Wire-to-Board Connector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.88 Billion |

| Market Size (2031) | USD 5.82 Billion |

| Growth Rate (2026 - 2031) | 3.58% CAGR |

| Fastest Growing Market | Latin America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wire-to-Board Connector Market Analysis by Mordor Intelligence

The wire-to-board connector market size is expected to grow from USD 4.71 billion in 2025 to USD 4.88 billion in 2026 and is forecast to reach USD 5.82 billion by 2031 at 3.58% CAGR over 2026-2031. Steady expansion stems from rising demand in electric vehicles (EVs), compact consumer devices, factory automation upgrades, and low-earth-orbit (LEO) satellites. Order growth of 7.0% and sales growth of 2.7% in 1H-2024 confirmed the industry’s resilience despite supply-chain pressures. Surface-mount automation, sub-2 mm pitch adoption, and higher-current designs above 6 A continue to shape product roadmaps. Asia-Pacific retains manufacturing leadership while Latin America emerges as the fastest-growing region. On the competitive front, incumbents rely on miniaturization and thermal know-how rather than price to defend positions, and selective acquisitions such as TE Connectivity’s USD 2.3 billion purchase of Richards Manufacturing signal ongoing consolidation.

Key Report Takeaways

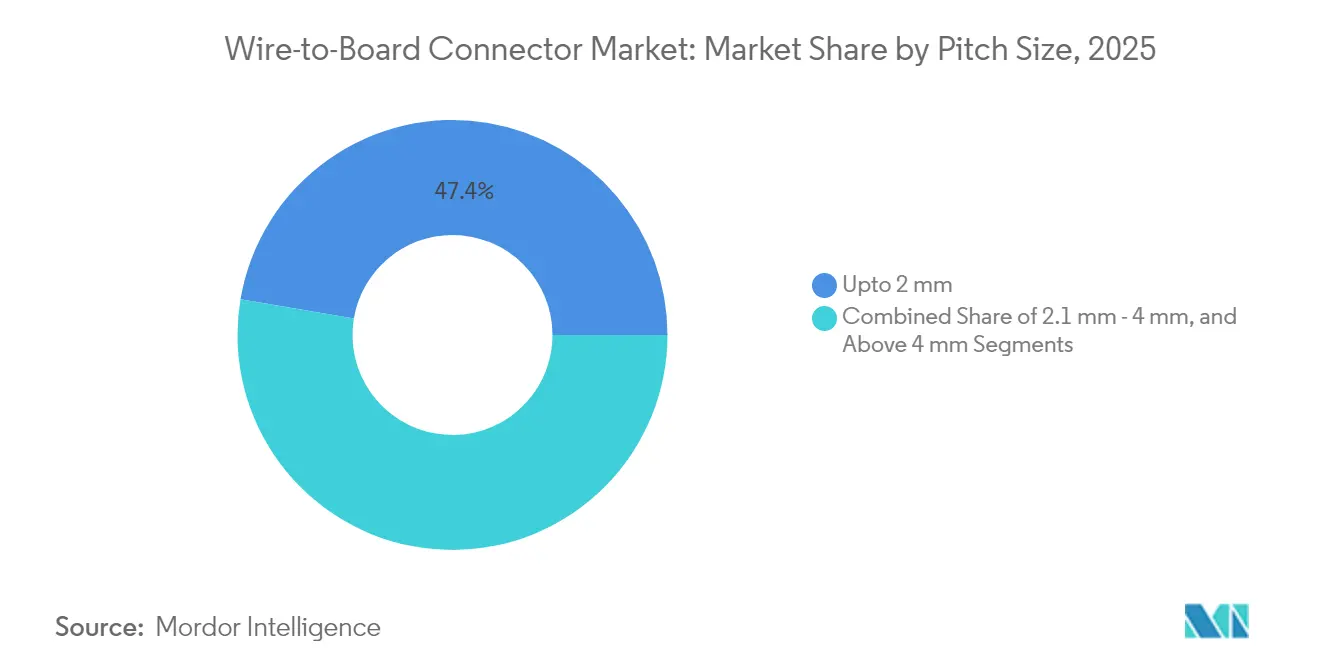

- By pitch size, sub-2 mm connectors held 47.35% of the wire-to-board connector market share in 2025 and are advancing at a 3.59% CAGR through 2031.

- By mounting type, surface-mount formats commanded 56.85% revenue share in 2025; through-2031 growth stands at 3.5% CAGR.

- By current rating, the 1.1-3 A class represented 41.15% of the wire-to-board connector market size in 2025, while above-6 A variants post the fastest 5.08% CAGR.

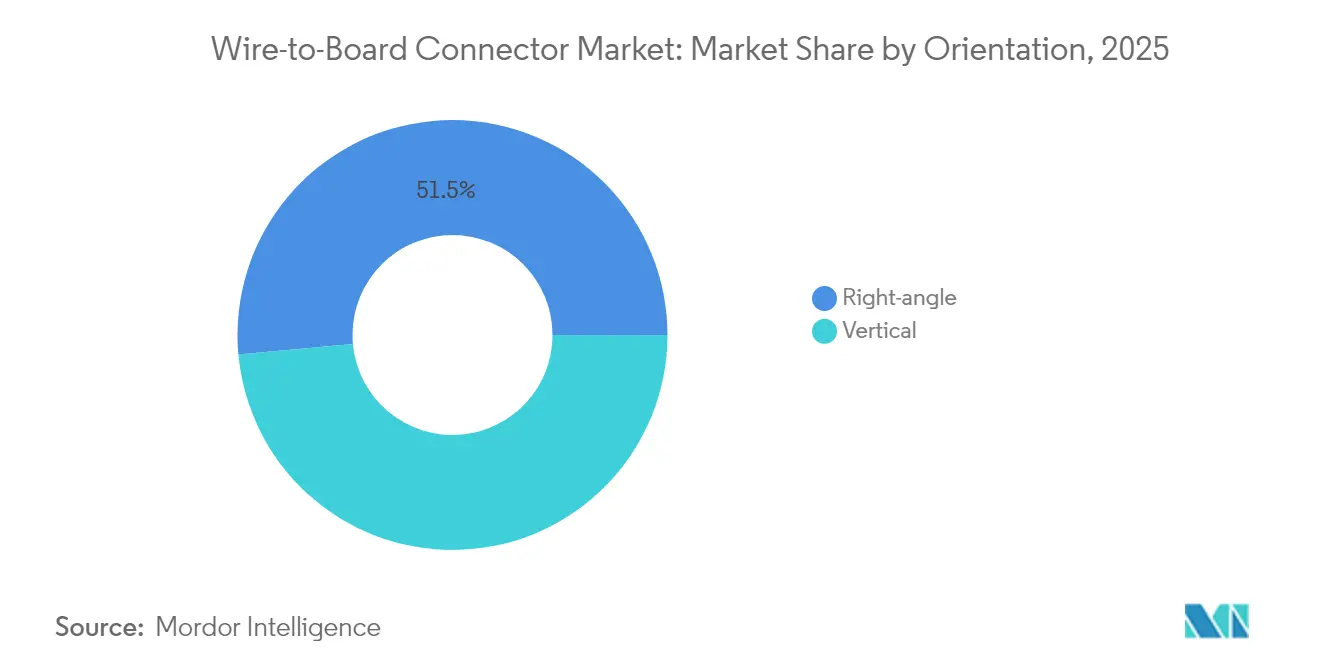

- By orientation, right-angle parts led with 51.45% share in 2025 while vertical layouts expand at a 5.82% CAGR.

- By end-user, consumer electronics retained 33.85% share in 2025; medical devices are projected to rise at 6.28% CAGR to 2031.

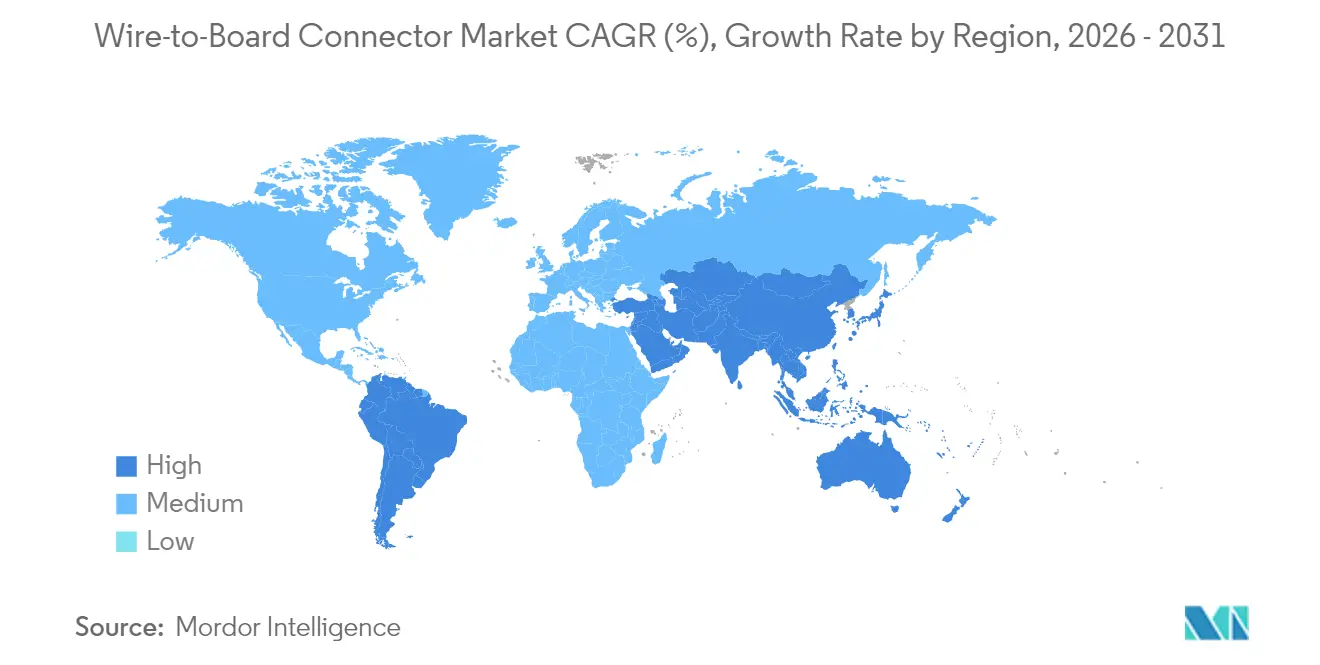

- By geography, Asia-Pacific accounted for 46.25% of 2025 revenue; Latin America records the highest 4.99% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wire-to-Board Connector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-compact wearables push sub-2 mm pitch | +0.80% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| EV-battery BMS demand for ≥6 A connectors | +1.20% | China, Europe, North America | Short term (≤2 years) |

| Brownfield factory automation retrofits | +0.60% | North America, EU, emerging APAC | Long term (≥4 years) |

| LEO-satellite vibration-resistant designs | +0.40% | US, Europe, China | Medium term (2-4 years) |

| Open-compute servers adopt faster mezzanines | +0.70% | North America, EU, APAC | Short term (≤2 years) |

| Medical disposables lift micro-WTB volumes | +0.50% | Global, regulatory in US, EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ultra-compact Wearables Driving Sub-2 mm Pitch Demand in Asia

Sub-2 mm connectors now dominate shipments because fitness trackers and smartwatches require ever-smaller footprints. Molex’s 0.175 mm pitch range illustrates how staggered contacts overcome soldering limits while keeping 0.35 mm pads. Metal Injection Molding supports mass production of microminiature housings with tight tolerances. Asia-Pacific manufacturers concentrate the necessary tooling, reinforcing the region’s lead. As form factors shrink, cross-disciplinary teams address signal integrity and electromagnetic interference concurrently.

Rapid EV-Battery BMS Adoption Boosting High-Current Connectors

Battery management systems in EV packs increasingly specify connectors above 6 A, the fastest-growing current class of the wire-to-board connector market. TE Connectivity’s HC-Stak cuts terminal size by up to 30% and supports aluminum cabling, easing vehicle mass targets. Specialized bushings such as PennEngineering’s ECCB maintain low resistance despite aluminum oxidation. [1]Assembly Magazine, “Contact Bushing Assembles Aluminum Bus Bars for EVs,” assemblymag.com Rising EV volumes in China, Europe, and North America create demand clusters that influence supplier footprints.

Automation Retrofits in Brownfield Factories Raising Sensor Refresh

Legacy plants are adding predictive-maintenance sensors, spurring refresh cycles for wire-to-board connectors that fit cramped control cabinets. IPC/WHMA-A-620 emphasizes tighter process control, vital when line stoppages carry high cost. North American and European factories set early pace, but Asia-Pacific adopters follow as cost-effective retrofit kits appear. Designs stress vibration tolerance and wide temperature ratings to match round-the-clock operation.

LEO-Satellite Constellations Requiring Vibration-Resistant Connectors

Commercial LEO launches demand connectors that survive intense vibration, atomic oxygen, and thermal cycling. TE Connectivity’s space-grade portfolio addresses these hazards. [2]TE Connectivity, “Factors That Affect Spacecraft Connectors,” te.com Harwin’s Datamate and Gecko series cover CubeSat through large-platform needs. Cost-sensitive “new-space” missions favor modular designs that balance reliability and affordability, fostering vendor differentiation based on test pedigree.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PCB land pads below 0.4 mm strain assembly yield | -0.9% | Global, acute in Asia-Pacific | Short term (≤2 years) |

| Solder-joint reliability above 125 °C under-hood | -0.7% | Global automotive | Medium term (2-4 years) |

| Trade-war tariffs inflate BOM costs | -0.4% | North America importers | Short term (≤2 years) |

| Counterfeit risk in dense connectors | -0.3% | Global, Asia-Pacific sourcing | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

PCB Real-Estate Shrink Limiting Landing Pads

Connector pads under 0.4 mm challenge pick-and-place accuracy and raise rework costs, depressing short-term growth. Denser layouts heighten crosstalk and thermal hotspots, forcing expensive high-Tg laminates that erode savings. Yield drops prompt some OEMs to delay next-gen layouts until assembly lines upgrade.

Solder-Joint Reliability at >125 °C Under-Hood

EV powertrains expose joints to sustained 150 °C and above. Studies show plating composition is critical to avoid brittle intermetallics at 200 °C. [3]Web Archive of J-STAGE, “Effect of Electroless Ni-P / Electrolytic Cu Plating on Solder Joint Reliability under High Temperature Environment of 200 °C,” web.archive.org Enhanced conductor structures extend current-carrying time by 230%, yet they raise material cost. Tier-1s weigh extra expense against warranty risk, tempering near-term adoption rates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pitch Size: Sub-2 mm Leads Miniaturization

Sub-2 mm connectors captured 47.35% of 2025 revenue and anchor the wire-to-board connector market’s miniaturization wave. The segment expands at a 3.59% CAGR to 2031 as smartphones, hearables, and implantables shrink boards further. The 2.1-4 mm class remains essential in automotive modules where mechanical robustness trumps size. Above-4 mm products cater to specialized high-current needs but steadily lose share.

Research prototyping 80 µm pitch contacts with <50 mΩ resistance hints at future disruption. Asia-Pacific fabs house most sub-2 mm tooling, reinforcing regional dominance. Designers must co-optimize signal integrity, thermal spread, and insertion force as pitches fall, making this slice of the wire-to-board connector market a nexus for cross-discipline collaboration.

By Mounting Type: Surface-Mount Retains Automation Edge

Surface-mount connectors owned 56.85% of 2025 sales, reflecting automation’s pull across consumer and industrial lines. Automated pick-and-place lowers cost per joint and limits PCB drilling, supporting a 3.5% CAGR. Through-hole remains critical for power electronics, where larger solder barrels aid heat dissipation and shock resistance.

Rework on dense surface-mount boards is costly because neighboring components block access. IPC/WHMA-A-620 calls for tighter process windows that many legacy lines struggle to meet. Asia-Pacific maintains the strongest surface-mount infrastructure, whereas some North American facilities still favor through-hole for rugged assemblies in the wire-to-board connector market.

By Current Rating: Above-6 A Segment Accelerates

Connectors rated 1.1-3 A retained 41.15% revenue in 2025, serving mainstream signal paths. Yet above-6 A designs post a 5.08% CAGR thanks to EV traction inverters and data-center power shelves. Up-to-1 A parts meet low-power IoT needs and lose share only slowly. The 3.1-6 A class bridges industrial controls and mid-power automotive loads.

HC-Stak illustrates how aluminum cabling plus better thermal paths shrink size by up to 30%. Thermal-electrical optimization studies confirm that welded conductor reinforcements extend lifetime more than increasing cross-section alone. These insights steer R&D budgets across the wire-to-board connector market.

By Orientation: Vertical Growth Outpaces Right-Angle

Right-angle formats kept 51.45% share in 2025 because they route harnesses neatly along boards. Vertical mounts, however, climb at 5.82% CAGR as handset and IoT designers cut device thickness. Vertical layouts improve airflow but raise stack-up height, demanding layout trade-offs. Signal path geometry also shifts impedance profiles; 112 Gbps links now push orientation to the design front-line.

Assembly houses favor whichever orientation reduces pick-and-place errors. Consequently, orientation choice tightens collaboration between electrical and manufacturing engineers inside the wire-to-board connector market.

By End-User Vertical: Medical Devices Gain Momentum

Consumer electronics held 33.85% of 2025 revenue, still the largest buyer group in the wire-to-board connector market. Single-use medical disposables propel that sector at a 6.28% CAGR as hospitals target cross-contamination risk. IT & telecom demand normalizes after heavy 2024 data-center builds linked to AI. Automotive revenues swing toward EV modules needing high-current, high-temperature parts, offsetting ICE declines.

Industrial automation benefits from sensor retrofits, whereas aerospace gains from recurring LEO launches. Regulatory frameworks such as FDA and CE mark influence material and traceability requirements, shaping connector specifications across all verticals.

Geography Analysis

Asia-Pacific generated 46.25% of 2025 turnover owing to clustered PCB and final-assembly capacity in China, Japan, and South Korea. Incentives draw supplementary builds to India, widening the regional base. Southeast Asian nations lead semiconductor packaging, pulling high-density connectors into local supply chains. These fundamentals keep the wire-to-board connector market firmly anchored in the region for the forecast horizon.

North America combines automotive assembly in Mexico, advanced aerospace in the United States, and medical device exports across the zone. Reshoring initiatives and tariff exposure are nudging selected connector lines back from Asia, yet cost gaps persist. Canada’s mining equipment sector adds pockets of demand for ruggedized variants of the wire-to-board connector market.

Europe aligns connector innovation with EV drivetrain rollouts and Industrie 4.0 upgrades. Germany spearheads high-current development for vehicles, while Nordic utilities integrate connectors into wind and grid-storage assets. Strict RoHS and REACH mandates drive global suppliers to adopt compliant chemistries. Latin America, led by Brazil’s automotive growth, posts the fastest 4.99% CAGR as OEMs deepen local content to buffer currency risk. Small but rising African and Middle-Eastern projects in solar micro-grids round out global exposure.

Note: Wire-to-Board Connector Market

Regulatory Landscape

Global wire-to-board connector supply is shaped by materials restrictions, safety and EMC requirements for end equipment, and trade policies that affect bill-of-material declarations and import costing. In the European Union, RoHS and REACH remain central for connector plastics, platings, and solders used in PCB terminations, and the REACH SVHC Candidate List reached 253 substances as of February 2026, reinforcing ongoing disclosure and substitution work across connector portfolios.

In 2026, two compliance anchors tightened operational requirements for suppliers serving industrial and cross-border supply chains. IEC published IEC 63171-3:2026 (May 2026), which increases standardization pressure for industrial connectivity used in export-oriented equipment programs. In April 2026, the United States revised Section 232 tariff implementation toward a classification-based full entered-value approach, changing how electronics importers model tariff exposure and putting more focus on country-of-origin and sourcing strategies. ECHA also updated REACH Annex XVII to reduce allowable lead content in soldered electronic components from 0.1% to 0.05% by weight, effective 1 August 2026, which is expected to drive re-qualification of solder finishes and updated material declarations for connector assemblies that rely on soldered terminations.

Value Chain Analysis

The wire-to-board connector value chain runs from upstream metals and polymers into high-precision component manufacturing, then through assembly and qualification, and finally to distribution and OEM/EMS integration. Key inputs include copper alloys and plated contact materials, along with engineering plastics such as LCP and PPS for high-temperature housings, with cost and availability volatility flowing quickly into connector pricing and lead times. Midstream, leading suppliers such as TE Connectivity, Molex, Amphenol, JST, Samtec, and Kyocera-AVX combine stamping, molding (including Metal Injection Molding for dense designs), plating, and automated assembly to deliver surface-mount and through-hole families spanning sub-2 mm pitch to higher-current designs used in EVs and industrial controls.

Downstream integration is concentrated in Asia-Pacific EMS and device assembly ecosystems, while industrial, automotive, and medical customers increasingly request dual sourcing and regional supply to reduce disruption from tariffs and logistics risk. Automation-led redesign and channel expansion are showing up in recent value-chain moves: Q5D and KYOCERA AVX extended a collaboration (May 2026) to develop custom IDC connectors optimized for robotic wire-harness assembly, and Neutrik Group Americas added DigiKey as a distribution channel partner (July 2026). Automotive material substitution is also influencing connector and termination choices, as SBT and TE Connectivity signed an agreement (July 2026) to advance aluminum-for-copper mass production in automotive wire harnesses, supporting demand for interfaces and contact systems compatible with aluminum conductors.

Competitive Landscape

The wire-to-board connector market is moderately fragmented. TE Connectivity, Molex, and Amphenol hold leading positions through broad portfolios and global plants. Competitive focus centers on pitch miniaturization, thermal headroom, and automated assembly yield rather than price undercutting.

Incumbents invest in Metal Injection Molding for sub-1 mm housings, in-house plating for 150 °C joints, and simulation that predicts electromagnetic coupling. TE Connectivity’s USD 2.3 billion acquisition of Richards Manufacturing in February 2025 widens automotive and industrial reach, illustrating selective consolidation. Patents around ultra-fine contacts and aluminum-compatible interfaces become key defensive tools. Emerging specialists which target space-qualified or disposable-medical niches find barriers manageable where compliance know-how deters new entrants.

Platform roadmaps converge on 224 Gbps PAM4 readiness and below-0.175 mm pitch experiments. Suppliers weigh synergy between volume consumer runs and bespoke aerospace lots, shaping capacity allocation decisions throughout the wire-to-board connector market.

Wire-to-Board Connector Industry Leaders

TE Connectivity Ltd.

Molex LLC

Amphenol ICC (Amphenol Corp.)

J.S.T. Mfg. Co. Ltd.

Samtec Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space is emerging where higher-density layouts, higher data rates, and automation constraints overlap, particularly in EV electronics, industrial retrofit kits, and AI data-center infrastructure. On the manufacturing side, large investments and facility expansions are creating room for suppliers to add automated capacity and qualify new process windows for fine-pitch and high-reliability terminations. JST announced a USD 500 million electronic connector manufacturing facility in Guntersville, Alabama (April 2026), focused on automated production for automotive, appliance, and consumer electronics connectors. TE Connectivity launched a USD 150 million automotive production facility in Nantong, China (June 2026) to manufacture high-voltage and high-speed data connectors for electric and software-defined vehicles.

Product and platform opportunities are also supported by standardization and multisourcing activity in adjacent high-density connectivity ecosystems used in data-center and AI architectures. In early 2026, US Conec, Corning, Fujikura, and Sumitomo Electric Lightwave formed a multi-source framework to broaden the MMC very small form factor platform to include expanded-beam optics for AI factory link architectures, and Corning introduced MMC connectors with PRIZM TMT expanded-beam ferrules at OFC 2026. While these are not wire-to-board products, they support a broader shift toward standardized, multi-sourced, compact interconnect platforms, giving wire-to-board suppliers room to differentiate through miniaturized pitches, improved EMI control, and high-temperature solder-joint performance for densely packaged electronics. Capacity additions in precision manufacturing also signal the supply-side push behind smaller geometries, such as TDConnex opening an 800,000 sq ft micro-precision factory in Xiamen, China with expanded MIM capability (May 2026).

Recent Industry Developments

- June 2026: Molex launched the HSAutoLink G connector system to support multi-gig automotive Ethernet connections up to 25 Gbps for ADAS compute and zonal architectures. The release targets higher-speed in-vehicle networks where signal integrity and packaging density drive connector redesign choices.

- May 2026: Samtec released mPOWER ultra micro power interconnect updates that add through-hole PCB termination options for vertical and right-angle configurations. The added termination style broadens manufacturability and reliability options in compact power interconnect use cases where mechanical retention and assembly robustness matter.

- November 2025: Molex announced availability of Quad-Row Shield connectors featuring a four-row layout with integrated EMI shielding to reduce signal interference. The design choice reflects demand for denser board-level interconnects that control EMI without adding external shielding steps.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the wire-to-board connector market covers connector systems used to terminate a wire harness and mate it to a printed circuit board, including the connector housing and contact interface sold into electronics assembly.

Scope exclusions: This sizing does not include board-to-board connectors, wire-to-wire connectors, bare metal terminals sold without a connector system, or cable assemblies sold as a finished kit.

Segmentation Overview

- By Pitch Size

- Upto 2 mm

- 2.1 - 4 mm

- Above 4 mm

- By Mounting Type

- Surface-Mount

- Through-Hole

- By Current Rating

- Up to 1 A

- 1.1 A - 3 A

- 3.1 A - 6 A

- Above 6 A

- By Orientation

- Vertical

- Right-angle

- By End-User Vertical

- Consumer Electronics

- IT and Telecommunication

- Automotive

- Industrial Automation

- Aerospace and Defense

- Medical Devices

- Others (Energy, Lighting)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public indicators that explain where connector demand is coming from and how it is moving by region. We refer to sources such as the US Census Bureau manufacturing and trade tables, UN Comtrade customs statistics, World Bank macro series, and OECD industrial production indexes to anchor directionally correct demand signals.

To make the model practical, we also review company filings, annual reports, investor presentations, and credible press coverage to understand mix shifts between automotive, industrial, and consumer electronics builds. Patent databases are used to sanity check technology movement in miniaturization, higher pin counts, and ruggedized designs. Where classification allows, an import/export shipment level database is selectively used to test trade flows for connector categories. These desk sources are not exhaustive, and we checked many other public references to collect, validate, and clarify assumptions.

Primary Interviews and Surveys

Primary work focuses on interviews and short surveys with connector manufacturers, component distributors, EMS procurement teams, and design engineers who specify interconnects in end equipment. Respondent input is used to confirm typical pricing bands, adoption of finer pitch connectors, and regional demand differences across APAC, EMEA, and the Americas, then to close gaps where public data is not specific enough.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 52% |

| Mid tier: 59% | Functional/Unit leaders: 33% | EMEA: 30% |

| Smaller Players: 14% | Managers: 55% | Americas: 18% |

Market-Sizing & Forecasting

Market size is built using a top-down approach where electronics production, automotive output, and industrial equipment activity are translated into a connector demand pool, then filtered to the share realistically served by wire-to-board interfaces. Once the demand pool is shaped, we corroborate it with selective bottom-up approximations, including sampled ASP by pitch and circuit count, channel checks on regional mix, and sanity checks against supplier revenue exposure to this connector family.

In this market, practical drivers include PCB assembly volumes, the share of devices using modular harness to PCB termination, average pins per connector in key applications, the shift toward smaller pitch designs, and the expected pricing curve as designs move from legacy to miniaturized formats. Forecasting is run using scenario analysis supported by a light multivariate regression, pairing leading indicators like industrial production and vehicle build outlook with expert views on electronics cycle recovery. Where bottom-up evidence is incomplete, the gap is handled through conservative range assumptions, reviewed again during primary validation.

Data Validation & Update Cycle

Outputs are checked in more than one way so unusual jumps do not slip into the final numbers. We compare the model result against independent signals like electronics output trends, trade movement, and realistic ASP bands, then investigate differences before sign-off.

A second analyst review is completed for logic, math, and year-over-year movement, and experts are re-contacted when a variance appears tied to a new program ramp, supply disruption, or a price swing. The report is refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery pass so clients receive the latest updated view.

Mordor Intelligence's Wire to Board Connector Market Estimate Compared With Other Published Estimates

Published market sizes for wire-to-board connectors can differ even when the topic name looks the same, because the scope and counting rules are not always aligned. The most common differences we see come from how adjacent connector families are treated, what is assumed for average selling price movement, and the year used as the base for the forecast.

In practice, the spread is usually driven by whether wire-to-wire and board-to-board revenue is blended into the total, whether cable assemblies are counted as connector value, and whether 2024 or 2026 is used as the anchor year when currency timing and pricing conditions were different. The table below shows how these choices can move the reported value. The distinction becomes clearer when the model counts only connector systems used to terminate wires to a PCB, which is the scope applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.88 B (2026) | |

| Global Consultancy A | USD 5.13 B (2024) | Uses an earlier base year and tends to report a broader application sweep, which can pull in connector revenue tied to bundled harnessing or adjacent interconnect categories when mapping styles and applications. |

| Research Portal B | USD 5.05 B (2024) | Anchors sizing in 2024 and applies a higher growth track into the early 2030s, which may rely on faster ASP progression and a wider inclusion of end equipment programs without the same level of exclusion checks for non-WTB connectors. |

Overall, differences are explainable once the base year and the exact connector family rules are made explicit. Our approach stays repeatable because the size is tied back to observable electronics and industrial activity signals, and then cross-checked with real-world pricing and mix feedback from the field.

Key Questions Answered in the Report

What is the current size of the wire-to-board connector market?

The wire-to-board connector market is valued at USD 4.88 billion in 2026 and is forecast to reach USD 5.82 billion by 2031.

Which pitch size segment leads the market?

Connectors with sub-2 mm pitch account for 47.35% of 2025 revenue and advance at a 3.59% CAGR through 2031.

How fast is the high-current (above 6 A) segment growing?

The high-current class records the fastest 5.08% CAGR due to EV battery management system demand.

Which region shows the strongest growth outlook?

Latin America is projected to expand at a 4.99% CAGR, driven by automotive and electronics investments.

What strategic moves are market leaders making?

TE Connectivity’s USD 2.3 billion acquisition of Richards Manufacturing and the HC-Stak launch illustrate moves to expand capacity and address EV thermal challenges.

How does automation influence mounting-type preference?

Surface-mount connectors dominate because automated pick-and-place lowers assembly cost and supports 56.85% of 2025 revenue.

Page last updated on: