Cable Connector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

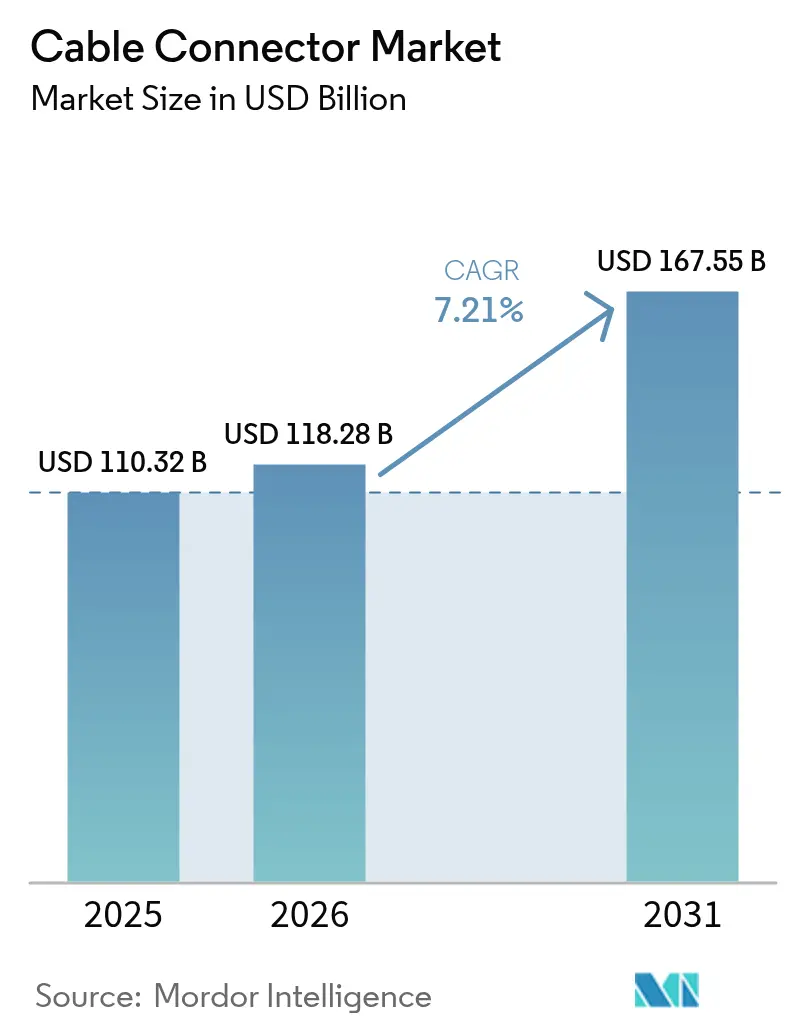

| Market Size (2026) | USD 118.28 Billion |

| Market Size (2031) | USD 167.55 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

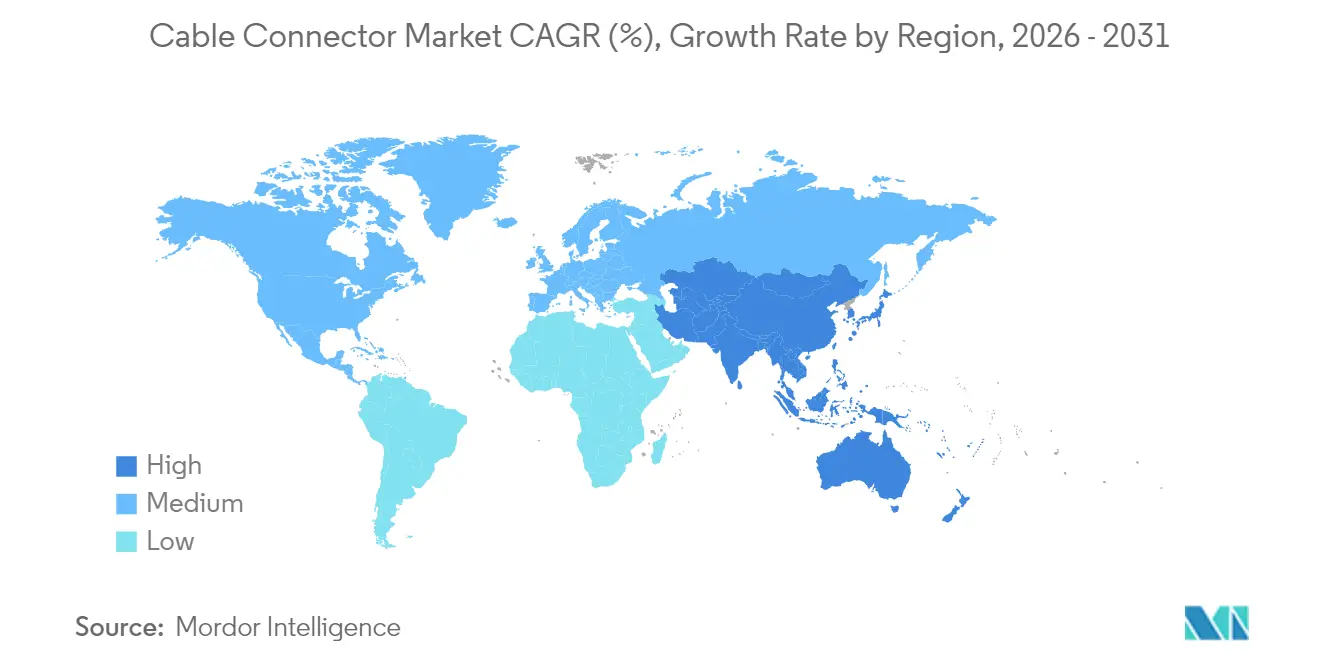

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

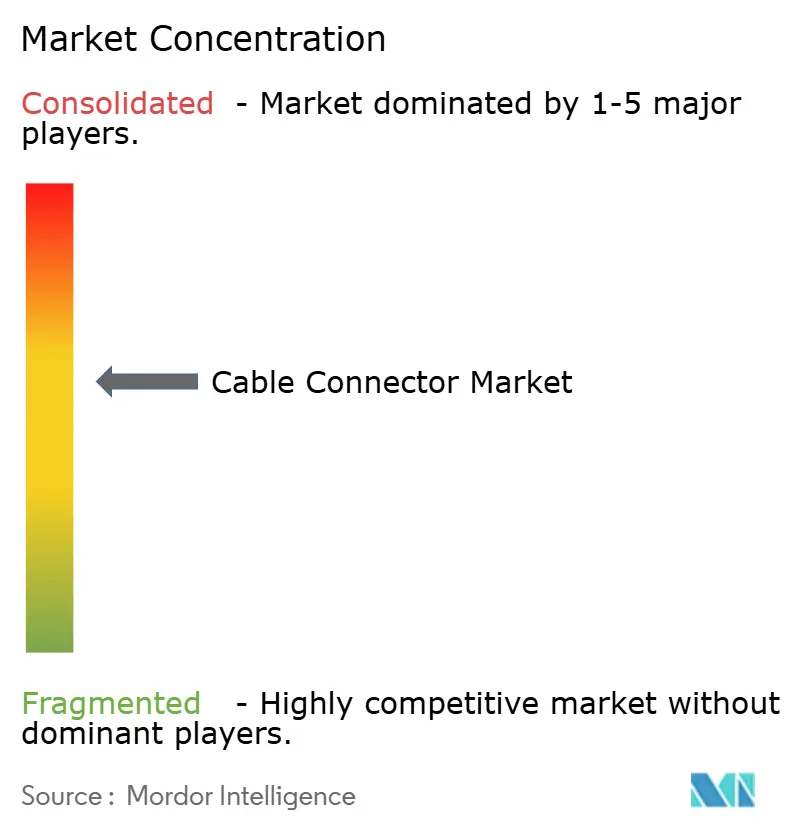

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cable Connector Market Analysis by Mordor Intelligence

The cable connector market size is expected to grow from USD 110.32 billion in 2025 to USD 118.28 billion in 2026 and is forecast to reach USD 167.55 billion by 2031 at 7.21% CAGR over 2026-2031. Current expansion reflects a decisive swing toward higher-value, technically advanced connector solutions that sustain pricing power even when copper and precious-metal costs remain volatile. Growth momentum stems from simultaneous 5G roll-outs, electric-vehicle (EV) production scaling, and hyperscale data-center upgrades that mandate ultra-high-speed interconnects. Asia-Pacific holds structural cost and scale advantages, but supply-chain diversification toward North America and Europe is accelerating as geopolitical tension rises. Competitive intensity remains moderate because design complexity, qualification cycles, and patent portfolios temper rapid commoditization, allowing incumbents to defend share while emerging Asian firms pursue cost-led disruption.

Key Report Takeaways

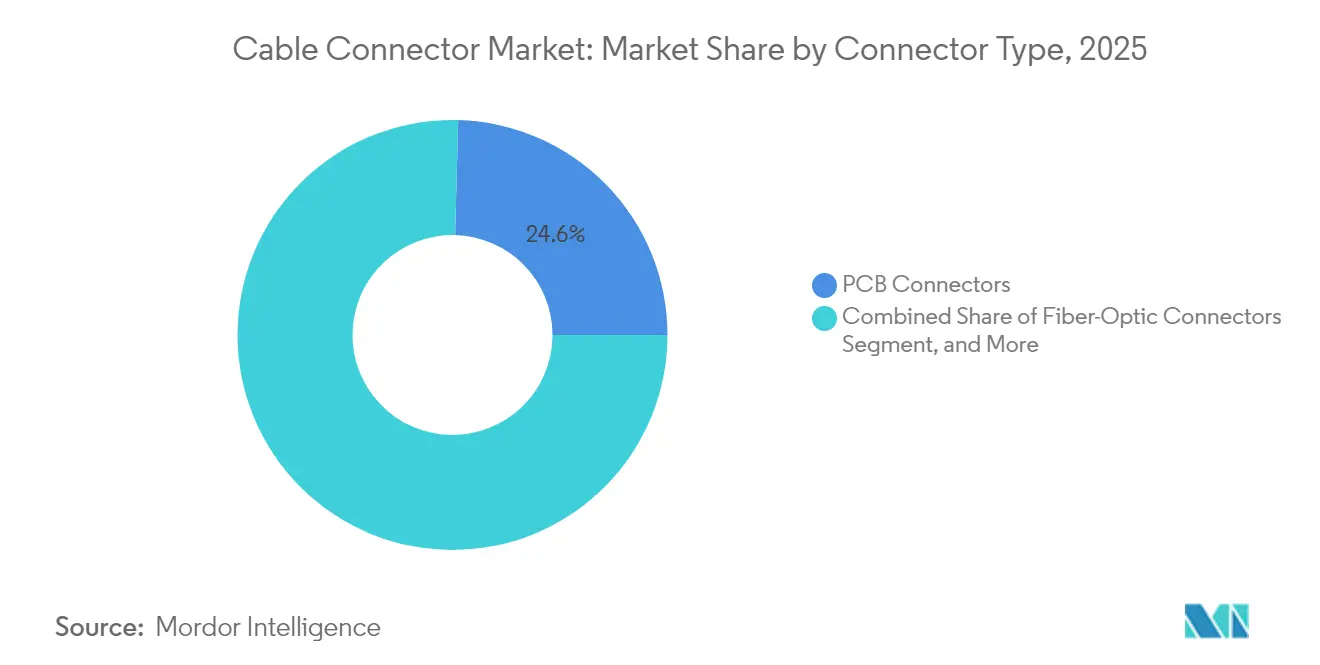

- By connector type, PCB connectors led with 24.58% of cable connector market share in 2025, while power and high-voltage EV connectors posted the fastest 8.52% CAGR through 2031.

- By mounting configuration, board-to-board solutions held 35.62% share of the cable connector market size in 2025, whereas panel or feed-through formats are projected to expand at a 8.78% CAGR.

- By end-user industry, consumer electronics accounted for a 26.92% share of the cable connector market in 2025; automotive and transportation are advancing at an 8.33% CAGR.

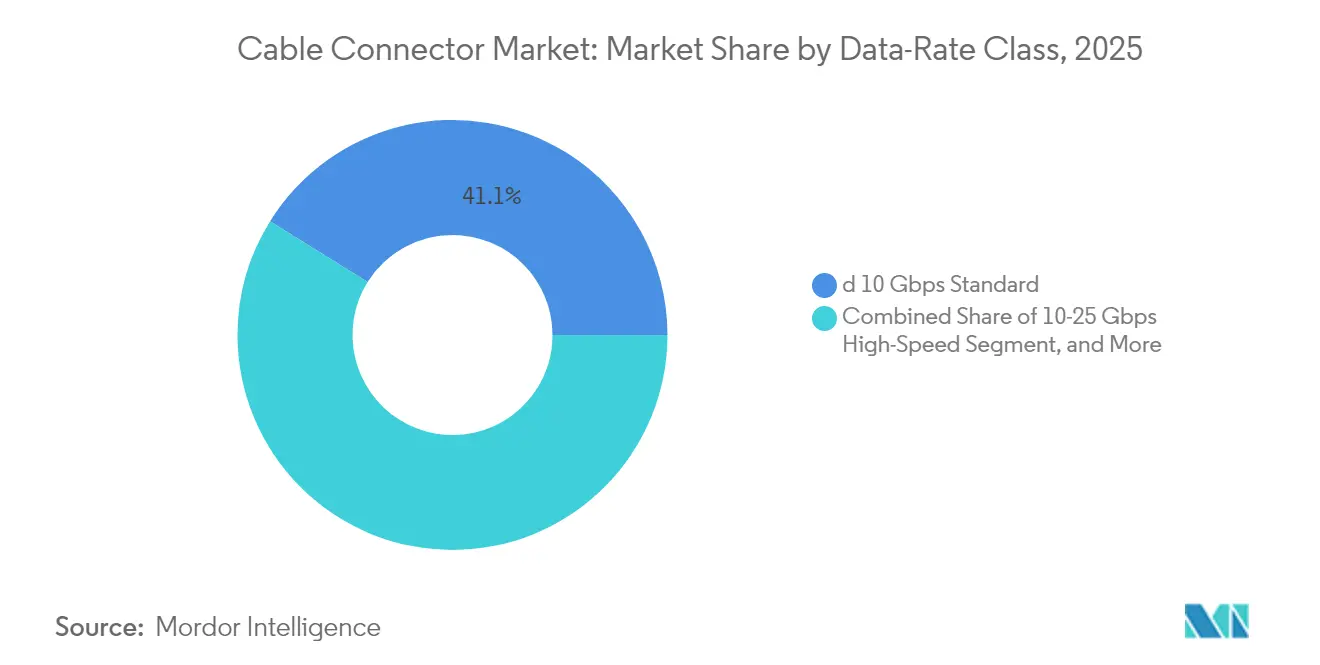

- By data-rate class, standard ≤10 Gbps connectors captured 41.12% share of the cable connector market in 2025, yet ultra-high-speed ≥25 Gbps solutions are growing at an 8.25% CAGR.

- By geography, Asia-Pacific commanded a 42.05% share of the cable connector market in 2025 and continues as the fastest region with an 7.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cable Connector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G roll-out and fiber backhaul densification | +1.8% | Global, APAC and North America | Medium term (2-4 years) |

| Miniaturization of electronics | +1.2% | Global, APAC hubs | Long term (≥ 4 years) |

| Rapid EV production ramp-up | +1.5% | Global, Europe and China | Medium term (2-4 years) |

| Co-packaged optics adoption | +0.9% | North America and APAC | Short term (≤ 2 years) |

| PCIe Gen5/Gen6 12 VHPWR GPU power spec | +0.7% | Global data-center nodes | Short term (≤ 2 years) |

| Government on-shore manufacturing incentives | +0.6% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Roll-out and Fiber Backhaul Densification

Global 5G deployment demands high-frequency connectors that preserve signal integrity at millimeter-wave bands while tolerating outdoor stressors and temperature swings.[1]Ericsson AB, “5G Infrastructure Requirements and Deployment Trends,” ericsson.com Each new 5G macro site integrates three to four times more fiber runs than legacy 4G sites, multiplying optical connector volume. Small-cell densification in urban cores further boosts demand for sealed, IP67/IP68 connectors capable of rapid field installation. Private 5G networks inside factories extend requirements to ruggedized connectors that resist oil mist, vibration, and thermal cycling. As densification accelerates, optical-connector suppliers that can combine low insertion loss with tool-less termination gain pricing leverage.

Miniaturization of Electronics

Smartphones, wearables, industrial sensors, and medical patches now integrate more functionality in tighter envelopes. Pitch distances below 0.5 mm and height profiles under 1 mm are becoming default design rules, pushing connector makers to invest in precision molding, vision-guided pick-and-place, and laser-welded shielding.[2]Samtec Inc., “Fine-Pitch Connector Manufacturing,” samtec.com Advanced cameras and VR headsets demand high-pin-count board-to-board connectors that withstand repeated hinge movement without intermittency. Industrial IoT deployments require similar compactness yet must survive −40 °C to 125 °C temperatures. Vendors that align with mini-LED backlighting and foldable-device roadmaps secure multi-year design wins that lock in demand over product lifecycles.

Rapid EV Production Ramp-up

The shift toward 800 V architectures and 350 A charging currents drives a niche for high-voltage, high-current connectors featuring advanced insulation and thermal paths.[3]Porsche AG, “Taycan 800 V Architecture and Charging Technology,” newsroom.porsche.com ISO 26262 functional-safety mandates introduce interlock and arc-fault detection features that increase part complexity and validation time. Automakers simultaneously pressure suppliers for lighter, space-saving designs to extend vehicle range, prompting exploration of copper-nickel-silicon alloys that offer comparable conductivity at lower weight. Each battery-electric vehicle uses three to four times more connectors than an internal-combustion model, and the cable connector market therefore scales directly with BEV assembly volumes.

Co-Packaged Optics Adoption

Hyperscale operators embrace co-packaged optics (CPO) to cut switch power by roughly 30% while hitting 51.2 Tbps bandwidth targets.[4]Broadcom Inc., “Co-Packaged Optics Solutions for Data Centers,” broadcom.com CPO integrates optical engines beside ASICs, eliminating pluggable optics and calling for bespoke, ultra-short copper interposers with alignment tolerances below 0.1 µm. Connector firms collaborate with switch-silicon vendors from the concept stage, which locks out fast-follower competitors. Designs must contain electromagnetic interference that rises steeply above 56 GHz, spurring investment in proprietary dielectric films and shield geometries. Early movers enjoy premium pricing because qualification demands extend well beyond commodity expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper and precious-metal price volatility | -0.8% | Global | Short term (≤ 2 years) |

| Alignment tolerances below 0.5 mm pitch | -0.6% | Global, high-tech hubs | Medium term (2-4 years) |

| High scrap rates for ultra-fine-pitch SMT | -0.4% | APAC manufacturing | Short term (≤ 2 years) |

| IP-rated sealing cost inflation | -0.3% | Global industrial sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility of Copper and Precious-Metal Prices

Copper traded between USD 8,000 and USD 11,000 per ton during 2024–2025, and gold plating jumped 40% year on year, slicing margins for cost-sensitive standard connectors. Selective plating and alloy substitution offset some swings, but long-term fixed-price contracts expose mid-tier suppliers to losses when raw-material hedges misalign. Larger vendors use scale to negotiate variable pricing clauses, but smaller firms struggle to absorb quarterly shocks. End customers push back on surcharges, slowing pass-through, and elongating cash-conversion cycles.

Alignment Tolerances Below 0.5 mm Pitch

As pitches tighten to meet miniaturization roadmaps, tooling accuracy must hold ±0.05 mm, raising capex by up to 80% compared with conventional lines. Vision inspection, force-feedback insertion testing, and specialized reflow profiles add process steps that extend time-to-volume and lift scrap rates above 7% in first production runs. The learning curve penalizes late entrants, and any latent alignment drift triggers latent field failures, undermining OEM confidence. Resultant warranty reserves and field-service campaigns act as direct hits to operating margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connector Type: Power Formats Accelerate in EV Platforms

The connector-type landscape shows PCB connectors retaining 24.58% cable connector market share in 2025, thanks to their omnipresence across consumer, telecom, and industrial electronics. Revenue in this segment stayed on pace with the overall cable connector market at a mid-single-digit CAGR, aided by shrinking pitch innovations and higher pin densities. Circular and rectangular connectors maintained solid positions in aerospace and defense as reliability certifications justify premium pricing and lengthy contracts. Fiber-optic interfaces prospered alongside data-center and 5G fronthaul investments, where reduced insertion loss and outdoor durability attract infrastructure spending. I/O and RF coaxial designs reinforced their niches in test equipment and instrumentation, where repeatability counts more than sheer volume. The standout growth story resides in power and high-voltage EV connectors, projected at an 8.52% CAGR through 2031. They benefit from every new battery-electric platform that mandates 800 V architectures and ultrafast charging demand, creating the fastest-moving pocket of the cable connector market.

Global OEM qualification criteria demand arc-suppression, touch-proof enclosures, and thermocouple integration to monitor junction temperatures. These design layers inflate the average selling price even as they limit qualified supplier pools. Established automotive-grade connector specialists leverage process technologies such as cavity-free over-molding to minimize resistive losses, while new entrants target cost-down variants for two-wheel electrification in India and Southeast Asia. Segment leaders that can harmonize international standards like IEC 62196 with regional charging protocols win multi-year sourcing deals. The combined effect positions the power connector segment as the largest contributor to incremental cable connector market size over the forecast horizon.

By Mounting Configuration: Panel Solutions Win at the Edge

Board-to-board assemblies dominated 35.62% of the cable connector market size in 2025, underpinned by complex multi-board electronics architectures that characterize mobile devices, laptops, and advanced driver-assistance systems. OEMs favor ultra-low-profile stacking connectors that survive torsional stress during drop events. Wire-to-board variants persist in markets where field-service interchangeability trumps internal space constraints, such as factory automation panels. Cable-to-cable links excel in modular robotic arms and renewable-energy combiner boxes where re-routing flexibility is paramount.

Panel or feed-through solutions, while representing a smaller base, chart a 8.78% CAGR into 2031 as edge-computing cabinets, outdoor 5G radios, and battery-storage enclosures require hermetic seals and rapid mating. IP67 and IP68 compliance add material layers and gasketing complexity that increase ticket prices. Hybrid power-and-signal feed-through models enable single-hole installations that trim labor time during tower climbs or skid-mount deployments. Vendors that pre-integrate EMC shielding and condensation venting capture specification wins among telecom tower OEMs. Consequently, panel configurations stand out as share-gainers in the cable connector market.

By End-User Industry: Vehicle Electrification Ups the Stakes

Consumer electronics held 26.92% share in 2025, buoyed by unit volumes in smartphones, tablets, and wearables. However, price sensitivity and continual miniaturization erode per-unit connector revenue. IT and telecom infrastructure purchases intensify demand for QSFP-DD and OSFP modules at 25 Gbps lanes and higher, catalyzing growth in high-speed board-edge connectors that complement fiber modules. Industrial automation requires metal-shell M12 and M8 connectors with vibration resistance, helping suppliers preserve margins when mass-market handset contracts tighten. Energy, power, and subsea projects order stainless-steel or titanium variants able to withstand pressure and corrosion, often at ten times the average market pricing.

Automotive and transportation surfaces as the fastest movers with an 8.33% CAGR. Each battery pack integrates thousands of signal and power terminals that monitor cell voltages, coolant-pump speeds, and inverter status. High-speed telematics, lidar systems, and in-cabin infotainment add separate connector stacks. Asia-Pacific assemblers press for cost-effective yet reliable connectors, while European luxury brands stipulate rigorous salt-spray and thermal-shock tests. Vendors proficient in zero-defect capabilities and automatic optical inspection present compelling value propositions, propelling automotive volumes to drive net new cable connector market size.

By Data-Rate Class: Ultra-High-Speed Lifts ASP

Standard ≤10 Gbps interfaces remained the volume leader at 41.12% share in 2025. These products power legacy Ethernet, USB 3.x, and HDMI 2.1 ecosystems where mature tooling yields competitive cost structures. High-speed 10–25 Gbps designs address enterprise storage, edge routers, and surveillance backhaul, often combining twin-ax cabling with low-profile mezzanine connectors to balance signal integrity and thermal dissipation.

Ultra-high-speed ≥25 Gbps formats command the steepest ASP uplift and post an 8.25% CAGR as 400G and 800G switch upgrades accelerate inside hyperscale data centers. PCIe Gen5 and Gen6 workloads draw on 12 VHPWR connectors for AI accelerator cards, driving robust orders among Tier-1 cloud providers. Signal-integrity challenges increase exponentially beyond 56 Gbps PAM4, requiring coherent copper-foil structures and selective plating to mitigate skin-effect losses. Suppliers with in-house simulation and test labs enjoy an entry barrier that supports healthy gross margins despite material inflation. Overall, speed class migration functions as a structural catalyst for premium-priced cable connector market subsegments.

By Material: Copper-Nickel-Silicon Gains Traction

Copper-alloy connectors accounted for a 36.22% share in 2025 owing to favorable conductivity and entrenched supply chains. Gold-over-nickel plating ensures oxidation resistance in data-center operating environments, although price spikes pressure bills of material. Aluminum and lightweight alloys notch incremental share in aerospace and EV domains, where every gram saved translates to range extension or fuel savings.

Engineering plastics such as PBT and LCP replace metal housings in moisture-tolerant or RF-transparent applications, with polymer scientists adapting flame-retardant grades that pass UL 94 V-0 while resisting reflow-oven shrinkage. Precious-metal-plated products stay mission-critical for spaceflight and surgical devices despite price fluctuations. The fastest-growing pocket is copper-nickel-silicon alloy, projected at a 8.84% CAGR, delivering better stress relaxation and spring properties than phosphor-bronze at comparable conductivity. Automakers embrace the alloy in 800 V battery connectors to keep contact resistance low across half a million load cycles. Resulting adoption lifts material innovation into an influencer role on the future cable connector market size.

Geography Analysis

Asia-Pacific retained a 42.05% share in 2025 as China, Japan, and South Korea clustered semiconductor, smartphone, and EV production in integrated supply ecosystems. Regional CAGR is forecast at 7.88%, buoyed by domestic 5G base-station rollouts and state incentives for local EV brands. Growing regional wage costs and geopolitical uncertainty prompt multinationals to add second-source capacity in Vietnam and India, yet proximity advantages and established tooling networks continue to anchor large production runs within China. Governments add grants for indigenous connector R&D to climb the value chain and reduce import reliance.

North America ranks second in revenue on the back of data-center construction that supports AI and machine-learning services. Hyperscale operators stipulate 800G optical links and 12 VHPWR power delivery, pushing local contract manufacturers to qualify new connector lines. The United States CHIPS and Science Act subsidizes on-shore tooling for high-speed interconnects, while Canada’s automotive clusters pivot toward EV assembly that consumes large numbers of sealed, high-current connectors. Mexico absorbs near-shored assembly volumes as OEMs hedge East-Asian exposure.

Europe posts steady expansion driven by automotive electrification and industrial automation investment. Germany’s machine-tool builders specify M12 and Push-Pull connectors that withstand 10 g vibration profiles, sustaining premium orders for ruggedized formats. The European Union’s strategic-autonomy policies channel grants toward connector manufacturing, boosting mid-size suppliers in Italy and Poland. United Kingdom data-center expansion and offshore wind installations lift demand for fiber-optic and subsea connectors, respectively, giving diverse avenues for cable connector market growth.

Competitive Landscape

The cable connector market remains moderately fragmented because no single vendor serves every application across voltage, speed, and environmental categories. TE Connectivity, Amphenol, and Molex leverage global tooling networks, vertical integration, and thousands of active patents to defend design-win pipelines, yet their cumulative share still trails the 80% mark that would signal high concentration. Specialists such as Hirose or Samtec win sockets in ultra-fine-pitch and high-speed niches by coupling agile R&D with dedicated customer-engineering teams.

Competitive strategy tilts toward automation investment that trims labor cost volatility and improves first-pass yield in pitches below 0.4 mm. Leading firms deploy in-line X-ray inspection and closed-loop plating thickness control to hit zero-defect targets sought by automotive OEMs. Corporate acquisitions intensify; Amphenol’s 2025 buyout of Carlisle Interconnect widened its aerospace footprint and pulled harsh-environment know-how into its catalog.

Partnerships also surface as switch silicon, optics, and cooling architectures converge. Foxconn Interconnect Technology’s joint program with NVIDIA exemplifies GPU-specific power interconnect co-development that brings in cooling channels and sense pin logic. White-space opportunities remain in 1.6T optical connectors, 800 V EV interfaces, and hydrogen-ready power connectors, each demanding fresh material science and standards participation. Suppliers able to combine cross-disciplinary IP gather pricing and margin advantages that shelter them from commodity headwinds.

Cable Connector Industry Leaders

Amphenol Corporation

TE Connectivity Limited

Molex LLC

Aptiv PLC

Yazaki Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: TE Connectivity announced a USD 150 million investment to expand high-voltage connector manufacturing in Mexico targeting 800 V EV systems.

- January 2025: Amphenol completed the USD 2.1 billion acquisition of Carlisle Interconnect Technologies, strengthening aerospace and military interconnect portfolios.

- December 2024: Molex unveiled a new co-packaged optics connector platform rated for 51.2 Tbps switching.

- November 2024: Hirose opened a USD 80 million plant in Vietnam focused on ultra-fine-pitch connectors for consumer electronics and automotive uses.

Global Cable Connector Market Report Scope

Cables and connectors are connectivity devices that are used to transmit data, signals, and power supply for electronic devices across different industries. Connectors are also referred to as input-output connectors and form the interface for linking electronic devices with the help of cables.

The report offers a comprehensive analysis of the demand and supply as well as current and future trends of the cable connectors market. The studied market has been segmented by type, end-user vertical, and geography. The study also includes the impact assessment of COVID-19 on the cable connectors market.

| PCB Connectors |

| Circular and Rectangular Connectors |

| Fiber-Optic Connectors |

| I/O and RF/Coaxial Connectors |

| Power and High-Voltage EV Connectors |

| Board-to-Board |

| Wire-to-Board |

| Cable-to-Cable |

| Panel/Feed-through |

| IT and Telecom |

| Automotive and Transportation |

| Consumer Electronics |

| Industrial Automation |

| Energy, Power and Sub-sea |

| Less than 10 Gbps Standard |

| 10-25 Gbps High-Speed |

| Greater than equal to 25 Gbps Ultra-High-Speed / PAM4 |

| Copper-Alloy |

| Aluminum and Lightweight Alloys |

| Engineering Plastics and Composites |

| Precious-Metal-Plated (Gold, Palladium) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Connector Type | PCB Connectors | |

| Circular and Rectangular Connectors | ||

| Fiber-Optic Connectors | ||

| I/O and RF/Coaxial Connectors | ||

| Power and High-Voltage EV Connectors | ||

| By Mounting Configuration | Board-to-Board | |

| Wire-to-Board | ||

| Cable-to-Cable | ||

| Panel/Feed-through | ||

| By End-user Industry | IT and Telecom | |

| Automotive and Transportation | ||

| Consumer Electronics | ||

| Industrial Automation | ||

| Energy, Power and Sub-sea | ||

| By Data-Rate Class | Less than 10 Gbps Standard | |

| 10-25 Gbps High-Speed | ||

| Greater than equal to 25 Gbps Ultra-High-Speed / PAM4 | ||

| By Material | Copper-Alloy | |

| Aluminum and Lightweight Alloys | ||

| Engineering Plastics and Composites | ||

| Precious-Metal-Plated (Gold, Palladium) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the cable connector market in 2026?

The cable connector market size stands at USD 118.28 billion in 2026 with a 7.21% CAGR outlook to 2031.

Which connector type grows fastest through 2031?

Power and high-voltage EV connectors record the quickest advance at an 8.52% CAGR as electric-vehicle adoption scales.

Why is Asia-Pacific dominant in cable connector output?

The region concentrates electronics and EV manufacturing and captures 42.05% market share, supported by integrated supply chains and 5G deployment momentum.

What is driving ultra-high-speed connector demand?

AI and machine-learning servers plus 800G network upgrades lift ?25 Gbps connector volumes at an 8.25% CAGR.

How do copper price swings impact connector suppliers?

Copper and gold volatility can shave up to 0.8 percentage points off forecast CAGR as material costs reach 25% of assembly expenses.

Which companies lead current market innovation?

TE Connectivity, Amphenol, Molex, Hirose, and Samtec steer technology through investments in high-voltage EV lines, co-packaged optics, and 224 G signal-integrity designs.

Page last updated on: