Structural Electronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

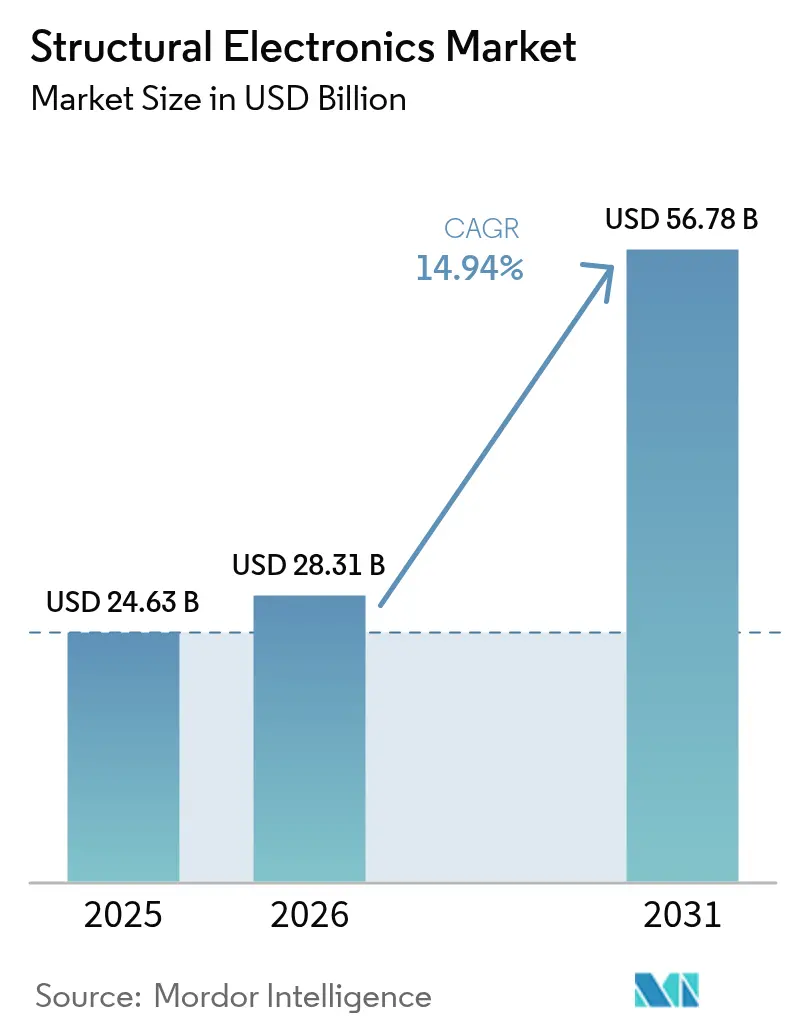

| Market Size (2026) | USD 28.31 Billion |

| Market Size (2031) | USD 56.78 Billion |

| Growth Rate (2026 - 2031) | 14.94% CAGR |

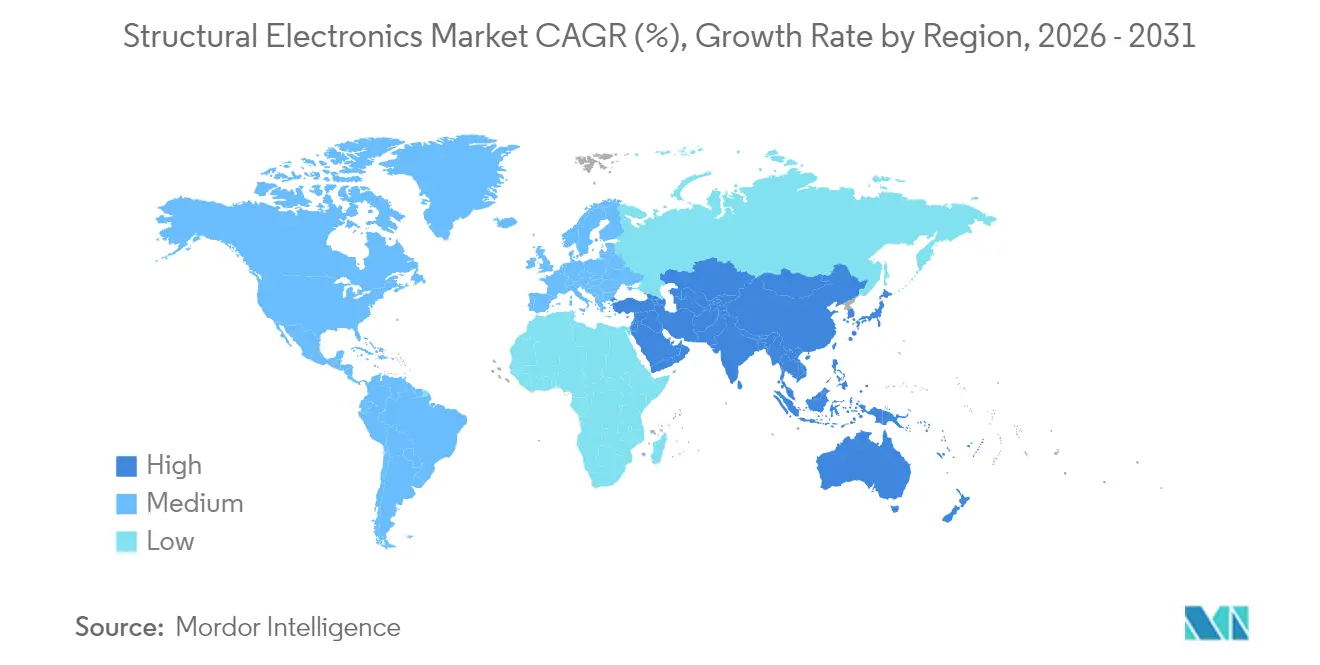

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

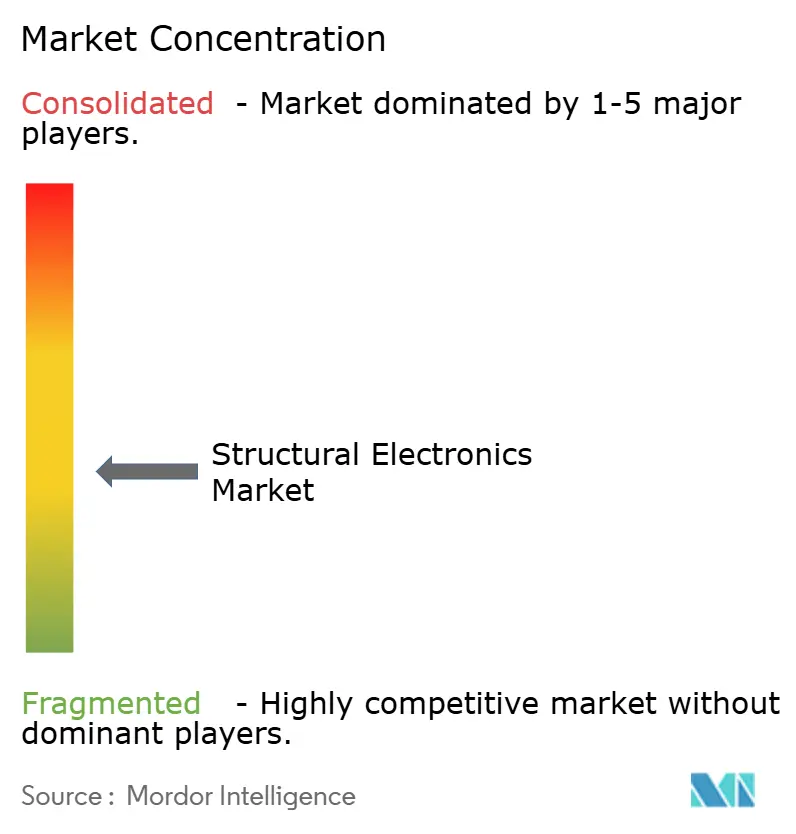

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Structural Electronics Market Analysis by Mordor Intelligence

The structural electronics market size was valued at USD 24.63 billion in 2025 and estimated to grow from USD 28.31 billion in 2026 to reach USD 56.78 billion by 2031, at a CAGR of 14.94% during the forecast period (2026-2031). This acceleration reflects fast-moving vehicle lightweighting mandates, semiconductor policy incentives, and fresh breakthroughs in 3-D in-mold electronics that embed circuitry directly into load-bearing parts. Automotive manufacturers now fold sensor skins and structural batteries into cabin panels to trim weight and extend electric-vehicle range, while Asia-Pacific consumer-electronics plants scale volume production of curved, touch-activated housings. Regulations such as the European Chips Act and the U.S. CHIPS and Science Act pump capital into advanced packaging hubs that simplify structural integration. Geographic growth remains anchored in Asia-Pacific manufacturing depth, but defense and smart-infrastructure projects in the Middle East lift future demand.

Key Report Takeaways

- By application, automotive captured 41.65% of the structural electronics market share in 2025, whereas healthcare wearables are projected to post the fastest 16.05% CAGR to 2031.

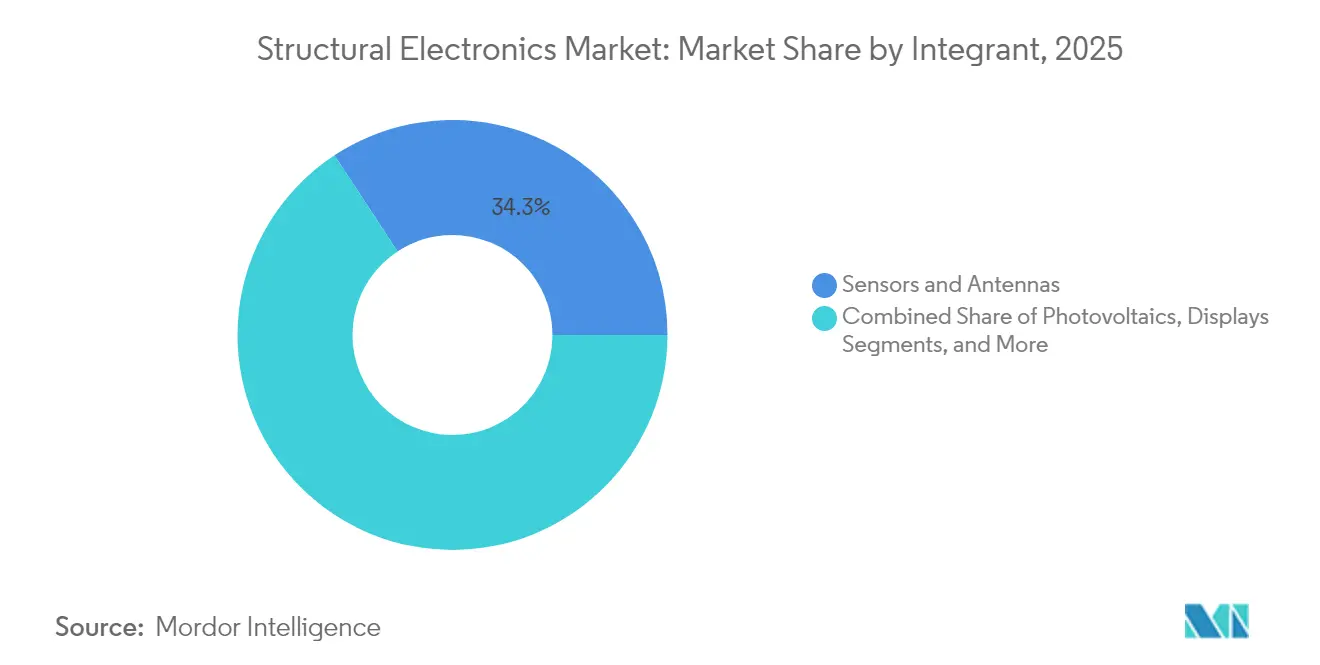

- By integrant, sensors held 34.25% share of the structural electronics market size in 2025, while photovoltaics are set to grow at a 16.88% CAGR through 2031.

- By manufacturing technology, in-mold electronics led with 50.72% revenue share in 2025; additive manufacturing is advancing at an 17.46% CAGR to 2031.

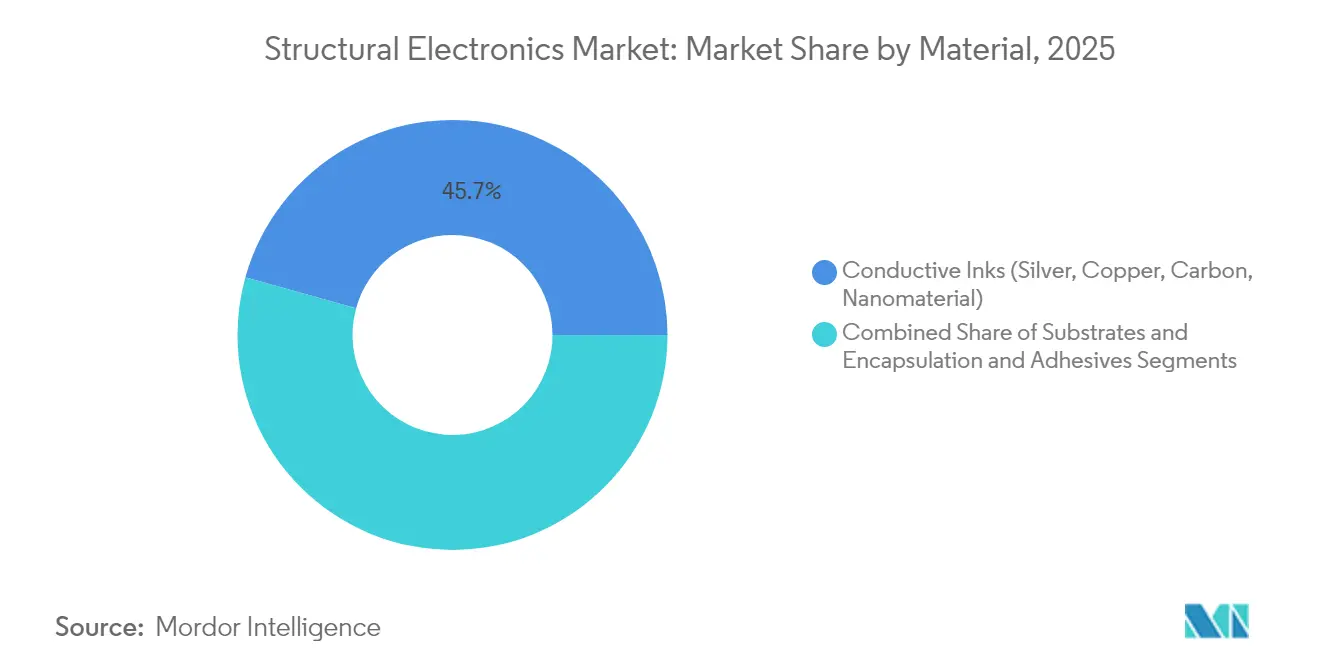

- By material, conductive inks accounted for 45.68% of revenue in 2025, whereas nanomaterial-based inks are slated to expand at a 18.25% CAGR through 2031.

- By geography, Asia-Pacific contributed 37.35% of 2025 revenue, while the Middle East and Africa region is forecast to register a 15.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Structural Electronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive lightweighting and EV-centric cabin electronics surge | +2.8% | Europe, North America | Medium term (2-4 years) |

| Mass adoption of 3-D in-mold electronics in Asia-Pacific consumer devices | +2.5% | Asia-Pacific, global | Short term (≤ 2 years) |

| FAA push for integrated sensor skins in composite airframes | +1.9% | North America, Europe | Long term (≥ 4 years) |

| Printed photovoltaics for battery-less IoT nodes in smart buildings | +1.7% | Global | Medium term (2-4 years) |

| Edge-AI wearables driving stretchable structural circuits | +2.1% | Global | Short term (≤ 2 years) |

| Defense demand for conformal antennas and smart surfaces | +1.4% | North America, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Automotive light weighting and EV-centric cabin electronics surge

European automakers face firm fleet-emission rules that prioritize lighter vehicles equipped with integrated power electronics. Sinonus AB’s carbon-fiber structural battery shows a 70% range boost coupled with 50% weight reduction, illustrating how a single composite part can both store energy and carry mechanical loads. The design also mitigates thermal-runaway concerns by replacing flammable liquid electrolytes with semi-solid chemistries. Automakers such as Volkswagen link these batteries with silicon-carbide inverters from onsemi to shrink component count and raise drivetrain efficiency. The debate around steel versus aluminum gigacasting further underscores the value of embedding circuitry into any structural material. The result is a rapid uptick in structural electronics market adoption across chassis, doors, and instrument panels.

Mass adoption of 3-D in-mold electronics in Asia-Pacific consumer devices

Consumer-device contract manufacturers in China, South Korea, and Vietnam are standardizing 3-D in-mold electronics that combine conductive inks, films, and resins in a single molding step. TactoTek’s injection-molded structural electronics (IMSE) process has verified a 60% drop in greenhouse-gas emissions and 70% less plastic usage versus traditional assembly. Covestro’s Makrofol polycarbonate films enable touch lighting and haptic feedback inside ultrathin shells. Regional research, such as organic electrochemical transistors from the University of Hong Kong, drives the next wave of wearable, on-sensor computing. Southeast Asia’s PCB sector, already above USD 2 billion in output, supplies multilayer backplanes that mate with these structural housings. Accelerated tooling cycles support product launches in smartphones, hearables, and smart-home hubs, lifting the structural electronics market across personal electronics.

FAA push for integrated sensor skins in composite airframes

New FAA system-safety rules issued in September 2024 make continuous structural-health monitoring a certification baseline for composite transport aircraft. Boeing’s USD 4.7 billion purchase of Spirit AeroSystems centers on embedding fiber-optic and piezoelectric sensors during lay-up to watch strain in real time.[1]Boeing, “Boeing to Acquire Spirit AeroSystems,” investors.boeing.com Earlier FAA approval of comparative-vacuum monitoring proved the viability of such embedded systems on commercial jets. NASA materials programs have validated sensor integration without weight penalties, enabling a shift away from manual inspections. Airlines anticipate lower unscheduled maintenance and higher fleet utilization, which accelerates demand for structural electronics market innovations in aerospace cabins, wings, and nacelles.

Printed photovoltaics for battery-less IoT nodes in smart buildings

Building-automation suppliers increasingly select dye-sensitized and perovskite photovoltaic films that harvest indoor light to power wireless sensors. Recent laboratory cells have reached 38% efficiency under fluorescent illumination. MIT researchers showed that flexible perovskites quintuple the RFID tag range while eliminating batteries. Hybrid harvesters combining PV with thermoelectric generators now deliver 192.5 µW under mixed-lighting, enough for Bluetooth beacons. Analog Devices’ LTC3109 power manager conditions the sub-1V outputs, letting facility managers deploy thousands of nodes without battery swaps. Solar-powered pilot projects in European office towers confirm reduced operating costs and higher occupant comfort, feeding mid-term structural electronics market growth in smart-building envelopes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex qualification cycles for structural electronics in aerospace | -1.8% | Global, chiefly North America and Europe | Long term (≥ 4 years) |

| Limited cycle-time throughput of additive-manufacturing lines | -1.5% | Global | Medium term (2-4 years) |

| Delamination risks in high-heat polymer substrates | -1.2% | Global | Short term (≤ 2 years) |

| Shortage of conductive nanomaterial supply outside Asia | -2.1% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of conductive nanomaterial supply outside Asia

Carbon-nanotube inks and pastes are concentrated in a handful of Chinese plants that together command over 40% of global output. Hurricanes that disrupted high-purity quartz in North Carolina exposed parallel weaknesses in raw-material chains essential for semiconductor substrates. Recent CNT scale-up announcements from U.S. and European producers remain short of demand growth projections. Automotive and aerospace buyers consequently face longer lead times and price spikes, constraining structural electronics market expansion until diversified sourcing becomes available.

Complex qualification cycles for structural electronics in aerospace

DO-254 hardware assurance and AC 20-107B material controls push development timelines for next-generation airframe electronics to 24–36 months and require USD 50–100 million in test spending Federal Aviation Administration. Programs must validate parts across –65 °C to 85 °C and 95% humidity, adding cost and risk. Boeing’s drive to insource fuselage production highlights how certification delays ripple through supply chains. Added paperwork for integrated aircraft-health-management data flows under AC 43-218 further complicates entry. These factors cool near-term uptake of structural electronics market solutions within commercial aviation, despite long-term efficiency benefits

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Integrant: Sensors underpin current demand while photovoltaics unlock the next wave

The sensor and antenna category contributed 34.25% revenue in 2025, buoyed by mandates for advanced driver-assistance systems and aircraft safety monitoring. Flight composite panels now embed fiber-optic arrays, whereas passenger-vehicle dashboards integrate radar and capacitive touch in one molded insert. Photovoltaics post the strongest 16.88% CAGR through 2031, driven by flexible perovskite modules that curve around building interiors and wearable tags. Structural integration allows power generation without separate housing, shrinking assembly cost, and opening new applications in asset tracking and indoor agriculture.

Structural batteries and micro-super-capacitors move beyond prototypes, illustrated by MXene ink devices delivering 611 F cm-3 volumetric capacitance. Displays follow automotive styling trends toward continuous curved surfaces enabled by OLED and micro-LED films. Interconnect materials confront copper volatility yet gain from silver-nanowire and MXene alternatives that sustain conductivity in bendable formats. Together, these shifts expand the structural electronics market as designers combine sensing, energy, and display functions within a single laminate.

By Manufacturing Technology: In-mold electronics dominate as additive processes accelerate

In-mold electronics captured 50.72% revenue in 2025 by fusing films, inks, and resin into lightweight parts that ship ready-to-install. Automotive door trims now host back-lit controls without separate PCBs, cutting wire harness weight. Consumer wearables adopt the same process for IP68-rated casings. Additive manufacturing records the highest 17.46% CAGR, supported by DARPA’s AMME program that 3-prints complex micro-circuits directly onto three-dimensional substrates. Aerosol-jet printing of MXene inks scales energy-dense capacitors, while multiphoton lithography pioneers printable organic bioelectronics.

Screen and flexographic presses remain cost-effective for large-area heaters and antennas on appliance panels. Inkjet platforms supply fine-feature prototypes before tooling commits to mass molding. This technology spreads, widening entry options, accelerating structural electronics market adoption in both high-volume and bespoke production runs.

By Material: Conductive inks still lead, but nanomaterials dictate innovation

Conductive inks held 45.68% revenue in 2025 on the back of mature silver-flake and carbon formulations. Automakers rely on these pastes for capacitive sliders embedded into center consoles. Price pressure and resource security spur equipment makers to test carbon-nanotube and graphene blends that lift conductivity 10% while cutting silver usage. Nanomaterial-based inks post a 18.25% CAGR to 2031, led by MXene, CNT, and graphene hybrids that satisfy low-temperature sintering and high-flex cycles.

Substrate innovation keeps pace, with Makrofol films tolerating automotive thermal cycling from -40°C to 125°C and maintaining dimensional stability. Adhesives suppliers develop thermally conductive yet flexible chemistries that dissipate localized heat without delamination. These advances safeguard device reliability and keep the structural electronics market expanding into harsher environments.

By Application: Automotive remains dominant while healthcare wearables surge

Automotive retained 41.65% revenue in 2025 as OEMs embed structural batteries and sensor-laden interior trims that shave curb weight and extend driving range. Volkswagen’s silicon-carbide inverter strategy complements this push by reducing mass and boosting power-train efficiency. Regulatory demand for hands-off ADAS functions sustains sensor integration across vehicle pillars and bumpers, firming the structural electronics market base.

Healthcare wearables achieve a 16.05% CAGR, thanks to self-assembling liquid-metal conductors that stay conductive under strain. Stretchable electronic strips sewn into textiles now host full circuits instead of simple interconnects, enabling continuous glucose, temperature, and motion monitoring. Aerospace and defense buyers pursue conformal antennas that streamline airframes and smart surfaces that change radar signatures, while consumer electronics brands exploit seamless touch and lighting on curved products.

Geography Analysis

Asia-Pacific delivered 37.35% of 2025 revenue by virtue of high-volume semiconductor, PCB, and molding ecosystems. China drives vertical integration, while Thailand and Malaysia add capacity that feeds global supply. Japan supplies over half the world’s multilayer ceramic capacitors, and partnerships such as Murata with QuantumScape diversify into solid-state battery ceramics.

Europe’s structural electronics market gains from automotive electrification milestones and EUR 80 billion (USD 94.06 billion) in Chips Act funds, targeting a 20% global semiconductor share by 2030. German OEMs refine giga casting with embedded circuits, whereas French construction firms pilot PV-powered sensor skins on retrofit facades.

The Middle East and Africa record the fastest 15.12% CAGR, propelled by defense modernization and smart-city rollouts. UAE’s EDGE Group explores AI-enabled satellite links that demand conformal antennas and lightweight power sources. Local governments entice suppliers with offset programs that seed domestic assembly lines, yet the region still imports most nanomaterials, a gap that could temper late-decade growth.

North America keeps momentum through aerospace projects and fresh CHIPS Act subsidies for advanced packaging foundries. Boeing’s acquisition of Spirit targets tighter integration of sensor-ready fuselage sections. Federal rules now favor home-grown supply, nudging structural electronics market participants to co-locate material, printing, and molding capabilities.

Competitive Landscape

The market remains moderately fragmented. Technology specialists such as TactoTek leverage IMSE patents to provide turnkey design-to-production services that cut parts count and carbon footprint by 60%. Large incumbents pursue vertical integration: Boeing internalized composite fuselage fabrication to align quality and accelerate sensor embedding. Material suppliers forge alliances, for instance, DuPont with Zhen Ding to co-develop high-density interposer laminates for structural use.

Additive-manufacturing entrants backed by DARPA funds accelerate inks and printers that output aerospace-grade circuits in a single build.[4]Military & Aerospace Electronics, “DARPA to Push Bounds of Additive Manufacturing,” militaryaerospace.com Consumer-electronics giants like Meta patent flexible interconnect tapes that fan out cameras along curved housings, hinting at future AR headsets. Start-ups commercialize stretchable sensors for digital health, partnering with garment brands to secure route-to-market. Competition therefore spans materials, manufacturing platforms, and turn-key system providers, keeping pricing pressure moderate and innovation pace high.

Structural Electronics Industry Leaders

TactoTek Oy.

Panasonic Corporation

Canatu Oy

Neotech AMT GmbH

Pulse Electronics (a Yageo Company)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: TSMC announced a USD 165 billion U.S. expansion that includes three fabs and advanced-packaging lines.

- February 2025: 3M joined the US-JOINT consortium to open a Silicon Valley R&D hub for advanced packaging.

- February 2025: Molex released Percept current sensors with 86% weight reduction for electric-mobility platforms.

- January 2025: Infineon started construction of a Thai backend facility to boost power-module output.

Global Structural Electronics Market Report Scope

The term, structural electronics (SE), refers to a next-generation based electronics technology, which involves the printing of functional electronic circuitries, across irregular-shaped architectures. SE is expected to replace bulky load-bearing structures within a circuitry with smart electronic components that can conform to complex shapes for ensuring optimum space utilization. SE offers different and better ways of implementing electronic functionalities into the products.

| Photovoltaics |

| Batteries/Super-capacitors |

| Sensors and Antennas |

| Displays (OLED/Micro-LED) |

| Conductors and Interconnects |

| In-Mold Electronics (IME) |

| Additive Manufacturing/3-D Printing |

| Aerosol Jet and Inkjet Printing |

| Screen/Flexographic Printing |

| Conductive Inks (Silver, Copper, Carbon, Nanomaterial) |

| Substrates (Polymer, Glass, Composite, Thermoset) |

| Encapsulation and Adhesives |

| Automotive - Interior and Exterior |

| Aerospace and Defense - Airframe, Smart Skins |

| Consumer Electronics - Whitegoods and Handhelds |

| Healthcare/Medical Devices |

| Industrial and Building Automation |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics (Denmark, Sweden, Norway, Finland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Gulf Cooperation Council Countries |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Integrant | Photovoltaics | |

| Batteries/Super-capacitors | ||

| Sensors and Antennas | ||

| Displays (OLED/Micro-LED) | ||

| Conductors and Interconnects | ||

| By Manufacturing Technology | In-Mold Electronics (IME) | |

| Additive Manufacturing/3-D Printing | ||

| Aerosol Jet and Inkjet Printing | ||

| Screen/Flexographic Printing | ||

| By Material | Conductive Inks (Silver, Copper, Carbon, Nanomaterial) | |

| Substrates (Polymer, Glass, Composite, Thermoset) | ||

| Encapsulation and Adhesives | ||

| By Application | Automotive - Interior and Exterior | |

| Aerospace and Defense - Airframe, Smart Skins | ||

| Consumer Electronics - Whitegoods and Handhelds | ||

| Healthcare/Medical Devices | ||

| Industrial and Building Automation | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics (Denmark, Sweden, Norway, Finland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Gulf Cooperation Council Countries | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the structural electronics market?

The structural electronics market size stands at USD 28.31 billion in 2026.

How fast will the market grow to 2031?

Revenue is forecast to rise to USD 56.78 billion, representing a 14.94% CAGR through 2031.

Which technology is expanding the quickest?

Additive manufacturing shows the fastest 17.46% CAGR as 3-D printing begins to fabricate complex circuits directly on structural parts.

What is the main barrier in aerospace adoption?

Lengthy DO-254 and AC 20-107B qualification cycles add up to three years and tens of millions of dollars in testing before new structural electronics can fly.

Page last updated on: