Ethernet Over Coax Equipment And Subscribers Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

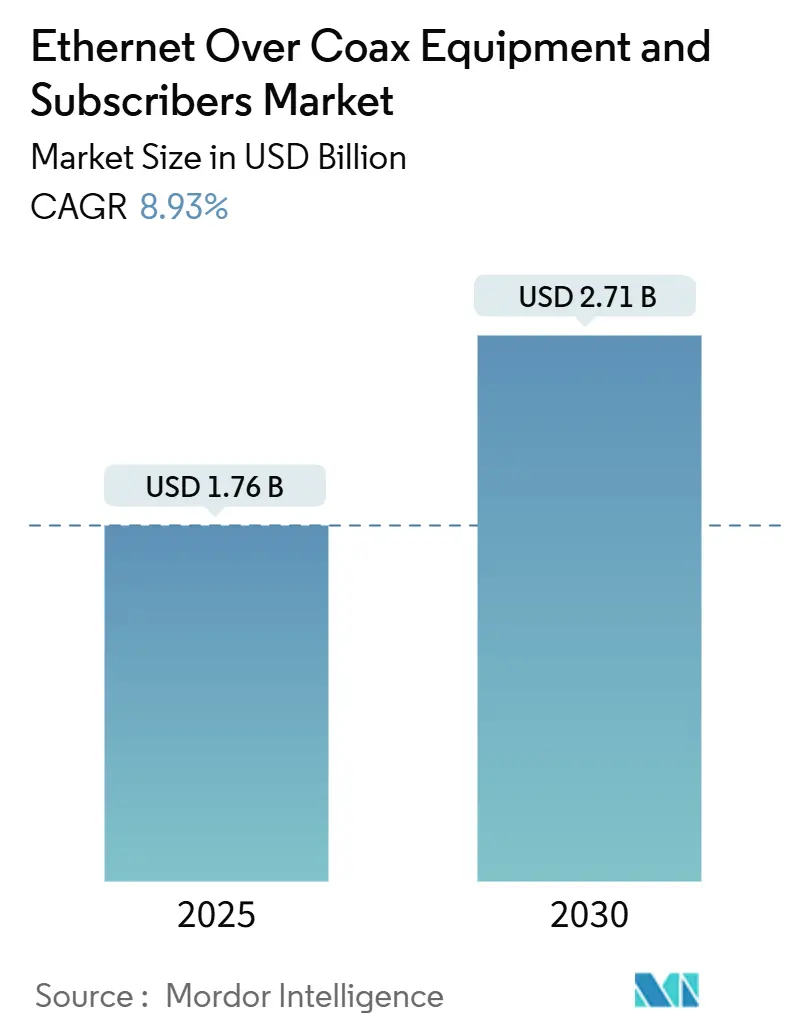

| Market Size (2025) | USD 1.76 Billion |

| Market Size (2030) | USD 2.71 Billion |

| Growth Rate (2025 - 2030) | 8.93% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethernet Over Coax Equipment And Subscribers Market Analysis by Mordor Intelligence

The Ethernet Over Coax Equipment and Subscribers market size reached USD 1.76 billion in 2025 and is projected to rise to USD 2.71 billion by 2030, advancing at an 8.93% CAGR over the forecast horizon. Operators continue to unlock latent capacity in legacy coax cabling to satisfy surging household demand for 4K/8K streaming and cloud-gaming traffic, while simultaneously postponing the high capital outlays tied to all-fiber builds. Growth remains closely linked to the ubiquity of coax inside multi-dwelling units and hospitality venues, where construction constraints and stringent permitting rules still favor upgrade projects over greenfield fiber trenching. North American cable companies underpin early adoption through DOCSIS 4.0 and Distributed Access Architecture (DAA) investments, whereas Asia-Pacific manufacturers drive the next wave by embedding G.hn Wave-2 chipsets into industrial IoT retrofits that require deterministic throughput. Price swings in copper-as high as 45% in 2024-are paradoxically reinforcing coax reuse economics because existing in-building wiring remains a sunk asset that operators can modernize with limited incremental metal consumption.

Key Report Takeaways

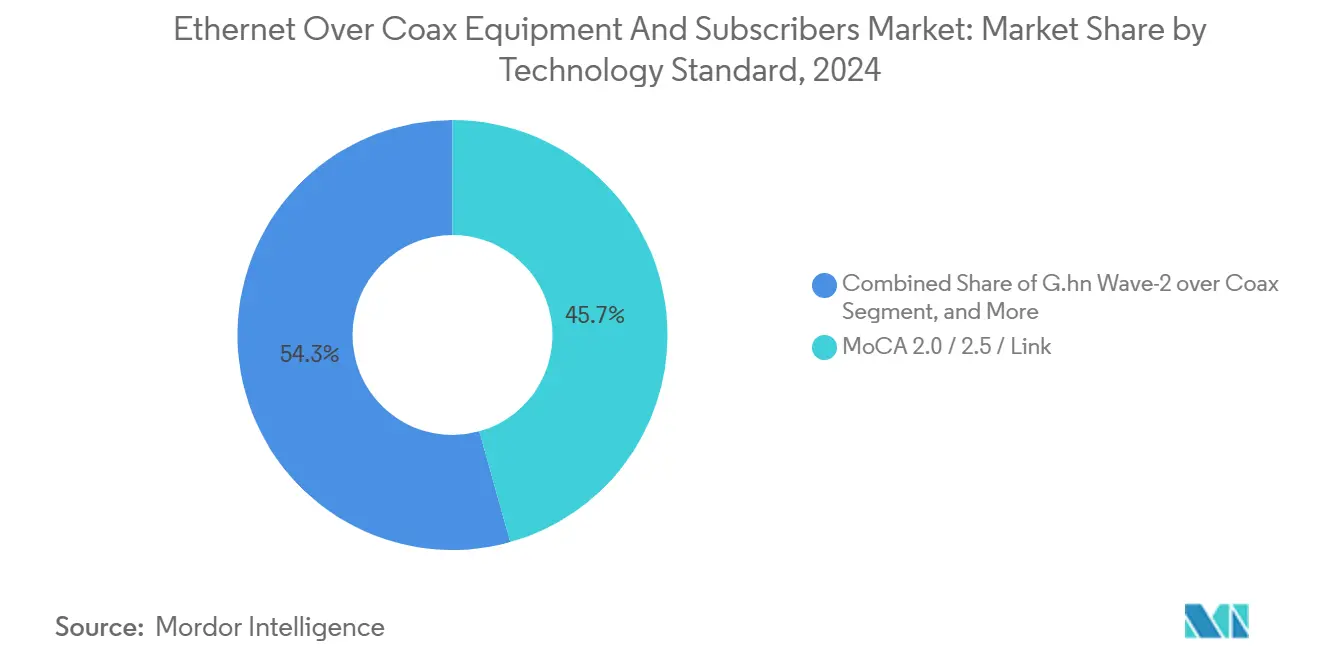

- By technology standard, MoCA 2.5 accounted for 45.67 % of Ethernet Over Coax Equipment And Subscribers market share in 2024, yet G.hn Wave-2 is expected to climb 9.19 % annually through 2030.

- By equipment type, home adapters dominated with 36.53 % revenue contribution in 2024; access modems are forecast to notch the fastest 9.73 % CAGR as operators migrate toward centralized DAA nodes.

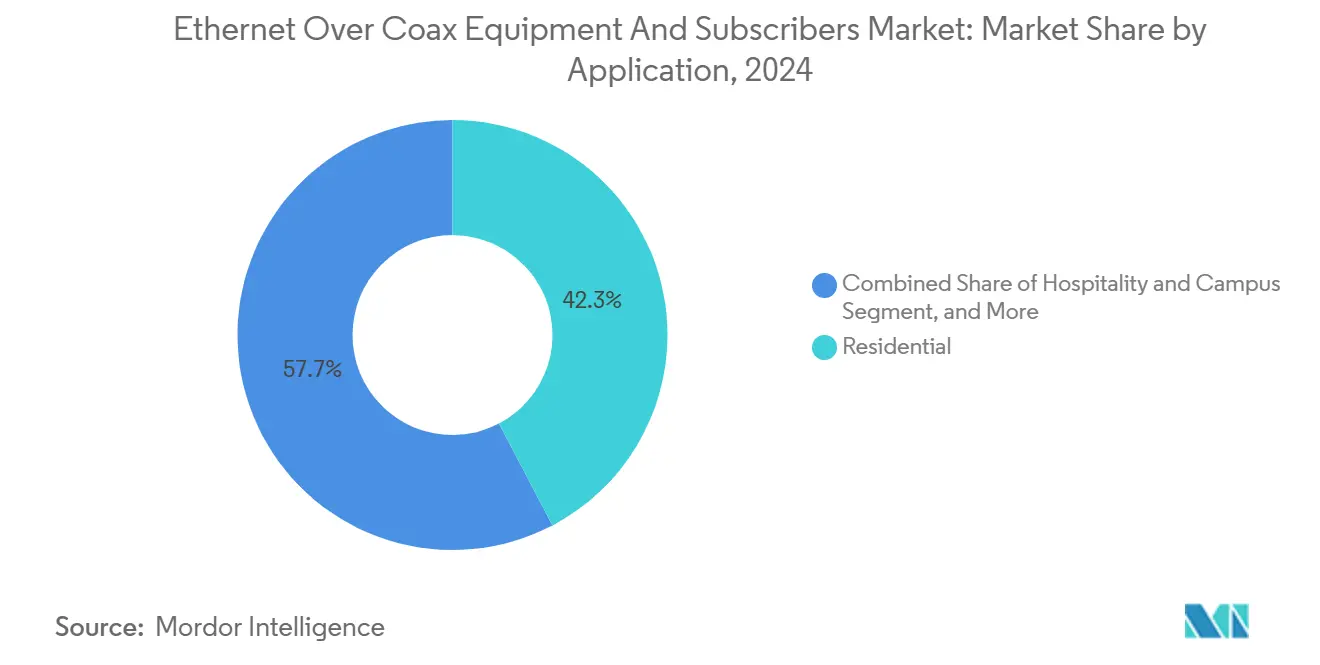

- By application, residential deployments held 42.31 % of the Ethernet Over Coax Equipment And Subscribers market size in 2024, whereas industrial IoT is poised for a 9.42 % CAGR to 2030.

- By subscriber category, retail consumers represented 43.96 % of 2024 value, but fiber and fixed-wireless ISPs show the strongest 10.32 % CAGR outlook because they increasingly rely on MoCA-Link for in-home distribution.

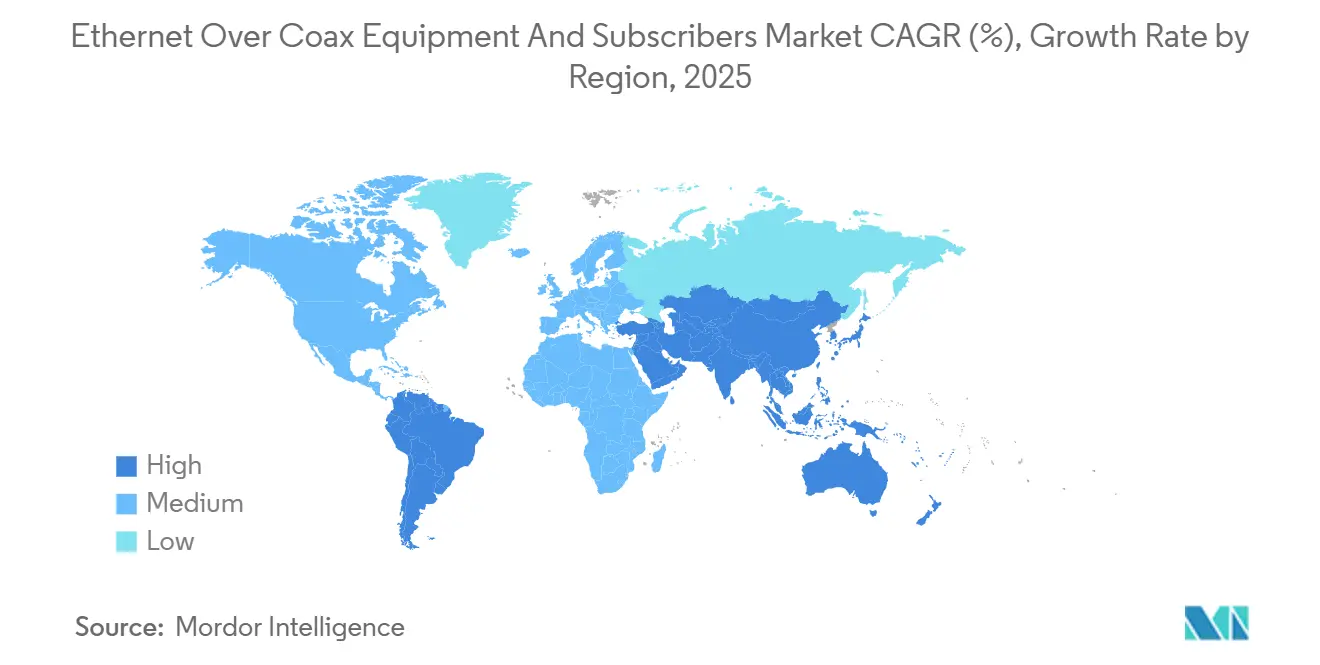

- By geography, North America led with 36.78 % of Ethernet Over Coax Equipment And Subscribers market share in 2024; the region should log healthy mid-single digit expansion through 2030 as DOCSIS 4.0 rollouts accelerate.

Global Ethernet Over Coax Equipment And Subscribers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding 4K/8K and cloud-gaming bandwidth needs | +2.1 % | Global, concentrated in North America and EU | Short term (≤ 2 years) |

| Cost-saving reuse of legacy coax | +1.8 % | Global, especially MDU-dense urban markets | Medium term (2-4 years) |

| Shift to Distributed Access Architecture | +1.4 % | North America core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Fixed-wireless CPE competition | +1.2 % | North America and EU, selective Asia-Pacific | Long term (≥ 4 years) |

| Industrial IoT adoption of G.hn | +0.9 % | Asia-Pacific manufacturing hubs, spill-over to MEA | Long term (≥ 4 years) |

| Satellite broadband pilots with MoCA-Link | +0.7 % | Rural North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Exploding 4K/8K and cloud-gaming bandwidth needs drive infrastructure stress

Mainstream 4K streaming and the rise of cloud gaming have elevated symmetrical traffic beyond what legacy asymmetric DOCSIS nodes were designed to handle.[1]The Economic Times, “China Launches World’s First 10G Broadband Network,” economictimes.indiatimes.com DOCSIS 4.0 allows 10 Gbps downstream and 6 Gbps upstream over the existing plant, giving cable operators a viable counter to fiber ISPs without extensive civil works. MoCA 2.5’s sub-5 millisecond latency delivers a wired backhaul outperforming mesh Wi-Fi inside dense apartments, thereby mitigating gamer complaints about lag. The subsequent load created by 8K content could exceed Wi-Fi 6 headroom, making wired coax backbones an attractive upgrade path for service providers. As a result, equipment vendors supplying 1.8 GHz amplifiers, splitters and MoCA-enabled gateways are benefitting from tier-one operator purchase orders.

Cost-saving reuse of legacy coax infrastructure versus fiber investment

Deploying fiber to each dwelling can cost USD 1,000-4,000 per unit in urban centers, whereas MoCA Access can lift speeds to 1 Gbps at close to 20 % of that cost. InCoax’s Finnish apartment project validated the capex arbitrage by delivering gigabit service without drywall demolition or tenant displacement. Copper price inflation further enhances the relative value proposition because re-terminating existing coax requires little new metal compared with new fiber or copper pulls. For brownfield factories, downtime quickly eclipses material costs, making non-intrusive coax overlays the favored choice for line managers keen to avoid lost production hours. Developers are now adding “coax-upgrade ready” clauses into building specs so owners can fast-track broadband modernization without navigating citywide fiber ordinances.

Operator shift to Distributed Access Architecture powers coax backhaul

DAA relocates PHY and MAC processing from the head-end deeper into the network, allowing operators to run 1.8 GHz coax segments purely as high-capacity backhaul from remote PHY devices to customer gateways. CommScope’s unified DOCSIS 4.0 platform enables operators to toggle between Full Duplex and Extended Spectrum modes, supporting incremental bandwidth upgrades while deferring costly fiber overlays. Large U.S. MSOs ordered more than 10,000 Teleste 1.8 GHz amplifiers in 2025 to prepare outside-plant drops for future 3 GHz extensions. This architectural realignment boosts demand for access modems, optical nodes, and intelligent amplifiers that can be managed centrally, underpinning the segment’s 9.73 % CAGR outlook.

Fixed-wireless CPE growth forces coax modernization

5G fixed-wireless providers now advertise 1 Gbps service without trenching, adding urgency for cable operators to future-proof coax plants. Satellite broadband firms such as Starlink rely on in-home MoCA-Link adapters to distribute rooftop signal throughout dwellings, demonstrating that coax remains valuable even when the primary access is wireless. Consequently, cable companies are bundling DOCSIS 4.0, Wi-Fi 7, and MoCA 2.5 in gateway SKUs to maintain a speed advantage over wireless competitors. Rural franchises that lack dense fiber corridors now employ hybrid designs combining fixed-wireless backhaul with coax last-drop, helping operators tap BEAD funds that allow secondary technologies where fiber proves uneconomic.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating FTTH roll-outs | −2.3 % | Global, led by Asia-Pacific and EU | Medium term (2-4 years) |

| Aging coax drops in dense MDUs | −1.7 % | Urban North America and EU | Short term (≤ 2 years) |

| Interference with legacy analog services | −1.1 % | Global, emerging markets | Long term (≥ 4 years) |

| Fiber-centric subsidy programs (BEAD, etc.) | −0.9 % | North America, expanding to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating FTTH roll-outs cannibalize coax investment

Government-backed fiber stimulus in China, Japan, and the EU shifts operator budgets away from coax hardware, especially when grants mandate fiber as the “technology of first resort”. The U.S. BEAD program earmarks USD 42.45 billion exclusively prioritizing FTTH, permitting coax only after economic infeasibility tests, which lengthens sales cycles for MoCA and G.hn vendors.[2]National Telecommunications and Information Administration, “Final Guidance for BEAD Funding,” ntia.gov As large operators secure public subsidies, they may postpone coax upgrades, creating short-term demand gaps for equipment suppliers. This policy tilt challenges market participants to position coax as an interim solution that dovetails with long-term fiber roadmaps rather than a competing path.

Aging coax infrastructure causes reliability challenges

MDU risers installed prior to 2000 often exhibit corrosion and impedance mismatches that degrade high-frequency signals needed for G.hn and MoCA waveforms. Urban electromagnetic noise further reduces usable throughput, forcing building owners to weigh the cost of coax remediation against one-time fiber overbuilds. When the remediation bill closes in on fiber install costs, many landlords opt for FTTH to sidestep repeat upgrade cycles, curbing addressable market size for retrofit equipment. Industrial users with deterministic latency needs also shy away from questionable coax segments, limiting G.hn penetration until certification of cable plant integrity can be assured.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Standard: MoCA 2.5 Sustains Lead While G.hn Gains Momentum

MoCA 2.5 held 45.67 % of the Ethernet Over Coax Equipment and Subscribers market share in 2024, supported by robust backward compatibility and the wide availability of chipsets.[3]Multimedia over Coax Alliance, “MoCA 2.5,” mocalliance.orgThe standard’s 2.5 Gbps net throughput satisfies most home-networking use cases, keeping customer acquisition costs low for operators. G.hn Wave-2, however, is advancing at a 9.19 % CAGR by delivering adaptive modulation that thrives on older or impaired coax-an advantage in brownfield factories and emerging-market apartment blocks.

Looking ahead, operators evaluating MoCA 3.0 trials against G.hn Wave-3 prototypes will weigh silicon availability, licensing terms, and industrial tool-chain integration. Vendors with dual-protocol silicon are increasingly favored, ensuring interoperability across hybrid access topologies. Standards competition will likely intensify once satellite and fixed-wireless ISPs formalize indoor distribution specifications, because those sectors value latency and self-organizing network features intrinsic to G.hn.

By Equipment Type: Access Modems Accelerate Centralization Shift

Home adapters commanded 36.53 % of 2024 revenue as consumers self-installed plug-and-play bridges to extend Wi-Fi coverage. Yet access modems, integral to remote PHY and DAA rollouts, are projected to climb 9.73 % annually, powered by DOCSIS 4.0 qualification wins and operator demand for centralized management.

The Ethernet Over Coax Equipment and Subscribers market size for access modems could reach USD 1.05 billion by 2030, given their pivotal role in converged gateways that aggregate fiber, coax, and Wi-Fi radios in a single enclosure. Modems that combine MoCA, G.hn, and 10G-EPON switching stand to capture incremental wallet share as operators simplify CPE inventories. Meanwhile, ruggedized switch nodes supplying Power over Coax for cameras and sensors are carving out an industrial vertical where extended distance and deterministic packet scheduling matter more than raw bandwidth.

By Application: Industrial IoT Becomes the Growth Engine

Residential networks still represented 42.31 % of 2024 revenue thanks to cable-operator service upgrades, yet industrial IoT deployments are on track for a 9.42 % CAGR because production lines can ill-afford downtime linked to fiber trenching. G.hn’s time-sensitive networking profile meets factory automation requirements, helping manufacturers avoid costly rewires while realizing sub-10 millisecond loop times.

Security and surveillance also exploit coax’s superior reach-up to 5,000 feet at 10 Mbps via extenders-where Ethernet falls short. In hospitality, gigabit MoCA Access enables IPTV and 1 Gbps internet with minimal guest-room disruption, strengthening average revenue per available room without a full-scale refurbishment. Collectively, non-residential domains now account for nearly half of installed ports, hinting that enterprise and industrial pain points will shape future product roadmaps.

By Subscriber Category: Fiber and Fixed-Wireless ISPs Outpace Incumbents

Retail consumers bought 43.96 % of units in 2024, largely through e-commerce channels, bundling MoCA adapters with Wi-Fi mesh kits. However, fiber and fixed-wireless ISPs exhibit a 10.32 % CAGR as they deploy coax inside premises to sidestep powerline noise and structural barriers that hobble Wi-Fi backhaul.

Cable and pay-TV operators still dominate absolute volumes, but competitive dynamics are shifting: satellite providers such as Dish have rejoined the MoCA Alliance to guarantee multi-gigabit room-to-room distribution once outdoor units deliver high-throughput Ka-band links. Enterprises are the smallest slice today, yet post steady double-digit expansion because coax runs within legacy office towers provides an immediate backbone for IoT sensors and high-definition video conferencing without added conduit.

Geography Analysis

North America accounted for 36.78 % of 2024 revenue, with U.S. MSOs deploying DOCSIS 4.0 amplifiers and remote PHY nodes in major metro markets. The Ethernet Over Coax Equipment and Subscribers market size for the region should exceed USD 1.15 billion by 2030 as operators leverage BEAD flexibility clauses to fund last-mile coax upgrades where fiber bids rank uneconomic. Canada is mirroring this blueprint across high-rise condos in Toronto and Vancouver, whereas Mexico prioritizes coax in tourist corridors where hospitality Wi-Fi upgrades command a premium average revenue per user.

Europe’s growth is mixed. Germany and the United Kingdom lean on coax-upgrade programs in tightly packed flats where fiber pull-throughs would breach fire barriers or heritage protections, but France and Spain accelerate FTTH thanks to generous state subsidies. The continent’s regulatory rigor around electromagnetic emission and aging-plant certification could temper short-term growth; nonetheless, ETSI alignment on MoCA Link spectrum masks will ease multi-vendor interoperability concerns, supporting steady adoption through 2030.

Asia-Pacific presents a bifurcated picture. China’s rapid 10G-PON rollout may reduce domestic coax demand, yet Japan, South Korea, and India favor G.hn for industrial automation retrofits. Australia’s mining sector taps ruggedized G.hn nodes to extend connectivity in dusty plants, while Southeast Asian hotels opt for MoCA Access to sidestep fiber imports subject to onerous customs duties. The Middle East and Africa register the fastest 9.24 % CAGR as smart-city projects piggyback coax into existing ducts, and the Medusa subsea cable promises to lower wholesale bandwidth prices, further motivating operators to offer gigabit-class coax services in North Africa.

Competitive Landscape

The Ethernet Over Coax Equipment and Subscribers industry features moderate fragmentation, with standards differentiation underpinning positioning. MaxLinear’s 2025 rebound to USD 95.9 million quarterly revenue highlights how chip suppliers ride customer inventory cycles while advancing MoCA 3.0 silicon tape-outs. InCoax Networks and Positron Access Solutions focus on hospitality and MDU retrofits, tailoring firmware to compensate for aging splitters and taps that plague older European buildings.

CommScope’s exit from its cable and connectivity segment via a USD 10.5 billion divestiture to Amphenol will refocus resources on access-network solutions, potentially accelerating its DOCSIS 4.0 node roadmap. Teleste scales amplifier shipments to North American MSOs, while Vantiva leads the modem race with the first commercially available DOCSIS 4.0 FDD gateway. Vendors that marry coax with Wi-Fi 7 and 10G-EPON switching stand to capture larger bills of material as operators consolidate CPE SKUs.

Patent litigation remains an undercurrent; Comcast’s ongoing suit against MaxLinear over MoCA IP underscores how intellectual property shapes royalty streams and market access. Niche players compete by embedding Power over Coax, low-temperature solder, or AI-based noise cancellation, features that larger vendors may integrate via acquisition. White-space opportunities include ruggedized G.hn nodes for petrochemical sites and MoCA Link adapters tuned for satellite backhaul, segments where incumbent IT vendors possess limited coax expertise.

Ethernet Over Coax Equipment And Subscribers Industry Leaders

MaxLinear, Inc.

Hitron Technologies Inc.

Actiontec Electronics, Inc.

goCoax Technology Co., Ltd.

Teleste Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: CommScope reported Q2 2025 net sales of USD 1.39 billion and agreed to sell its Connectivity and Cable Solutions unit to Amphenol for USD 10.5 billion, closing H1 2026.

- July 2025: CableLabs launched its DOCSIS 4.0 modem certification program, introducing higher fees and dual-standard testing options.

- June 2025: MoCA Alliance unveiled MoCA Link, enabling 2.5 Gbps indoor connectivity for 5G, satellite, and PON providers.

- May 2025: CableLabs certified Vantiva’s four-OFDM DOCSIS 3.1+ modem, unlocking 8–9 Gbps downstream without plant rebuild.

Global Ethernet Over Coax Equipment And Subscribers Market Report Scope

| MoCA 2.0 / 2.5 / Link |

| G.hn Wave-2 over Coax |

| DOCSIS EoC Bridging |

| Other Technology Standard |

| Home Adapters/Bridges |

| Service-Provider CPE/Gateways |

| Ethernet Extender Kits |

| Access Modems and Switch Nodes |

| Residential |

| Multi-Dwelling Units (MDU) |

| Hospitality and Campus |

| Industrial and IoT |

| Security and Surveillance |

| Retail Consumers |

| Cable / Pay-TV Operators |

| Fiber and Fixed-Wireless ISPs |

| Enterprises and SMB |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Technology Standard | MoCA 2.0 / 2.5 / Link | ||

| G.hn Wave-2 over Coax | |||

| DOCSIS EoC Bridging | |||

| Other Technology Standard | |||

| By Equipment Type | Home Adapters/Bridges | ||

| Service-Provider CPE/Gateways | |||

| Ethernet Extender Kits | |||

| Access Modems and Switch Nodes | |||

| By Application | Residential | ||

| Multi-Dwelling Units (MDU) | |||

| Hospitality and Campus | |||

| Industrial and IoT | |||

| Security and Surveillance | |||

| By Subscriber Category | Retail Consumers | ||

| Cable / Pay-TV Operators | |||

| Fiber and Fixed-Wireless ISPs | |||

| Enterprises and SMB | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the projected value of the Ethernet Over Coax Equipment And Subscribers market in 2030?

It is expected to reach USD 2.71 billion by 2030, reflecting an 8.93 % CAGR from 2025.

Which technology standard currently leads global deployments?

MoCA 2.5 holds roughly 45.67 % share, though G.hn Wave-2 is catching up quickly.

Why are industrial IoT users embracing coax upgrades?

G.hn-over-coax offers deterministic latency in brownfield factories without halting production for fiber pulls.

How do DOCSIS 4.0 upgrades impact coax equipment demand?

They are triggering a shift toward access modems and intelligent amplifiers designed for 1.8 GHz operation.

What role does the BEAD program play in the United States?

BEAD funding prioritizes fiber but allows coax when fiber proves uneconomic, thus sustaining retrofit opportunities.

Which region is forecast to grow the fastest through 2030?

Middle East and Africa, at a projected 9.24 % CAGR, thanks to smart-city and last-mile broadband initiatives.

Page last updated on: