Breast Ultrasound Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

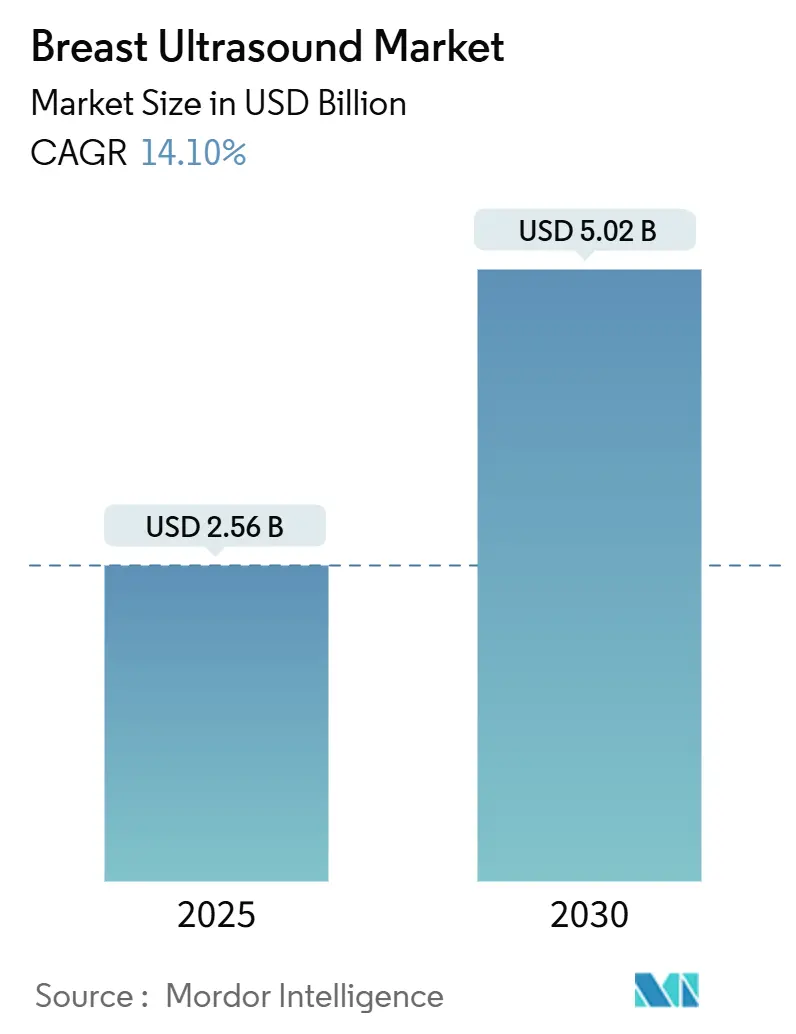

| Market Size (2025) | USD 2.56 Billion |

| Market Size (2030) | USD 5.02 Billion |

| Growth Rate (2025 - 2030) | 14.10% CAGR |

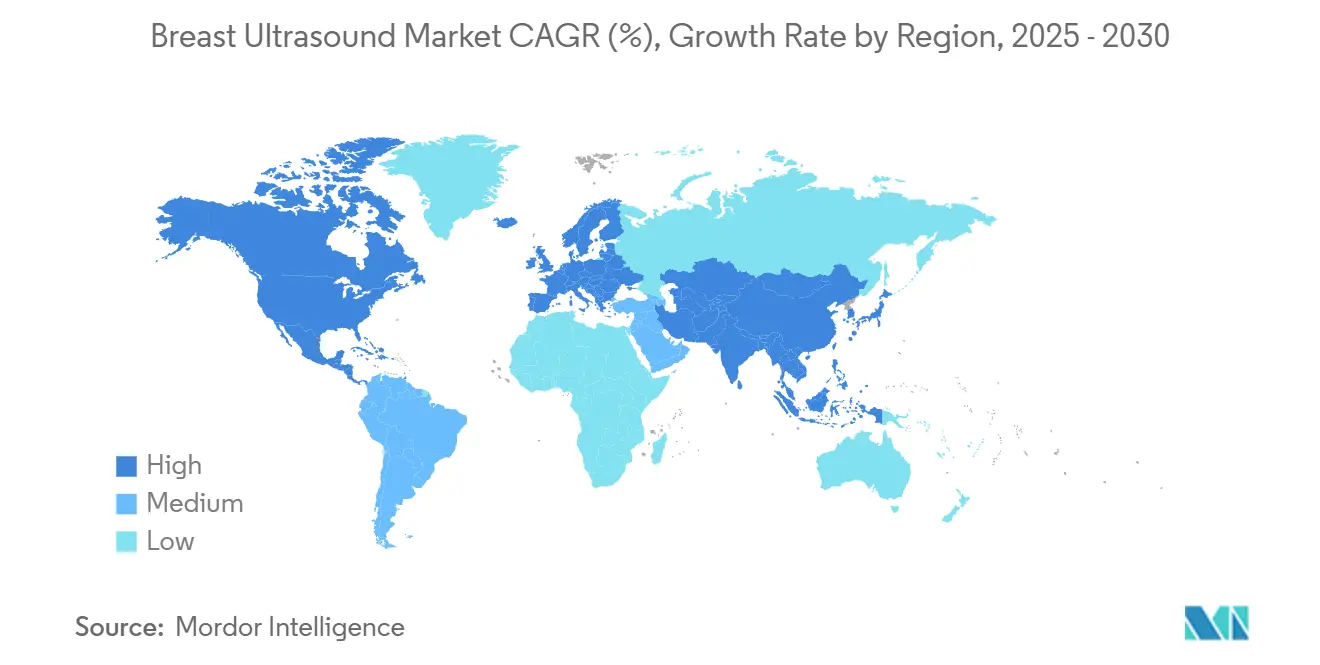

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Ultrasound Market Analysis by Mordor Intelligence

The breast ultrasound market size was USD 2.56 billion in 2025 and is forecast to reach USD 5.02 billion by 2030, delivering a 14.1% CAGR over 2025-2030. Growth is fueled by mandatory dense-breast notification rules, rapid adoption of automated platforms, and workflow-saving artificial intelligence that shortens scan times and mitigates sonographer shortages. Automated breast ultrasound (ABUS) platforms that integrate AI now detect cancers missed by mammography while cutting acquisition time by 40%, a capability that supports higher patient throughput and eases staffing constraints. Ongoing breakthroughs in microbubble contrast agents elevate lesion characterization accuracy, and hand-held semiconductor-based probes extend imaging beyond hospitals into mobile units and rural clinics. Consolidation among hardware manufacturers and AI software vendors underpins a shift toward end-to-end imaging ecosystems spanning acquisition, analytics, and cloud-based collaboration.

Key Report Takeaways

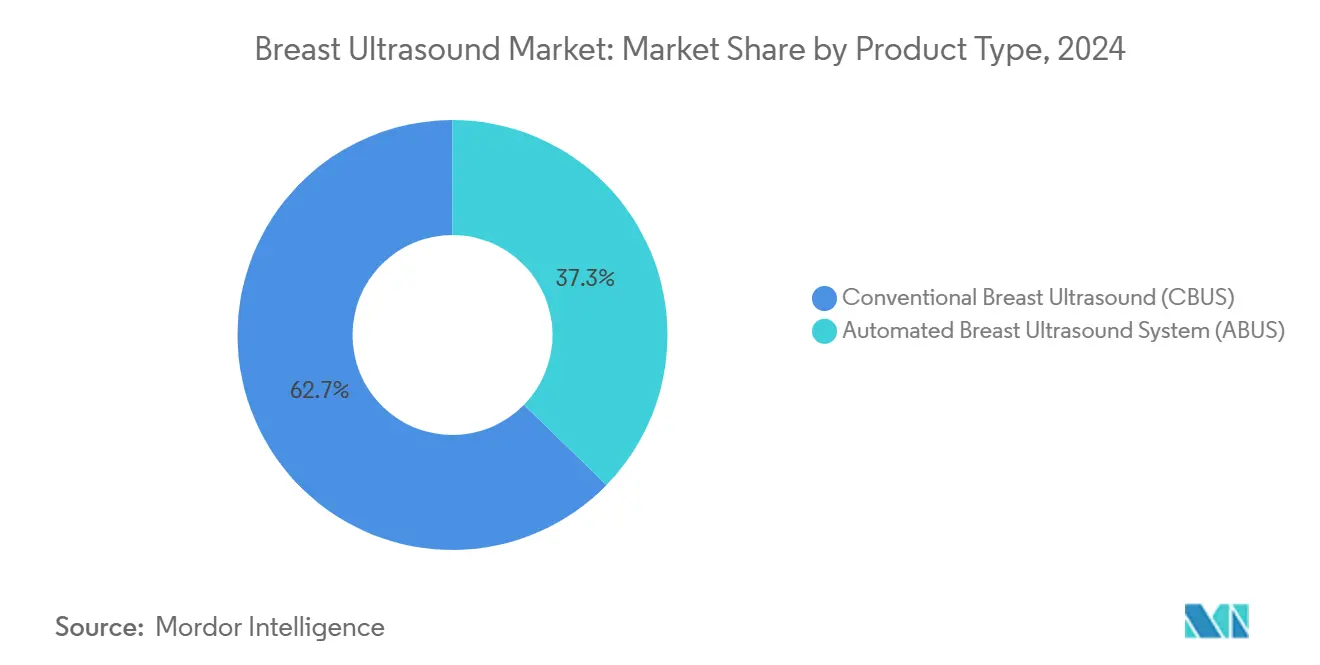

- By product type, conventional breast ultrasound held 62.7% breast ultrasound market share in 2024, while automated breast ultrasound is projected to expand at a 10.8% CAGR through 2030.

- By technology, 2D modalities led with 44.5% of the breast ultrasound market size in 2024; contrast-enhanced ultrasound is advancing at an 11.5% CAGR to 2030.

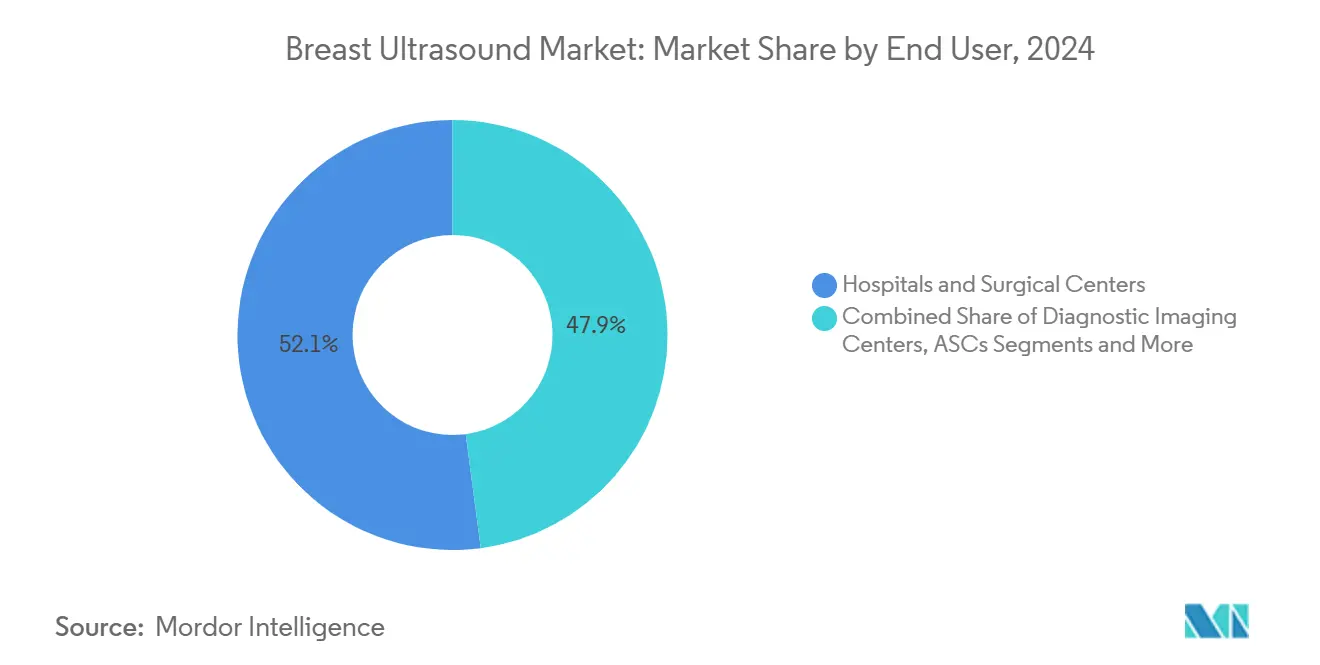

- By end user, hospitals and surgical centers accounted for 52.1% share of the breast ultrasound market size in 2024, and mobile screening units are forecast to record the fastest 12.7% CAGR between 2025-2030.

- By geography, North America commanded 35.6% breast ultrasound market share in 2024, whereas Asia Pacific is set to register an 8.4% CAGR over the same period.

Global Breast Ultrasound Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating dense-breast screening regulations | +3.20% | Global, early in North America & EU | Medium term (2-4 years) |

| AI-driven ABUS workflow reductions | +2.80% | North America & Asia Pacific, spill-over to EU | Short term (≤ 2 years) |

| Surge in portable/hand-held ultrasound | +2.10% | Global, strongest in emerging Asia Pacific markets | Medium term (2-4 years) |

| Contrast-enhanced micro-bubble breakthroughs | +1.90% | North America & EU, expanding into Asia Pacific | Long term (≥ 4 years) |

| Cloud-based teleradiology integration | +1.50% | Global, faster in developed economies | Medium term (2-4 years) |

| Value-based-care reimbursement incentives | +1.30% | North America first, gradual uptake in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Dense-Breast Screening Regulations

FDA amendments to the Mammography Quality Standards Act in September 2024 mandate that every mammography facility notify patients of breast density and the need for supplemental imaging.[1]Food and Drug Administration, “Important Information: Final Rule to Amend the Mammography Quality Standards Act (MQSA),” FDA.gov The rule covers more than 40 million annual screeners, compelling centers to add ABUS so patients need not be referred elsewhere. European jurisdictions with similar statutes reported 15-20% jumps in supplemental screening within two years, evidence that regulatory alignment drives accelerated equipment adoption. U.S. facilities now market “same-day dense-breast screening” packages that integrate ABUS with routine mammography, boosting patient satisfaction and lowering medico-legal exposure. Health systems cite capital investments in ABUS as risk-mitigation rather than discretionary spending, and early adopters track higher cancer-detection yields among women with heterogeneously or extremely dense tissue.

AI-Driven ABUS Workflow Reductions

Machine-learning algorithms integrated into leading ABUS platforms govern transducer positioning, automate nipple detection, and flag inadequate coverage in real time, trimming acquisition time by 40% while preserving sensitivity and specificity. AI-assisted protocols allow technologists with limited ultrasound training to execute high-quality exams after short upskilling, effectively multiplying the workforce amid 17.5% sonographer vacancy rates in England.[2]Thomas T., “Radiographer shortage in England 'is delaying breast cancer treatment',” theguardian.com Predictive analytics tailor scan parameters to patient anatomy, limiting rescans and enhancing consistency across sites. Hospitals report 25-30% throughput gains without hiring additional staff, a metric that underpins attractive return-on-investment calculations for AI-enabled systems.

Surge in Portable/Hand-Held Ultrasound Adoption

Semiconductor advances now compress cart-level imaging power into probes weighing under 300 grams and priced below USD 4,000, led by Butterfly Network’s iQ3 cleared in January 2024. Rural clinics, mobile vans, and home-health agencies deploy these devices for opportunistic breast imaging where fixed infrastructure is lacking. Cloud connectivity streams images to off-site radiologists for synchronous guidance, resolving expertise gaps in underserved zones. As value-based care incentivizes early detection outside hospital walls, portable units bridge access inequities, contributing a forecast 12.7% CAGR for mobile screening programs. Public-private partnerships in India now bundle hand-held scanners with tele-oncology platforms, broadening population-level detection.

Contrast-Enhanced Micro-Bubble R&D Breakthroughs

Next generation lipid-shelled and polymer-shelled microbubbles deliver superior stability and targeted binding, enabling both diagnostic and therapeutic applications in breast cancer.[3]Ying Huang, “Advances in Ultrasound-Targeted Microbubble Destruction (UTMD) for Breast Cancer Therapy,” Frontiers in Oncology, pmc.ncbi.nlm.nih.govClinical trials show 15-25% reductions in unnecessary biopsies by clarifying lesion vascularity compared with grayscale ultrasound. The FDA’s Breakthrough Device pathway shortened approval cycles, bringing first-in-class agents to market faster. Pairing contrast imaging with AI-guided quantification standardizes perfusion metrics, promising reproducible reports across sites. Researchers also exploit ultrasound-targeted microbubble destruction to locally release chemotherapeutics, hinting at a future theranostic ecosystem combining imaging and therapy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex of next-gen ABUS platforms | -2.50% | Global, hardest for small providers | Short term (≤ 2 years) |

| Global shortage of trained breast sonographers | -1.80% | Worldwide, acute in developed markets | Medium term (2-4 years) |

| Patchy reimbursement for supplemental ABUS | -1.40% | North America mainly, affects private markets elsewhere | Medium term (2-4 years) |

| Regulatory lag for AI algorithms | -1.10% | Global, uneven regional approvals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex of Next-Gen ABUS Platforms

AI-ready ABUS units cost USD 200,000-400,000, a steep outlay that competes with CT and MRI upgrades in capital budgets. Total cost of ownership further climbs once service contracts, transducer replacements, and dedicated technologist training are included. Smaller community hospitals often lack the screening volumes to amortize such investments within desired payback periods, reinforcing reliance on referral centers. Vendor financing schemes and pay-per-scan leasing aim to lower barriers, yet CFOs remain cautious while reimbursement for supplemental ultrasound remains inconsistent.

Global Shortage of Trained Breast Sonographers

Vacancy rates hit 17.5% in England, and more than 50% of U.S. sonographers are over 50 years old, pointing to imminent retirements. Pipeline constraints persist because clinical placements are limited and certification pathways lengthy. Breast ultrasound’s specialized ergonomics and interpretation nuances demand extra training, narrowing the labor pool further. Wage inflation and retention bonuses inflate operational costs, and despite AI assisting acquisition, interpretation still requires skilled radiologists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: ABUS Drives Innovation Despite CBUS Dominance

Conventional breast ultrasound systems controlled 62.7% of the breast ultrasound market size in 2024, anchored by entrenched workflows and lower purchase price. Operators value CBUS flexibility for targeted diagnostics and interventional guidance, functions ABUS currently complements rather than replaces. Yet ABUS, projected to post a 10.8% CAGR, adds population-scale efficiency by automating full-breast sweeps for dense-tissue screening. ABUS adoption accelerates as image quality gaps narrow and AI streamlines acquisition; GE HealthCare’s Invenia ABUS Premium cut scan time by 40% and secured FDA premarket approval in March 2025. Clinical trials show ABUS detects 26.8% of cancers missed by mammography, underscoring its complementary value. CBUS makers respond with AI-powered workflow aids, blurring product lines but sustaining CBUS relevance for targeted follow-up.

By Technology: Contrast Enhancement Emerges Amid 2D Leadership

2D ultrasound retained 44.5% breast ultrasound market share in 2024, buoyed by ubiquity, clinician familiarity, and favorable reimbursement codes. Integration of AI for speckle reduction and autofocus sustains image quality parity with more advanced systems. Volumetric 3D/4D ultrasound gains momentum inside automated platforms where standardized interpretation is essential. Elastography’s quantitative stiffness mapping augments malignancy differentiation, expanding its role in biopsy triage. Contrast-enhanced ultrasound, though niche, exhibits the fastest 11.5% CAGR owing to stabilized microbubble agents that improve lesion conspicuity and may obviate MRI in some equivocal cases. Adoption accelerates in academic centers and cancer institutes conducting therapy-response monitoring studies.

By End User: Mobile Units Challenge Hospital Dominance

Hospitals and surgical centers held 52.1% of the breast ultrasound market size in 2024, leveraging integrated multidisciplinary services and insurance relationships. Diagnostic imaging centers remain pivotal, servicing physician referrals with high-throughput workflows and extended hours. Specialized breast centers proliferate as women’s health programs spotlight holistic care. Mobile screening vans, projected to grow 12.7% CAGR, bridge geographic gaps, often funded through public-health grants or corporate wellness campaigns. Field data reveal mobile units attract first-time screeners, boosting early-stage detection rates. Ambulatory surgery centers increasingly perform biopsies, transitioning procedures from hospital outpatient departments to lower-cost settings and expanding point-of-care ultrasound demand.

Geography Analysis

North America commanded 35.6% breast ultrasound market share in 2024, powered by the United States’ rapid uptake of ABUS following dense-breast notification mandates and robust reimbursement infrastructure. Leading cancer centers integrate AI-enhanced platforms into routine screening, while Canada’s provincial health programs incentivize equitable access across remote regions. Mexico’s private hospitals adopt ABUS to attract medical tourists seeking comprehensive breast imaging packages.

Europe shows steady expansion anchored by organized screening programs and technology standardization within the EU. Germany and the United Kingdom pioneer research on AI-assisted ultrasound, with NHS pilots evaluating cloud-based reading hubs. France and Italy deploy mobile vans in rural provinces, and Spain experiments with transmission-based ultrasound tomography that eliminates compression, targeting dense-breast populations.

Asia Pacific is the fastest-growing region with an 8.4% CAGR thanks to infrastructure upgrades, rising breast-cancer awareness, and policy-backed early-detection drives. China’s multi-trillion-yuan health-reform agenda funds diagnostic imaging at county-level hospitals, including AI-ready ultrasound units. Japan’s aging demographic spurs adoption of high-resolution ABUS paired with AI triage algorithms validated by national radiology societies. India’s public-private screening partnerships deploy mobile vans equipped with hand-held probes and cloud-based reading platforms, achieving detection rates of 1.8 per 1,000 women screened. South Korea and Australia focus on research collaborations testing contrast-enhanced protocols in dense-breast cohorts.

Competitive Landscape

The breast ultrasound market exhibits moderate consolidation. GE HealthCare, Siemens Healthineers, Philips, and Hologic leverage broad portfolios and service networks to protect share, while focused challengers—Butterfly Network, Esaote, Mindray, QT Imaging—compete through specialization and price disruption. GE HealthCare’s USD 51 million purchase of Intelligent Ultrasound in July 2024 added AI voice-guided workflow, reinforcing vertical integration. Siemens Healthineers released Acuson Sequoia 3.5 with AI Abdomen and new HLX transducer, sharpening breast imaging capabilities. Hologic’s USD 350 million acquisition of Gynesonics extends its reach into therapeutic ultrasound, aligning with a strategy to capture imaging-to-therapy continuum.

Hand-held disruptors capitalize on semiconductor ultrasound-on-chip to democratize imaging, with Butterfly iQ3 priced at USD 3,899 serving primary-care and mobile segments. Partnerships between platform vendors and cloud-AI firms, such as GE HealthCare and RadNet integrating SmartMammo deep-learning algorithms, fortify ecosystem lock-in. Licensing and joint-development deals between microbubble developers and scanner OEMs are proliferating as contrast-enhanced ultrasound moves toward mainstream adoption.

Breast Ultrasound Industry Leaders

GE HealthCare

Siemens Healthineers

Hologic Inc.

Koninklijke Philips N.V.

Hitachi Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare launched Invenia ABUS Premium with FDA PMA; the AI-powered 3D platform delivers 40% faster scans and 35.7% higher cancer-detection yield when paired with mammography.

- February 2025: Butterfly Network introduced the iQ3 hand-held scanner leveraging P4.3 ultrasound-on-chip technology at USD 3,899.

- January 2025: Hologic finalized its USD 350 million acquisition of Gynesonics, adding the Sonata therapeutic ultrasound system.

Global Breast Ultrasound Market Report Scope

| Conventional Breast Ultrasound (CBUS) |

| Automated Breast Ultrasound (ABUS) |

| 2D Ultrasound |

| 3D/4D Ultrasound |

| Elastography |

| Doppler Ultrasound |

| Contrast-Enhanced Ultrasound |

| Hospitals & Surgical Centers |

| Diagnostic Imaging Centers |

| Breast Care Centers |

| Ambulatory Surgery Centers |

| Mobile Screening Units |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Conventional Breast Ultrasound (CBUS) | |

| Automated Breast Ultrasound (ABUS) | ||

| By Technology | 2D Ultrasound | |

| 3D/4D Ultrasound | ||

| Elastography | ||

| Doppler Ultrasound | ||

| Contrast-Enhanced Ultrasound | ||

| By End User | Hospitals & Surgical Centers | |

| Diagnostic Imaging Centers | ||

| Breast Care Centers | ||

| Ambulatory Surgery Centers | ||

| Mobile Screening Units | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast growth rate for the breast ultrasound market between 2025 and 2030?

The breast ultrasound market is expected to post a 14.1% CAGR from USD 2.56 billion in 2025 to USD 5.02 billion by 2030.

Which product category is growing fastest within breast ultrasound?

Automated breast ultrasound systems are projected to expand at a 10.8% CAGR thanks to dense-breast screening mandates and AI workflow gains.

Why is contrast-enhanced ultrasound gaining traction in breast imaging?

Microbubble advances and clinical studies show higher specificity that can cut unnecessary biopsies by up to 25%, driving an 11.5% CAGR for the segment.

How are mobile screening programs influencing adoption?

Mobile vans equipped with portable scanners reach underserved populations, supporting a 12.7% CAGR for the mobile end-user segment.

What regional market is expanding most rapidly?

Asia Pacific leads with an 8.4% CAGR, propelled by infrastructure investment in China, AI research in Japan, and large-scale screening initiatives in India.

How is AI addressing the sonographer shortage?

AI algorithms automate probe positioning and image quality checks, enabling technologists with minimal ultrasound experience to deliver high-quality exams and improving throughput by up to 30%.

Page last updated on: