Point-of-Care Ultrasound Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

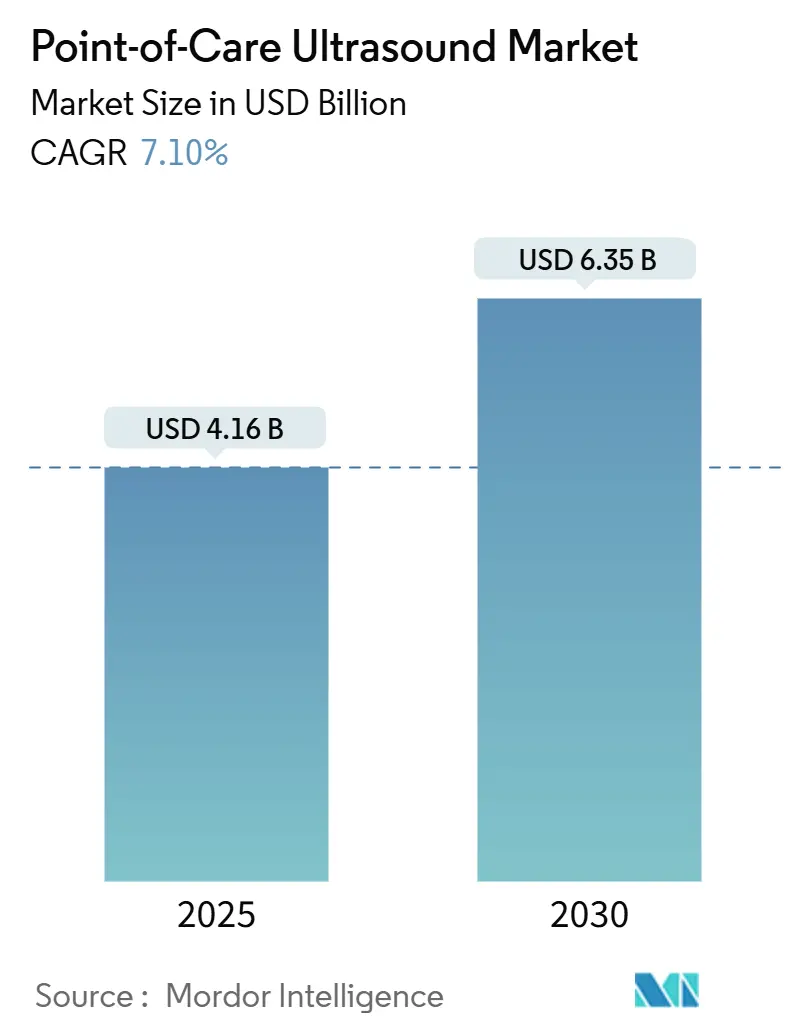

| Market Size (2025) | USD 4.16 Billion |

| Market Size (2030) | USD 6.35 Billion |

| Growth Rate (2025 - 2030) | 7.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Point-of-Care Ultrasound Market Analysis by Mordor Intelligence

The point-of-care ultrasound market size stands at USD 4.16 billion in 2025 and is forecast to reach USD 6.35 billion by 2030, reflecting a 7.1% CAGR over the period. Rapid semiconductor miniaturization has shifted ultrasound from centralized radiology suites to the bedside, while artificial-intelligence-driven image guidance now lets non-specialists capture diagnostic-quality scans within minutes. Growth is further propelled by rising procedural applications—particularly nerve blocks and vascular access—where real-time visualization lowers complication rates and shortens procedure time. Cybersecurity advisories on authentication bypass flaws and chip-supply volatility following Hurricane Helene highlight persistent operational risks that may temper near-term uptake. Competitive dynamics center on AI acquisition strategies, as established vendors lock in next-generation algorithms to defend platform share against lower-priced, chip-based entrants.

Key Report Takeaways

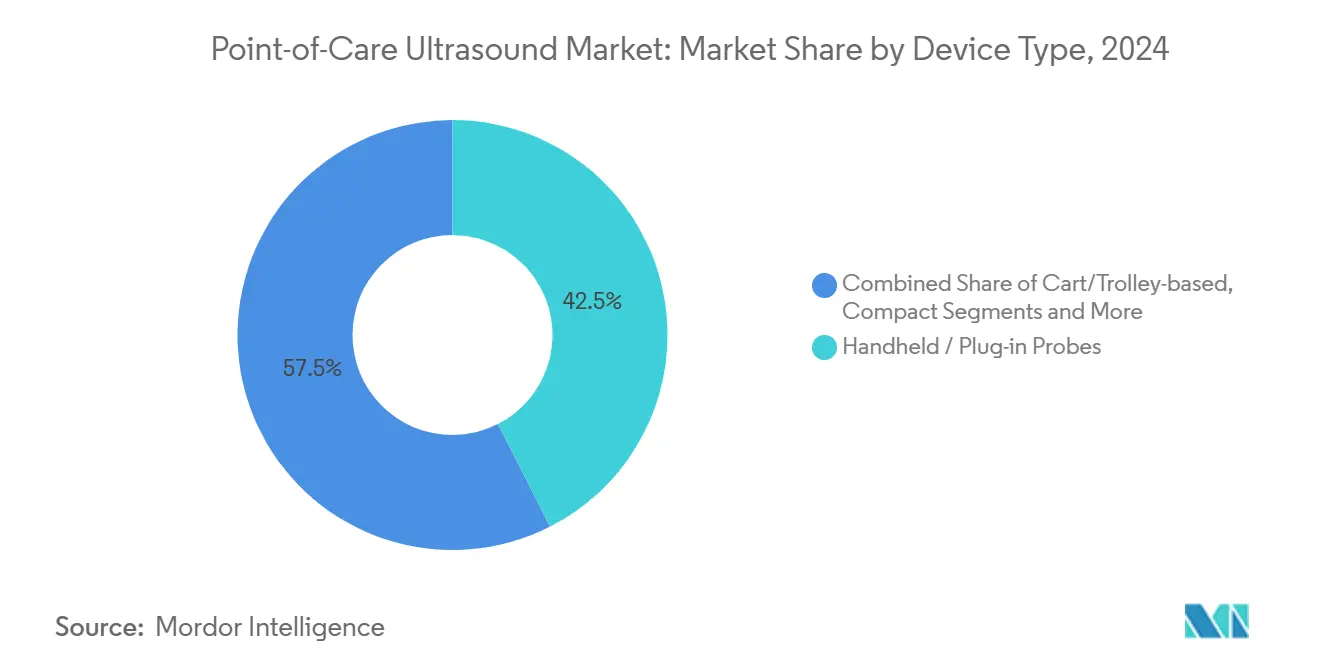

- By device type, handheld and plug-in probes led with 42.5% of the Point-of-Care Ultrasound market share in 2024, whereas ultrasound-on-chip/MEMS systems are projected to expand at an 18.4% CAGR through 2030.

- By application, emergency and critical care commanded a 38.0% share of the Point-of-Care Ultrasound market size in 2024; primary and internal medicine is advancing at a 16.2% CAGR to 2030.

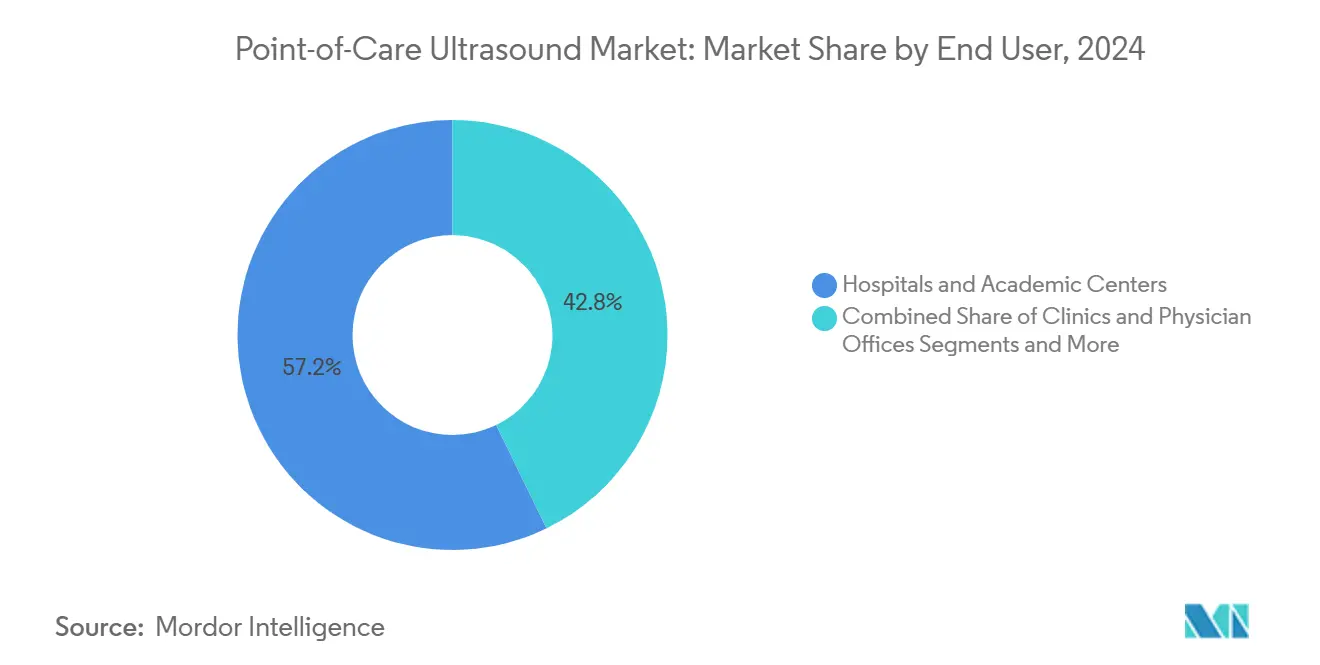

- By end user, hospitals and academic centers accounted for 57.0% of the Point-of-Care Ultrasound market size in 2024; home-care and tele-ultrasound platforms are set to grow at a 19.5% CAGR by 2030.

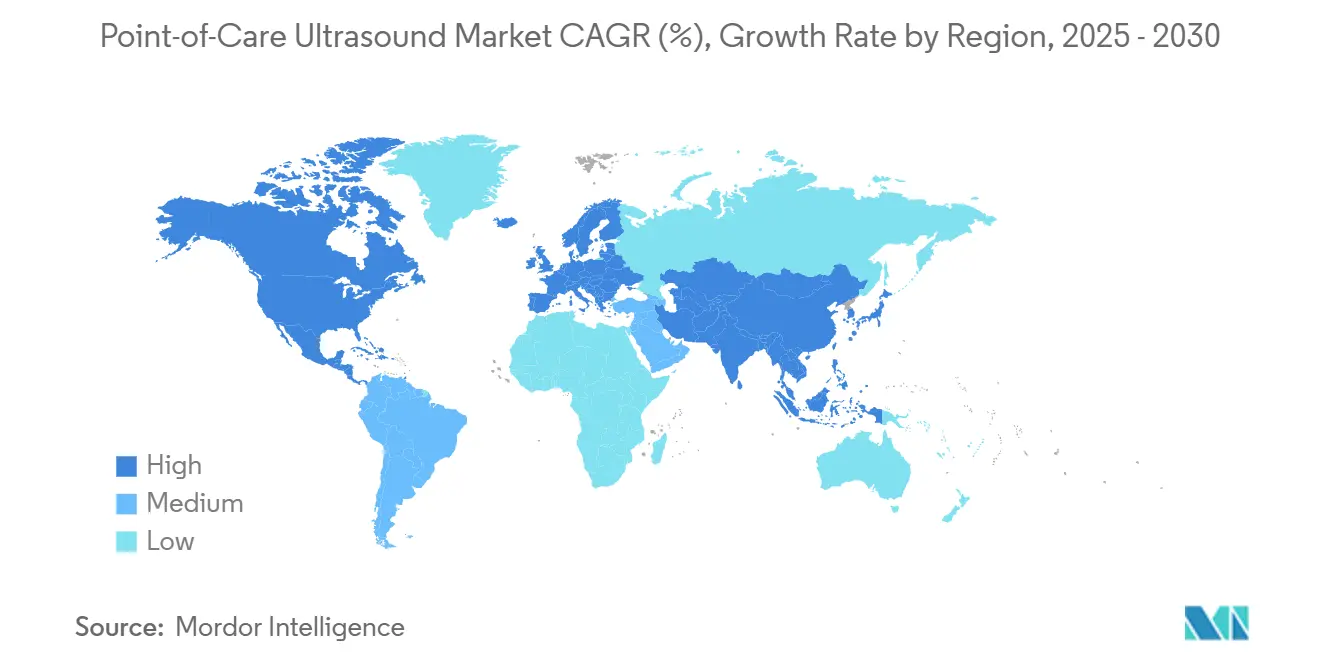

- By region, North America held 29.8% of the Point-of-Care Ultrasound market in 2024, while Asia Pacific is forecast to rise at an 11.5% CAGR through 2030.

Global Point-of-Care Ultrasound Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption Of Handheld POCUS In Emergency & Critical-Care Settings | +1.80% | Global, with early gains in North America & Europe | Short term (≤ 2 years) |

| Growing Integration Of AI For Image Guidance & Automated Interpretation | +1.50% | North America & APAC core, spill-over to Europe | Medium term (2-4 years) |

| Rising Procedural Applications Beyond Radiology (Nerve Blocks, Vascular Access) | +1.20% | Global, concentrated in developed healthcare systems | Medium term (2-4 years) |

| Shifting Reimbursement Models Toward Value-Based, Bedside Imaging | +0.90% | North America & EU, limited APAC adoption | Long term (≥ 4 years) |

|

Semiconductor "Ultrasound-On-Chip" Enabling |

+1.10% | Global, manufacturing concentrated in APAC | Short term (≤ 2 years) |

| Home-Based Chronic-Care Monitoring With Cloud-Connected POCUS | +0.80% | North America & Europe, emerging in urban APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Handheld POCUS in Emergency & Critical-Care Settings

Emergency departments now treat handheld scanners as essential equipment, achieving 92.5% diagnostic accuracy comparable with cart units. Paramedics replicate in-hospital findings in 79.5% of prehospital assessments, enabling earlier triage decisions. London’s Air Ambulance reported 83% adequate scan quality across 628 trauma encounters, validating field performance standards. Training has expanded from radiologists to emergency physicians, intensivists, and advanced practice providers, embedding bedside ultrasound into time-critical care pathways. As competencies normalize, procurement focuses on durable, sealed housings and infection-control-ready transducers to withstand high-turnover clinical environments.

Growing Integration of AI for Image Guidance & Automated Interpretation

FDA-cleared algorithms now recognize anatomical structures with more than 90% accuracy, minimizing operator dependency and shortening learning curves. UltraSight’s cardiac guidance software secured clearance in 2024 and lets novice users obtain diagnostic images in 96% of cases after just two hours of orientation. Siemens Healthineers’ Acuson Origin platform automates 500+ echocardiography measurements, cutting exam time and standardizing outputs. Samsung Medison’s purchase of Sonio illustrates how incumbent manufacturers secure AI pipelines to stay competitive. AI democratization aligns with workforce shortages by guiding non-specialists through probe positioning and offering real-time quality alerts.

Rising Procedural Applications Beyond Radiology (Nerve Blocks, Vascular Access)

Regional anesthesia now relies on ultrasound guidance, achieving 96.7% success in supraclavicular blocks versus 73.3% for alternate techniques. New guidelines from the American Society of Echocardiography formalize ultrasound-guided vascular cannulation, reinforcing its move from experimental to mainstream practice.[1]American Society of Echocardiography, “Guidelines for Ultrasound-Guided Vascular Cannulation,” asecho.org Pediatric vascular access also benefits, shortening fistula maturation time and curbing primary failure rates. As user confidence builds, revenue streams expand to disposable needle guides and integrated procedural software, further embedding POCUS into peri-operative workflows. Manufacturers bundle specialized presets and AI-driven targeting overlays to enhance repeatability for novice operators.

Shifting Reimbursement Models Toward Value-Based Bedside Imaging

Medicare’s 2025 Physician Fee Schedule assigns relative value units that recognize technological advances and real-time clinical impact. UnitedHealthcare now demands discrete documentation for POCUS interpretations, elevating the modality to a reimbursable diagnostic rather than an adjunct exam. Remote-patient-monitoring programs incorporate ultrasound in chronic-care bundles, expanding billing opportunities for cloud-connected probes. These incentives encourage providers to adopt standardized training and quality metrics, supporting a sustainable clinical and financial case for broader deployment. Long term, payer recognition is expected to reduce redundant imaging and hospital length of stay, improving overall cost-efficiency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Formal Training & Credentialing Frameworks For Non-Radiology Users | -1.40% | Global, more pronounced in developing markets | Medium term (2-4 years) |

| Reimbursement Gaps For Outpatient & Primary-Care Scans | -0.80% | North America & Europe, limited impact in APAC | Long term (≥ 4 years) |

| Cyber-Security & Data-Integration Risks With App-Based Probes | -0.60% | Global, concentrated in digitally advanced markets | Short term (≤ 2 years) |

| Chip-Supply Volatility Impacting Next-Gen Ultrasound-On-Chip Availability | -0.90% | Global, manufacturing bottlenecks in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Formal Training & Credentialing Frameworks for Non-Radiology Users

Few national licensing boards mandate point-of-care ultrasound competencies for paramedics or nurse practitioners, limiting widespread credentialing despite clinical demand.[2]International Journal of Paramedicine, “Prehospital Standards for Point-of-Care Ultrasound,” internationaljournalofparamedicine.com Certification bodies respond with specialty tracks—maternal-fetal, pulmonary, or cardiac—yet variable curriculum depth produces inconsistent skill levels. The American College of Physicians offers modular e-learning followed by hands-on assessments, but adoption remains voluntary. Liability insurers are cautious, heightening malpractice premiums when documentation shows inadequate operator training. These gaps slow purchasing decisions among smaller practices, constraining the Point-of-Care Ultrasound market until unified standards emerge.

Reimbursement Gaps for Outpatient & Primary-Care Scans

While hospital-based exams bill under established CPT codes, ambiguity persists for scans performed in primary-care offices, leading to claim denials and inconsistent payment cycles. European single-payer systems still classify many POCUS exams as bundled services, limiting incremental revenue streams for general practitioners. The financial uncertainty reduces capital budgets for devices in outpatient settings, delaying penetration beyond acute-care environments. Advocacy groups lobby for code revisions that mirror U.S. fee-schedule updates; however, policymaker timelines extend into late-decade horizons, sustaining a drag on growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Handheld Devices Lead Semiconductor Revolution

Handheld and plug-in probes captured 42.5% of the Point-of-Care Ultrasound market in 2024, reflecting clinician demand for pocket-sized tools deployable across hospital departments. The category benefits from platform updates such as Clarius’ ten-model wireless lineup compatible with both iOS and Android ecosystems, alongside Butterfly Network’s iQ3 that adds 3D imaging and on-device AI processing. Cart and trolley systems remain essential for comprehensive echocardiography and high-fidelity abdominal studies within radiology suites, yet their relative growth lags because portable probes now match resolution for many frontline tasks.

Ultrasound-on-chip systems form the fastest-growing subsegment, expanding at an 18.4% CAGR as semiconductor designs replace costly piezoelectric arrays, slashing entry prices below USD 4 K. Compact consoles offer a middle ground for emergency departments requiring larger displays without committing floor space. Emerging wearable patches facilitate continuous hemodynamic monitoring in intensive-care units, while tablet-based solutions attract interventionalists who need bigger screens but still value bedside maneuverability. This cascading innovation widens the addressable pool of users and underpins steady unit replacement cycles across the Point-of-Care Ultrasound market.

By Application: Emergency Care Dominance Yields to Primary Medicine Growth

Emergency and critical-care workflows secured 38.0% of the Point-of-Care Ultrasound market size in 2024, supported by established trauma protocols that demand fast triage and focused cardiac assessments. Portable devices proved instrumental in London’s “Pump, Pleura, and Pouring Blood” protocol, generating high-quality images in mobile environments.[3]Salman Naeem et al., “Implementation of Prehospital Point-of-Care Ultrasound Using a Novel Continuous Feedback Approach in a UK Helicopter Emergency Medical Service,” Scandinavian Journal of Trauma, Resuscitation and Emergency Medicine, sjtrem.biomedcentral.com Cardiology and vascular specialties adopted AI-guided presets, as Siemens’ Acuson Origin automates 500+ measurements, reducing operator variability.

Primary and internal medicine represents the fastest-expanding slice, advancing at a 16.2% CAGR through 2030 as family physicians integrate screenside liver and musculoskeletal scans into routine visits. Consumer-grade interfaces mimic smartphone ergonomics, encouraging adoption by clinicians unfamiliar with legacy cart controls. Obstetrics and gynecology maintain stable demand through specialty instruments like GE Voluson systems, while musculoskeletal practices embrace ultrasound-guided joint injections as standard of care. Overall, diversified clinical pathways broaden revenue streams and help embed POCUS in longitudinal care plans, solidifying the Point-of-Care Ultrasound market’s resilience.

By End User: Hospitals Lead While Telemedicine Accelerates

Hospitals and academic centers commanded 57.0% of the Point-of-Care Ultrasound market share in 2024, leveraging structured credentialing programs and purchasing scale to roll out networked devices across departments. Sutter Health’s seven-year partnership with GE HealthCare illustrates how large systems use enterprise contracts to standardize AI-enabled imaging workflows across 300 facilities.

Home-care and tele-ultrasound platforms hold the highest growth trajectory at 19.5% CAGR as remote-monitoring initiatives bundle connected probes into chronic-disease management kits. Clinics and physician offices increase uptake for in-house diagnostics that reduce referrals and boost patient retention. Ambulatory surgical centers embed ultrasound for nerve blocks and vascular access, enhancing same-day recovery protocols. Prehospital EMS units adopt handhelds after studies confirmed improved decision-making accuracy following streamlined training modules. Collectively, these varied end-user channels ensure sustained shipment momentum within the Point-of-Care Ultrasound market.

Geography Analysis

North America retained the largest regional stake at 29.8% in 2024, propelled by favorable reimbursement updates and early AI deployment across hospital systems. GE HealthCare’s USD 53 million acquisition of Intelligent Ultrasound and partnership deals such as the Tampa General adoption of AI-guided workflows illustrate how incumbents reinforce platform dominance. Yet rising cybersecurity alerts and diverging provincial credentialing criteria in Canada pose localized adoption hurdles, keeping market expansion tied to policy harmonization.

Asia Pacific is the fastest-growing region at an 11.5% CAGR through 2030, buoyed by Chinese vendors who grew domestic ultrasound share from 20% in 2011 to 35% in 2024. State subsidies under China’s New-Generation AI Plan fund algorithm development for imaging triage, while export-oriented manufacturers leverage lower production costs to undercut Western rivals. Mindray’s progression into the global top-four vendor cohort underscores regional ascendancy. Nevertheless, talent shortages and thin profitability margins moderate the long-term outlook.

Europe exhibits steady adoption as regulatory harmonization and workforce pressures promote AI-enabled solutions. Clarius and ThinkSono launched AI-guided probes tailored for European market needs, blending GDPR-compliant cloud storage with local language user interfaces. Middle East & Africa and South America remain nascent but promising; declining device prices combined with the modality’s portability foster diagnostic capacity in under-resourced clinics, encouraging multilateral aid programs to procure handheld systems for maternal-health and infectious-disease surveillance.

Competitive Landscape

The Point-of-Care Ultrasound market demonstrates moderate consolidation. GE HealthCare, Philips, and Siemens Healthineers command entrenched distribution networks and have accelerated AI asset purchases, typified by GE’s Intelligent Ultrasound buyout and Siemens’ AI Abdomen release. Butterfly Network disrupts price points through semiconductor-driven cost curves, offering sub-USD 4 K scanners with whole-body capability to broaden user bases.

Strategic collaborations shape competitive posture: GE HealthCare’s alliance with NVIDIA targets autonomous scanning, while Philips’ Elevate software upgrade reduces abdominal exam time by 50%, reinforcing differentiation via workflow efficiency. Large enterprises bundle hardware, cloud analytics, and training services, erecting ecosystem moats difficult for single-product startups to breach. Simultaneously, AI-focused newcomers partner with OEMs to embed algorithms in exchange for revenue-share arrangements, fostering symbiotic innovation.

Price-sensitive emerging markets spawn regional champions who tailor probes to local clinical guidelines and language interfaces, adding complexity to global competitive mapping. Overall, rivalry intensifies around AI, cloud interconnectivity, and specialized procedural accessories, sustaining a vibrant innovation pipeline that continually upgrades value propositions to end users.

Point-of-Care Ultrasound Industry Leaders

-

GE HealthCare

-

Philips Healthcare

-

Siemens Healthineers

-

Butterfly Network

-

Fujifilm Sonosite

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare and NVIDIA announced a collaboration to develop autonomous diagnostic imaging solutions that combine AI with ultrasound and X-ray modalities.

- March 2025: GE HealthCare launched AI-driven Invenia ABUS Premium 3D breast-ultrasound platform with integrated Verisound AI.

- October 2024: GE HealthCare completed USD 53 million acquisition of Intelligent Ultrasound’s clinical AI business.

- September 2024: Butterfly Network expanded its iQ3 ultrasound system to Europe after securing CE marking.

Global Point-of-Care Ultrasound Market Report Scope

| Cart / Trolley-based Systems |

| Compact Systems |

| Handheld / Plug-in Probes |

| Wearable / Patch Ultrasound |

| Tablet-based Ultrasound |

| Emergency & Critical Care |

| Cardiology & Vascular |

| Obstetrics & Gynecology |

| Musculoskeletal & Sports Medicine |

| Primary & Internal Medicine |

| Hospitals & Academic Centers |

| Clinics & Physician Offices |

| Ambulatory Surgical Centers |

| Pre-hospital / EMS Providers |

| Home-care & Tele-ultrasound Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Cart / Trolley-based Systems | |

| Compact Systems | ||

| Handheld / Plug-in Probes | ||

| Wearable / Patch Ultrasound | ||

| Tablet-based Ultrasound | ||

| By Application | Emergency & Critical Care | |

| Cardiology & Vascular | ||

| Obstetrics & Gynecology | ||

| Musculoskeletal & Sports Medicine | ||

| Primary & Internal Medicine | ||

| By End User | Hospitals & Academic Centers | |

| Clinics & Physician Offices | ||

| Ambulatory Surgical Centers | ||

| Pre-hospital / EMS Providers | ||

| Home-care & Tele-ultrasound Platforms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What was the worldwide revenue for handheld surgical tools in 2025?

The handheld surgical instruments market size reached USD 6.26 billion in 2025.

Which product category currently leads sales?

Forceps and spatulas hold the top slot with 28.1% share of 2024 revenue.

Why are ambulatory surgical centers attracting vendors?

ASCs are expected to grow at an 8.4% CAGR, driven by cost advantages and payer support for outpatient orthopedic procedures.

Which region is expanding fastest?

Asia Pacific is projected to post a 7.4% CAGR between 2025 and 2030 as infrastructure and regulatory reforms accelerate device uptake.

How will new FDA QMSR rules affect manufacturers?

The 2026 alignment with ISO 13485 will raise compliance costs but streamline global submissions, benefiting companies with robust quality systems.

Are disposable or reusable instruments gaining ground?

Reusable tools still dominate, yet disposable variants are the fastest-growing, propelled by infection-control savings of more than USD 400 per case.

Page last updated on: