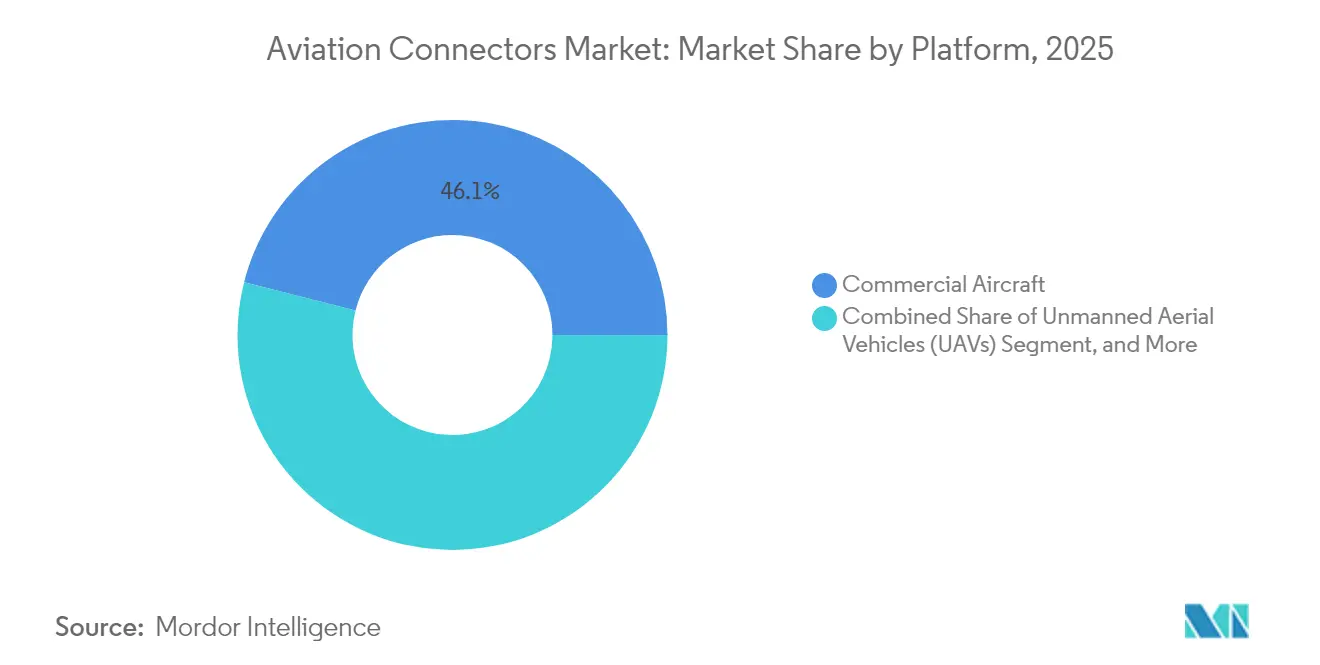

- By platform, commercial aircraft platforms accounted for 46.05% of 2025 spending, while unmanned aerial vehicles are projected to expand at a 7.82% CAGR over the forecast period.

- By material, aluminum alloys represented 41.05% of 2025 sales, yet composite and polymer connectors are on track for a 6.82% CAGR to 2031.

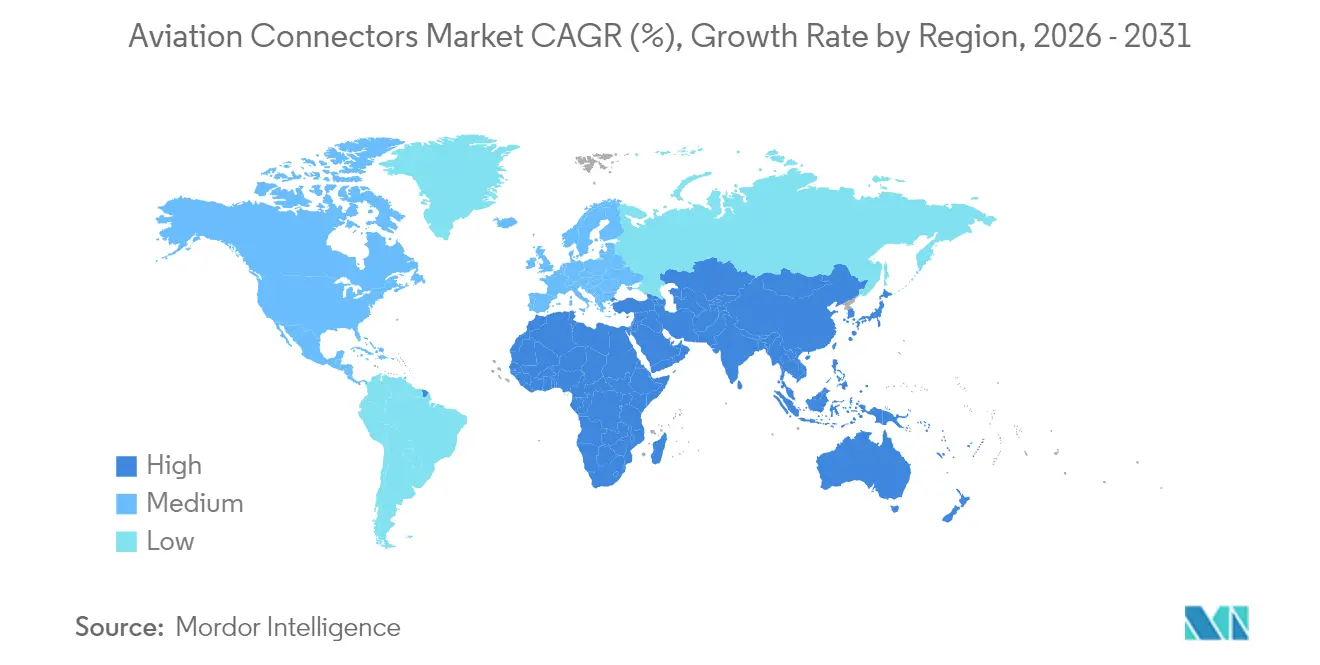

- By geography, North America led with 40.10% revenue in 2025, and Asia-Pacific is expected to register the fastest 8.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aviation Connectors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Commercial Aircraft Fleet Expansion | +1.2% | Global, particularly Asia-Pacific and North America | Medium term (2-4 years) |

| Rising Demand for Lightweight Aircraft Electrical Systems | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Proliferation of In-Flight Entertainment and Connectivity | +1.1% | Global, early adoption in North America and Middle East | Short term (≤ 2 years) |

| Increasing Adoption of More Electric Aircraft Architecture | +1.3% | Global, led by Airbus and Boeing programs | Long term (≥ 4 years) |

| Standardization of Modular Connector Interfaces by Aerospace OEMs | +0.5% | North America and Europe | Medium term (2-4 years) |

| Emergence of Urban Air Mobility Platforms Requiring High-Density Connectors | +0.7% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Commercial Aircraft Fleet Expansion

Global deliveries reached 1,180 jets through November 2024, and combined Airbus and Boeing backlogs now top 12,000 units, which locks in multi-year production visibility and secures a solid runway for the aviation connectors market. Asia-Pacific airlines absorb roughly 40% of new orders as traffic rebounds beyond 2019 levels, while single-aisle programs target sustained output rates above 60 jets per month. Each narrowbody contains about 1,200 connectors, and widebodies can exceed 2,500, so any production-rate uptick directly multiplies connector shipments. Lessors own more than half of the active fleet and increasingly specify standardized interfaces, encouraging OEMs to embed modular designs that streamline maintenance across varied operators. Cabin and cockpit retrofit programs for aging airframes further widen the installed base that needs periodic connector replacement.

Rising Demand for Lightweight Aircraft Electrical Systems

More Electric Aircraft configurations grow on the promise of 3-5% lower fuel burn and higher system reliability. Electric environmental control packs, ice-protection units, and flight-control actuators increase onboard generation from approximately 200 kVA on legacy types to over 1 MW on next-generation designs. [1]SAE International, “Aerospace Standards,” SAE.ORG This shift increases connector counts by up to 60% per airframe and prompts suppliers to deliver housings in composite or aluminum-lithium alloys that help keep weight in check. Eaton’s power panels on the Boeing 787, for instance, integrate more than 1,500 high-power contacts rated for 270 VDC and 115 VAC, supported by advanced thermal paths that handle greater current density. [2]Eaton Corporation, “Investor Presentation Q3 2025,” EATON.COM Research consortia in Europe have validated double-digit weight savings when aluminum is replaced with carbon-fiber-reinforced polymers, helping the case for high-performance composite shells.

Proliferation of In-Flight Entertainment and Connectivity

Satellite broadband evolved from a premium perk into an essential service. United Airlines committed to Starlink retrofits across over 1,000 aircraft in 2024, and each installation swaps roughly 900 legacy contacts for fiber optic terminations capable of multi-gigabit throughput. Panasonic’s Astrova platform runs 4K displays that require 10 Gbps fiber backbones, a ten-fold rise versus earlier copper architectures. Airlines monetize connectivity via tiered packages; sustained ancillary revenue reinforces quick retrofit payback, thereby accelerating demand. Fiber’s immunity to electromagnetic interference also harmonizes with increasingly electrified flight-control systems, reducing crosstalk risk inside densely packed cabins.

Increasing Adoption of More Electric Aircraft Architecture

High-voltage distribution on demonstrators such as NASA’s X-57 and Airbus’s earlier E-Fan initiatives has proven viable operation at 500-540 VDC, which demands arc-resistant contacts and expanded creepage distances.[3]NASA, “X-57 Maxwell Program,” NASA.GOVUrban Air Mobility prototypes follow similar electrical baselines. Connectors with integrated liquid-cooling passages are transitioning from test rigs to serial production for eVTOL motor controllers, thereby creating a new premium niche. Standardization efforts under SAE AIR8484 are establishing pin-outs and data-protocol norms, which will, over time, enable OEMs to dual-source without extended requalification.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Existing Backlog of Aircraft Deliveries | -0.6% | North America and Europe | Short term (≤ 2 years) |

| Volatility in Raw Material Prices | -0.8% | Global | Short term (≤ 2 years) |

| Qualification Delays Due to Rigorous Certification Cycles | -0.4% | North America and Europe | Medium term (2-4 years) |

| Limitations of Legacy Aircraft Wiring Harness Designs in Retrofit Programs | -0.3% | Mature fleets worldwide | Long ter |

| Source: Mordor Intelligence | |||

Existing Backlog of Aircraft Deliveries

Production targets have slipped as engine supply, labor, and documentation issues restrict output. Boeing’s 737 MAX line stayed capped at 38 units per month for most of 2024, which defers connector shipments linked to later fuselage build stages. Airbus faced similar pacing on the A320neo family after powerplant inspection cycles slowed final assembly. Suppliers that built inventory against earlier rate assumptions now carry higher working capital, and their milestone-linked payments shift right, tightening near-term cash flow. Smaller tier-three firms are especially vulnerable because they lack program diversity and must wait for single-aisle ramps to recover.

Volatility in Raw Material Prices

Gold averaged USD 2,350 per ounce in 2024, up 27% year on year, raising the cost of mandatory contact plating that ensures low resistance in avionics backplane connectors. Copper touched USD 4.10 per pound, and silver remained volatile between USD 28 and USD 32, all of which erode margins when contracts lack price-adjustment clauses. Large groups use hedging to cover 60-70% of their annual exposure, but niche players often cannot offset swings, so profitability compression spurs consolidation or subcontracting to bigger brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Fiber Optic Adoption Quickens as Bandwidth Demands Surge

RF interfaces account for the largest market share of 37.82% in 2025, as radar, satellite communication, and navigation systems require stable performance up to 40 GHz. Therefore, aircraft builders will continue to favor rugged coaxial lines in these applications. Printed circuit board connectors supporting AFDX and Time-Sensitive Networking within integrated modular avionics are migrating toward 1 Gbps and beyond, tightening impedance budgets that prompt suppliers to refine contact geometry. Fiber optic connectors are expanding at a 7.41% CAGR, faster than the aviation connectors market, as streaming-class entertainment, electronic flight bags, and predictive maintenance analytics move to higher bandwidth around the airframe. United’s 1,000-plus narrowbody Starlink campaign alone drives a requirement for more than 400,000 new fiber terminations by 2027.

The demand for fiber optics mirrors the shift from federated boxes to centralized network architectures. Collins Aerospace’s Pro Line Fusion utilizes optical backplanes to link processing clusters, reducing harness weight by nearly one-third while providing redundant paths that meet fail-safe mandates. RF connectors maintain their foothold in high-vibration areas, such as landing gear bays, whereas hybrid power-and-signal assemblies are gaining ground in emerging electric taxi systems. Overall, material advances and installer training are overcoming early pain points of fiber cleanliness and bend-radius control, so adoption will stay on a rising arc.

By Shape: Circular Connectors Retain Primacy Because of Environmental Sealing

Circular interfaces accounted for 56.10% of the 2025 turnover and are predicted to increase by 6.85% annually through 2031. Their inherent 360-degree EMI shielding, threaded coupling, and IP67 sealing are suited for wing root zones, engine pylons, and wheel wells, where fluids, temperature swings, and vibration converge. Rectangular devices thrive in dense avionics racks where board-to-board space runs tight; still, those housings rely on secondary gasketing for moisture protection, so inspection intervals end up shorter, raising the cost of ownership.

Composite circular shells approved to AS85049 cut weight by about 35% compared with aluminum while slotting into identical panel cutouts, an attribute fleet operators prize because it avoids harness redesign. Rectangular styles win incremental use in power distribution units where blade contacts carry over 100 A per position. On Urban Air Mobility demonstrators, both shapes coexist: round cases carry motor current, and slim rectangles ferry sensor data and battery telemetry inside tight nacelles. This blended architecture should increase overall connector counts and expand revenue for suppliers that can integrate varied geometries into a single module.

By Application: Avionics Still Lead but In-Flight Entertainment Accelerates

Avionics accounted for 34.10% of 2025 sales as flight-critical computers, navigation boxes, and surveillance radars require high-reliability multi-path wiring. Each widebody features approximately 300 avionics connectors per bay, all of which are qualified to DO-160G environmental standards. Meanwhile, in-flight entertainment and connectivity are increasing at a market-beating 7.76% CAGR, as airlines see a direct return from ancillary Wi-Fi revenue. Panasonic’s Astrova launch, featuring 4K OLED screens, establishes 10 Gbps optical links as the new baseline and extends data-grade connectors even into seat-back assemblies.

Power distribution harnesses grow as electrical loads rise beyond 1 MW on future twin-aisles. High-current circular plugs rated to 270 VDC move into proximity with integrated cooling loops to manage temperature rise, a design factor that can increase connector unit cost by 40% compared to air-cooled equivalents. Landing gear, lighting, and galley systems utilize LED drivers and brake-by-wire modules, which eliminate some legacy copper wiring but introduce digital loops to monitor health in real-time. Hence, the net effect remains an upward trajectory in connector value per aircraft despite some consolidation of sub-systems.

By End User: OEM Channels Dominate but Aftermarket Gathers Pace

Original equipment manufacturers generated 62.20% of 2025 revenue, driven by robust handovers from Airbus and Boeing. A single 787 or A350 integrates more than 2,500 connectors spanning avionics, cabin, and power domains. Automated assembly lines that produce 10,000 parts per day provide tier-one vendors with efficiency and help them secure long-term pricing.

The aftermarket, though smaller, is posting a 6.74% CAGR. The global fleet age for narrowbodies now averages just under 12 years, which prompts heavy checks earlier in the decade and triggers mandatory connector replacement when plating wear or insulation discoloration appears. Parts Manufacturer Approval suppliers offer 20-30% cost savings while meeting identical FAA TSO specifications. Airlines mix PMA and OEM units carefully to protect residual values, yet rising maintenance events guarantee a growing serviceable-material flow that benefits distributors stocking broad legacies.

By Platform: Commercial Jets Hold the Pot, UAVs Deliver Fastest Growth

Commercial aircraft platforms were responsible for 46.05% of 2025 demand, primarily driven by single-aisle programs that aim for monthly output exceeding 60 frames. Each narrowbody requires approximately 1,300 connectors across all systems, and incremental cabin options increase the bill-of-materials value. Military jets, such as the F-35, consume over 3,000 points of interconnect due to their dense electronic warfare and sensor suites, and deliveries remained above 140 units in 2024, providing a stable premium niche.

Unmanned aerial vehicles show a 7.82% CAGR as defense ministries allocate higher budgets to intelligence and strike capabilities. India’s 31-unit MQ-9B purchase in 2024 marked a shift toward long-endurance drones equipped with satellite links, utilizing rugged Micro-D and circular nano connectors. Business jets are adopting high-speed Ethernet for real-time cabin management, increasing connector content per aircraft by roughly 40% compared to earlier models. Helicopters and regional transports continue to modernize legacy wiring with AFDX upgrades, driving replacement sales even in modest production climates.

By Material: Aluminum Alloys Still Predominate while Composites Advance

Aluminum shells kept a 41.05% foothold in 2025 thanks to their balance of machinability, strength, and cost, but composites and high-performance polymers are advancing at a 6.82% CAGR. Carbon-fiber-reinforced PEEK housings weigh a third less than equivalent aluminum units yet survive 15 Grms vibration when bonded with metallic insets. Stainless steel reserves its role in engine mounts where continuous temperatures exceed 200 °C, although its density nearly triples the airframe weight contribution per connector.

Aluminum-lithium alloys offer an additional 10% mass reduction and are already featured in A350 structures. However, connector adoption is slower due to raw ingot costs that are three to four times higher than those of standard 6061. Nevertheless, weight-critical wing sensors have begun to justify the premium. Titanium and magnesium remain niche for severe-load conditions or electromagnetic shielding, and additive manufacturing is emerging as a route to lower waste on these expensive metals, potentially unlocking future share gains.

Geography Analysis

North America captured 40.10% of 2025 revenue, powered by Boeing’s 737 MAX and 787 lines plus Lockheed Martin’s F-35 final assembly operations. Connector majors cluster production in Mexico, taking advantage of labor costs that are approximately 60% lower than those in the domestic U.S. and leveraging near-shoring resilience under the USMCA. The region also benefits from strong defense spending that underwrites high-reliability interfaces for next-generation fighters and missile systems.

Europe maintains a rich aerospace ecosystem, with Airbus delivering 643 jets through November 2024 and complementing military output from Dassault and Leonardo. Regulatory harmonization under EASA simplifies multi-country sourcing, although post-Brexit dual certification adds extra lead time for U.K. facilities. Extensive wide-body fleets at European flag carriers generate recurring demand for retrofitting fiber optic upgrades inside cabins.

Asia-Pacific is the fastest-growing region at an 8.52% CAGR. COMAC’s C919 achieved eight deliveries in 2024 and targets 150 annually by 2028, while India’s new C295 line shipped its first transport aircraft in September 2024. Domestic supply-chain development policies in both nations drive aggressive local connector qualification programs, though high-reliability gaps still leave room for Western vendors. Fleet expansion across low-cost carriers and MRO capacity additions assure vibrant aftermarket growth, especially as cabin-connectivity retrofits scale throughout the decade.

Competitive Landscape

Competition sits at a moderate fragmentation. Amphenol’s USD 2 billion purchase of Carlisle Interconnect in May 2024 combined two leading harsh-environment portfolios, nudging the acquirer’s aerospace exposure to roughly 17% of consolidated revenue and reinforcing scale leverage across material sourcing and test labs. Eaton Aerospace posted USD 1.079 billion in Q3 2025 sales and secured a 25.9% operating margin, thanks to sole-source positions on Boeing 787 and Airbus A350 power panels, which shielded prices.

Technology rivalry centers on miniaturization, high-current density, and weight reduction. Glenair’s composite MIL-DTL-38999 shells trim mass by more than one-third while maintaining drop-in interchangeability, resulting in premium pricing on retrofit lines. Additive manufacturing specialists pursue titanium housings with internal EMI labyrinths that conventional machining cannot deliver, though certification cycles of 18-36 months still favor incumbents with established DER relationships at FAA and EASA. New entrants often carve out niches in urban air mobility prototypes, where connector specifications continue to evolve, offering a window for differentiated hybrid power and signal modules.

Regional supply strategies also shape rivalry. Amphenol, TE Connectivity, and Radiall have expanded Mexican and North African plants to diversify beyond China and align with near-shoring incentives. At the same time, Chinese and Indian policy makers push localization, but complex plating and precision machining processes keep barriers high. Overall, established brands leverage multi-decade qualification pedigree to defend share even as emerging programs open pockets of greenfield demand.

Aviation Connectors Industry Leaders

Amphenol Corporation

TE Connectivity Ltd.

Eaton Corporation

Smiths Group PLC

Carlisle Companies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Boeing awarded Amphenol a multi-year contract to supply composite circular connectors for the 737-MAX system-upgrade package, a deal covering more than 2 million units through 2030.

- November 2024: Eaton Aerospace reported Q3 2025 sales of USD 1.079 billion, a 14% year-over-year increase, and booked a 1.1 book-to-bill ratio signaling continued backlog growth.

- October 2024: Panasonic Avionics launched the Astrova in-flight entertainment platform with 4K OLED displays and 10 Gbps optical interfaces, securing a United Airlines retrofit covering over 500 jets.

- September 2024: Tata Advanced Systems delivered the first C295 transport aircraft from its Vadodara line, embedding more than 1,000 locally sourced connectors under India’s Make-in-India mandate.

Global Aviation Connectors Market Report Scope

The Aviation Connectors Market encompasses the production and distribution of connectors specifically designed for aviation applications, ensuring reliable and efficient electrical and data transmission in various aircraft systems. These connectors are critical components used across avionics, power distribution, lighting systems, and other essential functionalities in the aviation industry.

The Aviation Connectors Market Report is Segmented by Type (PCB, RF Connectors, Fiber Optic, Other Types), Shape (Circular, Rectangular), Application (Avionics, Power Distribution, Lighting Systems, Cabin Management, Landing Gear, and In-Flight Entertainment and Connectivity), End User (OEM, Aftermarket), Platform (Commercial Aircraft, Military Aircraft, Business Jets, Helicopters, UAVs), Material (Aluminum Alloys, Stainless Steel, Composite and Polymer, Other Materials), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| PCB (Printed Circuit Board) |

| RF Connectors |

| Fiber Optic |

| Other Types |

| Circular |

| Rectangular |

| Avionics |

| Power Distribution |

| Lighting Systems |

| Cabin Management |

| Landing Gear |

| In-Flight Entertainment and Connectivity |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| Commercial Aircraft |

| Military Aircraft |

| Business Jets |

| Helicopters |

| Unmanned Aerial Vehicles (UAVs) |

| Aluminum Alloys |

| Stainless Steel |

| Composite and Polymer |

| Other Materials |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Type | PCB (Printed Circuit Board) | ||

| RF Connectors | |||

| Fiber Optic | |||

| Other Types | |||

| By Shape | Circular | ||

| Rectangular | |||

| By Application | Avionics | ||

| Power Distribution | |||

| Lighting Systems | |||

| Cabin Management | |||

| Landing Gear | |||

| In-Flight Entertainment and Connectivity | |||

| By End User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Platform | Commercial Aircraft | ||

| Military Aircraft | |||

| Business Jets | |||

| Helicopters | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| By Material | Aluminum Alloys | ||

| Stainless Steel | |||

| Composite and Polymer | |||

| Other Materials | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the aviation connectors market?

The aviation connectors market size stands at USD 6.14 billion in 2026.

How fast is demand expected to grow over the forecast period?

Market value is projected to rise to USD 7.99 billion by 2031, delivering a 5.39% CAGR over 2026-2031.

Which connector type is expanding the quickest?

Fiber optic connectors are forecast to advance at a 7.41% CAGR thanks to rising on-board data-rate needs.

Why is Asia-Pacific the fastest-growing region?

COMAC C919 production, India’s new military transport lines, and expanding low-cost-carrier fleets drive an 8.52% CAGR in the region.

How does electrification influence connector demand?

More Electric Aircraft architectures lift electrical loads above 1 MW per widebody, increasing both connector counts and current-carrying requirements.

Which companies dominate global supply?

Amphenol, TE Connectivity, Eaton, Radiall, and ITT collectively account for about 55-60% of total revenue.

Page last updated on: