IT Connector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.14 Billion |

| Market Size (2031) | USD 10.58 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

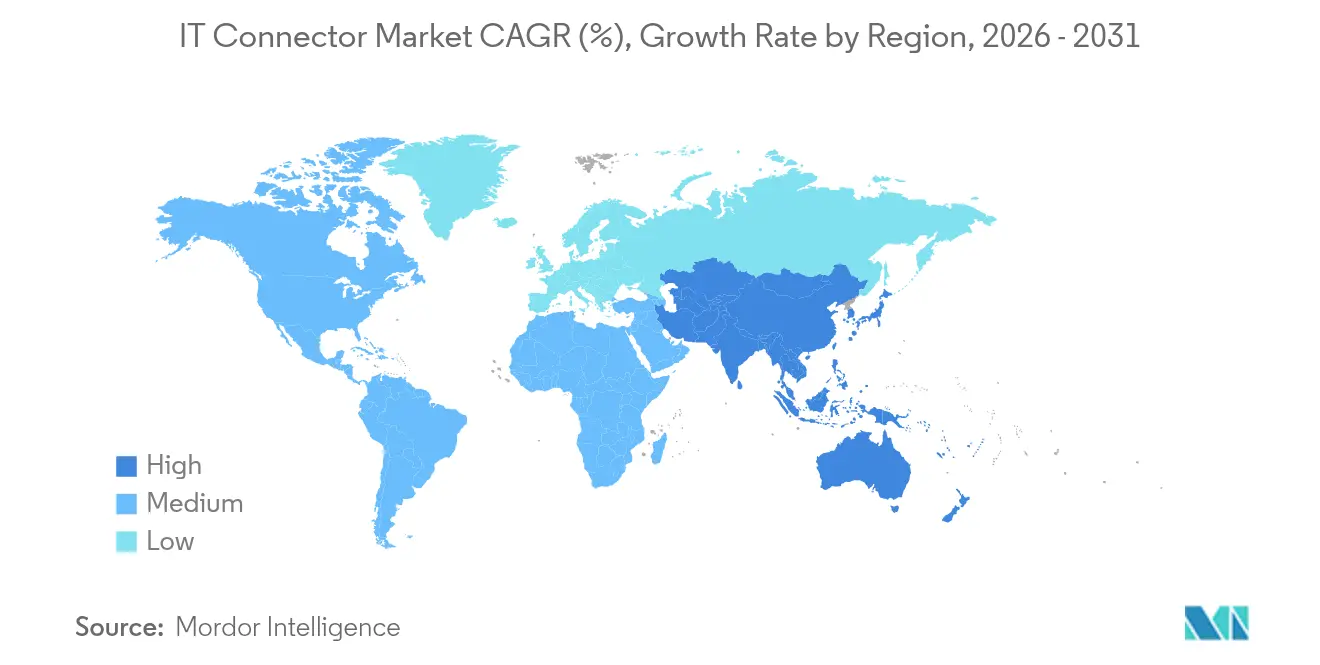

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

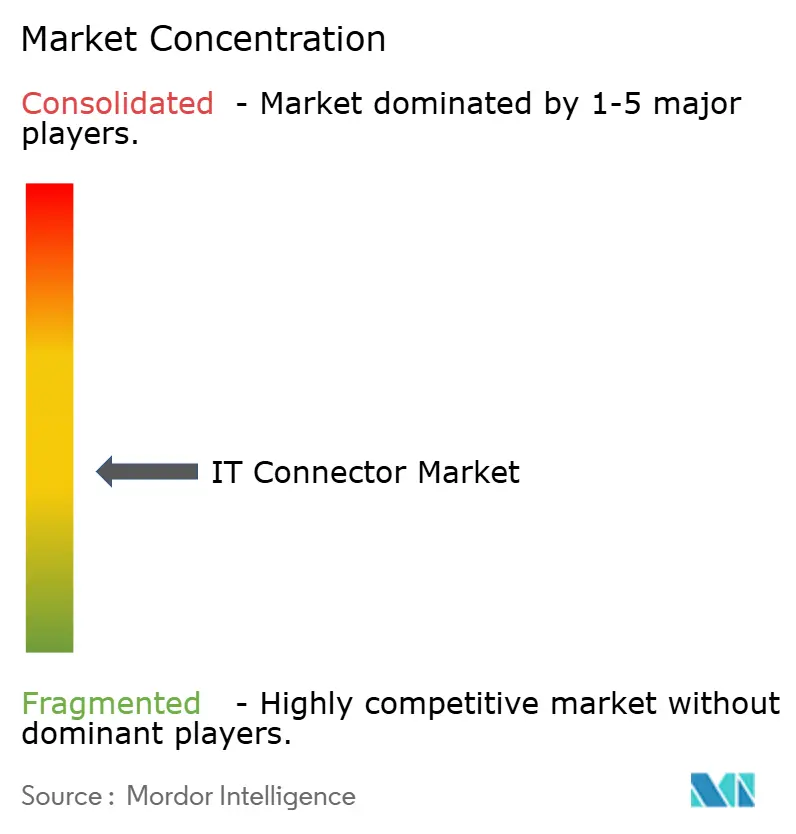

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IT Connector Market Analysis by Mordor Intelligence

IT connector market size in 2026 is estimated at USD 8.14 billion, growing from 2025 value of USD 7.72 billion with 2031 projections showing USD 10.58 billion, growing at 5.39% CAGR over 2026-2031. Growth stems from the urgent need to move data at 224 Gbps-per-lane and beyond inside hyperscale data centers, the region-wide acceleration of 5G / 6G deployments, and the automotive transition to zonal EE architectures in electric vehicles. Co-packaged optics, more efficient RF and VSFF designs, and the availability of on-shore semiconductor capacity funded by the U.S. CHIPS Act round out the demand drivers. At the same time, connector suppliers are working through thermal-mechanical limits above 112 Gbps PAM4 and margin pressure created by a volatile copper price environment.

Key Report Takeaways

- By connector type, PCB connectors led with 44.60% of the IT connector market share in 2025; IO/High-Speed Backplane and Pluggable is projected to expand at a 5.55% CAGR through 2031.

- By mounting configuration, board-to-board held 35.40% revenue share in 2025, whereas wire-to-board is advancing at 6.05% CAGR to 2031.

- By data-rate class, ≤10 Gbps commanded a 47.20% share of the IT connector market size in 2025; ≥56 Gbps PAM4 is rising at a 6.85% CAGR over the forecast period.

- By end-user industry, IT and telecom accounted for 37.40% share in 2025, while automotive and e-mobility is the fastest-growing segment at 3.25% CAGR through 2031.

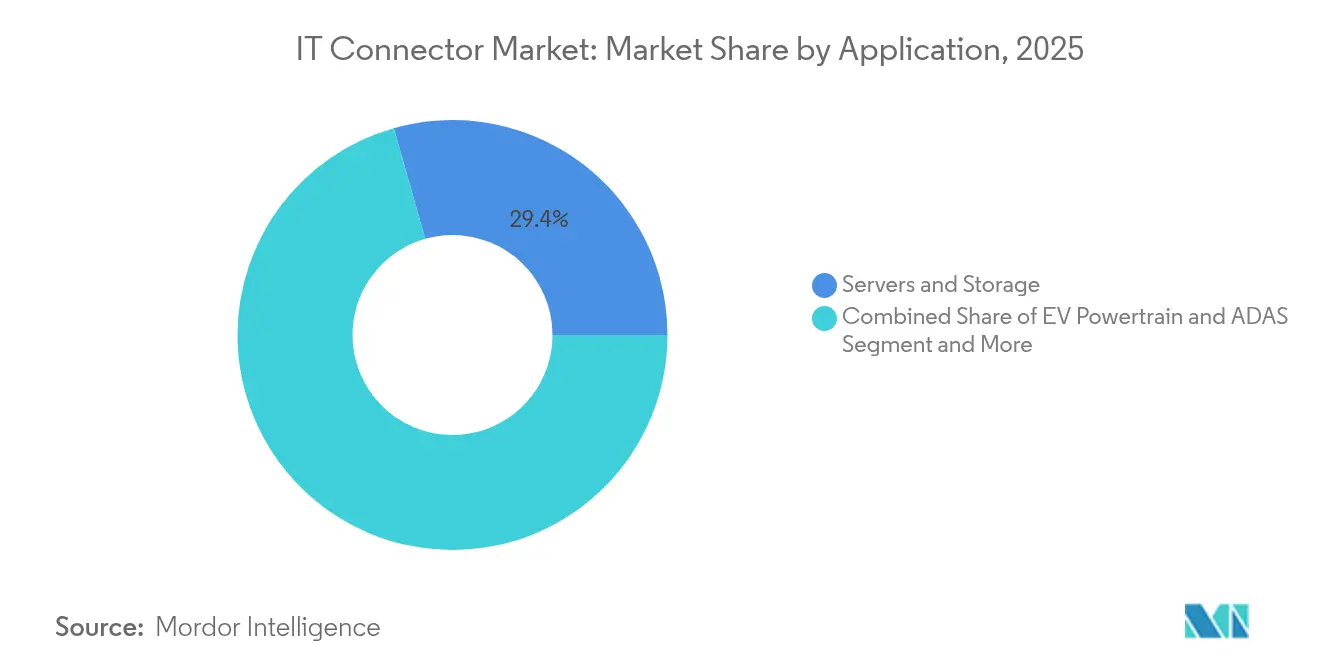

- By application, servers and storage occupied 29.40% of the IT connector market revenue in 2025. the 5G/6G base-station segment will compound 6.32% annually through 2031 as operators compress.

- By material, halogen-free compounds gain tractionStandard thermoplastics still capture 77.60% share thanks to established molding cycles and cost advantages. Yet low-halogen or halogen-free resins will rise 5.64% CAGR as REACH and RoHS tighten limits on halogens and brominated flame retardants.

- By geography, Asia Pacific captured 45.50% of the IT connector market share in 2025; the Middle East and Africa market is forecast to widen at 5.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IT Connector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for High-Speed (>25 Gbps) Interconnects in Hyperscale Data Centers | 1.2% | Global, with concentration in North America & Asia Pacific | Medium term (2-4 years) |

| Rapid 5G/6G Network Roll-outs Elevating RF & VSFF Connector Adoption in Asia | 0.9% | Asia Pacific, with spillover to North America | Short term (≤ 2 years) |

| Automotive Zonal EE Architectures Boosting High-Speed Board-to-Board Connectors in EVs | 0.7% | Global, with concentration in Europe & Asia Pacific | Medium term (2-4 years) |

| Growth of Co-Packaged Optics Accelerating IO Connector Innovation | 0.8% | North America & Asia Pacific | Long term (≥ 4 years) |

| Edge-AI & Industrial IoT Driving Rugged, Sealed Connectors in Factory Automation (EU Focus) | 0.6% | Europe, with spillover to North America | Medium term (2-4 years) |

| U.S. CHIPS Act–Backed On-Shore PCB Production Lifts Domestic Connector Demand | 0.5% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging demand for high-speed interconnects in hyperscale data centers

Bandwidth-hungry AI clusters are transitioning beyond 224 Gbps per lane, forcing connector designers to mitigate insertion loss and thermal rise inside cramped server trays. Molex cites rapid uptake of optical transceivers for 224 Gbps PAM4 links, noting that heat removal is now as critical as signal integrity. Activities range from evaluating PAM-6 / PAM-8 modulation to deploying co-packaged copper and optics that shorten electrical channels. Hyperscalers plan to bring 120-130 new sites online every year, compressing build schedules to six weeks and favoring high-density connector systems that can be kitted and assembled rapidly.

Rapid 5G / 6G network roll-outs elevating RF connector adoption

Spectrum auctions in markets such as Vietnam for the 2.6 GHz and 3.5 GHz bands are fueling mid-band macro and small-cell deployments. Massive-MIMO radios are scaling from 4T4R to 32T32R, spurring the shift to compact VSFF interfaces that compress fiber counts. Connector vendors are responding with SN-class footprints that quadruple port density inside front-haul shelves, while carrier-neutral host operators expand distributed antenna systems valued at USD 8.7 billion by 2028.[1]5G Americas, “Neutral Host Opportunities for 5G & Beyond,” 5gamericas.org

Automotive zonal EE architectures boosting high-speed connectors

Redesigning vehicle wiring into zonal domains can reduce harness weight by up to 40%, raising demand for multi-lane board-to-board connectors able to shuttle high-speed data between zone controllers and central compute modules. Molex’s MX-DaSH consolidates signal, power, and data, simplifying line-side routing. The electrified powertrain introduces high-current nodes that push the global high-voltage connector market toward USD 15 billion by 2033 at 6.5% CAGR. These dynamics make zonal EV platforms the fastest-growing design win category for the IT connector market.

Growth of co-packaged optics accelerating IO connector innovation

Integrating optical engines with ASICs eliminates retimer stages, lowering power by 30% and shrinking link budgets. The Optical Internetworking Forum unveiled a high-density connector project in Q1 2025 to formalize mechanical envelopes for co-packaged solutions. Ultra-low-loss fibers and blind-mate optical ferrules are being co-developed, creating new addressable revenue for connector companies skilled in opto-electronic alignment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper and Rare-Metal Price Volatility Raising BOM Costs | -0.7% | Global | Short term (≤ 2 years) |

| Thermal-Mechanical Reliability Limits at ≥112 Gbps PAM4 | -0.5% | Global, with concentration in North America | Medium term (2-4 years) |

| Lengthy Automotive PPAP Cycles Slowing Connector Design-ins | -0.3% | Global | Medium term (2-4 years) |

| Regulatory Push for Halogen-Free Plastics Increasing Re-qualification Costs (EU) | -0.4% | Europe, with spillover to global supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Copper and rare-metal price volatility raising BOM costs

Surging copper and palladium prices have triggered multiple component price notices, such as Panasonic’s January 2025 flex PCB increase.[2]Panasonic, “Electronic Materials News,” industrial.panasonic.com High-speed connectors use thick copper alloys and precious-metal platings, so even a 5% upswing can erode gross margins. Vendors are locking annual supply contracts, qualifying alternative platings, and redesigning contact beams to lower mass without compromising insertion cycles.

Thermal-mechanical reliability limits at high data rates

Exceeding 112 Gbps PAM4 stresses solder joints, lead frames, and housing plastics. Indium Corporation points to electromigration, tin whisker growth, and CTE mismatch as root causes of early field returns. Low-temperature solders and reinforced LCP housings offer partial mitigation, yet accelerated qualification now dominates the engineering roadmap for data-center interconnects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connector Type: IO/high-speed backplane outpacing legacy links

PCB connectors accounted for 44.60% of the IT connector market size in 2025, reflecting their ubiquity across motherboards, storage planes, and industrial controllers. Robust pin integrity, proven mating cycles, and broad component ecosystems keep this category entrenched in volume applications. The segment still benefits from the CHIPS Act-driven reshoring of PCB assembly, which lifts domestic demand for fine-pitch mezzanine formats.

The IO/high-speed backplane-and-pluggable group is forecast to grow at 5.55% CAGR, propelled by data center upgrades to QSFP-DD 800 and OSFP Xtreme cages capable of 112 Gbps per channel. RF/VSFF connectors benefit from 5G small-cell densification, while circular and rectangular housings remain essential for harsh-duty industrial controls. Microminiature options are seeing new use cases in robotic surgery and CubeSats that reward every millimeter saved.

By Mounting Configuration: wire-to-board gaining momentum

Board-to-board held a 35.40% share in 2025 and remains the workhorse for modular sub-assemblies. Stacked mezzanine and card-edge variants help OEMs meet tight Z-height restrictions inside laptops and switch blades. However, wire-to-board is advancing at 6.05% CAGR as designers favor harnesses that simplify maintenance in EV battery packs and household appliances.

Wire-to-wire assemblies continue to service motor drives and HVAC compressors where board real estate is limited. The miniaturization trend now extends across all mounting styles; Molex’s rugged miniaturized series offers 20-55% footprint reduction while retaining IP67 sealing, directly addressing robotics and outdoor telecom enclosures.

By Data-Rate Class: PAM4 technologies reshape the high-end

The ≤10 Gbps category held a dominant 47.20% share of the IT connector market size during 2025 because many industrial sensors, infotainment head units, and embedded PCs do not need bleeding-edge bandwidth. The cost-performance sweet spot of these connectors keeps them popular when link budgets favor longer cable runs or multiple drops.

The ≥56 Gbps PAM4 bracket will climb 6.85% CAGR to 2031 as AI inference, NVMe-oF storage fabrics, and disaggregated memory pools migrate to 224 Gbps lanes. OIF’s high-density proposal signals ecosystem alignment around thicker copper-sheet cages and low-skew pair routing that support upgrade paths beyond 800 Gbps per port.

By End-user Industry: automotive and e-mobility accelerating

IT & telecom retained 37.40% revenue in 2025, driven by cloud service expansions and continuous campus-backbone refurbishment. Hyperscalers’ preference for ODM hardware translates into high-volume demand for cage, mezzanine, and PAM4 twin-ax assemblies.

Automotive and e-mobility, though smaller, is set to grow 3.25% CAGR. SAE-level 2+ autonomy requires high-speed links between cameras, radar, and centralized ADAS processors, complementing the EV push for high-current battery connectors. Industrial automation and medical devices are also raising their share as edge AI uses rugged IP-rated housings that preserve signal integrity despite vibration and chemical exposure.

By Application: 5G/6G base-stations spearhead growth trajectory

Servers and storage occupied 29.40% of the IT connector market revenue in 2025. Tier-three colocation facilities, regional edge nodes, and AI super-clusters all rely on high-speed cages and orthogonal backplanes to balance cost with upgradability.

The 5G/6G base-station segment will compound 6.32% annually through 2031 as operators compress radio footprints and increase antenna counts. SN and MDC duplex fiber connectors, plus IPx coax links, are winning in remote radio heads tailored for mid-band coverage. EV powertrain / ADAS and factory robots follow closely, with collaborative robot arms debuting built-in connector modularity for hot-swap servo drive.

By Material: halogen-free compounds gain traction

Standard thermoplastics still capture 77.60% share thanks to established molding cycles and cost advantages. Yet low-halogen or halogen-free resins will rise 5.64% CAGR as REACH and RoHS tighten limits on halogens and brominated flame retardants. TE Connectivity and BizLink have each confirmed active conversion programs for eco-friendly jacketing.

Suppliers that expedite material qualification, including UL 94 V-0 approvals, position themselves for design-in wins on EU automotive platforms and consumer wearables that market sustainability credentials.

Geography Analysis

Asia Pacific dominated with 45.50% market revenue in 2025, led by China’s vertically integrated electronics base and India’s fast-growing telecom backbone. Mainland connector producers benefit from provincial incentives aimed at reliability upgrades, with the domestic connector sector forecast to add RMB 12.6 billion year-on-year during 2024. Japan and South Korea contribute through the early adoption of co-packaged optics inside advanced foundry lines.

North America ranks second. The CHIPS and Science Act has already channeled USD 6.6 billion to TSMC Arizona and USD 8.5 billion to Intel, underpinning a localized ecosystem for advanced substrates and connector cages compliant with 224 Gbps PAM4 thermal requirements. Aerospace and defense programs also pull through rugged circular MIL-spec variants that command premium margins.

Europe plays to its strengths in automotive, Industry 4.0, and medical. The push for halogen-free plastics has turned many OEMs into early adopters of eco-class housings. Meanwhile, the Middle East and Africa is set for 5.92% CAGR as hyperscalers install regional cloud zones and governments award smart-city fiber concessions, particularly in Saudi Arabia and the UAE. South America shows steady but lower expansion, weighted toward Brazilian telecom and Argentine industrial automation projects.

Regulatory Landscape

Compliance for IT connectors is shaped by hazardous-substance restrictions and interoperability standards that increasingly affect design choices and re-qualification cycles. In Europe, EU RoHS and REACH continue to push material substitutions, including the shift toward low-halogen or halogen-free compounds that is already reflected in supplier conversion programs; updated RoHS lead-exemption changes take effect in July 2026 (via Commission Delegated Directives (EU) 2025/1802, 2025/2363, and 2025/2364). These changes tighten allowable use cases for lead in specific solder and component categories, and they raise documentation and test burdens across global supply chains serving EU-bound equipment.

In parallel, connector makers track international electrotechnical standards that are adopted into regional regimes for market access and conformance claims. IEC publications in 2025-2026 such as IEC 61076-2-111:2025 (M12 power connectors) and the 2026 updates around circular connector specifications (including EN IEC 61076-2:2026 availability through CENELEC) reinforce a standardized baseline for circular and automation-adjacent interconnects that overlaps with IT/telecom edge and industrial networking deployments. As a result, traceability (materials declarations and conformity statements) becomes more important, and redesign or dual-qualification strategies are more common when high-speed interfaces move to new housings or resins.

Value Chain Analysis

The IT connector value chain starts with upstream raw materials (copper alloys, precious-metal plating inputs, and engineering polymers such as LCP/eco-compounds) and enabling manufacturing equipment (precision stamping, molding, plating, and high-speed test). It then moves through connector design and qualification, and finally to distribution and OEM/ODM integration in servers, storage, network equipment, and base-stations. For high-speed cages, mezzanine connectors, and optical-aligned interfaces, supply continuity increasingly depends on multi-sourcing and longer-term contracting as BOM exposure to copper and rare-metal volatility persists, and as qualification cycles at higher data rates (including 112 Gbps PAM4-class channels) extend engineering lead times.

Recent supply-chain actions point to tighter vertical coordination and ecosystem partnerships. In February 2025, TTI entered a global distribution partnership with Samtec, widening channel access for specialized connector portfolios. In 2026, Molex announced a long-term supply agreement with Prysmian for fiber optic cables to support AI-driven data center demand, while ITT signed a definitive agreement to acquire Aerospace Contacts LLC (USD 31 million) to deepen control over contact-system capabilities in high-reliability interconnects. A four-party framework involving TE Connectivity, Boway Alloy, SBT Ultrasonic, and Komax to industrialize aluminum-for-copper harness transitions also highlights how material and process changes are being coordinated across alloy supply, welding/joining, and harness automation, with knock-on implications for connector terminations and qualification across automotive-adjacent demand streams linked to high-speed board-to-board and wire-to-board ecosystems.

Competitive Landscape

TE Connectivity, Amphenol, and Molex anchor the leadership tier. TE Connectivity derived USD 5.7 billion from the Americas, USD 4.8 billion from EMEA, and USD 5.8 billion from APAC in FY 2024, reflecting a balanced geographic footprint.[4]TE Connectivity, “TE Connectivity 2024 Annual Report,” te.com Amphenol’s 27% stock gain in the past 12 months builds on acquisitions such as CommScope’s Outdoor Wireless Networks, which is expected to add USD 1.3 billion to 2025 sales.

Mid-tier firms are differentiating through domain focus: ZJK Industrial introduced liquid-cooled quick couplings for GPU servers at COMPUTEX 2025. Niche medical specialists such as Sumitomo Electric Lightwave earned 4.5/5 in the 2025 Lightwave+BTR Innovation Reviews for field-splicable optical connectors.

Competitive intensity is rising around system-level know-how. Customers increasingly request full-stack solutions: firmware, thermal models, and compliance test plans bundled with the physical connector. This service overlay rewards companies with cross-disciplinary engineering teams and advanced simulation toolchains. Smaller entrants concentrate on ultraminiature or eco-friendly niches, positioning themselves as acquisition targets for strategics looking to plug technology gaps.

IT Connector Industry Leaders

3M Company

Molex Inc. (Koch)

TE Connectivity Limited

Amphenol Corporation

Samtec Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

AI data center upgrades and the shift toward 224 Gbps-per-lane signaling are creating space in optical and hybrid interconnect architectures, especially where thermal limits and insertion-loss budgets constrain traditional electrical channels. In 2026, 3M announced capacity investment for Expanded Beam Optical (EBO) production (March 2026) and participated in an industry coalition to scale optical connections for AI data centers (May 2026). These actions signal alignment around more robust, contamination-tolerant optical interfaces for high-density deployments. Molex also completed its acquisition of Teramount in May 2026, adding detachable fiber-to-chip connectivity know-how aligned with co-packaged optics, which supports new design-in pathways for connector suppliers focused on tighter mechanical tolerances and optical alignment at scale.

A second opportunity area centers on supply-chain localization and capacity expansion tied to regional build-outs of IT infrastructure and electrified mobility electronics with high-reliability connector needs. JST announced a USD 500 million automated electronic connector manufacturing project in Alabama (April 2026), and HARTING announced a major expansion of its Americas manufacturing and R&D footprint across the US and Mexico (March 2026). These announcements reflect customer demand for shorter lead times and reduced cross-border risk for critical interconnect components. Separately, Hakusan announced a JPY 5 billion investment to build a second plant in Ishikawa, Japan (June 2026), to scale TMT ferrule production for ultra-compact VSFF optical connectors. Together, these moves point to room for suppliers that can pair high-speed electrical performance with eco-material compliance and regionally resilient production.

Recent Industry Developments

- July 2026: 3M and Microsoft announced a strategic partnership to deploy 3M Expanded Beam Optical (EBO) technology within Microsoft Azure cloud and AI data center infrastructure. The collaboration reinforces EBO as a scaled optical-interconnect option for high-uptime environments and tightens the link between hyperscaler requirements and connector technology roadmaps.

- May 2026: Molex completed the acquisition of Teramount Ltd., adding detachable fiber-to-chip connectivity capabilities aligned with co-packaged optics. The deal strengthens Molex's position in next-generation optical connectivity stacks where connector alignment and packaging tolerances become differentiators in AI server architectures.

- January 2026: Amphenol completed the acquisition of CommScope's Connectivity and Cable Solutions (CCS) business. The transaction expanded Amphenol's fiber and cable interconnect footprint, supporting broader end-to-end offerings for telecom and data center customers seeking integrated connectivity portfolios.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the IT connector market covers newly manufactured electro-mechanical connectors that carry data, signal, or low-to-mid-voltage power inside IT infrastructure equipment such as servers, storage systems, switches, and base-stations, with revenue measured in USD.

Scope exclusions: Cable assemblies, passive copper or optical cords longer than one meter, and connectors primarily made for automotive, appliances, or broad industrial uses are excluded.

Segmentation Overview

- By Connector Type

- PCB Connectors

- IDC Connectors

- IO/High-Speed Backplane and Pluggable

- Circular and Rectangular

- RF/VSFF (SN, CS, MMC)

- Microminiature/Nano Connectors

- By Mounting Configuration

- Board-to-Board

- Wire-to-Board

- Wire-to-Wire/Cable Assemblies

- By Data-Rate Class

- ≤10 Gbps

- 10-25 Gbps

- 25-56 Gbps

- ≥56 Gbps/PAM4 112 G

- By End-user Industry

- IT and Telecom (incl. Data Centers)

- Consumer Electronics and Computing

- Automotive and e-Mobility

- Industrial Automation/IIoT

- Healthcare and Medical Devices

- By Application

- Servers and Storage

- 5G/6G Base-Stations

- EV Powertrain and ADAS

- Factory Robotics and PLCs

- By Material

- Standard Thermoplastics

- Halogen-free/Eco-friendly Compounds

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building the demand context for IT hardware where connectors are designed in, then mapping how connector types flow into server, networking, and telecom equipment builds. We used public sources such as US International Trade Commission trade data, UN Comtrade, US Census Bureau manufacturing statistics, and International Telecommunication Union indicators to understand shipment direction, installed base growth, and regional intensity.

We also reviewed sources such as IEEE publications and other peer-reviewed engineering literature to check connector performance requirements that influence pricing (for example, higher speed I/O density and miniaturization). To keep the supply side grounded, we used company filings, investor presentations, and reputable press coverage for product mix cues and demand commentary, and we supplemented financial visibility using paid subscriptions that provide company financials and intelligence, patent coverage, and shipment-level import and export views where helpful. These are illustrative examples, and many other sources were also referenced during data collection, validation, and clarification throughout the study.

Primary Interviews and Surveys

Primary work focused on verifying what portion of connector revenue is tied to IT equipment builds, and on sense-checking pricing behavior as speeds, port counts, and form factors shift. Interviews covered connector manufacturers, component distributors, and engineering and procurement stakeholders at IT hardware and telecom equipment organizations across APAC, EMEA, and the Americas, and the respondent input was used to close gaps from desk findings and confirm the final totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 39% |

| Mid tier: 54% | Functional/Unit leaders: 33% | EMEA: 34% |

| Smaller Players: 15% | Managers: 55% | Americas: 27% |

Market-Sizing & Forecasting

Sizing begins with a top-down build that reconstructs the addressable connector value pool from IT infrastructure equipment activity, then applies connector content and pricing logic tied to each equipment group. Inputs that commonly matter include server and storage shipment trends, network port growth and speed migration (such as higher-speed I/O adoption), data center buildout signals, unit-level connector density, and typical selling price movement as designs shift toward smaller pitches and higher performance.

To corroborate the totals, we also run selective bottom-up checks using sampled product line revenues, channel feedback on mix, and ASP times volume approximations for key connector families. This helps adjust for under-coverage when public disclosures are limited. Forecasts are produced using scenario analysis, where volume drivers (IT equipment builds and upgrades) and pricing drivers (mix shifts, higher-speed attach rates, and cost pass-through behavior) are projected separately and then recombined into market value. When bottom-up detail is missing for smaller suppliers or niche connector types, the gap is handled through ratio-based allocation anchored on validated end-equipment demand signals and interview feedback.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals such as trade movement direction, IT hardware shipment trends, and stated demand patterns from industry stakeholders, before the final numbers are signed off. If variances look unusual, we revisit assumptions such as connector content per system and the pricing path, then recalculate the model with notes kept for traceability.

We also run multi-step internal reviews so calculation logic, units, and currency handling are consistent across regions and years. Reports are refreshed annually, with interim updates when material events change demand or pricing assumptions, and a fresh pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's IT Connector Market Size Measured Against Other Published Estimates

Published market sizes for IT connectors can differ more than expected because the boundary between connectors, cable assemblies, and broader electronics interconnect products is not drawn the same way by all publishers. Differences also show up when pricing is treated as a single blended average, or when older exchange-rate timing is carried forward even after large currency moves.

A refresh-led gap is common in this market because ASPs shift with speed migration and connector density, and those movements need periodic re-checks through interviews and public demand signals rather than being assumed as a straight-line trend. By tying currency timing and ASP updates to the most recent validation checks each cycle, Mordor Intelligence reduces drift in the value series that can happen when models are not re-tuned after mix changes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.14 B (2026) | |

| Global Consultancy A | USD 8.70 B (2026) | This figure commonly runs higher when cable assemblies and longer passive cords are counted alongside connectors, and when blended pricing assumes faster ASP expansion without re-checking mix shifts by speed grade. |

| Industry Association B | USD 7.50 B (2026) | This value can come out lower when the scope is limited to a narrower set of board-level connectors used in enterprise hardware, and when currency conversion uses earlier average rates that lag recent movements. |

The spread across the table is mainly explained by scope edges (connectors only versus connectors plus assemblies) and by how pricing and currency are refreshed across the same year. With clear inclusion rules and repeatable checks on IT equipment demand signals, the estimate stays traceable to practical drivers and can be updated without rewriting the whole model.

Key Questions Answered in the Report

What is the current size of the IT connector market?

The IT connector market stands at USD 8.14 billion in 2026 and is projected to reach USD 10.58 billion by 2031.

Which region commands the largest demand for IT connectors?

Asia Pacific leads with 45.50% market revenue, supported by expansive electronics manufacturing and rapid 5G roll-outs.

Which connector type is growing the fastest?

IO / high-speed backplane and pluggable connectors are forecast to grow at a 5.55% CAGR through 2031, buoyed by hyperscale data-center bandwidth upgrades.

How will 5G and 6G deployments affect connector demand?

Expanded mid-band spectrum use and massive-MIMO radio installations are lifting demand for RF and VSFF interfaces that pack higher density into base-station and fronthaul gear.

Why are automakers shifting toward zonal EE architectures?

Zonal layouts cut wiring weight, lower material cost, and support centralized compute, thereby increasing the need for multi-lane board-to-board connectors able to carry high-speed data and power inside electric vehicles.

What environmental regulations are influencing material choices?

EU RoHS and REACH directives are pushing connector makers toward halogen-free compounds, a material class projected to advance at a 5.64% CAGR between 2026 and 2031.

Page last updated on: